(THE COMMON PROBLEM OF EARNING $500K AND LIVING WITH DEBT)

August 7, 2023

Hello everyone,

The rules around money management appear to be relatively simple.

Don’t spend more than you make.

Don’t buy things when you don’t have the money to cover it with cash or a credit card.

Pay off credit cards at the end of the month, so interest is not accrued.

Keep a pot of money aside in another bank account for emergencies.

Pay yourself first.

Invest on a consistent basis.

Simple rules, yet many of us break the rules and find ourselves in deep water. Why is that? The answer is often complex and often relates to our behaviour around money.

Let me share a story with you.

My father was a dentist. He ran a practice for 47 years and served as a dentist in the war. For many years, my mother who was a trained nurse was his dental nurse. My father was an excellent dentist, but he was poor at running the business side of his practice. He often didn’t charge patients for examinations and would often let people only pay half price for dentures he had made them. This is admirable, no doubt, but it is not sustainable when you are running a business and have bills to pay to support your family.

So, my mother basically took over the management of the dental practice and clearly itemized the cost of procedures, which was placed on the wall in the waiting room. There was a possibility to pay in installments, but it was strictly monitored by my mother. In essence, she became the dental nurse and the finance manager of the practice.

My mother taught me a lot about financial management. Her mantra was to live simply, grow your wealth and invest in education. I lived a comfortable life growing up, but we never went on grand holidays or trips, didn’t ever eat out, did all the domestic chores ourselves and mowed the lawns, and tended to the garden ourselves as well. We were happy with simple pleasures. The home was always filled with music, and books were a go-to when you were looking for something to do. All meals were homemade from scratch and there were always baked treats on the kitchen bench to enjoy. We had many cats and dogs as pets, and they were treated as part of the family. In fact, it was often the case that dogs in the street where we lived would crash at our place for the day, where they could chill out and enjoy attention and love from us. Their owners often left them alone during the day, and, as we know, pets crave companionship. Dinnertime conversations had an intellectual depth to them as the whole family shared an interest in history, literature, and finance.

My mother kept a book that monitored how we spent our money. So, every month, we knew exactly how much we had spent and where it had been spent. Every three months at least, funds would be invested in a specific item – be it a share, index fund, gold, or even bonds. In that way, extra income that was made from the practice wouldn’t get burned in day-to-day spending. The big-ticket spending item in our household was education. My brother has a Ph.D. in European History, and I finished my 10 years of study with an MBA.

There was no keeping up with the Jones in our household, and no desire to participate in the commercialization of special holidays like Easter, and Christmas. We observed the holidays, but our celebrations were simple.

The point here is that it is not necessary to spend a lot of money to have a good life. And how much you earn does not determine how well you will live. It is what you do with the funds and how you behave with that money that controls what your life and your future will look like.

When you get a pay rise, what do you do with that extra income?

You survived without it before, so wouldn’t it seem prudent to put it aside in a savings account for emergencies? There are high-yielding savings accounts out there. You just need to do some research. For example, there is one called the Lending Club High-Yield Savings Account which offers 4.50% (APY). It has no minimum balance requirement after $100 to open the account, no monthly fee and it offers an ATM card.

Or you could pay yourself first by allotting a portion of it to an investment.

Building a framework helps.

For a financially sustainable lifestyle, simple math is involved.

What are your fixed costs each month or quarter and do you make enough to cover these?

Mortgages, car payments, childcare, taxes, utilities, food, school fees, insurance, etc.

Then work out where the rest of your money goes by thinking in categories.

Travel, personal spending, entertainment, dining out, activities/sports for the children.

Can you cover these costs easily without diving into your credit card each month?

The best way to think about your spending is to ask yourself questions?

Do I need this fancy car? Do I need two cars?

Do I need a fancy vacation every year?

Do I need to dine out several times a month?

Do I need to pay for all these camps/activities and sports for my children?

If paying for all this lifestyle is crippling you, then why are you doing it?

Are you in the comparison game? Are you listening to that little voice in your head that is comparing your finances to others?

Stop doing this. It’s a waste of time and energy and will bring you no joy.

You need to get to a place where your happiness is not dependent on having things. A happy and contented person is one who has plenty of savings and investments and is not in a panic about paying bills each month. You just need to shift your perspective a little.

You will enjoy life more and have much less stress and grow your wealth too. Surely, a win-win situation.

Have a great week.

Cheers,

Jacquie

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-08-07 20:00:352023-08-07 23:23:50August 7, 2023

Artificial intelligence (AI) took center stage in 2023 as the investment sweetheart, with the big tech leviathans basking in the limelight.

All eyes have been on the “Magnificent Seven” – Alphabet (GOOGL), Amazon (AMZN), Apple (AAPL), Meta (META), Microsoft (MSFT), Nvidia (NVDA) and Tesla (TSLA) – as they dance in the glow of their massive market capitalizations on the grand stage of the broad market (SPX)(QQQ).

Yet, hidden in the wings and enjoying a spectacular resurgence in 2023 following a calamitous act in 2022 are several AI and AI-adjacent rising stars, such as C3.ai (AI).

Now, don't be misled by the meteoric 250% ascension of C3.ai's stock this year. The numbers behind the scenes haven't exactly been show-stopping.

While C3.ai had a promising opening act with a year-over-year revenue growth peaking at 42%, the company's balance sheet still stubbornly shows red, and its last quarter's revenue was more or less a carbon copy of the previous year.

In 2022, C3.ai flaunted an impressive 38% revenue jump. However, the story told a different tale in 2023, which saw a rather modest growth of 6% to $267 million.

A glance at the horizon of fiscal 2024 predicts a growth rate oscillating between 10% and 20%. The company's tapering progress was conveniently pinned on macro headwinds that allegedly led corporate giants to reassess their software expenses.

Let’s further dissect this multilayered enigma.

A chameleon of sorts, C3.ai has a history of evolving with the times. Starting as C3 Energy, it later donned the garb of C3 IoT (Internet of Things) before finally settling on the moniker of C3.ai in 2019, just as AI began to twinkle in the market's eye.

C3, despite its shiny AI cloak and a lucrative IPO back in 2020, is mostly dishing out the same machine learning algorithms it was developing pre-rebranding. Sure, these algorithms have the knack to automate and speed up tasks, but tagging them as groundbreaking AI tools is an area where the bears and bulls lock horns.

Mainly courting large-scale energy, industrial, and governmental clients, C3 rakes in over 30% of its revenue from a joint operation with energy titan Baker Hughes (BKR) — though that's due to wind down in fiscal 2025.

Meanwhile, in response to slowing growth, C3 made the significant decision last year to transition from subscription to usage-based fees. This strategy aims to attract potential customers during tough economic times. However, this change could decrease short-term revenues and make their offering less appealing, as customers may perceive this pricing model as less predictable and harder to budget for.

It's also impossible to overlook the formidable competitors breathing down C3's neck: Amazon Web Services (AWS), Microsoft's Azure, Google Cloud Platform (GCP), and other cloud infrastructure titans already offering comparable AI solutions tailored for enterprises.

Tech analysts are raising their glasses to C3, setting price targets even higher, but the consensus figure sits at $24.36. If you’re keeping score, this represents a potential plunge of nearly 40% from C3.ai's current stock price. With the stock's price-to-revenue multiple at 15 and over 4x its book value, it seems like it might have reached its peak, given the present state of the business.

Yet, the winds could change if the company outperforms in the upcoming year. They're forecasting revenue to hit up to $320 million for fiscal 2024 (wrapping up in April).

That would represent a 20% leap from the previous fiscal year, a marked improvement from last year's rather drab sub-6% growth. However, investors might have been hoping for a bigger pie, considering AI's the rising star this year.

Peering into C3.ai's future growth prospects is akin to looking through a smoky glass — the company's sudden transition to usage-based fees and the potential departure of Baker Hughes in 2025 only exacerbate this uncertainty.

Toss in the fact that C3.ai is still very much painted red with unprofitability based on generally accepted accounting principles (GAAP), and you've got a company whose financial health raises more questions than it answers.

By no means am I asserting that C3.ai's voyage is bound to hit an iceberg. Still, the numerous "maybes" clouding the company's landscape aren't very reassuring.

Unless you're an adrenaline junkie eager to strap in for this roller-coaster, adopting a "wait and watch" stance with C3.ai may be wise to see if it can genuinely metamorphose into a high-growth stock.

