Truth be told, it’s the really boring, sedentary, go-nowhere markets that drive me nuts, cause me to tear my hair out, and urge me on to an early retirement.

The week started with such promise.

Sunday night I witnessed the first Space X landing of a rocket in California which I could clearly see from the top of Berkeley’s Grizzly Peak some 250 miles away. It was fascinating to see four separate jets steer the spacecraft earthward.

Financial markets had a different landing in mind, the hard kind, if not a crash.

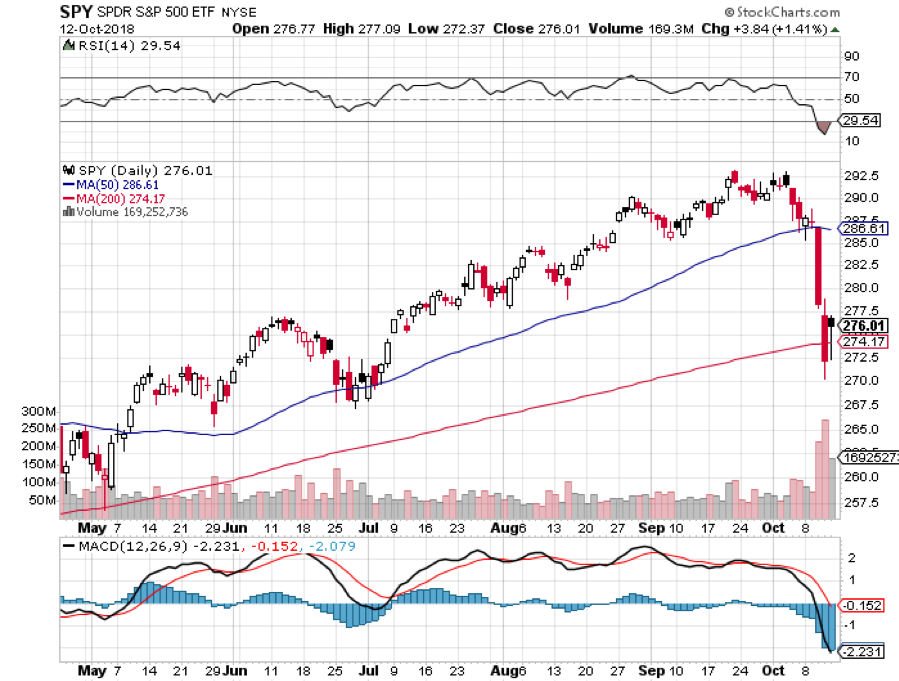

I absolutely love the market we had last week which saw the third biggest down day in history, volatility explode, and $2.6 trillion in stock market capitalization vaporize.

I had to blink when I saw NASDAQ (QQQ) down an incredible 350 points in one day. My Mad Hedge Market Timing Index hit an all-time low at 4.

No wonder insider selling hit $10.3 billion in August, another record. Maybe they know something we don’t.

Chinese Gamer Tencent Postponed their US IPO. It seems they noticed that market conditions had become unfavorable. I know investment bankers hate passing on an opportunity to ring the cash register. I used to be one.

There is no better feeling than being 100% cash going into one of these crashes and then having panicked investors puke their best quality positions to me at a market bottom.

On Thursday, I backed up the truck and issued four perfectly timed Trade Alerts, picking up Microsoft (MSFT), Apple (AAPL), and the S&P 500 (SPY), and covering my short position in the bond market (TLT).

In fact, I believe I had my best week of the year even though I only added modestly to my annual return. Look at the charts below and you’ll see that I suffered a 9% drawdown during the February meltdown. Maybe I’m getting wiser as I get older? One can only hope.

This time, I managed to limit my loss to a modest 2.5% and am nearly unchanged on the month despite the Dow Average at one point nearly giving up all its gains for 2018. This is also against a horrific backdrop of hedge fund performance that is now showing losses for 2018.

The Volatility Index (VIX) made a move for the ages, at one point kissing the $29 handle, up from $11 two weeks ago. During the 600-point swoosh down on Thursday, I couldn’t get any of my staff on the phone. The entire company was logged into their personal trading accounts, buying puts on the iPath S&P 500 VIX Short-Term Futures ETN (VXX) as fast as they could.

Which leads me to believe that the bottom is near. Earnings and valuation support start kicking in big time at these levels, and the blackout period for company share buybacks started ending with the bank earnings last Friday.

When you take a $1 trillion buyer out of the market, it has a huge effect no matter how strong the fundamentals are. Start buying those dips. Their return is similarly eventful. I’ve already started to invest my 95% cash position.

Further eroding confidence was the president’s statement that the Federal Reserve is crazy. So, now we know the president appoints crazy people to the most important financial positions in the country. White House control of interest rates ahead of elections. Why didn’t I think of that?

Sparking the Friday melt-up was a statement by JP Morgan (JPM) CEO Jamie Diamond saying that a 40-basis point rise in rates is no big deal. The bull market is on. His earnings beat all expectations.

My 2018 year-to-date performance has bounced back to 27.56%, and my trailing one-year return stands at 35.87%. October is almost flat at -0.84%. Most people will take that in these horrific conditions.

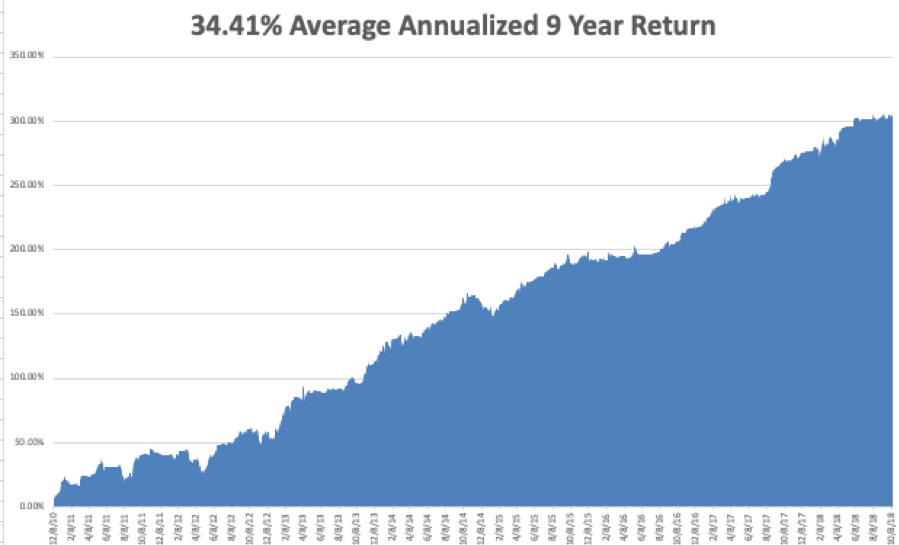

My nine-year return appreciated to 304.03%. The average annualized return stands at 34.41%.

This coming week will be pretty sedentary on the data front.

Monday, October 15 at 8:30 AM brings us September Retail Sales.

On Tuesday, October 16 at 9:15 AM, September Industrial Production is announced.

On Wednesday, October 17 at 8:30 AM, September Housing Starts are published.

Thursday, October 18 at 8:30, we get Weekly Jobless Claims. At 10:00 we learne the September Index of Leading Economic Indicators.

On Friday, October 19, at 10:00 AM, the September Housing Starts are out. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I will spend this week on my Southeastern US roadshow, giving strategy luncheons in Savannah, GA, Atlanta, GA, Miami, FL, and Houston, TX. I love meeting my readers mano a mano who are often a source of my best trading ideas. It looks like I’ll miss Hurricane Michael by three days.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader