Featured Trade:

(WHY THE DOW IS GOING TO 120,000),

(X), (IBM), (GM), (MSFT), (INTC), (DELL), ($INDU), (NFLX), (AMZN), (AAPL), (GOOGL),

(THE MAD HEDGE CONCIERGE SERVICE HAS AN OPENING),

(TESTIMONIAL)

For years, I have been predicting that a new Golden Age was setting up for America, a repeat of the Roaring Twenties. The response I received was that I was a permabull, a nut job, or a conman simply trying to sell more newsletters.

Now some strategists are finally starting to agree with me. They too are recognizing that a ganging up of three generations of investment preferences will combine to drive markets higher during the 2020s, much higher.

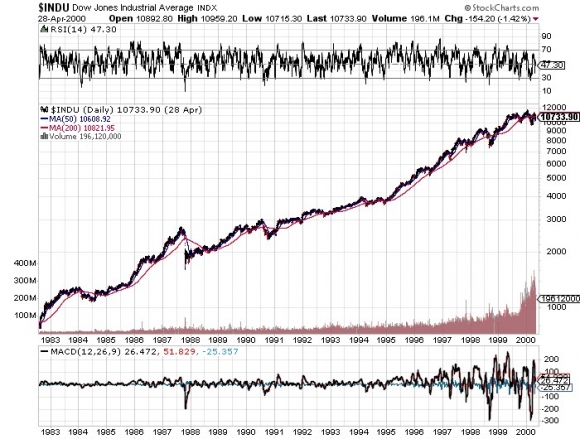

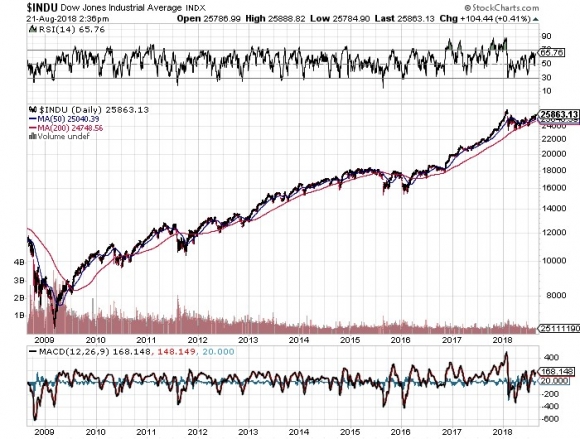

How high are we talking? How about a Dow Average of 120,000 by 2030, up another 465% from here? That is a 20-fold gain from the March 2009 bottom.

It’s all about demographics, which are creating an epic structural shortage of stocks. I’m talking about the 80 million Baby Boomers, 65 million from Generation X, and now 85 million Millennials. Add the three generations together and you end up with a staggering 230 million investors chasing stocks, the most in history, perhaps by a factor of two.

Oh, and by the way, the number of shares out there to buy is actually shrinking, thanks to a record $1 trillion in corporate stock buybacks.

I’m not talking pie in the sky stuff here. Such ballistic moves have happened many times in history. And I am not talking about the 17th century tulip bubble. They have happened in my lifetime. From August 1982 until April 2000 the Dow Average rose, you guessed it, exactly 20 times, from 600 to 12,000, when the Dotcom bubble popped.

What have the Millennials been buying? I know many, like my kids, their friends, and the many new Millennials who have recently been subscribing to the Diary of a Mad Hedge Fund Trader. Yes, it seems you can learn new tricks from an old dog. But they are a different kind of investor.

Like all of us, they buy companies they know, work for, and are comfortable with. During my Dad’s generation that meant loading your portfolio with U.S. Steel (X), IBM (IBM), and General Motors (GM).

For my generation that meant buying Microsoft (MSFT), Intel (INTC), and Dell Computer (DELL).

For Millennials that means focusing on Netflix (NFLX), Amazon (AMZN), Apple (AAPL), and Alphabet (GOOGL).

That’s why these four stocks account for some 40% of this year’s 7% gain. Oh yes, and they bought a few Bitcoin along the way too, to their eternal grief.

There is one catch to this hyper-bullish scenario. Somewhere on the way to the next market apex at Dow 120,000 in 2030 we need to squeeze in a recession. That is increasingly becoming a topic of market discussion.

