I am writing this to you from Indian Rock Beach, Florida, an extended sand bar outside of Tampa on the west coast. Cabin cruisers pass by every five minutes. There is not much fishing though with rain and temperatures in the low 40s, the coldest of the year. leaving a lot of free time for indoor work. Every building is missing a chunk of wall or roof if not totally destroyed from the October hurricane Helena, including my own Airbnb. The last hurricane here took place in 1921.

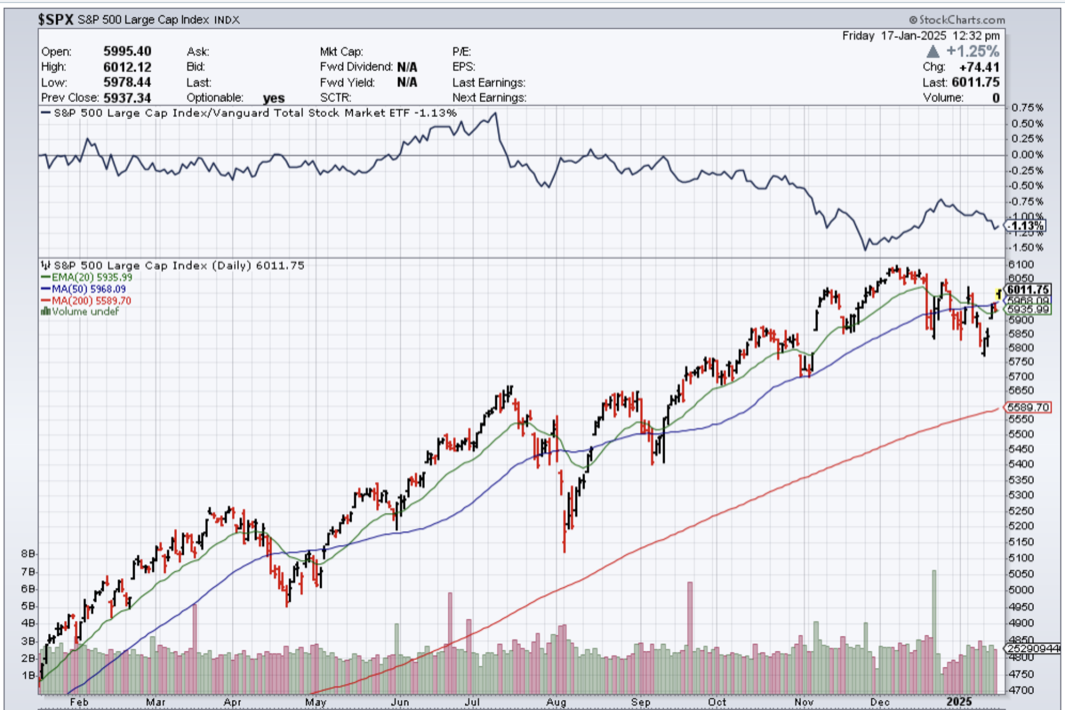

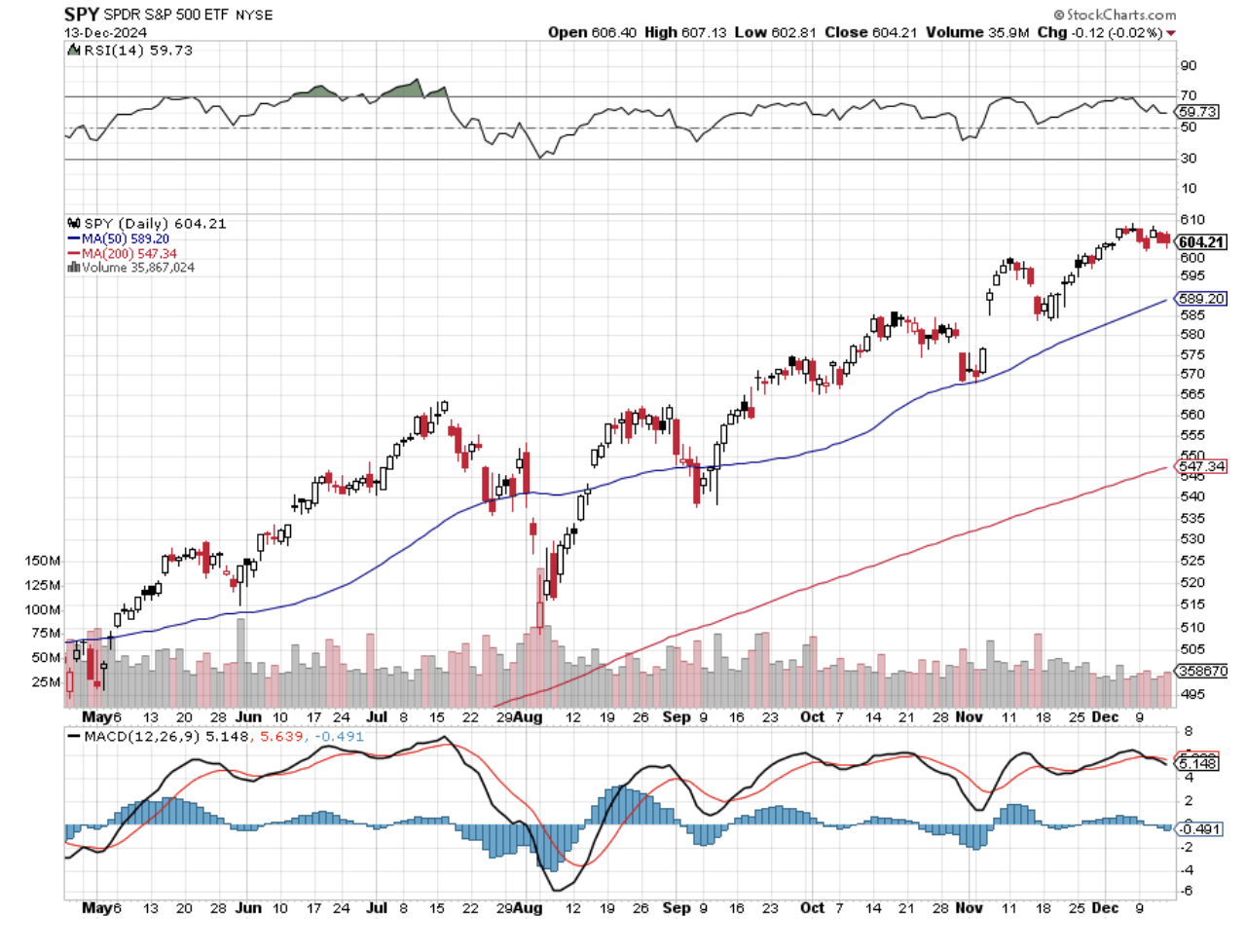

Everywhere I look, hedge fund managers are derisking, cutting exposure, and laying on hedges. The reason is that no one has a handle on what is going to happen in financial markets in the short term. Do we go up, down, or nowhere? The rapid unwind of the post-election rally has put the fear of markets back in them once again.

There is also a rare shortage of news in the financial media. It’s as if someone is sucking all the oxygen out of the room.

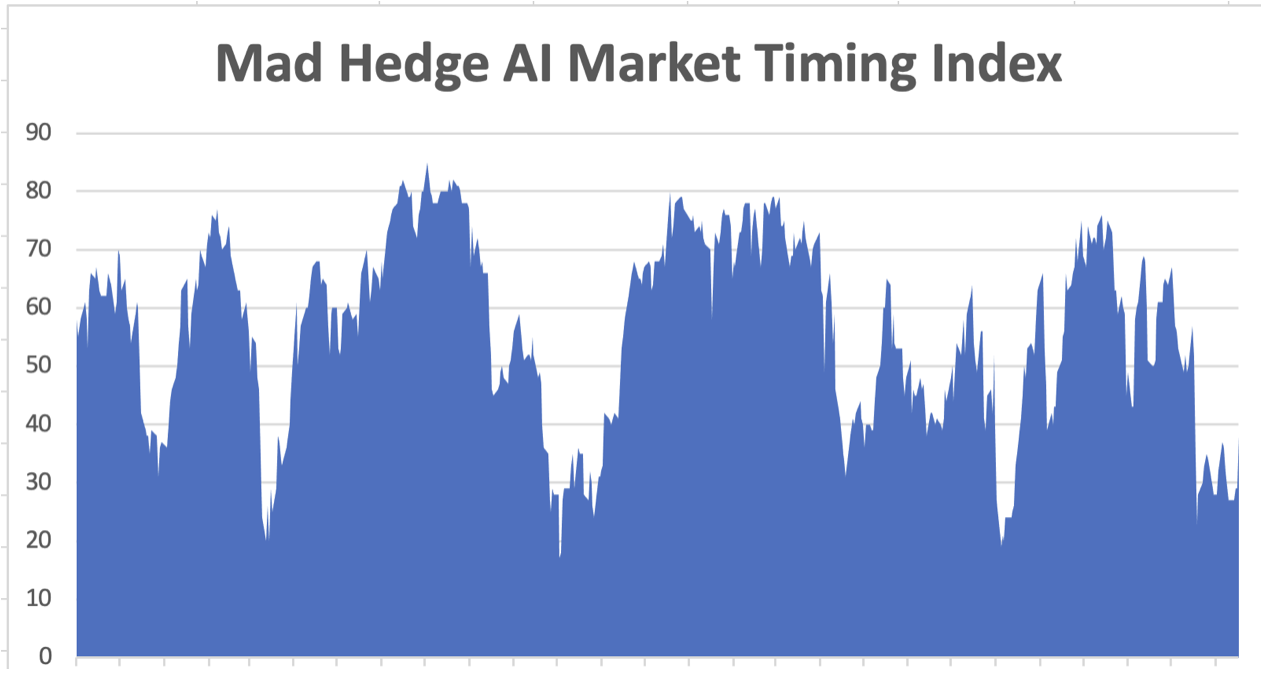

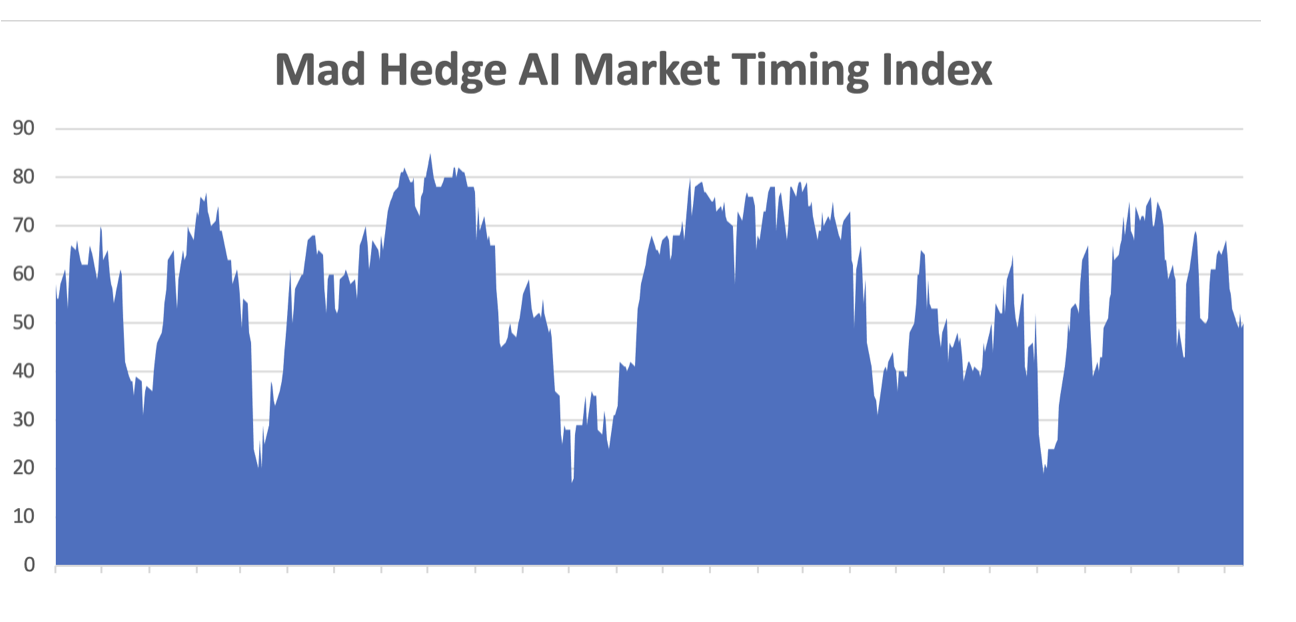

We had about a week where the Mad Hedge Market Timing Index in the mid-twenties was enticing us back into the market. I was expecting a hot December Consumer Price Index to give us a nice selloff and the perfect entry point I had been waiting a month for, in line with all the economic warm data of the last three months.

But it was not to be. The CPI printed at a cool 2.9% YOY and the Dow Average opened up 700 points the next morning, the first step in a 1,700-point three-day rally. Half the December losses came back in a heartbeat.

So much for the great entry point.

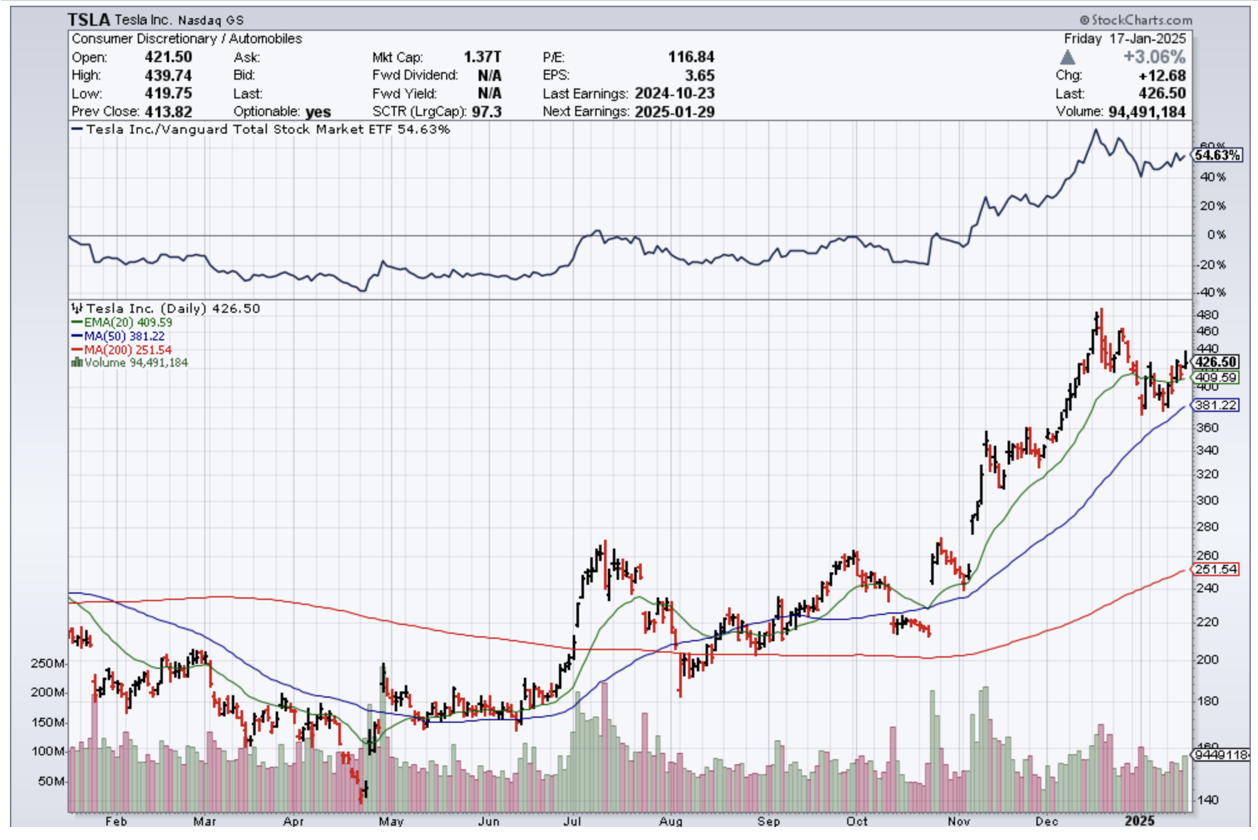

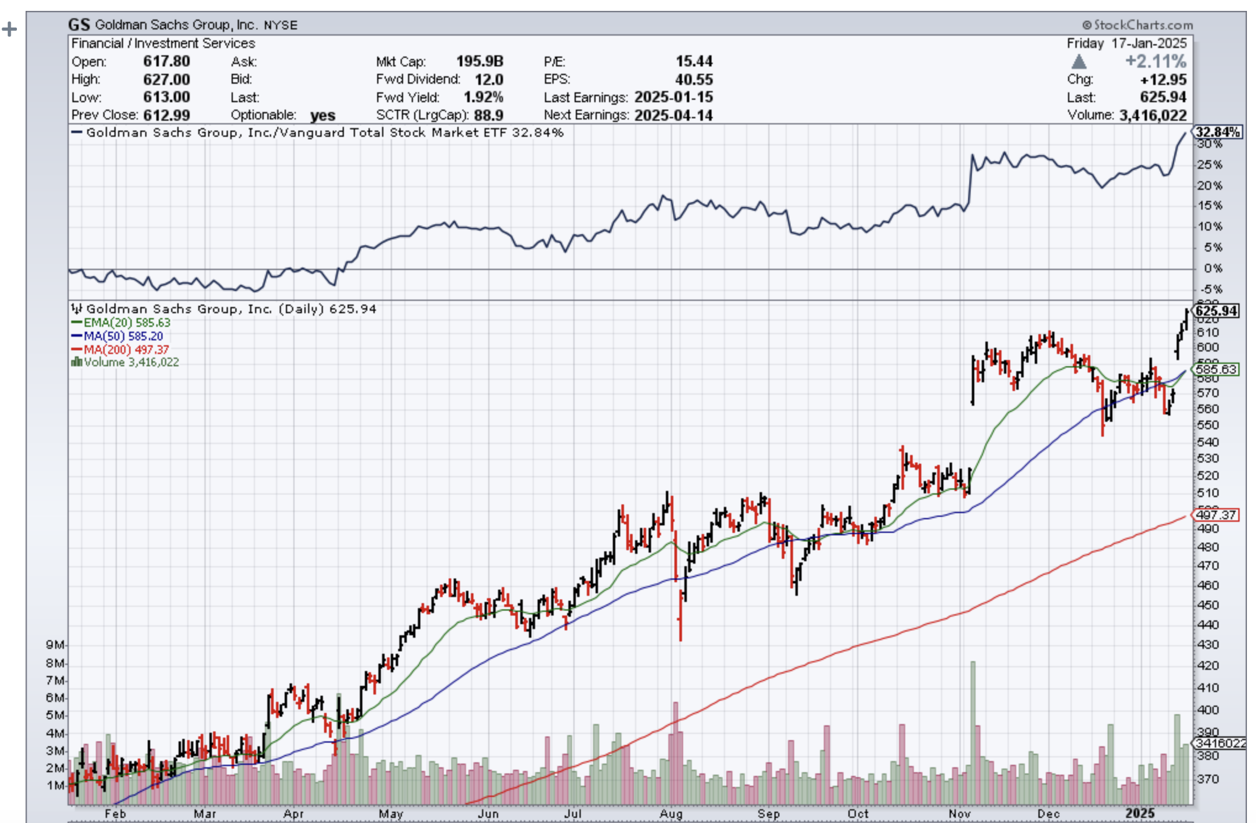

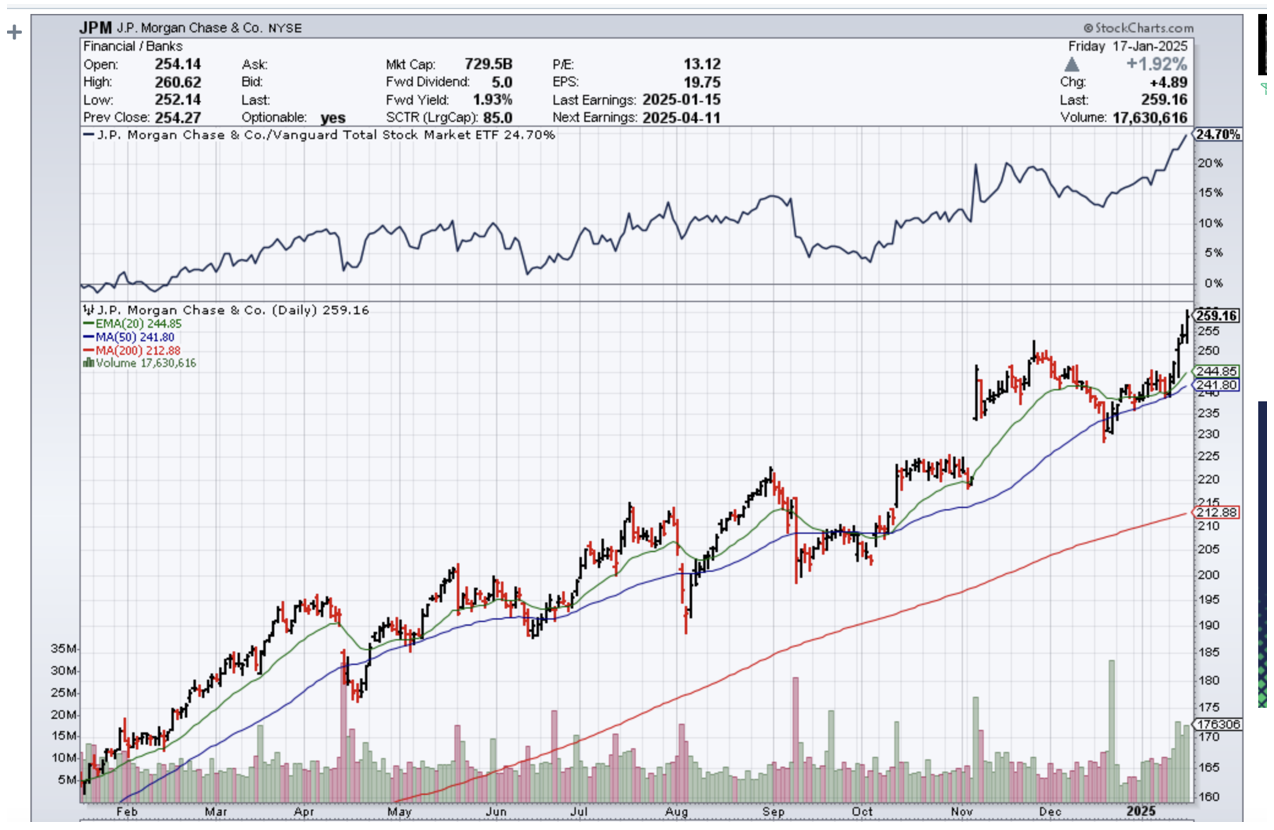

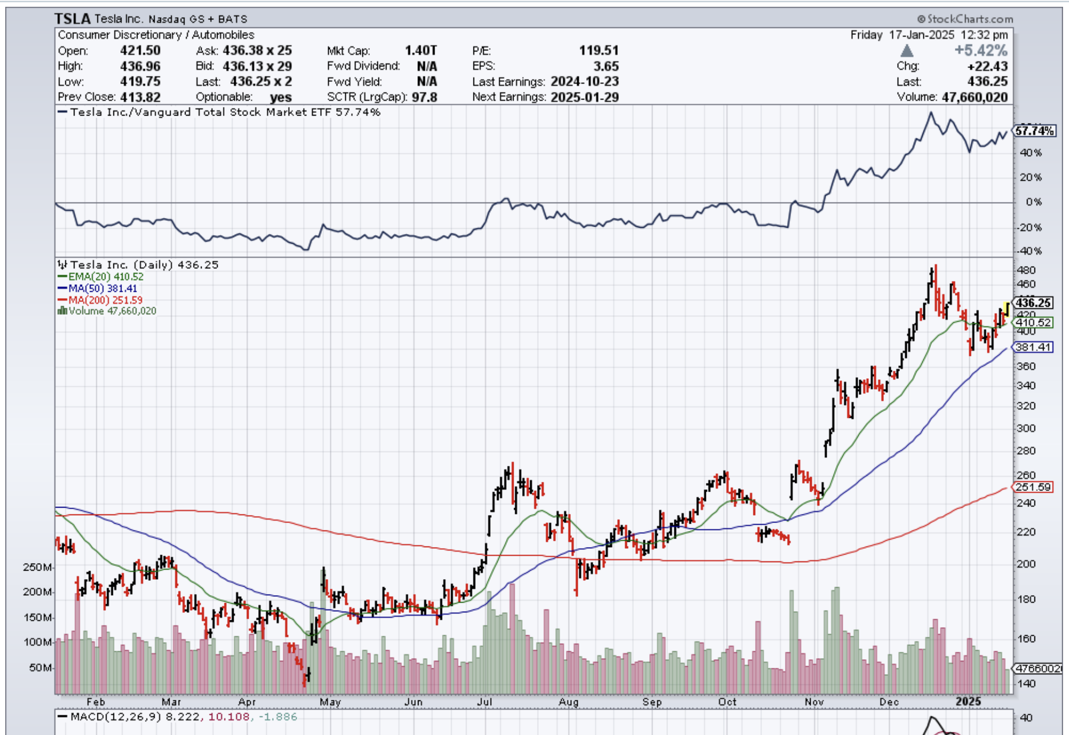

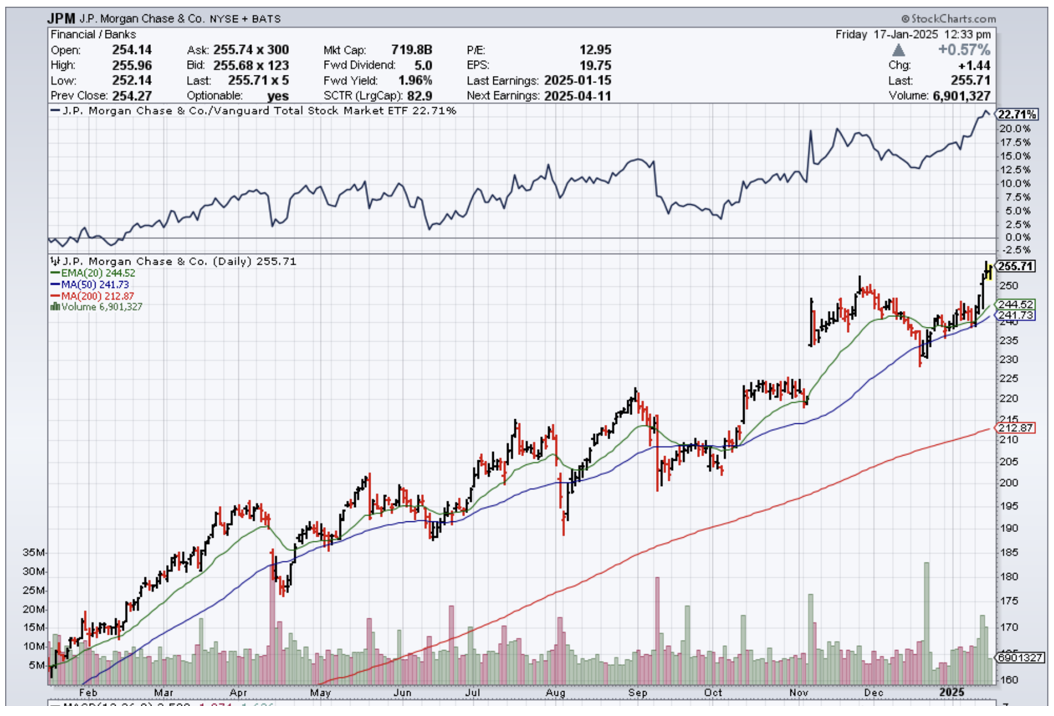

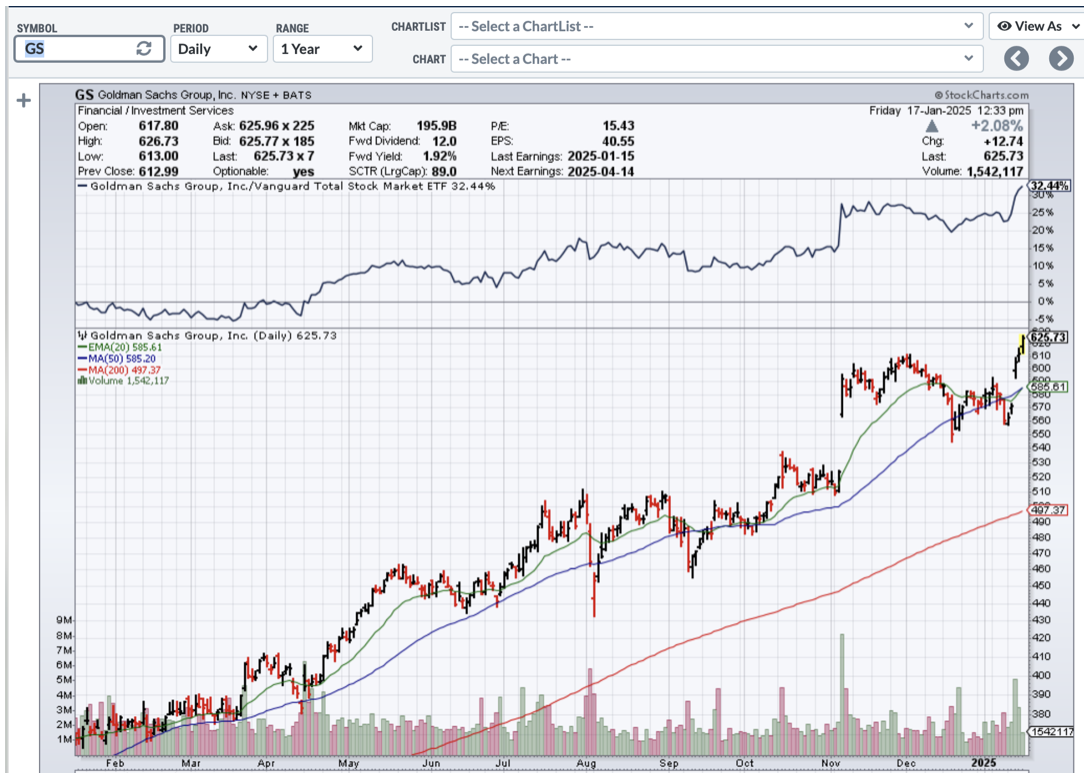

All of my target stocks like (GS), (MS), (JPM), (C), and (BAC) went ballistic. I only managed to get into a long in Tesla (TSLA) because the implied volatility was a sky-high 70%. That way, the stock could take a surprise hit and I still would have a safety cushion large enough to eke out the maximum profit by the February 20 option expiration. What’s next? How about a $100 in-the-money bearish Tesla put spread, once the rally burns out?

I can’t remember a time when there was such a narrow field of attractive trading targets. Rising interest rates have killed off bonds, foreign currencies, precious metals, and real estate. A weak China has destroyed commodities and energy, with US overproduction contributing to the latter. Only financials look interesting for the short term and big tech for the long term.

At that point, financials are not exactly undiscovered investments, but they should have another three months of life in them. That’s when big tech should reclaim the leadership, when we get another surprise AI-driven earnings burst.

What does this get us in the major indexes? With so much of the stock market on life support, not much, maybe 10% at best. After that, who knows?

There is no point in looking for any more financial news today (Sunday), as there isn’t any with a holiday tomorrow. So I am headed out for a one-hour walk of the beach.

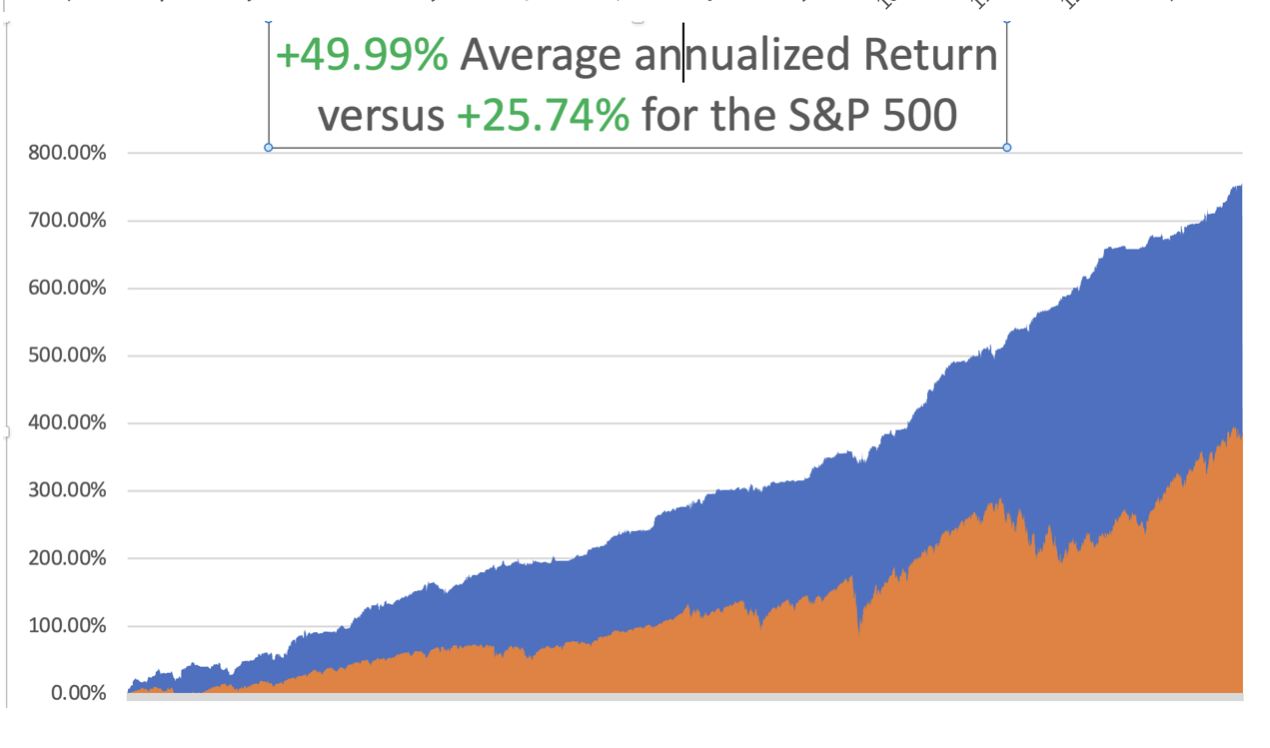

We managed to grind out a +2.07% return so far in January. That takes us to a year-to-date profit of +2.07% so far in 2025. My trailing one-year return stands at +75.92%. That takes my average annualized return to +49.99% and my performance since inception to +753.93%.

I stopped out of my long position in (TLT) near cost. My January 2025 (TSLA) expired on Friday at its maximum profit point, soaring a torrid $50 in the two days going into expiration.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 74 of 94 trades were profitable in 2024, and several of those losses were really break-evens. That is a success rate of +78.72%.

Try beating that anywhere.

My Ten-Year View – A Reassessment

When have to substantially downsize our expectations of equity returns in view of the election outcome. My new American Golden Age, or the next Roaring Twenties is now looking at a headwind. The economy will completely stop decarbonizing. Technology innovation will slow. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. My Dow 240,000 target has been pushed back to 2035.

Consumer Price Index Cools at 0.2%, or 3.2% YOY, the first drop in six months. Economists see the core gauge as a better indicator of the underlying inflation trend than the overall CPI which includes often-volatile food and energy costs. The headline measure rose 0.4% from the prior month, with over 40% of the advance due to energy.

Los Angeles Fires to Cost $270 Billion, with only $30 billion covered by insurance. Inflation will rise as the cost of construction labor and materials soar. Tradesmen around the country are packing their trucks and heading west to snare work at double the normal rate. There is no trade here as the new home builders are not involved, who are set up to only build mass-produced tract homes. Yet another black swan for 2025.

$4 Trillion in Asset Management Disrupted by the Los Angeles Fires, with some relocating office space and supporting staff members who have lost their homes. The LA area is home to large industry players like Capital Group, TCW Group, hedge funds Oaktree Capital and Ares Management.

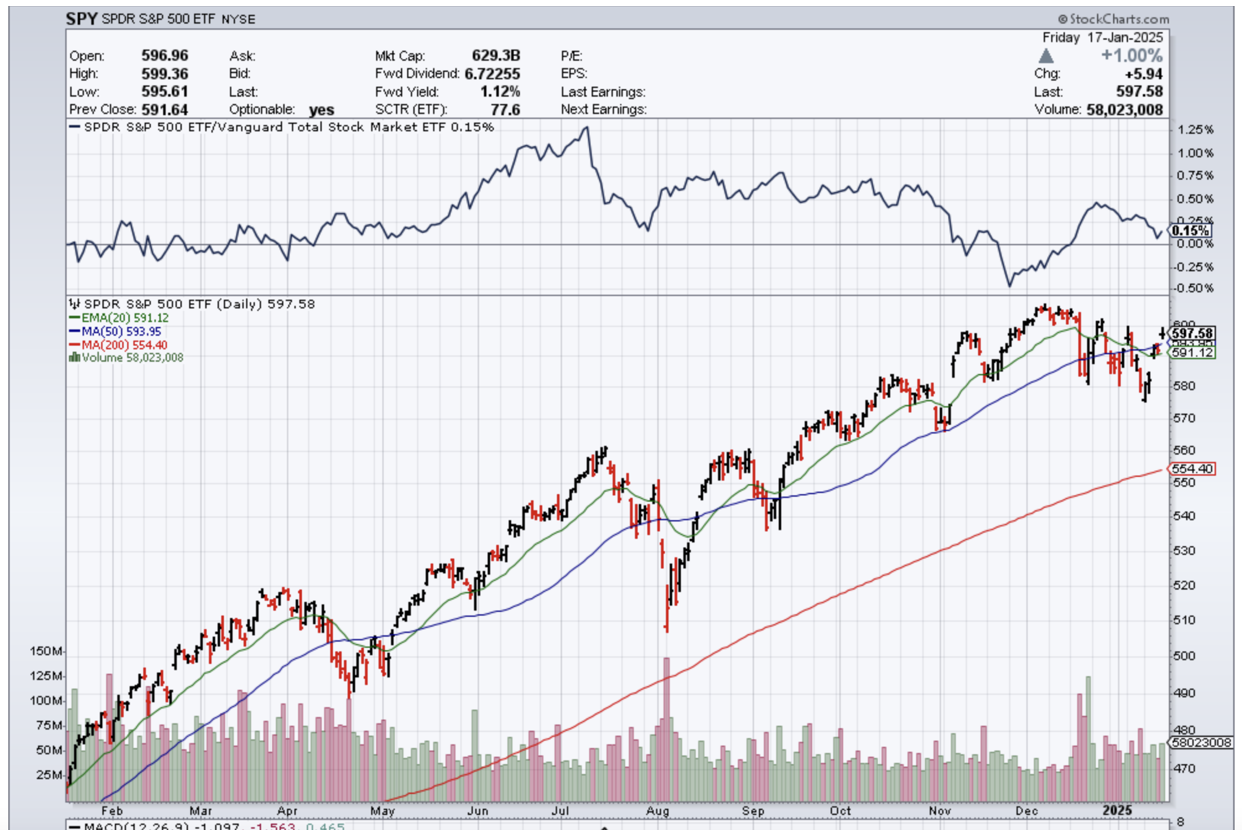

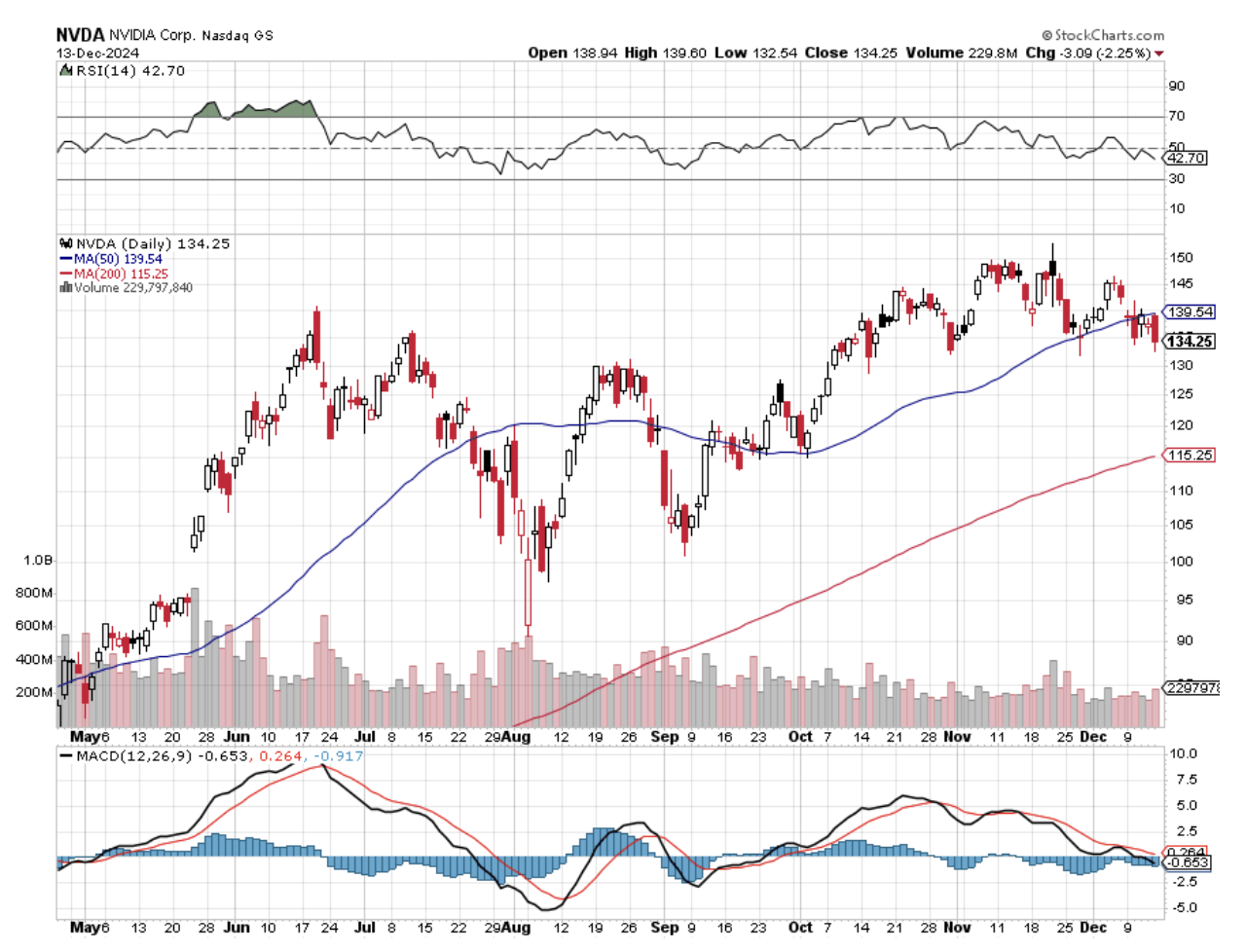

Bonds Hit 14-Month Lows at a 4.80% Yield, as fixed income dumping continues across the board. “Higher Rates for longer” don’t fit in here anywhere. But there may be a BUY setting up for (TLT) at 5.0%. The Trump Bump is Gone, stock markets giving up all their post-election gains. Technology was especially hard hit, with lead stock NVIDIA down 15%. It seems that people finally examined the implications of what Trump was proposing for the stock market. Tax-deferred selling of the enormous profits run up under the Biden administration is a big factor. Amazon is Getting Ready for Another Run. Strong earnings and continuing excitement about artificial intelligence will help Amazon stock move back into the green. The e-commerce and cloud company to beat estimates when it reports its fourth-quarter results—analysts are expecting a profit of $1.48 a share on sales of $187.3 billion, according to data from FactSet. Buy (AMZN) on dips. JP Morgan Announces Record Profits, boosted by volatility tied to the US elections in November. Trading revenue at the firm rose 21% from a year earlier, jumping to $7.05 billion. Fixed income was the star, with revenue beating analysts’ estimates, while equities-trading revenue fell short. Buy (JPM) on dips. Goldman Sachs Beats. The firm’s fourth-quarter profits more than doubled to $4.1 billion, buoyed by strength in its investment bank, expansion of its asset management business, and a surprise $472 million gain from a balance sheet bet. Goldman ended 2024 as the best-performing stock among major US banks with a 48% advance. The bank is positioning itself for a long-awaited resurgence in deals after ditching major parts of a consumer foray.

Morgan Stanley Doubles Profits. Equities were the big winner, with revenue jumping 51% in the quarter and reaching an all-time high for the full year. In the wealth business, net new assets fell just shy of estimates even as revenue topped expectations. SEC Sues Elon Musk, alleging the billionaire violated securities law by acquiring Twitter shares at “artificially low prices.” In his purchases, Musk underpaid for Twitter shares by at least $150 million, the SEC says. Musk bought Twitter in 2022 for about $44 billion, later changing the name to X. Expect this case to get lost behind the radiator next week. Fed Minutes are Turning Hawkish, making an interest rate cut at the March 19 meeting unlikely. Inflation is stubbornly above target, the economy is growing at about 3% pace and the labor market is holding strong. Put it all together and it sounds like a perfect recipe for the Federal Reserve to raise interest rates or at least to stay put. EIA Expects Weak Oil Prices for All of 2025. Many analysts expect an oversupplied oil market this year after demand growth slowed sharply in 2024 in the top consuming nations: the U.S. and China. The EIA said it expects Brent crude oil prices to fall 8% to average $74 a barrel in 2025, then fall further to $66 a barrel in 2026. Housing Starts were up 3.0% in December, with single-family homes up only 3%, while multifamily saw a 59% rise. It should shift away from home sales crushed by 7.2% mortgage rates. You can write off real estate in 2025. EV and Hybrid Sales Reach a Record 20% of US Vehicle Sales in 2024 and now account for 10% of the total US fleet. And you wonder why oil prices are so low. That includes 1.9 million hybrid vehicles, including plug-in models, and 1.3 million all-electric models. Tesla continued to dominate sales of pure EVs but Cox Automotive estimated its annual sales fell and its market share dropped to about 49%. SpaceX Starship Blows Up on test launch number seven. The Federal Aviation Administration issued a warning to pilots of a “dangerous area for falling debris of rocket Starship,” according to a pilots’ notice. Looks like that Mars trip will be delayed.

On Monday, January 20, the markets are closed for Martin Luther King Day.

On Tuesday, January 21 at 8:30 AM EST, nothing of note takes place.

On Wednesday, January 22 at 8:30 AM, the API Crude Oil Stocks are printed.

On Thursday, January 23 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, January 24 at 8:30 AM, Existing Home Sales are published. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, back in the early 1980s, when I was starting up Morgan Stanley’s international equity trading desk, my wife Kyoko was still a driven Japanese career woman.

Taking advantage of her near-perfect English, she landed a prestige job as the head of sales at New York’s Waldorf Astoria Hotel.

Every morning, we set off on our different ways, me to Morgan Stanley’s HQ in the old General Motors Building on Avenue of the Americas and 47th street and she to the Waldorf at Park and 34th.

One day, she came home and told me there was this little old lady living in the Waldorf Towers who needed an escort to walk her dog in the evenings once a week. Back in those days, the crime rate in New York was sky-high and only the brave or the reckless ventured outside after dark.

I said, “Sure, what was her name?”

Jean MacArthur.

I said, "THE Jean MacArthur?"

She answered, “Yes.”

Jean MacArthur was the widow of General Douglas MacArthur, the WWII legend. He fought off the Japanese in the Philippines in 1941 and retreated to Australia in a dramatic night PT Boat escape.

He then led a brilliant island-hopping campaign, turning the Japanese at Guadalcanal and New Guinea. My dad was part of that operation, as were the fathers of many of my Australian clients. That led all the way to Tokyo Bay where MacArthur accepted the Japanese in 1945 on the deck of the battleship USS Missouri.

The MacArthurs then moved into the Tokyo embassy where the general ran Japan as a personal fiefdom for seven years, a residence I know well. That’s when Jean, who was 18 years the general’s junior, developed a fondness for the Japanese people.

When the Korean War began in 1950, MacArthur took charge. His landing at Inchon Harbor broke the back of the invasion and was one of the most brilliant tactical moves in military history. When MacArthur was recalled by President Truman in 1952, he had not been home for 13 years.

So it was with some trepidation that I was introduced by my wife to Mrs. MacArthur in the lobby of the Waldorf Astoria. On the way out, we passed a large portrait of the general who seemed to disapprovingly stare down at me taking out his wife, so I was on my best behavior.

To some extent, I had spent my entire life preparing for this job.

I had stayed at the MacArthur Suite at the Manila Hotel where they had lived before the war. I knew Australia well. And I had just spent a decade living in Japan. By chance, I had also read the brilliant biography of MacArthur by William Manchester, American Caesar, which had only just come out.

I also competed in karate at the national level in Japan for ten years, which qualified me as a bodyguard. In other words, I was the perfect after-dark escort for Midtown Manhattan in the early eighties.

She insisted I call her “Jean”; she was one of the most gregarious women I have ever run into. She was grey-haired, petite, and made you feel like you were the most important person she had ever run into.

She talked a lot about “Doug” and I learned several personal anecdotes that never made it to the history books.

“Doug” was a staunch conservative who was nominated for president by the Republican party in 1944. But he pushed policies in Japan that would have qualified him as a raging liberal.

It was the Japanese who begged MacArthur to ban the army and the navy in the new constitution for they feared a return of the military after MacArthur left. Women gained the right to vote on the insistence of the English tutor for Emperor Hirohito’s children, an American Quaker woman. He was very pro-union in Japan. He also pushed through land reform that broke up the big estates and handed out land to the small farmers.

It was a vast understatement to say that I got more out of these walks than she did. While making our rounds, we ran into other celebrities who lived in the neighborhood who all knew Jean, such as Henry Kissinger, Ginger Rogers, and the UN Secretary-General.

Morgan Stanley eventually promoted me and transferred me to London to run the trading operations there, so my prolonged free history lesson came to an end.

Jean MacArthur stayed in the public eye and was a frequent commencement speaker at West Point where “Doug” had been a student and later the superintendent. Jean died in 2000 at the age of 101.

I sent a bouquet of lilies to the funeral.

Kyoko passed away in 2002.

In 2014, China’s Anbang Insurance Group bought the Waldorf Astoria for $1.95 billion, making it the most expensive hotel ever sold. Most of the rooms were converted to condominiums and sold to Chinese looking to hide assets abroad.

The portrait of Douglas MacArthur is gone too. During the Korean War, he threatened to drop atomic bombs on China’s major coastal cities.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2022/08/macarthur-family-e1661786429655.jpg345450april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-01-21 09:02:342025-02-20 12:40:37The Market Outlook for the Week Ahead, or Now We are Entering the Great Unknown

Below please find subscribers’ Q&A for the January 15 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Sarasota, Florida.

Q:What would I recommend right now for my top five stocks?

A: That’s easy. Goldman Sachs (GS), Morgan Stanley (MS), JP Morgan (JPM), Citibank (C), and Bank of America (BAC). There's five right there—the top five financials that are coming out of a decade-long undervaluation. A lot of the regional banks, which are also viable, are still trading to discount the book value, which all the financials used to trade out only a couple of years ago. Of course, JP Morgan's reaching a two-year return of around double, but the news just keeps getting better and better, so buy the dips. Buy every sell-off in financials and you will be a happy camper for the year.

Q: What do you think about Robin Hood (HOOD)?

A: Well, the trouble with Robinhood is it’s very highly dependent on crypto volumes. If you think crypto is going to go higher and volumes will increase, this is a great play. However, you get another 95%, out-of-the-blue selloff in crypto like we had three years ago and Coinbase (COIN) will follow it right back down again. On the last downturn, there were concerns that Coinbase would go under, so if you can hack the volatility, take a shot, but not with my money. I have the largest banks in the country that are about to double again; I would much rather be buying LEAPS in that area and getting anywhere from 100% to 1000% percent returns on a 2-year view—much more attractive risk-reward for me. And they pay a dividend.

Q: How do you define a 5% correction?

A: Well, if you have a $100 stock and it drops $5, that is a 5% correction.

Q: Can you please explain what Tesla 2X leverage actually means and is it a way to trade Tesla as an alternative?

A: I steer people away from the 2Xs because the tracking error is really quite poor. You only get 1.5% of the upside, but 2.5 times the downside over time. These are more day trading vehicles. They take out huge fees, and huge dealing spreads—it's a very expensive way to trade. Far cheaper is just to buy Tesla (TSLA) stock on margin at 2 to 1, and there your tracking error is perfect, your fees are much lower, and you just have the margin interest rate to pay on the position, which is 6% a year or 50 basis points a month. No reason to make the ETF people richer than they already are. They keep coining these products—1x, 2x, 3x long shorts on every one of the high volume stocks, and it sucks a lot of people in, but it's higher risk, lower returns for the amount of money you're risking as far as I'm concerned. So that's the way to do it.

Q: What are your projections for Nvidia (NVDA)?

A: I think not just Nvidia, but all of the big tech is going to be kind of trading in a sideways range for a while, maybe 6 months, and then we get an upside breakout if you get the earnings breakout, which we are all expecting. AI is still in business, and still growing gangbusters. There are always a lot of Cassandra's out there saying that we're going to crash anytime, and I just don't see it. I know a lot of these people, I'm in touch with a lot of the companies, I see Beta releases of all products, the consumer products, and…the slowdown just ain't happening, I'm sorry. And I've been through a lot of these tech booms over the last 40 years, and this is only showing signs of just getting started.

Q: How come Tesla (TSLA) is up and down $30 every couple of days?

A: Number one, it is the most actively traded stock in the market right now. It has implied volatility on the options of 70%, which is really the highest in the market of any individual stock. That just creates immense amounts of trading by options traders, volatility traders, by call writing, and 2x and 3x ETF long and short players. All of the financial engineering and new products that we see all gravitate toward the high volume stocks like Nvidia, Tesla, and Apple because that's where the money is being made. Some days Tesla accounts for 25% of all the market trading. Financial engineers go where the action is, where the volume is, where the customer demand is.

Q: Why do you expect only 5% to 10% corrections if the Fed rate cuts get completely priced out?

A: I don't expect the Fed to keep cutting interest rates. We should get another rate cut this year, and that may be it for the year. If inflation comes back (and of course, all of the new administration’s policies are highly inflationary) it’s just a question of how long it takes for it to hit the system.

Q: Do you believe I should hold all of my municipal bonds (MUB) with 10-year call protection at 4.75%?

A: On a tax-adjusted basis, I would say yes. You know, stock markets may peak and deliver a zero return, and in that situation, muni bonds are very attractive. The nice thing about bonds is that you hold on to maturity—you get 100% of your money back. With stocks, that is not always the case. Stocks you have to trade because the volatility can be tremendous. And in fact, what I do is I keep all of my money in one year Treasury bills. Last time I did this, which was in September, I locked in a one-year return for 5%.

Q: Would you prefer to buy deep in the money and put spreads on top of any rally?

A: Absolutely yes. If this is a real trading year, you not only buy the dips, you sell the rallies. We did almost no real selling last year. We really only did it in June and July because the market essentially went straight up, except for two hickeys. This could be the year of not only call sprints but put spreads as well. You just have to remember to sit down when the music stops playing.

Q: You say buy the dips; what would your dip be in JP Morgan (JPM)?

A: Well lower volatility stocks by definition have smaller drawdowns. JP Morgan (JPM) is one of those, so I'd be very happy to buy a 5% dip in JP Morgan. If it drops more, you double the position on a 10% pullback. Higher volatility stocks like Tesla—I'm really waiting for 10% or 20% corrections. You saw I just bought a 22% correction twice in Tesla with it down 110 points. One of those trades is at max profit right now and the other one has probably made half its money since yesterday. That is the game. The amount of dip you buy is directly related to the volatility of the stock.

Q: Should you let your cash go uninvested?

A: Yes, never let your cash go uninvested just sitting as cash. Your broker will take that money and put it in 90-day T-bills and keep the money for himself. So buy 90-day T-bills as a cash management tool—they're paying about 4.21% right now— and you can always use those as collateral under my positions on margin.

Q: Is Home Depot (HD) a buy on the LA reconstruction story?

A: I would say no, Los Angeles is probably no more than 5% of Home Depot's business—the same with Lowe's (LOW). A single city disaster is not enough to move the stock for more than a few days, and the fact is: Home Depot is mostly dependent on home renovation, which tends not to happen during dead real estate markets because, you know, it takes the flippers out of the market. It really needs lower interest rates to get Home Depot back up to new highs.

Q: Do you expect a big market move at the end of the day when the Fed makes its announcement?

A: The market has basically fully discounted the move on January 28, and if anything happens, there'll probably be a “sell on the news.” So, I expect we could give up a piece of the recent performance on the announcement of the Fed news.

Q: Should we expect trade alerts for LEAPS coming from you?

A: Absolutely, yes. However, LEAPS are something you really only want to do on down moves. If we don't get any, we'll just do the front-month call spreads. You can still make 10%, 20% a month just concentrating on financial call spreads.

Q: What would have happened to our accounts if we kept the (TLT) $82-$85 iShares 20+ Year Treasury Bond ETF (TLT) call spread and it went all the way down to $82?

A: The value of your investment goes to zero. Of course, it was declining at a very slow rate, and the $80: you might have gotten a bounce off the $85 level. But if the inflation number had come in hot, as had all other economic data of the last month, then you could have easily gotten a gap down to $82 and lost your entire investment, because two days is not enough time to expiration to recover that 3-point loss. And that's why I stopped out yesterday.

Q: Didn't David Tepper buy China (FXI)?

A: With both hands last September, yes he did. And my bet is he got out before he got killed. I mean, that's what hedge funds do. He probably got out close to cost, and you likely won't see him promoting China again anytime in the near future.

Q: I have June 530 puts on the S&P 500, should I get rid of them?

A: Yes, I don't see a big crash coming. You probably paid a lot going all the way out to June, and it's probably not worth hanging on to. Put spreads are the better way to go—that cuts your cost by two-thirds and those you only want to put on at market tops.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or JACQUIE'S POST, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have a comfortable seat next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini can navigate it.

I am anything but Houdini, so I foray downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure and to keep me up to date with the onboard gossip. The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

Chicago’s Union Station

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way, like Omaha, Salt Lake City, and Reno, to Google obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my favorite photos from the trip below, although there is only so much you can do from a moving train and an iPhone 16 Pro.

Somewhere in Iowa

The Thumbnail Portfolio

Equities – buy dips, but sell rallies too Bonds – avoid Foreign Currencies – avoid Commodities – avoid Precious Metals – avoid Energy – avoid Real Estate – avoid

1) The Economy – Cooling

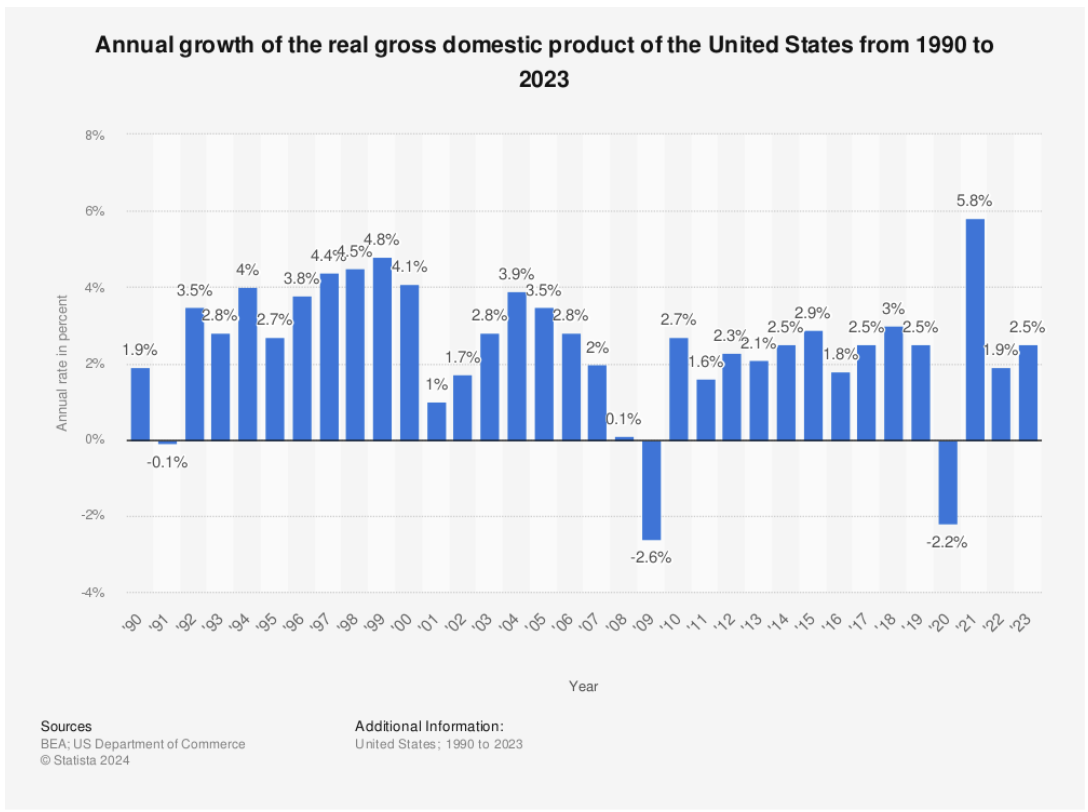

I expect a modest 2.0% real GDP growth with a 4.0% inflation rate, giving an unadjusted shrinkage of the economy of negative -2% for 2025. That is down from 0% in in 2024. This may sound discouraging, but believe me, this is the optimistic view. Some of my hedge fund buddies are expecting a zero return over the next four years.

Virtually all independent economists expect the new administration's economic policies will be a drag on both the US and global economies. Trade wars are bad for everyone. When your customers are impoverished, your own business turns south. This is a big deal, since the Magnificent Seven, which accounted for 70% of stock market gains last year, get 60% of their profits from abroad.

The ballooning National Debt is another concern. The last time Trump was in office, he added $10 trillion to the deficit through aggressive tax cuts and spending increases. If this time, he adds another $10-$15 trillion, the National Debt could reach $50 trillion by 2030.

There are two issues here. For a start, Trump will find it a lot harder and more expensive to fund a National Debt at $50 trillion than $20 trillion. Second, borrowing of this unprecedented magnitude, double US GDP, will send interest rates soaring, causing a recession.

The only question then is whether this will be a pandemic-style recession, which took stocks down 30% and recovered quickly, or a 2008 recession which demolished stocks by 52% and dragged on for years.

Hope for the best but expect the worst, unless you want to consider a future career as an Uber driver.

The outlook for stocks for 2025 is pretty simple. You are going to have to work twice as hard to make half the money you did last year with twice the volatility. You will not be able to be as nowhere near aggressive in 2025 as you were in 2024It’s a dream scenario for somebody like me. For you, I’m not so sure.

It’s not that US companies aren't growing gangbusters. I expect 2% GDP growth, 15% profit growth, and 12% net margin growth in 2025. But let’s face reality. Stocks are the most expensive they have been in 17 years and we know what happened after 2008. Much of the stock market gain achieved last year was through hefty multiple expansions. This is not good.

Big tech companies might be able to deliver 20% gains and are still the lead sector for the market. Normally that should deliver you a 15%, or $800 gain in the S&P 500 (SPX). We might be able to capture this in the first half of 2025.

Financials will remain the sector with the best risk/reward, and I mean the broader definition of the term, including banks, brokers, money managers, and some small-cap regional banks. The reason is very simple. Their income statements will get juiced at both ends as revenues soar and costs plunge, thanks to deregulation.

No passage of new laws is required to achieve this, just a failure to enforce existing ones. The hint for this is a new SEC chair whose primary interest is promoting the Bitcoin bubble. Buy (GS), (MS), (JPM), (BAC), (C), and (BLK).

However, this is anything but a normal year. Uncertainty is at an eight-year high, thanks to an incoming administration. If the promised policies are delivered, inflation will soar and interest rates will rise, as they already have. We could lose half or all of our stock market gains by the end of 2025.

The big “tell” for this was the awful market performance in December, down 5%. The Dow Average was down ten days in a row for the first time in 70 years. Santa Claus was unceremoniously sent packing. People Are clearly nervous. But then they should be with a bull market that is approaching a decrepit five years in age.

There is a bullish scenario out there and that has Trump doing absolutely nothing in 2025, either because he is unwilling or unable to take action. After all, if the economy isn’t actually broken, why fix it? Better yet, if you own an economy it is better not to break it in the first place.

Nothing substantial can pass Congress with a minuscule one-seat majority in the House of Representatives. There will be no new presidential action through tariffs and only a few token, highly televised deportations, not enough to affect the labor market.

Stocks will not only hold, but they may add to the 15% first-half gains for the year. I give this scenario maybe a 50% probability.

The first indication this is happening is when the presidential characterization of the economy flips in a few months from the world’s worst to the world’s best with no actual change in the numbers. Trump will take all the credit.

You heard it here first.

Frozen Headwaters of the Colorado River

3) Bonds (TLT), (TBT), (JNK), (PHB), (HYG), (MUB), (LQD) Amtrak needs to fill every seat in the dining car to get everyone fed on time, so you never know who you will share a table with for breakfast, lunch, or dinner.

There was the Vietnam Vet Phantom Jet Pilot who now refused to fly because he was treated so badly at airports. A young couple desperately eloping from Omaha could only afford seats as far as Salt Lake City. After they sat up all night, I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a “See America Pass.” Mennonites returned home by train because their religion forbade travel by automobiles or airplanes.

The big question to ask here after a 100-basis point rise in bond yields in only three months is whether the (TLT) has suffered enough. The short answer is no, not quite yet, but we’re getting close. Fear of Trump policies should eventually take ten-year US Treasury bond yields to 5.00%, and then we will be ready for a pause at a nine-month bottom. After that, it depends on how history unfolds.

If Trump gets everything he wants, inflation will soar, bonds will crash, and 5.00% will be just a pit stop on the way to 6.00%, 7.00%, and who knows what? On the other hand, if Trump gets nothing he says he wants, then both bonds stocks and bonds will rise, creating a Goldilocks scenario for all balanced portfolios and investors.

That also sets up a sweet spot for entry into (TLT) call spreads close to 5.00% yields. A politician campaigning on one policy, then doing the opposite once elected? Stranger things have happened. The black swans will live.

If your basic assumption for interest rates is that they stay flat or rise, then you have to love the US dollar. Currencies are all about expected interest rate differentials and money always pours into the highest-paying ones. Tariffs will add fat to the fire because any reduction in international trade automatically reduces American trade deficits and is therefore pro-dollar.

This means that you should avoid all foreign currency plays like the plague, including the Euro (FXE), Japanese yen (FXY), British Pound (FXB), Canadian dollar (FXE), and Australian dollar (FXA).

A strong greenback comes with pluses and minuses. It makes our exports expensive and less competitive and therefore creates another drag on the economy. It demolishes traditional weak dollar plays like emerging markets and precious metals. On the other hand, it attracts substantial foreign investments into US stocks and bonds, which has been continuing for the past decade.

Above all, be happy you are paid in US dollars. My foreign clients are getting crushed in an increasingly expensive world.

5) Commodities (FCX), (BHP), (RIO), (VALE), (DBA) Look at the chart of any commodity stock and you see grim death. Freeport McMoRan (FCX), BHP (BHP), and Rio Tinto (RIO), they’re all the same. They’re all afflicted with the same disease, over-dependence on a robustly growing China, which isn’t growing robustly, if at all.

I firmly believe that this will continue until the current leadership by President Xi Zheng Ping ends. He has spent the last decade globally expanding Chinese interests, engaging in abusive trade practices, hacking, and attacking American allies like Taiwan and the Philippines.You can only wave a red flag in front of the US before it comes back to bite you. A trade war with the US is now imminent.

This will happen sooner than later. The Chinese people don’t like being poor for very long. This is why I didn’t get sucked in on the Chinese long side in the fall, as many hedge funds did.

If China wants to go back to playing nice, as they did in the eighties and nineties, China should return to return to high growth and commodities will look like great “Buys” down here. If they don’t, American growth alone should eventually pull commodities up, as our economy is now growing at a long-term average gross unadjusted 6.00% rate. So the question is how long this takes.

It may pay to start nibbling on the best quality bombed-out names now, like those above.

Snow Angel on the Continental Divide

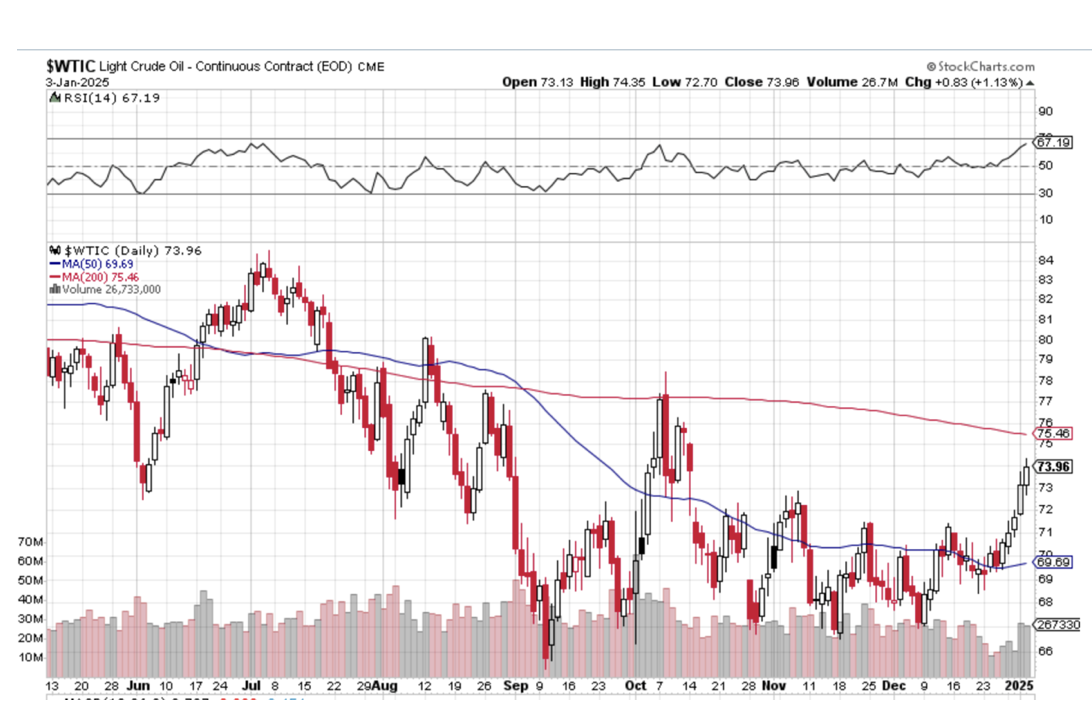

6) Energy (DIG), (USO), (DUG), (UNG), (USO), (XLE), (LNG), (CCJ), (VST), (SMR) Energy was one of the worst-performing sectors in the market for the second year in a row and 2025 is looking no better. New supplies are surging, while demand remains stuck in the mud, with the US now producing an incredible 13.5 million barrels a day. OPEC is dead.

EVs now make up 10% of the US auto fleet, and much more in other countries, are making a big dent. Some 50% of all new car sales in China, the world’s largest market, are EVs. The number of barrels of oil needed to increase a unit of American GDP is plunging, as it has done for 25 years, through increased efficiencies. Remember your old Lincoln Continental that used to get eight miles per gallon? Now it gets 27.

Worse yet, a major black swan hovers over the sector. If the Ukraine War somehow ends, some ten million barrels a day of Russian oil will hit the market. Oil prices should plunge to $50 a barrel.

There are always exceptions to the rule, and energy plays not dependent on the price of oil would be a good one. So is natural gas, which will benefit from Cheniere Energy’s (LNG) third export terminal coming online, increasing exports to China. Ukraine cutting off Russian gas flowing to Europe will assure there is plenty of new demand.

But I prefer investing in sectors that have tailwinds and not headwinds. Better leave energy to the pros who have the inside information they need to make money here.

If someone is holding a gun to your head tell you that you MUST invest in energy, go for the new nuclear plays like (CCJ), (VST), and (SMR). We are only at the becoming of the small modular reactor trend, which could accelerate for decades.

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders.

The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly, that it blew a passenger train over on its side. In the snow-filled canyons, we saw a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It’s a good omen for the coming year. We also see countless abandoned 19th-century gold mines and the broken-down wooden trestles leading to huge piles of tailings, relics of previous precious metals booms. So, it is timely here to speak about the future of precious metals.

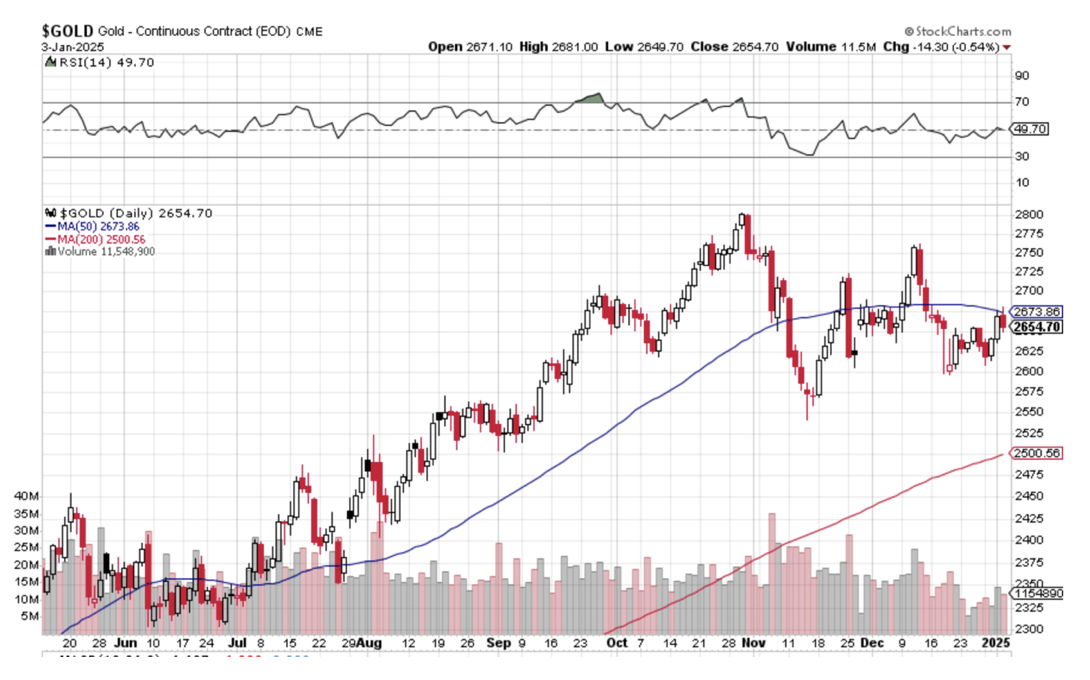

We certainly got a terrific run on precious metals in 2025, with gold at its highs up 33% and silver up 65%. The miners did even better. Even after the post-election selloff, it was still one of the best-performing asset classes of the year.

But the heat has definitely gone out of this trade. The prospect of higher interest rates for longer in 2025 has sent short-term traders elsewhere. That’s because the opportunity cost of owning precious metals is rising since they pay no interest rates or dividends. And let’s face it, there was definitely new competition for hot money from crypto, which doubled after the election.

The sector is not dead, it is resting. Central bank buying of the barbarous relic continues unabated, especially among sanctioned countries, like Russia and China. Gold is still the principal savings vehicle for many Chinese. They are not going to recover confidence in their own currency, banks, or government anytime soon. And there is still slow but steadily rising industrial demand from solar sectors.

Gold supply has also been falling for years, while costs are rising at least at double the headline inflation rate. So it’s just a matter of time before the supply/demand balance comes back in our favor. Where the final bottom is anyone’s guess as gold lacks the traditional valuation parameters of other asset classes, like dividends or interest paid. We’ll just have to wait for Mr. Market to tell us, who is always right.

Give (GLD), (SLV), (GDX), (GOLD), and (WPM) a rest for now but I’ll be back.

Crossing the Great Nevada Desert Near Area 51

8) Real Estate (ITB), (LEN), (KBH), (PHM), (DHI)

The majestic snow-covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies in advance to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada. It is a route long traversed by roving bands of Indians, itinerant fur traders, the Pony Express, my own immigrant forebearers in wagon trains, the Transcontinental Railroad, the Lincoln Highway, and finally US Interstate 80, which was built for the 1960 Winter Olympics at Squaw Valley, California. Passing by shantytowns and the forlorn communities of the high desert, I am prompted to comment on the state of the US real estate market.

Real estate was a nice earner for us in 2024 in the new homes sector. The election promptly demolished this trade with the prospect of higher interest rates for longer. Expect this unwelcome drag to continue in 2025.

I am not expecting a housing crash unless interest rates take off. More likely it will continue to grind sideways on low volume. That’s because the market has support from a structural shortage of 10 million homes in the US, the debris left over from the 2008 housing crash. That’s why there is still a Millennial living in your basement. Homebuilders now prioritize profit margins over market share.

I expect this sector to come back someday. New homebuilders have the advantage of offering free upgrades and discounted in-house financing. Avoid for now (DHI), (KBH), (TOL), and (PHM).

Crossing the Bridge to Home Sweet Home

9) Postscript We have pulled into the station at Truckee amid a howling blizzard.

My loyal staff have made the ten-mile trek from my estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been cooling in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that’s all for now. We’ve just passed what was left of the Pacific mothball fleet moored near the Benicia Bridge (2,000 ships down to six in 80 years). The pressure increase caused by a 7,200-foot descent from Donner Pass has crushed my plastic water bottle. Nice science experiment!

The Golden Gate Bridge and the soaring spire of Salesforce Tower are just coming into view across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my MacBook Pro, iPad, and iPhone, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten-mile night hike up Grizzly Peak tonight and still get home in time to watch the ball drop in New York’s Times Square on TV.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I’ll shoot you a Trade Alert whenever I see a window open at a sweet spot on any of the dozens of trades described above, which should be soon.

Good luck and good trading in 2025!

John Thomas

The Mad Hedge Fund Trader

The Omens Are Good for 2025!

https://www.madhedgefundtrader.com/wp-content/uploads/2013/01/Zephyr.jpg342451april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-01-08 09:00:172025-02-20 12:40:412025 Annual Asset Class Review

(MARKET OUTLOOK FOR THE WEEK AHEAD or CATCHING THE NEXT MARKET TOP), plus (A LIFETIME OF FLIGHT INSTRUCTION),

(JPM), (NVDA), (BAC), (C), (CCJ), (MS), (BLK), (TSLA)

We all learned as children how to win at “Merry Go Round.” All you have to do is remember to sit down when the music stops playing.

We are now entering a market with the greatest uncertainty since the pandemic. This is when expansive election promises meet harsh reality. And the new president has to attempt to deliver on his almost uncountable promises with a one-seat majority in the House of Representatives, the smallest in history.

In 2025, you are going to have to work twice as hard to make half the money with double the volatility. Markets like this are the sweet spot for Mad Hedge Fund Trader, which makes money in all market conditions. We are entering 2025 with a 30X multiple for NASDAQ, near a record high. Since 2012, the value of the Magnificent Seven has exploded from $1 trillion to $18 trillion, and you are buying, or at least staying long, on top of that move.

Amidst all the euphoria, someone failed to notice that the Republicans actually lost two seats in the House, and two more were given away in cabinet appointments. They probably don’t realize that Republicans die faster than Democrats because they are, on average, ten years older.

There are also more Democratic women who, on average, live six years longer than men. That means the slim majority will be gone in six months. Am I the only one who pays attention to demographics?

No House means no money to do anything. Many of the new administration’s proposals cost enormous amounts of money. My ancestors came from Missouri before they moved to California during the gold rush in 1849, which is known as the “Show me” state.

Show me.

So, in my early take on the New Year, look for a 10%-15% rally in stocks led by the same old sectors during the first half of 2025. Buy election winners and sell the losers. Artificial intelligence is accelerating faster than ever, and that is going on independent of Washington. Embrace the bubble. Call it the “pre-reality” rally.

After that, look for a give-back of some, if not all, of this rally. Tax cuts and spending increases will explode the National Debt well beyond the current $36 trillion. Inflation will return. Interest rates will rise. A trade war will exact a high price. Perhaps two million small businesses will go under, thanks to their loss of cheap supplies from China. Antitrust law will only be enforced against the left coast Magnificent Seven, and everyone else will get a free pass.

And now it’s my turn to deliver you a harsh reality. Every recession and stock market in my lifetime has started during a Republican administration, and I am pretty old. The causes are always the same. The expectation of tax cuts and hands-off on regulation creates over-investment and excessive leverage that always ends in tears. When that peaks, stocks crash, and a recession ensues.

Except that this time, it’s different. The incoming administration promises to sow the seeds of its most destructive policies, a trade war, and massive tax cuts during a booming economy that explodes the deficit and inflation “on day one.” That means we could see an earlier recession than a later one. That is when the music stops playing.

That is fine with me. I make more money in down markets than I do in up markets. That is because I get the hockey stick effect of falling share prices, rising volatility, and soaring options premiums to play on the downside.

As for you, I’m not so sure. I don’t have to run faster than the bear to survive, just faster than you.

It could be a great year to “Sell in May and Go Away.” I’m already booking summer cruises on Cunard (https://www.cunard.com/en-us).

A lot of readers have been asking about my take on the sudden collapse of the Bashar al Assad regime in Syria in the context of my nearly 60 years of experience in the region. I have never been to Syria; just viewed it from a distance from the Golan Heights in Israel.

The one-liner here is that it is a huge win for the US and the West and a huge loss for Russia, Iran, and the main terrorist groups.

It ejects Russia from the Middle East for the time being after making massive 50-year investments there in military support. Syria will default on all of its billions of dollars in debts to Russia. Russia built the enormous Aswan Dam on the Nile, then saw defaults here, too, when Egypt sided with the West after the Camp David Accords.

Russia built the world's third largest military in Iraq, with 5,000 tanks, which the US then completely destroyed in the first Gulf War, where I participated. Their failure in Afghanistan caused the collapse of the Soviet Union. Russia has lost its only Mediterranean port at Aleppo, and its ships there have already been withdrawn. At this point, there must be a lot of unemployed Middle East experts in Moscow.

Iran has been fighting a proxy war against Israel and the US through Hamas, Hezbollah, and Syria for 45 years, which it has just ignominiously lost. It used to supply Gaza with weapons by trucking them through Syria and loading them on ships. It now has to go all the way around Africa, and there is no one there to take them anyway.

The cost of this victory to the US has been zero: no money, no troops, no heavy equipment. Sometimes, doing nothing is the right thing. The cost to Russia and Iran has been exponential.

Of course, in the Middle East, be careful what you wish for because you might end up getting something far worse. Assad may have just been replaced with another anti-western terrorist group. That is why President Biden has directed the complete destruction of all arms stockpiles in Syria, with the assistance of Israel and Turkey. We have their exact latitude and longitude in seconds. Better there to be no weapons and have an incoming regime that is toothless in Syria than having them fall into the hands of the next terrorist group. There are no defenders in Syria at the moment.

Finally, I was amazed to see Assad’s extensive classic and race car collection, the ultimate symbol of modern dictators. Can I make a bid on the 1956 Cadillac? To where and who do I send my offer?

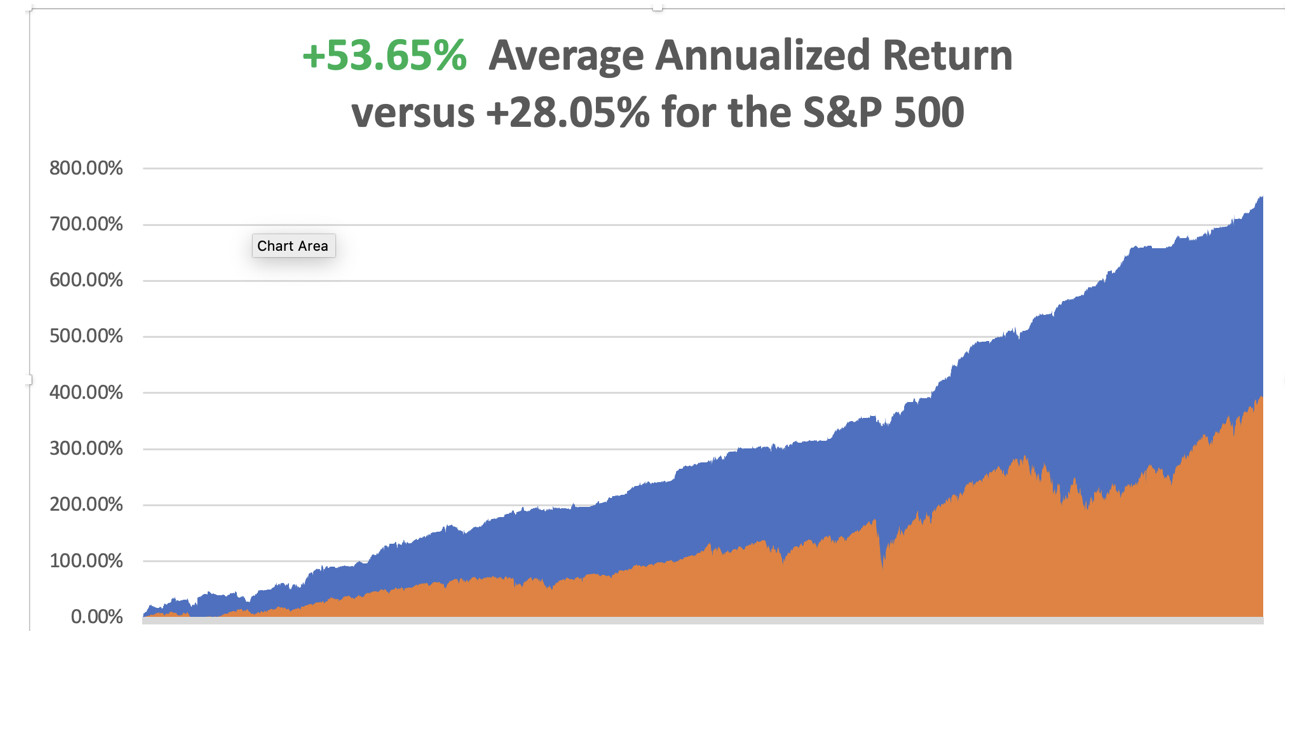

In December, we have gained +2.53%. My 2024 year-to-date performance is at an amazing +74.53%.The S&P 500 (SPY) is up +26.62%so far in 2024. My trailing one-year return reached a nosebleed +75.21%. That brings my 16-year total return to +751.16%.My average annualized return has recovered to an incredible +53.65%.

My bet that the market wouldn’t drop below pre-election levels proved wildly successful. As a result, all of my long positions will expire at max profit. They are anywhere from 7% to 70% in the money. That includes (JPM), (NVDA), (BAC), (C), (CCJ), (MS), (BLK) and a triple long in (TSLA). My largest position was a triple weighting in Tesla, which went up the most. This is the first time I have been able to pull this off in the 16-year history of the Mad Hedge Fund Trader.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 74 of 94 trades have been profitable so far in 2024, and several of those losses were really break evens. That is a success rate of +78.72%.

Try beating that anywhere.

My Ten-Year View – A Reassessment

When we have to substantially downsize our expectations of equity returns in view of the election outcome, my new American Golden Age, or the next Roaring Twenties, is now looking at a headwind. The economy will completely stop decarbonizing. Technology innovation will slow down. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. My Dow 240,000 target has been pushed back to 2035.

On Monday, December 16, at 8:30 AM EST, the S&P Global Flash PMI is out. On Tuesday, December 17 at 8:30 AM, the Retail Sales are published.

On Wednesday, December 18, at 8:30 AM, the Building Permits are printed.

On Thursday, December 19 at 8:30 AM, the US GDP Growth Rate is announced.

On Friday, December 20, Core PCE is printed. It is effectively the last trading day of the year as the BSDs take off on vacation, and the “B” team sticks around to handle the low-volume holiday trading. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, in the seventies, Air America was not too choosy about who flew their airplanes at the end of the Vietnam War. If you were willing to get behind the stick and didn’t ask too many questions, you were hired.

They didn’t bother with niceties like pilot licenses, medicals, passports, or even real names. On some of their missions, the survival rate was less than 50%, and there was no retirement plan. The only way to ignore the ratatatat of bullets stitching your aluminum airframe was to turn the volume up on your headphones.

Felix (no last name) taught me to fly straight and level so he could find out where we were on the map. We went out and got drunk on cheap Mekong Whiskey after every mission just to settle our nerves. I still remember the hangovers.

When I moved to London to set up Morgan Stanley’s international trading desk in the eighties, the English had other ideas about who was allowed to fly airplanes. Julie Fisher at the London School of Flying got me my basic British pilot’s license.

If my radio went out, I learned to land by flare gun and navigate by sextant. She also taught me to land at night on a grass field guided by a single red-lensed flashlight. For fun, we used to fly across the channel and land at Le Touquet, taxiing over the rails for the old V-1 launching pads.

A retired Battle of Britain Spitfire pilot named Captain John Schooling taught me advanced flying techniques and aerobatics in an old 1949 RAF Chipmunk. I learned barrel rolls, loops, chandelles, whip stalls, wingovers, and Immelmann turns, everything a WWII fighter pilot needed to know.

John was a famed RAF fighter ace. Once, he got shot down by a Messerschmitt 109, parachuted to safety, took a taxi back to his field, jumped into his friend’s Spit, and shot down another German. Every lesson ended with a pint of beer at the pub at the end of the runway. John paid me the ultimate compliment, calling me “a natural stick and rudder man,” no pun intended.

John believed in tirelessly practicing engine off-landings. His favorite trick was to reach down and shut off the fuel, telling me that a Messerschmitt had just shot out my engine and to land the plane. When we got within 200 feet of a good landing, he turned the fuel back on, and the engine coughed back to life. We practiced this more than 200 times.

When I moved back to the US in the early nineties, it was time to go full instrument in order to get my commercial and military certifications. Emmy Michaelson nursed me through that ordeal. After 50 hours of flying blindfolded in a cockpit, you get very close with someone.

Then came flight test day. Emmy gave me the grim news that I had been assigned to “One Engine Larry,” the most notorious FAA examiner in Northern California. Like many military flight instructors, Larry believed that no one should be allowed to fly unless they were perfect.

We headed out to the Marin County coast in an old twin-engine Beechcraft Duchess, me under my hood. Suddenly, Larry shut the fuel off, told me my engines failed, and that I had to land the plane. I found a cow pasture aligned with the wind and made a perfect approach.

Then he asked, “How did you do that?” I told him. He said, “Do it again,” and I did. Then he ordered me back to base. He signed me off on my multi-engine and instrument ratings as soon as we landed without bothering with the rest of the test. Emmy was thrilled.

I now have to keep my many licenses valid by completing three takeoffs and landings every three months. I usually take my kids and make a day of it, letting them take turns flying the plane straight and level.

On my fourth landing, I warn my girls that I’m shutting the engine off at 2,000 feet. They cry, “No, Dad, don’t.” I do it anyway, coasting in bang on the numbers every time.

A lifetime of flight instruction teaches you not only how to fly but how to live as well. It makes you who you are. Thus, my insistence on absolute accuracy, precision, risk management, and probability analysis. I live my life by endless checklists, both short and long-term. I am the ultimate planner, and I have a never-ending obsession with the weather one week out.

It passes down to your kids as well.

Julie became one of the first female British Airways pilots, got married, and had kids. John passed on to his greater reward many years ago. There are no surviving Battle of Britain pilots left. The last one passed away this year. Emmy was an early female hire as a United pilot. She married another United pilot and was eventually promoted to full captain. I know because I ran into them in an elevator at San Francisco airport ten years ago, four captain’s bars adorning her uniform.

Flying is in my blood now, and I’ll keep flying for life. I can now fly anything anywhere and am the backup pilot on several WWII aircraft for air shows, including the B-17, B-24, and B-25 bombers, the P-51 Mustang fighter, and, of course, Supermarine Spitfires.

Captain John Schooling would be proud.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Captain John Schooling and His RAF 1949 Chipmunk

A Mitchell B-25 Bomber

A 1932 De Havilland Tiger Moth

Flying a P-51 Mustang

The Next Generation

A Supermarine Spitfire Mark IX

https://www.madhedgefundtrader.com/wp-content/uploads/2024/12/daughters.png8161086april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-12-16 09:02:222024-12-16 11:12:58The Market Outlook for the Week Ahead, or Catching the Next Market Top

(MARKET OUTLOOK FOR THE WEEK AHEAD or WHY THE MAG SEVEN ARE FADING) plus (HOW TO GET A TESLA FOR FREE),

(NVDA), (GLD), (JPM), (BAC), (C),

(CCJ), (MS), (BLK) (TSLA), (TLT)

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.