Mad Hedge Technology Letter

April 17, 2019

Fiat Lux

Featured Trade:

(ALPHABET DOMINATES WITH GOOGLE MAPS)

(GOOGL), (AMZN), (YELP), (UBER)

Mad Hedge Technology Letter

April 17, 2019

Fiat Lux

Featured Trade:

(ALPHABET DOMINATES WITH GOOGLE MAPS)

(GOOGL), (AMZN), (YELP), (UBER)

Remember Google Maps?

Google will start monetizing it, let me tell you about it.

The web mapping service developed by Google gifting access to satellite imagery, aerial photography, street maps, 360° panoramic views of streets has been around since the beginning of this generation of big tech and is what I would consider legacy technology.

Legacy technology is often associated with failure as the out of date nature isn’t applicable to the tech scene and the commercialization of it today.

In a candid letter, Jeff Bezos wrote to shareholders that Amazon will “occasionally have multibillion-dollar failures.”

Silicon Valley tech will have its share of implosions stemming from ill-fated industry decisions correlating to heavy losses.

Google Maps won’t be one of these slip-ups.

However, a whole catalog of instances can be chronicled from Microsoft’s purchase of Nokia’s handset division to Google’s social media foray in Google Plus.

It hasn’t gone all pear-shaped for Alphabet in 2019. I strongly believe they are one of the companies of the year harnessing YouTube in ways consumers never imagined.

Adding color to the story, any remnant of apprehension to any bearish feelings about Alphabet should vanish once investors understand how lucrative Google Maps will become.

Google has spent decades and billions of capital honing the application and in terms of market share they have cultivated a monopoly.

Uber’s S-1 filing shined some light on Google Maps characterizing it as a must-have input into their business saying, “We do not believe that an alternative mapping solution exists that can provide the global functionality that we require to offer our platform in all of the markets in which we operate.”

Uber sunk $58 million integrating Google Maps into its services from 2016-2018 along with continuous payments to its Google Cloud arm to host Uber’s data.

The strong relationship with Uber shows how Alphabet is adept at milking 3rd party apps for what they are worth.

Alphabet’s stake in Uber is projected to be $5 billion from the $250 million investment in Uber in 2013.

The party doesn’t stop there with Uber paying Alphabet $631 million from 2016-2018 in digital marketing services and another $70 million for technology infrastructure.

To say that Google firmly has its tribal marks tattooed into Uber’s skin is an understatement.

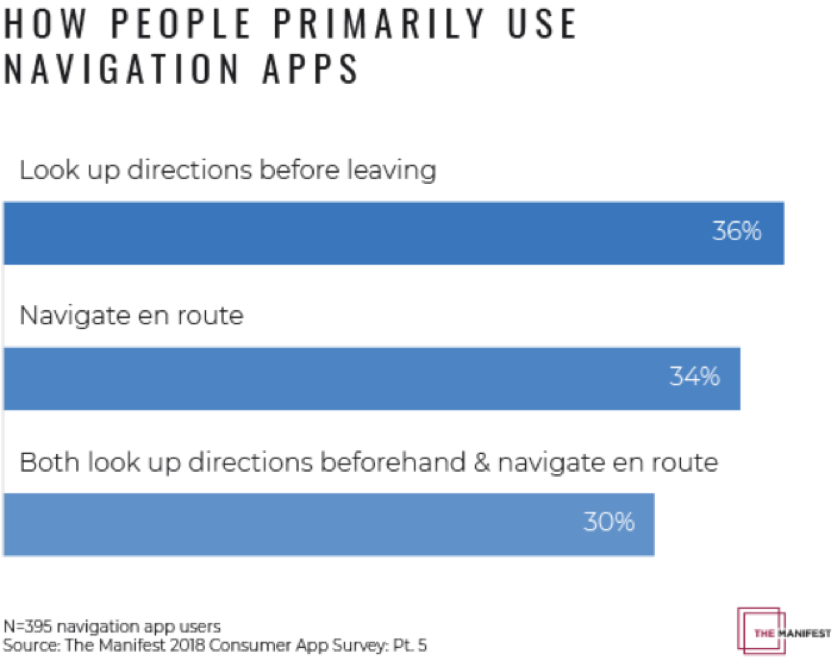

Almost 80% of smartphone users regularly use navigation apps.

