Mad Hedge Technology Letter

January 17, 2019

Fiat Lux

Featured Trade:

(WHY FINTECH IS EATING THE BANKS’ LUNCH),

(WFC), (JPM), (BAC), (C), (GS), (XLF), (PYPL), (SQ), (SPOT), (FINX), (INTU)

Mad Hedge Technology Letter

January 17, 2019

Fiat Lux

Featured Trade:

(WHY FINTECH IS EATING THE BANKS’ LUNCH),

(WFC), (JPM), (BAC), (C), (GS), (XLF), (PYPL), (SQ), (SPOT), (FINX), (INTU)

Going into January 2018, the big banks were highlighted as the pocket of the equity market that would most likely benefit from a rising rate environment which in turn boosts net interest margins (NIM).

Fast forward a year and take a look at the charts of Bank of America (BAC), Citibank (C), JP Morgan (JPM), Goldman Sachs (GS), and Morgan Stanley (GS), and each one of these mainstay banking institutions are down between 10%-20% from January 2018.

Take a look at the Financial Select Sector SPDR ETF (XLF) that backs up my point.

And that was after a recent 10% move up at the turn of the calendar year.

As much as it pains me to say it, bloated American banks have been completely caught off-guard by the mesmerizing phenomenon that is FinTech.

Banking is the latest cohort of analog business to get torpedoes by the brash tech start-up culture.

This is another fitting example of what will happen when you fail to evolve and overstep your business capabilities allowing technology to move into the gaps of weakness.

Let me give you one example.

I was most recently in Tokyo, Japan and was out of cash in a country that cash is king.

Japan has gone a long way to promoting a cashless society, but some things like a classic sushi dinner outside the old Tsukiji Fish Market can’t always be paid by credit card.

I found an ATM to pull out a few hundred dollars’ worth of Japanese yen.

It was already bad enough that the December 2018 sell-off meant a huge rush into the safe haven currency of the Japanese Yen.

The Yen moved from 114 per $1 down to 107 in one month.

That was the beginning of the bad news.

I whipped out my Wells Fargo debit card to withdraw enough cash and the fees accrued were nonsensical.

Not only was I charged a $5 fixed fee for using a non-Wells Fargo ATM, but Wells Fargo also charged me 3% of the total amount of the transaction amount.

Then I was hit on the other side with the Japanese ATM slamming another $5 fixed fee on top of that for a non-Japanese ATM withdrawal.

For just a small withdrawal of a few hundred dollars, I was hit with a $20 fee just to receive my money in paper form.

Paper money is on their way to being artifacts.

This type of price gouging of banking fees is the next bastion of tech disruption and that is what the market is telling us with traditional banks getting hammered while a strong economy and record profits can’t entice investors to pour money into these stocks.

FinTech will do what most revolutionary technology does, create an enhanced user experience for cheaper prices to the consumers and wipe the greedy traditional competition that was laughing all the way to the bank.

The best example that most people can relate to on a daily basis is the transportation industry that was turned on its head by ride-sharing mavericks Uber and Lyft.

But don’t ask yellow cab drivers how they think about these tech companies.

Highlighting the strong aversion to traditional banking business is Slack, the workplace chat app, who will follow in the footsteps of online music streaming platform Spotify (SPOT) by going public this year without doing a traditional IPO.

What does this mean for the traditional banks?

Less revenue.

Slack will list directly and will set its own market for the sale of shares instead of leaning on an investment bank to stabilize the share price.

Recent tech IPOs such as Apptio, Nutanix and Twilio all paid 7% of the proceeds of their offering to the underwriting banks resulting in hundreds of millions of dollars in revenue.

Directly listings will cut that fee down to $10-20 million, a far cry from what was once status quo and a historical revenue generation machine for Wall Street.

This also layers nicely with my general theme of brokers of all types whether banking, transportation, or in the real estate market gradually be rooted out by technology.

In the world of pervasive technology and free information thanks to Google search, brokers have never before added less value than they do today.

Slowly but surely, this trend will systematically roam throughout the economic landscape culling new victims.

And then there are the actual FinTech companies who are vying to replace the traditional banks with leaner tech models saving money by avoiding costly brick and mortar branches that dot American suburbs.

PayPal (PYPL) has been around forever, but it is in the early stages of ramping up growth.

That doesn’t mean they have a weak balance sheet and their large embedded customer base approaching 250 million users has the network effect most smaller FinTech players lack.

PayPal is directly absorbing market share from the big banks as they have rolled out debit cards and other products that work well for millennials.

They are the owners of Venmo, the super-charged peer-to-peer payment app wildly popular amongst the youth.

Shares of PayPal’s have risen over 200% in the past 2 years and as you guessed, they don’t charge those ridiculous fees that banks do.

Wells Fargo and Bank of America charge a $12 monthly fee for balances that dip below $1,500 at the end of any business day.

Your account at PayPal can have a balance of 0 and there will never be any charge whatsoever.

Then there is the most innovative FinTech company Square who recently locked in a new lease at the Uptown Station in Downtown Oakland expanding their office space by 365,000 square feet for over 2,000 employees.

Square is led by one of the best tech CEOs in Silicon Valley Jack Dorsey.

Not only is the company madly innovative looking to pounce on any pocket of opportunity they observe, but they are extremely diversified in their offerings by selling point of sale (POS) systems and offering an online catering service called Caviar.

They also offer software for Square register for payroll services, large restaurants, analytics, location management, employee management, invoices, and Square capital that provides small loans to businesses and many more.

On average, each customer pays for 3.4 Square software services that are an incredible boon for their software-as-a-service (SaaS) portfolio.

An accelerating recurring revenue stream is the holy grail of software business models and companies who execute this model like Microsoft (MSFT) and Salesforce (CRM) are at the apex of their industry.

The problem with trading this stock is that it is mind-numbingly volatile. Shares sold off 40% in the December 2018 meltdown, but before that, the shares doubled twice in the past two years.

Therefore, I do not promote trading Square short-term unless you have a highly resistant stomach for elevated volatility.

This is a buy and hold stock for the long-term.

And that was only just two companies that are busy redrawing the demarcation lines.

There are others that are following in the same direction as PayPal and Square based in Europe.

French startup Shine is a company building an alternative to traditional bank accounts for freelancers working in France.

First, download the app.

The company will guide you through the simple process — you need to take a photo of your ID and fill out a form.

It almost feels like signing up to a social network and not an app that will store your money.

You can send and receive money from your Shine account just like in any banking app.

After registering, you receive a debit card.

You can temporarily lock the card or disable some features in the app, such as ATM withdrawals and online payments.

Since all these companies are software thoroughbreds, improvement to the platform is swift making the products more efficient and attractive.

There are other European mobile banks that are at the head of the innovation curve namely Revolut and N26.

Revolut, in just 6 months, raised its valuation from $350 million to $1.7 billion in a dazzling display of growth.

Revolut’s core product is a payment card that celebrates low fees when spending abroad—but even more, the company has swiftly added more and more additional financial services, from insurance to cryptocurrency trading and current accounts.

Remember my little anecdote of being price-gouged in Tokyo by Wells Fargo, here would be the solution.

Order a Revolut debit card, the card will come in the mail for a small fee.

Customers then can link a simple checking account to the Revolut debit card ala PayPal.

Why do this?

Because a customer armed with a Revolut debit card linked to a bank account can use the card globally and not be charged any fees.

It would be the same as going down to your local Albertson’s and buying a six-pack, there are no international or hidden fees.

There are no foreign transaction fees and the exchange rate is always the mid-market rate and not some manipulated rate that rips you off.

Ironically enough, the premise behind founding this online bank was exactly that, the originators were tired of meandering around Europe and getting hammered in every which way by inflexible banks who could care less about the user experience.

Revolut’s founder, Nikolay Storonsky, has doubled down on the firm’s growth prospects by claiming to reach the goal of 100 million customers by 2023 and a succession of new features.

To say this business has been wildly popular in Europe is an understatement and the American version just came out and is ready to go.

Since December 2018, Revolut won a specialized banking license from the European Central Bank, facilitated by the Bank of Lithuania which allows them to accept deposits and offer consumer credit products.

N26, a German like-minded online bank, echo the same principles as Revolut and eclipsed them as the most valuable FinTech startup with a $2.7 Billion Valuation.

