Global Market Comments

September 28, 2018

Fiat Lux

Featured Trade:

(WHAT WILL TRIGGER THE NEXT BEAR MARKET?)

(JPM), (SNE), (TLT), (ELD), (AMZN),

(WEDNESDAY, OCTOBER 17, 2018, HOUSTON

GLOBAL STRATEGY LUNCHEON)

Global Market Comments

September 28, 2018

Fiat Lux

Featured Trade:

(WHAT WILL TRIGGER THE NEXT BEAR MARKET?)

(JPM), (SNE), (TLT), (ELD), (AMZN),

(WEDNESDAY, OCTOBER 17, 2018, HOUSTON

GLOBAL STRATEGY LUNCHEON)

To paraphrase Leo Tolstoy in Anna Karenina, all bull markets are alike; each bear market takes place for its own particular reasons.

Now that the wreckage of the past financial crises is firmly in our rearview mirror, it is time for us to start pondering the causes of the next one. I’ll give you a hint: It will all boil down to excessive debt…again.

Global quantitative easing has been going on for a decade now, keeping interest rates far too low for too long. The unintended consequences will be legion, and the day of atonement may be a lot closer than you think.

The 1991 bear market was prompted by the Savings & Loan Crisis, where too many unsophisticated financial institutions in a newly unregulated world dreadfully mismatched asset and liabilities.

Every time I drive by a former Home Savings and Loan branch, with its unmistakable quilt decorations and accents, I remember those frightful days. Back then, when I looked at buying a home in San Francisco, the seller burst into tears when the price I offered would have generated a negative equity bill due for him.

The 2000 Dotcom crash can easily be explained by the monstrous amounts of debt provided to stock speculators. The 2008 crash was produced by massive, unregulated, and largely unknown lending to the housing sector through complex derivatives that virtually no one understood, especially the buyers.

So, here we are in 2018 nearly a decade out of the last crisis. Potential disasters are lurking everywhere under the surface while blinder constrained investors blithely power ahead. Once they metastasize, they rapidly feed into each other, creating a domino effect. They always do.

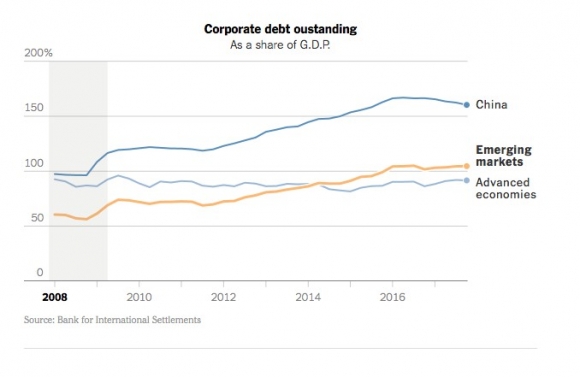

Emerging Market Debt

Lacking domestic capital markets with any real depth, companies in emerging economies prefer to borrow in U.S. dollars. When the dollar is weak that’s great because it means liabilities on the balance sheet shrink when brought back into the home currency. When the greenback is strong, the opposite happens. Dollar debt can grow so large that it can wipe out a company’s total equity.

This is already happening in a major way in Turkey, where the lira has plunged 50% in the past year, effectively doubling their debt. And once it starts, a global contagion kicks in as all emerging companies become suspect. This is not a small problem. Emerging market debt has rocketed from 55% to 105% of GDP since 2008.

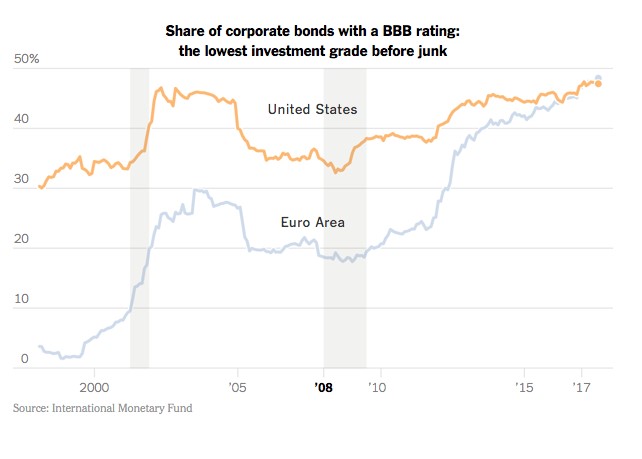

The Rise of Junk Borrowers

In recent years there has been a massive expansion in borrowing by marginal credits. This is taking place because fixed income investors are willing to accept a large increase in the amount of risk for only a small marginal rise in interest rates.

There is now $1.4 trillion in low grade BBB bonds outstanding, with one-third of this one downgrade away from junk. There has also been a dramatic rise in “covenant lite” issuance, which minimizes the rights of bond holders in the event of default. When the next round of trouble arrives, you can expect this market to shut down completely, as it did in 2008.

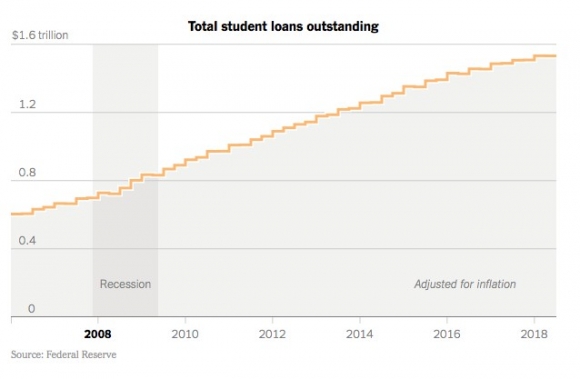

Student Loans

These have been the sharpest rising form of borrowing over the past decade, doubling to $1.5 trillion. Some 10% are now in default. This acts as a major drag on the economy as heavily indebted students don’t borrow, buy homes or cars, or really participate in the economy in any way, banned by lowly FICO scores. This is why millennials in general have been slow to enter the housing market for the first time.

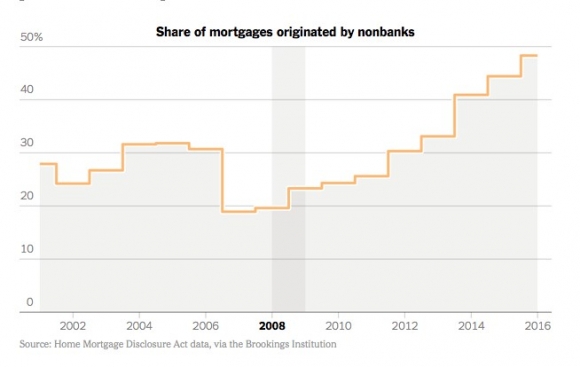

Shadow Banking

Would you like to know today’s equivalent of subprime the lending that took the financial system down in 2008? That would be shadow banking, or off the books, unreported lending by hedge funds, private equity funds, and mortgage companies. Again, this is all in pursuit of high interest rates in a low interest rate world.

Yes, liars’ loans are back, just not to the extent we saw 10 years ago…yet. I’m waiting for my cleaning lady to get offered a great refi package again, just as she was in the run-up to the last crisis. How many of these loans are out there? No one has any idea, especially the Fed. As a result, nearly 50% of all mortgage lending is now from unregulated nonbank sources.

The Outlier

Remember when Sony (SNE) was almost put out of business by a hack attack from North Korea? What if they had done this to JP Morgan (JPM)? That would have created a chain reaction of defaults throughout the financial system that would have been impossible to stop. When this happened in 2008, it took the Fed three months to reopen markets such as commercial paper. If big bankers need a reason to lie awake at night, this is it.

I’m not saying that markets can’t go higher before they go lower. In fact, I dove back into Amazon (AMZN) only this morning.

However, as an Australian farmer told me on my last trip down under, “Be careful when you cross the field, mate. Deadly snakes abound.” Add up all the above and it will turn into a giant headache for investors everywhere.

Mad Hedge Technology Letter

September 26, 2018

Fiat Lux

Featured Trade:

(DID SIRIUS OPEN UP PANDORA'S BOX?),

(SPOT), (P), (SIRI), (AAPL), (AMZN)

In a flurry of deals, the music streaming industries consolidation is powering on as some of the industry’s biggest players have completed new acquisitions.

Is there a new King of the Castle?

Not yet.

In any case, the shakeout still allows Spotify to claim itself as the No. 1 company in the music streaming industry, but Apple (AAPL) and Sirius XM (SIRI) have gained.

There is still work to be done for the trailing duo but it is a step in the right direction.

Apple’s deal with Shazam, which just gained approval, was consummated last December, but was held up by European regulators over antitrust problems.

The Europeans have clamped down on American tech companies of late forcing them to play nicer after decades of running riot inside the region.

The Shazam app analyzes then pinpoints titles from music, movies, and television shows based on a brief sample through the device’s microphone.

If your neighbors are blasting the tunes upstairs at a Friday night shindig and you want to find out what song is causing you to lose sleep at night, just turn on your microphone and upload it into Shazam.

Shazam will tell you exactly the song’s title and the artist’s name.

Even dating back to 2013, this app was among the top 10 most popular apps in the world.

In 2018, Shazam has carved out a user base of more than 150 million monthly average users (MAU) and growing.

Shazam is used more than 20 million times per day.

An opportunity lies in urging Shazam users to then adopt Apple music.

Interestingly enough, to upgrade the quality of the app’s functionality, Apple is stripping away digital ads in Shazam.

Apple has made an unrelenting attempt to avoid introducing lower grade tech that could potentially taint its clean-cut brand.

Recently enough, film producers have complained that Apple is completely averse to any content with gratuitous violence, excessive drug use, and candid sex scenes.

Apple wants to cultivate and sell its pristine image.

Digital ads also fail to make the cut.

This spotless image boosts Apple’s pricing power along with the high quality of products that has seen Apple retain its place as the producer of the best smartphone in the world.

Other smart phone brands are still in catchup mode with a brand image significantly inferior to Apple’s.

And Apple CEO Tim Cook isn’t even interested in monetizing Apple music, and is more focused on “doing the right thing” for it.

Yes, the job of every company is to be in the black, but the No. 1 responsibility for a modern tech company is to grow and grow profusely.

Tech investors pay for growth, period.

As investors have seen with Netflix, companies can always raise prices after seizing market share because of the stranglehold on eyeballs inside a walled garden.

That potent formula has been the bread and butter of powerful tech companies of late.

Spotify is a captive of the music industry, of which it is entirely dependent for its source of goods, in this case songs.

At the same time, the music industry has fought tooth and nail to destroy the likes of Spotify, which benefits immensely from distributing the content it creates.

History is littered with failed music streaming services outgunned in the courtroom. Pandora (P) is the biggest public name out there whose share price has tanked over the long haul.

Pandora has created a proprietary algorithm offering song recommendations to listeners, but it is more or less an online music streaming app heavily reliant on a freemium pricing model with ads.

Sirius XM Holdings, a satellite radio company, signaled its intent in the music streaming business by taking a 19% in Pandora’s business last year.

It has followed that up now by completing a full takeover of the Oakland, California company for $3.5 billion.

This move adds 75 million users to its 36 million usership on Sirius and, in my view, the main objective is an eyeball grab to buy more listeners dragging them into its walled garden.

To triple a user base instantly to 75 million listeners is a boon for Sirius, which now has the firepower to legitimately compete with Spotify.

Pandora has been shopping itself around for the past two years, and companies such as Facebook were whispered to be eyeing this company.

Facebook chose to focus on developing dating and romance functions on its platform, and has mainly ignored the music streaming possibilities.

More critically, it allows Sirius to diversify out of the car space where satellite radio is predominantly used.

As much as Americans love to drive, the home is where they rest, and sleep, and Pandora will unlock a path into the home of listeners.

Synergies between home audio through Pandora, and car audio through Sirius should be evident over time.

The music streaming industry, such as the television streaming industry, has become fiercely competitive as of late. And this is a prudent move for Sirius to buy a new customer base at the same time as moving into the home.

The trend of tech companies penetrating the home and making it as smart as possible is revived constantly.

This piece of news isn’t as earth-shattering as Amazon’s (AMZN) smart home product launch event, but nonetheless indicates another leg up in competition for fresh user growth and its data.

This M&A surge is occurring amid a backdrop of the music industry’s obsession to exterminate Spotify and the other music streaming companies.

They are on a mission to force up the royalties these Internet giants must pay to pad their pockets and protect their interests.

Royalties are the music streaming companies’ main cost, and for Spotify, these royalty payments eat up 78% of total revenue.

But that does not mean Spotify is a bad company or even a bad stock.

Every company has its share of pitfalls. Throw in the mix that Amazon (AMZN) and Apple have music streaming services that do not even need to make a profit, and you will understand why some might be wary about putting new money to work in music streaming business stocks.

The primary reason that Spotify shares will outperform for the foreseeable future is because it is the preeminent music streaming platform.

Also, there is favorable latitude to make way toward the goal of monetization, and ample space to improve gross margins.

Global streaming revenue growth has gone ballistic as the migration to mobile devices and cord cutting has exacerbated the monetization prospects of the music industry.

Streaming revenue was a shade under $2 billion in 2013, and continued to post a growth trajectory of more than 40% each year since.

As it stands now, total global streaming revenue registered just a tick under $7 billion per year in 2017, and that was an improvement of 41.1% from 2016.

The choice among choices is Spotify in 2018.

The company was dogged by many years of famous artists removing their proprietary content from the platform citing unfavorable terms.

Eventually, almost all artists have relented and reinstalled their music on Spotify. They depend on alternative moneymaking avenues to compensate for lack of royalties, mainly live music.

Spotify has seized even more industry power with its new function of completely bypassing the music industry altogether, by offering a way for aspiring artists to directly upload music content onto its online platform.

Crushing the middleman has been a widespread theme in the tech industry for the past few decades, and the music industry is no different.

As technology has hyper-accelerated, the cost of producing music has plummeted giving access to just about anyone who has any talent.

No need to rent a sound studio for thousands of dollars per hour anymore in West Hollywood, and the music industry knows it.

It could be possible that the next cohort of viral artists will never cough over a dime to the music industry, and the bulk of the profits will be collected by a music streaming titan that distributes their content online.

How does Spotify make money?

It earns its crust of bread through paid subscriptions but lures in eyeballs using an ad-supported free version of its platform.

Naturally, the paid version is ad-less, and this subscription is around $5 to $15 per month.

In the second quarter, Spotify’s paid subscription volume surpassed 83 million, a sharp uptick of 40% YOY.

Ad-supported users came in at more than 101 million, even under the damage that General Data Protection Regulation (GDPR) did to western tech companies.

The ad-supported subscribers rose 23% YOY, and the paid version expects between 85 million to 88 million paid subscribers in the third quarter.

Many of the new paid subscribers are converts from its free model.

Spotify is poised to increase revenue between 20% to 30% for the rest of 2018.

The rise of Spotify's developing data division could extract an additional $580 million of revenue in 2023, making up 2% of total revenue.

When Spotify did go public, the robust price action was with conviction, making major investors - such as China’s Tencent, which possess a 9.1% stake and Tiger Global Management, which owns 7.2% - happy stakeholders.

In the last quarter’s earnings report, Spotify CFO Barry McCarthy reiterated the company’s goal to push gross margins from the mid-20% range to “gross margins in the 30% to 35% range.”

A jump in gross margins would go a long way in making Spotify appear more profitable, and that is the imminent goal right now.

Bask in the glow of the growth sweet spot Spotify finds itself in right now.

For the time being, the music division of Amazon and Apple are just a side note, even with Apple’s purchase of Shazam.

But Apple is vigorously improving its service products as its software and services segment moves from strength to strength, but that doesn’t particularly mean Apple Music.

Investors must sit on their hands to see how Sirius’s acquisition of Pandora plays out. These are by no means two extraordinary companies, and a major overhaul is required to make these two mediocre companies into one overperformer.

If you had to choose among Sirius, Pandora, or Spotify, then cautiously leg into a few shares of Spotify to test the waters.

Mad Hedge Technology Letter

September 25, 2018

Fiat Lux

Featured Trade:

(AMAZON’S HOME INVASION),

(AMZN), (GOOGL), (HBB), (PG)

In another resplendent display of corporate expertise, Amazon (AMZN) debuted its stunning new lineup of smart home products aiming to dominate your inside walls.

In total, Amazon gave consumers 15 new devices to dabble with – an unprecedented amount.

Amazon Echo, Amazon’s smart speaker, also received a software update.

Jeff Bezos’ company is traversing where they have never been before, infiltrating the car with the Echo Auto, executing location-based routines such as directing drivers running on a brand-new operating system.

Other products in the shop window were smart devices related to security, a clock, an upgraded Echo Dot, and a microwave.

The biggest nugget delivered in this release event was the advent of the Amazon Echo-on-a-chip – Amazon Connect Kit.

Essentially, it would allow any third-party manufacturer that vies for smart home supremacy to embed an Amazon produced chip into its product and design the architecture around it.

This foray has already turned heads with appliance companies already raving about this new development.

Consumer product companies such as Hamilton Beach (HBB) and Procter & Gamble (PG) are in the midst of engineering its own products centered around the Amazon connect kit.

North America sales and marketing senior vice president at Hamilton Beach Scott Tidey said his company has been “surprised at how easy it is to use the Alexa Connect Kit to prototype devices and create Alexa commands with just a few lines of code.”

In the near future, consumers could be maneuvering around their homes with products possessing a legion of these new Amazon proprietary chips.

Amazon is bent on penetrating your home and turning it into the smart home you always dreamed of, and this is one of the in-roads that will take them to the holy grail.

This hard-charging approach has been effective.

Wait to see which products go viral, then go after market share like crazy.

This approach made the Amazon Kindle a favorite of many tablet goers.

It helps that Amazon products are crafted with intense precision and great attention to detail.

As more consumers devour new Amazon devices, the synergistic effects benefit its comprehensive eco-system.

Once a customer becomes entirely drenched in Amazon products, it becomes the backbone to a customer’s existence.

Ask the millennial generation, and a good portion of them entirely depend on Amazon to fuel their daily routine.

Any replacement services would waste them hours and be a whole lot pricier.

As the voice assistants become widely adopted, it could blow a hole in Google (GOOGL) search.

Google search is still reliant on its desktop search, even though more and more people are migrating to its mobile search platform.

But if Amazon can stay ahead of Google in the voice assistant race, it could supplant Google as the premier search engine.

It might be an existential crisis for Google search and the minions of Google ad tech engineers.

Google is still wholeheartedly reliant on advertisement revenue, which is its profit engine.

Although, the cash cow digital advertisement business has made the company famously rich, regulation is a ticking time bomb, as the government has a bull’s-eye marked at this Silicon Valley mainstay.

Amazon has smartly moved up the value chain of search, and believes voice-activated search will be the revolutionary search function in the next few years.

It’s hard to argue with its prognosis.

Providing enough high-caliber accoutrements that mesh with its voice supported portfolio will expedite adoption and put strenuous pressure on Google to evolve faster.

Even worse, the golden years for digital advertisement have passed and the pressure on margins could exacerbate.

Fighting Amazon would provoke the margin bears and in one fell swoop, Alphabet, which is waiting on Waymo to take off, could get hip-checked by the Seattle-based company.

As the FANGs start to bleed over into each other’s business, these new product events take on a more important meaning.

The Amazon-effect has the tendency to destroy smaller company’s stocks, but going forward, large companies will be just as badly affected as Amazon branches off into new spheres spearheading revolutionary initiatives.

This speaks volumes to the innovation of Amazon, and why the best innovators will always stay one step ahead.

Amazon is rated the No. 1 company by the Mad Hedge Technology Letter and after this stellar debut of various IoT products, it’s hard not to like them even more.

And if Amazon’s connect kit catches fire and Google is forced to concede this hardware to Amazon, it would be a kick in the midsection to Google whose IoT strategy is not sticking as strongly as it would like.

Amazon does not want to co-exist with other companies. However, it smartly concedes certain segments until it is confident in taking that segment over.

This is why Amazon’s in-house brands are starting to wreak havoc on the third-party sellers on its e-commerce platform.

Amazon ingenuously chose to make a microwave because the technology hadn’t changed much in a generation, yet it was in dire need of simplification.

Seize the low-hanging fruit before you tackle the more difficult challenges.

Once Amazon masters the simpler devices in the home, watch out!

The rest of the home will be up for grabs too because of the same reason many companies heed way to Amazon – it does it way better than any other company for a fraction of the cost.

The multiplier effect will be in full force when Amazon finally constructs its shiny new headquarter somewhere outside of Seattle giving Amazon more manpower to fulfill Bezos’ vision.

My bet is that it will be placed smack dab in the middle of Washington D.C. – a stone’s throw away from the White House where Bezos has been increasingly active adding to his army of lobbyists.

With regulation on the verge of breaking social media’s back, Bezos is acutely aware of protecting his assets as if his life depended on it.

Bezos also has a house in Washington and owns the Washington Post.

Amazon doesn’t rest on its laurels because it doesn’t dominate 80% of the Android market, and it must be the aggressor and the disruptor at the same time.

Rolling out 15 smart products blew away the drooling audience and left them befuddled and craving for more.

Amazon must do it another way than Google and its way; the Amazon way, is the winning strategy.

It’s hard to imagine that Google is still reliant on a legacy business to print them money. And as the digital ad industry sinks, Google will sink, too.

Google still hasn’t found the next answer that can marshal it to safe waters.

Its eggs are still in one basket – unlike Amazon.

As Amazon steamrolls the little companies that never had a chance, the threat of them taking out a Google- or a Facebook-size company grows exponentially.

Ironically, Amazon’s digital ad business is set to surpass $4 billion by the end of the year, and it’s not even the main aim for Bezos.

The digital ad business is a side business for Bezos.

His visions are grander and awe-inspiring, and this product rollout affirms this vision.

This is the beginning of something much more powerful. Any investor who thinks Amazon shares are expensive is crazy.

The report of bribery in Amazon’s system and the subsequent short-term weakness in the shares is a great chance to buy Amazon on the dip because this stock is going higher.

Anybody would be a fool to short Amazon.

This company exudes quality, and many would agree with me.

Global Market Comments

September 19, 2018

Fiat Lux

Featured Trade:

(THE QUANTUM COMPUTER IN YOUR FUTURE),

(AMZN), (GOOG),

(WEDNESDAY, OCTOBER 17, 2018, HOUSTON

GLOBAL STRATEGY LUNCHEON)

Mad Hedge Technology Letter

September 19, 2018

Fiat Lux

Featured Trade:

(IBM’S SELF DESTRUCT),

(IBM), (BIDU), (BABA), (AAPL), (INTC), (AMD), (AMZN), (MSFT), (ORCL)

International Business Machines Corporation (IBM) shares do not need the squeeze of a contentious trade war to dent its share price.

It is doing it all by itself.

Stories have been rife over the past few years of shrinking revenue in China.

And that was during the golden years of China when American tech ran riot on the mainland before the dynamic rise of Baidu (BIDU), Alibaba (BABA), and Tencent, otherwise known as the BATs.

Then the Oracle of Omaha Warren Buffett drove a stake through the heart of IBM shares earlier this year by announcing he was fed up with the company’s direction and dumped a 35-year position.

Buffett unloaded all of his shares in favor of putting down an additional 75 million shares in Apple (AAPL) in the first quarter of 2018.

Topping off his Apple position now sees Buffett owning a mammoth 165.3 million total shares in the resurgent tech company.

Buffett’s shrewd decision has been rewarded, and Apple’s stock has rocketed more than 20% since he jovially declared his purchase in May.

IBM has been a rare misstep for Buffett, who took a moderate loss on his IBM position disclosing an average cost basis of $170 on 64 million shares that Berkshire bought in 2011.

IBM has flatlined since that Buffett interview, and slid around 25% since its peak in mid-2014.

IBM is grappling with the same conundrum most legacy companies deal with – top line contraction.

In 2014, IBM registered a tad under $93 billion in annual revenue, and followed up the next three years with even lower revenue.

A horrible recipe for success to say the least.

In an era of turbo-charged tech companies whose value now comprise over a quarter of the S&P, IBM has really fluffed its lines.

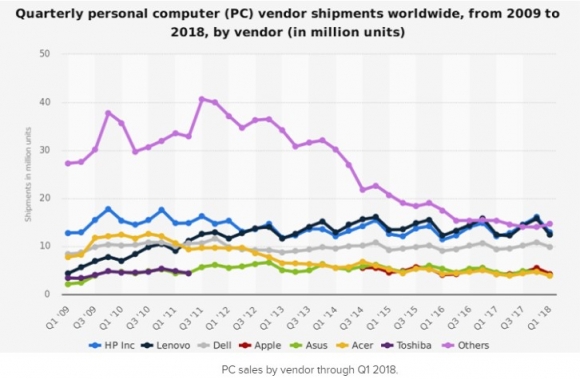

IBM’s prospects have been stapled to the PC market for years.

A recent JP Morgan note revealed the PC market could contract by 5% to 7% in the fourth quarter because of CPU shortages from Intel (INTC).

The report’s timing couldn’t have been worse for IBM.

The PC industry has been tanking for the past six consecutive years unable to shirk shrinking volume.

Intel is another company I have been lukewarm on lately because it is being outmaneuvered by chip competitor Advanced Micro Devices (AMD).

Even worse, this year has been a bad one for Intel’s management, which saw former CEO Brian Krzanich resign for sleeping with a coworker.

The poor management has had a spillover effect with Intel needing to delay new product launches as well.

To read more about my timely recommendation to pile into AMD in mid-August at $19, please click here.

Meanwhile, AMD shares have gone parabolic and surpassed an intraday price of $34 recently.

Investors should ask themselves, why invest in IBM when there are so many other tech companies that are growing, and growing revenue by 20% or more per year?

If IBM does manage to eke out top line growth in 2018, it will be by 1% to 2%, similar to Oracle’s recent performance.

Unsurprisingly, the price action of Oracle (ORCL) for the past year has been flatter than a bicycle ride around Beijing.

Live by the sword and die by the sword.

Thus, the Mad Hedge Technology Letter has been ushering readers into high-performance stocks that will bring technological and societal changes.

If you put a gun to my head and forced me to give sage investment advice, then the answer would be straightforward.

Buy Amazon (AMZN) and Microsoft (MSFT) on the dip and every dip.

This is a way to print money as if you had a rich uncle writing you checks every month.

Legacy tech is another story.

The IBMs and the Oracles of the world are bringing up the tech sector’s rear.

To add insult to injury, the lion’s share of IBM’s revenue is carved out from abroad, and the recent surge in the dollar is not doing IBM any favors.

IBM’s Watson initiative was billed as the savior for Big Blue.

The artificial intelligence initiative would integrate health care data into an actionable app.

The expectations were high hoping this division would drag up IBM from its long period of malaise.

IBM bet big on this division ploughing more than $15 billion into it from 2010-2015, predicting this would be the beginning of a new renaissance for the historic American company.

This game changing move fell on deaf ears and has been a massive bust.

IBM swallowed up three companies to ramp up this shift into the AI world - Phytel, Explorys, and Truven.

The treasure trove of health care data and proprietary analytics systems these companies came with were what this division needed to turn the corner.

These three companies were strong before the buy out and engineers were upbeat hoping Watson would elevate these companies to another level.

Wistfully, IBM Management led by CEO Ginni Rometty grossly mishandled Watson’s execution.

Phytel boasted 160 engineers at the time of IBM’s purchase and confusingly slashed half the workforce earlier this year.

Engineers at the firm even lamented that now, even smaller firms were “eating them alive.”

Unimpressed with the direction of the artificial intelligence division at IBM, many of these three companies’ best and brightest engineers jumped ship.

The inability for IBM to integrate Watson reared its ugly head in plain daylight when MD Anderson Cancer Center in Texas halted its Watson project after draining $62 million.

This was one of many errors that Watson AI accrued.

The failure to quicken clinical decision-making to match patients to clinical trials was an example of how futile IBM had become.

In short, a spectacular breakdown in execution mixed with an abrupt brain drain of AI engineers quickly imploded the prospect of Watson ever succeeding.

In 2013, IBM confidently boasted that Watson would be its “first killer app” in health care.

Internal leaks shined a brighter light on IBM’s subpar management skills.

One engineer described IBM’s management as having “no idea” what they were doing.

Another engineer said they were uncertain of a “road map” and “pivoted many times.”

Phytel, an industry leader at the time focusing on population health management, was bleeding money.

The engineers explained further, chiming in that IBM’s management had zero technical experience that led management wanting to create products that were “simply impossible.”

Not only were these products impossible, but they in no way took advantage of the resources these three companies had at their disposal.

Do you still want to invest in IBM?

Fast forward to today.

IBM is being sued in federal court with the plaintiff’s, former employees at the firm, claiming the company unfairly discriminated against elderly employees, firing them because of their age.

The documents submitted by the plaintiff’s state that “IBM has laid off 20,000 employees who were over the age of 40” since 2012.

This prototypical legacy company has more problems than the eye can see in every nook and cranny of the company.

If you have IBM shares now, dump them as soon as you can and run for cover.

It’s a miracle that IBM shares have eked out a paltry gain this year. And this thesis is constant with one of my overarching themes – stay away from all legacy tech firms with no cutting-edge proprietary technologies and stagnating growth.

________________________________________________________________________________________________

Quote of the Day

“Some say Google is God. Others say Google is Satan. But if they think Google is too powerful, remember that with search engines unlike other companies, all it takes is a single click to go to another search engine,” said Alphabet cofounder Sergey Brin.

Global Market Comments

September 12, 2018

Fiat Lux

THE FUTURE OF AI ISSUE

Featured Trade:

(THE NEW AI BOOK THAT INVESTORS ARE SCRAMBLING FOR),

(GOOG), (FB), (AMZN), MSFT), (BABA), (BIDU),

(TENCENT), (TSLA), (NVDA), (AMD), (MU), (LRCX)