Global Market Comments

February 21, 2019

Fiat Lux

Featured Trade:

(SHORT SELLING SCHOOL 101),

(SH), (SDS), (PSQ), (DOG), (RWM), (SPXU), (AAPL),

(VIX), (VXX), (IPO), (MTUM), (SPHB), (HDGE),

Global Market Comments

February 21, 2019

Fiat Lux

Featured Trade:

(SHORT SELLING SCHOOL 101),

(SH), (SDS), (PSQ), (DOG), (RWM), (SPXU), (AAPL),

(VIX), (VXX), (IPO), (MTUM), (SPHB), (HDGE),

Global Market Comments

February 11, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or DON’T STAND NEXT TO THE DUMMY),

(AAPL), (MSFT), (TSLA), (VIX), (TLT), (TBT), (FXI)

When I was a war correspondent (Cambodia, Laos, Iraq, Kuwait, Indonesia), my seniors gave me a sage piece of advice that saved my life many times.

“Don’t stand next to the dummy.”

Don’t go near the guy wearing the Hawaiian shirt, NY Yankees baseball cap, and aviator sunglasses. You want to be dressed in the same color as the troops and blend in as much as possible. Otherwise, the enemy will aim at the dummy and hit you.

As much as I tried, at 6’4” I was never going to blend in anywhere in Asia. So, I went into the stock market instead.

Now 50 years later, I am facing another dummy problem. Except that the next hit I may take will be of the financial kind rather than the metallic one.

The reaction to the Trump tax cuts is going to be far worse than any benefits the privileged class was able to reap from the cuts in the first place. Listening to the proposals aired, I shudder: A maximum 70% tax rate, the end of special estate tax treatment, a millionaire’s surtax, and the banning of corporate share buybacks.

It’s that last one that that will be particularly damaging for the US economy. Often, a company’s best possible investment is in its own shares where returns are frequently higher than possible through investing in their own business. Just think of all those shares Apple (AAPL) bought at $25, now at $170, and Microsoft (MSFT) picked up at $10.

This is one of the only occasions were management and shareholder interests are one and the same. The event is tax-free as long as you don’t sell your shares. And companies don’t have to pay dividends on stock they have retired, boosting profits even further.

The media loves pandering to the most extreme views out there. I know because I used to do it myself. Cooler heads will almost certainly prevail when the tax code is completely rewritten again in two years. Still, one has to worry.

The week had plenty for we analysts and strategists to chew on.

Is the Fed pausing because of political pressure or an economy that is falling apart? Neither answer is good for equity holders. Start cutting back risk while you can. There are lots of bids on the way up, but none on the way down as December showed.

There has lately been a rising tide of weak data to confirm the negative view.

Factory orders nosedived 0.6% in November, the worst in a year. Funny how nobody wants to make stuff ahead of a recession. ISM Non-Manufacturing Index Cratered to 56.7. Should we be worried? Hell, yes! Why are we getting so many negative data points and stocks keep rising?

Farm sector bankruptcies are soaring, hitting a decade high. Apparently, the trade wars and global warming aren’t working for them. Ironically, ag prices are about to take off to the upside when a Chinese trade deal gets done. Buy the ags for a trade.

Tesla (TSLA) cut prices again in a blatant bid for market share and global domination. The low-end Tesla 3 price drops to $42,900. Next stop $35,000. Too bad they laid off my customer support personnel to cut costs. I can’t find my AM radio.

China trade talks (FXI) hit the skids, taking the stock market down with it as an administration official concedes they are “nowhere close to a deal” with the deadline 3 weeks off. Trump desperately needs a deal while the Chinese don’t, who think they can do better under the next president. If you disagree with this view in China, your organs get harvested and sold on the open market.

The European economy is also going down the drain with the EC’s forecast of economic growth cut from 1.9% to 1.3%. The US-China trade war is cited as a major factor. The global synchronizes slowdown accelerates. Looks like they’ll have more time to drink cheap wine and smoke Gauloises.

The Volatility Index (VIX) hit $15 and that seems to be the bottom for the time being. The market was more overbought than at any time since July. Is the “fear gauge” signaling that happy days are here again? I doubt it. Don’t whistle past the graveyard.

The Mad Hedge Market Timing Index is entering danger territory with a reading of 67 for the first time in five months. Better start taking profits on those aggressive leveraged longs you bought in early January. Your best performers are about to take a big hit. The market has since sold off 500 points, proving its value.

There wasn’t much to do in the market this week, given that I am trying to wind my portfolio down to 100% cash as the market peaks.

I stopped out of my short portion in Apple when my stop loss was triggered by pennies. The second I was out, it began a $6 selloff. Welcome to show business.

I used a major 3 ½ point rally in the bond market to put on a new double short position there. The yield on the ten-year US Treasury bond has to plunge to 2.40% in a month, a three-year low, for me to lose money on this position. It’s a bet that I am happy to make.

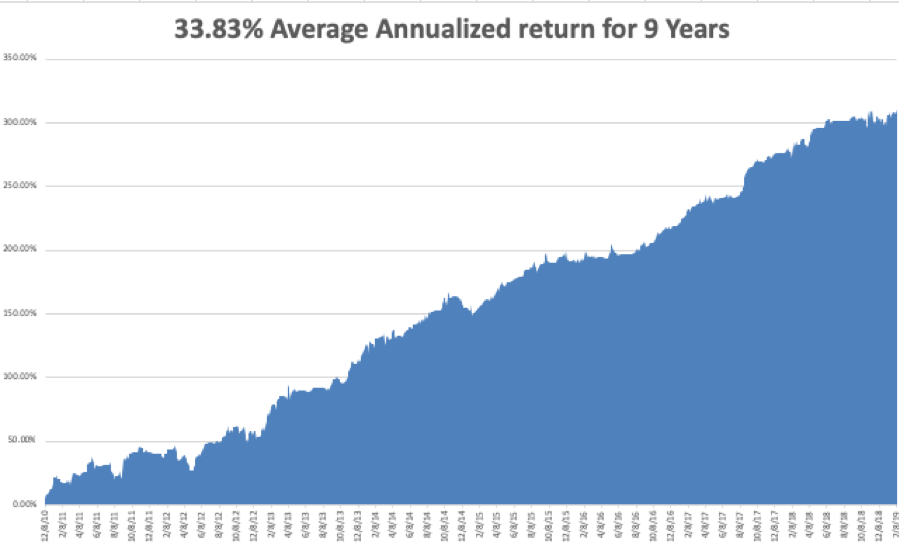

My 2019 year to date return leveled out at +10.03%, boosting my trailing one-year return back up to +35.75%.

My nine-year return maintained +310.17%, a new high. The average annualized return stabilized at +33.83%.

I am now 70% in cash and triple short the bond market.

Government data is finally starting to trickle out now that the government shutdown is over.

On Monday, February 11 there is nothing of note to report. Everything important is delayed.

On Tuesday, February 12, 10:00 AM EST, we get the January NFIB Small Business Index. Earnings for Activision Blizzard (ATVI) are out and should be a complete disaster, along with Twilio (TWLO).

On Wednesday, February 13 at 8:30 AM EST, the all-important January Consumer Price Index is published. Barrick Gold (GOLD) reports.

Thursday, February 14 at 8:30 AM EST, we get Weekly Jobless Claims. We also get December Retail Sales which should be good.

On Friday, February 15, at 8:30 AM EST, the February Empire State Index is out. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I will be battling my way through the raging snowstorms of the High Sierras trying to get over Donner Pass to my Lake Tahoe estate. Unless I clear the six feet of snow off the roof soon, or the house will get crushed from the weight as it did three years ago.

Where are all those illegal immigrants hanging out in front of 7-Eleven now that I need them?

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

February 7, 2019

Fiat Lux

Featured Trade:

(THE DEATH OF THE COLLEGE DEGREE),

(GOOGL), (IBM), (AAPL), (BABA), (BIDU)

If you’re an educator not at a top 25 American university, you might want to stop reading right now.

Disruption.

You’re either on the right or wrong side of it.

I’ve detailed numerous subsets of the economy and society that have been transformed by sharp shifts in technological innovation.

But the one industry that has stealthily moved into the heart and center of technological disruption is education.

For centuries, universities and higher learning institutions had a stranglehold on critical information required to successfully perform in the cutting-edge knowledge economy of those times.

Then on September 15, 1997, a mere 21 years ago, Google search launched its free services to the world and grabbed the monopoly of information away from the college system.

This website effectively caused the cost of information to crater to zero and its free website is ranked #1 as of February 2019 with over 4.5 billion monthly active users.

The ensuing 21 years has been a renaissance in the ability to distribute information propelled by this one platform, and the result is that billions have the ability to study and read up on what they want and when they want.

The ability to learn for free combined with a tight labor market is a promising landscape for job seekers, with analysts forecasting more opportunities for professionals without a degree.

Job-search site Glassdoor amassed a list of various employers no longer bound by requiring applicants to possess a 4-year bachelor’s degree.

These firms aren’t your second-rate companies either made up of gold standard workplaces such as Google, Apple, and IBM.

In 2017, IBM's vice president of talent Joanna Daley confided that about 15% of IBM’s new hires don't have a four-year bachelor qualification.

She emphasizes hands-on experience through coding boot camp or industry-related vocational classes as explicit criteria to get hired.

This development bodes poorly for the future of universities and boosts the prospects of alternative education.

Online college offers working adults ample flexibility in furthering their education.

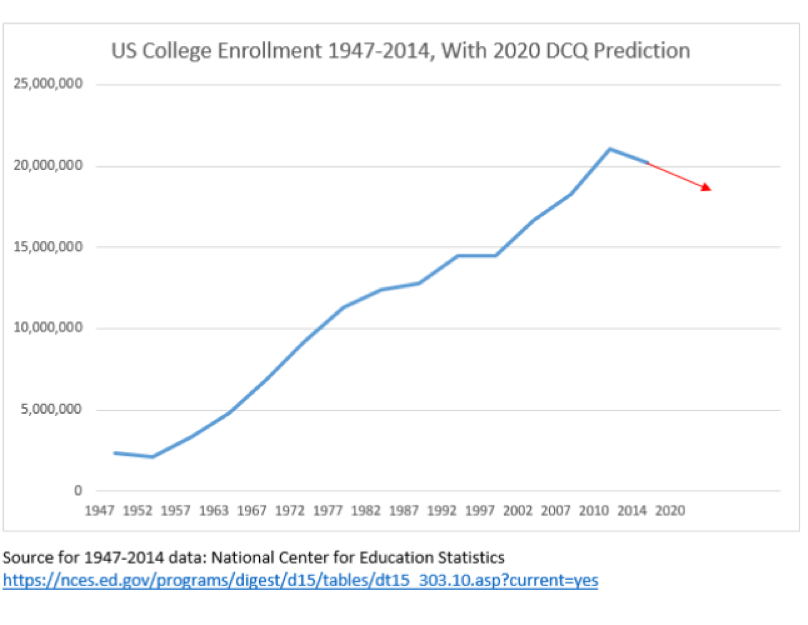

According to the most recent federal statistics from 2016, roughly one out of every three, or 6.3 million college students learned online.

Even though online courses are becoming more widespread, the best and brightest aren’t attending these schools.

However, it did hijack the marginal student that was on the fence for a 4-year university and brought them into the orbit of for-profit online courses and the revenues that came with it.

That was the first stage of online forces imposing financial pressure on the education marketplace.

Now analysts are discovering the second major trend with higher rated students opting out of the university system altogether.

In many cases, a 4-year university degree is a bad value proposition.

Why is that?

Costs.

In a capitalistic economy that lives and dies by the mantra of buy low and sell high – universities seem to be getting sold short lately.

The exorbitant costs to obtain a 4-year degree has led to an outsized student debt bubble and removed the mystique of this once treasured qualification.

A growing chorus of bipartisan voices has pigeonholed student debt as a major problem across the country.

In the previous presidential election, Democratic candidate Bernie Sanders called this situation “outrageous” as national student debt has spiraled out of control to the amount of $1.5 trillion.

This has been a terrible commercial for the younger generations to follow in the footsteps of the indebted Millennial generation.

And with Generation Z tech savvy at building stand-alone firms buttressed by Instagram and YouTube platforms, why go to college anymore?

Or to nail one of those jobs developing iPhones in Cupertino, why not take a few coder boot camps and self-develop a portfolio impressive enough to score an Apple interview?

The bottom line is that there are workarounds for a fraction of the price.

And because tech firms have outpaced analog companies in salaries and hiring for the past two decades, there is an outsized bias on compiling technical skills that will lead a candidate down a path to a salary of over $100,000 quicker than a 4-year degree can.

Not many other industries can claim the same.

The cracks are beginning to reveal themselves in the overall university apparatus.

Universities had years of record revenue that they reinvested into the system to enhance programs, staff, buildings, stadiums, and infrastructure.

The financial catalyst was the rise of the Chinese college student.

The latest statistics nailed the number of Chinese nationals in America studying for 4-year degrees at over half a million.

Many of those were trained up with engineering-related degrees and bolted back home to find jobs at Baidu (BIDU), Tencent, or Alibaba (BABA) powering Chinese Inc.

However, the drop off in demographics from young Chinese and Americans are forcing universities to fight for a shallower pool of candidates with less attractive degrees relative to the value of degrees of past generations.

The second-tier universities are hardest hit with examples galore.

Alcorn State University in Mississippi saw a dramatic 69.45% decrease in applications in 2018 and its rural location didn’t help either.

Alabama State University is feeling the pinch with a 33.06% drop in application in recent years.

If you thought the University of New Orleans was clawing its way back to relevancy after Hurricane Katrina, you are mistaken with its 38.23% drop in applications.

Military schools haven’t been spared either with applications to The United States Air Force Academy crashing 28.12% over the past ten years.

A confluence of deadly trends is about to beset the university system and schools will likely go bust.

Technology is giving a reason for students to bypass the system while also speeding up the financial timebombs many universities are about to confront.

Then we must ask ourselves, will universities even exist in the future?

Probably, but perhaps just the top 25 elite schools that are still worth the high costs.

Mad Hedge Technology Letter

February 6, 2019

Fiat Lux

Featured Trade:

(ALPHABET WOWS THEM AGAIN),

(GOOGL), (AMZN), (AAPL), (MSFT)

Alphabet (GOOGL) is entangled in the same imbroglio as Apple (AAPL), that is why I have held back on issuing any trade alerts on this name.

The stalwart is still grinding out a respectable 20% of revenue growth in their core business but the underlying conundrum is that their hyper-growth segments are 5 times or more diminutive than their bread and butter of digital ads.

Apple is addressing the same type of strain in attempting to flip high octane revenue drivers into a bigger piece of the pie – the services business trails the hardware business by a large margin.

This phenomenon highlights how investors demand tech companies to grow at elevated rates and a maturing business model isn’t given any free passes.

Investors simply migrate towards higher growth names period.

That being said, Alphabet’s digital ad business is one of the premier tech divisions in all of technology and the American economy.

How powerful is it?

They did $32.6 billion in sales last quarter.

If you look at that number without context, it is quite impressive, but there are several lurking impediments.

This 20% QOQ growth is flatter than a pancake offering evidence that the best days are behind them.

No investors like to hear the dreaded “P word” thrown into a company’s business trajectory – peak.

In respect to revenue growth rates, I expect Google’s digital ad business to gradually decline relative to competition.

This segment also battles with the law of large numbers.

It’s simply difficult to accelerate revenue rates at a 25% YOY clip when revenues are already over $30 billion per quarter. Again, this is another Apple problem and a side effect of being overly successful in one part of the business model.

If investors' tepid reaction about these aspects of the core business telegraph dissatisfaction, then discovering further ancillary problems might be the final dagger in the heart.

Google search’s price per click cratered 29% YOY indicating that variables in the current marketing environment have significantly blunted Google’s pricing power.

Traffic Acquisition Cost (TAC) represents the cost for a company to acquire internet traffic onto their assets.

Alphabet faced a 15% YOY rise in TAC costs last quarter to $7.44 billion illustrating the difficulty in keeping these high costs down.

The bulk of the $7.44 billion stems from a widely known agreement with Apple contracting Google search as its default search engine on Apple devices.

This TAC expense has been surging the past few years and Alphabet has little negotiating power.

Expect an annual 15-20% rise in TAC expenses as long as Alphabet’s digital ads are expanding the standard vanilla 20% most investors expect them to grow.

As a whole, TAC costs soaked up 23% of the digital ad revenue which was in line with analysts’ expectations.

However, I expect this number to surpass 25% before winter because I believe Google search’s ad business will confront ceaseless growth problems.

Amazon’s (AMZN) new-found digital ad business is an influential factor in this story.

New marketing dollars aren’t being showered on Google as they once were, over 50% of product searches populate from Amazon.com today boding poorly for the future of Google search.

This optionality could be a large reason in driving the cost per click downwards.

CEO of Amazon Jeff Bezos refused to enter the digital ad game for years but his recent change of heart will correlate to subduing Google digital ad model.

Consumers are finding less incentive to search on Google for products when they just can smartly and efficiently search on Amazon directly.

Clearly, this only affects product searches and not searches on other informative content such as widely popular searches including “top 10 places to travel in Europe” or “best Thanksgiving recipes.”

Google’s “other revenues” is chugging along nicely with 31% YOY growth headed by Google’s cloud business and hardware division.

This is what Alphabet needs to focus on going forward similar to Microsoft and Amazon web services.

Yes, Google is the 3rd biggest cloud player but miles behind the top two.

Being in catch-up mode is no fun and is part of the reason capital expenditures exploded and came in $1.38 billion higher than expected.

Alphabet simply isn’t doing a good job at executing relative to Amazon and Microsoft frittering away more capital in the name of growth but not curating the type of growth that current expenses justify.

Higher costs damaged operating margins coming down 2% YOY to 21%.

Even more worrisome is that there has been no material progress on the Waymo business.

This is the year that Alphabet expected the technology to roll out to the masses.

However, this broad-based integration will not happen as fast as they would like.

I blame regulation and consumers' hesitation to quickly adopt this new technology.

Alphabet is reliant on this business to carry them to the next level of growth and I believe it can become a $100 billion per year business in a $2 trillion addressable market.

But when you peruse through the “Other Bets” category which houses Alphabet’s other companies such as health venture Verily, the $154 million in revenue was a huge miss against the $187.4 million expected.

Estimates aside, the pitiful fact that Waymo only brings in revenue of less than 1% of total revenue is disappointing.

Summing things up, Alphabet is a great company and is a long-term buy and hold stock even with short term transitory headaches.

In the near term, there is uneasiness about the decreasing profitability, exploding expense factors, a heavy reliance on weakening core business revenue, and a lack of top-line contribution of “other revenues” relative to their core business.

Long term, Alphabet’s game-changing investments have yet to show signs of life in terms of real revenue expansion even though Alphabet is the global leader of artificial intelligence and self-driving technology.

Investors would like to see actionable steps to incorporate this best of breed technology that funnels down to the top and bottom line.

Investors are stuck with a stale digital ads business that has locked the stock into a holding pattern essentially trading sideways for the past year until they prove they are ready to take the next step up.

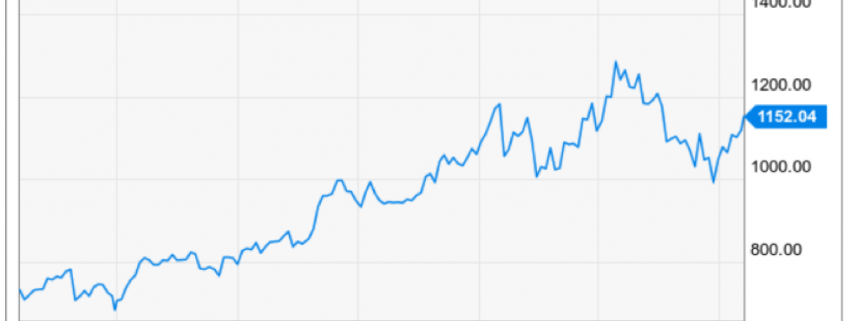

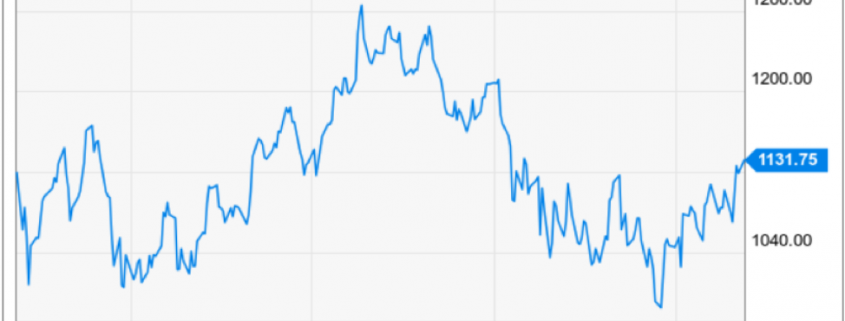

Looking at Alphabet’s chart, the stock has iron-clad support at $1,000 which it tested in April 2018 and December 2018.

Using this entry point as the lower range would be sensible as I don’t foresee any demonstrably negative news blindsiding the stock, and I surmise that investors will start receiving positive news on Waymo’s roll out towards the middle of the year.

Global Market Comments

February 5, 2019

Fiat Lux

Featured Trade:

(A NOTE ON OPTIONS CALLED AWAY)

(TLT), (AAPL),

(THE GOVERNMENT’S COMING WAR ON MONEY)

Mad Hedge Technology Letter

February 5, 2019

Fiat Lux

Featured Trade:

(THE FINTECH COMPANY YOU’VE NEVER HEARD OF),

(FISV), (AAPL), (GOOGL), (FDC), (PYPL), (SQ)

Here’s a company for you involved in technology’s tectonic shift towards FinTech in 2019.

They aren’t new, but you’ve probably never heard of them.

It’s Fiserv Inc. (FISV) which sells financial technology and can include customers such as banks, credit unions, securities broker-dealers, leasing, and finance companies.

An inflection point is occurring within the global business and that is financial technology and the rapid integration of it.

Financial institutions are building products around this concept and Fiserv has a head start on the others with more than 30 years of experience in aiding banks, thrifts, and credit unions, managing cash and processing payments, loans, and account services.

The Wisconsin-based company constructed an unstoppable machine leveraging its time-honored relationships and expertise to bring banking to all the screens that pervade daily life.

“Innovation, Integration and Scale” has been the motto that has served this company well for so long.

The company cut its teeth in the trenches helping banks move money long before it became the next big thing.

Five years ago, under the leadership of CEO Jeff Yabuki, there was a corporate flashpoint with upper management realizing they needed to evolve or die.

Yabuki anticipated a near future fueled by mobile wallets and changing consumer expectations - an always-on, never-off connected world.

An environment where consumers want what they want when they want it.

There has been no letup in this trend.

Silicon Valley companies were always the 800-pound gorilla in the room and Fiserv didn’t want to become sideswiped by them.

And in 2014, at the Money 20/20 conference in Las Vegas, Yabuki set out his vision that continues to prevail today.

The financial services industry had become obsessed with point-of-sale transactions.

And at $200 billion in annual domestic sales, it was a business that resonated to all corners of the FinTech world.

It was sensical to persuade consumers to use branded credit or debit cards to pay for stuff in stores and online.

At the time, that was bread-and-butter banking.

To the banks' chagrin, Silicon Valley has gotten in on the act with the likes of Apple (AAPL), Alphabet (GOOGL), PayPal (PYPL), Square (SQ) firing warning shots.

They formulated products of their own, whipped up the necessary scale and maximized the reverberating network effects.

Yabuki urged financiers at the conference to double down on what they did best while looking to grab low-hanging fruits in the short-term.

The business beyond point-of-sale was theirs waiting on a decorative platter – the opportunity was a $55 billion behemoth consisting of consumer-to-consumer, business-to-business and consumer-to-business transactions.

Embracing FinTech translated into massive speed advantages, stauncher security-laced products while offering traditional bank customers higher quality service at their convenience.

Fiserv erected a platform to help financial institutions focus on payments beyond POS called Network for Our World.

The goal of this NOW Network was to help customers' flow of money by paying bills and getting paid.

These entrepreneurs are looking for more efficient ways to collect money owed - they are a lucrative addressable audience for bankers.

The Fiserv sales pitch is working wonders according to the data. The company has 12,000 clients worldwide, with 85 million online banking end-users.

It has rolled out innovative products for payments, processing, risk and compliance, customer service and optimization.

The company has become ever so profitable with a 3-year EPS growth rate of just 15%, but in the last quarter, this metric surged to 23% and projected to rise.

Fiserv also dabbled with some M&A hauling in debit-based assets of Elan Financial Services.

The stellar acquisition, with annual revenue of over $170 million, extends Fiserv’s leadership in payments, broadens client reach and scale, and provides new solutions to enhance the value proposition of the existing 3,000 debit solutions clients.

The deal also gave Fiserv ownership of Money Pass, the second largest surcharge-free ATM network in the U.S., with over 33,000 in-network ATMs.

They also added other major pieces with the purchase of First Data Corp (FDC).

The maneuver is strategically solid, and Fiserv will benefit from a parlay of idiosyncratic opportunities from the combined synergies.

Fiserv will be able to refer First Data's merchant-acquiring services to the banks it currently works with.

I predict cost savings of $1 billion from the deal and potential upside from platform rationalization, which has not yet been included in synergies.

There will be significant upside potential from interest expense savings given refinancing FDC's debt at investment-grade.

Dipping your toe into this name before its multiple inevitable expands is a good long-term strategy.

Profitability is increasing while management has made moves that will fatten its top line business from the 5% internal growth today.

All these growth levers will push up revenues in the upcoming quarters - Fiserv happens to be the right company in the right industry at the perfect time in the technology cycle.

The stock is up over 1,000% in 10 years.

In February 2009, the stock was meddling around $8 and the $83 it trades at today demonstrates the potency of FinTech and the strength in their underlying business model.

I would wait for a sell-off to get into this one, but it’s a keeper.