Mad Hedge Technology Letter

December 20, 2019

Fiat Lux

Featured Trade:

(THE BIG TECH TRENDS OF 2020)

(AAPL), (GOOGL), (FB), (AMZN), (NFLX)

Mad Hedge Technology Letter

December 20, 2019

Fiat Lux

Featured Trade:

(THE BIG TECH TRENDS OF 2020)

(AAPL), (GOOGL), (FB), (AMZN), (NFLX)

The year is almost in the rear-view mirror – I’ll make a few meaningful predictions for technology in 2020.

Although iPhones won’t go obsolete in 2020, next year is shaping up as another force multiplier in the world of technology.

Or is it?

A trope that I would like to tap on is the severe shortage of innovation going on in most corners of Silicon Valley.

Many of the incumbents are busy milking the current status quo for what it’s worth instead of targeting the next big development.

Your home screen will still look the same and you will still use the 25 most popular apps

This almost definitely means the interface that we access as a point of contact will most likely be unchanged from 2019.

It will be almost impossible for outside apps to break into the top 25 app rankings and this is why the notorious “first-mover advantage” has legs.

The likes of Google search, Gmail, Instagram, Uber, Amazon, Netflix and the original list of tech disruptors will become even more entrenched, barring the single inclusion of Chinese short-form video app TikTok.

The FANGs are just too good at acquiring, cloning or bludgeoning upstart competitors.

It’s the worst time to be a consumer software company that hasn’t made it yet.

Advertising will find itself migrating to smart speakers

Amazon and Google have blazed a trail in the smart speaker market but ultimately, what’s the point of these devices in homes?

Exaggerated discounting means hardware profits have been sacrificed, and the lack of paid services means that they aren’t pocketing a juicy 30% cut of revenue either.

These companies might come to the conclusion that the only way to move the needle on smart speaker revenue is to infuse a major dose of audio ads to the user.

So if you are sick to your stomach of digital ads like I am, you might consider dumping your smart speaker before you are forced to sit through boring ads.

Amazon’s Alexa will lose momentum

In a way to triple down on Alexa, Amazon has installed it into everything, and this is alienating a broad swath of customers.

Not everyone is on the Amazon Alexa bandwagon, and some would like Amazon’s best in class products and services without involving a voice assistant.

Privacy suspicion has gone through the roof and smart speakers like Alexa could get caught up in the personal data malaise dampening demand to buy one.

Your voice is yours and 2020 could be the first stage of a full onslaught of cyber-attacks on audio data.

Don’t let hackers steal your oral secrets!

Cyber Warfare and AI

Hackers have long been experimenting with automatic tools for breaking into and exploiting corporate and government networks, and AI is about to supercharge this trend.

If you don’t know about deep fakes, then that is another thorny issue that could turn into an existential threat to the internet.

Not only could 2020 be the year of the cloud, but it could turn into the year of cloud security.

That is how bad things could get.

A survey conducted by Cyber Security Hub showed 85% of executives view the weaponization of AI as the largest cybersecurity threat.

On the other side of the coin, these same companies will need to use AI to defend themselves as fears of data breaches grow.

AI tools can be used to detect fraud such as business email compromise, in which companies are sent multiple invoices for the same work or workers duped into releasing financial information.

As AI defenses protect themselves, the sophistication of AI attacks grows.

It really is an arms race at this point with governments and private business having skin in the game.

Facebook gets out of the hardware game because consumers don’t trust them

Remember Facebook Portal – it’s a copy of the Amazon Echo Show.

The only motive to build this was to bring it to market and expect Facebook users to adopt it which backfired.

Facebook will find it difficult convincing users to use more than Facebook and Instagram software apps.

Don’t wait on Facebook to roll out some other ridiculous contraption aimed at stealing more of your data because there probably won’t be another one.

This again goes back to the lack of innovation permeating around Silicon Valley, Facebook’s only new ideas is to copy other products or try to financially destroy them.

China continues to out-innovate Silicon Valley.

The rise of short-form video app TikTok is cementing a perception of China as the home of modern tech innovation, partly because Silicon Valley has become stale and stagnated.