Midjourney prompt: "AI Darling or Delusion"

https://www.madhedgefundtrader.com/wp-content/uploads/2023/08/ss-080723-mhai-c2.jpg6901051Douglas Davenporthttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDouglas Davenport2023-08-07 17:23:382023-08-07 17:31:02AI DARLING OR DELUSION

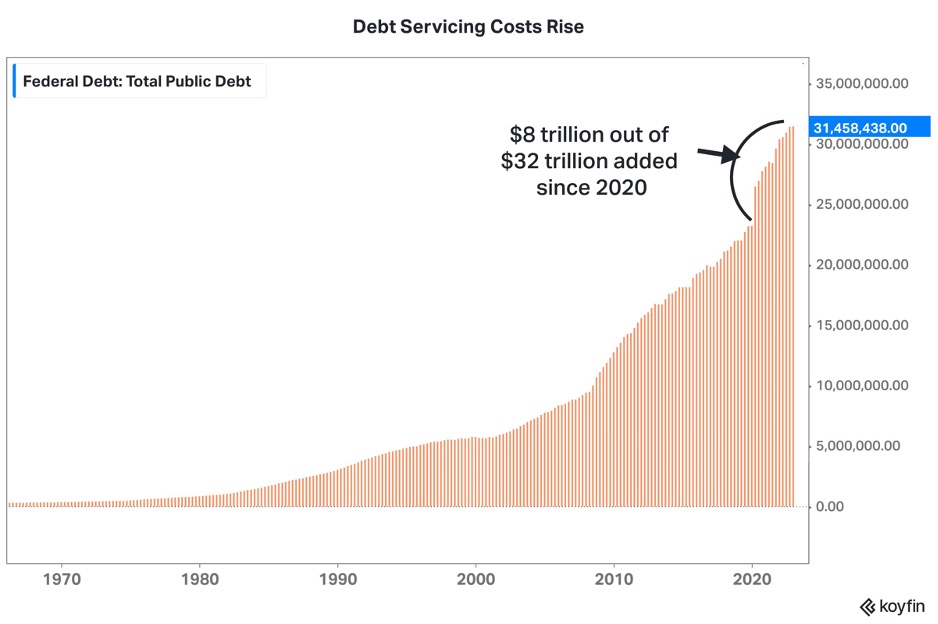

Fitch Ratings’ decision to strip the US of its AAA credit ranking to AA+ sets the stage for inflation to come roaring back, and tech stocks to underperform in the short term.

Why?

The downgrade risks bond yields blowing out, which in turn will potentially cause the U.S.’s interest payments on the debt to shift substantially higher.

That is exactly what investors don’t want to hear, in particular concerning technology stocks.

Tech stocks, along with U.S. housing prices, are most susceptible and sensitive to interest rate shocks and this could be a doozy.

The smaller the tech company is, the more reliant they are on initial debt funding to develop the company.

Big tech will be more insulated from this chaos because they are the equivalent of the reams of home buyers that purchased homes at a sub-3% interest rate that is fixed for 30 years.

As long as revenue is growing okay-ish, big tech will be fine, and the latest earnings reports have proved that with big tech’s unimpressive single-digit growth.

It’s nothing special but good enough for the times.

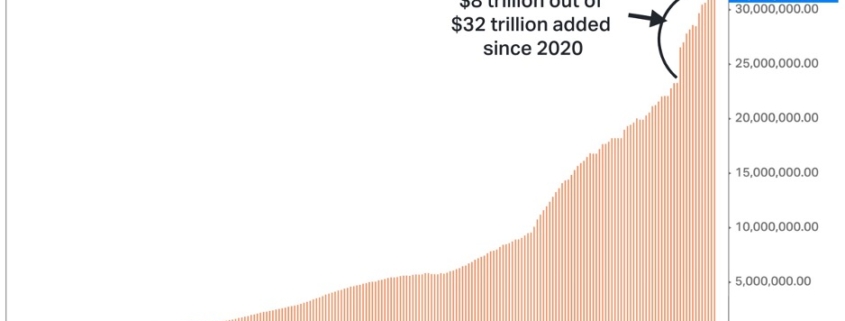

The booming federal deficits are the heart of the bear case for Treasuries and, even more poignant, the massive federal mismanagement of the country, no matter which political party has been in charge.

Take for instance, over 20 years and 3 presidents, a certain country would spend over $10 trillion in Afghanistan and the result is replacing the Taliban with the Taliban.

Many would say that wad of federal money probably wasn’t worth the paltry result.

Now, what we finally have is a real-life example of the consequences of government underperformance.

The U.S. economy is the most vibrant, productive, and profitable economy in the world.

Free market capitalism has catapulted the U.S. to build the largest and most successful tech industry in the world that is the envy of the rich world.

Now, exploding bond yields move to the fore as the largest risk for technology stocks.

The downgrade also means that Fed Chair Jerome Powell and the Central Bank will have a harder time pivoting when they want to because yields could spike and could have another dose of inflation to fight against.

The downgrade could invite a horde of algo traders and hedge fund pros to pile into the short-bond trade because where there is smoke, there is fire.

In the short term, don’t expect the 30-year US treasury yield to hit 10% which was the case in 1987.

However, a turn for the ugly and yields surpassing last year’s 4.35% is just in sign after this last melt up.

The stage could be set for the 30-year to reset at higher increments between 5%-6% with no relief in sight.

This sort of level is highly prohibitive to tech stocks in the short term, therefore, I would believe a repricing would need to take place to balance itself out.

In all honestly, tech needs a break and this appears as if it is the trigger to cool down tech stocks which have been on a pulsating trend to the upside in 2023.

Ultimately, I would describe the downgrade as inevitable. The rising (and accelerating) deficit begs the question of fiscal amateurism.

Congress has been behaving as if unlimited dollar binge spending has no consequence.

Furthermore, we can kiss smaller tech companies tapping the debt market goodbye.

Conditions keep tightening in tech and it’s becoming harder to thread the needle for the unknown quantity.

I would stick with investments in known quantities with strong balance sheets, as they will perform better in a spiking bond yield scenario.

Reload the ammo to buy the dip on those guys.

U.S. Congress is now on call to reign in the massive fiscal deficits or face yet another downgrade and even higher interest payments on federal bonds.

That would be materially negative for tech stocks in the medium term.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/08/debt-service.jpg624938Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-08-07 14:02:312023-08-22 17:07:35What the Downgrade Means for Tech

I am writing this to you from the British Airways first class lounge at Rome’s Leonardo da Vinci airport. I arrived here early to avoid the hordes of travelers certain to follow.

At the entrance to the departure area, there is a 20-foot-high bronze statue of the great artist and scientist holding a model of his 15th century imaginative helicopter design. He never built it, but I have seen modern-day life-sized copies.

You’re really taking your life in your hands taking a taxi in Rome. The only law seems to be qui audet, vincit, or who dares, wins (the motto of the British Special Air Service).

I know the 140 on the odometer was only in kilometers so I shouldn’t worry. What concerned me was that we were being passed by other cars doing at least 180.

Tighten that seat belt!

One disturbing practice of Italian drivers is that they never commit to a lane. They drive on the center line until they see a gap in the traffic then they go for it.

There’s nothing like coming home, only to be slapped in the face by a wet kipper. That was delivered by a black swan in the form of the Fitch downgrade of US debt from AAA to AA+ which shaved a shocking seven points off the (TLT) in a week.

The (TLT) held up valiantly in the face of the surprise red-hot Q2 GDP figure of 2.4%, indicating that a soft landing was a done deal. But once the Fitch report was out, it was all over but the crying. The (TLT) now looks like it could double bottom at the October 2022 low of $90.

I thought it was a huge overreaction. Fitch was only mirroring Standard & Poor’s identical downgrade in 2011, the last time a default was in the cards. The US economy and its debt remain the strongest in the world.

But with Republican members of Congress threatening a debt default at every opportunity, what was Fitch supposed to tell its customers? Any lender who threatens not to pay gets downgraded, the US Treasury, you, and even me. The real question is why it took so long. Take your trading loss on the (TLT) out of your next campaign donation.

You never argue with Mr. Market, who is always right. What the selloff does is set up the LEAPS of the century, the (TLT) 2025 $90-$95 vertical bull call spread with a certain 100% profit built in. However, given last week’s experience, I’d rather be late in this trade than early.

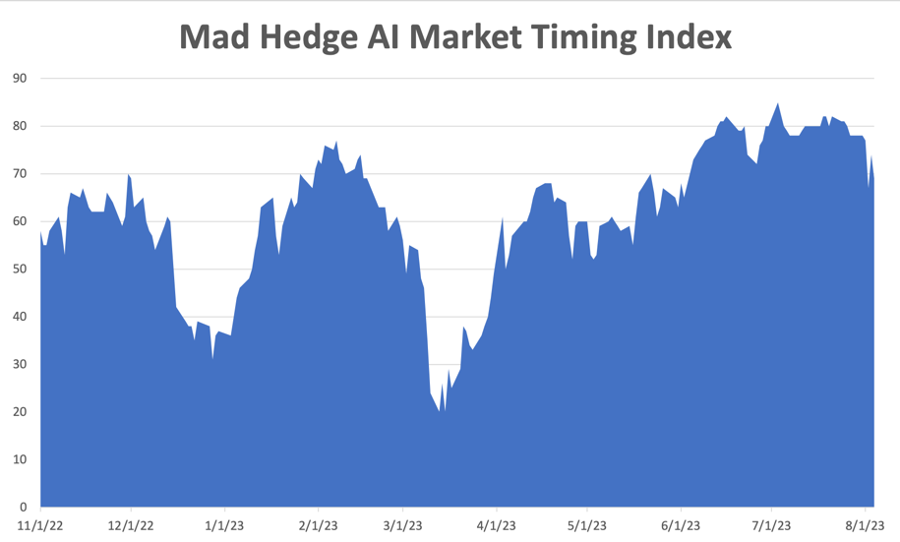

We now have the curious situation with the Mad Hedge AI Market Timing Index stock at an extremely overbought level of 80 for two months, the result of a non-stop melt-up in big technology stocks. The begging question now is how far we pull back before an explosive yearend rally ensues. That will be your last entry point for stocks in 2023.

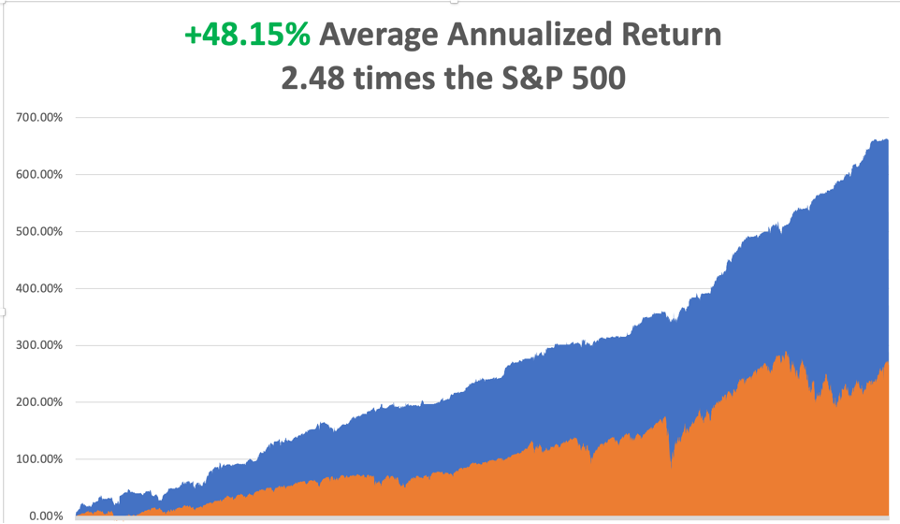

So far in August, we are down -4.70%. My 2023 year-to-date performance is still at an eye-popping +60.80%. The S&P 500 (SPY) is up +17.80% so far in 2023. My trailing one-year return reached +91.08% versus +11.46% for the S&P 500.

That brings my 15-year total return to +657.99%. My average annualized return has fallen back to +48.15%, another new high, some 2.48 times the S&P 500 over the same period.

Some 41 of my 46 trades this year have been profitable.

I really took it in the shorts stopping out of my long position in the (TLT), losing 4.00%, my second largest loss of 2023. Reversion to the mean is a bitch. Every time I break my own risk control rules, I come to regret it. I could have stopped out the day before with only a 1.73% loss. The one consolation is that I went into this correction 90% in cash. I bet the rest didn’t.

See, even old dogs can make mistakes.

The Nonfarm Payroll Drops to 187,000, a one-year low, less than expectations. The Headline Unemployment Rate returned to 3.5%, a 50-year low. The soft-landing scenario lives! That’s supposed to be impossible in the face of 5.25% interest rates. Average hourly earnings grew at a restrained 3.6% annual rate. Half of the new jobs were in health care. At the rate we are aging, that is no surprise.

JOLTS and Layoffs Drop, indicating a slight weakening in labor demand, an important Fed goal. JOLTS fell from 9.62 to 9.58 million in May, a two-year low, while layoffs dipped from 1.55 million to 1.53 million. This is despite red-hot GDP growth.

Panic Buying of Hedge Fund Shorts, drove the markets in July, with many throwing in the towel on bearish bets. This “smart money” has been chasing the market since it bottomed in October. The most extreme buying, like we saw last week, is often the sign of a short-term market top.

US Home Construction Rockets, up 0.5% in June, in an attempt to meet the insatiable demand for new homes. They can’t build them fast enough even though prices are rising fast.

US Debt Downgradedfrom AAA to AA+ by the well-known Fitch rating agency for only the second time in history. Bonds (TLT) took it on the nose. The January 6 attack on the capitol and standoff over the debt ceiling crisis were cited as the reasons. US bonds are still the safest and most liquid investment in the world when held to expiration.

Uber Announces First Ever Profit on a quarterly basis and $1 billion in free cash flow. The company has emerged as the preeminent ride-sharing company. The shares dropped 5% on a “sell the news” move on top of a double since May. Buy (UBER) on a much bigger dip.

AMD Beats Even as PC Market Slows in Q2 earnings, with revenues down 18% YOY, better than expected. H2 is expected to be hot as data center demand grows thanks to exploding AI demand.

SEC Bans Coinbase from Trading, except in Bitcoin itself. The Federal agency regards all NFTs as unregistered securities. The move is a body blow to the NFT market, which I always regarded as a scam and knocked 25% off the value of (COIN). Avoid (COIN) like Covid 3.0.

Apple Reports Earnings Decline, down 1.4% in its Q3, and expects the same in Q4. iPhone sales took a steep dive, the longest slowdown in its history and knocked 3.2% off of the Teflon stock. Weak foreign currencies also delivered a hit for the most global of companies. But revenues beat at an astonishing $81.8 billion, thanks to rising service sales. Buy (AAPL) on a bigger dip, which was up 47% so far in 2023.

Amazon Soars on Earnings Beat, nearly double Wall Street estimates as its massive bet on AI pays off big time. Aggressive cost-cutting helped. (AMZN) has laid off 100,000 in the past ear, replaced by machines. Amazon Web Services (AWS), the 800-pound gorilla in the sector, also prospered. Buy (AMZN) on dips.

Airbus Delivers an Incredible 381 Aircraft, in the first seven months of 2023 as the global plane shortage worsens. The European consortium booked 60 new orders in July alone. Buy Boeing (BA) on dips, up 105% from the October low.

Airbnb is Looking Good on the back of a massive increase in international travel. In some cities like Tokyo, you can’t even find an Airbnb rental. At a restaurant I visited in Florence last week, 100% of the customers were American, mostly from the east coast. Local regulations banning short-term rentals are also crimping supply. Buy (ABNB) on dips, already up 50% since May alone.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, August 7 at 9:00 AM EST, the Used Car Prices are out, a recent big swing factor in the inflation calculation.

On Tuesday, August 8 at 8:30 AM, the NFIB Business Optimism Index is released.

On Wednesday, August 9 at 2:30 PM, the Crude Oil Stocks are published.

On Thursday, August 10 at 8:30 AM, the Weekly Jobless Claims are announced. The Consumer Price Index for July is printed, the principal inflation indicator.

On Friday, August 11 at 2:30 PM, the Producer Price Index is published. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, one of the great shortcomings of San Francisco is that we only have a theater district with two venues and it is in the Tenderloin, the worst neighborhood in the city, an area beset with homeless, drug addicts, and prostitution.

I was walking to a parking lot after a show one evening when I passed a doorway. Three men were violently attacking a blond woman. Never one to miss a good fight, I dove in, knocking two unconscious in 15 seconds (thank you Higaona Sensei!). Unfortunately, number three jumped to my side, pulled a knife, and stabbed me.

The attacker and the woman ran off, leaving me bleeding in a doorway. I drove over the Golden Gate Bridge to Marin General Hospital, bleeding all over the front seat of my car, where they sewed me up nicely and put me on some strong drugs.

The doctor said, “You shouldn’t be doing this at your age.”

I responded that “good Samaritans are always rewarded, even if the work is its own reward.”

Fortunately, I still had my Motorola Flip Phone with me, so I called Singapore from my hospital bed for a market update. I liked what I saw and bought 100 futures contracts on Japan’s Nikkei 225. This was back in 1999 when anything you touched went straight up.

