Apple (AAPL) iPhones overheat and this could mean lower quality phones in the future.

Spend the amount of an expensive laptop for a handheld device and the customer becomes bitter – that’s a pretty crappy business model.

The old Apple wouldn’t have slipped up like this – the one helmed by Steve Jobs.

Even more ironic, Apple is specifically renowned for its software expertise, but all signs point to their engineering team botching the latest iteration of the products that Steve Jobs built.

The latest black eye for the company in Cupertino is heaped onto the already large set of problems like China banning their products and declining iPhone sales.

Apart from a titanium finish, the iPhone doesn’t really give much of a reason to upgrade to the new version and why would someone go the extra mile when there is a high chance of battery heating problems.

Apple will issue a software update that would address customer complaints about the latest iPhone 15 models.

Apple said that the new iPhone models were running hot because of a combination of bugs in iOS 17, bugs in apps, and a temporary set-up period.

Apple is preparing to release a new iOS 17 update to address "a few conditions" it has "identified" that can cause the new iPhone 15 models with a titanium frame to run warmer than expected.

Days after the new iPhone release on Sept. 22, customers who stood in line at Apple stores complained their new phones were overheating to the point of being too hot to hold and even shutting down on their own, with some folks recording temperatures above 120 degrees.

The complaints are mainly about the iPhone 15 Pro and Pro Max.

The 15 Pro Max did become noticeably hot after using a MacBook Pro's 140W power adapter to charge it.

Negative press about the new iPhone could dampen sales as the company has experienced an overall year-over-year sales slump in the last three quarters.

Apple is trying to sell the iPhone 15 Pro Max (1TB storage) for as much as a high-end laptop, around $1,600 (before taxes).

Apple’s new high-end models, the $999 iPhone 15 Pro and $1,199 iPhone 15 Pro Max have a redesigned titanium enclosure with an aluminum frame to make them easier to repair.

Apple’s problems with their new iPhones epitomize the current state of tech companies.

Many firms like Google, Facebook, and so on try to sell the same product with no noticeable upgrades.

The bulk of people won’t see much difference between using an iPhone 14 and iPhone 15.

Tim Cook was never a visionary and now that iPhones are declining, his response appears to double down as an expert operations specialist.

This won’t cut it when the company needs more spice.

Running the company more efficiently and streamlined won’t solve the issue of the flagship products losing sales.

A transformative shift in the management is needed to reimagine what the future could be something more akin to his predecessor Steve Jobs.

Many years on, Cook is still living off of Steve’s ideas, but the issue now is the diminishing returns is now resulting in negative growth.

The diminishing returns happen because Cook is holding onto ideas that have grown stale.

That never happened before and shareholders hate it.

In fact, Apple has been previously lauded for its aggressive creativity, and by and large, that has vanished from their current staff.

Apple needs a kick in the butt and it’s highly possible that all the great talent that used to be in Apple has been chased out because the company became too comfortable and too corporate.

Thursday wasn’t a great day for technology stocks ($COMPQ).

It’s not always smooth sailing from the bottom left to the top right.

It never is.

Stocks like Amazon (AMZN) were down more than 4% and other lower-tier growth stocks were down a lot more.

The price action in tech was a knee-jerk reaction after Fed Chair Jerome Powell signaled “higher for longer” for US interest rates ($TNX).

Powell was slightly a little bit more hawkish than consensus had it, and I don’t believe that will have any weight in the short or long term.

Funnily enough, Fed Futures are still pricing in no interest rate hike at the next meeting, even though Powell said there is one more hike.

There is still a deep-seated psychology that the Fed will pivot and this concept that the Fed has our back is not going away with itty bitty hikes.

Is there much of a difference between 5.25% and 5.5%?

The answer is no.

I would say that Powell's slow-walking this whole rate situation has done a lot more damage than good.

In more than 3 years since inflation was supposed to be transitory, inflation is still stuck at 3.7%.

Imagine living in a house with severe water damage to the wall and allowing it to fester over 3 years.

Tech continues to do well relative to expectations because Powell’s minuscule rate hikes have been sanitized to the investor audience.

Investors are scared of uncertainty and Powell is full of certainty.

Investors also don’t believe Powell will do anything to scare the tech market as we approach a federal government shutdown yet again.

Powell keeps pedaling this version of economic success, possibly because it is an election year.

Talking up tech stocks isn’t bad and Powell said that a soft landing is not the Fed's baseline expectation; it's merely a "plausible outcome."

Ultimately, tech investors believe Powell will pivot.

The proof is in the pudding.

Let’s look at the short and long end of the treasury curve.

The 10-year US treasury is yielding 4.43% and the 30-year US treasury bond is yielding 4.53%.

This means for an extra 20 years of duration, investors are rewarded an extra measly .10% worth of juice, precisely because investors think Powell will drop the front end of the curve like a hot potato.

Investors are just waiting it out.

Thus, Powell has telegraphed that we are basically at the peak of rates which is highly bullish for tech stocks.

Tech stocks are down just slightly in the past 30 days which I would characterize as a massive victory in relative terms.

In normal financial times, tech stocks would be thrown out with the bath water and we haven’t seen that happen.

Any selloff has been pristinely orderly and that’s a bullish sign in the short-term.

I am not saying that tech stocks have unlimited upside, but I do believe there is a solid bottom under them and they will most likely bounce around in a range-bound fashion.

Remember that for most of this year stocks like Apple (AAPL), Nvidia (NVDA), Meta (META), and so on rose while treasury yields spiked.

I don’t see why this correlation will screech to an immediate stop.

The likely bet is it continues but at a slower pace.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-09-22 15:02:572023-09-22 18:14:27The New Correction is the Sideways One

Global Market Comments

September 20, 2023 Fiat Lux

Featured Trade:

(FRIDAY, OCTOBER 31 MIAMI, FLORIDA GLOBAL STRATEGY LUNCHEON)

(WHY I HAVE BECOME SO BORING),

(SPY), (QQQ), (IWM), (AAPL), (TSLA),

(TACKLING THE INFLATION MYTH),

(AAPL), (GOOG), (FB)

I have recently received a few complaints from readers that I have become boring. I have to confess that they are right.

I am not a person who boredom comes to easily. I’m the guy who climbed the Matterhorn, crossed the Sahara Desert on the back of a camel, and went to surfing school.

And that’s just what I did last year! Oh, and I’m also headed for the world’s hottest combat zone.

However, I do admit that I have become boring on the trading front.

If I get a request for one thing more than any other, it is for recommendations of stocks that will rise by at least ten times over the next ten years.

Readers want to know the names of shares of companies that they can just buy and forget about, and then retire rich as Croesus a decade down the road.

What could be more reasonable?

I happen to have sent out quite a few of these over the years.

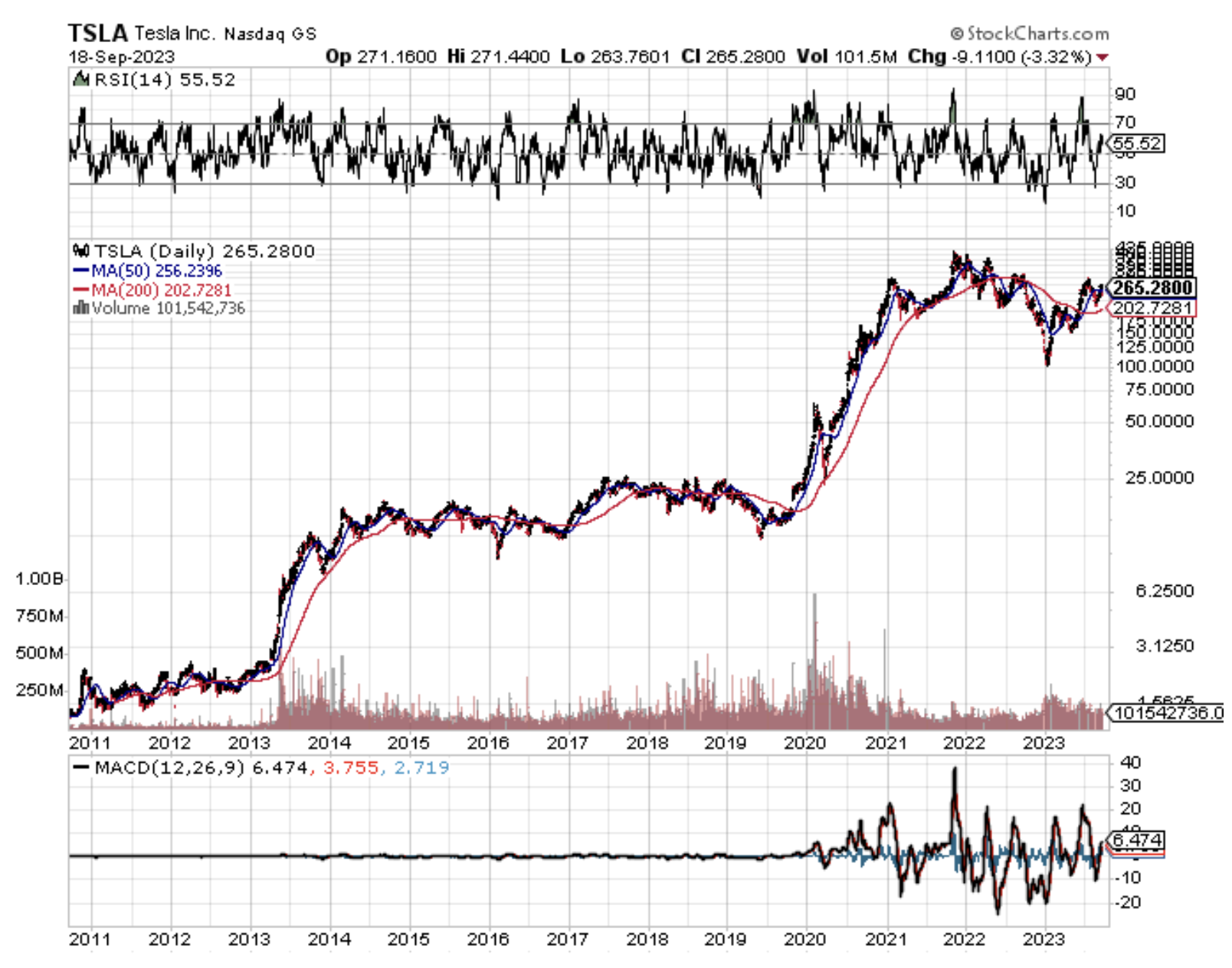

Whenever I attend my global strategy luncheons around the world, someone inevitably thanks me for my effort to cajole them into buying Tesla (TSLA) at a split-adjusted $2.50. Nothing seemed more questionable at the time (2010) in the wake of the Great Recession and financial crisis.

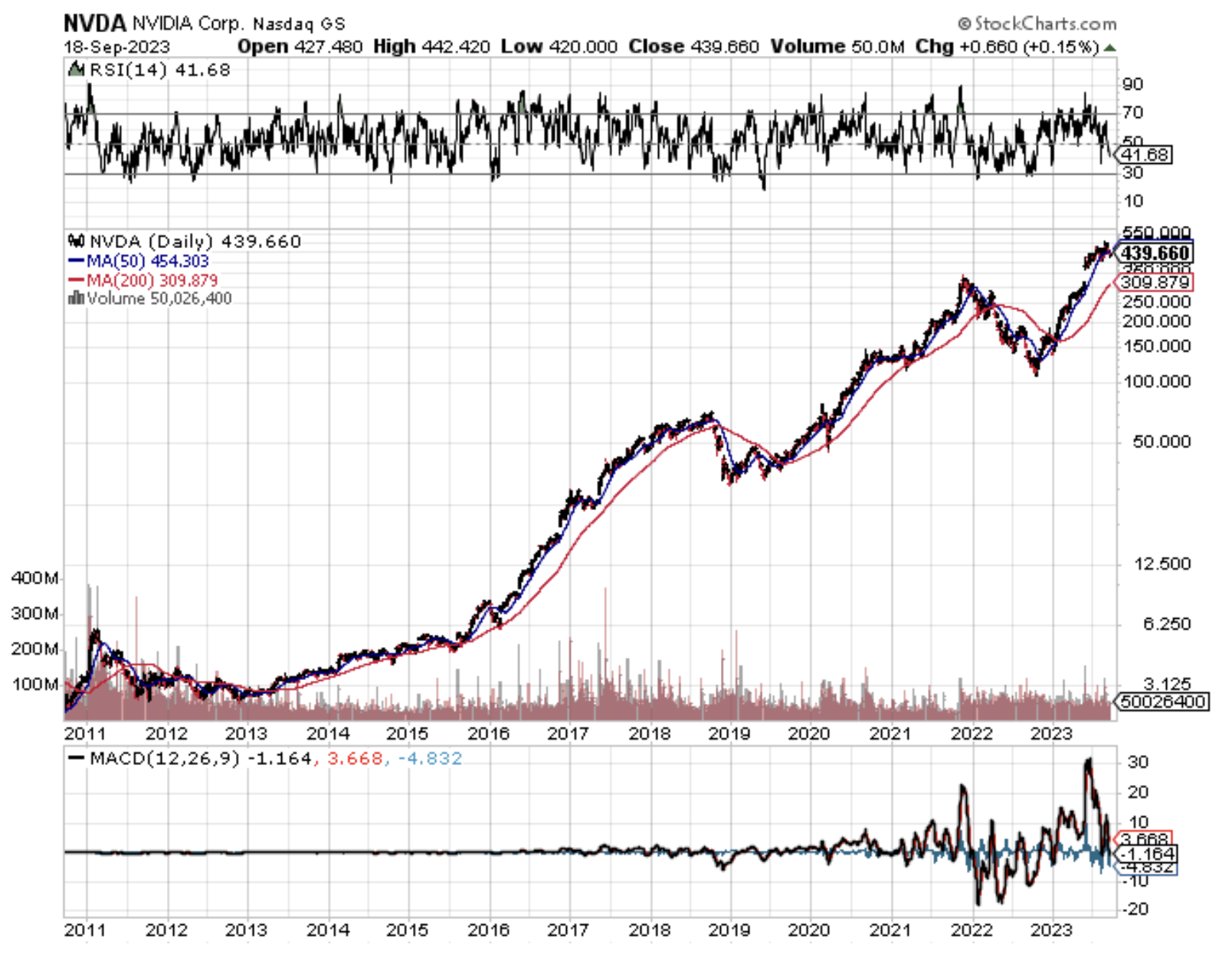

At my New York luncheon in June, a guest pressed a one-ounce American Gold Eagle into my hand and said thanks for NVIDIA (NVDA). He bought it at $15 and rode it all the way up to $450.

He then doubled his money by jumping into Apple (AAPL) at $56 (on a split-adjusted basis) and rode the express train to $200, again after my pleading.

Then there was the reader who offered me his mega yacht in the Mediterranean for a week for free because I virtually forced him to buy Moderna (MRNA) just before the pandemic before it rocketed 50X. It was nice cruising the Mediterranean last summer on his advice.

It’s not that I have suddenly become averse to dishing out ten-baggers. I have not grown weary in my old age either, although I confess to finding those erectile dysfunction and baldness ads on TV more fascinating by the month.

No, the real problem is that the stock markets are just not offering anything right now. And here is where I give you some great trading tips.

When stock markets are rising and financial assets are generally in “RISK ON” mode, you want to own single stocks.

Individual shares have “betas”, or a propensity to move, that is far greater than indexes. If an index rises 10%, some of its individual components can move anywhere from 15%-100%.

When stock markets are in correction (down) or consolidation (sideways) mode, as we are now, the higher betas of stocks work against you. They fall faster than the index.

Therefore, in flat and falling markets you want to trade indexes, like the S&P 500 big cap index (SPY), the NASDAQ technology index (QQQ), and the Russell 2000 small cap index (IWM). Better yet, don’t execute any trades at all, especially if you are already up 60% on the year.

Keep your powder dry. A dollar at a market bottom is worth $10 at a market top.

Your mistakes trading these relatively nonvolatile (read boring) instruments earn you less money. The risk/reward for short-term trading right now is terrible.

Therefore, by trading stocks in up markets and indexes only in down markets, you create an inbuilt bias in your portfolio that works in your favor.

A classic example of how this works was to see the market reactions to corporate earnings announcements in July. In these risk-averse times, winners were rewarded modestly, but losers were taken out to the woodshed and beaten senseless.

Look at the recent charts for Apple (AAPL), Tesla (TSLA), and Disney (DIS) and you’ll see what I mean. I bet the owners of these companies wish they had been trading indexes in August, which barely moved. Is 3% the new 10% correction?

These are all fundamentally great companies for the long term. But when people run for cash, they will often sell whatever has the most profit, and all three of these names met that standard. Investors were, in effect, raiding the piggy bank.

Of course, you can try and be clever and go long stocks in rising markets, and then sell them short in falling ones.

My half-century of experience tells me that this is easier said than done.

While many managers will promise you this bit of investing in gymnastics, very few can actually deliver. Most professionals are unable to time markets with this precision, let alone individuals.

Needless to say, don’t try this at home.

What? Me Boring?

https://www.madhedgefundtrader.com/wp-content/uploads/2015/07/John-Thomas1-e1436361891975.jpg389400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-09-20 09:04:372023-09-20 16:18:39Why I Have Become So Boring

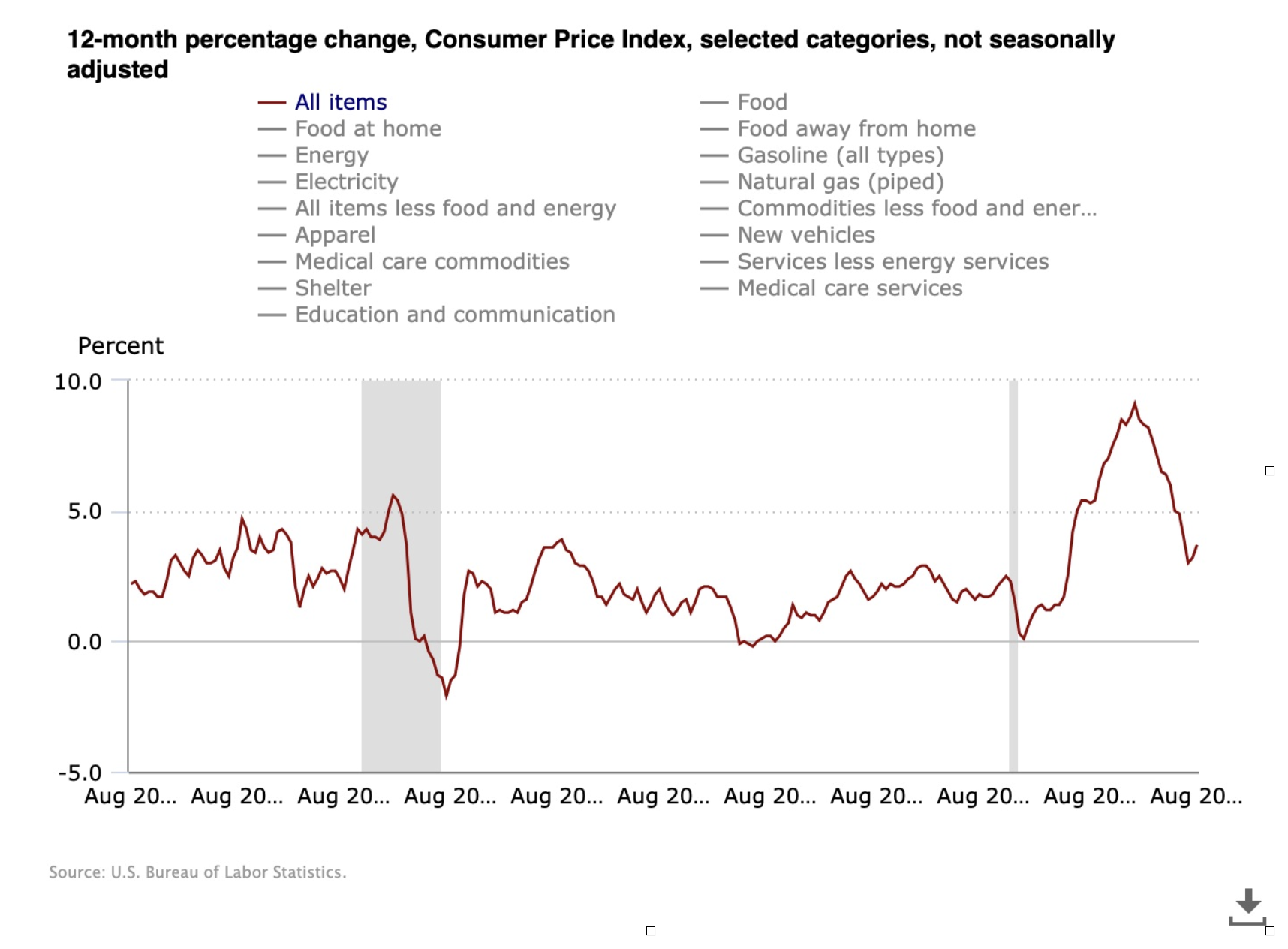

I have long told my listeners at conferences, webinars, and strategy luncheons my definition of the “new inflation”: the price for whatever you have to buy is rising, as with your home, health care, and a college education.

The price of the things you need to sell, such as your labor and services, is falling.

So while official government numbers show that the overall rate of inflation is muted at multigenerational highs, the reality is that the standard of living of most Americans is being squeezed at an alarming rate by both startling price increases and real wage cuts.

I finally found someone who agrees with me.

David Stockman was president Ronald Reagan’s director of the Office of Management and Budget from 1981-1985. I regularly jousted with David at White House press conferences, pointing out that the budgets he was proposing would not produce a balanced budget, as he claimed.

Instead, I argued that they would lead to an enormous expansion of the federal deficit. In the end, I was right, with the national debt growing 400% during the Reagan years.

To his credit, David later admitted to running two sets of books for the national accounts, one for external consumption for people like me, and a second internal one for the president with much more dire consequences.

When David finally made the second set of books public, there was hell to pay. It was a fiery departure. I knew Ronald Reagan really well, and when the cameras weren’t rolling, he could get really angry.

After a falling out with Reagan over exactly the issues I brought up, Stockman disappeared for three decades.

He is now back with a vengeance.

He is running a blog named David Stockman’s Contra Corner (click here for the link at http://davidstockmanscontracorner.com ), a site he says “where mainstream delusions and cant about the Welfare State, the Bailout State, Bubble Finance, and Beltway Banditry are ripped, refuted and rebuked.” (Good writing was never his thing).

Despite this rant, there is no place I won’t go to discover some valid arguments and useful statistics, and Stockman is no exception.

For a start, home utility prices have been skyrocketing for the past decade, nearly doubling. Over the last 12 months alone, it has jumped by 5.3%, while natural gas is up more than 10%, compared to an annual Consumer Price Index rise of only 3.3%.

But utilities have such a low 5% weighting in the Fed’s inflation calculation it barely moves the needle.

Wait, it gets better.

Gasoline costs have also been on a relentless uptrend since the nineties. Crude oil is up from a $10 low to today’s print of $95. Retail gasoline has popped from $1 a gallon to $5.50 in California, and that’s off from the year’s high at $3.50.

That works out to an annualized increase of 57%, or more than triple the official inflation rate.

The nation’s 40 million renting households have been similarly punished with price increases. They have averaged a 5.0% annual rate, nearly double the inflation rate.

The country’s 75 million homeowners are getting hit in the pocketbook as well. They have seen the cost of water, sewer, and trash collection balloon at a 4.8% annualized rate. And this has been an almost entirely straight-line move, with no pullbacks. And home insurance? It is absolutely through the roof.

David recites a dirty laundry list of Fed omissions and understatements on the inflation front, including gold, silver, and commodities prices.

All of these nickels and dimes add up to quite a lot for a family of four who is trying to scrape by on a median household income of $69,000 a year. And Heaven help you if you try to live on that in California.

The cost of a few items has declined, but not by much. They are largely composed of cheap import substitutes from Asia, including apparel, shoes, household furniture, consumer electronics, toys, and appliances.

One area the Fed data doesn’t remotely come close to measuring is the plunging cost of technology. How do you measure the savings from products that didn’t exist 20 years ago, like smart phones, iPods, iPads, and solid-state hard drives? How do you measure the cost of services that are handed out for free as Google, Facebook, and X do?

I can personally tell the cost of my own business is probably 90% cheaper to run than it would have three decades ago. I remember shelling out $5,000 for a COMPAQ PC that costs $300 today but has 1,000 times the performance.

David finishes withhis usual tirade against the Fed, accusing them of obsessing over the noise of the daily data releases and missing the long-term trend.

Anyone like myself who watched in horror how long it took our central bank to recognize the seriousness of the 2008 financial crisis pr the pandemic would agree.

This all reminds me of what a college Economics professor once told me during the late 1960’s. “Statistics are like a bikini bathing suit. What they reveal is fascinating, but what they conceal is essential.”

What They Reveal is Fascinating....

https://www.madhedgefundtrader.com/wp-content/uploads/2015/08/Bikini-Clad-Girl.jpg410316Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-09-20 09:02:032023-09-20 16:22:14Tackling the Low Inflation Myth

I wouldn’t say that the IPO market is back - hardly not.

There is still a long way to go before the floodgates open, but the ARM IPO is a good start and its successful debut is a good example for others that are sitting off the fence.

British chipmaker Arm (ARM) debuted on the public markets jumping 25% in trading.

The chipmaker's go-public is the most high-profile IPO that the Nasdaq has seen since 2021's IPO boom, which cycled into a bust in 2022.

However, just because these IPOs are moving doesn't mean their valuations are not a sticking point. In Arm's case, the company reportedly sought a valuation of between $60 billion and $70 billion.

Likewise, Instacart — valued at $39 billion at the close of its 2021 funding round — is reportedly now seeking a $9.3 billion valuation.

Arm is a unique company, especially among tech companies. As a chip designer, Arm's customers include some of the biggest names in tech, including Apple (AAPL).

The company has been through a number of transitions over the last several years. In 2016, SoftBank acquired Arm, taking it private for around $30 billion. In 2021, Nvidia (NVDA) attempted to acquire Arm in a deal that failed after regulatory tussling for almost a year and a half.

Recently, Arm has sought to shift its revenue model, altering pricing and rolling out a changed customer licensing strategy.

In short, Arm's return to the public markets was a pivotal moment.

The positive response to this IPO won’t thaw the IPO market completely but will set the stage for 2024 such as payment processor Stripe and computer software provider Databricks.

I will say that the bar has risen significantly for tech firms who want to go public.

Before, many could go public with just hope and dreams with promises of a pot of gold at the end of the rainbow.

This usually meant paltry revenue and massive cash burn at the time of IPO.

Moving forward, it’s obvious that tech companies will need to be more mature to go public and there will be more emphasis on quality management than any time before.

This is because interest rates are still highly elevated and management teams won’t be able to tap the debt markets so easily for a bailout.

Artificial intelligence-related IPOs will also be in an advantageous position to do well post-IPO because that is where the hot money is targeting.

Instead of a slew of capital chasing the new IPOs, I do believe we default back into a rotation of big tech being the safety trade.

Higher bond yield and accelerating tech stocks is an odd couple that appears to be working like clockwork in 2023.

The next spike up in yield could happen soon with the catalyst being the price of a barrel of oil hitting that $100 per barrel mark.

As for ARM, it’s sitting at $56 per share which is down from the $65 per share.

Once the euphoria subsides, wait for a dip in the $40s to buy into ARM, at that price, ARM would be valued at around $50 billion and I would call that a steal for the long-term buy-and-hold readers.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-09-18 16:02:162023-09-18 17:14:55Will the Tech IPO Market Thaw?

For here it is September, and the stock market is behaving like it is only July. July was different from normal as well, going straight up almost every day when it is usually asleep. This year, July acted like May, when you’re supposed to sell and go away.

If you’re thoroughly confused by all of this, so am I. The historic cyclicality of the markets, the ebb and flow of share prices according to the calendar, has gone out the window. But then, what isn’t confusing these days?

I went to buy a green drink from Whole Foods on Friday and the counter was closed because of staff shortages. Whole Foods unable to sell a green drink?

I tried to climb the Matterhorn this summer but was told that the guides weren’t taking anyone up because of the extreme heat. The mountain was literally melting, dropping rocks on the heads of climbers. No climbing the Matterhorn in Switzerland? I went to the Dolomites instead where you climb ice-free shear rock faces.

I tried to get into the Pantheon in Rome this summer and was met with a five-hour line. The Sistine Chapel in the Vatican was worse. When I first went there in the 1960’s the place was empty. The fact is that Italy now has more tourists than Italians. Oh, and the pope is from Argentina.

Has the world gone mad?

What has happened is that there has been a great pull forward that took place in financial markets during the first half of the year. I’ve seen this before. When a conclusion becomes obvious, everyone jumps on the bandwagon and brings everything forward.

So from January to July stock markets saw the blatantly obvious future that inflation would fall, interest rates decline, the US dollar weaken, and commodities and precious metals would rise. That’s why the “Magnificent Seven” led.

What happens next?

Now shares have to wait until these predictions actually happen before they can move any further. Markets have moved as far as they can on faith alone. Next, we need facts. This could take weeks or even months.

I knew this was going to happen. That’s why I went pedal to the metal, full speed ahead, damn the torpedoes aggressive during the first half of the year and clocked a 60% profit. I expected that if you didn’t make a profit in the first half of the year, you wouldn’t have any profits in 2023 at all.

And the trade alert drought continues.

There isn’t a day that goes by when I am not asked if America’s $33 trillion national debt will destroy the economy, cause the stock market to crash, and bring the end of Western Civilization. The answer is no, never, not in our lifetimes.

The reason is very simple. Any dollar the government borrows today sees its purchasing power go to zero in 30 years. That’s where the massive Civil War debt went, that's where the WWI debt went, and that’s where the gigantic WWII debt went, some 105% of GDP. Today’s debt will similarly vaporize over time.

Who pays for this cataclysmic decline in value? US government debt holders, who similarly see their purchasing power disappear over time. It turns out that the ultimate avoiders of risk, investors in US government debt, not only don’t get paid for their cowardice, they lose their entire principal as well, at least in terms of purchasing power.

There is a wonderful article in Barron’s this week entitled “Government Debt Needs to Be Repaid, And Other Myths About the Federal Deficit” by Paul Sheard which explains how all this works, which I quote below in its entirety.

“The U.S. national debt currently stands at $32.91 trillion, and 10 months into this fiscal year, the U.S. government has spent $1.6 trillion more than it has collected in revenue. Those intimidating figures animate political battles that can shut down the government and even bring it to the brink of default. But the meaning of this money isn’t as simple as it seems. Five myths in particular deserve straightening out.

The first is that the government has to borrow in order to spend and run deficits. It’s the other way around. The government creates money (injects it into the economy) when it spends and destroys money (withdraws it from the economy) when it taxes. The government taxes variously to correct for negative externalities, to redistribute income, and to modulate aggregate demand; “raising revenue” is just a cover story.

A related myth is that the government needs to repay its debt. “Debt” is a misnomer; government debt is just money (or purchasing power) in another form. A $20 bill is a liability of the Fed, which makes it a liability of the federal government. A $20 bill never has to be repaid; it just is. Fundamentally, Treasuries aren’t much different.

That government debt never needs to be repaid doesn’t mean the government can or should create as much of it as it likes.

Too big a pile of debt because of prior and ongoing budget deficits may be inflationary, as too much money chases insufficient goods and services. That will require some combination of monetary and fiscal tightening. A mountain of debt may indicate a government that is too big and intrusive in the economy for many people’s liking, an issue that can be fought out at the ballot box.

A third myth is that the Fed prints money when it does quantitative easing. The money-printing happens when the government runs a budget deficit; QE just changes the form of that money.