China has also bolted ahead in 5G technology, fintech payment technology, unmanned aerial vehicle (UAV) and is giving America a run for their money in AI.

China’s semiconductor industry is rapidly catching up to the US after billions of government subsidies pouring into the sector.

Silicon Valley needs to decide whether they want to live in a tech world dominated by Chinese rules or not.

Augmented Reality: Is this finally the real deal?

Augmented reality (AR) is still mainly used for games but could develop some meaningful applications in 2020.

Virtual Reality (VR) and AR will play a big role in sectors such as education, navigation systems, advertising and communication, but the hype hasn’t caught up with reality.

One use case is training programs that companies use to prepare new workers.

However, AR applications aren't universally easy or cheap to deploy and lack sophistication.

AR adoption will see a slight uptick, but I doubt it will captivate the public in 2020 and it will most likely be another year on the backburner.

Apple’s New Projects

Apple has two audacious experimental projects: a pair of augmented-reality glasses and a self-driving car.

The car, for now, has no existence outside of a few offices in California and some hires from companies like Tesla.

And, at the earliest, the glasses won’t hit shelves until 2021,

The car is likely to fizzle out and Apple will be forced to double down on digital content and services to keep shareholders happy which is typical Tim Cook.

The 5G Puzzle

Semiconductor stocks have been on fire as investors front-run the revenue windfall of 5G and the applications that will result in profits.

Select American cities will onboard 5G throughout 2020, but we won’t see widespread adoption until later in the year.

5G promises speeds that are five times faster than peak-performance 4G capabilities, allowing users to download movies in five seconds.

With pitiful penetration rates at the start, the technology will need to grow into what it could become.

The force multiplier that is 5G and the high speeds it will grace us with probably won’t materialize in full effect until 2021.

Each of the nine tech developments in 2020 I listed above negatively affects US tech margins and that will follow through to management’s commentary in next year’s earnings and guidance.

Tech shares are closer to the peak and the bull market in tech is closer to the end.

Innovation has ground to a halt or is at best incremental; companies need to stop cloning each other to death to grab the extra penny in front of the steamroller.

Profit margins will be crushed because of heightened regulation, transparency issues, monitoring costs, and the unfortunate weaponizing of tech has been a brutal social cost to society.

Tech is saturated and waiting for a fresh catalyst to take it to the next level, but that being said, tech earnings will still be in better shape than most other industries and have revenue growth that many companies would cherish.

Mad Hedge Technology Letter

December 18, 2019

Fiat Lux

Featured Trade:

(CYBER SECURITY IS STILL A BUY)

(SYMC), (PANW), (CSCO), (FTNT), (AAPL), (MSFT)

What does the technology sector’s “last gasp up” mean for tech stocks?

At the Mad Hedge Lake Tahoe Conference in late October, I correctly identified that the tech sector would experience a last leg to the price appreciation that has been part of a broader 10-year bull market in American equities.

The past 7 weeks have been nothing short of spectacular for tech shares as not only have the heavy hitters delivered in spades, like Apple (AAPL) and Microsoft (MSFT), but tech growth shares have been released from the penalty box after a short-dated growth scare and joined the rally with zeal.

How long will the “last gasp up” last?

The bar was set exceptionally low in 2019 because senior management spun the trade war acrimony into the accounting calculus effectively offering CFOs a chance to lower expectations to the point of getting away with murder.

Even with earnings’ expectations reset at nadir data points, performance was a mixed bag.

Superior tech companies were able to jump over the pitiful expectations, then if that wasn’t enough, they pushed backwards any inklings of earnings growth by guiding as low as they possibly could.

An archetypal example is Palo Alto Networks (PANW) whose shares dipped more than 8.5% in pre-market trading after issuing their quarterly earnings report.

The company announced sales of $771.9 million with an adjusted EPS of $1.05 topping analysts' estimates.

Why did shares sully?

Palo Alto Networks tanked guidance by telling investors they expect sales between $838 million and $848 million in the second quarter.

The expectation represented a midpoint sales forecast of $843 million, which is lower than the consensus estimates of $845.12 million.

The adjusted EPS in the second quarter is estimated to be $1.11–$1.13, below the consensus earnings forecast of $1.30.

Palo Alto Networks is forecasting sales between $3.44 billion and $3.46 billion with an EPS between $4.9 and $5.0 for next year, compared to analyst projections of $3.46 billion in revenue and an EPS of $5.07 in 2020.

PANW accounts for a big piece of the pie in the cybersecurity trade comprising 16.2% in 2019.

Overall industry growth is strong at 10.4%, and PANW managed to increase its sales by 22.3% to $633.7 million.

This cybersecurity company is one of my favorite tech stalwarts and is as rock-solid as they come for a second-tier tech growth company.

Another trend that dovetails closely with the last gasp up thesis is buying growth.

At this stage in the tech cycle, the low hanging fruit has been plucked and tech companies are increasingly finding it hard to generate organic growth.

Companies are now resorting to inorganic growth with Palo Alto Networks announcing that it will acquire Aporeto for $150 million in an all-cash transaction.

This isn’t just a one-off for PANW, they have acquired four other companies in 2019 to plug into their growth puzzle.

They have also completed the acquisition of an IoT cybersecurity firm Zingbox.

Palo Alto Networks acquired two cloud security startups in July as well - Demisto to gain traction in the AI security segment and Twistlock, the leader in container security.

The other top players in this field are Cisco (CSCO), Fortinet (FTNT) and Symantec (SYMC).

The bullish secular trend in cybersecurity is watertight and comments from Nikesh Arora, CEO of Palo Alto Networks, only reconfirmed the strength in cybersecurity when he said, “As a growing number of organizations move their business to the cloud, developers increasingly rely on cloud-native technologies such as containers and serverless infrastructure to accelerate the development, testing, and deployment of modern applications and services.”

What’s next for investors?

Barring any exogenous shocks, the last gasp up continues and recent macro policy developments have supported this hypothesis as well as the tailwinds of an improving economy.

Palo Alto Networks is part of a high growth segment and many corporates are on record contemplating lower enterprise tech spending heading into 2020.

This sets up another incredibly low bar for cybersecurity companies to hop over next year and I believe the best in show such as PANW, Fortinet, Cisco, and Symantec will pass with flying colors.

The interesting acid test will occur at the end of 2020 when tech firms and sub-segments of tech such, as cybersecurity, release commentary on whether 2021 guidance could signal ensuing risk of being dragged into recessionary turbulence.

A 2021 tech sector recession is certainly not priced into current tech share valuations in this frothy period of asset appreciation.

Global Market Comments

December 16, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOOD NEWS IS OUT)

(FXI), (AAPL), (FXB), (VIX), (USO), (BABA), (NSC), (MSFT), (GOOGL)

After a China trade deal, UK election and a NAFTA 2.0 are announced, what is left to drive the stock market?

That is a very good question and explains why the Dow Average was up only a microscopic 3.33 points on Friday. It had spent much of the day down.

It’s not a pretty picture.

Not only is the market running out of drivers, the economic data is still decelerating, with the GDP running a 1.5% rate, inflation rising, and corporate earnings growth at zero, with earnings multiples at 17-year high.

A Wiley Coyote moment comes to mind.

And while we are finishing a great 27% year (56% for the Mad Hedge Fund Trader), we are in effect getting three years of performance packed into one. Not only did we pull forward a good chunk of 2020’s performance, we borrowed heavily from 2018 as well, coming in at such a low start as we did.

Thus 2019 might well get bookended by an 8% gain in 2018 and another 8% year in 2020, with dividends. Blame it all on the massive liquidity burst we got from the Fed that started last December and continues unabated.

Stocks have been floated by a tidal wave of new money creation worldwide. Globally, new money creation is running at a $1 trillion a month rate and much of that is ending up in the US stock market, especially in technology shares.

The rush was enough to drive Apple (AAPL) to a new all-time high at $275, pushing its market capitalization up to a staggering $1.2 trillion. It could surpass Saudi ARAMCO’s $2 trillion valuation in a year or two.

Steve Jobs’ creation now accounts for a mind-blowing 6% of the S&P 500 and 4% of total US stock market capitalization. It’s the best argument I’ve ever heard for becoming a hippy and dropping out of college after one quarter.

Which leads us to paint a picture for the 2020 stock market. Even the most optimistic outlook for next year, that of Ed Yardeni, is calling for only a 10% gain. Many prognostications are calling for negative numbers next year.

You might be better off parking your money in a 2% CD and taking a cruise around the world. I’ve done that before, and it works fantastically well.

You’re only going to have one shot at making money in 2020. Wait for a 10%-20% nosedive to go long. My guess is that happens when it becomes clear that the Democrats are dominating in the polls (Joe Biden is currently 14 points ahead in swing state Pennsylvania). No matter who wins, less borrowing, less spending, and higher taxes will prevail.

Then stocks will rally 10% AFTER the election because the uncertainty is gone. That will get you a 20%-30% profit in 2020, but only of you are a trader and follow the Mad Hedge Fund Trader. After basking in their own brilliance in 2019, 2020 might be a year when indexers wish they never heard of the term.

In the end, corporate earnings growth always wins, especially in tech, which is still growing at 20% a year. Remember, my 2030 forecast for the Dow Average is 125,000.

China (FXI) won big in mini trade deal. We rolled back a tariff increase that was never going to happen and the Chinese buy $50 billion worth of soybeans they were going to buy anyway, except at half the price that prevailed two years ago. All of it will come out of stockpiles built up during the trade war. Only the ag sector is affected, which is 2% of the US economy. The ag markets aren’t buying it. If this were a real trade deal, stocks would be up 1,000 points, not 89.

Conservatives won big in UK election. The British pound (FXB) is up 2% and stocks are soaring. A hard Brexit is coming, so look for Scotland to secede and Northern Ireland to join the Republic. The UK will be gone as we know it. Britain’s standard of living will plummet. Great Britain will no longer be great, and the Russians financed the whole thing.

Volatility crashed, as complacency rules supreme. Don’t buy (VIX) until we see the $11 handle again.

Chinese copper purchases hit a 13-month high, up 12.1% in November, to 483,000 metric tonnes. It explains the 78% move up in Freeport McMoRan (FCX) since October, the world’s largest producer. Obviously, someone believes a trade deal is coming. My long LEAP players love it.

US Consumer inflation expectations rebounded, up 0.1% to 2.5%, accounting to the New York Fed. That’s crawling up from a five-year low, a slightly positive economic note.

Saudi ARAMCO went public, with a 10% pop in the shares on the first two days, providing a $24 billion fund raise. This is one of the top three largest IPOs in history after Alibaba (BABA) and Softbank. It values the company at $1.88 trillion. Oil (USO) is down a dollar on the news, no longer needing artificial support to get the deal done. This could be one of the seminal shorts of our generation.

NAFTA 2.0 was signed, removing a potential negative from the market. It is 90% of the original NAFTA, not the “greatest trade deal in history” as claimed. Buy the main North/South railroad, Norfolk Southern (NSC) on the news.

Weekly Jobless Claims soared to a two-year high, by 49,000 to 252,000. Are stores laying people off from Christmas early this year, or did they never hire in the first place because the retail businesses are gone? Peak jobs are in. US job growth is now far slower than in the Obama era, as is GDP growth.

Most US companies will have fewer staff in 2020, except Mad Hedge Fund Trader. More automation and algos mean fewer humans. Only a capital spending freeze caused by the trade war kept a low of low-skilled people in their jobs.

This was a week for the Mad Hedge Trader Alert Service to catapult to new all-time highs.

My long positions have shrunk to my core (MSFT) and (GOOGL), which expire with the coming December 20 option expiration.

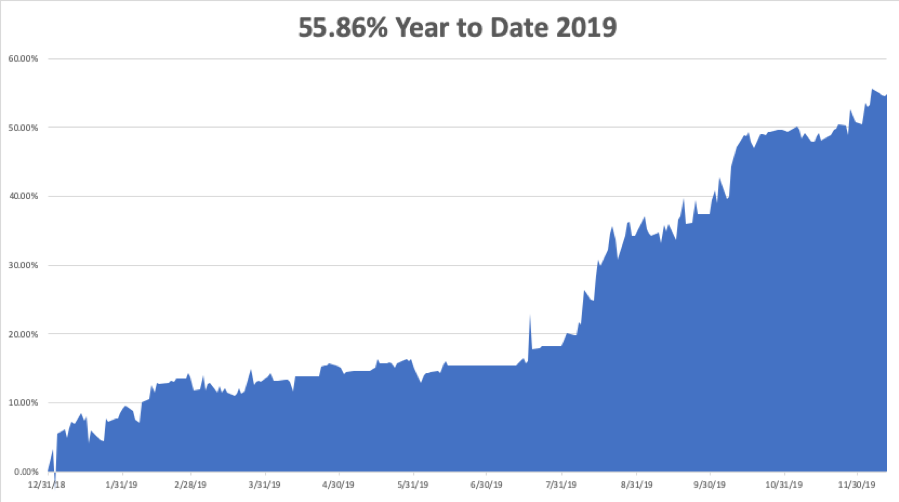

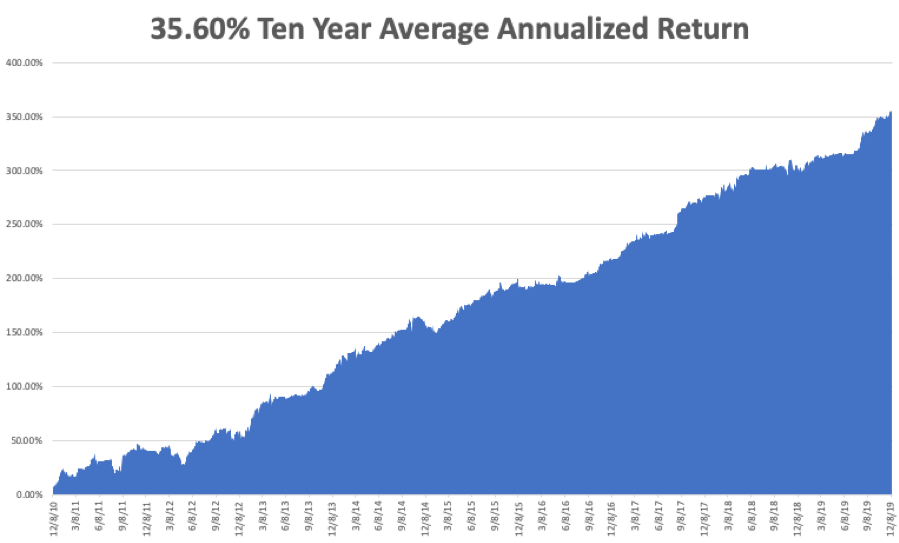

My Global Trading Dispatch performance ballooned to +356.00% for the past ten years, a new all-time high. My 2019 year-to-date catapulted back up to +55.86%. December stands at an outstanding +4.85% profit. My ten-year average annualized profit rebounded to +35.59%.

The coming week will be a noneventful one on the data front, with some housing data and the Q3 GDP on the menu. Anyway, everyone else will be out Christmas shopping or attending parties.

On Monday, December 16 at 9:30 AM, New York Empire State Manufacturing Index for December is out.

On Tuesday, December 17 at 9:30 AM, Housing Starts for November are released.

On Wednesday, December 18 at 11:30 AM, US EIA Crude Stocks for the previous week are announced.

On Thursday, December 19 at 8:00 AM Existing Home Sales are published. At 8:30 AM, we get Weekly Jobless Claims.

On Friday, December 20 at 9:30 AM, the final read on US Q3 GDP is printed. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, after blowing out 1,200 Christmas trees, the Boy Scouts will be taking down the tree lot for the year. And who do they turn to when it comes to wielding a chain saw or sledge hammer?

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

December 13, 2019

Fiat Lux

Featured Trade:

(WHY THE FANGS ARE BREAKING INTO YOUR HOME)

(GOOGL), (AAPL), (AMZN), (ALRM), (ADT), (ARLO), (RESI), (PANW), (CRWD), (FTNT), (CSCO), (CMCSA), (BBY)

The house is the new smartphone and I will tell you why.

The projected market growth of 18% in smart home technology sales according to Acumen Researching and Consulting will deliver opportunities to shape and prioritize this sector.

The revenues up for grabs from the smart home mean that internet of things’ (IoT) companies will create systems that mesh together with the bare minimum human participation, meaning that tech will have a dramatic influence in our daily lives.

I get several moans and groans a day that the Mad Hedge Technology Letter only shines the spotlight on the FANGs.

But it is hard not to when it comes to the future of the home.

Just look at recent M&A activity.

Automation and connected smart appliances have consumed Amazon by recently acquiring Eero, producer of routers for apartments, houses, and multi-story homes, and after already paying $1 billion to acquire Ring, a doorbell-camera startup. It had also bought Blink, a smart camera maker in 2017.

Google hasn’t shied away either by investing in smart home products pocketing Nest, a firm producing smart home products, for $3.2 billion.

Nest took a few years to sort out its production phase but finally managed to launch new temperature sensors, a video doorbell, and an outdoor smart camera.

What are the trending IoT products now?

The flavors of the day are smart lights, security, entertainment systems, and temperature control.

They are the low hanging fruit of the smart home industry – a de facto gateway into this world.

Most of these smart devices operate with voice assistants, but because of the nature of competition, certain products are aligned with certain ecosystems and compatibility issues will persist until the competition flushes itself out.

A layman’s example would be Apple’s Homekit dovetailing nicely with Apple’s Siri.

Companies are in the first innings of the product iteration cycle and the variations of smart home products are endless stemming from showers that remember preferred water temperature and flow rates or climate-control systems that change in real-time to suit the user.

Security of home networks and connected devices are still a controversial question mark because the receiver of this type of data has the keys to the most intimate details of personal lives.

Even avid technologists are hesitant to dive in and put up smart home products all over the house, and most are being cautious.

In fact, privacy issues are the most distinct headwind to fresh adoption rates.

Many people simply aren’t willing to make the jump yet until they are more convinced of its use case.

Even with all the reservations, an alternative global shipment company believes smart home devices will post 24% in growth next year.

For the smart home device believers, this cohort averages 6 smart home devices per household and will certainly rise to 7 or 8 by the end of 2020.

Popular items include the Amazon Echo, Google Home, and Apple (AAPL) HomePod.

Smart speakers are already present in 36% of American homes and rising.

Consumers are also worried about technology invading their daily lives along with allowing artificial intelligence to dominate personal decision making.

Others have concluded that items such as smart microwaves are a waste of money and are unneeded when analog devices function admirably.

Another legitimate reason is that the software and technology involve a perceived steep learning curve to operate which many people do not have the patience for.

And some are just burnt out by the volume of technology thrown in our faces.

Who wants to operate 50 apps on their phone to control their smart home devices when there are other pressing needs in life?

Companies with skin in the game are Alarm.com (ALRM), ADT (ADT), Arlo Technologies (ARLO) and Resideo Technologies (REZI) and they will be outsized winners if they can solve many of the industries lingering issues.

The value thesis in the case of home automation companies is that they are financially efficient, time-effective, boost wellness and will be easy to use.

About 11% of U.S. broadband households have smart thermostats and Nest’s smart thermostat is the most popular.

Networked security cameras by Arlo are in 10% of homes.

Video doorbells from Amazon.com (AMZN), Google are in 8% of homes and help deter theft of e-commerce packages.

Smart light bulbs and lighting are at 8% market share while smart door locks are at 7% penetration.

There are several second derivates bet on this as well.

The most common user interface for the smart home is apps on a smartphone or tablet and voice commands to smart speakers are second.

The conundrum of installation complexities leads to the demand of professional installers.

This demand has delivered opportunities for companies like Comcast's (CMCSA) Xfinity and Vivint.

Electronics retailer Best Buy (BBY) has stepped up its footprint in this market as well.

Another stock play would be cybersecurity companies because they will win contracts protecting the software that smart home products rely on.

Hackers are getting more sophisticated and a private cybersecurity company Firewalla can track where data is flowing to and from your devices.

Firewalla management recommends buying devices from reputable home automation companies like Amazon and Google because they have more accountability and are of higher quality.

There will be a huge onramp of cybersecurity contracts doled out to the likes of Palo Alto Networks, Inc. (PANW), CrowdStrike Holdings, Inc. (CRWD), Fortinet, Inc. (FTNT), and Cisco Systems, Inc. (CSCO).

We are in the first mile of a marathon and smart home product manufacturers, cybersecurity companies, 5G internet, and semiconductor companies will all benefit from the broad-based integration of these next-generation home consumer products.

Mad Hedge Technology Letter

December 11, 2019

Fiat Lux

Featured Trade:

(CHERRY-PICKING IN TECH TODAY)

(ZM), (CRM), (GOOGL), (AAPL)

The valedictorian of the IPO class Zoom Video Communications, Inc. (ZM) is finally on sale at a discount.

If readers want to indulge themselves in a high caliber tech growth stock to buy and hold stock, this is the one for you.

This one has no regulatory headwinds as well as an added bonus.

Zoom’s share price has dropped 40% since hitting the heights of $102 in July which was coincidentally the high for most post-IPO tech stocks of 2019.

It’s been an elevator straight down to no man’s land since then, but investors would be foolish to paint all hyper-growth companies with the same brush.

Filtering out the wheat from the chaff is critical and Zoom is the stock that still has the gloss on its outside package buttressed by its best in show video conferencing software.

There are no other proper alternatives in this sub-sector of software.

A few days ago, the stock slid 9% even though the company crushed expectations with its latest quarterly result and outlook.

Zoom generated revenue of $166.6 million representing a growth rate year on year of 85%.

The company then offered a forecast of $175 million next quarter when analysts only estimated $165 million.

Remember that this company grew 96% just 2 quarters ago and it would be illogical to believe that the stock is being penalized from faltering to 85% today.

Any tech company would give a left leg for 85% growth.

Zoom was trading at 33.5 times my calendar 2020 estimates compared to the fast growth software as a service (SaaS) median at 12.9 times.

Then software stocks started indiscriminately selling off on earnings over the past few weeks irrelevant to the quality of news because of worries to the broader bull market in tech stocks.

It’s true that tech stocks aren’t cheap now, and the skittishness rears its ugly head when bullet-proof earnings’ results are met with a cascade of selling.

Salesforce (CRM) was a software company that was penalized for pricey M&A because the company has been unable to organically grow forcing them to buy growth.

Buying growth is not necessarily a bad strategy but buying growth at this point in the economic cycle naturally means that companies will need to overpay for growth because of expensive valuations.

Zoom is perfectly positioned to outperform in the next 2-3 years.

The advancing runway is wide open with no competition in sight and a generous growth trajectory is firmly on their side.

We Company singlehandedly destroyed positive biased market momentum for any tech growth stock this summer, but on the bright side, quality post-IPO growth stocks are more reasonably priced with compelling entry points.

At around $60, Zoom looks appetizing and is a convincing buy and hold. At some point, this software company could become a takeover target for a larger corporate because companies such as Google (GOOGL) and Apple (AAPL) will need to acquire growth moving forward.

I am impressed with Zoom's superior products, growth prospects, and scalable business model, and the stock’s near-term risk/reward trade-off is attractive after the 9% haircut this past week.

There is an actionable and manageable clear path to a $2 billion revenue run rate with strong margin expansion potential and with its flagship product growing around 80-90%, its next growth driver in Zoom Phone could translate well into a meaningful revenue stream.

Zoom Phone is the next springboard to further success for this company.

Anyone that has used Zoom as a product can confirm the veracity of its superior performance standards.

This isn’t the type of stock to trade short-term, the volatility undermines any potential entry points.

If the broader market holds up in 2020, and Zoom isn’t a $100 stock by yearend, then the stars should align by 2021 because the value extraction potential is substantially robust in Zoom’s business model.

We finally have a reasonable level to scale into Zoom, and if it drops into the $50 range, it’s not just a scale-in type of scenario, investors should buy as much as they can with two hands.

Growth stocks can only be pinned down for so long and the best and brightest have been unfairly penalized with the rest. And let me remind you, this patch of softness in shares is only ephemeral and now is the time to act.