N26 will come to America sometime in the spring and already boast 2.3 million users.

They execute in five languages across 24 countries with 700 staff, most recently launching in the U.K. last October with a high-profile marketing blitz across the capital.

Most of their revenue is subscription-based paying homage to the time-tested recurring revenue theme that I have harped on since the inception of the Mad Hedge Technology Letter.

And possibly the best part of their growth is that the average age of their customer is 31 which could be the beginning of a beautiful financial relationship that lasts a lifetime.

N26’s basic current account is free, while “Black” and “Metal” cards include higher ATM withdrawal limits overseas and benefits such as travel insurance and WeWork membership for a monthly fee.

Sad to say but Bank of America, Wells Fargo, and the others just can’t compete with the velocity of the new offerings let alone the software-backed talent.

We are at an inflection point in the banking system and there will be carnage to the hills, may I even say another Lehman moment for one of these stale business models.

Online banking is here to stay, and the momentum is only picking up steam.

If you want to take the easy way out, then buy the Global X FinTech ETF (FINX) with an assortment of companies exposed to FinTech such as PayPal, Square, and Intuit (INTU).

The death of cash is sooner than you think.

This year is the year of FinTech and I’m not afraid to say it.

Global Market Comments

August 14, 2018

Fiat Lux

Featured Trade:

(WHY BANKS HAVE PERFORMED SO BADLY THIS YEAR),

(JPM), (C), (GS), (SCHW), (WFC),

(HOW FREE ENERGY WILL POWER THE COMING ROARING TWENTIES),

(SPWR), (TSLA)

I went to the local branch of Wells Fargo Bank (WFC) yesterday, and I was appalled. The bank occupied the most expensive corner in town. It was staffed by a dozen people, all of whom spoke English as a second language.

Ask even the simplest question and they had to call a support center and wait 10 minutes on hold for the answer. It took an hour for me to open a checking account for one of my kids. The branch was in effect a glorified call center.

I thought, "This can't last." And it won't.

Banks were supposed to be the sector to own this year. They had everything going for them. The economy was booming, interest rates were rising, and regulations were falling like leaves in the fall.

Despite all these gale force fundamental tailwinds the banks have utterly failed to deliver. The gold standard J.P. Morgan is up only 8.46% on the year, while bad boy Citibank (C) is down 5.47%, and the vampire squid Goldman Sachs (GS) is off a gut-punching 10.27%. Where did the bull market go? Why have bank shares performed so miserably?

The obvious reason could be that the improved 2018 business environment was entirely discounted by the big moves we saw in 2017. Last year, banks were the shares to own with (JPM) shares up a robust 24.5%, while (C) catapulted by 29.3%.

It is possible that bank shares are acting like a very early canary in the coal mine, tweeting about an approaching recession. Loan growth has been near zero this year. That is not typical for a booming economy. It IS typical going into a recession.

When the fundamentals arrive as predicted but the stock fails to perform it can only mean one thing. The industry is undergoing a long-term structural change from which it may not recover. Yes, the bank industry may be the modern-day equivalent of the proverbial buggy whip maker just before Detroit took over the transportation business.

Managing a research service such as the Mad Hedge Technology Letter, it is easy to see how this is happening. Financial services are being disrupted on a hundred fronts, and the cumulative effect may be that it will no long exist.

This explains why this is the first bull market in history where there has been no new hiring by Wall Street. What happens when we go into a bear market? Employment will drop by half and those expensive national branch networks will disappear.

Financial services are still rife with endless fees, poor service, and uncompetitive returns. Online brokers such as Robin Hood (click here) will execute stock and option transactions for free. Now that overnight deposits actually pay a return they make their money on margin loans. They have no branch network but are still SIPC insured.

Legacy brokers such as Fidelity and Charles Schwab (SCHW) used to charge $25 a share to execute and are still charging $7.00 for full-service clients. And it's not as if their research has been so great to justify these high prices either. In a world that is getting Amazoned by the day, these high prices can't stand.

Regular online banking service also pay interest and are about to eat the big banks' lunch. Many now pay 1.75% overnight interest rates and offer free debit and credit cards, and checking accounts. Of course, none of these are household names yet, but they will be.

To win the long-term investment game you have to identify the industries of the future and run from the industries of the past. The legacy financial industry is increasingly looking like a story from the past.

Featured Trade:

Below please find subscribers Q&A for the Mad Hedge Fund Trader April Global Strategy Webinar with my guest co-host Mike Pisani of Smart Option Trading.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Are you out of Alphabet (GOOGL) and Microsoft (MSFT)?

A. I'm out of Alphabet and I'm in Microsoft, but only for the very short term. I'm waiting for another big meltdown day to go back and buy everything back because I think the FANGs and technology in general are still in a secular bull market.

Q. Are Advanced Micro Devices (AMD) and NVIDIA (NVDA) affected by the underperformance of Bitcoin?

A. They are. Bitcoin has been an important part of the chip story for the last two years because mining, or the creation of bitcoins, creates enormous demand for chips to do the processing. I think selling in bitcoin is over for the time being. You had a $25 billion in capital gains taxes that had to be paid by April 15.

People were paying those bills by selling their bitcoins. That's over now, and bitcoin is rallied about 30% since Tax Day because of that. So, yes, bitcoin is getting so big that it is starting to affect the chip sector meaningfully. That is another reason why we see secular long-term growth in the entire chip sector.

Mike Pisani: Interesting take on bitcoin today, and I've been with you on it. I think the worst of it is over; it's going to go. Today is the largest volume day we've seen on it so far. We're up over 15,500 contracts traded.

Q: If you're 100% cash, is now a good time to commit funds to the equity market?

A. Franz, I would say nein. Absolutely not. 2009 was the time to commit funds to the equity market. If you're 100% cash now I would stay out for the next six months. We may get a good entry point over the summer or the fall. I'll let you know when that happens because I will be jumping back in myself.

But right now, a week ahead of the worst six months of equity investment of the year, I would stay away and do research instead. Read your Mad Hedge Fund Trader letters. Build a list of names that you're going to buy on the next meltdown and practice buying meltdowns with your practice account, which doesn't use real money.

There's a lot of things you can get ready to do for the next leg up in the bull market, but buying right now, NO! I would put that in the category of, "Is it time to start shorting bonds question?" that we got a few minutes ago.

Q: Why did tech stocks sell off when they have great earnings results?

A: It's called, "Buy the rumor, sell the news." So many people already own the stocks and were expecting good earnings that there was no surprise when they were announced. These are some of the most over-owned stocks in history.

Everybody in the world owns them. Many people have multiple weightings in them, so when we enter a high-risk macro environment, which we have now, you want to get rid of the most over-owned stocks. That is exactly why all of these stocks that have had great runs are selling off, even though they have great earnings report.

Q: Are financials a good play here with interest rates rising though 3%?

A. Normally I would say yes. However, the macro background for the general market are so negative they are overwhelming any positive fundamentals specific to individual sectors like banks and stocks like Citigroup (C). By the way, financials all reported great results and got killed, so that is why I bailed out of my (C) position this morning at around cost. If you throw the best news in the world on a stock and it won't go up, it's time to get out of there.

Q: Would an unleveraged inverse ETF like the ProShares Short S&P 500 ETF (SH) be good at a spike even now?

A. Yes, but when I say spike up better expect at least 20 (SPY) points or 1,000 Dow points. All these downside ETFs are great but you've got to get in at the right price. You know as they say in trading school, the profit is always made on the "BUY" and not on the "SELL."

So, if you can get on one of these super spikes up on the short side that is a great trade. So is the ProShares Ultra Short ETF (SDS) if you want to do the 2X leverage short fund. We've recently started doing this every month. We've been shorting (SPY)s and buying (VIX) on every one of these spikes up, and it's been working like a charm.

Q: Here's the best question of the day. Your timing has been perfect says Mary in Chicago, Ill.

A: Well, I'll take that kind of question all day long. Thank you very much. You're too nice to do that.

Q: Richard is asking would you buy an NVIDIA (NVDA) LEAP?

A: I would wait for meltdown days. Remember this is a market that gives you lots of meltdown days. Just wait for the next presidential tweet and you might get another 600-700-point dip in the markets. Those are the days you buy LEAPS. You don't have to get buy writing Trade Alerts like I do. You can just enter a limit order in your account. Put it as a stupidly low level to "BUY" and you may get hit. And that's where you really make the big money in this kind of market.

Q: Is there a good one- or two-month trade in Amazon?

A: Yeah, Paul, with this volatility you can pick a big winner like Amazon and you know to buy the 250-point dips and sell the rallies. These ranges are so wide now that even a beginner can make money. So, I would say you have to wait until after tomorrow on Amazon and let them get their earnings out. We know they're going to be great. They're doing home deliveries now to your car.

Q: Can long bond interest rates go up to 4%, and if that happens what would the market do?

A: Yes, they can go up to 4%, and I expect them to probably do that next year. What will it do to the market? Answer: Cause a bear market and a recession. Is that answer clear enough? My bet is that interest rates cap in this cycle much lower than they did in past cycles, maybe 4%-5%. We have been used to zero cost of money for so long that a move to 4% would be like stabbing somebody in the chest. People are much less able to deal with rising rates than they ever have been in the past, so watch this space.

Q: Should I buy the ProShares Ultra Short Treasury ETF (TBT) or the iShares 20+ Year Treasury Bond Fund (TLT)?

A: Brad, it's really is a leverage question for you. The (TLT) is 1X; the TBT is 2X, so I would be taking profits on the (TBT) here and then buying a couple of points lower. Or if you want to keep it for the long term you can but remember the cost of carry on the TBT is around 7% a year.

Q: Yves in Paris, France is asking: What possible scenario will you see material wage growth that could lead to higher inflation?

A: We're starting to see that now with the ultra-low unemployment rates. People are having great difficulty hiring anyone in technology. But at the minimum wage level there seems to be plenty of supply. The other possibility is that the cost of everything else goes up but wages, because technology is replacing jobs so fast there may never be any increase in wages.

So, we will get inflation, but nothing like the inflation we saw in the past driven by rising wages, commodity prices, oil prices, and interest rates. Yes, money is a commodity, which can add quite a lot to the cost of leveraged companies like airlines, REITs, and so on.

Q: Will rising interest rates force the US dollar up?

A. The answer is yes! It has been a long time coming, but if rates continue to rise from here, you can expect that to lead to a continuously rising dollar and falling foreign currencies, and that will become a major drag on the economy and corporate earnings going forward.

Q: When is a good time to buy TIPS?

A: Just like your Treasury bond short, I would buy Treasury Inflation Protected Securities (TIPS) on the next rally in bond prices (TLT) and dip in yields. That will give you a decent entry point. That said, TIPS have been a horrible performer for the last 10 years because there has just been no inflation. A lot of people just keep TIPS as a hedge in their portfolio and it just costs them money every year.

Q: Which could blow up, Brad wants to know, TBT or TLT?

A: The easy answer there is probably neither. But if I had to pick between the two, the (TBT) would be the one to blow up because it's a 2X and has a lot less liquidity. So, I can't image in what world has (TBT) blowing up, but then I don't watch zombie TV shows either.

Q: I think US equities are expensive. Are emerging markets (EEM) or Europe (HEDJ) a better bet for the rest of the year?

A: I would say yes. Because if interest rates here in the US go higher that means a stronger dollar. That means a weaker US stock market. Because US companies are punished by a rising dollar. And European and Asian companies benefit from a rising dollar and falling home currencies, so that makes Europe the first choice of any of the global markets.

Q: Does oil going to $100 have a chance of bringing down the US economy?

A: Absolutely yes. If oil prices don't start to slow down, they will start having a big impact on the economy because that means rising prices for any energy consumer, which is you and me.

With no ability to offset that by rising prices of your products that would put a squeeze on any oil consuming industry, which is why things like the transports and consumer staples have been performing so poorly. If we get to $100, then you're really looking at a full-on recession and bear market for stocks. By bear market I mean down 25% or more in stocks.

Q: How do you see the India ETF?

A: We like it. India is the No. 1 pick of any hedge fund investor in emerging markets, and the ETF you can buy there is the PowerShares India Portfolio ETF (PIN).

Global Market Comments

April 23, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE COMES THE FOUR HORSEMEN OF THE APOCALYPSE),

(SPY), (GOOGL), (TLT), (GLD), (AAPL), (VIX), (VXX), (C), (JPM),

(HOW TO AVOID PONZI SCHEMES),

(TESTIMONIAL)

Have you liked 2018 so far?

Good.

Because if you are an index player, you get to do it all over again. For the major stock indexes are now unchanged on the year. In effect, it is January 1 once more.

Unless of course you are a follower of the Mad Hedge Fund Trader. In that case, you are up an eye-popping 19.75% so far in 2018. But more on that later.

Last week we caught the first glimpse in this cycle of the investment Four Housemen of the Apocalypse. Interest rates are rising, the yield on the 10-year Treasury bond (TLT) reaching a four-year high at 2.96%. When we hit 3.00%, expect all hell to break loose.

The economic data is rolling over bit by bit, although it is more like a death by a thousand cuts than a major swoon. The heavy hand of major tariff increases for steel and aluminum is making itself felt. Chinese investment in the US is falling like a rock.

The duty on newsprint imports from Canada is about to put what's left of the newspaper business out of business. Gee, how did this industry get targeted above all others?

The dollar is weak (UUP), thanks to endless talk about trade wars.

Anecdotal evidence of inflation is everywhere. By this I mean that the price is rising for everything you have to buy, like your home, health care, college education, and website upgrades, while everything you want to sell, such as your own labor, is seeing the price fall.

We're not in a recession yet. Call this a pre-recession, which is a long-leading indicator of a stock market top. The real thing shouldn't show until late 2019 or 2020.

There was a kerfuffle over the outlook for Apple (AAPL) last week, which temporarily demolished the entire technology sector. iPhone sales estimates have been cut, and the parts pipeline has been drying up.

If you're a short-term trader, you should have sold your position in April 13 when I did. If you are a long-term investor, ignore it. You always get this kind of price action in between product cycles. I still see $200 a share in 2018. This too will pass.

This month, I have been busier than a one-armed paper hanger, sending out Trade Alerts across all asset classes almost every day.

Last week, I bought the Volatility Index (VXX) at the low, took profits in longs in gold (GLD), JP Morgan (JPM), Alphabet (GOOGL), and shorts in the US Treasury bond market (TLT), the S&P 500 (SPY), and the Volatility Index (VXX).

It is amazing how well that "buy low, sell high" thing works when you actually execute it. As a result, profits have been raining on the heads of Mad Hedge Trade Alert followers.

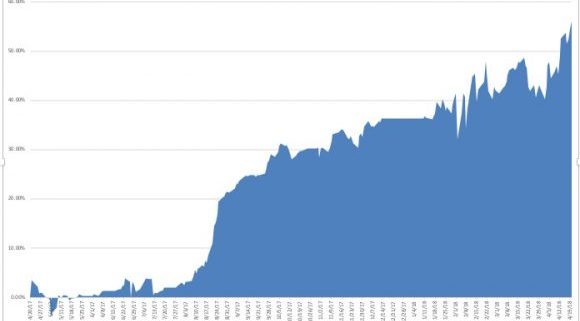

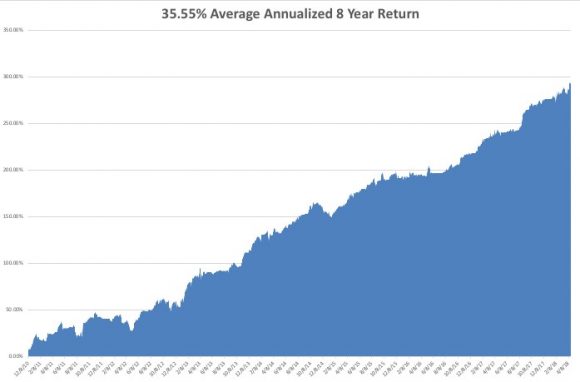

That brings April up to an amazing +12.99% profit, my 2018 year-to-date to +19.75%, my trailing one-year return to +56.09%, and my eight-year performance to a new all-time high of 296.22%. This brings my annualized return up to 35.55% since inception.

The last 14 consecutive Trade Alerts have been profitable. As for next week, I am going in with a net short position, with my stock longs in Alphabet (GOOGL) and Citigroup (C) fully hedged up.

And the best is yet to come!

I couldn't help but laugh when I heard that Republican House Speaker Paul Ryan announced his retirement in order to spend more time with his family. He must have the world's most unusual teenagers.

When I take my own teens out to lunch to visit with their friends, I have to sit on the opposite side of the restaurant, hide behind a newspaper, wear an oversized hat, and pretend I don't know them, even though the bill always mysteriously shows up on my table.

This will be FANG week on the earnings front, the most important of the quarter.

On Monday, April 23, at 10:00 AM, we get March Existing-Home Sales. Expect the Sohn Investment Conference in New York to suck up a lot of airtime. Alphabet (GOOGL) reports.

On Tuesday, April 24, at 8:30 AM EST, we receive the February S&P CoreLogic Case-Shiller Home Price Index, which may see prices accelerate from the last 6.3% annual rate. Caterpillar (CAT) and Coca Cola (KO) report.

On Wednesday, April 25, at 2:00 PM, the weekly EIA Petroleum Statistics are out. Facebook (FB), Advanced Micro Devices (AMD), and Boeing (BA) report.

Thursday, April 26, leads with the Weekly Jobless Claims at 8:30 AM EST, which saw a fall of 9,000 last week. At the same time, we get March Durable Goods Orders. American Airlines (AAL), Raytheon (RTN), and KB Homes (KBH) report.

On Friday, April 27, at 8:30 AM EST, we get an early read on US Q1 GDP.

We get the Baker Hughes Rig Count at 1:00 PM EST. Last week brought an increase of 8. Chevron (CVX) reports.

As for me, I am going to take advantage of good weather in San Francisco and bike my way across the San Francisco-Oakland Bay Bridge to Treasure Island.

Good Luck and Good Trading.

There is no better sight to a hungry trader than blood in the water.

?Buy them when they?re cryin? is an excellent investment strategy that always seems to work.

There are rivers of tears being shed over the banking industry right now.

Federal Reserve officials openly told investors that after the December ?% rate hike that they would continue to do so on a quarterly basis. Only weeks later, a collapse in the stock market shattered this scenario to smithereens.

I doubt we?ll see any more Fed action in 2016.

This caught investors in bank shares wrong footed in a major way.

But wait! It gets worse!

Among the largest holders of American bank shares are the Persian Gulf sovereign wealth funds, including those for Saudi Arabia, Kuwait, Oman, Qatar, and the United Arab Emirates, my old stomping grounds. Pieces of me are still there.

The collapse in oil prices (USO) has put their budgets in tatters and they now have to sell stock to fund wildly generous social service programs. The farther Texas tea drops, the more shares they have to sell, and at $26 a barrel they have to sell bucket loads.

Had enough? There?s more.

The junk bond market (JNK) and oil company shares are suggesting that up to half of all American oil companies will go bankrupt sometime this year, mostly small ones. It all depends on how long oil stays under $40.

Unfortunately, the oil industry has been the most prolific borrower from banks for the last decade. The covenants on many of these loans require borrowers to pump and sell oil to meet interest payments NO MATTER THE PRICE! It?s a perfect formula for maxing out production and selling into a hole.

So fear of widespread energy defaults has also been dragging down bank shares as well.

Some of the moves so far in this short year have been absolutely eye popping. Bank of America (BAC) has plunged 31% from its recent high, while Citibank (C) is down 32% and JP Morgan is off 19%. Basically, they all had a terrible year just in the month of January.

Bank shares have been beaten so mercilessly that they are approaching levels last seen at the nadir of the 2009 financial crisis.

Except that this time, there is no financial crisis, not even the hint of one. For the past seven years, banks have been relentlessly raising capital, reducing leverage, and growing BIGGER.

They proved last time that they were too big to fail. Now they are REALLY too big to fail. Default rates aren?t even a fraction of what we saw during the bad old days. Energy industry borrowing is only a tenth the size of bank home loan portfolios going into the crisis.

Blame the Dodd-Frank financial regulation bill, which requires banks to hold far more capital In US Treasury bonds (TLT) than in the past, which by the way, are doing spectacularly well.

Blame ultra cautious management.

Whatever the reason, Big US banks are now solid as the Rock of Gibraltar.

Which means I?m starting to get interested. Interest rates don?t go down forever, nor does the price of oil. And scares about loan defaults are being wildly exaggerated by the media, as always.

But there is more than one way to skin a cat.

All of these companies issue high yield preferred stock with exceptionally high dividends. For example, Bank of America issued 6.2% yielding paper as recently as October. It is paying something like 8% now.

Since these securities are stock, you get to participate in price appreciation when the panic subsides. A guaranteed 8% return, plus the prospect of substantial capital appreciation? Sounds like a pretty good deal to me.

Google bank preferred shares and you will find an entire world out there of specialist advisors, dedicated newsletters and even day trading and hedging recommendations.

One thing to keep in mind here is that you should only buy ?non callable? paper. This prevents issuers from stealing your paper when better times return to cut their interest payouts.

There is another way to play this beleaguered sector.

You can buy the iShares S&P US Preferred Stock Index Fund ETF (PFF), which owns a basket of preferred stocks almost entirely made up of bank shares. As of today it was yielding 5.62%. To visit the fund?s website, please click link: https://www.ishares.com/us/products/239826/ishares-us-preferred-stock-etf.

Regular readers of this letter are probably weary of me harping away about the financials as a great place to put your money for the rest of 2014.

Never mind that these names have all jumped 10% in the past month. But this is not an ?I told you so? story. This is more of a ?But wait, there?s more,? story.

The basis for my call is quite simple. I believe that bond prices are peaking, and yields bottoming. As mining the yield curve is a major source of bank profits, borrowing short term and lending long term, a rise in interest rates falls straight to the bottom line. Thus, buying banks is an indirect way of selling short the bond market.

However, there are many more reasons to overweight this long neglected sector. In a market that has gone virtually straight up for the past three years, many large institutions are going to be forced to roll money out of leaders, like my favored technology, energy and health care, into laggards, such as the financials.

Expect this trend to accelerate as we head into yearend institutional book closing, which start as early as October 30.

Look at other important drivers of bank profits, and you?ll find them at multi decade lows.

Trading and investment banking volumes are off 30%-40% from mean historic levels. We options traders already know this all too well, as turnover has cratered and spreads widened due to investor lack of interest.

This is especially true of put options, which are now being given away virtually for free. Volatility that seems to permanently live at the $12 handle is another such indicator of this disinterest.

This will not last. If my ?Golden Age? scenario plays out in the 2020?s (click here for ?Get Ready for the Coming Golden Age?), trading and investment banking volumes will not only double to return to the norms, they will skyrocket tenfold from today?s tedious, moribund levels.

Indeed, I have recently discovered an entire subculture of financial oriented private equity firms currently amassing portfolios that are betting on precisely such an outcome. Think of big, smart, long-term money. The big bets on the coming decade are being made now.

There is another ripple in the case for banks. After passage of the Financial Stability Act of 2010, otherwise known as ?Dodd Frank?, banks became target numero uno of the federal government. The public?s demand for accountability for the 2008-09 crash knew no bounds.

As a result, the fines and settlements with the big banks, most of which were rescued from bankruptcy by the government, now well exceed $100 billion. Four years into the enforcement onslaught, the Feds are running out of scandals to prosecute. There is nothing left for the banks to plead guilty to.

This means that a major portion of the banks? costs are about to disappear, not only new massive fines, but hundreds of millions of dollars in legal fees and diverted management time as well. More money drops to the bottom line.

Dramatically rising income? Substantially falling costs? Sounds like ?Ka-ching? to me, and a ?BUY? for the bank stocks.

The bottom line is that bank stock could double from here in coming years. It is not hard to pick names. Bank of America (BAC) took the big hit on fines and settlements, and therefore should enjoy the largest bounce.

So should Citigroup (C), which came the closest to vaporizing. And for good measure, I?ll throw in American Express (AXP) as a play on the burgeoning credit card spending by the growing class of well to do.

Barney Frank Had a Few Things to Say

Barney Frank Had a Few Things to Say