The consensus now is that an impending inverted yield curve will force a recession sometime between August 2019 to August 2020. Throwing fat on the fire will be a one-time only tax break and deficit spending that burns out sometime in 2019. These will be a major factor in U.S. corporate earnings growth dramatically slowing down from 26% today to 5% next year.

Bear markets in stocks historically precede recessions by an average of seven months so that puts the next peak in top prices taking place between February 2019 to February 2020.

When I get a better read on precise dates and market levels, you’ll be the first to know.

To read my full research piece on the topic please click here to read “Get Ready for the Coming Golden Age.”

Dow 1982-2000 Up 20 Times in 18 Years

Dow 2009-Today Up 4.3 Times in 9 Years So Far

https://www.madhedgefundtrader.com/wp-content/uploads/2018/08/John-on-mechanical-bull-story-1-image-3-e1534972073238.jpg313250MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-23 01:08:052018-08-22 21:23:50Why the Dow is Going to 120,000

Mad Hedge Technology Letter August 22, 2018 Fiat Lux

Featured Trade: (WHAT’S IN STORE FOR TECH IN THE SECOND HALF OF 2018?), (GOOGL), (AMZN), (FB), (UTX), (UBER), (LYFT), (MSFT), (MU), (NVDA), (AAPL), (SMH)

Tech margins could be under pressure the second half of the year as headwinds from a multitude of sides could crimp profitability.

It has truly been a year to remember for the tech sector with companies enjoying all-time high probability and revenue.

The tech industries’ best of breed are surpassing and approaching the trillion-dollar valuation mark highlighting the potency of these unstoppable businesses.

Sadly, it can’t go on forever and periods of rest are needed to consolidate before shares relaunch to higher highs.

This could shift the narrative from the global trade war, which is perceived as the biggest risk to the current tech market to a domestic growth issue.

Healthy revenue beats and margin growth have been essential pillars in an era of easy money, non-existent tech regulation, and insatiable demand for everything tech.

Tech has enjoyed this nine-year bull market dominating other industries and taking over the S&P on a relative basis.

The lion’s share of growth in the overall market, by and large, has been derived from the tech sector, namely the most powerful names in Silicon Valley.

Late-stage bull markets are fraught with canaries in the coal mine offering clues for the short-term future.

Therefore, it is a good time to reassess the market risks going forward as we stampede into the tail end of the financial year.

The shortage of Silicon Valley workers is not a new phenomenon, but the dearth of talent is going from bad to worse.

Proof can be found in the controversial H-1B visa program used to hire foreign tech workers mainly to Silicon Valley.

A few examples are Alphabet (GOOGL), which was granted 1,213 H-1B approvals in 2017, a 31% YOY rise.

Alphabet’s competitor Facebook (FB) based in Menlo Park, Calif., was granted 720 H-1B approvals in 2017, a 53% YOY jump from 2016.

This lottery-based visa for highly skilled foreign workers underscores the difficulty in finding local American talent suitable for a role at one of these tech stalwarts.

Amazon (AMZN) made one of the biggest jumps in H-1B approvals with 2,515 in 2017, a 78% YOY surge.

The vote of non-confidence in hiring Americans shines an ugly light on American youth who are not applying themselves to the domestic higher education system as are foreigners.

For the lucky ones that do make it into the hallways of Silicon Valley, a great salary is waiting for them as they walk through the front door.

Reportedly, the average salary at Facebook is about $250,000 and Alphabet workers take home around $200,000 now.

Pay packages will continue to rise in Silicon Valley as tech companies vie for the same talent pool and have boatloads of capital to wield to hire them.

This is terrible for margins as wages are the costliest input to operate tech companies.

United Technologies Corp. (UTX) chief executive Gregory Hayes chimed in citing a horrid “labor shortage in the U.S. and in Europe.”

He followed that up by saying the company will have to grapple with this additional cost pressure.

Certain commodity prices are spiraling out of control and will dampen profits for some tech companies.

Uber and Lyft, ridesharing app companies, are sensitive to the price of oil, and a spike could hurt the attractiveness to recruit potential drivers.

The perpetually volatile oil market has been trending higher since January, from $47 per barrel and another spike could damage Uber’s path to its IPO next year.

Will Uber be able to lure drivers into its ecosystem if $100 per barrel becomes the new normal?

Probably not unless every potential driver rolls around in a Toyota Prius.

If oil slides because of a global recession instigated by the current administration aim to rein in trade partners, then Uber will be hard hit abroad because it boasts major operations in many foreign megacities.

A recession means less spending on Uber.

Either result will be negative for Uber and ridesharing companies won’t be the only companies to be hit.

Other victims will be tech companies incorporating transport as part of their business model, such as Amazon which will have to pass on more delivery costs to the customer or absorb the blows themselves.

Logistics is a massive expense for them transporting goods to and from fulfillment centers. And they have a freshly integrated Whole Foods business offering two-hour free delivery.

Higher transport costs will bite into the bottom line, which is always a contentious issue for Amazon shareholders.

Another red flag is the deceleration of the global smartphone market evident in the lackluster Samsung earnings reflecting a massive loss of market share to Chinese foes who will tear apart profit margins.

Even though Samsung has a stranglehold on the chip market, mobile shipments have fell off a cliff.

Damaging market share loss to Chinese smartphone makers Xiaomi and Huawei are undercutting Samsung products. Chinese companies offer better value for money and are scoring big in the emerging world where incomes are lower making Chinese phones more viable.

The same trend is happening to Samsung’s screen business and there could be no way back competing against cheaper, lower quality but good enough Chinese imitations.

Pouring gasoline on the fire is the Chinese investigation charging Micron (MU), SK Hynix, and Samsung for colluding together to prop up chip prices.

These three companies control more than 90% of the global DRAM chip market and China is its biggest customer.

The golden days are over for smartphone growth as customers are not flooding into stores to buy incremental improvements on new models.

Customers are staying away.

The smartphone market is turning into the American used car market with people holding on to their models longer and only upgrading if it makes practical sense.

Chinese smartphone makers will continue to grab global smartphone market share with their cheaper premium versions that western companies rather avoid.

Battling against Chinese companies almost always means slashing margins to the bone and highlights the importance of companies such as Apple (AAPL), which are great innovators and produce the best of the best justifying lofty pricing.

The stagnating smartphone market will hurt chip and component company revenues that have already been hit by the protectionist measures from the trade war.

They could turn into political bargaining chips and short-term pressures will slam these stocks.

This quarter’s earnings season has seen a slew of weak guidance from Facebook, Nvidia (NVDA) mixed in with great numbers from Alphabet and Amazon.

Beating these soaring estimates is not a guarantee anymore as we move into the latter part of the year.

Migrating into the highest quality names such as Amazon and Microsoft (MSFT) with bulletproof revenue drivers would be the sensible strategy if tech’s lofty valuations do not scare you off.

Tech has had its own cake and ate it too for years. But on the near horizon, overdelivering on earnings results will be an arduous chore if outside pressures do not relent.

It’s been fashionable in the past for market insiders to call the top of the tech market, but precisely calling the top is impossible.

The long-term tech story is still intact but be prepared for short-term turbulence.

“By giving people the power to share, we're making the world more transparent,” – said cofounder and CEO of Facebook Mark Zuckerberg.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-22 03:05:032018-08-22 06:23:58What’s in Store for Tech in the Second Half of 2018?

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or

IS THE TRADE WAR ON OR OFF?),

(AAPL), (UUP), (EEM), (NFLX), (TSLA), (GOOGL), (SOYB),

(SOME SAGE ADVICE ABOUT ASSET ALLOCATION)

Is the trade war on or off? Trillions of dollars in cash flow and investment depend on the answer to the question.

Traders and investors can be forgiven for being confused. It was only a week ago that a doubling of duties on Turkish imports were threatened because of an American pastor locked up there two years ago, triggering a stock meltdown.

Then, on Wednesday night presidential economic advisor Larry Kudlow hinted that he would meet with a Chinese trade delegation, prompting a 400-point Dow melt-up. Please note that except for Apple (AAPL), technology stocks did not participate in the rally one iota.

In the meantime, Apple continued its relentless march to my $220 target for $2018, so you might think about taking some money off the table. The market capitalization now stands at a staggering $1.05 trillion, the largest in the world.

It vindicates my call that at any time the administration could suddenly declare victory in the trade war, prompting a major stock market rally, regardless of the outcome.

So what happens next. Expect the trade talks to fail, or not happen at all. Market meltdowns will be followed by melt-up, then meltdowns again. Certainly, that's what the soybean (SOYB) market believes, that new canary in the coal mine for our global trade wars. It barely moved this week.

Hey, if trading were easy it would pay the federal minimum wage rate of $7.25 an hour, so quit your complaining!

As if trade wars were the only thing to worry about these days.

There is a mass protest underway at Alphabet (GOOGL) over the company's proposal to re-enter the China market. No one wants to assist the Middle Kingdom's harsh censorship regime, and some 1,000 employees have already signed a petition to this effect.

Emerging markets (EEM) continue to get pounded by trade wars and a strong U.S. dollar (UUP), which has the effect of increasing their companies' local currency debt.

Elon Musk continues his slow motion public nervous breakdown, cutting Tesla's stock at the knees down to $305. I hope you all took my advice last week to unload the stock at $380.

Netflix (NFLX) shares are undergoing a serious pullback now that it is in between upgrade launches, and the trade wars and strong dollar eat into international subscriber growth, about 80% of the total. Don't forget to buy this dip.

With the Mad Hedge Market Timing Index stuck dead on 50, I am not inclined to reach for trades here. A reading of 50 gives you the perfect "do nothing" indicator. As is always the case when I return from vacation my first few trades are a rude awakening. August is now showing a modest return of 0.23%. My 2018 year-to-date performance has clawed its way up to 25.03% and my nine-year return appreciated to 302.61%. The Averaged Annualized Return stands at 34.91%. The more narrowly focused Mad Hedge Technology Fund Trade Alert performance is annualizing now at an impressive 32.24%.

This coming week housing statistics will give the most important insights on the state of the economy. On Monday, August 20, there will be nothing of note to report. It will just be another boring summer day.

On Tuesday, August 21, same thing.

On Wednesday, August 22 at 9:15 AM, we learn July Existing Home Sales. Will the rot continue? Weekly EIA Petroleum Inventory Statistics are out at 10:30 AM. The Fed Minutes from the meeting six weeks ago are out at 2:00 PM EST.

Thursday, August 23 leads with the Weekly Jobless Claims at 8:30 AM EST, which saw a fall of 12,000 last week to 212,000. Also announced are July New Home Sales. The two-day Jackson Hole Symposium of central bankers starts in the morning.

On Friday, August 24 at 8:30 AM EST, we get July Durable Goods. Then the Baker Hughes Rig Count is announced at 1:00 PM EST.

As for me, it is back to school week for me, so I will be making the rounds with the new teachers at two schools. I have to confess that at my age I have trouble distinguishing between the students and the teachers.

Finally, a sad farewell to Aretha Franklin, the Queen of soul, who provided me with a half century of listening pleasure. When I was young, I couldn't afford to go see her, and when I got old I didn't have the time. Isn't life lived backward?

Good luck and good trading.

UP, DOWN, UP, DOWN!

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-20 01:07:242018-08-20 01:07:24The Market Outlook for the Week Ahead, or Is the Trade War on or Off?

That's right, Amazon (AMZN) will join Facebook (FB) and Alphabet (GOOGL) as the last member of the triumvirate dominating the global digital ad industry.

That is what all signs are pointing to.

In a survey conducted by PricewaterhouseCoopers (PwC), the global digital ad industry increased by 21% YOY to $88 billion in 2017.

Of that growth, Facebook and Alphabet commanded 90% of it.

Mobile ad growth exploded last year because of the migration to smartphones increasing by 36.2% YOY in 2017.

Mobile ad revenue accounted for 56.7% of the digital ad dollars.

Search ad growth decelerated from 48% to 46% market share, but overall revenue climbed 18% to $40.6 billion reflecting the preference for older generations to use desktop search as their go-to platform.

Younger generations prefer dynamic video advertising, which suits mobile devices and tablets.

This segment grew 33% to $11.9 billion and is set to eat into search ad market share going forward.

