Global Market Comments

March 5, 2013

Fiat Lux

Featured Trade:

(THE GREAT YAWN OF 2013),

(INDUSTRIES THAT YOU WILL NEVER HEAR FROM ME ABOUT)

Contrary to widespread predications, the sun rose this morning and the world did not end. The overnight reduction in our defense spending did not prompt expansionist, vengeful Mexicans to try to retake California and Texas, kicking soccer balls all the way. Cigar chomping Cuban communists did not capture Florida. Hockey stick brandishing Canadians failed to even launch another punitive military excursion into upstate New York.

The more pedestrian predications failed to materialize, as well. Lines at airports were shorter than usual, as so many had delayed travel on the first day of The Great Sequestration. Planes did not fall out of the sky. It turns out that air traffic controllers are exempt from cuts, as are a lot of other key government services. Schools opened. Over the weekend, we learned that the actual disbursement of federal subsidies doesn?t slow for another six months.

Checking the San Francisco papers over the weekend, it looks like we?ll lose a million dollars here and two million there. In a state with a GDP of $2.7 trillion it doesn?t amount to spare pennies found under the sofa cushions by the cleaning lady. Virtually all military bases in the Bay Area were closed during the nineties, as they were so old and decrepit. Many of the rotting Quonset huts were hastily erected in WWII, and one red brick naval facility dated back 150 years. Even in conservative San Diego, the last bastion of defense spending in the Golden State, the pink slips going out are not even a blip on the radar.

California, which accounts for 15% of America?s population and 17% of the GDP, is remarkably immune from anything that happens in Washington. That?s because when it became a state in 1849, it took three months to get here by sailing ship around Cape Horn, or six months by wagon along the Santa Fe Trail. The distances were so great, the ties of dependence were never established, unlike in the East. But the wealth did pour out. The Union Army won the Civil War financed by California gold.

The financial markets crash didn?t crash either. The Dow average closed the day up 38 at 14,127. That is a mere handful of points off of a five-year high, and only 37 points short of the all time high of 14,164 set on October 9, 2007. If anything, the markets are crashing upwards. What gives?

This is turning out to be one of the ?emperor has no clothes? moments in financial history. The $84 billion sequestration amounts to only 32 basis points of US GDP, 2.3% of the total federal budget for 2013, and 8.4% of the budget deficit. That means $916 billion in budget deficit remains to stimulate the economy. In other words, it might cancel out the positive effect of Apple?s iPhone 5 launch on economic growth.

There are some parts of the country that will certainly feel the pain from sequestration. But these are in parts of the country that most Americans don?t care about. The worst hit will be in Washington DC itself, or within lobbyist lunching distance of the nations capital. That?s why defense spending accounts for 20% of state GDP in Virginia and Maryland, but only 2% in New York.

Let?s look at the positive effect of the sequester on the financial markets. The budget deficit has fallen substantially, arresting the fall of the Treasury bond market. We have seen the first substantial cuts in defense spending since the Soviet Union collapsed 20 years ago, enabling the? "peace dividend".

The sequestration does have the effect of cancelling out some of the stimulus provided by the Federal Reserve?s Ben Bernanke. Ben will simply respond by making up the difference through expanding quantitative easing and extending the zero interest rate policy. This is what financial markets see when they refuse to sell off.

I should add that my prescient forecast that sequestration would amount to a big nothing has been fabulous for the performance of my model portfolio, which is up 29% so far in 2013. In fact, it looks like this sequester is going so well, we should plan on having a second one.

