Tech workers are slowly losing their leverage in the job market that has largely been unforgiving to the average tech worker.

Part of that is due to inching closer to the much-awaited recession that everyone has been waiting for so investors can finally take advantage of 0% interest rates again.

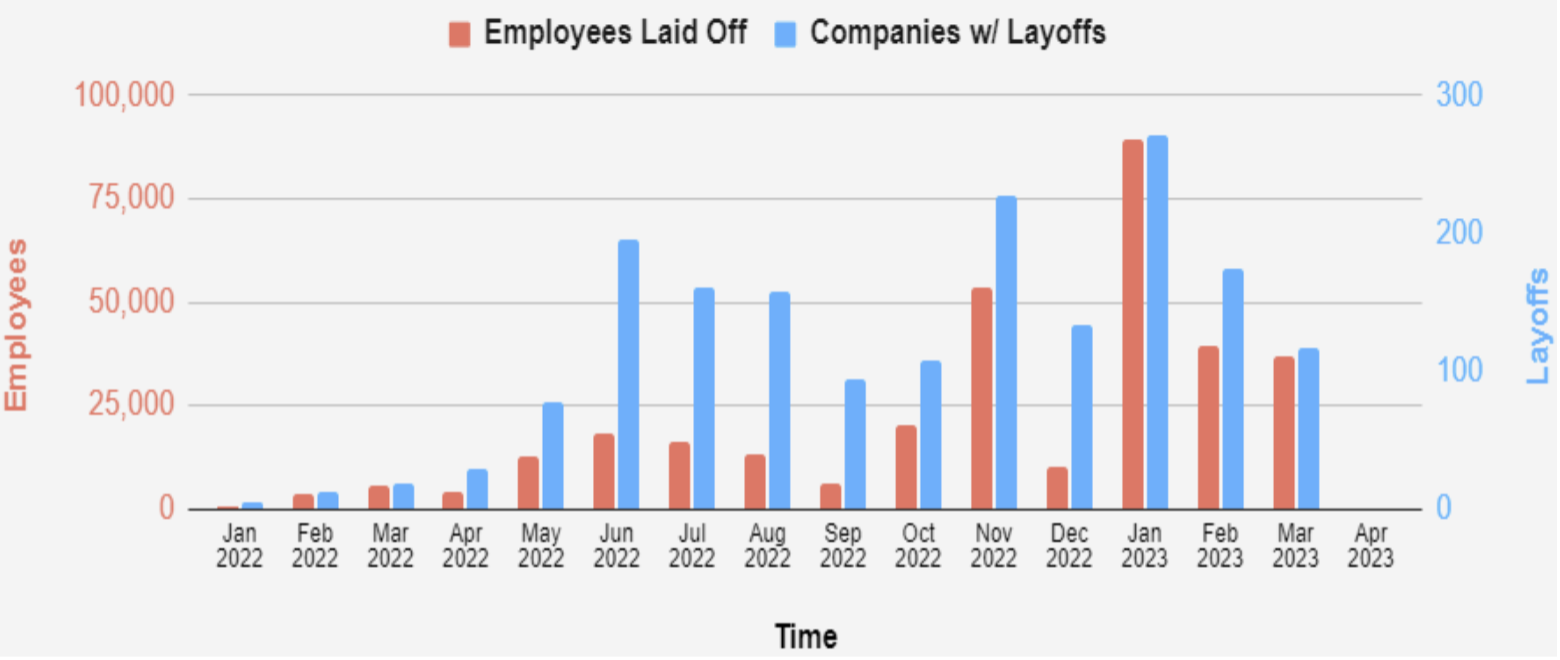

The number breakdown shows that around 330,000 tech workers have been fired by 1,600 tech firms.

In the first month of 2023, 167,000 of those cuts occurred representing an acceleration of tech firings lately.

Some of the noteworthy cuts have been 27,000 jobs at Amazon, 12,000 at Google, and 10,000 at Meta.

Sure, the top 10% are untouchable and can work from a nuclear submarine if desired, but the average joe schmoe is living on borrowed time in the tech sector.

News of Google removing free snacks and artisanal brewed coffee from the offices in Mountain View, California struck fear into the hearts of the ultra-pampered tech worker that has never known a staff reduction in their career.

Now many tech workers who gave the middle finger to their middle manager before the lockdowns are now romanticizing how good things were before 2020.

Many tech workers now regret moving on to van life or moving to the beach of Cancun to sell donkey rides to digital nomads.

They want their old job back and specifically, they want their old pay level back.

Empirical evidence suggests that the so-called Great Resignation is now morphing into the Great Regret.

Thousands of workers began quitting their jobs in early 2021 because they didn’t “feel” empowered or appreciated by their boss. Feelings were hurt. Tears were shed.

These workers who felt jilted jumped at the chance to increase their salary during the arbitrary lockdowns because of a tight labor market.

Now, as life returns to normal, many of the perks they signed up for are being rescinded and the cost-of-living crisis is dumping fuel on the bonfire.

A third of office workers said the cost-of-living crisis had changed how they feel about their current job.

Just under a quarter said they were tired of hybrid working, mostly because they have minimal access to the higher ups they need to connect with for specific promotions.

Lack of access equates to lower positions and the obvious knock on of lower pay, lower benefits, and lower team morale.

Many are also moonlighting secretly while working full time jobs which have resulted in a big reduction in efficiency.

The once game changing pay rises now pale in comparison to the rising cost of living.

More than four in five workers admitted to keeping in touch with their former managers, with almost a third stating that this was for the primary purpose of keeping the door open for future job opportunities

Painful rounds of deep lay-offs in the tech sector and warnings of a looming recession appear to have smashed the lingering leverage workers still thought they had to crowbar a nice wage increase.

As much as 330,000 tech layoffs jump out on paper, tech firms need to fire over 1 million employees.

The fat hasn’t been trimmed to the bone yet.

The recession will approach in 2023 and this will be the optimal chance to set the record straight for employers to grab back negotiating leverage from the renegade employees while shrinking down to a leaner operation.

Tech is in great position to weather the recession and will be the first industry to over perform after the recession ends.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/04/layoff.png6601560Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-05 17:02:292023-04-26 00:10:48Reverting Back to Normal Staffing Levels

(MARKET OUTLOOK FOR THE WEEK AHEAD, or QE IS BACK!)

(SPY), (BITCOIN), (GLD), (SLV), (ARKK), (NVDA),(AAPL), (GOOGL), (META), (SCHW), (MS), (FRC), (TLT), (KBWH)

Remember the endless flood of the money supply that went on for a decade, floating all boats?

It's back!

One need look no further than the Fed balance sheet, which ratcheted up a breathtaking $297 billion last week. That offsets three months worth of quantitative tightening if it even still exists.

This is further confirmed by the classic QE asset classes, which saw their best week in a year. Bitcoin jumped by 30%, gold (GLD) gained 8%, silver (SLV) popped 12%, and technology stocks went on a tear. Even bonds did well, with the (TLT) up $8.00 from the previous week’s low.

Big tech stocks like (NVDA), (AAPL), (GOOGL), and (META) are now seen as the new “safe “stocks, thanks to their gigantic balance sheets and immense cash flows. Tech funds have seen net inflows for the past four consecutive weeks, delivering the largest new investment in three years. The ARK Innovation Fund (ARKK) saw its biggest inflows since the 2021 peak.

It's the regional banking crisis that is reverting the Fed to its old habits, all prompted by the mindless management of Silicon Valley Bank. All California assets were dumped as California was about to fall into the ocean, like Charles Schwab (SCHW), Bank of America (BAC), and First Republic Bank (FRC).

That puts the Fed in a quandary, which renders its interest rate decision on Wednesday, March 22 at 2:00 PM EST, because the last thing you do in a financial crisis is raise interest rates. That’s what the Fed did in 1929, extending the Great Depression from 10 days to 10 years.

My bet is that they raise by 25 basis point one more time because it’s already in the mail. The regional banking crisis has pulled forward any recession and therefore the recovery.

After that, there will be no interest rate rises for a decade, which the Fed may hint at in its statement and the following press conference. The cuts will start in June and continue rapidly after that. That’s when the economic data catch up with the reality that is happening right now, which is hugely deflationary.

(NVDA) and (TSLA) already know this, which are rising sharply on Friday.

The action certainly caught the attention of the US Treasury, which seemed willing to jump in with guarantees at the drop of a hat. There has been a massive flight of capital from the heartland to the coasts where the top 20 “too big to fail” banks live.

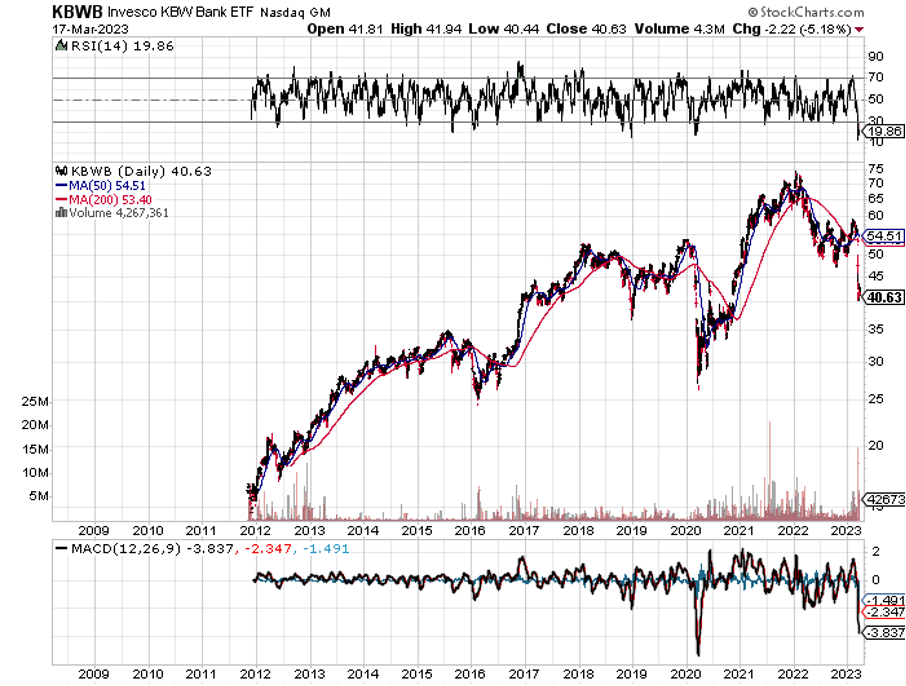

It’s another example of an industry deregulating itself out of existence, which obtained looser capital requirements after heavy lobbying in 2018. At one point, JP Morgan bank, the safest of the safe, was turning down new account applications. This means that the trade of the decade is setting up for the banks. In the wake of the 2008 financial crisis, the Invesco Bank ETF (KBWB) rose 75% in a year. I expect the same to happen this time around. It has already plunged by 30% in 2023, so it has to rise by 50% just to get back to where it was in January, but with bank deposits now guaranteed and more safeguards in place.

And if you are worried about hidden unrealized losses on bank balance sheets, I list below the safest banks ranked by capital ratios NET of losses when marked to market.

14.5% Goldman Sachs (GS)

13.4% Morgan Stanley (MS)

11.5% JP Morgan Bank (JPM)

11.3% Citigroup (C)

8.7% State Street

5.9% Bank of America (BAC)

No surprise that (GS) and (MS) is at the top where the mark-to-market culture is strong. A strong dose of regulation from the SEC helps too. (BAC) takes a big hit because of the largest holdings of low-yielding mortgages which can’t be marked to market unless they are sold or defaulted.

The crisis brought the traditional recession indicators out of the closet last week. A big one is crude oil prices, which hit a 2 ½ year low at $65 a barrel. It turns out that not only banks but oil producers are hurt by high interest rates as well. Some 120 million barrels have gone into storage in the beast nine months and the market is oversupplied by 300,000 barrels a day.

Only OPEC Plus can put in a floor by cutting production, which they are loathed to do as it brings immediate spending cuts. Or the greatest oil trader in history, Joe Biden of Delaware, can cover his short in the Strategic Petroleum which he sold at $90 last year. You may have to wait for a future Republican administration for that to happen.

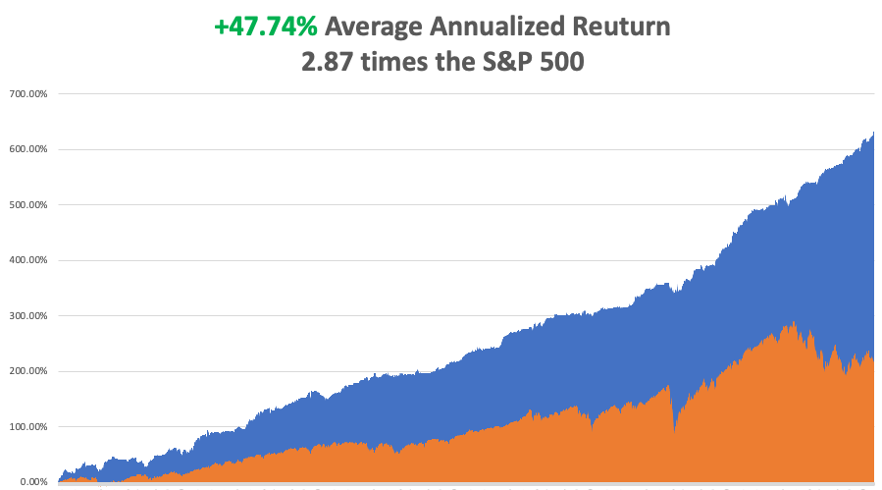

While markets crashed, investors have been jumping out of windows, the world appeared to be ending, and the rain continuing incessantly, Mad Hedge continued on up tear with March up +5.61%.

My 2023 year-to-date performance is now at an eye-popping +31.37%. The S&P 500 (SPY) is up +2.63% so far in 2023. My trailing one-year return maintains a sky-high +87.76% versus -15.55% for the S&P 500.

That brings my 15-year total return to +628.56%, some 2.87 times the S&P 500 (SPX) over the same period. My average annualized return has recovered to +47.76%, another new high.

At the market lows, I covered shorts in my Tesla and March NVIDIA positions. I religiously adhered to my stop loss discipline, stopping out of my April short in NVIDIA (NVDA) when the melt-up ensued, my only remaining equity short. I also established a new short in (TLT) at the market high, my first since August.

Silicon Valley Bank fails to sell, but the FDIC stepped in to guarantee all deposits. The FDIC took over Signature Bank in New York as well. If they hadn’t, there would be lines snaking out the doors of every small bank in America Monday morning. The cost is being born by steeper deposit insurance premiums for the banking industry, which will no doubt cause some grumbling. There are 100 banks that would leap to buy Silicon Valley Bank to gain a franchise in the world’s fastest growing technology center. They just need a few hours to get a handle on the bank’s loan portfolio, which only the former management really understand. Buy banks and brokers on dips (SCHW).

Is Platinum the Precious Metals Play of 2023? I am told by the insiders who know that platinum (PPLT) could be the big precious metals play of 2023. The white metal has become the principal metal used in the manufacture of catalytic converters for conventional internal combustion cars of which 15 million a year is still made in the US. There is rising demand for hydrogen fuel cells and the green hydrogen movement. The world’s second largest producer of platinum is Russia, whose supplies have been cut off. As a result, there is expected to be a 556,000-ounce shortage this year after two years of surpluses.

Say Goodbye to the 50 Basis Point Rate Hike, at the Fed meeting on March 22 in the wake of a regional banking Crisis. It’s now a quarter point….or nothing at all. In 48 hours, we have gone from “higher rates for longer” to “maybe the next rate rise is the last one.” Tech stocks are buying it after holding up incredibly well. Buy tech and big banks on dips (JPM), (BAC), (C), (SCHW).

Core Inflation Comes in Moderate, up 0.4% and 0.5% without food and energy. That is a 6.0% YOY rate, down from the 2023 high of 8.7%. Stocks extended a 300-point rally on the news. Inflation has been running at a 3.5% annual rate for the past four months, my yearend target.

Mortgage Rates Dive, off the back of a three-day, $8.00 rally in the bond market. Mortgage rates plunged by 50 basis points to 6.50% and may have more to go. Will this kick off the spring residential real estate market?

Gold (GLD) Breaks Out, crossing a key technical level and setting the options market on fire. Some gold minders saw options volume up 400%. Did the regional banking crisis put the top in interest rates, which have been weighing heavily on gold? Or maybe it’s just an old fashioned flight to safety triggered by the financial crisis. It could be presaging a global economic recovery and a coming commodity boom. (GOLD) LEAPS on the way.

Ron Baron Loaded the Boat with Charles Schwab (SCHW) Shares on Friday, as all the smart money did, including Mad Hedge. My old friend was also an early investor in Tesla (TSLA) and is now one of the largest outside shareholders. When someone offers you a dollar for 40 cents, you take it!

Swiss National Bank Steps in to Bail Out Credit Suisse, taking pressure off US market. I knew they would come in as I was a director of UBS for a year, The Swiss take care of their own. More importantly, the rolling global bank crisis has put the fear of God into the Fed, meaning that the 25 basis point hike next week may be the last for a decade. Buy “RISK ON”, especially banks.

Europe Raises Interest Rates by 50 Basis Points, catching up with the US. It’s an overreaction given the fragility of the banking system. The markets didn’t like the move. Europe has inflation at 2% higher than the US so they really had no choice

Weekly Jobless Claims Drop to 192,000, a surprising fall. The worker shortage continues unabated. It’s the biggest decline since July. If the Fed were looking for a reason to continue quantitative tightening this is it.

First Republic Bank is for Sale, the next bailout target. The mere fact that it is based in California is the problem, which many investors now apparently believe is about to break off of the North American Continent and fall into the Pacific Ocean. You never see a bank with $70 billion in cash and equivalents get in trouble. Morgan Stanley (MS) and JP Morgan are thought to be in the bidding. A group of banks deposited $30 billion into (FRC) to firewall the rest of the banking system.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, March 20, there are no data points of note.

On Tuesday, March 21 at 7:00 AM, the Existing Home Sales are announced. On Wednesday, March 22 at 7:00 AM, the Federal Reserve Open Market Committee announces its interest rate decision. A hike of 25 basis points is in the market. The published statement and following press conference will be the most important of the year, indicating whether they recognize the seriousness of the regional banking crisis and are now leaning hawkish or dovish. On Thursday, March 23 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, March 17 at 8:30 AM, the Durable Goods are released.

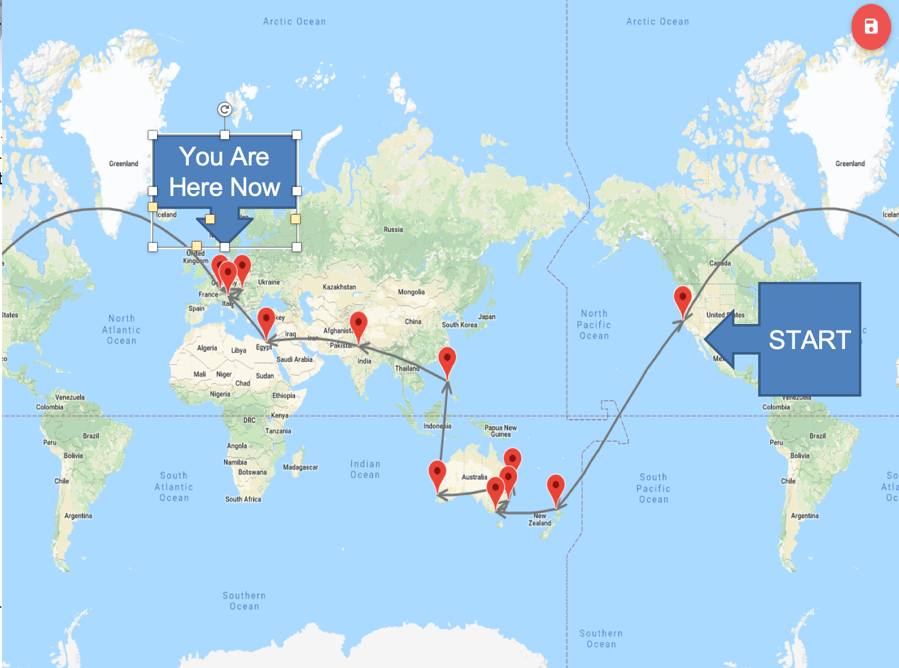

As for me, I recall my last trip around the world in 2018. I took the trip because I feared climate change would soon make visits to the equator impossible because of intolerable temperatures and the breakdown of civilization. As it turned out, the global pandemic came six months later, making such travel out of the question for two years.

I beat Phileas Fogg by 55 days, who needed 88 days to complete his trip around the world to settle a gentleman’s bet. But then, he had to rely on elephants, sailing ships, and steam engines to complete his epic voyage, or at least, the one imagined by Jules Verne.

I actually took a much longer route, using a mix of Boeings and Airbuses to fly 80 hours over 40,000 miles on 18 flights through 12 countries in only 33 days. Incredibly, our baggage made it all the way, rather than see its contents sold on the black markets of Manila, New Delhi, or Cairo.

It was a trip around the world for the ages, made even more challenging by dragging my 13 and 15-year-old girls along with me. I have always considered my most valuable asset to be the trips I took to Europe, Africa, and Asia in 1968. The comparisons I can make today some 55 years later are nothing less than awe-inspiring. I wanted to give the same gift to them.

It began with a 12 ½ hour flight from San Francisco to Auckland, New Zealand. Straight out of the airport, I rented a left-hand drive Land Rover and drove three hours to high in the steam-covered mountains of Rarotonga where we were dinner guests of a Māori tribe. To earn my dinner of pork and vegetables cooked underground, I had to dance the haka, a Māori war dance.

The Haka

Of course, with kids in tow, a natural stop was the Hobbit Village of Hobbiton 1½ hours outside of Auckland. I figured the owners of the idyllic sheep farm were earning at least $25 million a year showing tourists the movie set.

In all, I put 1,000 miles on the car in four days, even crossing New Zealand’s highest mountain range on a dirt road. The thick forests were so primeval my daughter expected to see a dinosaur around every curve. We reached our southernmost point at Mt. Ruapehu, a volcano used as the inspiration for Mt. Doom in Peter Jackson’s Lord of the Rings.

The Real Mount Doom

The focus of the Australia leg were ten strategy lectures which I presented around the country. I was mobbed at every stop, with turnouts double what I expected. The Mad Hedge Fund Trader and the Mad Hedge Technology Letter picked up 100 new subscribers in the Land Down Under in five days.

Maybe it was something I said?

My kids’ only requirements were to feed real kangaroos and koala bears, which we duly accomplished on a freezing cold morning outside Melbourne. We also managed to squeeze in a tour of the incredible Sydney Opera House in between lectures, dashing here and there in Uber cabs.

I hosted five Mad HedgeGlobal Strategy Luncheons for existing customers in five days. The highlight was in Perth, where eight professional traders and I enjoyed a raucous, drunken meal. They had all done well off my advice, so I was popular, to say the least. Someone picked up the tab without me even noticing.

After that, it was a brief ten-hour flight to Manila in the Philippines, with a brief changeover in Hong Kong, where massive protest demonstrations were underway. Ever the history buff, I booked myself into General Douglas MacArthur’s suite at the historic Manila Hotel. The last time I was here, I interviewed President Ferdinand Marcos and his lovely wife Imelda. After a lunch with my enthusiastic Philippine staff and I was on my way to the airport.

I took Malaysian Airlines to New Delhi, India, which has lost two planes over the last five years and where the crew was definitely on edge. I asked why a second plane was lost somewhere over the South Indian Ocean and the universal response was that the pilot had gone insane. Security was so tight that they confiscated a bottle of Jamieson Irish Whiskey that I had just bought in duty free.

India turned out to be a dystopian nightmare. If climate change continues, this is your preview. With temperatures up to 120 degrees in 100% humidity, people were dying of heat stroke by the hundreds. Elephants had to be hosed down to keep them alive. It was so hot you couldn’t stray from the air conditioning for more than an hour. The national radio warned us to stay indoors.

In Old Delhi, the kids were besieged by child beggars pawing them for food and there were mountains of trash everywhere. In the Taj Mahal, my older daughter passed out and we had to dump our remaining drinking water on her to cool her down and bring her back to life. We spent the rest of the day sightseeing indoors at the most heavily air-conditioned shops.

If global temperatures rise by just a few more degrees, you’re going to lose a billion people in India very soon.

On the way to Abu Dhabi, we flew directly over the tanker war at the Straits of Hormuz, one of my old flight paths during my Morgan Stanley days. It was too dusty to see any action there. We got a much better view of Sinai and the Red Sea, which, I told the kids, Moses parted 5,000 years ago (they’ve seen Charlton Heston in The Ten Commandments many times).

The Red Sea

Upon landing at Cairo, Egypt’s ever-vigilant military intelligence service immediately picked me up. Apparently, I was still in their system dating back to my coverage of Henry Kissinger’s shuttle diplomacy for The Economist in 1976. That was all a long time ago. Having two kids with me meant I was not there to cause trouble, so they were very friendly. They even gave us a free ride to the downtown Nile Hilton.

After India, Cairo, and the Sahara Desert were downright pleasant, a dry and comfortable 100 degrees. We did the standard circuit, the pyramids, and the Sphynx followed by a camel ride into the desert.

If you are the least bit claustrophobic, don’t even think about crawling into the center of the Great Pyramid on your hands and knees as we did. I was sore for two days. We spent the evening on a Nile dinner cruise, looking for alligators, entertained by an unusually talented belly dancer.

The next stage involved a one-day race to Greece, where we circled the Acropolis in all its glory, and then argued with a Greek taxi driver on how to get back to the airport. We ended up taking an efficient airport train, a remnant of the 2000 Athens Olympics. If impoverished and bankrupt Athens has such great airport train, why doesn’t New York or San Francisco?

It was a quick hop across the Adriatic to Venice Italy, where we caught an always exciting speed boat from the Marco Polo to our Airbnb near St. Mark’s Square. We ran through the ancient cathedral and the Palace of the Doges, admiring the massive canvases, the medieval weaponry, and of course, the dungeon.

One of the high points of the trip was a performance of Vivaldi’s Four Seasons in the very church it was composed for. A ferocious thunderstorm hit, flooding the plaza outside and causing the lead violinist’s string to break, halting the concert (rapid humidity change I guess).

When we got home with soggy feet, the Carabinieri had cordoned off our block with police tape because a big chunk of our 400-year-old roof had fallen into the street. It taxed my Italian to the max to get into our apartment that night. The Airbnb host asked me not to mention this in my review (I didn’t).

The next day brought a circuitous trip to Budapest via Brussels. Budapest was a charm, a former capital of the Austria-Hungarian Empire and the architecture to prove it. The last time I was here 55 years ago, the Russian Army was running the place and it was grim, oppressive, and dirty.

Today, it is a thriving hot spot for Europe’s young, with bars and night clubs everywhere. Dinners dropped from $150 in Venice to $30. We topped the night with a Danube dinner cruise with a folk dancing troupe. I’m telling you, you can live there like a king for $1,000 a month.

Visiting the Golden Age in Budapest

The next morning, we drew closer to our final destination of Switzerland. A four-hour train ride brought us to my summer chalet in Zermatt and some much-needed rest. At the end of a long valley and lacking any cars, Zermatt is one of those places where you can just give the kids 50 Swiss francs and tell them to get lost. I spent mornings hiking up from the valley floor and afternoons getting caught up on the markets and my writing.

There’s nothing like recharging my batteries in the clean mountain air of the Alps. The forecast was rain every day for two weeks, but it never showed. As a result, I ended up hiking ten miles a day to the point where my legs were made of lead by the end.

The only downer was watching helicopters pick up the bodies of two climbers who fell near the top of the Matterhorn. As temperatures rise rapidly, the ice holding the mountain together is melting, leading to a rising tide of fatal accidents.

I caught my last flight home from Milan. Anything for one more great dinner in Italy, which I enjoyed in the Galleria. At the train station, I chatted with a troop of Italian Boy Scouts in blue uniforms headed for the Italian Alps. The city was packed with Chinese tour groups, and there was a one-month wait to buy tickets for Leonardo DaVinci’s The Last Supper. Another Airbnb made sure I stayed up all night listening to the city’s yellow trolleys trundle by.

Finally, an 11-hour flight brought me back to the City by the Bay. Thanks to two sleeping pills of indeterminate origin I went to sleep over England and woke up over Oregon, preparing for a landing. It seems that somewhere along the way I proposed marriage to the Arab woman sitting next to me, but I have no memory of that whatsoever. At least that’s what the head flight attendant thought.

I am now planning this summer trip. After the Queen Mary and the Orient Express should I climb the Matterhorn again? Or should I summit Mount Kilimanjaro in Africa first? No transatlantic trip should ever be wasted. And I have to get home in time to join a 50-mile hike with the Boy Scouts in New Mexico and then cart two kids off to college.

What a great problem to have.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2023/03/spqr.jpg185246Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-03-20 09:02:082023-03-20 12:01:30The Market Outlook for the Week Ahead, or QE is Back!

Up to $2 trillion in liquidity into the banking system should do the job in the financial sector.

This is highly bullish tech shares and the growth-based tech stocks will experience the best windfalls from this psychological and fiscal reset of the American banking system.

It’s true tech stocks did need a little help as 2022 was really a struggle for them, but 2023 has been brighter with the “buy the dip” mentality back with vengeance.

After the gangbuster January, we’ve been waiting for some direction as to what will happen to tech stocks and now we have gotten the signals.

In short, tech stocks will go higher.

Now, I truly believe that the buy-the-dip mentality will become firmly entrenched and investors should dig deep to execute bullish positions as I expect tech stocks to roar ahead.

Many know about the FDIC, SPIC insured deposits of up to $250,000, but the Fed has rolled out the red carpet for the banking system and lent money to the banks that even don’t need it.

Banks borrowed up to $350 billion in cheap loans from the Fed.

Nearly $143 billion went to holding companies for two major banks that failed over the past week, Silicon Valley Bank and Signature Bank, triggering widespread alarm in financial markets.

Ironically, public tech stocks benefited the most from the government helping the financial industry and it was a crypto-biased bank that bled itself to edge of catastrophe.

Although this creates a moral hazard, I am not really in the business to tell someone what is right or what is wrong in terms of systemic risk.

But knowing that the Fed has the backs of the banks and stock market no matter what is highly bullish for tech stocks in the short-term.

This opens up liquidity like a reservoir opening up its water channels.

Expect a lot more capital sloshing around the financial system that will naturally fall into tech stocks from the boring behemoths to the cash-burning peons.

The tide will lift most boats in this situation.

The bank term financing program should be able to inject enough reserves into the banking system to reduce the reserve deficit and reverse the tightening that took place last year.

I anticipate that the new program will be attractive to a wide range of institutions, apart from those currently facing liquidity problems.

The longer this program sustains itself the better for tech stocks.

Say goodbye to quantitative tightening.

The era of balance sheet reduction is now dead as the Fed is too worried to rock the boat.

Going from QT to printing money which is what this discount window effectively was has stunned the market to the upside.

Moving forward, expect rate hike expectations to dissipate and lower bond yields which will contribute to another tech market rally and in turn a lower dollar.

Most of everything will have a high chance to deliver decent tech gains from ARK Innovation ETF (ARKK) to the Apple’s (AAPL) and Google’s (GOOGL) of the world.

When the Fed wants to widen the goalposts this wide, you don’t need Ronaldo to score a goal.

Buy the dip in tech until we truly see a systemic credit risk or if inflation comes back shooting past the first pandemic peak to form a double top.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-03-17 16:02:032023-03-30 23:34:30Highly Bullish for Tech Stocks

(MARKET OUTLOOK FOR THE WEEK AHEAD, or MAKING A SILK PURSE FROM A SOW’S EAR)

(META), (GOOGL), (MSFT), (AAPL), (AMZN), (NFLX), (TSLA), (SPY), (TLT), (ENPH), (UUP), (GLD), (SLV), (EEM)

On the up days, we see the kindly ministrations of Dr. Jekyll.

On the down days, we suffer from the evil hand of Mr. Hyde.

To say that traders are confused would be an understatement. Many seasoned pros have told me that this is one of the most difficult markets they have ever seen.

Fridays have been particularly treacherous when weekly options expire. Some 56% of all options trading now takes place with expirations of five days or less. Trading before 4:00 PM sees billions of dollars of hot money trying to force closing prices just in or out of the money for key at-the-money strike prices.

What is especially disturbing is that some 80% of the gain in the S&P 500 (SPY) this year has been in just seven names, Meta, (META), Alphabet (GOOGL), Microsoft (MSFT), Apple (AAPL), Amazon (AMZN), Netflix (NFLX) and Tesla (TSLA). Most other stocks went nowhere….or down. That much concentration means that any rallies lack confidence and will fail….for now.

Remember these names because when we finally do get a real upside breakout, they will be the leaders. You can take that to the bank.

Thanks to turmoil in the House of Representatives intent on a national default, bonds have given up 70 of the 120-basis point drop in yields since October. That deprives us of one of our biggest money makers of 2022, our long bond trades.

That means were are also seeing the automatic flip side of the bond trade, a strong US Dollar (UUP), and weak precious metals, (GLD) and (SLV), and emerging markets (EEM).

This too shall end.

If it was excess liquidity that caused stocks to rocket for 13 years, then maybe we should be focusing on what little liquidity is left. That would be the font of government money pouring into infrastructure and alternative energy plays.

Some $370 billion I know available for investment in ESG, would most of it going into the battery industry for the burgeoning electric vehicle industry. Even foreign firms like Finland’s Neste is moving to the US to cash in on federal munificence, converting an old US oil refinery to produce diesel fuel out of animal and vegetable fat (click here for the link).

Probably the best bet here is in California-based Enphase Energy (ENPH), which makes a 40% gross profit margins on microinverters for solar panels and has just seen a 42% dive in its share price. That makes (ENPH) a BUY. Hint: solar stocks always follow the price of oil to which it is tied, which has lately been down.

Some nimble and aggressive trading managed to push me back in the green for February, taking me up +0.93% on the month. That’s a dramatic improvement of +5.48% from a week ago.

You might even call it making a silk purse from a sow’s ear.

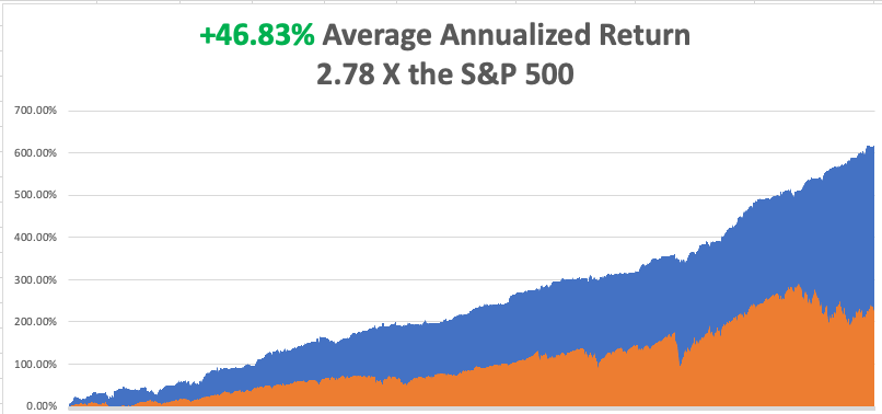

My 2023 year-to-date performance is still at the top at +23.28%. The S&P 500 (SPY) is up +4.32% so far in 2023. My trailing one-year return maintains a sky-high +86.58% versus -12.97% for the S&P 500.

That brings my 15-year total return to +620.47%, some 2.78 times the S&P 500 (SPX) over the same period. My average annualized return has recovered to +46.83%, still the highest in the industry.

Last week, I piled on a Tesla (TSLA) March $155-$260 short strangle betting that the stock can stay within a $95 range for 19 trading days. I also added a deep in-the-money long in the bond market for the first time in six weeks. Both positions turned immediately profitable.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

Q4 GDP Dips, from 3.9% to 2.7% in the October-December quarter. Consumption took a dive, which is amazing over the holidays. This is nowhere near a recession.

Fed Minutes Show More Hikes to Come, with the emphasis on the plural. That could take the overnight borrowing rate to a 5.40% high. It certainly pees on the parade for the falling interest rates crowd. The Tail is Wagging the Dog, with short, dated options, often same-day expiration dominating trading every Friday. Billions of dollars are battling around key strike prices attempting to force expirations in or out of the money. No place for the little guy. Better to take Fridays off. Netflix Slashes Prices in 30 countries, taking the stock down a modest 3%. (NFLX) is still the leader in the sector with 231 million subscribers, followed by Amazon (200 million), Disney Plus (162 million, HBO Max (95 million, Peacock (18 million), and Hulu 47 million). Buy (NFLX) and (AMZN) on dips. Individual 401k’s Lost 23% in 2022, according to a study from Fidelity. High inflation is shrinking the remaining purchasing power even faster. A rising number of workers are also borrowing against their 401k’s to make ends meet. Such loans can go up to 50% of the principal. Better start making up the losses or you’ll be spending your golden years working at Taco Bell. Apple to Add Glucose Monitor on its Watches, to aid diabetic clients. Some 38 million Americans have diabetes and given the obesity epidemic that figure is certain to rise. It highlights Big Tech’s move into the low-hanging fruit in health care. Existing Home Sales Dive 0.7% in January, to a 4 million annualized rate, the weakest since October 2010. That makes 12 consecutive months of falling sales. The Median Home Price sold rose to $359,000. An imminent national debt crisis and spiking interest rates is not a great environment in which to sell your home. Biden Ukraine Visit Tanks Gas and Oil Prices, cutting Russia’s chances of a win and eventually leading to a flood of oil on the market. Biden’s visit is sending the message to Putin that there’s no chance of a win here. Energy is hitting two-year lows across the board. Only energy stocks are staying high. Energy is getting so cheap it might be worth a trade. Germany Accelerates Move Towards Alternatives, permanently cutting all ties with Russia energy. Europe’s biggest economy, and the fourth largest in the world, hopes to get 80% of its electricity from solar and wind by 2030. Hydrogen is also entering the picture. Other countries will follow.

On Monday, February 27 at 8:30 AM EST, US Durable Goods are out.

On Tuesday, February 28 at 9:00 AM, the S&P Case Shiller National Home Price Index for December is released.

On Wednesday, March 1 at 10:00 AM, the ISM Manufacturing PMI is printed. On Thursday, March 2 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, March 3 at 8:30 AM, the ISM Non-Manufacturing PMI. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, I usually get a request to fund some charity about once a day. I ignore them because they usually enrich the fundraisers more than the potential beneficiaries. But one request seemed to hit all my soft spots at once.

Would I be interested in financing the refit of the USS Potomac (AG-25), Franklin Delano Roosevelt’s presidential yacht?

I had just sold my oil and gas business for an outrageous profit and had some free time on my hands so I said, “Hell Yes,” but only if I get to drive. The trick was to raise the necessary $5 million without it costing me any money.

To say that the Potomac had fallen on hard times was an understatement.

When Roosevelt entered the White House in 1932, he inherited the presidential yacht of Herbert Hoover, the USS Sequoia. But the Sequoia was entirely made of wood, which Roosevelt had a lifelong fear of. When he was a young child, he nearly perished when a wooden ship caught fire and sank, he was passed to a lifeboat by a devoted nanny.

Roosevelt settled on the 165-foot USS Electra, launched from the Manitowoc Shipyard in Wisconsin, whose lines he greatly admired. The government had ordered 34 of these cutters to fight rum runners across the Great Lakes during Prohibition. Deliveries began just as the ban on alcohol ended.

Some $60,000 was poured into the ship to bring it up to presidential standards and it was made wheelchair accessible with an elevator, which FDR operated himself with ropes. The ship became the “floating White House,” and numerous political deals were hammered out on its decks. Some noted guests included King George VI of England, Queen Elisabeth, and Winston Churchill.

During WWII Roosevelt hosted his weekly “fireside chats” on the ship’s short-wave radio. The concern was that the Germans would attempt to block transmissions if broadcast came from the White House.

After Roosevelt’s death, the Potamac was decommissioned and sold off by Harry Truman, who favored the much more substantial 243-foot USS Williamsburg. The Potamac became a Dept of Fisheries enforcement boat until 1960 and then was used as a ferry to Puerto Rico until 1962.

An attempt was made to sail it through the Panama Canal to the 1962 World’s Fair in Seattle, but it broke down on the way in Long Beach, CA. In 1964 Elvis Presley bought the Potomac so it could be auctioned off to raise money for St. Jude Children’s Research Hospital. It sold for $65,000. It then disappeared from maritime registration in 1970. At one point there was an attempt to turn it into a floating disco.

In 1980 a US Coast Guard cutter spotted a suspicious radar return 20 miles off the coast of San Francisco. It turned out to be the Potomac loaded to the gunnels with bales of illicit marijuana from Mexico. The Coast Guard seized the ship and towed it to the Treasure Island naval base under the Bay Bridge. By now the 50-year-old ship was leaking badly. The marijuana bales soaked up the seawater and the ship became so heavy it sank at its moorings.

Then a long rescue effort began. Not wanting to get blamed for the sinking of a presidential yacht on its watch the Navy raised the Potomac at its own expense, about $10 million, putting its heavy lift crane to use. It was then sold to the City of Oakland, Ca for a paltry $15,000.

The troubled ship was placed on a barge and floated upriver to Stockton, CA, which had a large but underutilized unionized maritime repair business. The government subsidies started raining down from the skies and a down-to-the-rivets restoration began. Two rebuilt WWII tugboat engines replaced the old, exhausted ones. A nationwide search was launched to recover artifacts from FDR’s time on the ship. The Potomac returned to the seas in 1993.

I came on the scene in 2007 when the ship was due for a second refit. The foundation that now owned the ship needed $5 million. So, I did a deal with National Public Radio for free advertising in exchange for a few hundred dinner cruise tickets. NPR then held a contest to auction off tickets and kept the cash (what was the name of FDR’s dog? Fala!).

I also negotiated landing rights at the Pier One San Francisco Ferry Terminal, which involved negotiating with a half dozen unions, unheard of in San Francisco maritime circles. Every cruise sold out over two years, selling 2,500 tickets. To keep everyone well-lubricated I became the largest Bay Area buyer of wine for those years. I still have a free T-shirt from every winery in Napa Valley.

It turned out to be the most successful fundraiser in the history of NPR and the Potomac. We easily got the $5 million and then some. The ship received a new coat of white paint, new rigging, modern navigation gear, and more period artifacts. I obtained my captain’s license and learned how to command a former coast guard cutter.

It was a win-win-win.

I was trained by a retired US Navy nuclear submarine commander, who was a real expert at navigating a now thin-hulled 73-year-old ship in San Francisco’s crowded bay waters. We were only licensed to cruise up to the Golden Gate bridge and not beyond, as the ship was so old.

The inaugural cruise was the social event of the year in San Francisco with everyone wearing period Depression-era dress. It was attended by FDR’s grandson, James Roosevelt III, a Bay area attorney who was a dead ringer for his grandfather. I mercilessly grilled him for unpublished historical anecdotes. A handful of still-living Roosevelt cabinet members also came, as well as many WWII veterans.

As we approached the Golden Gate Bridge, some poor soul jumped off and the Coast Guard asked us to perform search and rescue until they could get a ship on station. No body was ever found. It certainly made for an eventful first cruise.

Of the original 34 cutters constructed only four remain. The other three make up the Circle Line tour boats that sail around Manhattan several times a day.

Last summer I boarded the Potomac for the first time in 14 years for a pleasant afternoon cruise with some guests from Australia. Some of the older crew recognized me and saluted. In the cabin, I noticed a brass urn oddly out of place. It contained the ashes of the sub-commander who had trained me all those years ago.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Captain Thomas at the Helm

https://www.madhedgefundtrader.com/wp-content/uploads/2023/02/yatch.jpg7201200Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-27 09:02:412023-02-27 15:39:05The Market Outlook for the Week Ahead, or Making a Silk Purse from a Sow’s Ear

In 2019, Google claimed that it had achieved what it called quantum supremacy. The company claimed to have built a computer with capabilities far beyond those of traditional computers.

In a report published in Nature, Google said its quantum computer managed to calculate something that would take a normal machine 10,000 years.

What practical applications Google's performance will have in the real world is still unclear. The initial computation was a demonstration of capability rather than a product that will have a significant commercial impact any time soon.

Having a horse in the race will also mean they can turn it up a notch once they receive more direction on where this might lead.

Like so many of its other companies, Alphabet invests heavily in the latest computer technology.

Many of these ventures probably won't bring in much money; others, on the other hand, will likely recoup the company's entire research budget and then some. And the good thing about Alphabet is that it's so busy that a single project, such as B. quantum computing, will not decide on the entire investment.

I am not going to sit here and say that Google is a quantum computing company because it’s not, but they are ready to pounce if the opportunity presents itself.

Quantum Computing (QUBT)

Quantum Computing is an innovative company focused on its namesake. It sees a market opportunity in the ability to create a service that coordinates computing needs.

There are providers of quantum computers, such as IonQ or Rigetti. Then there are customers in large companies, universities, or research laboratories. Quantum Computing sits in the middle, making software to help customers manage their quantum computing needs.

Currently, quantum computing has almost no revenue. Management acknowledges that the company is still in the early stages of market development and understanding customer use cases.

QUBT stock is highly speculative, as are most other companies in the sector. However, as the market for quantum computing vendors and customers grows, a brokerage service that connects the two could represent a fairly profitable niche.

IBM (IBM)

Tech analysts like to compare IBM to companies like Radio Shack and Eastman Kodak (KODK) as a dinosaur inevitably heading towards the dustbin of history.

However, the truth is much more nuanced.

IBM still achieves $60 billion a year in total revenue, and that number is actually on the rise again. They also have a PE ratio of 21 as its ongoing operations in consulting, services, and cloud, among others, are very profitable. And IBM continues to invest heavily in research and development, including quantum computing.

IBM's quantum computing division promises to unlock information beyond the reach of even the world's fastest supercomputers. The IBM partnership for quantum computing already involves 160 Fortune 500 companies as well as national laboratories and academic institutions. These partners work in areas such as finance, chemistry, and logistics.

Microsoft (MSFT)

Like IBM, Microsoft wants to take the lead in the emerging field of quantum computing. Microsoft has an inbuilt advantage, as its Azure cloud platform already has a massive installed base with a variety of Fortune 500 customers.

Now Microsoft is building its quantum computing capabilities directly into Azure. Microsoft describes this as “the world’s first full-featured, open cloud ecosystem for quantum computing.”

It makes a lot of sense that this would be offered as part of a cloud package. After all, most customers probably don't need their own supercomputer. Rather, they want the ability to buy that computing power only when they need it.

If Microsoft can seamlessly integrate this experience into its native Azure platform, it could be a major win, both for this product and for securing greater market share in cloud computing.

Applied Materials (AMAT)

Another approach to betting on quantum computing stocks is to be long on suppliers. Given that the technology is still very new, it can be difficult to determine which companies will ultimately be among the winners in this space. What is certain, however, is that if quantum computing catches on, we will need faster and more powerful semiconductors.

Applied Materials is one of the industry leaders in terms of patents and industry know-how when it comes to manufacturing chips that will be used in quantum computing hardware. During a gold rush, you want to be the one selling the shovels. Applied Materials should be the shovel dealer for the quantum computing industry.

In the meantime, Applied Materials' existing business is extremely profitable.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-24 16:02:212023-02-28 17:44:32Part 2: The Best of the Rest in Quantum Computing

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-02-24 09:04:012023-02-24 11:27:10February 24, 2023

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.