Google Maps is the most popular navigation app by a country mile with 67% of market share.

One billion people consistently use Google Maps.

It is the go-to navigation app for nearly 6x more people compared to the runner up app Waze with 12% market share.

The superior performance of the app has allowed it to branch off into a Yelp-like hybrid app accumulating reviews of businesses and institutions that are conveniently dotted around its map.

Multi-functional terrain was integrated to make the maps more 3D and route navigation from point A to B routes has steadily improved since its inception.

The increasing detail showing even roofs of sheds and the Google street view offering a point of view vantage point boosting the reliability of the app.

The result of making the app better is that navigators can easily discern locations and follow routes clearly.

Most would concede that they use the app to look up specific street routes.

By implementing digital ads into the experience, product and service offers will possibly populate in real time as the user glances at the app’s directions.

A vast amount of services such from food to personal grooming to even cannabis club ads could be applicable and ad companies will pay top dollar to post on Google Maps.

Google could also offer personalized recommendations to users and collect an affiliate fee if the user clicks on an attached link transferring the customer to a 3rd party landing page.

They already benefit from this strategy on Google Flights.

Google might even be tempted to implement a Groupon model with group discounts on services positioned on Google Maps.

Google Maps is hands down the most underappreciated app and most under monetized tech asset in the world.

Another possible revenue generation avenue would be the advent of Google Maps voice ads en route to a destination that would promote a 5 or 10 second voice commercial of a businesses that the user is physically passing by.

The unintended effects of Google’s audacious transformation of their proprietary Map service spells doom for Yelp’s business model.

Google’s move into digital ads of maps effectively means that Yelp will be relegated to an inferior version of Google Maps without the map technology.

Google has accumulated enough personal data to draw up any type of profile for particularly Android users voraciously consuming data on Gmail, Google Maps, Google Search and Google Chrome.

These four data generators will allow Google to formulate a shadow profile based on individual tastes with daily use of these four Google properties.

Alphabet has a time-honored model of building assets that become utilities and once they monopolize the utility, they sprinkle the digital ad pixie-dust effectively monetizing the asset that was once free of charge.

They have followed the same road map for Gmail, Google Search, YouTube, and if Waymo can become a utility, prepare from Google digital ads inside the screens of Waymo autonomous cars.

When many sulked that this could be one of those billion-dollar failures that Bezos whined about, Google has decided to supercharge Google Maps by cross-pollinating the power of Google maps with its digital advertising knowhow.

This powerful cocktail of forces working in tandem will accelerate its revenue growth along with the resurgence of its YouTube digital ad revenue.

I believe this new lever of revenue growth isn’t priced into Alphabet shares yet, and withstanding any random black swan shocks to the broader economy, Alphabet is poised to outperform the rest of the trading year.

Short Yelp on any and every rally - Google has made their business model redundant.

Global Market Comments

April 16, 2019

Fiat Lux

Featured Trade:

(WHY YOU WILL LOSE YOU JOB IN THE NEXT FIVE YEARS,

AND WHAT TO DO ABOUT IT),

(BLK)

Global Market Comments

April 15, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR QE IS BACK!),

(SPY), (TLT), (TSLA), (DIS), (FCX), (GOOG), (MSFT), (AMZN)

Let me warn you in advance that I am only going off drugs long enough to write this newsletter.

This year’s flu has finally laid me low and let me tell you it is a real killer. Perhaps it is my advanced age that has magnified its effects. Then I developed an allergic reaction to the flu medicine I was taking. For a couple of days there, I was looking like the Michelin Man.