QE is really just a debt refinancing operation of the consolidated government—that is, the government including the Fed—whereby it refinances one form of debt (government bonds or guarantees) into another (reserves). QE changes the composition of the (consolidated) government debt in the hands of the private sector, but it doesn’t directly add one iota of new purchasing power. For every dollar the Fed “pumps into” the economy by doing QE, it “sucks out” a dollar of assets. Conversely, quantitative tightening just returns assets to private sector portfolios, expunging reserves in the process.

Reserves are like banknotes: The Fed can withdraw them, but it never has to repay them as such. It looks like the government has to repay Treasuries, but this is an institutional artifact. In extremis, the Fed could convert all outstanding Treasuries into reserves, and it could maintain monetary control by it, rather than the fiscal authorities, paying interest on reserves.

Japan is the poster child for a miserable-looking fiscal picture. Yet, the Bank of Japan, the pioneer of QE, owns almost half of the stock of outstanding Japanese government securities and, at the same time, since 2016 has managed the 10-year yield, with some leeway, to be “around zero percent.”

It is precisely because the government can create money at will that the modern monetary and fiscal architecture has been designed to put shackles on its ability to do so: The creation of an “independent” central bank withinthe government, the central bank not allowing the government’s account with it to go into overdraft, the central bank not buying bonds directly from the government, and governments issuing debt securities rather than leaving their deficits in the form of reserves all serve that purpose. But what the government taketh away, it can give back. Faced with the need, it could loosen those shackles.

A fourth, and related, myth is that banks could, if so moved, “lend out” the excess reserves created by QE. Banks can lend these reserves to one another but they cannot turn them into lending to companies and households in the broader economy.

It isn’t just the government that creates money. Banks do, too. A fifth myth is that banks are just financial intermediaries “taking in” deposits and “lending them out.” Not so. Banks create money when they lend. For an individual bank making a new loan, it may not feel like this, because the first thing borrowers do is spend their money. If none of that money flows back into the same bank, its reserves at the central bank will decline by the amount of the loan. It will then probably want to attract deposits to “fund” the loan, but doing so will just top up its lost reserves. Bank lending for the system is entirely self-funding (so long as none of the money created leaks into bank notes).

The U.S. economy currently produces about $27 trillion of goods and services annually, a little more than the amount of federal debt held by the public and the QE-embracing Fed. The money needed to sustain this giant prosperity-generating machine comes from the government running deficits and from banks extending credit, with the Fed’s activities linking the two. Political debates and decisions currently are based on a befuddled grasp of how this monetary system works. The stakes for society are too high for that.”

So far in August, we are down -4.70%. My 2023 year-to-date performance is still at an eye-popping +60.80%. The S&P 500 (SPY) is up +17.10% so far in 2023. My trailing one-year return reached +92.45% versus +8.45% for the S&P 500.

That brings my 15-year total return to +657.99%. My average annualized return has fallen back to +48.15%, another new high, some 2.50 times the S&P 500 over the same period.

Some 41 of my 46 trades this year have been profitable.

Beige Book Shows Consumer Spending Slowing, long a pillar of this recovery, as the last of the pandemic bonuses work their way for the system. It’s putting a dent in corporate profits and hints at a shrinking economy, contrary to recent economic data.

The US Dollar (UUP) is Soaring, thanks to “higher interest rates for longer” and a strengthening US economy. Asian currencies are at ten-month lows and central bank intervention is looking. The dollar shorting selling opportunity of the decade is setting up.

China Restricts Sales of iPhones (AAPL), barring sales to government agencies. It’s only a small nick in overall sales, but certainly casts of cloud over doing business in the Middle Kingdom. Some $200 billion, (AAPL)’s market cap has been vaporized.

Weekly Jobless Claims Dive, down 13,000 to 216,000, a seven-month low. It’s the fourth consecutive decline and not what the Fed wanted to hear.

Rate Hikes Will Drag on the Economy for at Least a Decade, as the Fed's $8.24 trillion balance sheet unwinds, according to the San Francisco Fed. The balance sheet was only at $800 million before the 2008 Great Recession.

Saudi Arabia and Russia Engineer Short Squeeze on Oil (USO), taking the price over $90 a barrel this year. Large production cuts announced in June will be maintained until yearend. Will Biden counter with a release from the Strategic Petroleum Reserve, or SPR?

Tesla’s Chinese EV Deliveries Rise 9.3% in August, thanks to aggressive price cuts. There is a two-month wait for the Model Y. Chinese rival BYD (BYD), with its Dynasty and Ocean series of EVs and petrol-electric hybrid models, recorded deliveries of 274,086 passenger vehicles in August, a jump of 57.5% year-on-year. China has the world’s largest car market.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, September 11, US Consumer Inflation Expectations are announced.

On Tuesday, September 12 at 8:30 PM EST, NFIB Business Optimism Index is released. Apple announced the new iPhone 15.

On Wednesday, September 13 at 8:30 AM, the Core Inflation Rate for August is published.

On Thursday, September 14 at 8:30 AM, the Weekly Jobless Claims are announced. ARM started trading after its IPO, which was five times oversubscribed. NVIDIA tried but failed to take over the chip maker.

On Friday, September 15 at 2:30 PM, the Producer Price Index for August is published. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, not just anybody is allowed to fly an aircraft in Hawaii. You have to undergo special training and obtain a license endorsement to cope with the Aloha State’s many aviation challenges.

You must learn how to fly around an erupting volcano, as it can swing your compass by 30 degrees. You must master the fine art of not getting hit by a wave on takeoff since it will bend your wingtips forward. And you’re not allowed to harass pods of migrating humpback whales at a low level, a sight I will never forget.

Traveling interisland can be highly embarrassing when pronouncing reporting points that have 16 vowels. And better make sure your navigation is good. Once a plane ditched interisland and the crew was found six months later off the coast of Australia. Many are never heard from again.

And when landing on the Navy base at Ford Island you were told to do so lightly, as they still hadn’t found all the bombs the Japanese had dropped during their Pearl Harbor attack in 1941.

You are also informed that there is one airfield on the north shore of Molokai you can never land at unless you have the written permission from the Hawaii Department of Public Health. I asked why and was told that it was the last leper colony operating in the United States.

My interest piqued, the next day found me at the Hawaiian state agency with an application in hand. I still carried my UCLA ID which described me as a DNA researcher, which did the trick.

When I read my flight clearance to the controller at Honolulu International Airport, he blanched, asking if I had authorization because he’d never seen one before. I answered that yes, I did, I really was headed to the dreaded Kalaupapa Airport, the Airport of no Return.

Getting into Kalaupapa is no mean feat. You have to follow the north coast of Molokai, a 3,000-foot-high series of vertical cliffs punctuated by spectacular waterfalls. Then you have to cut your engine and dive for the runway in order to land into the wind. You can only do this on clear days, as the airport has no navigational aids. The crosswind is horrific.

If you don’t have a plane it is a 20-mile hike down a slippery trail to get into the leper colony. It wasn’t always so easy.

During the 19th century, Hawaiians were terrified of leprosy, believing it caused the horrifying loss of appendages, like fingers, toes, and noses, leaving bloody open wounds. So, King Kamehameha I exiled lepers to Kalaupapa, the most isolated place in the Pacific.

Sailing ships were too scared to dock. They simply threw their passengers overboard and forced them to swim for it. Once on the beach, they were beaten a clubbed for their possessions. Many starved.

Leprosy was once thought to be a result of sinfulness or infidelity. In 1873, Dr. Gerhard Henrik Armauer Hansen of Norway was the first person to identify the germ that causes leprosy, the Mycobacterium leprae.

Thereafter, it became known as Hanson’s Disease. A multidrug treatment that arrested the disease, but never cured it, did not become available until 1981.

Leprosy doesn’t actually cause appendages to drop off as once feared. Instead, it deadens the nerves, and then rats eat the fingers, toes, and noses of the sufferers when they are sleeping. It can only be contracted through eating or drinking live bacteria.

When I taxied to the modest one-hut airport, I noticed a huge sign warning “Closed by the Department of Health.” As they so rarely get visitors the mayor came out to greet me. I shook his hand but there was nothing there. He was missing three fingers.

He looked at me, smiled, and asked, “How did you know?”

I answered, “I studied it in college.” Even today, most are terrified of shaking hands with lepers.

Not me.

He then proceeded to give me a personal tour of the colony. The first thing you notice is that there are cemeteries everywhere filled with thousands of wooden crosses. Death is the town’s main industry.

There are no jobs. Everyone lives on food stamps. A boat comes once from Oahu a week to resupply the commissary. The government stopped sending new lepers to the colony in 1969 and is just waiting for the existing population to die off before they close it down.

Needless to say, it is one of the most beautiful places on the planet.

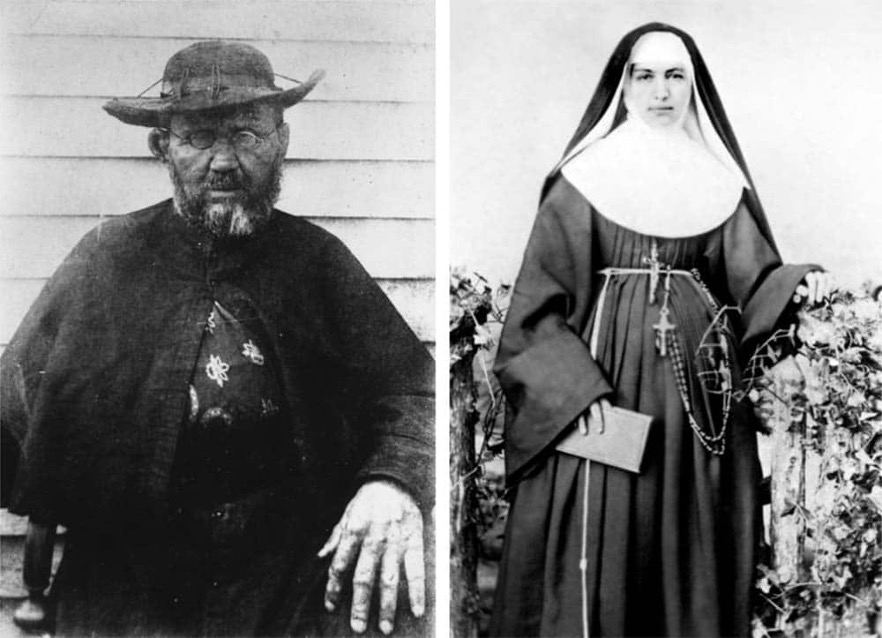

The highlight of the day was a stop at Father Damien’s church, the 19th century Belgian catholic missionary who came to care for the lepers. He stayed until the disease claimed him and was later sainted. My late friend Robin Williams made a movie about him, but it was never released to the public.

The mayor invited me to stay for lunch, but I said I would pass. I had to take off from Kalaupapa before the winds shifted.

It was an experience I will never forget.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Airport of No Return

Father Damien

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-09-11 09:02:122023-09-11 16:04:06The Market Outlook for the Week Ahead, or The Big Pull Forward

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.