Mad Hedge Technology Letter

October 10, 2018

Fiat Lux

Featured Trade:

(DON’T BUY SURVEYMONKEY ON THE DIP),

(SVMK), (GOOGL), (CRM)

Mad Hedge Technology Letter

October 10, 2018

Fiat Lux

Featured Trade:

(DON’T BUY SURVEYMONKEY ON THE DIP),

(SVMK), (GOOGL), (CRM)

If a company takes almost 20 years and still isn’t profitable - it probably never will.

Granted, tech firms are given a Rapunzel-length leash to collect users, scale out the product, refine algorithms to industry standard, and build up the engineering team.

I know this takes time – it doesn’t happen in one day.

After whipping up a frenzy of momentum and venture capitalists claiming stakes, tech stocks usually go public.

This is the common process of what it takes to construct a Silicon Valley tech firm, and there are no shortcuts to this long hard slog.

And if after almost 20 years, amid a nine-year bull market, a tech firm in the most dominating sector in the world cannot figure how to be in the black, investors should stay away from this company in droves.

SurveyMonkey (SVMK), who recently achieved a blockbuster IPO, were the rock stars of the tech world for one day and one day only.

The stock peaking after the first trading day is a ghastly signal and ominous sign.

Their fifteen minutes of fame is all they will get because this practically ex-growth company has no indicators of a rosier future.

The company went public at $12 per share and even that was too generous.

The stock took off like a banshee, on the verge of overshooting the $20 level before falling back to grace.

The stock is now trolling around $13, and on the verge of heading to the purgatory of single digits.

What caused such a swan dive after such a promising start?

On the surface, everything looks like peaches and daffodils – a growing Silicon Valley cloud company even with Facebook spin doctor Sheryl Sandberg on the board.

The optics pass all the marks.

But wait a second, looking at the nuts and bolts, it’s crystal clear why this stock has been throttled back.

The first half of 2018, SurveyMonkey presided over a tepid 3% of paid user growth.

Yes, SurveyMonkey is growing, but not by much.

In this same period, the company lost $27.2 million and this was after an annual 2017 loss of $24 million.

Profitability isn’t exactly their forte.

The 14% of revenue growth the company secured was done after taking a machete and gutting margins to appear pretty for the IPO.

And it’s painfully obvious that SurveyMonkey is failing at converting the freemium users into paid converts.

The online survey doesn’t exactly have the highest barriers of entry.

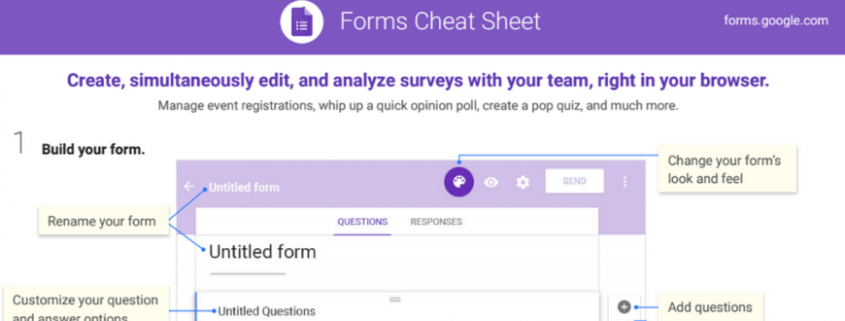

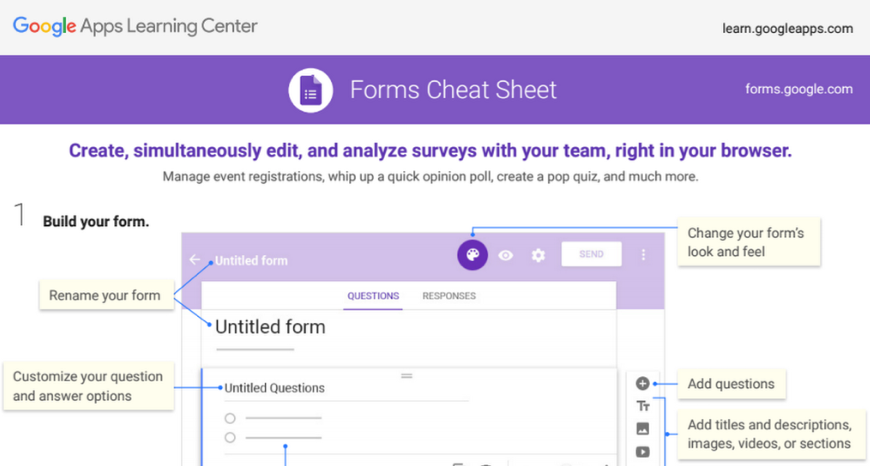

Google (GOOGL) Forms is the competitor in this space offering straightforward free surveys with basic analysis.

The tool is highly functional.

The pricing structure to SurveyMonkey’s individual membership is presented as a luxury service like the US postal service.

The individual service costs $384 per year and rises all the way up to the bloated price of $1,188 per year.

Any individual paying $1,188 per year for this needs to check themselves into a mental hospital.

Google Forms could easily undercut this pricing model by offering survey tool packages for a fraction of this amount.

The “team plan” is also laughable by charging $75 per month for up to three users, and this type of plan is capped at an exorbitant $225 per month.

Let’s remember that Microsoft offers Microsoft Office 365 Personal for an annual total of $59.99 and is million times more useful.

This annual subscription comes with premium versions of Word, Excel, PowerPoint, OneDrive, OneNote, Outlook, Publisher, and Access.

The OneDrive cloud service includes 1 terabyte (TB) of cloud storage.

Just by this simple comparison, it is easy to see which service is of value and which service is building castles in the sky.

With the explosion of service-as-a-software (SaaS) apps flooding desktops, I imagine the paid version of SurveyMonkey would be first on the chopping block due to its overly ambitious pricing.

In this strategy, the company is more concerned about milking as much as they can from each existing paid user instead of juicing up the core user base.

Effectively, this is a poor management decision, and the company is harming the growth of the potential paid usership base by robbing all incentive to convert to the paid version.

As Netflix masterfully proved, draw in the eyeballs at a lower price, build up the service to an optimum quality level, and subscribers never leave.

The opposite strategy is an indirect way of management believing the product is not good enough or the niche is too small to perpetualize a solid relationship.

And since growth numbers aren’t accelerating, there is infinitesimal reason to even consider investing in this fading company.

SurveyMoney has also racked up the debt - $317 million of it to be precise putting its debt $100 million over total revenue in 2017.

They were burning cash quickly and only had $43 million left in the coffers.

Part of the rationale for going public was a way to pay down debt.

Another chunk of proceeds from the IPO will be used to pay taxes.

The company has no innovative roadmap going forward and using the cash to pay down existing obligations shows the anemic level of intent from this company.

The silver lining in this company is that the losses of $76.4 million in 2016 were pared back in 2017.

In the IPO prospectus, SurveyMonkey noted that most unpaid customers do not become paid customers.

Even though the product is useful and it’s a long-time favorite of mine, the stock is a different animal.

There was not much meat in the prospectus and most of it were dry bones.

The IPO day was buoyed by the $40 million in stock venture-capital arm of Salesforce (CRM) pocketed, but that short-term boost has faded quickly as investors have dissected this company in every which way.

Use their free survey tools but avoid paying for the paid version and don’t buy the stock.

There are many other fishes in the sea.

Mad Hedge Technology Letter

October 9, 2018

Fiat Lux

Featured Trade:

(LIVING ON THE EDGE),

(AMZN), (MSFT), (HPE), (GOOGL)

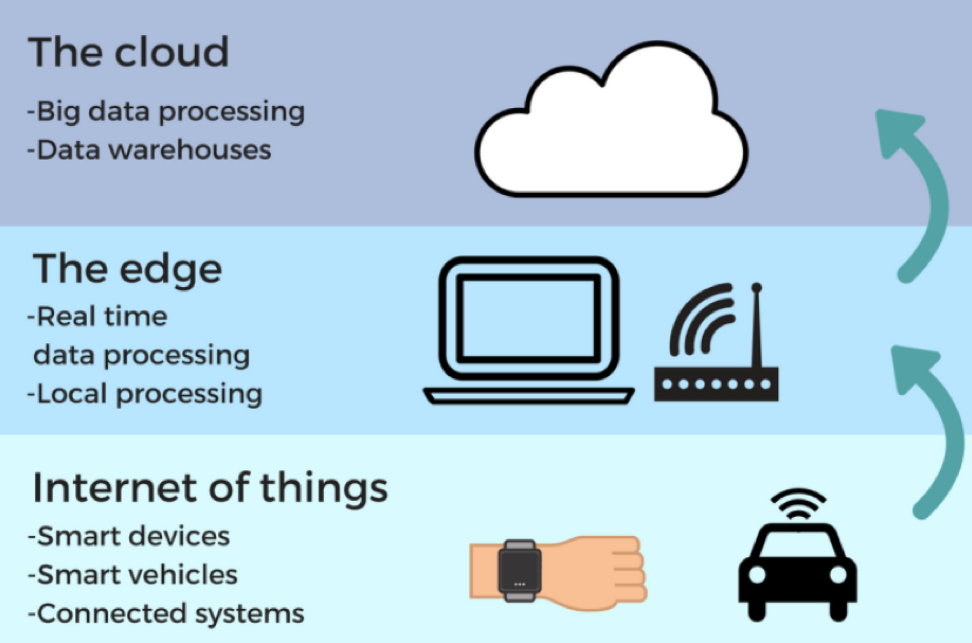

What is Edge Computing?

Edge computing is processing data at the edge of your network.

The data being generated will not only occur in a centralized data-processing storage server anymore, but at different decentralized locations closer to the point of data generation.

This is what everyone is talking about and is an epochal development for tech companies and the businesses they run.

The last generation of IT saw a massive migration to the cloud as centralized servers stored the sudden hoard of data that never existed before.

Edge computing bolsters data performance, boosts reliability, and cuts the costs of operating apps by curtailing the distance data must flow which effectively reduces latency and bandwidth headaches.

Edge computing is revolutionizing IT infrastructure as we know it.

No longer will we be forced to use these monolith-like giant server farms for all our data needs.

Epitomizing the Silicon Valley culture of becoming faster and more agile to disrupt, tech infrastructure is getting the same potent cocktail of performance enhancers underlying the same characteristics.

According to research firm Gartner, around 80% of enterprises will shutter legacy data servers by 2025, compared to 10% in 2018.

Keeping the data near the points of data creation is the logical step to enhance and optimize data processes.

Cloud computing depends on superior bandwidth to handle the data load.

This can create a severe bottleneck if bombarded with a heavy dose of devises all communicating with the centralized servers.

The edge computing industry already in the initial stages of ramping up will be worth $6.72 billion by 2022, up from $1.47 billion in 2017.

Underpinning this crucial IT is the imminent inauguration of 5G networks powering IoT devices.

Simply put, the amount of raw data which will need swift processing is about to explode. Relying on a slower, centralized servers is not the solution, and the edge offers a suitable solution to accommodate the new generation of technology.

And as technology starts to permeate every corner of the globe, data will need to be instantaneously processed locally in cutting-edge technology such as self-driving cars.

Waiting on communicating with a centralized server in another continent is just not plausible.

A self-driving car only has milliseconds to react in hazardous conditions.

Other critical and data heavy operations such as wind turbines, medical robots, airplanes, oil rigs, mining vehicles, and logistics infrastructure only function if operated at peak levels and an interruption to connectivity could be fatal.

Telecom companies and IT firms will experience the biggest sea of changes from edge computing in the next five years.

These two sectors are confronting a significant ramp up in network load and will find it challenging to deliver the results to operate the apps and services they are responsible to run.

This new IT technology is the answer.

The industry adopting edge computing the fastest is retail because of the troves of data collected by IoT sensors and cameras.

Companies will be able to analyze the performance of products and edge computing is the technology that will capture the data.

The adoption of edge computing will perfectly take advantage of the boom in IoT devices and uptick of internet speeds through 5G.

Sales of PC’s, tablets, and smartphones have matured, and aren’t seeing the same pop in growth rates like before.

However, the IoT industry will expand by 30% in the next five years boding well for the broad-based integration of edge computing.

In total, the number of connected devices in the next five years will balloon from 17.5 billion in 2017 to over 31 billion in 2023.

The first iteration of 5G IoT devices will be on the market in 2020 deploying industrial process monitoring and control.

This is not a flash in the plan technology and many firms already or are about to roll-out an edge computing strategy.

In a recent report, 72.7% of tech firms already possess a solid edge computing plan or it is in the works.

If you include all the tech firms who expect to invest in edge computing in the next year, the number catapults to 93.3%.

The same survey continued to delve into the mindset of edge computing for tech management by asking about the importance of the technology.

Over 70% of firms characterized edge computing as important, bifurcated into two categories with the first being “critically important” which 22.2% of respondent agreed with.

Another 49.6% of respondent described edge computing as “very important.”

Firms cited that improved application performance is the largest benefit of edge computing followed by real time data analytics and data streaming.

It is not the death of cloud computing yet.

Even though centralized, slower, and negatively affected by long distance, cloud computing still has a place in the future of IT.

About two-thirds of tech firms plan to utilize a hybrid centralized cloud – edge computing strategy.

Even if they did not combine this strategy, companies would most likely separate the operations responsible for two distinct set of tasks filtered by the level of time sensitivity.

The overwhelming and imminent adoption of IoT devices means IT departments are crafting a substantially higher budget for edge computing to satisfy their operational needs.

Large recipients of this technology will turn out to be companies related to manufacturing, smart cities and transportation as well as energy and healthcare.

This technology really cuts across the entire spectrum of global industries.

Data usually does not discriminate, and applications of new tech is fueling a rapid rise of performance optimization that no other sectors can claim.

Let’s do a quick rundown of the edge computing players.

The three cloud behemoths of Amazon Web Services (AWS), Microsoft (MSFT) Azure, and Google (GOOGL) Cloud are constructing edge gateways and edge analytics into their IoT offerings aiding workload distribution across edge and cloud services.

Microsoft has over 300 edge computing patents and launched its Azure IoT Edge service integrating container modules, an edge runtime, and a cloud-based management interface.

Amazon Web Services offers AWS CloudFront content delivery infrastructure and AWS Greengrass IoT service building on the momentum of pioneering centralized cloud technology.

Dell’s IoT division invested $1 billion in R&D to help drive Edge Gateways and VMware's Pulse IoT Center.

Hewlett Packard Enterprise (HPE) devoted $4 billion to its edge network portfolio. HPE operates edge services, mini-data centers, and smart routers.

These are just some of the initiatives from some of the main players in the field.

Expect companies to become a lot more connected while possessing the speed, high performance, and agility to optimally entertain this new-found connectivity.

Mad Hedge Technology Letter

October 1, 2018

Fiat Lux

Featured Trade:

(ZINC AIR BATTERIES WILL REVOLUTIONIZE ELECTRIC CARS),

(TSLA), (NIO), (FB), (GOOGL), (NFLX)

As Panasonic ramps up its battery production at the Tesla Gigafactory 1 in Sparks, Nevada, the demand and business for renewable energy has never been more robust.

And as the world’s population balloons and man-made pollutants roil the natural ecosphere, business needs an answer to these potential apocalyptic bombshells or there will be nowhere clean enough to live.

Energy security and population growth will have a complicated relationship going forward and cannot be ignored for the sake of mankind.

This isn’t me being a tree-hugging, Birkenstock-trotting, save-the-earth, love and peace-type of guy.

This problem is real and whoever discovers the solution could reap untold profits.

The answer has been found - rechargeable zinc air batteries.

Spearheading this massive initiative is South African-born entrepreneur, sports team owner, Los Angeles Times owner, and more importantly the founder, chairman and CEO of NantEnergy Dr. Patrick Soon-Shiong.

This El Segundo, California-based company presented an utter game changer to the future of the world and the world’s economy.

NantEnergy debuted a rechargeable battery powered by oxidizing zinc with oxygen from the air for commercial use at the One Planet Summit in New York.

It also has the capability to store energy.

Not only is this technology and product cutting edge, but it has the cost basis to support broad-based scalability and adoption.

Ramkumar Krishnan, chief technology officer of NantEnergy claimed this revolutionary battery can “deliver energy for $100 per kilowatt-hour (kWh).”

Lithium-ion batteries have been the mainstay choice for clean energy or clean enough energy since 1992, and its usage varies in cost from $300 to $500 kWh.

Tesla, with its phalanx of superior engineers, has been able to suppress that cost all the way down to a level between $100 to $200 kWh level.

NantEnergy has already registered more than100 related patents in its name and envisions a $50 billion addressable market.

I believe the addressable market is substantially bigger.

For all the hoopla about lithium-ion batteries, there are severe drawbacks in its usage and application.

Let’s concisely run down the pitfalls of batteries of this ilk.

Once out the factory door, the performance starts to go downhill.

Lithium-ion batteries react poorly to high temperatures.

These batteries become inoperable if completely discharged.

There is a slight chance a battery could burst into flames and burn off your face.

Simply put, lithium-ion batteries incorporate cobalt, an extremely toxic material hazardous to human health.

If a Samsung Galaxy smartphone explodes, cover your mouth to avoid inhaling the cobalt-laced fumes.

Dr. Soon-Shiong characterized this new technology as the “holy grail” of renewable energy.

Wide-scale adoption would bring the need for cobalt to its knees.

No longer would tech companies need to scramble to secure a sufficient amount of cobalt supply from the deepest reaches of the Congo jungle.

It would be the end of cobalt as we know it.

At first, lithium would be required for a stopgap measure while engineers refine the battery on its way to a full-fledged zinc alone battery.

The lithium placeholder would only be temporary.

The clean energy movement must be grinning widely as the potential to finally do away with cobalt from renewable energy has pronounced social and economic consequences.

An estimated 1.4 billion people still live in the dark and do not have access to electricity.

This technology is being tested in villages in Africa and desolate communities in Asia as we speak.

The absence of electricity isolates these undeveloped communities in third-world Africa and Asia without access to health care, education, and technology.

It’s hard to kick-start your life as a sprouting little kid when you’re lost in the dark half the time.

Importing fossil fuel to put these communities online is unfeasible and just plain too expensive for communities that have a dire shortage of capital.

Currently, NantEnergy’s rechargeable zinc air batteries are online in 110 villages located in nine Asian and African countries.

The batteries have been combined to establish a microgrid system powering entire areas.

The company will start delivery this product next year widening its type of use to telecommunications towers.

The next step after that would be the home energy storage market targeting California and New York as the first American cities.

Engineers have pointed out that this development could transform the electric grid into a “round-the-clock carbon-free system.”

In addition, with cooperation with Duke Energy, a major utility, NantEnergy’s batteries have been powering communications towers in America for the past six years.

The design is mind-boggling utilitarian - plastic, a circuit board, and zinc oxide wrapped up in a briefcase-size shell.

One charge can offer 72 hours of battery life.

The charging process is easy - electricity from solar installations is stored by converting zinc oxide to zinc and oxygen.

The discharge process is straightforward, too - the system produces energy by oxidizing the zinc with air.

The pursuit of energy reduction is in full throttle, and this is the next leg up for energy aficionados.

Your lithium-ion-run Tesla could become a legacy company in a matter of years if this technology disrupts Elon Musk’s brainchild.

Lately, Musk has been falling behind the eight ball with fresh innovators hot on his heels.

This is the latest company to enter into its market even though still in the incubation stage.

Competitors have popped out of nowhere and are coming for his bacon.

Shanghai headquartered electric car manufacturer Nio (NIO) went public and raised more than $2 billion.

Even though it is not yet a threat to Tesla, it shows that Tesla isn’t the only game in town anymore.

In any case, NantEnergy has the magic to unlock the “holy grail” of renewable energy. And if it can promise on its cost projections, I see no reason why this won’t be furiously adopted by corporations worldwide.

As it is, America has been losing out in the Congo, as China has cornered the cobalt market there.

And, as the evolution of fracking technology quelled the Middle-East situation, it could also have the same effect in the Congo.

More excitingly, it could put online an additional 1.2 billion new customers to devour iPhones and watch Netflix (NFLX).

Companies such as Facebook (FB) and Alphabet (GOOGL) have been developing a way for these remote and poverty-prone places to use Internet from a satellite.

They would need electricity first to power their devices unless Mark Zuckerberg has found a way to use a smartphone without electricity.

NantEnergy’s renewable batteries have already cut the need of 1 million lithium-ion batteries, and warded off the need to release 50,000 metric tons of carbon dioxide since 2012.

California is the flag-bearer in renewable energy policy by forcing its populace to be at 100% carbon-free electricity by 2045.

Musk is on record by saying he expects to break the 100-kWh level, which would contribute to better power storage and expedited electric vehicle (EV) adoption.

In contrast, energy storage analyst Mitalee Gupta at GTM Research has retorted that he’s “unsure $100/kWh is achievable this year.”

Musk, being a naturally optimistic entrepreneur, sets targets then does everything he can to break them.

Either way, two South African born visionaries are doing their part to crater the cost per kWh in the renewable energy market, and Elon Musk might not be the biggest disruptor from South Africa.

Time will tell if this market will become zinc-based or lithium-based – the higher-grade technology eventually wins out spelling doom for Musk.

But it appears that Musk has other things to worry about now.

NantEnergy plans to inaugurate a battery manufacturing facility in California next year.

As for Tesla, buy the car and not the stock.

And for Nio, don’t buy the car or the stock.

Global Market Comments

September 26, 2018

Fiat Lux

SPECIAL CAR ISSUE

Featured Trade:

(SAY GOODBYE TO THAT GAS GUZZLER),

(GM), (F), (TSLA), (GOOGL), (AAPL)

Do you want to get in on the ground floor of another major new trend?

Well, here’s another new trend. Get this one right and your retirement funds should multiple like rabbits.

There have been some pretty amazing announcements by governments lately.

The United Kingdom has banned the use of gasoline-powered engines by 2040.

China is considering doing the same by 2035.

And now the State of California is targeting 100% alternative energy use by 2040. That’s only 22 years away.

The only unknown is what such a planned obsolescence program will look like, and how soon it will be implemented.

With 20% of the U.S. car market, don’t take the Golden State’s ruminations lightly.

California was the first state to require safety glass, seat belts, and catalytic converters, and the other 49 eventually had to follow. Some 20% of the market is just too big to ignore.

The death of the car is now upon us, and it is still early, very early.

This is a very big deal.

Earlier in my lifetime, car production directly and indirectly accounted for about one-third of the U.S. economy.

Much of the growth during our earlier Golden Ages, in the 1920s and the 1950s, were driven by a never-ending cycle of upgrades of our favorite form of transportation, and the countless ancillary products and services needed to support them. Tail fins, radios, and tons of chrome assured you always had to have the next new model.

Today, 253 million automobiles and trucks prowl America’s roads, about half the world’s total, with an average age of 11.4 years.

The demise of this crucial industry started during the 2008 crash, when (GM) and Chrysler (owned by Fiat) went bankrupt. Only more conservatively run, family owned Ford (F) survived on its own.

The government stepped in with massive bailouts. That was the cheaper option for the Feds, as the cost of benefits for an entire unemployed industry was far greater than the cost of the companies absorbed.

If it hadn’t done so, the auto industry would have decamped for a new base near the technology hubs in California, and today would be a decade closer to their futures than they are now.

And remember, the government made billions of dollars of profits from its brief foray into the auto industry as an investor. It was one of the best returns on investment in history in major size.

I’ll breakout the major directions the industry is now taking. Hint: It doesn’t have much to do with traditional metal bashing.

The Car as a Peripheral

The important thing about a car today is not the car, but the various doodads, doohickeys, gizmos, and gadgets they stick in them.

In this category you can include 24/7 4G wireless, full Internet access, mapping software, artificial intelligence, and learning programs.

(GM) is now installing more than 100 microprocessors in its vehicles to control and monitor various functions.

Good luck doing your own tune-ups.

The Car as a Service

When you think about it, automobile ownership is a wildly inefficient use of capital. It is usually a family’s second largest expense, after their home, running $30,000 to $80,000.

It then sits unused in garages or public parking for 96% to 98% of the day. Insurance, maintenance, and liability costs can be off the charts.

What if your car was used 24/7, as is machinery in well-run industrial plants? Your cost drops by 96% to 98% to the point where it is almost free.

The sharing economy is the way to accomplish this.

We are already seeing several start-ups attempting to achieve this in major U.S. cities, such as Zipcar, Car2Go, Getaround, RelayRides, and City CarShare.

What happens to conventional car companies when consumers shift from ownership to sharing? Demand plunges by 96% to 98%.

Perhaps that is why auto shares (GM), (F) have performed so abysmally this year relative to technology and the main market.

Self-Driving Technology

This is the hottest development area in the industry, with Apple (AAPL), Alphabet (GOOG), and the big European carmakers committing thousands of engineers.

Let’s say your car is now comfortably driving you to work, allowing you to read the morning papers and catch up on your email. Or maybe you’re lazy and would rather watch the season finale of Game of Thrones.

What else is possible?

How about if, instead of parking, your car drops you off, saving that exorbitant fee.

Then it joins Uber, picking up local riders and paying for its own way. It then dutifully returns to pick you up at your office when it’s time to go home.

Since the crash rate for computers is vastly lower than for humans, car insurance rates will collapse, gutting that industry.

Ditto for life insurance, as 35,000 people a year will no longer die in car crashes.

Half of all emergency room visits are the result of car accidents, so that business disappears too, dramatically shrinking health care costs in the process.

I have been letting my new Tesla S-1 drive me since last year, and I can assure you that the car can drive better than I can, especially at night.

What better way to get home after I have downed a bottle of Caymus cabernet at a city restaurant?

Driverless electric cars are totally silent, increasing the value of land near freeways.

Nor do they require much maintenance, as they have so few moving parts. Exit the car repair industry.

I could go on and on, but you get the general idea.

For more on the topic, please read “Test Driving Tesla's Self Driving Technology” by clicking here.

Virtual Reality

After 30 years of inadequate infrastructure budgets, trying to get into any America city center is a complete nightmare.

Only last week, a cattle truck turned over on the Golden Gate Bridge, bringing traffic to a halt. Fortunately, a cowboy traveling to a nearby rodeo was able to unload his horse and lasso the errant critters (no, it wasn’t me!).

Even if you get into the city, you will be greeted by a $40 tab for a parking space. Hopefully, no one will smash your windows and steal your laptop (happened to me last year).

Why bother?

Thirty years ago, teleconferencing services pitched themselves as replacing the airplane.

Today, we are taking the next step, using Skype and GoToMeeting to conduct even local meetings, as we do at the Mad Hedge Fund Trader.

Virtual reality is clearly the next step, providing a 3D, 360 degree experience that makes you feel like you and your products are actually there.

Better to leave that car in the garage where it can get a top up on its charge. BART is cheaper anyway, when it runs.

New Materials

We are probably five years away from adopting the carbon fiber technology now used in the aircraft industry for mass-market cars. Carbon has one-tenth the weight of steel, with five times the strength.

The next great leap forward for electric cars won’t be through better batteries. It will come through a 70% reduction of the mass of a car, tripling ranges with existing technology.

San Francisco Becomes the Car Capital of the World

This will definitely NOT happen, as sky-high rents assure that the city by the bay will never attract large, labor-intensive industries.

Instead, the industry will develop much as the one for smartphones. The high value-added aspects, design and programming, will stay in California.

The assembly of the chassis, the body, and the rest of the vehicle will be best done in low-cost, tax-free states with a lot of land, such as Texas and Nevada.

What will happen to Detroit? It has already become a favored destination of new venture capital financial start-ups - the cost of offices and housing is virtually free.

Global Market Comments

September 25, 2018

Fiat Lux

Featured Trade:

(AI AND THE NEW HEALTH CARE),

(GOOGL), (XLP), (XLV), (MRK), (BMY), (PFE),

(MONDAY, OCTOBER 15, 2018, ATLANTA, GA,

GLOBAL STRATEGY LUNCHEON)

Mad Hedge Technology Letter

September 25, 2018

Fiat Lux

Featured Trade:

(AMAZON’S HOME INVASION),

(AMZN), (GOOGL), (HBB), (PG)