This all bodes well for Amazon, which can take advantage of these various channels to pump through more ads that companies are clamoring to buy on Amazon's e-commerce platform.

Video ads would be ripe for Amazon Prime Video too, Amazon's on-demand media content service.

By 2021, Amazon's digital ad profits will eclipse its cloud profits solidifying Amazon as the best American tech company because of its multitude of premium profit drivers.

As time goes by, the quality of Amazon's company ascends with no restraints.

The Mad Hedge Technology Letter rates Amazon as the best publicly traded tech stock and that will not change anytime soon.

Amazon's digital ad revenue shot up 129% YOY to $2.2 billion.

This growth rate would make any investor drool.

Amazon might want to shift this business over from the "other" line item on its earnings report because it is blossoming into a main engine of growth and profit.

As Facebook and Alphabet have demonstrated, the digital ad game is a high profit, zero sum game, and Amazon is in perfect position to capitalize going forward.

Amazon's e-commerce business is the foolproof platform that can attract digital ad dollars in droves.

Not only are customers already buying products on Amazon.com, but they are usually purchasing numerous items highlighting the suitability of Amazon populating relevant ads to its customers.

Amazon's strategy to sell high-volume, good value for money products fits nicely into the digital ad strategy with plenty of opportunity for ad buyers to roll out ad campaigns to the masses.

Amazon continues to augment its digital ad tech team creating new tools and has now started directly approaching brands directly racking up digital ad sales.

Amazon's gain is Facebook and Alphabet's loss.

If Amazon goes full steam into the ad tech game, it could do what it has done to brick-and-mortar retail - deflate prices.

This is a worrying sign for Facebook, which is already on the ropes after realizing its business model has some major holes.

Alphabet's strategic position is superior to Facebook's, but it is very much still a one-trick ad tech pony.

The attempt to reintegrate a censored version of its Google search into China makes sense when other FANGs are coming for their lunch stateside.

This epitomizes the current tech climate - evolve now or die.

Amazon is working on a new video ad product that it will place in its search results.

This new product is currently in beta testing mode.

These video ads will be 90 seconds or less and will direct customers to a custom landing page or directly to an official website where they can purchase the item.

The video ad will only be shown for users of iPhones and iPads initially.

Amazon is requiring companies to pay a minimum of $35,000 for this new type of ad campaign. Some of its prominent ad buyers such as Procter and Gamble are already testing out this service to curate the perfect video ads to place inside Amazon search.

At first, the inventory for these video ads will be restricted.

Amazon Media Group is the in-house sales team responsible for selling these new products.

For example, in Germany, the habitual Amazon customer carries out a systematic routine to buy Amazon products.

First, customers will perform astute research on potential products and analyze different price points to gain a comprehensive picture of the market using their smartphone.

The customer later adds the desired items into the shopping cart.

At a later date, the customer purchases the item on a different device, and in many instances, mobile is used just to research products when the customer is out and about.

This multi-leg buying process gives Amazon multiple chances where it can fit in some video ads for the customers.

It is true that the minimum $35,000 will make it harder for small businesses to compete, but this is tailor-made for larger companies to offer a compelling case to customers while leveraging their brand awareness.

It is entirely possible that Amazon will surpass $8 billion in digital ad revenue in 2018 and then blow by $16 billion by 2020.

Of that $16 billion in revenue, $12 billion could be booked as operating profit showing off the juicy margins that make this industry so attractive for the neutral observer.

Yes, Amazon has the largest and best product search engine in the world, and it's time to start leveraging this asset to drive monetization growth.

Specifically, the ability for customers to click on an ad and be shuttled over to Amazon.com for final purchase.

This is the x-factor missing out on Facebook and Google search models.

Amazon has the capability to cherry-pick revenue from each part of the process up until the delivery to the door.

This opens a slew of extra revenue down the road as it enhances the shopping experience because Amazon has full control over the whole process.

This runs parallel with Amazon changing how its ad tech operates to accommodate the emphasis on generating huge growth numbers in ad volume and sales.

Small ad buyers usually work through an agency to integrate with Amazon while larger ad buyers work with Amazon's in-house team.

In the next few weeks, sponsored websites outside of Amazon's ecosystem will start advertising to shoppers who are able to click a link directly moving the buyer back to Amazon.com.

The sponsored ad route is a direct shot at Google search and Facebook.

Unsurprisingly, Amazon converts sales at a 350% higher rate than Google, underscoring the effectiveness of digital ads for Amazon.

When customers are already on the Internet to shop, shoppers could do a lot worse than clicking on a direct link funneling them to Amazon.com.

Posting baby photos on Facebook is not likely to convert users into product buyers.

Neither is checking your Gmail account, translating foreign language on Google Translate, or using Google Search to populate results usually not related to shopping.

These methods fail to convert an Internet surfer to product buyers to the detriment of Facebook and Google search.

Amazon has the perfect business model for selling digital ads.

This robust ad business will spur Amazon shares more than $2,000, and the quality of the sum of the parts keeps rising.

Execution is the only roadblock. And as most of us know, Amazon is one of the most innovative and cleanly executed companies in the world with visionary strategists.

Each generation grows up in its own unique environment.

Childhood experiences differ more and more as the world rapidly changes because of hyper-accelerating technology.

Millennials are usually defined as children born between 1981 to 1996.

They were the last generation to grow up outside breathing crisp, fresh air and meandering around the neighborhood with their friends looking for excitement.

Generation Z is the first generation in America generally raised indoors because of their overwhelming preference and broad-based addiction to technology.

Social media stocks have been a huge winner from this new paradigm shift in the behavior of young adults.

Instead of running around the block in packs, children are laser focused on these platforms communicating with the entire world and propping up their social lives.

Children meet a lot less than they used to and convening on a social media platform of choice has become the new normal.

Platforms such as Twitter (TWTR), Instagram and Snapchat (SNAP) have convincingly won over these new eyeballs even so much so that the new "going out" is congregating on Snapchat with a group of friends.

Facebook (FB) is now considered a legacy social media platform full of millennials and the older crowd.

Generation Z do not fancy drugs or drinking like the youth before them, rather, their panacea is video games and a lot of them.

These new societal trends will hugely affect your portfolio going forward.

A battle royal game is a video game category mixing the survival, exploration and scavenging elements together with last-man-standing gameplay.

These types of games predominantly contain 100 players sharing the same experience on a broadband connection.

This genre has been all the rage with PlayerUnknown's Battlegrounds (PUBG) piling up 400 million gamers across the globe selling 50 million copies of the game.

Of the 400 million gamers, 88% access the game via mobile devices highlighting the vigorous shift to mobile for younger generations.

PUBG made more than $700 million in sales in 2017.

The rise of the billion-dollar video games is alive and well.

In fact, Activision Blizzard (ATVI) stakes claim to eight gaming franchises commanding more than $1 billion in annual revenue with titles such as Overwatch, Candy Crush, and Call of Duty.

The popularity of video games will drive GPU manufacturers Nvidia (NVDA) and AMD (AMD) to new heights because gamers require high-quality GPUs to effectively game.

Nvidia CEO Jensen Huang even spouted that "the success of Fortnite and PUBG are just beyond comprehension" boosting GPU sales and capturing the imagination of global youth.

Fortnite, a "Hunger Games" style battle royal video game mirroring PUBG, has taken the world by storm in 2018.

This cultural juggernaut surpassed the 125 million gamer mark in just one year.

In February 2018, Epic Games, the maker of Fortnite, earned $126 million in one month, and it was the first time it passed PUBG in monthly sales.

In April 2018, it followed up monster February numbers by pulling in $296 million.

The growth trajectory is parabolic. Hold onto your hats.

Fortnite sparkles in the sunlight because its free-to-play model does not exclude anyone and is available on all devices.

At first, Fortnite was available for iOS customers and Samsung Android holders because it inked an exclusive deal with Samsung.

This week is the first week Epic Games is rolling out Fortnite to non-Samsung Android users with an interesting caveat.

The Android version of Fortnite bypasses Google Play (Google's app store on Android) preferring to sell the game direct for download from its official website.

This highlights that content is truly king.

Epic Games is betting the surge in popularity for its juggernaut game will sell itself.

This decision will cost Alphabet (GOOGL) $70 million per year in commission.

Apple makes it mandatory that any app downloaded to its devices must be downloaded from Apple's app store.

However, Android doesn't have the same requirements as its system is more functional, open, and a developer's dream.

Simply put, there are ways to download the game on Android without ever touching Google Play.

Going forward this could have a similar effect Spotify (SPOT) had on Wall Street on its IPO.

The middlemen or broker app could get bypassed in favor of direct sales.

Apple pockets commission on 30% of all in-app spending raking in around $60 million from Fortnite.

In-game add-on revenue is how Fortnite makes money from this free-to-play game.

The bulk of spending comes in the form of costumes better known as skins, where players pay to dress up their character in various garments selected for purchase.

The other revenue stream is a season subscription on sale for $10.

The tech sector has been migrating to subscription-based offerings and video games are no different.

This could play havoc with Alphabet's Google Play and Apple's app store down the line if prominent content producers choose to bypass their stores to sell directly.

The lack of video game exposure to the FANG group is mind-boggling. It seems they have their finger on the pulse of every other major trend in technology but have missed out on this one.

Microsoft (MSFT) is the closest FANG-like stock deep inside the video game ecosphere by way of its famous console Xbox.

In fact, Microsoft earns more than $10 billion per year from its gaming segment surpassing Nintendo at $9.7 billion per year.

This doesn't eclipse Sony's gaming revenue, which is $17 billion per year, but the 36% YOY growth in Xbox-related revenue signals its intent in the gaming industry that plays second fiddle to its cloud and software businesses.

Gaming is just a side business for Microsoft right now.

Ironically, Tencent has a 40% stake in Epic Games and is patiently waiting for government approval to sell Fortnite in China, which could be painstakingly arduous.

If Tencent gets the green light, Fortnite could develop into a monster business in 2018, and this is just the beginning.

Regrettably, Tencent has been mired in regulatory issues with the communist government reluctant to approve selling in-game products, which usually make up the bulk of revenue.

Recent blockbuster hit "Monster Hunter: World" was blocked by censors after debuting to great fanfare on August 8, 2018.

This title was expected to be one of the most popular video games of 2018.

Chinese state censors are on a short-term crusade to block the video game industry from receiving critical licenses and is the main reason for Tencent shares' headwinds.

Tencent shares peaked in January and are down almost 15% in 2018 because of uncertain gaming revenues.

Investors need to wake up and understand the gaming industry is about to mushroom because of demographics and the migration away from outdoor activity.

Following generations will have an even stronger bias toward technology-based indoor entertainment.

We are entering into the unknown of $4 billion per year video game businesses based on just one title and not one company.

Fortnite made PUBG's $700 million in revenue last year look paltry.

Gamers will soon see the rise of a $5 billion game franchise in 2019 and the sky is the limit.

This industry has growth, growth, and more growth and these single titles could surpass revenue of large semiconductor or hardware companies.

Don't underestimate the power of your child gaming away in your basement, he or she is part and parcel of a wicked tech growth driver about which not many people know.

Unfortunately, Epic Games is not a public company and shares cannot be purchased, but the success of Fortnite means that investors must pay heed to these new developments.

I am highly bullish on the video game sector and a big proponent of Activision (ATVI). A secondary name would be EA Sports (EA), which curates the Madden and FIFA franchises.

ATVI has felt the Fortnite effect in its share price selling off 11% because of investors' nervousness of Fortnite siphoning off ATVI gamers.

This short-term drop is a nice entry point into a solid video gaming company with various successful franchises that have withstood the test of time.

The 200-day moving average has provided ironclad support on the way up, and the Fortnite phenomenon won't last forever.

I would avoid the video game ETF ticker symbol GAMR because it includes one of my bona fide shorts - GameStop (GME).

It's mainly comprised of American, Japanese, and a Korean name but it would be sensible to focus on the companies with the highest quality comprehensive content.

The ETFs recent drop is also due to the strength of Fortnite.

"Companies in every industry need to assume that a software revolution is coming." - said Silicon Valley venture capitalist Marc Andreessen.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-15 01:05:372018-08-15 01:05:37How to Play the New Fortnite Gaming Fad

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.