Then, I passed out.

An hour later, I woke up, called Singapore again and bought another 100 futures contracts, not remembering the earlier buy. This went on all night long.

The next morning, I was awoken by a call from my staff who excitedly told me that the overnight position sheets had just come in and I had made 40% on the day.

Was there some mistake?

Then I got a somewhat tense call from my broker. I had a margin call. I had also exceeded the exchange limits for a single contract and owned the equivalent of $200 million worth of Nikkei. I told them to sell everything I had at market and go 100% cash.

That was exactly what they wanted to hear.

That left me up 60% on the year and it was only May.

I then called all of the investors in my hedge fund. I told them the good news, that I wouldn’t be doing any more trades for the fund until I received my performance bonus the following January and was taking off on a long vacation. With a 2%/20% payout in those days, that meant I was owed 14% of the underlying assets of the fund at a very elevated valuation.

They said, "That’s great, have fun. By the way, how did you do it?"

I answered, “Great drug selection.” No questions were asked.

Then I launched on the mother of all spending sprees.

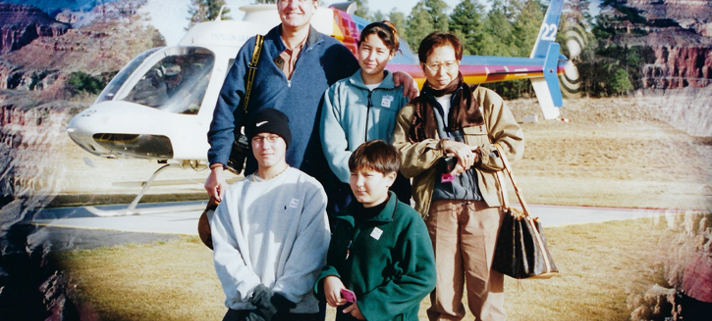

I flew to Germany and picked up a new Mercedes S600 V12 Sedan at the factory in Stuttgart for $160,000. I then immediately road-tested it on the Autobahn at 130 mph. I made it to Switzerland in only two hours. After all, my old car needed a new seat.

Next, I bought all new furniture for the entire house, each kid selecting their own unique style.

Then, I took the family to Las Vegas where we stayed in the “Rain Man Suite” at the Bellagio Hotel for $10,000 a night, where both the 1988 Rain Man and 2009 The Hangover were filmed.

I bought everyone in the family black wool Armani suits, plus a couple of Brionis for myself at $8,000 a pop. For good measure, I chartered a helicopter for a tour of the Grand Canyon the next day.

At the end of the year, I sold my hedge fund based on the incredible strength of my recent performance for an enormous premium. I then left the stock market to explore a new natural gas drilling technology I had heard about called “fracking”.

Four months later, the Dotcom Crash ensued in earnest.

I still have the scar on my right side, and it always itches just before it rains, which is now almost never. But it was worth it, every inch of it.

It’s all true, every word of it and I’ll swear to it on a stack of bibles.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/09/john-thomas-family-picture.png560712Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-08-07 09:02:512023-08-07 09:56:22The Market Outlook for the Week Ahead, or Taking It in the Shorts

(WHERE THE 10-YEAR TREASURY YIELD COULD BE HEADING AND WHY WE SHOULD CARE?)

August 4, 2023

Hello everyone,

Treasury yields rose on Thursday as investors digested fresh economic data and weighed Fitch’s U.S. downgrade from AAA to AA+ citing “fiscal deterioration” and concerns about growing general debt. The 10-year Treasury was up 11 basis points at 4.187%. The yield on the 2-year Treasury was flat at 4.887%.

What is a Treasury yield?

The Treasury yield is the annual interest rate that the U.S. government pays on one of its debt obligations, expressed as a percentage. In other words, Treasury yield is the annual return investors can expect from holding a U.S. government security with a given maturity.

Why is the 10-year Treasury yield important?

The 10-year Treasury yield indicates the overall state of the stock market and the general economy. Higher yields can indicate higher inflation expectations. It also influences many other interest rates, including mortgage interest rates, auto loans and business loans. Yields have a see-saw effect on these rates.

When the 10-year yield goes up, so do mortgage rates, and other borrowing rates. When the 10-year yield declines and mortgage rates fall, the housing market strengthens, which in turn has a positive impact on economic growth and the economy.

The 10-year Treasury yield also impacts the rate at which companies can borrow money. When the 10-year yield is high, companies will face more expensive borrowing costs that may reduce their ability to engage in the types of projects that lead to growth and innovation.

The 10-year Treasury yield can also impact the stock market, with movements in yield creating volatility. Rising yields may signal that investors are looking for higher-return investments but could also spook investors who fear that rising rates could draw capital away from the stock market.

The chart below shows possible targets on the U.S. 10-year benchmark yield.

In the short term, the latest advance in yields commenced on their 3.7268% low of July 19th. We can see that support now lies at 4.00/3.92%, with an opportunity for rally toward potential targets around the 4.36% and 4.80% levels, before exhaustion. Then we may see a medium-term pullback before another possible rally in yields.

Wishing you all a wonderful weekend.

Cheers,

Jacquie

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-08-04 20:00:412023-08-04 21:02:15August 4, 2023

Isn’t it interesting that self-driving cars and the software that launched this phenomenon are not required to pass a driving test, yet humans are?

I am here today to challenge the basic premise that software backed by artificial intelligence can drive a car better than a human.

Take left turns without a traffic light:

Artificial intelligence has consistently failed to successfully complete this standard objective.

This somewhat riskier driving maneuver must take into account drivers on the other side of the road, which humans can do, but the back-tested data in the self-driving software cannot predict external variables that could come into play.

This is why the software malfunctions on a left turn when a bird defecates on the windshield believing it’s an accident worthy of a full stop and yes a full stop right in the middle of oncoming traffic.

These types of poor decisions occur more often than you think with this “cutting-edge” technology.

The truth is that self-driving car technology has been very slow to develop.

Elon Musk has been talking about Tesla's Full Self-Driving technology for years. In 2016, the CEO said that Tesla's driver-assist feature Autopilot will be able to drive better than a human in two to three years.

He also said that by 2018, it would be possible to remotely summon a Tesla (TSLA) across the country.

In 2019, he said that Tesla could have a fleet of a million robotaxis by the end of 2020 if the company pumped out hundreds of thousands of FSD cars.

FSD is currently under investigation by the federal government in 2023.

Twenty years on from the start, no real product to show for except many unintended road deaths and rich Silicon Valley software engineers that peddle this false theory that software is better at driving than humans.

What’s the current situation today?

100% self-driving technology amounts to little more than a bunch of glorified tech demos. FSD isn’t the real deal.

In demos, you see what the creators want you to see, and they control for things that they'd rather you didn't.

To an AI, a slight change could be catastrophic. After all, how is it supposed to know what an appropriate response to a slight or sudden change is when it doesn’t understand everything it’s looking at?

How will it handle when the weather goes from sunny to hail, or when there’s deer in the headlights at the edge of the road?

It is unequivocally wrong to believe that software is better at real-time driving than a human, and therefore this industry will never mushroom into what investors think it might.

Self-driving cars are a 2-ton weapon ready to kill pedestrians, cyclists, and little kids.

The interesting thing to look for is whether these venture capitalists and investors double down on failed technology and pull strings to get this circus on public roads with the rest of us.

It’s entirely possible that this could happen in limited areas like the states of Arizona and California.

At the very minimum, if all 50 states do green-light such technology, we will need to wait another 15 or 20 years.

It’s not as imminent as Elon Musk tells us.

Don’t believe self-driving is the secret sauce that will be the next leg in revenue for Silicon Valley.

The benefits of this are not coming any time soon.

Outdoing the smartphone is proving to be almost impossible. Who would have known that the smartphone would have such staying power and longevity?

Tech is still utterly reliant on smartphone revenue until someone can supplant it and package it nicely in a consumer-friendly way. The road to that type of achievement is littered with good intentions.

ANOTHER LONG WHILE FOR SELF-DRIVING TO HIT THE MASSES

https://www.madhedgefundtrader.com/wp-content/uploads/2023/08/autodrive.png408870Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-08-04 15:02:272023-08-21 18:04:07Self-Driving Cars Are Here

“Restaurants get you in with food to sell you liquor; religions get you in with belief to sell you rules.” – Said Lebanese-American Risk Analyst Nassim Nicholas Taleb

https://www.madhedgefundtrader.com/wp-content/uploads/2022/10/taleb.png800430Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-08-04 15:00:232023-08-04 16:31:19Quote of the Day - August 4, 2023

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.