The Market Outlook for the Week Ahead, or Visibility is Poor

I have a pretty good view from my home on a mountaintop in San Francisco.

To the west, I can see through the Golden Gate Bridge all the way out to the Farallon Islands 20 miles off the coast. To the south, there is Stanford’s Hoover Tower and all of Silicon Valley. In the winter I can look east and see the snow-covered High Sierras 200 miles away.

However, during last year’s wildfires, I couldn’t see a thing. Visibility ended at 100 yards, the cars parked outside were covered in ash, and I could barely breathe. We were all confined indoors.

I kind of feel that’s the way the stock market is right now. You can’t see a thing, so it’s better to stay indoors.

Not only are market gyrations subject to unpredictable and random, out-of-the-blue influences. The old playbook about cross market correlations and how asset classes respond at different points of the economic cycle doesn’t work either.

The good news is that August is over, the second worth trading month of the year. The bad news? September is the WORST trading month of the year!

So, what does a trader do on the first day of the worst investment month of the year?

Research.

That's what I’ll be doing, waiting for the next cataclysmic collapse to buy or the next euphoric bubble to sell short. Until then, I’ll be sitting tight. Just running my existing long/short trading book, I’ll be up 3.4% by the September 20 option expiration date in 15 trading days.

There is one BIG positive for the economy that no one is talking about. The home ATM is open for business, and open like it’s never been open before.

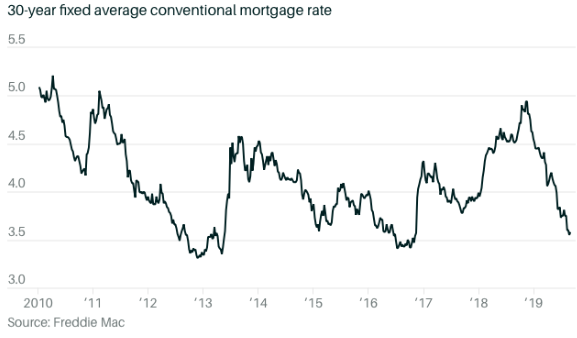

The thirty-year fixed rate mortgage rate is now at 3.56%, 10 basis points over a decade low and 20 basis points above an all-time low (see the chart below). There are currently $9.4 trillion of outstanding home mortgages in the US. Some $5 trillion is in Fannie Mae and Freddie Mac conforming loans, some 90% of which have interest rates higher than the current market.

If just ten million of these mortgages refinance obtaining an average of $4,560 in annual savings each, that will amount to a de facto tax cut of $456 billion per year, not an inconsequential amount. And Goldman Sachs thinks we could be in for as much as 37 million refis. It could be enough to offset the negative impact of the trade war.

As for the past week, it seemed like a disaster a day.

Trump ordered all US companies out of China. Like you can reverse 40 years’ worth of trillions of dollars of investment with a Tweet. If they did, an iPhone would cost $10,000 and your low-end laptop $15,000. An escalation of the trade war is the last thing your 401k wanted to hear. Kiss that early retirement goodbye.

Oil crashed (USO) on trade war escalation, with the industry now seeing a recession as a sure thing. Russian cheating on quotas is pouring the fat on the fire creating a massive supply glut in the face of shrinking demand. Take a long nap before considering any energy investment (XLE). The long-term charts show they are all going to zero.

Prime Minister Boris Johnson suspended Parliament, prompting a free fall in the pound. It’s to keep Parliament from blocking his hard Brexit, where it would certainly loose by a landslide. It’s all up to the Queen now, the monarch, not the rock group.

The yield inversion is deepening, with the US Treasury selling two-year notes today at a 1.56% yield, with ten-year yield closing at 1.45%. And that’s with the Treasury selling a total of a gob smacking $113 billion worth of bonds last week, which should have driven rates UP! US ten-year TIPS now showing negative interest rates.

Company stock buy backs are fading. That's a big deal as corporations retiring their own shares have been the biggest buyers in the market for the past two years. As if you needed another reason for downside risk.

US 15% tariffs hit on Sunday, and the Chinese paused in retaliation. Christmas is about to get more expensive. Many large retailers won’t make it until the new year. Keep selling short Macy’s (M) on rallies.

Bond yields hit new lows, at 1.44% for ten-year US Treasury bonds. The next stop is zero. Fixed income markets are saying that a recession is imminent. “Inversion” will be the world of the year for 2019. Go refi that home if you can get a banker on the phone!

There is no way out of the next recession, says hedge fund titan Ray Dalio. With global rates below zero, you can’t cut to stimulate business. You can’t do any more quantitative easing either, as the world is already glutted with paper. This is the trap Japan has been caught in for the last 30 years. It is all sobering food for thought.

US growth slowed with the second reading of the Q2 GDP marked down from 2.1% to 2.0%. The downturn has continued since the economy peaked 18 months ago. Q3 will be much worse when the trade war and earnings downgrades hit big time. And then there’s the soaring deficit. Sow the wind, reap the whirlwind.

