Come join me for the Mad Hedge Fund Trader’s Global Strategy Luncheon, which I will be conducting high in the Alps in Zermatt, Switzerland. The event begins at 12:00 noon on Friday, September 29, 2023.

A three-course meal will be provided and there will be an open discussion on the crucial issues facing investors today will take place. You are welcome to attend in your mountain climbing gear, if necessary. One year, a guest descended from the Matterhorn summit to attend.

I’ll be giving you my up-to-date view on stocks, bonds, foreign currencies, commodities, precious metals, energy, and real estate. And to keep you in suspense, I’ll be throwing a few surprises out there too. Tickets are available for $277.

I’ll be arriving early and leaving late in case anyone wants to have a one-on-one discussion, or just sit around and chew the fat about the financial markets.

The event will be held at a central Zermatt hotel, the details of which will be emailed directly to you with your confirmation.

I look forward to meeting you, and thank you for supporting my research. To purchase tickets for the luncheons, please the BUY NOW! button above or click here.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-09-14 09:04:542023-10-02 09:40:03SOLD OUT - September 29 Zermatt, Switzerland Strategy Seminar

About a year ago, I received a call from a friend of Tony Robbins, the renown, six foot seven inch motivational speaker. He said he was looking for billionaires to participate in a future project.

I answered that I wasn’t a billionaire yet, but that he should call me in a couple of years when I might be there.

Last week, the end result of the project landed on my desk, his book, Money, Master the Game, The 7 Simple Steps to Financial Freedom, by Tony Robbins.

Since it was a near miss of a project of my own, I thought I would give it a quick read. I wasn’t expecting much. After all, the guy walks on burning coals for a living.

I couldn’t have been more wrong. Tony has put together a very coherent, readable, and extremely well researched tome. He has even put to use a formidable research team of his own to produce some fascinating findings about the very long-term returns of different investment strategies.

I was so impressed that I called a hedge fund friend to see if he had heard of the book. Not only had he heard of it, but his CEO had read it and ordered everyone in the company to read it, down to the kid in the mail room. A call to another hedge fund garnered the same response.

Five minutes later, I was on the Amazon website ordering copies for all of my adult kids.

Read the book and you can’t help but notice that Tony Robbins seems to know everyone on the planet. Warren Buffet and Bill Gates? Sure thing. The Dalai Lama? No problem. That is not faint praise, as I am not a slouch at name-dropping myself.

What is useful to both you and me is that Tony has interviewed at length the leading investment lights of our age and extracted their innermost investment secrets.

Name the top dozen investment gurus of the last 40 years and they are all there; hedge fund legends Ray Dalio and Paul Tudor Jones.

Index fund creator John C. Bogle. Legendary long-only managers David Swensen, Mary Callahan Erdos, and Sir John Templeton. The iconoclasts T. Boone Pickens and Carl Icahn are also there.

I know most of these people myself, and you have read their interviews in the hallowed pages of this newsletter. He certainly skimmed the cream.

The introduction is a bit retail. I suppose that Tony is trying to ease the amateur investors in there slowly and prepare them for the rude shocks that follow.

Then he shatters reader preconceptions outlining his nine investment myths. I have been hammering away at my own followers for years on many of these.

The sad truth is that much of Wall Street is trying to skin you alive, leaving your investment well-being at the bottom of their list of priorities. Almost no one reliably beats the market year after year, except myself and a handful of others, and it took me 50 years trying to get there.

Fees are always larger than you think. Published mutual funds results overstate profits, as they have a strong survivor bias. Target-date mutual funds can be disastrous. Fund managers close their losers as fast as they can to skew their results.

Annuities don’t fit into the modern world. Trading means losing for most people. Almost no one can time the market (except me, again). Chasing manias can be the perfect buy high, sell low strategy.

At the end of the day, a balanced portfolio of index mutual funds and Treasury bonds rebalanced annually is probably the best solution for most.

Let me make it clear. This is not a “how to trade” book. Nor is it a “get rich quick scheme.” It is a sober and thoughtful analysis of how the average working person should invest their savings over the course of their lifetime.

At 565 pages, the book is a bit of a wristbreaker. But it is one of the best investment books that I have ever read. And I have read most of them published over the last 100 years.

In fact, I didn’t even read the book, I listened to it on an audio book from Audible.com while backpacking in the High Sierras, which is also owned by Amazon.

As I spend so much time researching and writing these letters, I have little other choice.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/03/MONEY-Master-the-Game.jpg548365Arthur Henryhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngArthur Henry2023-09-14 09:02:522023-09-14 09:30:54The Blockbuster Read in the Hedge Fund Community

Nvidia, the American multinational technology company renowned for its innovations in graphics processing units (GPUs), is currently in negotiations to assume a pivotal role as the 'anchor' investor in the forthcoming initial public offering (IPO) of Arm Ltd. This potential move has sent ripples of excitement, speculation, and even some concern throughout the tech industry, as it could have profound implications for the global semiconductor landscape. Nvidia's involvement as the primary investor in Arm's IPO is a development laden with complexity, implications for competition, and potential for reshaping the semiconductor industry as we know it.

A Storied History of Innovation

Before delving into the current negotiations, it's crucial to acknowledge the historic significance of both Nvidia and Arm in the technology world. Nvidia, founded in 1993, has earned its reputation as a powerhouse in the GPU market. The company's graphics cards have powered everything from high-end gaming systems to scientific research and artificial intelligence applications. Notably, Nvidia's GPUs played a pivotal role in the development of AI, driving the deep learning revolution through their remarkable processing capabilities.

Arm Ltd., on the other hand, has a distinguished legacy of producing energy-efficient microprocessor designs. Founded in the UK in 1990, Arm's intellectual property (IP) is found in countless devices worldwide, from smartphones and tablets to embedded systems and servers. Arm's designs have become the cornerstone of mobile computing, offering a blend of power efficiency and performance that has made it a preferred choice for a wide array of applications.

The Proposed Deal: Nvidia as an 'Anchor' Investor

Now, the news that Nvidia is in discussions to become an 'anchor' investor in Arm's IPO is causing considerable buzz and speculation. An 'anchor' investor typically plays a substantial role by providing a significant investment, thereby lending credibility and stability to an IPO. In this case, Nvidia's involvement would not only inject a substantial amount of capital into Arm's IPO but also solidify a strategic partnership between the two tech giants.

The proposed deal would see Nvidia invest a substantial sum, potentially amounting to billions of dollars, to acquire a considerable stake in Arm. Such a move would have a series of far-reaching implications, not only for the companies involved but for the broader tech industry.

Implications for Competition

One of the central concerns surrounding this potential deal is its impact on competition within the semiconductor industry. Arm has long been recognized for its commitment to licensing its processor designs to a broad range of companies, enabling innovation and competition in the market. If Nvidia, known for its vertical integration strategy, becomes a significant stakeholder in Arm, it raises questions about the future availability of Arm's technology to competitors. Will Nvidia's ownership of Arm limit access to these designs, potentially stifling competition and innovation in the semiconductor space?

This concern is particularly relevant given Nvidia's ongoing efforts to acquire Arm entirely, a deal that has faced regulatory scrutiny and opposition from several quarters, including some of Nvidia's competitors. The combination of Nvidia's GPU technology and Arm's CPU designs could potentially create a formidable technology juggernaut, further consolidating the industry.

Global Regulatory Scrutiny

The proposed deal between Nvidia and Arm has already attracted the attention of regulatory bodies worldwide. Multiple jurisdictions are closely scrutinizing the transaction due to its potential to reshape the semiconductor landscape and influence the competitive dynamics of the industry. Regulatory approval is a significant hurdle that must be overcome for this deal to proceed, and any perceived threat to competition may slow down or even halt its progress.

China, in particular, has been cautious about this potential partnership. The Chinese semiconductor industry heavily relies on Arm's IP, and any restrictions on access to Arm's designs could significantly impact Chinese tech companies' ability to compete globally. Consequently, the Chinese government's stance on the deal is likely to play a pivotal role in its outcome.

Reshaping the Semiconductor Landscape

If the deal goes through, Nvidia's role as the 'anchor' investor in Arm's IPO could reshape the semiconductor landscape in various ways. Nvidia could leverage Arm's extensive customer base, which includes companies from various industries, to further expand its reach in markets such as automotive, data centers, and the Internet of Things (IoT). This strategic alliance could potentially result in more tightly integrated hardware and software solutions.

Additionally, the collaboration between Nvidia and Arm could accelerate innovation in AI and deep learning, as both companies have made significant strides in these fields. Combining Arm's CPU designs with Nvidia's GPU prowess could yield even more powerful and energy-efficient AI solutions, potentially revolutionizing industries that rely on AI technologies.

Potential Benefits and Concerns

The potential benefits of Nvidia becoming the 'anchor' investor in Arm's IPO are undeniable. It could inject a significant amount of capital into Arm, enabling further research and development, as well as supporting Arm's growth in various markets. This, in turn, could result in more advanced and energy-efficient processor designs, benefiting a wide range of industries.

However, there are also concerns, including the potential for market consolidation and reduced competition, as mentioned earlier. It's essential that the deal, if approved, includes safeguards to ensure that Arm's IP remains accessible to a broad range of companies, promoting innovation and competition in the semiconductor space.

Global Impact

The ramifications of this deal extend far beyond the companies involved. The semiconductor industry is a vital component of the global tech ecosystem, with implications for national security, economic competitiveness, and technological progress. As a result, governments and regulatory bodies worldwide are closely monitoring developments related to Nvidia's potential role in Arm's IPO.

Furthermore, the semiconductor shortage that has plagued industries ranging from automotive to consumer electronics has highlighted the critical role that chip manufacturers play in the modern world. Any consolidation or changes in the semiconductor landscape can have far-reaching consequences for industries and economies worldwide.

Conclusion

The news of Nvidia's discussions to become the 'anchor' investor in Arm's IPO is a significant development in the tech world. It has generated considerable interest, not only because of the potential financial implications but also because of the potential impact on competition, innovation, and the broader semiconductor industry.

The proposed deal is a complex and multifaceted undertaking, with regulatory hurdles and global implications. Whether it proceeds and how it is structured will determine its ultimate impact on the tech industry and the world at large. Regardless of the outcome, the tech world will be watching closely, as this partnership between two tech giants has the potential to shape the future of the semiconductor industry for years to come.

Midjourney prompt: “Nvidia in Talks To Be ‘Anchor’ Investor in Arm's IPO”

https://www.madhedgefundtrader.com/wp-content/uploads/2023/09/ss-091323-mhai-c1.jpg583871Douglas Davenporthttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDouglas Davenport2023-09-13 17:25:212023-09-13 17:27:38Nvidia Could Become ‘Anchor’ Investor in Arm's IPO

If there is a company I would tell my grandkids to work for then it would be semiconductor company Qualcomm (QCOM).

Why?

Even Apple (APPL) can’t replace them so easily and that counts for a lot in this day and age.

We learned just as much as Qualcomm said that it will supply Apple with 5G modems for smartphones through 2026.

Qualcomm expected to lose the Apple smartphone business, because they expected Apple to use an internally developed 5G modem starting in 2024.

They couldn’t develop the product fast enough so it is back snapping up modems with QCOM.

QCOM is the best of breed for smartphone chips and they can be found in every flagship Android device.

I am specifically referring to QCOM’s Snapdragon products which are a suite of system on a chip (SoC) semiconductor products for mobile devices.

The Snapdragon's central processing unit (CPU) uses the ARM architecture.

This line of chips is incredibly competitive and one of the foundational reasons to hold the stock.

Samsung’s SoC competitor named the Exynos is still a far cry from the Snapdragon no matter how hard they try and it seems like each iteration of the Exynos flagship SoC is always a generation behind the Snapdragon.

Apple do use their own SoC with the newest one named the Apple A17 Bionic, but QCOM will still monopolize the Android market with their own Snapdragon that is actually slightly better than the A17 Bionic chip.

The Snapdragon 8 Gen 3 beats the CPU clock speed of the A17 Bionic.

This doesn’t always translate to better real-world performance, but it’s still an impressive feat.

People believe the new Taiwan Semiconductor Manufacturing Company (TSM) 3 nanometer (nm) processing can lose to the advanced 4nm node on the 8 Gen 3.

However, Apple will probably maintain a CPU lead, thanks to better software tuning and more transistors in the same area thanks to a smaller 3-nanometer node.

Basically, Snapdragon is a little faster but Apple has higher performance because of its superior software.

There is no denying that Apple has fantastic software.

On the revenue side, this is great news for the staying power of Snapdragon products and continued sales to Apple will boost Qualcomm’s handsets business, which reported $5.26 billion in sales in the past quarter and could soften the blow of potentially losing a critical customer.

About 21% of Qualcomm’s fiscal 2022 revenue of $44.2 billion came from Apple.

APPL purchased Intel’s smartphone modem division in 2019 to build its own modem. However, evidence suggests that it will be challenging for Apple to move away from Qualcomm’s chips because of their complexity.

Qualcomm also makes money from Apple through cellular licensing fees, which were about $1.9 billion in 2022.

Qualcomm continues to collect royalties from Apple under a six-year agreement. That agreement was struck at the end of a legal battle between Apple and Qualcomm over royalties that was settled in 2019.

Qualcomm says that it expects to only supply 20% of the modems needed for Apple’s 2026 smartphone launch, signaling that it likely still expects the Apple business to eventually decline.

Apple’s new iPhone called iPhone 15 uses QCOM modems as do many other high-end smartphones.

It’s hard to believe that QCOM’s market capitalization is only $125 billion. The eye test alone makes me think this is a half a trillion-dollar company.

Revenue is accelerating and they offer a 2.9% dividend yield.

I can’t talk more about the high quality of products made by QCOM.

This company will have staying power and even if Apple decides to move on, there are a slew of companies ready to gobble up QCOM chips.

Readers shouldn’t trade this stock, but they should buy and hold for the long haul.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-09-13 15:02:482023-09-13 15:06:57A Great Chip Stock to Buy and Hold

Many of us are on the lookout to increase our income.

There are some ways to do this.

We know with interest rates surging our cash in savings accounts receive higher yield and 90-day T-bills also offer a good 5%+ yield.

But is there anything else besides Bonds where investors can find robust returns?

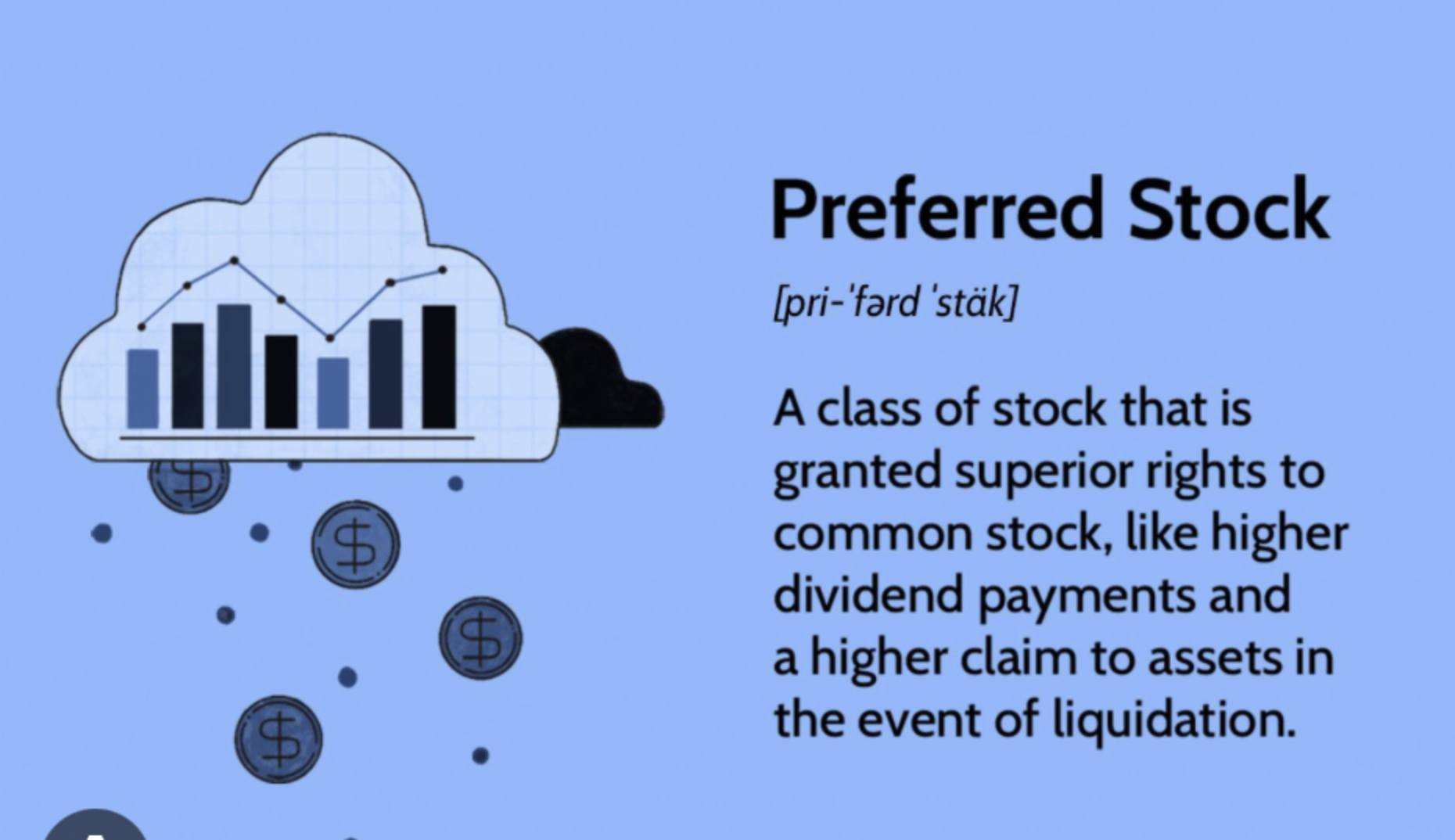

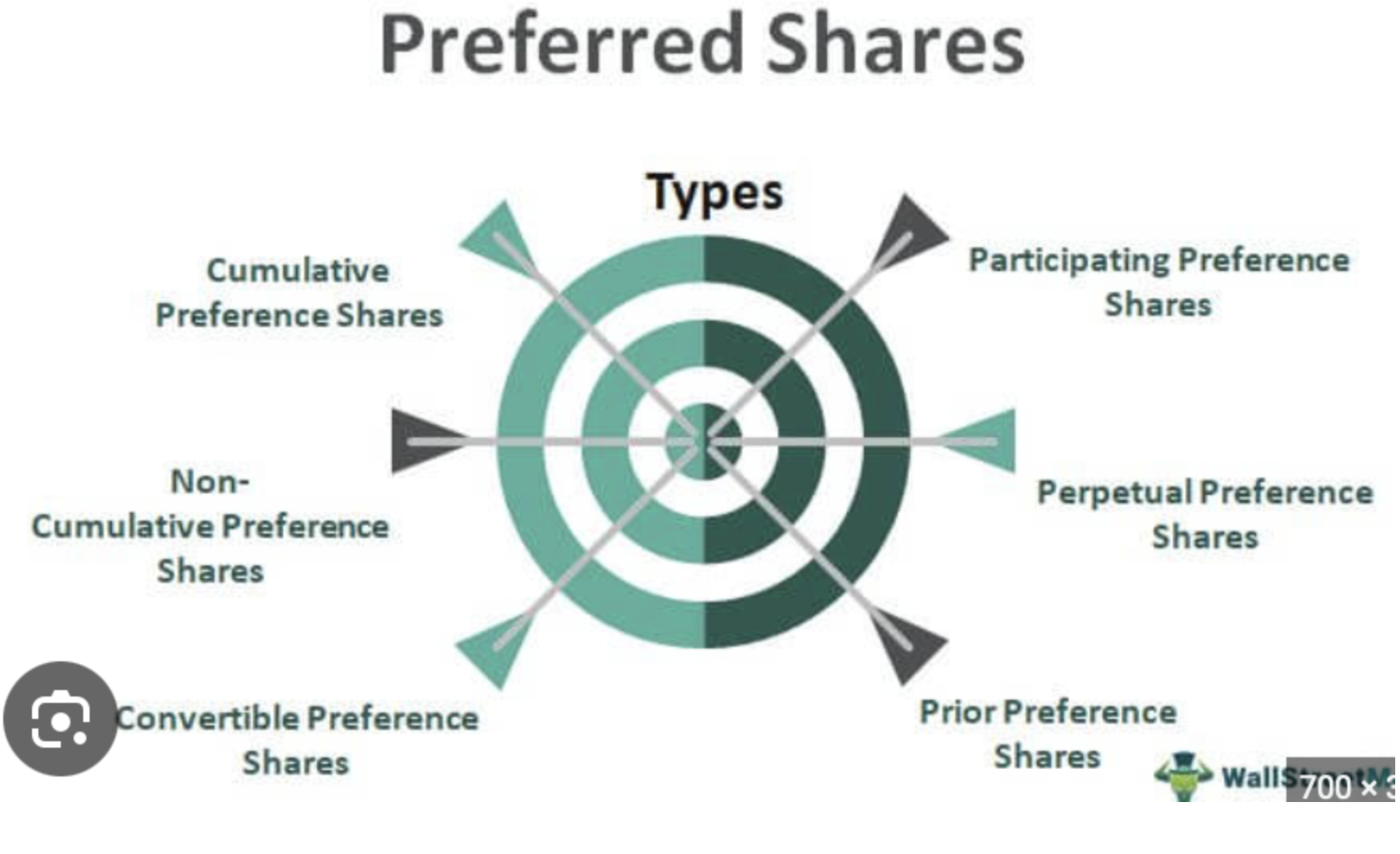

Preferred stocks are one option that comes to mind.Both my mother and I owned these in the 1990’s and early 2000’s. They combine elements of stocks and bonds in one investment.

Preferreds are attractive because they provide the stability of fixed-dividend payments, which is bond-like, but they also offer equity like appreciation. So, it is a nice balance. (Note, that the equity price appreciation is often lower than common stock.)

Bonds are offering 5%+ right now, but a preferred stock gets investment grade security that yields 6.5% - which is solid income – without taking on too much credit risk.

Most investors are attracted to preferred stocks because they offer more consistent dividends than common shares and higher payments than bonds. Preferreds are issued with a fixed par value and pay dividends based on a percentage of that par, usually at a fixed rate. Let’s say that a preferred stock had a par value of $100 per share and paid an 8% dividend. To calculate the dividend, you would need to multiply 8% by $100 (the par value), which comes out to an annual dividend of $8 per share. If dividend payments are made quarterly, each payment will be $2 per share.

One downside of preferreds is that they don’t have the same voting rights as common shareholders.The company is not beholden to preferred shareholders the way it is to traditional equity shareholders.

To recognise a preferred stock, look for a P at the end of the ticker symbol.

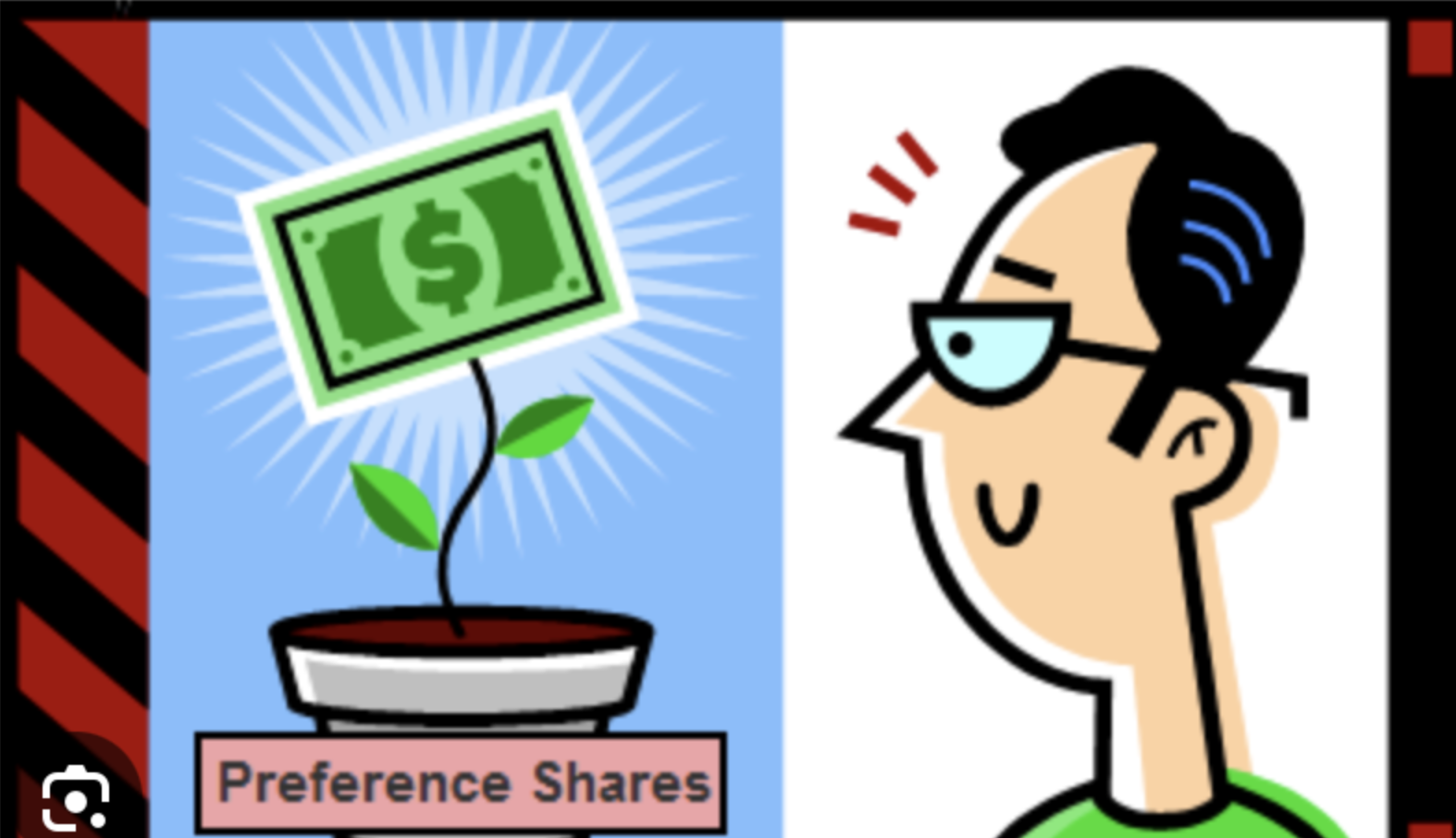

Convertible shares are preferred shares that can be exchanged for common shares at a fixed rate. This can be very lucrative for preferred shareholders if the market value of common shares increases. (This is the type of preferred shares my mother and I held). Once the shares have been exchanged the shareholder gives up the benefit of a fixed dividend and cannot convert common shares back to preferred shares.

Cumulative preferred shares have a clause that protects the investor against a downturn in company profits.If revenues are down, the issuing company may not be able to afford to pay dividends.Cumulative shares require that any unpaid dividends must be paid to preferred shareholders before any dividends can be paid to common shareholders. If a company guarantees dividends of $10 per preference share but cannot afford to pay for three consecutive years, it must pay a $40 cumulative dividend in the fourth year before any other dividends can be paid.

Non-Cumulative shares do not entitle an investor to missed dividends. (If one year the company decides not to pay dividends, they won’t pay it the next year.As a result, the investor loses his or her right to claim any unpaid dividends.) Interest on a non-cumulative deposit is paid on a regular basis, whereas interest on a cumulative deposit is paid at maturity.

Participatory Preferred shares provide an additional profit guarantee to shareholders. All preference shares have a fixed dividend rate, which is their chief benefit. However, on top of that chief benefit, participatory shares guarantee additional dividends in the event that the issuing company meets certain financial goals. So, for example, if the company has a really good year and meets a predetermined profit target, holders of participatory shares receive dividend payments above the normal fixed rate.

Instead of looking for single stocks that offer preferreds, you could look at SPDR ICE Preferred Securities ETF (ticker: PSK), which yields 6.5%.

You could also look at ETF’s that focus on dividend paying stocks which offer another avenue for income. Pro-Shares S&P Dividend Aristocrats ETF (NOBL) is one that comes to mind. It’s an $11.65 billion fund that tracks the S&P 500 Dividend Aristocrat Index. The yield is 1.95% and year to date return is 4.43%.

The yield doesn’t appear crash hot when you first see it, but long-term, you have to remember this is stock investing, and therefore you get the opportunity for price appreciation.So, over the long term you will most probably receive better returns those bonds.

The much talked about recession that may happen or may not happen, whether it be hard, soft or in the middle of those descriptions is background noise at the moment, but it is always wise to hold high quality companies in a stock portfolio, and companies that have dividends which keep growing tend to be those high-quality companies.

From time to time, I receive an email from a subscriber telling me that they are unable to get executions on trade alerts that are as good as the ones I get. There are several possible reasons for this:

1) Markets move, sometimes quite dramatically so.

2) Your Trade Alert email was hung up on your local provider’s server, getting it to you late. This is a function of your local provider’s capital investment and is totally outside our control.

3) The spreads on deep-in-the-money options spreads can be quite wide. This is why I recommend readers place limit orders to work in the middle market. Make the market come to you.

4) Thousands of market makers read Global Trading Dispatch. The second they see one of my Trade Alerts, they adjust their markets accordingly. This is especially true for deep-in-the-money options. A spread can go from totally ignored to a hot item in seconds. I have seen daily volume soar from 10 contracts to 10,000 in the wake of my Trade Alerts.

On the one hand, this is good news, as my Trade Alerts have earned such credibility in the marketplace. It is a problem for readers encountering sharp elbows when attempting executions in competition with market makers.

5) Occasionally, emails just disappear into thin air. This is cutting edge technology, and sometimes it just plain doesn’t work. This is why I strongly recommend that readers sign up for my free Text Alert Service as a back up. Trade Alerts are also always posted on the website as a secondary back up and show up in the daily P&L as a third. So, we have triple redundancy here.

The bottom line on all of this is that the prices quoted in my Trade Alerts are just ballpark ones with the intention of giving traders some directional guidance. You have to exercise your own judgment as to whether the risk/reward is sufficient with the prices you are able to execute yourself. Sometimes it is better to pay up by a few cents rather than miss the big trend. The market rarely gives you second chances.

Good luck and good trading.

John Thomas

https://www.madhedgefundtrader.com/wp-content/uploads/2012/09/BusinessJohnThomasProfileMap2-11.jpg264400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-09-13 09:02:282023-09-13 15:48:18On Executing Trade Alerts

In the ever-evolving world of biotechnology, only a few names consistently stand out.

For years, Gilead Sciences (GILD) has stood out as more than just another player; it has consistently taken center stage as a star performer. This distinction is not based on superficial glitz but on Gilead's profound impact on the healthcare industry, particularly within the competitive HIV drug marketplace.

Biktarvy, Descovy for PrEP, and Sunlenca are more than mere pharmaceutical labels. Each represents a breakthrough, a monumental feat in a domain where every scientific discovery is not just valuable but potentially transformative. These aren't just drugs; they're the culmination of relentless research, dedication, and innovation.

Yet, even stars face challenges.

The recent pandemic cast an unexpected shadow over Gilead's illustrious record. The fallout? A notable drop in HIV diagnoses and prescriptions. While many companies might buckle under such pressure, Gilead's history tells a story of resilience and adaptability.

True to form, Gilead rose from the pandemic's challenges, focusing on an area of vast potential: oncology. Though the oncology division currently represents only a fraction of its total revenue, the rate at which it’s growing is astounding. In fact, its current pace outpaces most other sectors in Gilead's portfolio.

But let's step back for a moment and consider the broader picture.

Gilead is more than its product lineup. It's an embodiment of innovation. With a portfolio boasting over 60 active research programs, Gilead is a veritable treasure trove for investors hungry for dividends.

The numbers speak for themselves: a 31.6% dividend growth over the last five years, punctuated by an impressive 3.84% yield. For investors, this isn’t just a statistic; it's a promise of consistent returns.

The story of "Veklury" (remdesivir) is particularly noteworthy, providing a glimpse into Gilead’s financial agility and foresight. Introduced as a beacon of hope in the fight against COVID-19, Veklury saw sales soar to unprecedented heights.

When market murmurs hinted at a potential sales slump for the drug, Gilead pivoted, securing FDA approval to expand Veklury's application to a broader range of liver conditions. Consider the magnitude of this move: over 100 million Americans are grappling with liver diseases.

With this demographic being particularly susceptible to COVID-19, the market potential for Veklury is undeniable. However, the narrative of global health is as fluid as it is unpredictable. While COVID-19 might not dominate every headline as it once did, its presence is still felt worldwide. A recent surge in hospitalizations in the U.S. is a stark reminder of the virus's lingering threat.

Now, if we dive deeper into the financial intricacies of Gilead over the past five years, a pattern of resilience emerges.

The company boasts a 22.9% growth in revenue, accompanied by a 12.8% increase in free cash flow. And while Veklury’s contributions are significant, removing its influence paints a broader picture of a firm that’s consistently navigated both favorable winds and stormy seas.

Their adaptability shines through in the numbers. Gilead's oncology segment saw a remarkable 38% YoY growth in Q2 2023, generating $728 million in revenue. If these figures are any indicator of the future, the oncology division may soon be a powerhouse in Gilead’s financial framework, potentially contributing up to $10 billion.

Pivotal to Gilead’s revenue story are Biktarvy and Descovy. Their H1 2023 sales figures stand at $5.65 billion and $965 million, respectively. Predicting stratospheric growth rates might be ambitious, but data suggests that steady, upward progress isn’t just probable—it's expected.

The stock market is known for its whims, but seasoned analysts believe Gilead might currently be undervalued. The biotech industry is a roller-coaster, full of unexpected turns, but with Gilead at the helm, the ride promises to be exhilarating.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-09-12 18:00:082023-09-12 18:39:06A Star Performer in the Biotech Universe

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.