When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-09-03 11:55:052019-09-03 11:55:05Trade Alert - (OKTA) September 3, 2019 - SELL-TAKE PROFITS

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-09-03 10:56:252019-09-03 10:56:25Trade Alert - (STX) September 3, 2019 - SELL-STOP LOSS

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to the six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-09-03 09:55:362019-09-03 09:55:36September 3, 2019 - MDT Alert (FL)

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-09-03 09:28:192019-09-03 09:28:19September 3, 2019 - MDT Pro Tips A.M.

I have a pretty good view from my home on a mountaintop in San Francisco.

To the west, I can see through the Golden Gate Bridge all the way out to the Farallon Islands 20 miles off the coast. To the south, there is Stanford’s Hoover Tower and all of Silicon Valley. In the winter I can look east and see the snow-covered High Sierras 200 miles away.

However, during last year’s wildfires, I couldn’t see a thing. Visibility ended at 100 yards, the cars parked outside were covered in ash, and I could barely breathe. We were all confined indoors.

I kind of feel that’s the way the stock market is right now. You can’t see a thing, so it’s better to stay indoors.

Not only are market gyrations subject to unpredictable and random, out-of-the-blue influences. The old playbook about cross market correlations and how asset classes respond at different points of the economic cycle doesn’t work either.

The good news is that August is over, the second worth trading month of the year. The bad news? September is the WORST trading month of the year!

So, what does a trader do on the first day of the worst investment month of the year?

Research.

That's what I’ll be doing, waiting for the next cataclysmic collapse to buy or the next euphoric bubble to sell short. Until then, I’ll be sitting tight. Just running my existing long/short trading book, I’ll be up 3.4% by the September 20 option expiration date in 15 trading days.

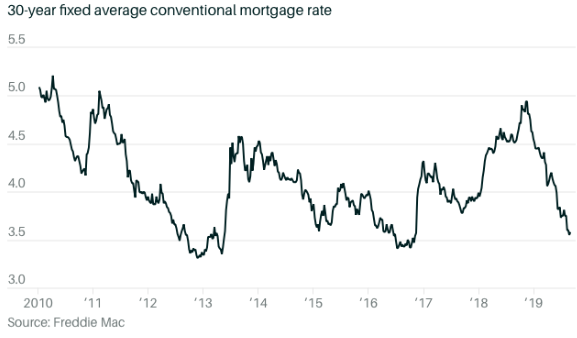

There is one BIG positive for the economy that no one is talking about. The home ATM is open for business, and open like it’s never been open before.

The thirty-year fixed rate mortgage rate is now at 3.56%, 10 basis points over a decade low and 20 basis points above an all-time low (see the chart below). There are currently $9.4 trillion of outstanding home mortgages in the US. Some $5 trillion is in Fannie Mae and Freddie Mac conforming loans, some 90% of which have interest rates higher than the current market.

If just ten million of these mortgages refinance obtaining an average of $4,560 in annual savings each, that will amount to a de facto tax cut of $456 billion per year, not an inconsequential amount. And Goldman Sachs thinks we could be in for as much as 37 million refis. It could be enough to offset the negative impact of the trade war.

As for the past week, it seemed like a disaster a day.

Trump ordered all US companies out of China. Like you can reverse 40 years’ worth of trillions of dollars of investment with a Tweet. If they did, an iPhone would cost $10,000 and your low-end laptop $15,000. An escalation of the trade war is the last thing your 401k wanted to hear. Kiss that early retirement goodbye.

Oilcrashed (USO) on trade war escalation, with the industry now seeing a recession as a sure thing. Russian cheating on quotas is pouring the fat on the fire creating a massive supply glut in the face of shrinking demand. Take a long nap before considering any energy investment (XLE). The long-term charts show they are all going to zero.

Prime Minister Boris Johnson suspended Parliament, prompting a free fall in the pound. It’s to keep Parliament from blocking his hard Brexit, where it would certainly loose by a landslide. It’s all up to the Queen now, the monarch, not the rock group.

The yield inversion is deepening, with the US Treasury selling two-year notes today at a 1.56% yield, with ten-year yield closing at 1.45%. And that’s with the Treasury selling a total of a gob smacking $113 billion worth of bonds last week, which should have driven rates UP! US ten-year TIPS now showing negative interest rates.

Company stock buybacks are fading. That's a big deal as corporations retiring their own shares have been the biggest buyers in the market for the past two years. As if you needed another reason for downside risk.

US 15% tariffs hit on Sunday, and the Chinese paused in retaliation. Christmas is about to get more expensive. Many large retailers won’t make it until the new year. Keep selling short Macy’s (M) on rallies.

Bond yields hit new lows, at 1.44% for ten-year US Treasury bonds. The next stop is zero. Fixed income markets are saying that a recession is imminent. “Inversion” will be the world of the year for 2019. Go refi that home if you can get a banker on the phone!

There is no way out of the next recession, says hedge fund titan Ray Dalio. With global rates below zero, you can’t cut to stimulate business. You can’t do any more quantitative easing either, as the world is already glutted with paper. This is the trap Japan has been caught in for the last 30 years. It is all sobering food for thought.

US growth slowed with the second reading of the Q2 GDP marked down from 2.1% to 2.0%. The downturn has continued since the economy peaked 18 months ago. Q3 will be much worse when the trade war and earnings downgrades hit big time. And then there’s the soaring deficit. Sow the wind, reap the whirlwind.

US Consumer Sentiment took a dive from 98.4 to 89.8 in August. Has the spending boom just peaked? If so, we’re all toast. The "tariff cliff" is already taking its toll.

The Mad Hedge Trader Alert Service has posted its best month in two years. Some 22 or the last 23 round trips, or 95.6%, have been profitable, generating one of the biggest performance jumps in our 12-year history.

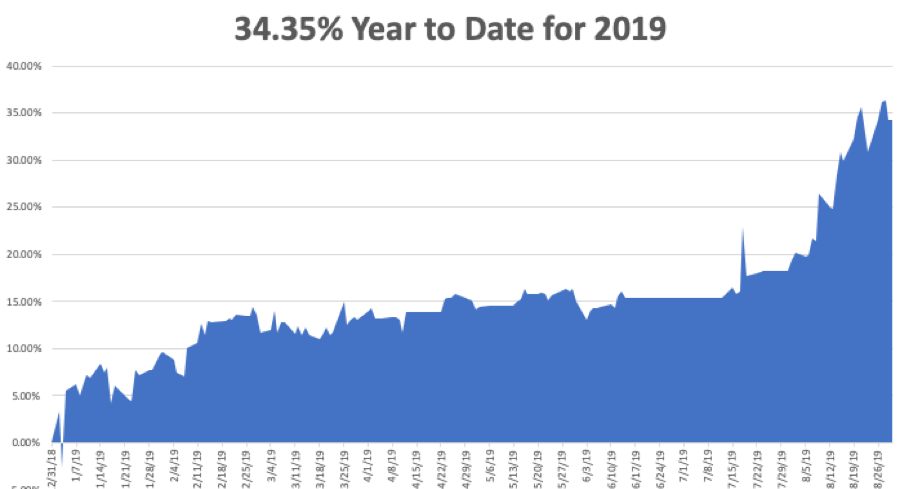

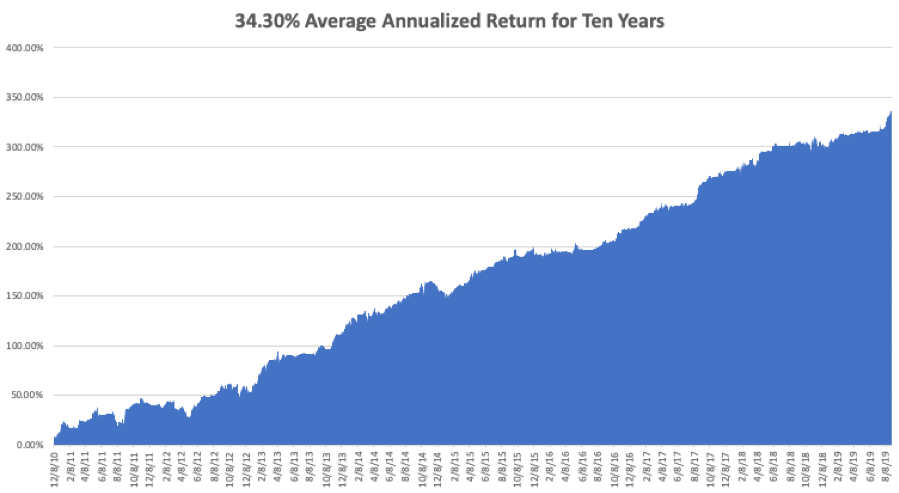

My Global Trading Dispatch has hit a new all-time high of 334.48% and my year-to-date shot up to +34.35%. My ten-year average annualized profit bobbed up to +34.30%.

I raked in an envious 16.01% in August. All of you people who just subscribed in June and July are looking like geniuses. My staff and I have been working to the point of exhaustion, but it’s worth it if I can print these kinds of numbers.

As long as the Volatility Index (VIX) stays above $20, deep in-the-money options spreads are offering free money. I am now 60% invested, 40% long big tech and 20% short Walmart (WMT) and the Russell 2000, with 20% in cash. It rarely gets this easy.

The coming week will be all about jobs, jobs, jobs.

Monday, September 2, markets were closed for the US Labor Day.

Today, Tuesday, September 3 at 10:00 AM, the August ISM Purchasing Manager’s Index is out.

On Wednesday, September 4, at 2:00 PM, the Fed Beige Book for July is published.

On Thursday, September 5 at 8:30 AM EST, the Weekly Jobless Claims are printed. At 10:30, we learn the ADP Report for private hiring.

On Friday, September 6 at 8:30 AM, the August Nonfarm Payroll Report is printed.

The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I’ll be filling out the paperwork for my own home refi. JP Morgan Chase Bank (JPM) is offering the best deals, in my case a 30-year fixed rate no-cash-out jumbo loan for only 3.4%. Now where did I put that tax return?

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/06/john-thomas-camping.png431322Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-09-03 02:02:172019-10-14 09:45:45The Market Outlook for the Week Ahead, or Visibility is Poor

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-08-30 09:26:092019-08-30 09:26:09August 30, 2019 - MDT Pro Tips A.M.

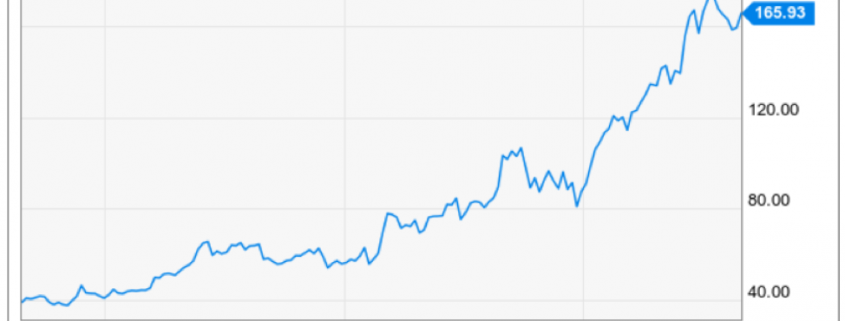

A tech company that I won’t hesitate to pull the trigger on new trade alerts is Veeva Systems (VEEVA).

The most recent results illustrate how investors can never discount strong cloud companies even if the elevated levels of risk scare many people out of making committed investments.

Q2 was another strong quarter with total revenue of $267 million, up 27% year-over-year.

Subscription revenue grew 28% year-over-year, and non-GAAP operating margin was 39%.

Veeva has now passed the $1 billion revenue run rate.

This is 1.5 years ahead of the target first laid out in 2015, an influential contributor to this success has been customer satisfaction.

Strong momentum in Commercial Cloud contributed to outperformance in Q2.

In core customer relationship management (CRM), Veeva continues to extend its leadership position with new small and medium business (SMB) customers and additional enterprise expansions.

Customers continue to adopt more CRM add-ons. This happens on a product-by-product and region-by-region basis.

I’ll offer a few pertinent examples.

Veeva CRM Engage had one of its strongest quarters as 4 top 20 pharmas expanded their use of Engage to new field teams.

Customers are attracted by the deep functionality and multi-platform support of Engage and the tight integration with CRM.

Veeva notched some important design wins at the top 20 pharma for Events Management.

A current customer has been using core CRM globally for many years and recently decided to expand their Veeva relationship to include Events Management in more than 90 countries over time.

They chose Veeva because of the deep functionality and professional services capabilities needed for global events management rollout.

They will replace multiple custom systems and spreadsheets leading to a more efficient and compliant global process.

This type of commitment to Veeva’s products is a positive sign as it tries to retain a more long-standing customer.

Who else does Veeva Systems work with?

They recently signed their 10th top 20 Pharma for Vault QualityDocs. Following their success with Vault PromoMats, eTMF and Submissions.

The pharma customers selected QualityDocs as part of their move away from the legacy content management platform.

What is Veeva QualityDocs?

It is software that provides superior ease-of-use and seamless collaboration, Vault QualityDocs reduces compliance risk and improves quality processes.

It accelerates review and approval workflows and facilitates sharing of GxP documents among employees and partners.

The dire need for modernization is driving the move to Veeva in this area as is the benefit of having QMS integrated with QualityDocs and Training on the Vault platform.

This is another great example of the innovation Veeva captures from an underserved market.

There has also been meaningful progress in 3 targeted industries: consumer packaged goods (CPG), chemicals, and cosmetics.

Since announcing the new Vault Claims product last quarter, Veeva now has projects in place at 3 top CPG companies.

Veeva is also making similar inroads in chemicals and cosmetics industries.

In total, Veeva now has major business at a top 20 CPG, a top 20 cosmetics company and 2 major chemical companies.

And this is just the beginning.

I’ll continue to bet on this stock going up.

It’s the best health tech cloud play out there, no reason not to love the direction of the company.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/08/veeva-aug30.png568974Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-08-30 05:02:112019-08-30 04:48:27Diving Back Into Veeva Systems

“I don't want to be liked.” – Said Founder of Alibaba Jack Ma

https://www.madhedgefundtrader.com/wp-content/uploads/2019/08/jack-ma.png400310Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-08-30 05:00:142019-08-30 04:48:16August 30, 2019 - Quote of the Day

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.