However, I did have a lot of time to read research. And what I learned was sobering.

For a start, we are fully back to a quantitative easing market. In one fell swoop, the Fed went from an expectation of four interest rate hikes in 2019 to none. By ending quantitative tightening early, it has cut the amount of cash it is withdrawing from the financial system from $4.3 trillion to only $1.5 trillion.

The Fed is in effect reflating the bubble one more time. And what do you do in a QE-driven economy. YOU BUY EVERYTHING! This explains why stocks, bonds, commodities, and energy have all been marching upward in unison this year even though that is supposed to be theoretically impossible.

Yes, the decade long liquidity-driven bull market may have another leg up to go.

A higher high inevitably leads to a lower low. The trades you are executing now may be akin to picking up pennies in front of a steam roller. We are clearly planting the seeds of the next financial crisis. But for now, the pain trade is clearly to the upside.

Those of who who traded through the dotcom bubble are seeing déjà vu all over again. Huge money-losing tech companies are now floating IPOs on a daily basis. This too will end in tears, which is why I have recommended to followers to avoid all of them. This is a sucker’s game.

There is a cloud behind this silver lining. After a ballistic 21.43% move in the Dow Average in four months, markets are trading as if risk is a thing of the past. The euphoria is here and complacency rules. That means the number of new possible low risk/high return trades out there has fallen to zero.

There is another cloud to worry about. The more excess stimulus the Fed provides the economy now, the fewer resources it will have to get us out of the next recession, which might be only a year off. As a result, everyone is long but extremely nervous. They are still participating in the party but are standing next to the exit door. Pent up volatility is building like a volcano ready to explode.

The other great revelation is that markets have been trading extremely short term in nature, only one quarter ahead of what the real economy is doing. So, a stock market meltdown in Q4 2018 discounted a collapsing GDP growth in Q1 2019 of a 1% rate or less. That is down 80% from a year ago peak.

The ultra-strong market in Q1 is anticipating an economic rebound in Q2, After that, who knows?

That’s why I am moving both of my trading portfolios for Global Trading Dispatch and the Mad Hedge Technology Letter to 100% cash positions in the coming week.

Last week was the week when Walt Disney (DIS) morphed from being a has-been media stock hobbled by a failing holding in ESPN to a dynamic company that is suddenly taking over the world. The reward was an eye-popping 25% move in three weeks, which we caught.

Copper demand is rocketing, off of soaring global electric car production. Each vehicle needs 22 pounds of the red metal, and 4 million have been built so far. That number reached 5 million by June. Take a second bite of the apple with (FCX) as well.

General Electric got slaughtered again, with an earnings downgrade from Morgan Stanley. It will take years to sort out this mess. Avoid (GE).

The 30-year fixed rate mortgage plunged to 4.03% and may save the spring selling season for residential real estate.

Apple Topped $200. It looks like the market is finally buying the services story. Stand aside for the short term. It’s had a great run, up 42% from the December low. I’m waiting for 5G until I buy my next iPhone, probably next year.

The Mad Hedge Fund Trader hit a new all-time high briefly, up 15.46% year to date, and beating the pants off the Dow Average. Good thing I didn’t buy the bearish argument. There’s too much cash floating around the world. However, my downside hedges in Disney and Tesla cost me some money when I stopped out. I was late by a day.

We are taking profits on a six-month peak of 13 positions across the GTD and Tech Letter services and will wait for markets to tell us what to do next.

April is so far down -1.50%, as my downside hedges in Tesla (TSLA) and Disney (DIS) cost me some sofa change. My 2019 year to date return retreated to +13.92%, paring my trailing one-year return back up to +27.22%.

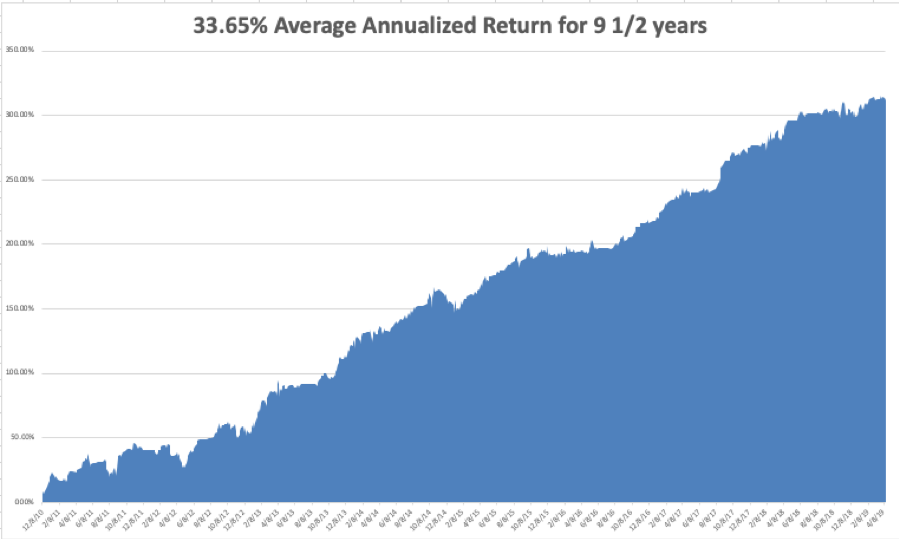

My nine and a half year return backed off to +314.06%. The average annualized return appreciated to +33.65%. I am now 100% in cash.

The Mad Hedge Technology Letter has gone ballistic, with an aggressive and unhedged 30% long which expires this week. It is maintaining positions in Microsoft (MSFT), Alphabet (GOOGL), and Amazon (AMZN), which are clearly going to new highs.

It’s going to be a dull week on the data front after last week’s fireworks.

On Monday, April 15 at 8:30 AM, we get the April Empire State Index. Citibank (C) and Goldman Sachs (GS) report.

On Tuesday, April 16, 9:15 AM EST, we learn March Industrial Production. Netflix (NFLX) and IBM (IBM) report.

On Wednesday, April 17 at 2:00 PM, we get the Fed Beige Book Indicators. Morgan Stanley reports (MS).

On Thursday, April 18 at 8:30 the Weekly Jobless Claims are produced. At 10:00 AM EST, we obtain the March Index of Leading Economic Indicators. American Express (AXP) reports.

On Friday, April 19 at 8:30 AM, the markets are closed for Good Friday.

As for me, I am staying planted in my bed reading up on research and watching HBO until I kick this flu. After that, I should be good for the rest of the year.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

April 11, 2019

Fiat Lux

Featured Trade:

(THE MEANS TO A FRIGHTENING END)

(AMZN), (FB), (GOOGL), (AAPL)

Death of websites.

I love doing presentations to small businesses on my free time, partly to stay in touch with the pulse of the Davids who have the unenviable task of fighting uphill against the Goliaths.

It’s bad enough that the tech giants have scaled locally turning one’s local playground into a disadvantage.

The presentation is aptly titled "Content is King... But Only Through One’s Ownership" where the same parallels are explored and unpacked for my audience.

Proprietary Content – must be yours and you must own it on your own turf - your blog, your vlog, your app, and so on, it goes for everything.

Repurposing content on other platforms as a supplement to your own is one thing, but the moment you adopt an enemy platform as your main platform, that’s your coup de grâce.

SMEs (small businesses enterprise) believe it’s plausible to work with the higher ups, but don’t forget they have every incentive to cut you off from the fountain of youth.

One could say the best skill big tech has today is undermining their competition.

Facebook doesn’t allow posting content that criticizes Facebook, have you ever wondered why?

Website innovation has grinded to a halt because of the PageRank algorithm from Google, everybody is making websites the same, a top nav, descriptive text, a smattering of images and a handful of other elements arranged similarly.