US Consumer Sentiment took a dive from 98.4 to 89.8 in August. Has the spending boom just peaked? If so, we’re all toast. The "tariff cliff" is already taking its toll.

The Mad Hedge Trader Alert Service has posted its best month in two years. Some 22 or the last 23 round trips, or 95.6%, have been profitable, generating one of the biggest performance jumps in our 12-year history.

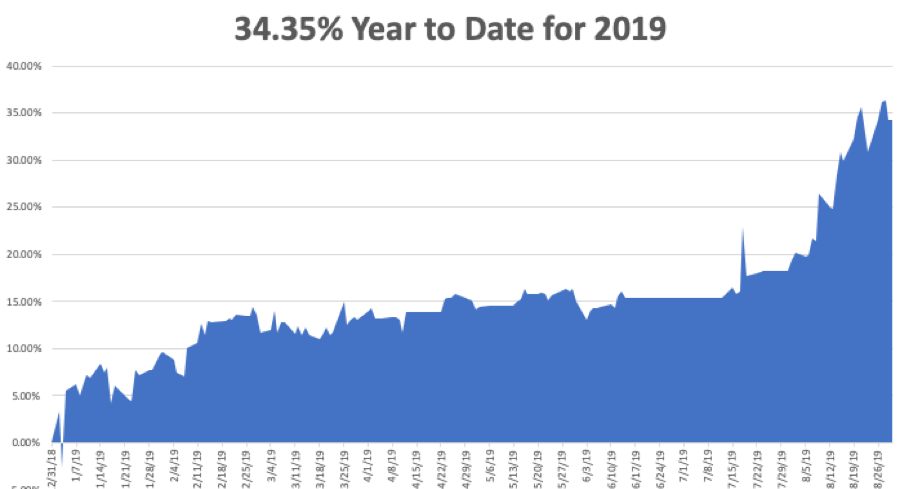

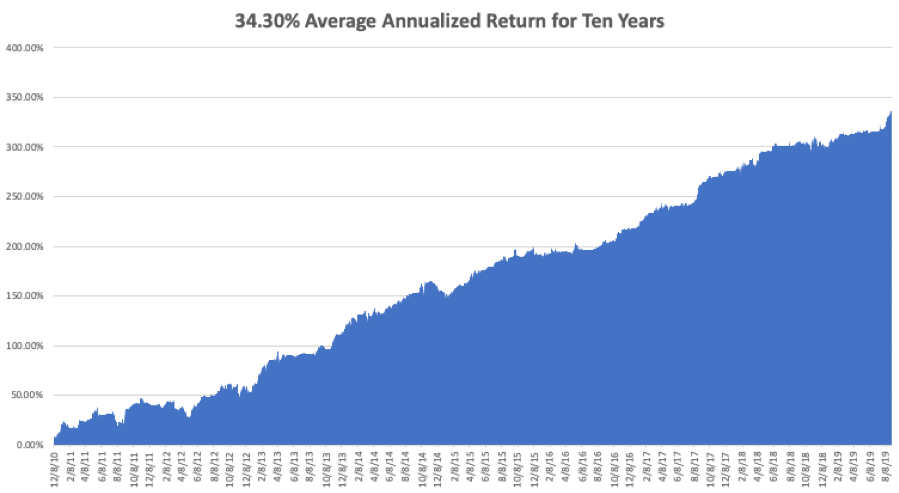

My Global Trading Dispatch has hit a new all-time high of 334.48% and my year-to-date shot up to +34.35%. My ten-year average annualized profit bobbed up to +34.30%.

I raked in an envious 16.01% in August. All of you people who just subscribed in June and July are looking like geniuses. My staff and I have been working to the point of exhaustion, but it’s worth it if I can print these kinds of numbers.

As long as the Volatility Index (VIX) stays above $20, deep in-the-money options spreads are offering free money. I am now 60% invested, 40% long big tech and 20% short Walmart (WMT) and the Russell 2000, with 20% in cash. It rarely gets this easy.

The coming week will be all about jobs, jobs, jobs.

Monday, September 2, markets were closed for the US Labor Day.

Today, Tuesday, September 3 at 10:00 AM, the August ISM Purchasing Manager’s Index is out.

On Wednesday, September 4, at 2:00 PM, the Fed Beige Book for July is published.

On Thursday, September 5 at 8:30 AM EST, the Weekly Jobless Claims are printed. At 10:30, we learn the ADP Report for private hiring.

On Friday, September 6 at 8:30 AM, the August Nonfarm Payroll Report is printed.

The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I’ll be filling out the paperwork for my own home refi. JP Morgan Chase Bank (JPM) is offering the best deals, in my case a 30-year fixed rate no-cash-out jumbo loan for only 3.4%. Now where did I put that tax return?

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader