Mad Hedge Technology Letter

February 28, 2019

Fiat Lux

Featured Trade:

(WHY ETSY KNOCKED IT OUT OF THE PARK),

(ETSY), (AMZN), (WMT), (TGT), (JCP), (M)

Mad Hedge Technology Letter

February 28, 2019

Fiat Lux

Featured Trade:

(WHY ETSY KNOCKED IT OUT OF THE PARK),

(ETSY), (AMZN), (WMT), (TGT), (JCP), (M)

I wrote to readers that I expected online commerce company Etsy to “smash all estimates” in my newsletter Online Commerce is Taking Over the World last holiday season, and that is exactly what they did as they just announced quarterly earnings.

To read that article, click here.

I saw the earnings beat a million miles away and I will duly take the credit for calling this one.

Shares of Etsy have skyrocketed since that newsletter when it was hovering at a cheap $48.

The massive earnings beat spawned a rip-roaring rally to over $71 - the highest level since the IPO in 2015.

Three catalysts serving as Etsy’s engine are sales growth, strength in their core business, and high margin expansion.

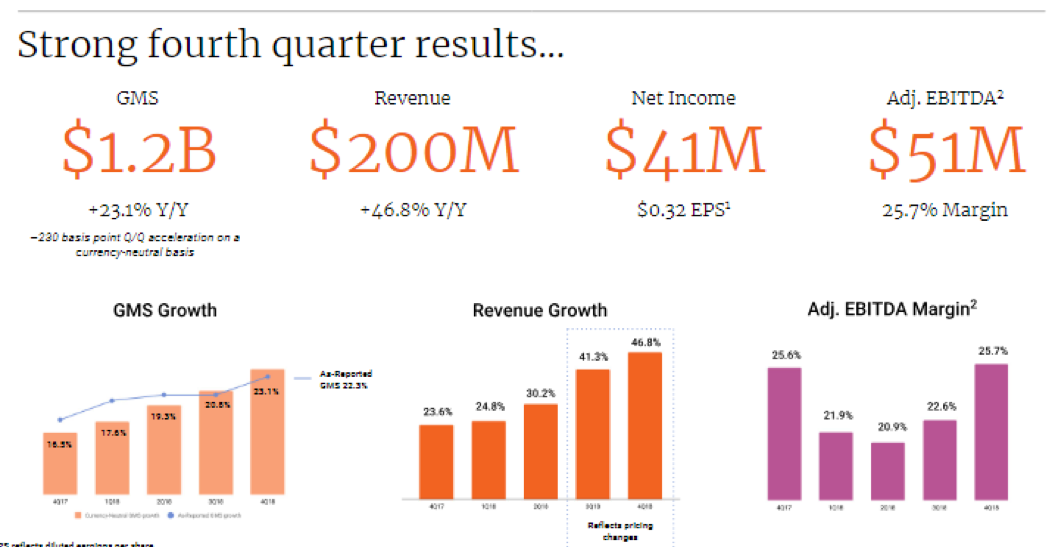

Sales growth was nothing short of breathtaking elevating 46.8% YOY – the number sprints by the 3-year sales growth rate of 27% signaling a firm reacceleration of the business.

The company has proven they can handily deal with the Amazon (AMZN) threat by focusing on a line-up of personalized crafts.

Some examples of products are stickers or coffee mugs that have personalized stylized prints.

This navigates around the Amazon business model because Amazon is biased towards high volume, more likely commoditized goods.

Clearly, the personalized aspect of the business model makes the business a totally different animal and they have flourished because of it.

Active sellers have grown by 10% while active buying accounts have risen by 20% speaking volumes to the broad-based popularity of the platform.

On a sequential basis, EPS grew 113% QOQ demonstrating its overall profitability.

Estimates called for the company to post EPS of 21 cents and the 32 cents were a firm nod to the management team who have been working wonders.

Margins were healthy posting a robust 25.7%.

The holiday season of 2018 was one to reminisce with Amazon, Target (TGT), and Walmart (WMT) setting online records.

Pivoting to digital isn’t just a fad or catchy marketing ploy, online businesses harvested the benefits of being an online business in full-effect during this past winter season.

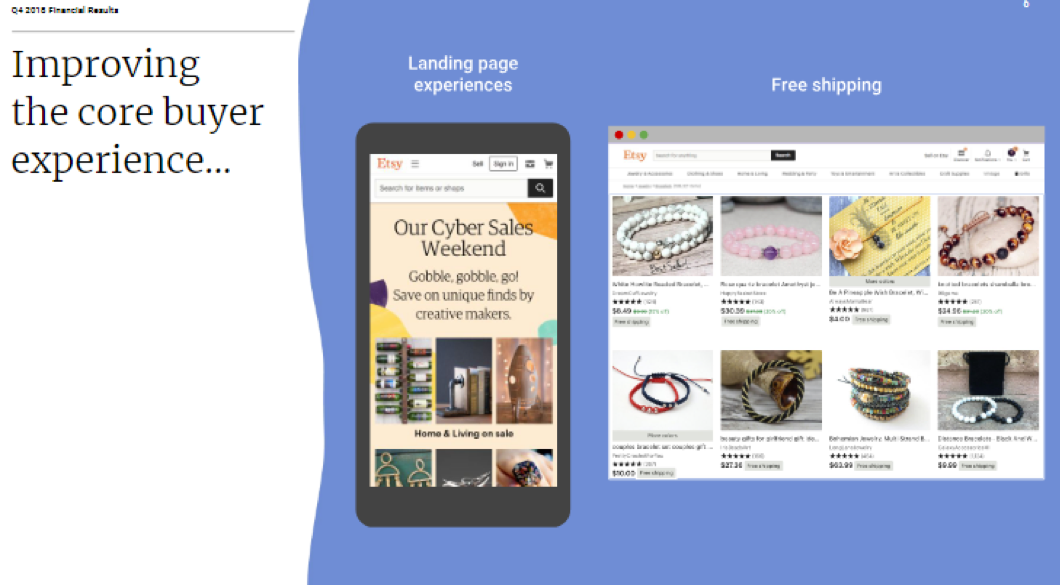

Etsy’s management has been laser-like focusing on key initiatives such as developing the overall product experience for both sellers and buyers, enhancing customer support and infrastructure, and tested new marketing channels.

Context-specific search ranking, signals and nudges, personalized recommendations, and a host of other product launches were built using machine learning technology that aided towards the improved customer experience.

New incremental buyers were led to the site and returning customers were happy enough to buy on Etsy’s platform multiple times voting with their wallet.

The net effect of the deep customization of products results in unique inventory you locate anywhere else, differentiating itself from other e-commerce platforms that scale too wide to include this level of personalization.

Backing up my theory of a hot holiday season giving online retailers a sharp tailwind were impressive Cyber Monday numbers with Etsy totaling nearly $19,000 in Gross Merchandise Sales (GMS) per minute marking it the best single-day performance in the company’s history.

Logistics played a helping hand with 33% of items on Etsy capable to ship for free domestically during the holidays which is a great success for a company its size.

This wrinkle drove meaningful improvements in conversion rate which is evidence that product initiatives, seller education, and incentives are paying dividends.

Overall, Etsy had a fantastic holiday season with sellers’ holiday GMS, the five days from Thanksgiving through Cyber Monday, up 30% YOY.

Forecasts for 2019 did not disappoint which calls for sustained growth and expanding margins with GMS growth in the range of 17% to 20% and revenue growth of 29% to 32%.

Execution is hitting on all cylinders and combined with the backdrop of a strong domestic economy, consumers are likely to gravitate towards this e-commerce platform.

Expanding its marketing initiatives is part of the business Josh Silverman explained during the conference call with Etsy dabbling in TV marketing for the first time in the back half of 2018, and finding it positively impacting the brand health metrics particularly around things like intending to purchase.

However, Etsy has a more predictable set of marketing investments through Google that offers higher conversion rates and the firm can optimize to see how they can shift the ROI curve up.

Etsy can invest more at the same return or get better returns at the existing spend from Google, it is absolutely the firm's bread and butter for marketing, particularly in Google Shopping, and some Google product listing ads.

With all the creativity and reinvestment, it’s easy to see why Etsy is doing so well.

Online commerce has effectively splintered off into the haves and have-nots.

Those pouring resources into innovating their e-commerce platform, customer experience, marketing, and social media are likely to be doing quite well.

Retailers such as JCPenney (JCP) and Macy’s (M) have borne the brunt of the e-commerce migration wrath and will go down without a fight.

Basing a retail model on mostly physical stores is a death knell and the models that lean feverishly on an online presence are thriving.

At the end of the day, the right management team with flawless execution skills must be in place too and that is what we have with Etsy CEO Josh Silverman and Etsy CFO Rachel Glaser.

Buy this great e-commerce story Etsy on the next pullback - shares are overbought.

Mad Hedge Technology Letter

February 26, 2019

Fiat Lux

Featured Trade:

(WHY THE BIG PLAY IS IN SOFTWARE),

(AMZN), (WMT), (ZEN), (FB), (TWLO)

Buy and hold domestic software companies for dear life because that is what the market is giving you.

Take them with both hands.

These revenue models should revolve around developing the lucrative North American digital consumer markets.

Tech is all about giving you pockets of dispersion and my job to herd you into these pockets of opportunity created by pockets of dispersion.

We have once again been delivered a few more poignant indicators allowing us to gauge the market appetite for certain tech barometers.

Incandescent as can be, recent news of hardware companies planning to bring exorbitant foldable phones to market has me profusely shaking my head.

Huawei announced plans to debut the Mate X foldable 5G smartphone with a price tag of a staggering $2,600.

This followed an announcement by Korean behemoth Samsung to roll out the Samsung's Galaxy Fold and the Koreans plan to sell this luxury product for $1,980.

Chinese Huawei Mate X is 5G-supported and can simply fold into a slimmer 6.6-inch smartphone or unfold into an 8-inch tablet.

This is another case of smart manufacturers overreaching for a market that doesn’t exist and shouldn’t exist.

I believe the demand for screen-related smart products at this price point is scant at best.

If you compare foldable phones to a $600 high-tier Samsung Android smartphone with a 6-inch screen, Samsung and Huawei would need to convince consumers the extra $1,500 or in Samsung’s case, $2,200 is worth the extra relative wad of cash.

My bet is that these foldable phones aren’t worth even $300 more of aggregated incremental value let alone $500 and for many consumers like me, it’s worth zilch.

In no way, aside from the gimmick of buying one of these novelties, does buying a foldable phone justify the price.

This is another example of the common-sense factor that has been completely absent from a product cycle.

Product viability and product desirability do not walk hand in hand.

The screen-related smart device market is saturated, evident by the elongated refresh cycle in smartphone usership.

Blame the expensive price tags of over $1,000 and the removal of carrier subsidies that have caused the upgrade cycle to skyrocket from 2.39 years in 2016 to 2.83 years in late 2018.

Then there is the touchy issue of cannibalizing other hardware product lines as many of the potential foldable phone customers might interchange the foldable phone with normal smartphones.

This all screams bad strategy with companies saddled in a glut of inventory.

It takes R&D years to follow through and develop the technology to bring it to market, and it is entirely conceivable this could become a big write-off.

If price cuts happen shortly after the debut, prospects look bleak.

In general, consumer sentiment has soured for more of this type of tech. Many people are just exhausted from screen time and the cycle of the newest hardware screens is failing to excite existing customers bases.

The only conclusion I can make is that tech today is about software, software, and particularly domestic software.

If you compare software to hardware head to head now, software functionality is still increasing 15% YOY juicing up efficiency and productivity.

What will foldable phones offer a digital nomad or working professional?

Not much.

It highlights the absence of a productivity or functionality boost that digital device users are scouring for now.

Stay away from hardware.

Why is domestic software preferred over international software that scales the earth five times around?

Regulation.

It has reared its ugly head again.

The avalanche of negative headlines applied to American big tech is finally becoming a self-fulfilling prophecy.

It was only a matter of time until someone took note, and in this case, various Asian governments have taken note.

In a bid to blunt American tech’s first mover advantage, the Indian government has written up a draft of regulatory measures in order to make the Indian tech landscape a fairer playground.

This will have the intended effect of creating a national powerhouse of tech firms employing local people.

India has effectively taken a page out of China’s playbook using home-field advantage to nurture homegrown talent.

Large American tech companies have made India a playground of binge investments lately with Amazon (AMZN) shelling out $5 billion and Walmart (WMT) brazenly pouring $15 billion into e-commerce heartthrob Flipkart.

This is awful news for them.

They will have to adjust to India’s new-found zeal for digital regulation and a heavy restructuring of the business model could be in the cards in 2019 along with higher costs of running these businesses.

India has followed China in its footsteps demanding data to be localized meaning data centers won’t be able to run and store Indian data abroad.

American participants will have no other choice but to pony up the extra costs.

Readers might forget that India is the current battleground of global tech growth and Amazon will not have unfettered market access like they did breaking into Europe and dominating e-commerce from the start.

Amazon and Walmart can thank Facebook (FB) which has been the main culprit in bringing wave after monstrous wave of heavy criticism on a whole industry.

Facebook has effectively brought forward the regulatory storm that otherwise would have happened a few years later down the road.

In any case, this makes life harder for data-oriented companies who wish to navigate hazardous foreign tech climates.

Domestic angst against local tech has given the rubber stamp for full-on data government mandates abroad from India to Vietnam.

What does this all mean?

In 2019, data regulation could shrink expected growth levers while hardware companies are becoming even more desperate as these Hail Marys could quickly turn into liabilities.

I nailed software picks Zendesk (ZEN) and Twilio (TWLO) amongst others from a strong group of enterprise software stocks.

Twilio’s performance could potentially become my best pick of 2019, it’s on a straight line up even with all this clutter and chaos around the world.

Global Market Comments

February 22, 2019

Fiat Lux

Featured Trade:

(FEBRUARY 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(NVDA), (MU), (AMD), (LRCX), (GLD), (FXE), (FXB), (AMZN),

(PLAY IT SAFE WITH ANTHEM), (ANTM), (CI)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader February 20 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: If there is a China trade deal, should I buy China stocks, specifically Alibaba?

A: To a large extent, both Chinese and US stocks have already fully discounted a China trade deal, so buying up here could be very risky. The administration has been letting out a leak a day to support the stock market, so I don’t think there will be much juice left when the announcement is actually made. The current high levels of US stocks make everything risky.

Q: Is it time to buy NVIDIA (NVDA)?

A: The word I’m hearing from the industry is that you don’t want to buy the semiconductor stocks until the summer when they start discounting the recovery after the next recession (which is probably a year off from this coming summer). The same is true for Micron Technology (MU), Advanced Micro Devices (AMD), and Lam Research (LRCX).

However, if you’re willing to take some heat in order to own a stock that’s going to triple over the next three years, then you should buy it now. If you’re a long-term investor, these are the entry points you die for. Looking at the charts it looks like it is ready to take off.

Q: Should I be shorting the euro (FXE), with the German economy going into recession?

A: No. We’re at a low for the euro so it’s a bad time to start a short. It’s interest rates that drive the euro more than economies. With the U.S. not raising interest rates for six months, maybe a year, and maybe forever, you probably want to be buying the currencies more than selling them down here.

Q: Would you buy the British pound (FXB) on Brexit fears?

A: I would; my theory all along has been that Brexit will fail and the pound will return to pre-Brexit levels—30% higher than where we are at now. I have always thought that the current government doesn’t believe in Brexit one iota and are therefore executing it as incompetently as possible.

They have done a wonderful job, missing one deadline after the next. In the end, Britain will hold another election and vote to stay in Europe. This will be hugely positive for Europe and would end the recession there.

Q: What do we need to do for the market to retest the highs?

A: China trade deal would do it in a heartbeat. If this happens, we will get the 5% move to the upside initially. Then we’re looking at a double top risk for the entire 10-year bull market. That’s when the short players will start to come in big time. You’d be insane to new positions in stocks here. There is an easy 4,500 Dow points to the downside, and maybe more.

Q: Do you think earnings growth will come in at 5%, or are they looking to be zero or negative?

A: Zero is looking pretty good. We know companies like to guide conservative then surprise to the upside; however, with Europe and China slowing down dramatically, that could very well drag the U.S. into recession and our earnings growth into negative numbers. The capital investment figures have been falling for three months now. US Durable Goods fell by 1.2% in January.

This explains why companies have no faith in the American economy for the rest of this year. This was a big reason why Amazon (AMZN) abandoned their New York headquarters plans. They see the economic data before we do and don’t want to expand going into a recession.

Q: When will rising government debt start to hurt the economy?

A: It already is. Foreign investors have been pulling their bids for fear of a falling US dollar. They have also become big buyers of gold (GLD) in order to avoid anything American, so we have a new bull market there. In the end, the biggest hit is with business confidence.

Nothing good ever comes from exploding US deficits and companies are not inclined to invest going into that. That is a major factor behind the sudden deterioration in virtually all data points over the past month.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

February 20, 2019

Fiat Lux

Featured Trade:

(WALMART’S DRAMATIC SAVE),

(WMT), (AMZN)

This is not your father’s Walmart (WMT).

