Cord-cutting is going into overdrive as linear TV viewership has just fallen below 50% nationally in July for the first time.

Big changes are about to happen.

This has major ramifications for not only the tech sector but for the broader economy, society, and geopolitics.

We are here to talk about the tech and the sinking of linear TV does mean relative gains for online streamers.

Broadcast and cable each hit a new low of 20% and 29.6% of total TV usage, respectively, to combine for a linear television total of 49.6%.

Has the quality of linear TV channels soured in quality or what is the deal?

It could be a functional reason, as Baby Boomers are watching linear tv because they haven’t figured out the streaming thing yet.

The ease of flipping on the tv with a remote cannot be understated.

In the future, the result is that linear tv penetration will be down to 20% level in around 20 years.

The players that will begin advancing further center stage into the national consciousness are YouTube (GOOGL), Netflix (NFLX), and Amazon Prime Video (AMZN).

They saw month-over-month viewership increases of 5.6%, 4.2%, and 5%, respectively, in July.

Don’t expect a rebound, because linear tv is bleeding viewers reflecting how bad TV channels have become.

Ad revenue across our media network coverage fell 13% on average in Q2, down from -8% in 1Q, which included the Super Bowl.

That being said, certain streamers haven’t exactly cracked the code either, as Peacock, Disney+, Hulu, ESPN+, Paramount+, Max and Discovery+ were down by about 500,000 combined.

However, on the whole, subscriber growth was 8.5% year-over-year with highlights like Netflix adding 5.9 million subscribers in the second quarter.

Comcast's Peacock (CMCSA) was able to grow its subscriber base 84% year-over-year to 24 million, up from the prior 13 million, as the streamer works to catch up to its peers amid a significant lag.

Direct-to-consumer advertising (DTC) grew 27% on average across media companies including Disney (DIS), Comcast, Warner Bros. Discovery (WBD), and Paramount (PARA). That's double from the 13% growth posted in the first quarter.

Comcast is the farthest behind, as only 14% of its estimated revenues are expected to come from DTC in 2024 with the other 85% stemming from its linear networks. Disney is the farthest along, with DTC revenue expected to surpass linear network revenue for the first time in 2024.

As linear tv is headed to the dustbin of history, streaming is also getting more expensive.

Personally, that is what I have seen as many platforms are starting to push the $100 plus per month level.

Many might remember when streaming was $20-$40 per month.

Therefore, I am not surprised to see single-digit growth for streaming as high prices crimps demand.

It’s true that mass media is fracturing into different niches and communities and that isn’t so fantastic for big media corporations as it could mean higher costs and a smaller total addressable audience.

I still do believe there is growth in streaming but not at the elevated levels like the 20% or 30% range.

Customer acquisition will also become more difficult and expensive as people really need to be convinced to move platforms or online channels.

The golden age of streaming growth is over and now each inch will be fought tooth and nail by more competition.

In the short term, I believe a dip in CMCSA should be bought, as they are still driving users to the Peacock platform. NFLX is still worth a trade on the dip as well, but I would avoid DIS until they structurally upgrade the company.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-08-16 16:02:232023-08-27 19:39:58Cord-Cutting is Taking Over

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GREAT ROTATION OF 2023 IS ON)

(AAPL), (TSLA), (NVDA), (GOOGL), (OXY), (QQQ),

(TSLA), (WPM), (UNG), (BRK/B), (RIVN), (TLT)

When I boarded the Queen Mary II in early July, big technology stocks (AAPL), (TSLA), (NVDA), (GOOGL) were on fire and knew no bounds, while bonds (TLT) were holding steady at a 3.40% yield. Energy stocks (OXY) were scraping the bottom.

One month later and big tech is in free fall while energy, commodities, and precious metals have taken over the lead. Bonds are probing for new lows at a 4.20% yield and may have another $5.00 of downside.

The Great Rotation of 2023 has begun!

The only question is how long it will last.

I happen to believe that we are into a traditional summer correction that could last until the usual September or October bottom. That is when I will be picking up long-term bull LEAPS with both hands. After that, it’s off to the races once again to new all-time highs once again.

Except that this time, everything will go up, both big tech, the domestics recovery plays, and bonds. That’s because they will be discounting the next great market mover, several successive cuts in interest rates by the Federal Reserve certain to take place in 2024.

We all know that markets discount market-moving developments six to nine months in advance. That means you should start buying about….September or October.

Perhaps the best question asked at my many strategy luncheons this summer came from a dear old friend in London. “Where is all the money coming from to pay for all this”? The answer is, well complicated. I’ll give you a list”

1) All of the Quantitative Easing money created since 2008, some $10 trillion worth, is still around. It is just sleeping in 90-day T-bills.

2) With inflation basically over, thanks to hyper-accelerating technology and collapsing energy prices, the case for the Fed to stop raising and start cutting interest rates is clear.

3) Falling interest rates trigger a collapse in the US dollar.

4) Earnings at big tech companies explode, which earn about half of their revenues from abroad.

5) The falling interest rate sectors are also set alike. These include energy, commodities, precious metals, and bonds.

6) A cheap greenback pours gasoline on the economy.

7) The $1 trillion in stimulus approved last year provides the match as most of it has yet to be spent.

8) China finally recovers and turbocharges all of the above trends.

9) 2024 is a presidential election year and the economy always seems to do mysteriously well going into such events.

10) All we are left to do is sit back and watch all our positions go up, figure out how we are going to spend all that money, and sing the praises of the Mad Hedge Fund Trader.

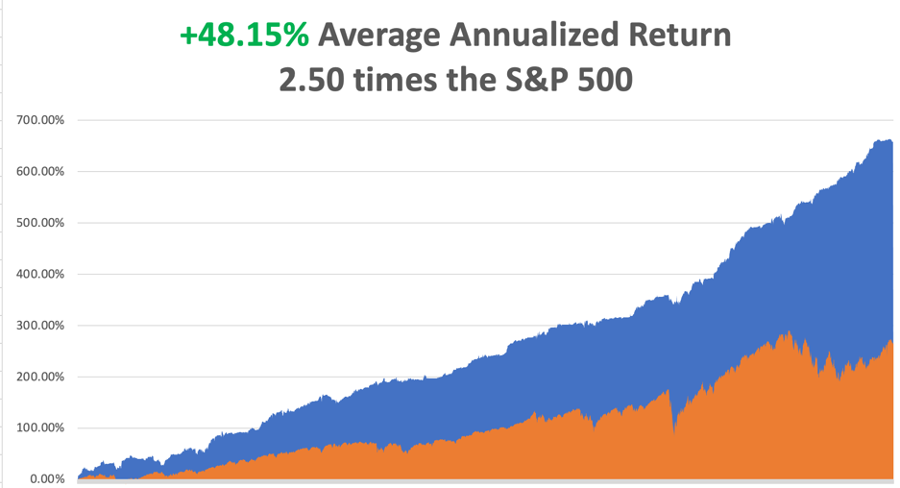

So far in August, we are down -4.70%. My 2023 year-to-date performance is still at an eye-popping +60.80%. The S&P 500 (SPY) is up +17.10% so far in 2023. My trailing one-year return reached +92.45% versus +8.45% for the S&P 500.

That brings my 15-year total return to +657.99%. My average annualized return has fallen back to +48.15%, some 2.50 times the S&P 500 over the same period.

Some 41 of my 46 trades this year have been profitable.

The Nonfarm Payroll drops to 187,000 in July, a one-year low, less than expectations. The Headline Unemployment Rate returned to 3.5%, a 50-year low. The soft-landing scenario lives! That’s supposed to be impossible in the face of 5.25% interest rates. Average hourly earnings grew at a restrained 3.6% annual rate. Half of the new jobs were in health care. At the rate we are aging, that is no surprise.

Rating Agencies Strike Again, with Moody’s threatened downgrade of a dozen regional banks. Stocks took it up on the nose giving up Monday’s 400-point gain. Higher funding costs, potential regulatory capital weaknesses, and rising risks tied to commercial real estate are among strains prompting the review, Moody’s said late Monday. The summer correction is finally here.

Berkshire Hathaway Post Record Profit, with profits up 38% and interest and other investment income growing sixfold as Warren Buffet’s trading vehicle goes from strength to strength to strength. Sky-high interest rates enabled its Geico insurance holding to really coin it this time. Buffet turns 93 this month. Keep buying (BRK/B) on dips. Our LEAPS are looking great, up 327% in 11 months.

Rivian Beats, losing only $1.08 a share versus an expected $1.41. The stock jumped 3% on the news. The gross profit per vehicle showed a dramatic improvement at $35,000. The production forecast edged up from 50,000 to 52,000 vehicles for 2023. Momentum is clearly improving making our LEAPS look better by the day. Buy (RIVN) on dips as the next (TSLA).

Deflation Hits China, as the post-Covid recovery continues to lag. Their Consumer Price Index fell 0.3% YOY. Imports and exports are falling dramatically as trade sanctions bite. Youth unemployment hit a new high as 11.6 million new college grads hit the market. Global commodities could get hit but so far the stocks aren’t seeing it. Avoid anything Chinese (FXI), even the food.

Inflation Jumps, 0.2% in July and 3.2% YOY. Rents, education, and insurance (climate change) were higher while used cars were down 1.3% and airfares plunged by 8.1%. Stocks rallied on the small increase preferring to focus on the smallest back-to-back increase in two years. Bonds (TLT) rallied big. The big question is what will the Fed do with this?

Weekly Jobless Claims came in at a strong 278,000, showing the Fed’s high-interest rate policy is having an effect on the jobs market. Stocks want to know how much longer it will last.

Natural Gas Soars to a new high and accomplished an upside breakout on all charts. European gas prices have just jumped 40%. An Australian strike shut down an LNG export facility. Energy traders are looking for higher highs. My (UNG) LEAPS, a Mad Hedge AI pick, are looking great, doubling off our cost in two months.

Biden Cracks Down on Technology Investment in China, especially on our most advanced tech which can be used in weapons development. Tech investment in the Middle Kingdom is already down 70% over the last two years. No point in selling China the rope with which to hang us.

Home Mortgage Rates Hit a 22-Year High, at 7.08%. But the existing home market is heating up and the new home market is absolutely on fire in anticipating of a coming rate fall. You can’t beat a gale-force demographic tailwind.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, August 14 at 8:00 AM EST, the US Consumer Inflation Expectations are out,

On Tuesday, August 15 at 8:30 AM, US Retail Sales are released.

On Wednesday, August 16 at 2:30 PM, the US Building Permits are published.

On Thursday, August 17 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, August 18 at 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, occasionally, I tell close friends that I hitchhiked across the Sahara Desert alone when I was 16 and I am met with looks that are amazed, befuddled, and disbelieving, but I actually did it in the summer of 1968.

I had spent two months hitchhiking from a hospital in Sweden all the way to my ancestral roots in Monreale, Sicily, the home of my Italian grandfather. My next goal was to visit my Uncle Charles who was stationed at the Torreon Air Force base outside of Madrid, Spain.

I looked at my Michelin map of the Mediterranean and quickly realized that it would be much quicker to cut across North Africa than hitching all the way back up the length of Italy, cutting across the Cote d’Azur, where no one ever picked up hitchhikers, then all the way down to Madrid, where the people were too poor to own cars. So one fine morning found me taking deck passage on a ferry from Palermo to Tunis. From here on, my memory is hazy and I remember only a few flashbacks.

Ever the historian, even at age 16, I made straight for the Carthaginian ruins where the Romans allegedly salted the earth to prevent any recovery of a country they had just wasted. Some 2,000 years later it, worked as there was nothing left but an endless sea of scattered rocks. At night, I laid out my sleeping bag to catch some shut-eye. But at 2:00 AM, someone tried to bash my head in with a rock. I scared them off but haven’t had a decent night of sleep since.

The next day, I made for the spectacular Roman ruins at Leptus Magna on the Libyan coast. But Muamar Khadafi pulled off a coup d’état earlier and closed the border to all Americans. My visa obtained in Rome from King Idris was useless.

I used to opportunity to hitchhike over Kasserine Pass into Algeria, where my uncle served under General Patton in WWII. US forces suffered an ignominious defeat until General Patton took over the army 1n 1943. Some 25 years later, the scenery was still littered with blown-up tanks, destroyed trucks, and crashed Messerschmitts. Approaching the coastal road, I started jumping trains headed west. While officially the Algerian Civil War ended in 1962, in fact, it was still going on in 1968. We passed derailed trains and smashed bridges. The cattle were starving. There was no food anywhere.

At night, Arab families invited me to stay over in their mud brick homes as I always traveled with a big American Flag on my pack. Their hospitality was endless, and they shared what little food they had.

As a train pulled into Algiers, a conductor caught me without a ticket. So, the railway police arrested me and on arrival took me to the central Algiers prison, not a very nice place. After the police left, the head of the prison took me to a back door, opened it, smiled, and said “si vou plais”. That was all the French I ever needed to know. I quickly disappeared into the Algiers souk.

As we approached the Moroccan border, I saw trains of camels 1,000 animals long, rhythmically swaying back and forth with their cargoes of spices from central Africa. These don’t exist anymore, replaced by modern trucks.

Out in the middle of nowhere, bullets started flying through the passenger cars splintering wood. I poked my Kodak Instamatic out the window in between volleys of shots and snapped a few pictures.

The train juddered to a halt and robbers boarded. They shook down the passengers, seizing whatever silver jewelry and bolts of cloth they could find.

When they came to me, they just laughed and moved on. As a ragged backpacker, I had nothing of interest for them.

The train ended up in Marrakesh on the edge of the Sahara and the final destination of the camel trains. It was like visiting the Arabian Nights. The main Jemaa el-Fna square was amazing, with masses of crafts for sale, magicians, snake charmers, and men breathing fire.

Next stop was Tangiers, site of the oldest foreign American embassy, which is now open to tourists. For 50 cents a night, you could sleep on a rooftop under the stars and pass the pipe with fellow travelers which contained something called hashish.

One more ferry ride and I was at the British naval base at the Rock of Gibraltar and then on a train for Madrid. I made it to the Torreon base main gate where a very surprised master sergeant picked up a half-starved, rail-thin, filthy nephew and took me home. Later, Uncle Charles said I slept for three days straight. Since I had lice, Charles shaved my head when I was asleep. I fit right in with the other airmen.

I woke up with a fever, so Charles took me the base clinic. They never figured out what I had. Maybe it was exhaustion, maybe it was prolonged starvation. Perhaps it was something African. Possibly, it was all one long dream.

Afterwards, my uncle took for to the base commissary where I enjoyed my first cheeseburger, French fries, and chocolate shake in many months. It was the best meal of my life and the only cure I really needed.

I have pictures of all this which are sitting in a box somewhere in my basement. The Michelin map sits in a giant case of old, used maps that I have been collecting for 60 years.

Mediterranean in 1968

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2023/08/young-john-1968-scaled-e1692035288591.jpg429400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-08-14 09:02:072023-08-14 14:39:58The Market Outlook for the Week Ahead, or the Great Rotation of 2023 is On

It’s incredible that a 7% increase year-over-year in revenue means an extra $5 billion in just one quarter.

That’s what happens when a company is a behemoth, and the company I am talking about is Alphabet, or better known as Google (GOOGL).

Some of these tech companies are so large that growth rates don’t mean much unless they are negative.

Whether it is 3% or 6%, the nominal amount of revenue increase is gargantuan.

The law of large numbers is certainly valid in these situations so don’t expect multi-trillion dollar tech firms to grow 30% or 40% like they used to.

As I correctly predicted, Google and similar companies are doing just fine this earnings season, and I believe they could have gotten away with even 3% growth.

The 7% growth translated into a 7% bump in GOOGL shares this morning showing that investors care more about the additional $5 billion in revenue rather than the low growth rate.

For the fourth straight quarter, Google reported growth in the single digits as it reckons with a pullback in digital ad spending that reflects concerns about the economy.

Across the industry, investors will be looking for updates on cost-cutting measures implemented earlier in the year and the impact of artificial intelligence investments on profitability.

Revenue in Google’s cloud unit, which includes infrastructure and productivity apps, increased 28%.

Google’s ad revenue rose 3.3% to $58.14 billion, up from $56.29 billion last year. YouTube ads came in above analyst expectations at $7.67 billion marginally up from $7.34 billion the year before.

Google’s “search and other” revenue rose to $42.63 billion, up slightly from last year.

The only “growth” part of the business has been the cloud and even that is starting to taper off.

Up until recently, they were expanding that business around 35% year-over-year and now they are down to 28%. In a few years, they will be down to the teens.

Google is slowing down but that doesn’t mean they aren’t profitable.

The cash cow of the ad business keeps churning out the revenue and Microsoft hasn’t turned out to be the threat to Google search that investors first thought when ChatGPT came out.

Investors reacting to 7% growth by pouring money into the stock are a good omen for the rest of big tech.

It means that these other companies, like Apple, only need to marginally outperform to get rocket fuel in their stock and I will take that for all its worth.

Any worst-case scenario will not come to fruition.

Any tech analyst who is bearish this year can be described in one way – unemployed.

The fake narrative of an “earnings recession” and higher interest rates hasn’t even put a dent in the strength of tech.

It’s like throwing pebbles at the Titanic.

Even scarier for the bears, this was supposed to finally be the entry point when a dip could present itself so the bears could get into tech to try and salvage a terrible year.

Well, now, they need to chase another 7% because Google’s ship has sailed and I have conviction that Apple will jump over the low bar for its shares to have a similar effect.

As for GOOGL, I am a buyer on the next mini-dip.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-07-26 17:02:492023-07-31 15:51:46Good Signs for Tech

The probability of a recession taking place over the next 12 months is now low ranging as high as 20%. If it reaccelerates, not an impossibility, you can take that up to 100%.

And here’s the scary part. Bear markets front-run recessions by 6-12 months, i.e. now.

We’ll get a better read on the inflation numbers over the coming months. If inflation turns hot again, the Fed will be forced to raise rates to once unimagined levels.

So, it’s time to start asking the question of what the next recession will look like. Are we in for another 2008-2009 meltdown, when friends and relatives lost homes, jobs, and their entire net worth? Or can we look forward to a mild pullback that only economists and data junkies like myself will notice?

I’ll paraphrase one of my favorite Russian authors, Fyodor Dostoevsky, who in Anna Karenina might have said, “All economic expansions are all alike, while recessions are all miserable in their own way.”

Let’s look at some major pillars of the economy. A hallmark of the 2008 recession was the near collapse of the financial system, where the ATMs were probably within a week of shutting down nationally. The government had to step in with the TARP, and mandatory 5% equity ownership in the country’s 20 largest banks.

Back then, banks were leveraged 40:1 in the case of Morgan Stanley (MS) and Goldman Sachs (GS), while Lehman Brothers and Bear Stearns were leveraged 100:1. In that case the most heavily borrowed companies only needed markets to move 1% against them to wipe out their entire capital. That is exactly what happened. (MS) and (GS) came within a hair’s breadth of going the same way.

Thanks to the Dodd Frank financial regulation bill, banks cannot leverage themselves more than 10:1. They have spent a decade rebuilding balance sheets and reserves. They are now among the healthiest in the world, having become low-margin, very low-risk utilities. It is now European and Chinese banks that are going down the tubes.

How about real estate, another major cause of angst in the last recession? The market couldn’t be any more different today. There is a structural shortage of housing, especially at entry level affordable prices. While liar loans and house flipping are starting to make a comeback, they are nowhere near as prevalent as a decade ago. And the mis-rating of mortgage-backed securities from single “C” to triple “A” is now a distant memory. (I still can’t believe no one ever went to jail for that!).

And interest rates? We went into the last recession with a 6% overnight rate and a 7% 30-year fixed rate mortgage. Here we are once again.

The auto industry has been in a mild recession for the past two years, with annual production stalling at 15 million units, versus a 2009 low of 9 million units. In any, case the challenges to the industry are now more structural than cyclical, with new buyers decamping en masse to electric vehicles made on the west coast.

Of far greater concern are industries that are already in recession now. Energy has been flagging since oil prices peaked 18 months ago, despite massive tax subsidies. It is suffering from a structural oversupply and falling demand.

Retailers have been in a Great Depression for five years, squeezed on one side by Amazon and the other by China. A decade into store closings and the US is STILL over-stored. However, many of these shares are already so close to zero that the marginal impact on the major indexes will be small.

Financials and legacy banks are also facing a double squeeze from Fintech innovation and collapsing interest rates. All of those expensive national networks with branches on every street corner will be gone later in the 2020s.

And no matter how bad the coming recession gets technology, now 30% of the S&P 500, will keep powering on. Combined revenues of the “Magnificent Seven” in Q1 are at records. That leaves a mighty big cushion for any slowdown. That’s a lot more than the “eyeballs” and market shares they possessed a decade ago.

So, netting all this out, how bad will the next recession be? Not bad at all. I’m looking at a couple of quarters' small negative numbers, like two back-to-back -0.1%’s. Then we’ll see a recovery and probably another decade of decent US growth.

The stock market, however, is another kettle of fish. While the economy may slow from a 2.2% annual rate to -0.1% or -0.2%, the major indexes could fall much more than that, say 30% to 40%.

Earnings multiples are still at a 19X high compared to a 9X low in 2009. Shares would have to drop 53% just to match the last low. Equity weightings in portfolios are low. Money is pouring out of stock funds into bond ones.

Corporations buying back their own shares have been the principal prop from the market for the past three years. Some large companies, like Kohls (KSS), have retired as much as 50% of their outstanding equity in ten years.

The Next Bear Market is Not Far Off

https://www.madhedgefundtrader.com/wp-content/uploads/2019/08/What-the-Next-Recession-Will-Look-Like.jpg400400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-07-21 09:04:122023-07-21 15:33:10What the Next Recession Will Look Like

The future is here, and for some, the news isn’t good.

The big picture suggests that generative artificial intelligence stocks will benefit handsomely from this groundbreaking technology, but the losers aren’t as obvious as one might think.

If one might believe this is the cue to jumping head first into becoming an artificial intelligence programmer then think again.

Ironically enough, many of these jobs will, yes, be taken by the very technology itself, and we have received confirmation that this trend is likely to occur from management that makes the decisions of which staff to pay.

Why pay humans when an algorithm can do the same job?

Recently, a prominent generative AI executive stated that coders are at risk of losing jobs in the next 2-4 years.

This executive originates from one of the leading companies in the space, so it’s not like some fake expert offering his two cents either.

During an interview, this executive suggested that countries like India, where many IT jobs get outsourced, might be in trouble in the next few years because firms can just adopt AI tools to write, read, and review codes.

Even labor laws can’t prevent this giant replacement of human labor.

Tech giants like Google and Microsoft have shared similar concerns, though they argue that AI will create new jobs and humans need to co-exist with the technology.

Here is a quick summary of what I learned.

Outsourced coders up to level three programmers will be gone in the next year or two.

That's because new generative AI models "are like really talented grads" and will replace those who sit "in front of a computer" and never get noticed.

So it affects different models in different countries in different ways in different sectors.

In the United States, the two-week notice is real, and coders and engineers at international IT firms are at risk once Silicon Valley figures out they are expendable.

I must say that this might be the job apocalypse that many have been predicting.

The belt-tightening going on in Silicon Valley is just the beginning.

Next, we will see AI get rid of even more lucrative positions.

Google (GOOGL) CEO Sundar Pichai and Microsoft (MSFT) CEO Satya Nadella have also previously shared concerns about potential job loss due to AI.

Pichai and Nadella have repeatedly said that AI will eliminate grunt work.

In large corporations, many workers do just that – grunt work.

Not everyone is making strategic decisions that affect the direct fortunes of the company like Nadella and Pichai. Not everyone is Elon Musk.

AI will replace humans and CEOs like Pichai and Nadella are just being polite because they preside over a massive workforce.

They cannot come out in public and say that everyone will get fired. If they did that, workers would protest, revolt, and unionize as fast as possible. At the bare minimum, they will lay down flat and barely move a finger, resulting in company morale tanking.

At the stock level, this will boost revenue, margins, and profitability to a new golden era of tech stocks.

Workforces are about to get even leaner, and I am not talking about just firing the chief diversity officer or the chief climate change officer. The chief vegan foods officer for the office cafeteria was fired in the last round of cuts. The next round of cuts will start migrating up the value chain and it will be oh so painful.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-07-19 16:02:502023-08-01 13:22:21Coders Are Next To Go

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-07-12 09:06:122023-07-12 11:17:33July 12, 2023

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.