Google’s algorithms and the self-regulating nature of their ecosystem have perverted the chance to have a unique online experience.

Most internet users have probably discovered that most websites don’t work well and the execution of them is lousy.

Many companies are not contributing enough resources to build out their site properly, or just don’t have the cash to fund it or a mix of the two.

About 95% of customer service calls originate from the company’s webpage because of payment problems, disfunction, misleading content, or simply because the website is down.

Ask any small business and they will tell you they deal with their domain being down for hours at a time because of some unknown server problem.

Not only is capitalism only working for a small group of Americans, but so are websites, such as massive companies like Amazon.com who have worked wonders with its e-commerce site.

Because the internet and namely websites are the key to building businesses, Silicon Valley is now using the concept of websites and their position as de-facto moderators to prevent others from developing proper websites, killing off the competition.

Alphabet is notorious for ranking their own products at the top of page one of any Google search.

Amazon has followed the same practice by sticking their in-house brands at the top of any Amazon search on Amazon.com.

And remember that none of this can be called “antitrust” because these borderline tactics offer consumers lower prices but that is only because consumers are brainwashed to believe Amazon offers the lowest price.

What if the same products are available for half of Amazon’s in-house brands, would Amazon volunteer to post their in-house brands on the second page, the graveyard of search results?

I would guess no.

Websites used to give businesses a chance, remember in the mid-90s when a website of any ilk was impressive as if someone was walking on water.

What can we expect next?

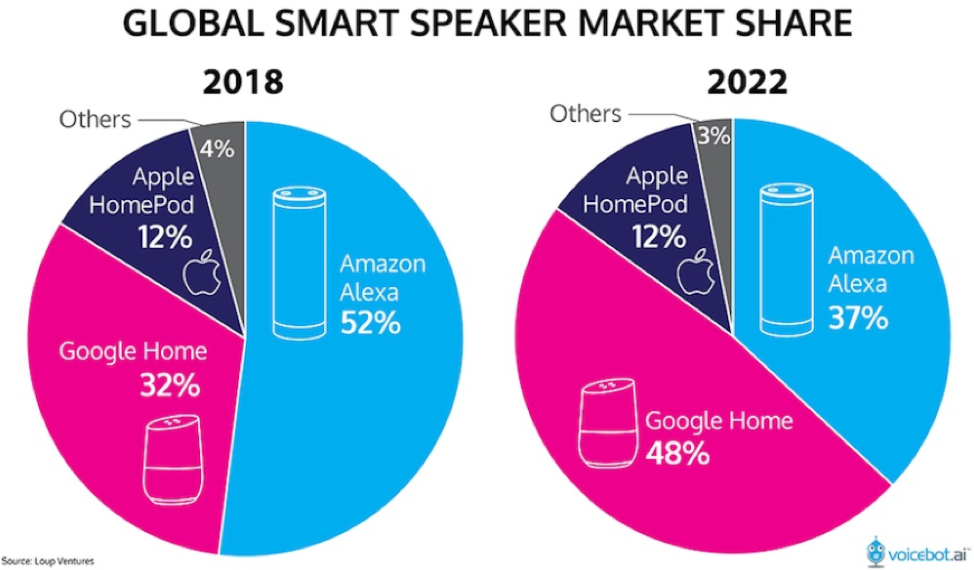

Amazon, Google, and Apple are taking their shows to artificial intelligence voice platforms.

SMEs could at least throw hail marys on standard internet searches with visual screens, but once content migrates over to voice platforms owned by Silicon Valley, then its game, set, and match.

For instance, a local business such as Joe’s Furniture Moving Business who, with the internet and visual screens, is searchable through search engines and can be even located on Google Maps with a concrete address.

Once we migrate the lions share of content to voice platforms over the next 15 years, Google Home, Apple HomePod, or Amazon Alexa could easily choose to remove Joe’s Furniture Moving Business information because they make more money offering you information of a moving service they own or have a stake in.

The advent of 5G will refine the voice technology and enhance the machine learning techniques needed to complete the migration of content.

Once the world crosses an inflection point where the technology and volume of content on smart speakers outweigh the hassle to use a keyboard or mobile screen, this effectively makes these smart speaker manufacture Gods of the World because they will own the voice-based internet.

They will be the gatekeepers of all global information, business, and development in the world and we will need to satisfy their algorithms to get our own content uploaded on their voice platforms.

And because of the nature of voice, users cannot see what else is out there, users will only hear what these companies tell us offering an outsized opportunity to manipulate the user experience generating more dollars for these powerful platforms.

By the end of 2019, 74 million Americans will be using smart speakers, giving these smart speaker firms adequate data to fine tune their products.

Eventually, all Americans will be forced to use it or will not be able to function, similar to the effects of a laptop, email, and smartphone combination now.

Once these voice platforms become ubiquitous, websites will be deemed irrelevant – consumers will simply have a choice of Google Home, Amazon Alexa, and Apple HomePod and blindly trust what they tell you is in your best interests.

Pick your poison.

That’s right, users won’t control content in about 15 years, a scary thought, and now you understand why these companies will even give their voice A.I. platforms for free if they have to and probably will in the future.

Global Market Comments

April 5, 2019

Fiat Lux

Featured Trade:

(APRIL 3 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (VIX), (TSLA), (BA), (FXB), (AMZN), (IWM), (EWU)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader April 3 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: I’ve gotten a lot of newsletters but not many trades. Why is that?

A: Perfect trades do not happen every day of the year. They happen a few times a year and they tend to bunch up. Most time in the market is spent waiting for an entry point and then piling on 5 or 10 trades rapidly. We’re letting our profits run and waiting for new trades to open up, so just be patient and we’ll get you more trades than you can chew on.

If you have to ask this question, you are probably overtrading. The goal is to make yourself rich, not your broker. The other newsletters that offer a trade alert every day don’t publish their performance as I do and lose money for their followers hand over fist.

Q: Are we on track for a market peak in May?

A: Yes; if we keep climbing up, eventually hitting new highs this month, then we are setting up perfectly for a pretty sharp pullback around May 10th. That would be a good time to get rid of all your longs and put on some short positions, certainly deep in the money put spreads—we’ll be knocking quite a few of those out in the end of April/beginning of May.

Q: Are you worried about the Russell 2000 (IWM) climb?

A: I’m not. If you look at the chart, every up move has been weak, and every down move has been strong. Looking at the chart, it’s still in a clear downtrend dragging all the other markets, and this is because small-cap stocks do poorly in recessions or market pullbacks.

Q: How severe and how long do you see the coming bear market being?

A: If history repeats itself, then it’s going to be rather shallow. The last move down was only three months long and that stunned a lot of people who were expecting a more extreme pullback. I don’t see conditions in place that indicate a radically deep pullback—25% at most and 6-12 months in duration, which won’t be enough to liquidate your portfolio and justify the costs of getting out now and trying to get back in later. They key thing is that there are no systemic threats to the market other than the exploding levels of government borrowing.

Q: If you had the Tesla (TSLA) April $310-$330 vertical bear put spread, would you keep it?

A: Probably, yes, because you have a $15 cushion against a good news surprise and a lot less at risk. I got out of my Tesla (TSLA) April $300-$320 vertical bear put spread because my safety cushion shrank to only $5 and the risk/reward turned sharply against me.

Q: Should we be buying the Volatility Index (VIX) here for protection?

A: Not yet; we still have enough momentum in the stock market to hit all-time highs. After that, you really want to start looking at the VIX hard, especially if we get down to the $12 level. So good thinking, just not quite yet—as we know in the market, timing is everything.

Q: Are you getting nervous about the short Disney (DIS) calls?

A: I’m always nervous, every day of the year about every position, and yes, I’m watching them. You are paying me to be nervous so you can go play golf. We may take a small hit on the calls if the stock keeps rising, but that will be offset by a bigger gain on the call spread we’re long against.

Q: When is the quarterly option expiration?

A: It was on March 15 and the next one is June 21. This is an off-month expiration coming up on April 18th, and that’s only 12 trading days away.

Q: If you get a hard Brexit (FXB) in the next few weeks, what will happen to the pound?

A: It’s risen about 10% in the last few weeks on hopes of a Brexit outright failure. If that doesn't happen, the pound will get absolutely slaughtered.

Q: If China (FXI) is stimulating their economy, will that eventually help the U.S.?

A: Stimulus anywhere in the world always gets back to the U.S. because we’re the world’s largest market. So, yes, it will be positive.

Q: Would you consider trading UK stocks under Brexit fail?

A: Yes, and there is a UK stock ETF, the iShares MSCI United Kingdom ETF(EWU) and you’re looking at a 20%-25% rise in the British stock market if they completely give up on Brexit or just have another election.

Q: What are your thoughts on the China trade war?

A: The Chinese are in no rush to settle; that’s why we keep missing deadline after deadline and all the positive rumors are coming from the U.S. side. It’s looking more like a photo op trade deal than an actual one.

Q: If we get a top in stocks in May, how far do you expect (SPY) to go?

A: Not far; maybe 5% or 10%, you just have to allow all the recent players who got in to get out again, and if the economy slows to, say, a 1% rate in Q1, that’s not a panicky type market. That’s a 10% correction market and what we’ll probably get. If the economy then improves in Q2 and Q3, then we may go back up again to new highs. We seem to have a three quarter a year stock market and therefore, a three quarter a year stock market. Q1 is always a write off for the economy.

Q: Do you still like Amazon (AMZN)?

A: Absolutely, yes—it’s going to new highs. And it’s also starting to make a move on the food market, cutting prices at Whole Foods, which it owns, for the 3rd time this year. So, it’s moving on several fronts now, including healthcare. There’s at least a double in the company long term from these levels, and a triple if they break the company up.

Q: If you bought the stock in Boeing (BA) instead of the option spread, would you stay long?

A: I would, yes. It’s a great company and there's an easy 10% move in that stock once they get the 737 MAX back off the ground again which they should do within the month.

Q: What do you think about food stocks with big name brands like Hershey (HSY)?

A: I’ve never really liked the food industry. It’s really a low margin industry. You’re looking at 2% a year earnings growth against the big food companies vs 20% a year growth in tech which is why I stick with tech. My advice is always to focus on the few sectors that are the best 5% of the market and leave the dross for the index funds.

Q: With the current bullish wave in the market (SPY), what sector/stocks do you think have the most momentum to break out another 10% to 15% gain in the next one to three months?

A: The next 10% to 15% in the market will only happen after we drop 5-10% first. I believe this is the last 5% move of the China trade deal rally and after that, markets will fall or go to sleep for six months.

Q: Do you expect 2019 to be more like 2018 or 2017? We know you are predicting the (SPX) will hit an all-time high of 3000 in 2019. Do you think it zooms up to a blow-off top in Q2/Q3 and then pulls back in Q4, like 2018? Or, do you expect a steadier ascent with minor pullbacks along the way (like 2017), closing at or near the year's highs on Dec 31? This guidance will really help.

A: I think we have made most of the gains for 2019. Only the tag ends are lifted. We have already hit the upside targets for most strategists, and mine is only 7% higher. After that, there is a whole lot of boring ahead of us for 2019 and the (VIX) should drop to $9. After complaining about horrendous market volatility in December, traders will beg for volatility.

Good Luck and Good Trading

John Thomas

CEO & Publisher

Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

April 3, 2019

Fiat Lux

Featured Trade:

()

(GOOGL), (NFLX), (AMZN)