The focus of this letter is to show people how to make money through investing in fast growing, highly profitable companies which have stiff, long-term macroeconomic winds at their backs. That means I ignore a large part of the US economy whose time has passed and are headed for the dustbin of history. According to the Department of Labor's Bureau of Labor Statistics, the eight industries listed below are least likely to generate positive job growth in the next decade. As most of these stocks are already bombed out, it is way too late to short them. As an investor, you should consider this a 'no go' list. I have added my comments, not all of which should be taken seriously. 1) Realtors - Despite a halving of prices, and therefore commissions, the number of realtors is only down 10% from its 1.3 million peak in 2006. This business is dying? for a major rationalization. 2) Pharmaceuticals - With a number of blockbuster drugs seeing patents expire soon and going generic, the downsizing at the major firms has been ferocious. The survivors will merge to cut costs, sending more masses to the unemployment office. 3) Newspapers - these probably won't exist in five years, save the Wall Street Journal and the New York Times, as five decades of hurtling technological advances have already shrunk the labor force by 90%. Go online, or go away. 4) Airline employees - This is your worst nightmare of an industry, as management has no idea what interest rates, fuel costs, or the economy will do, which are the largest inputs into their business. Pilots will eventually work for minimum wage just to keep their flight hours up. 5) Big telecom - Can you hear me now? Nobody uses landlines anymore, leaving these companies with giant rusting networks that are costly to maintain. Since cell phone market penetration is 90%, survivors are slugging it out through price competition, cost cutting, and all that annoying advertising. 6) State and Local Government - With employment still at levels private industry hasn't seen since the seventies, firing state and municipal workers will be the principal method of balancing ailing budgets. Expect class sizes to soar to 80, to put out your own damn fires, and to keep the 9 mm loaded and the back door booby-trapped for home protection. 7) Installation, Maintenance, and Repair - I have explained to my mechanic that the electric motor in my new Tesla S-1has only five moving parts, compared to 300 in my old clunker, and this won't be good for business. But he just doesn't get it. The winding down of our wars in the Middle East is about to dump a million more applicants into this sector. The last refuge of the trained blue-collar worker is about to get cleaned out. 8) Bank Tellers - Since the ATM made its debut in 1968, this profession has been on a long downhill slide. Banks have lost so much money in the financial crisis, they can't afford to hire humans any more. It hasn't helped that 283 banks have closed during the recession, with many survivors merging to cut costs (read fire more people). Your next bank teller may be a Terminator.

Out With the Old

And in With the New

Global Market Comments

March 4, 2013

Fiat Lux

Featured Trade:

(MARCH 6 GLOBAL STRATEGY WEBINAR),

(THE DEATH OF GOLD, PART II),

(GLD), (GDX), (GDM), (FXE), (UUP), (FXB), (GBB), (USO), (CU),

(THE REAL ESTATE MARKET IN 2030),

(TESTIMONIAL)

SPDR Gold Shares (GLD)

Market Vectors Gold Miners ETF (GDX)

GOLD MINERS INDEX (GDM)

CurrencyShares Euro Trust (FXE)

PowerShares DB US Dollar Index Bullish (UUP)

CurrencyShares British Pound Sterling Tr (FXB)

iPath GBP/USD Exchange Rate ETN (GBB)

United States Oil (USO)

First Trust ISE Global Copper Index (CU)

I have been pounding the table trying to get readers out of gold since early December. Now, my friend at stockcharts.com, Mike Murphy, has produced a stunning series of charts showing that this may be more than just a short-term dip and another buying opportunity.

Mike explains that a number of traditional chart, technical, and intermarket signs are flashing serious warning signals. At the very least, we are going to test $1,500 an ounce sometime soon. If that doesn?t hold, then $1,250 is in the cards.

To make matters particularly fiendish for traders, we may see a false breakdown through $1,500 first, well into the 1,400?s, that sucks in tons of capitulation sellers before an uptrend resumes. It is a scenario that will be enough to test even the most devoted of gold bugs.

At risk is nothing less than the end of a bull market that is entering its 12th year. The shares of gold miners suggest that the demise of the bull market is already a foregone conclusion. The index for this group (GDM) has breached major support once again and is looking for a new four year low. Since this index usually correlates very highly with the barbarous relic, the grim writing is on the wall.

A strong dollar does not auger well for gold either. Look at the chart below, and you see the dollar basket (UUP) has punched through to an eight month high. Until two weeks ago, this was primarily a weak yen story. But since then, both the euro (FXE) and Sterling (FXB) have collapsed, adding fuel to the fire. And it is not just gold that is feeling the heat. The entire commodities space has been the pain trade, including oil (USO), copper (CU), and other hard assets.

There are a host of reasons why the yellow metal has suddenly become so unloved. The largest holder of the gold ETF (GLD), John Paulson, is getting big redemptions in his hedge fund, forcing him to sell. This is why the selling is so apparent in the paper gold markets, like the ETF?s, but not the physical.

India has suddenly seen its currency, the rupee, drop against the greenback. That reduces the buying power of the world?s largest gold importer. With years of pernicious deflation ahead of us, who needs a traditional inflation hedge like the yellow metal?

Here is the final nail in the coffin for gold. Look at the last chart of the Federal Reserve Bank of St. Louis?s measurement of the broader monetary base. It shows that it has exploded to the upside in recent months. In the past, gold matched the rise in the money supply step for step. Now it?s not. If a market can?t rally on fabulous news, which it has obviously failed to do since the last QE was launched in September, then you sell the daylights out of it. That is what most traders believe.

The screaming conclusion here is that traders are pouring their money into stocks instead of gold. Now, paper trumps gold. Conditions for the barbarous relic will, therefore, probably get worse before they get better.

Ben Bernanke affirmed as much last week when he told Congress that quantitative easing would continue unabated for the foreseeable future. That means rising stocks and flat bonds, all of which are bad for gold. The bottom line here is that when gold makes its first run at $1,500, I am not going to jump in as a buyer.

Weekly December, 2011 to February, 2013

Adjusted Monetary Base

Reserve Bank of St. Louis

Suddenly Going Out of Style

A number of analysts, and even some of those in the real estate industry, are finally coming around to the depressing conclusion that there will never be a recovery in residential real estate. Long time readers of this letter know too well that I have been hugely negative on the sector since late 2005, when I unloaded all of my holdings. However, I believe that 'forever' may be on the extreme side. Personally, I believe there will be great opportunities in real estate starting in 2030.

Let's back up for a second and review where the great bull market of 1950-2007 came from. That's when a mere 50 million members of the 'greatest generation', those born from 1920 to 1945, were chased by 80 million baby boomers born from 1946-1962. There was a chronic shortage of housing, with the extra 30 million never hesitating to borrow more to pay higher prices. When my parents got married in 1949, they were only able to land a dingy apartment in a crummy Los Angeles neighborhood because he was an ex-Marine. This is where our suburbs came from.

Since 2005, the tables have turned. There are now 80 million baby boomers attempting to unload dwellings on 65 million generation Xer's who earn less than their parents, marking down prices as fast as they can. As a result, the Federal Reserve thinks that 35% of American homeowners either have negative equity, or less than 10% equity, which amounts to nearly zero after you take out sales commissions and closing costs. That comes to 42 million homes. Don't count on selling your house to your kids, especially if they are still living rent free in the basement.

The good news is that the next bull market in housing starts in 20 years. That's when 85 million Millennials, those born from 1988 to yesterday, start competing to buy homes from only 65 million gen Xer's. By then, house prices will be a lot cheaper than they are today in real terms. The next interest rate spike will probably knock another 25% off real estate prices. Think 1982 again.

Fannie Mae and Freddie Mac will be long gone, meaning that the 30 year conventional mortgage will cease to exist. All future home purchases will be financed with adjustable rate mortgages, forcing homebuyers to assume interest rate risk, as they already do in most of the developed world. With the US budget deficit problems persisting beyond the horizon, the home mortgage interest deduction is an endangered species, and its demise will chop another 10% off home values.

For you millennials just graduating from college now, this is a best case scenario. It gives you 15 years to save up the substantial down payment banks will require by then. You can then swoop in to cherry pick the best neighborhoods at the bottom of a 25-year bear market. People will no doubt tell you that you are crazy, that renting is the only safe thing to do, and that home ownership is for suckers. That's what people told me when I bought my first New York co-op in 1982 at one tenth its current market price.

Just remember to sell by 2060, because that's when the next intergenerational residential real estate collapse is expected to ensue. That will leave the next, yet to be named generation, holding the bag, as your grandparents are now.

Global Market Comments

March 1, 2013

Fiat Lux

Featured Trade:

(TRADE ALERT SERVICE CLOCKS 26% GAIN IN 2013)

(A CONVERSATION WITH THE BOOTS ON THE GROUND),

(DINNER WITH NOBEL PRIZE WINNER JOSEPH STIGLITZ)

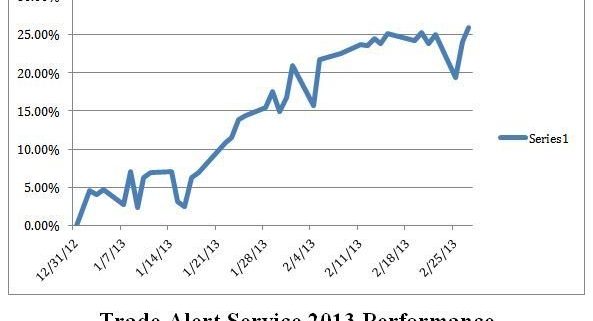

The Trade Alert Service of the Mad Hedge Fund Trader has posted a 26.01% profit year to date, taking it to another new all time high. The 26-month total return has punched through to an awesome 81.06%, compared to a miserable 15% return for the Dow average during the same period. That raises the average annualized return for the service to 36%, elevating it to the pinnacle of hedge fund ranks.

My bet that the stock markets would move sideways to up small during the month of February has paid off big time, as I continued to run sizeable long positions in the S&P 500 and the Russell 2000 (IWM). In the end, the Dow gained only 80 points for the month, an increase of only 57 basis points. My substantial short volatility positions are contributing to profits daily. I booked nice profits from holdings in American International Group (AIG) and copper producer, Freeport McMoRan (FCX). I also prudently doubled up my short positions in the Japanese yen.

It has truly been a month where everything is working. Even my short positions in deep out of the money calls on the (SPY) are substantially contributing to my P&L. While the (SPY) has been going up, it has not been appreciating fast enough to hurt the position. In the meantime, I have been able to dodge the bullets that have been killing off other hedge funds, including those in gold (GLD), oil (USO), and commodities (CORN), (CU).

All told, the last 18 consecutive recommendations of the Trade Alert Service have been profitable. I have eight trades to go to beat this record. Watch this space.

Global Trading Dispatch, my highly innovative and successful trade-mentoring program, earned a net return for readers of 40.17% in 2011 and 14.87% in 2012. The service includes my Trade Alert Service, daily newsletter, real-time trading portfolio, an enormous trading idea database, and live biweekly strategy webinars. To subscribe, please go to my website at www.madhedgefundtrader.com, find the ?Global Trading Dispatch? box on the right, and click on the lime green ?SUBSCRIBE NOW? button.

I have spent many hours speaking at length with the generals who ran our wars in the Middle East, like David Petraeus, James E. Cartwright, and Martin E. Dempsey. To get the boots on the ground view, I attended the graduation of a friend at the Defense Language Institute in Monterey, California, the world's preeminent language training facility.

As I circulated at the reception at the once top-secret installation, I heard the same view repeated over and over in the many conversations swirling around me. While we can handily beat armies, defeating an idea is impossible. With the planet's fastest growing population, Muslims are expected to double from one to two billion by 2050, the terrorists can breed replacements faster than we can kill them. The US will have to maintain a military presence in the Middle East for another 100 years. The goal is not to win, but to keep the war at a low cost, slow burn, over there, and away from the US.

I have never met a more determined, disciplined, and motivated group of students. There were seven teachers for 16 students, some with PhD's and all native Arabic speakers. The Defense Department calculates the cost of this 63-week, total emersion course at $200,000 per student.

They are taught not just language, but also the history, culture, and politics of the region as well. I found myself discussing at length the origins of the Sunni/Shiite split in the 7th century, the rise of the Mughals in India in the 16th century, and the fall of the Ottoman Empire after WWI, and this was with a 19 year old private from Kentucky whose previous employment had been at Wal-Mart! I doubt most Americans her age could find the Middle East on a map. Students graduated with near perfect scores. If you fail a class, you get sent to Afghanistan, unless you are in the Air Force, which kicks you out of the service completely.

As we feasted on hummus and other Arab delicacies, I studied the pictures on the wall describing the early history of the DLI in WWII, and realized that I knew several of the participants. The school was founded in 1941 to train Japanese Americans in their own language to gain an intelligence advantage in the Pacific war. General 'Vinegar Joe' Stillwell said their contribution shortened the war by two years. General Douglas McArthur believed that an army had never before gone to war with so much advance knowledge about its enemy. To this day, the school's motto is 'Yankee Samurai'.

My old friends at the Foreign Correspondents' Club of Japan will remember well the late Al Pinder. He spent the summer of 1941 photographing every Eastern facing beach in Japan, successfully smuggled them out hidden in a chest full of Japanese blow up dolls and sex toys. He then spent the rest of the war working for the OSS in China. I know this because I shared a desk in Tokyo with Al for nearly ten years. His picture is there in all his youth, accepting the Japanese surrender in Korea with DLI graduates.

I Guess I Should Have Studied Harder

Global Market Comments

February 28, 2013

Fiat Lux

Featured Trade:

(SUNDAY WITH PRESIDENT JIMMY CARTER)