Peel back a layer or two of that thin veneer and in Walmart, you have nothing closely resembling the Walmart you grew up with.

This would have been a coup de grâce for many companies facing the tsunami of tech strength crushing business models left and right.

Yet, Walmart has found a way to turn the tables and flourish when many industry experts thought this once legacy shopping business was careening towards extinction.

Walmart’s outstanding performance of growing e-commerce sales 43% YOY in the winter quarter of 2018 is a proclamation that they are here to stay through hell or high water and it’s the e-commerce segment leading the charge.

Betting the ranch on e-commerce has them inevitably on a collision course heading directly towards competitor Amazon (AMZN).

Instead of shriveling up and waving the white flag, Walmart’s President and CEO Doug McMillon is acutely aware that the overall pie is growing and there is room for more than just Amazon.

His company’s recent success echoes this trend of the overall marketing growing, and I believe passing the acid test of the 2018 winter shopping season is concrete evidence that Walmart has a prosperous future if they can navigate around four objectives.

First, triple-down on the e-commerce strategy which could translate into being a tad cavalier to operating margins.

This would take a machete to short-term profitability, but I believe Walmart investors are starting to believe in this tech pivot and further margin erosion can be stomached because they are currently conditioned for it.

To capture a larger footprint in the e-commerce market, data analytics specialists will need to be recruited in heavy numbers and convinced of the future vision of Walmart.

The turn of the calendar year means that end of the year bonuses are out and now is the time to capture the horde of tech talent sitting on the open market waiting to be put on Walmart’s books.

Walmart could potentially leap into position to nab some of these tech high flyers who specialize in Python and SQL programming languages. The demand for these wizards is insatiable and the key to any corporate digital migration strategy.

Second, being able to penetrate the target audience a notch above than what Walmart is traditionally accustomed to.

This would correlate into higher average spend per Walmart transaction which would become a feedback loop into Walmart carving out higher-grade product line-ups to compensate increasingly pressured margins.

Third, enhance the logistics and fulfillment strategy by automating more of the business process through robotics and a streamlined IT department.

Walmart has been in the process of scaling out this portion of the business process and they are probably the only one that can pull this off because of the gigantic addressable market and flowing access to capital.

Fourth, originate an educational program coaching up spendthrift customers on how to access its products digitally.

Investors must remember that a large swath of Walmart’s customers aren’t at the top of the socioeconomic ladder and seamlessly culling them into the digital orbit is a responsibility shouldered on upper management.

The goal is to gradually migrate every type of order variant online or through self-checkout means, and self-navigating through these payment and service barriers could be a hindrance as Walmart’s customer base is less tech-savvy than Amazon’s prime subscription customer base.

However, the smaller digital native customer base on a percentage basis is offset by the 4,700 physical stores allowing these partially digital-savvy customers to click and collect.

I view the click and collect distribution channel as a bridge towards becoming fully digital and if Walmart can provide superior customers service, this cohort will likely stick with Walmart’s full-service digital offerings in the future once they upgrade.

In the distant future, it’s almost guaranteed these physical stores end up as fulfillment centers with robotic automation or some type of mix of the two.

Walmart is starting to get serious looks as an e-commerce powerhouse, and I have consistently described Walmart as the next FANG. This latest earnings report reinforces this thesis.

I champion some of the moves to add to product lines such as online brands Art.com and female garment retailer Bare Necessities.

If Walmart could whip up an in-house brand similar to Amazon Basics, that would also be a gamechanger. That step is down the road and Walmart would need to accumulate higher expertise to convert certain products from the 3rd party variety.

Another growth inducer would be establishing a subscription-based service similar to Amazon Prime. Software as a subscription (SaaS) is all the rage in technology and for all the right reasons as this recurring revenue is a boon for the CFO and stabilizes finances.

The Arkansas-based firm forecasted e-commerce annual sales growth of 35% and indicated that huge sums of capital would be allocated into remodeling store units, reinforcing the e-commerce platform, and juicing up its supply chain operations.

Walmart is only scratching the surface and it would take a debacle of epic proportions or a massive recession crimping product demand to knock off Walmart from this high-speed train of positive momentum.

Yes, I agree this company isn’t even close to Amazon now, but the catch-up potential and that path to catch up is clear as daylight.

There is no need to chase shares at this price, but I can say that Walmart is on the verge of locking itself up at the $100 price point as an eternal support level moving forward.

If shares sell off to $90 because of the recent buying from oversold conditions, it could be one of the last times ever to secure a price that cheaply for a precious FANG company.

The company is also famous for continuously raising its dividend.

Walmart is an intriguing stock for the rest of 2019, particularly if the momentum snowballs from here.

Global Market Comments

February 19, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or ALARM BELLS ARE RINGING)

(SPY), (TLT), (GLD), (AMZN)

There is not a single hedge fund manager out there today who doesn’t believe that stock markets are on the verge of a very sharp selloff.

Earnings are falling. Europe is tipping into recession. The money supply is shrinking at a dramatic pace (see chart below). And government borrowing will double this year as compared to last. Yet the major indexes are 5% of an all-time high with valuations at an 18X multiple, the high end of the historic range.

You may be wondering why a correction, if not a new bear market, hasn’t already started yet. Every trader on Wall Street is nervously awaiting a China trade deal, possible weeks away, that they can all sell into, including me. The China negotiations have robbed traders of a decent short side entry point for a year now.

You may think I am being excessively cautious with these views. However, US equity mutual funds have suffered eleven straight weeks of outflows worth $80 billion, an all-time record. You really wonder what is supporting the market here. Are we in for a “Wiley Coyote” moment?

Who is left to buy the market? Short coverers, algorithms, and corporations buying back their own shares. There are in effect no real net investors.

One can’t help but notice the constantly worsening in the economic data that took place last week. Was this all happening in response to the December stock market crash? Or is it heralding a full-blown recession that has already started?

This is all backward-looking data, in some cases as much as two months. But what followed the December crash? The January government shut down which we already know pared 75 basis points off of Q1 GDP growth. That’s why companies announced middling earnings for Q4 but horrendous guidance for Q1.

December Retail Sales came in at a disastrous ten-year low. If you’re looking for an early recession indicator, this is a big one. Maybe it’s because the prices are falling so fast?

The NY Fed slashed Q1 GDP estimates to below 2% with more cuts to come. Trade war uncertainty cited as the number one reason.

Consumer Spending is slowing. That means the recession is near. Fund managers are universally moving into defensive and value stocks. So, should you.

Car Sales fell at the fastest rate in a decade, as US Manufacturing Output drives off a cliff. There is also a subprime crisis going on here, if you haven’t heard.

Amazon (AMZN) told New York City to drop dead as it canceled plans to build a second headquarters in New York, thanks to opposition from a local but vociferous minority. Some 25,000 jobs went down the toilet. More likely, they don’t want to expand their business right ahead of a recession. Jeff Bezos can see into the future infinitely better than you and I can.

You have to take Jeff’s thoughts seriously. Amazon added more square feet in the US than any other company last year, bringing the total to 288 million square feet. That is a staggering 28 World Trade Centers. Do they know something we don’t?

In the meantime, American Personal Debt is soaring, hitting a new apex at $13.5 trillion. Some 9.1% of this is already delinquent, and credit cards are being canceled at an alarming pace.

Business Confidence hit a two-year low, and Consumer Confidence hits an eight-year low. It seems a government shutdown and a stock market crash are not good for business. Now that stocks are up, will confidence return?

Inflation hit a one year low, with the Consumer Price Index coming in at only 1.9%. It means the next recession will bring deflation.

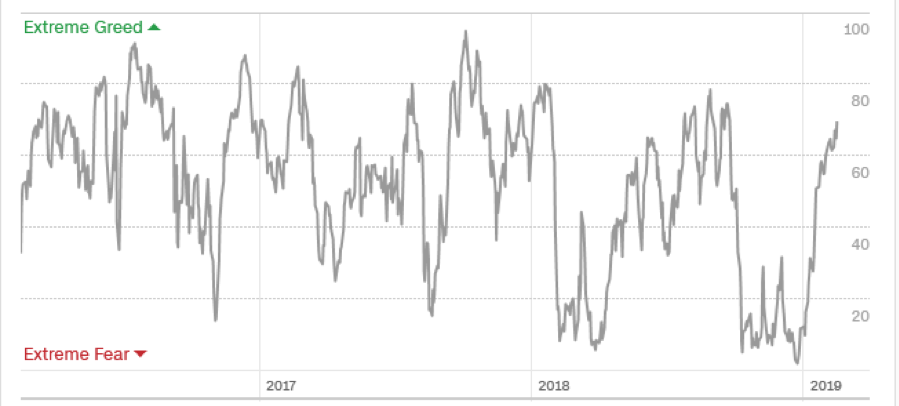

The Mad Hedge Market Timing Index is entering danger territory with a reading of 70 for the first time in five months. Better start taking profits on those aggressive leveraged longs you bought in early January. Your best performers are about to take a big hit. The market has since sold off 500 points proving its value.

There wasn’t much to do in the market this week, given that I am trying to wind my portfolio down to 100% cash as the market peaks.

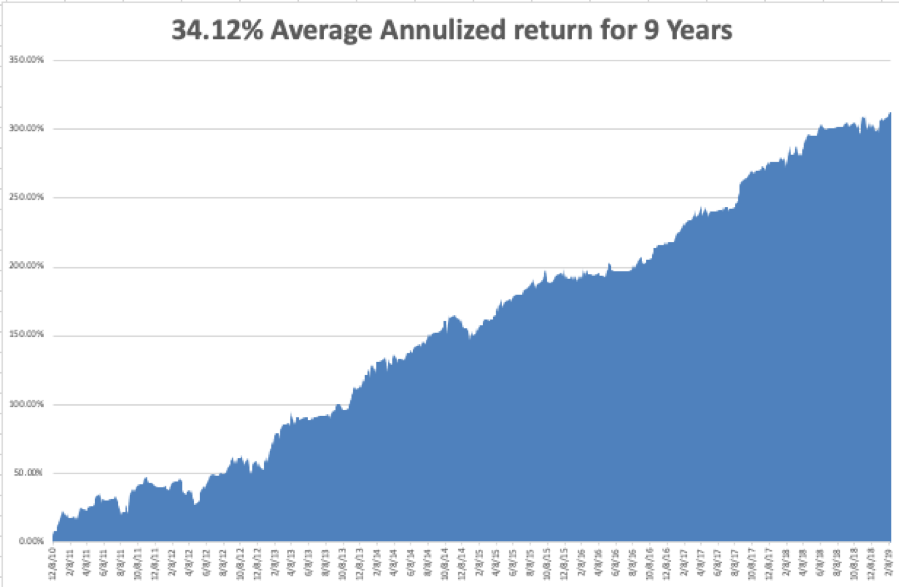

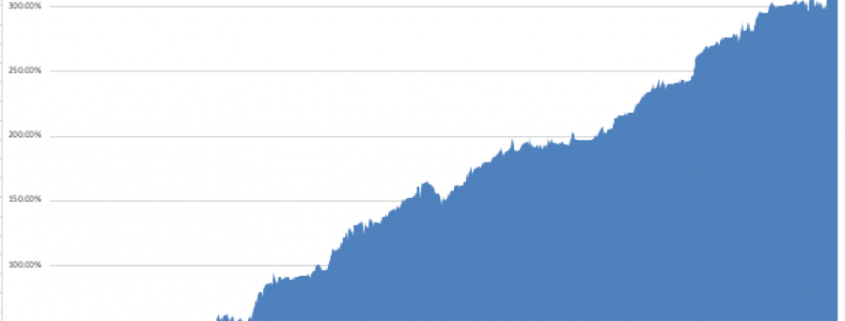

February has so far come in at a hot +3.31%. My 2019 year to date return leveled out at +12.79%, boosting my trailing one-year return back up to +34.12%.

My nine-year return clawed its way up to +312.93%, another new high. The average annualized return ratcheted up to +34.12%.

I am now 90% in cash and 10% long gold (GLD), a perfect downside hedge in a “RISK OFF”. We have managed to catch every major market trend this year, loading the boat with technology stocks at the beginning of January, selling short bonds, and buying gold (GLD).

Government data is finally starting to trickle out now that the government shutdown is over.

On Monday, February 18 was Presidents Day and the markets were closed.

On Tuesday, February 19, 10:00 AM EST, the Homebuilders Index is released.

On Wednesday, February 20 at 2:00 AM EST, Minutes from the January FOMC meeting are released. How dovish are they really?

Thursday, February 21 at 8:30 AM EST, we get Weekly Jobless Claims. At 10:00 AM, Existing Home Sales are out.

On Friday, February 22, there will be a half a dozen public Fed speakers suggesting that interest rates will go up, down, or sideways. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’ll be digging out from the massive series of snowstorms that hit me at my Lake Tahoe Estate. Snowfall this season has so far hit 50 feet and is challenging the 70-foot record from three years ago.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader