Mad Hedge Technology Letter

May 2, 2018

Fiat Lux

Featured Trade:

(FACEBOOK GOES FROM STRENGTH TO STRENGTH),

(FB), (AMZN), (GOOGL), (NFLX)

Mad Hedge Technology Letter

May 2, 2018

Fiat Lux

Featured Trade:

(FACEBOOK GOES FROM STRENGTH TO STRENGTH),

(FB), (AMZN), (GOOGL), (NFLX)

Everyone and their mother was waiting for Facebook (FB) to fluff their lines, but they defied the odds by posting solid performance.

The data police can go back to eating doughnuts because it is obvious that regulation won't fizzle out the precious growth drivers that Mark Zuckerberg relies on to please investors.

I even begged readers to buy the regulatory dip, and I was proved correct with Facebook shares rebounding from $155 to $173.

The dip buying was proof that investors have faith in Facebook's business model.

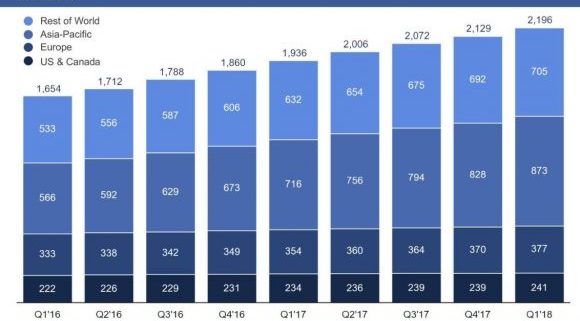

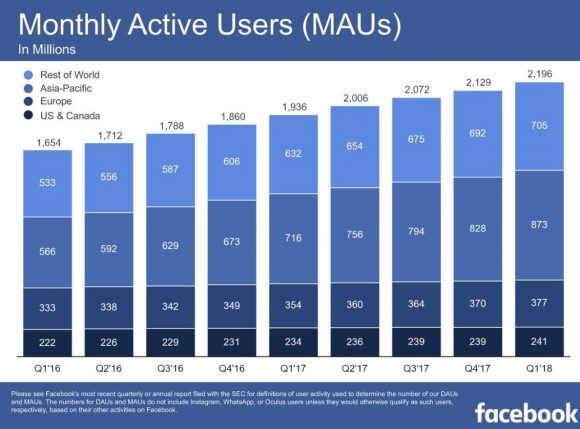

The Cambridge Analytica scandal threatened to tear apart the quarterly numbers and place Facebook in the tech doghouse, but stabilization in Monthly Active Users (MAU) and bumper digital ad revenue growth was the perfect elixir to an eagerly anticipated earnings report.

Facebook showed resilience by growing (MAU) to 2.2 billion, up 13% at a time when attrition could have reared its ugly head.

The market breathed a huge sigh of relief as the Facebook beat came to light.

The battering that Facebook received in the press effectively lowered the bar and Facebook delivered in spades.

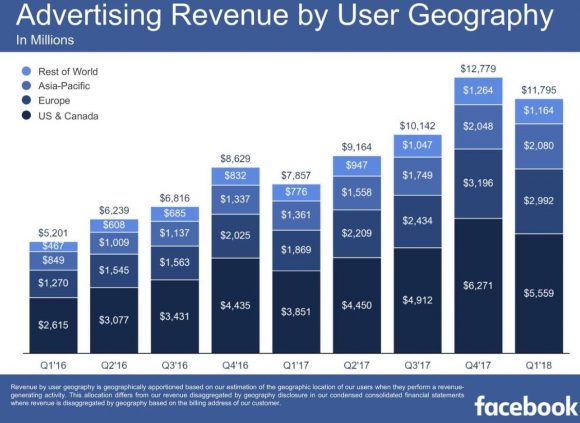

The unfaltering migration to mobile continues throughout the industry with mobile digital ad revenue making up 91% of ad revenue, which is a nice bump from the 85% last quarter.

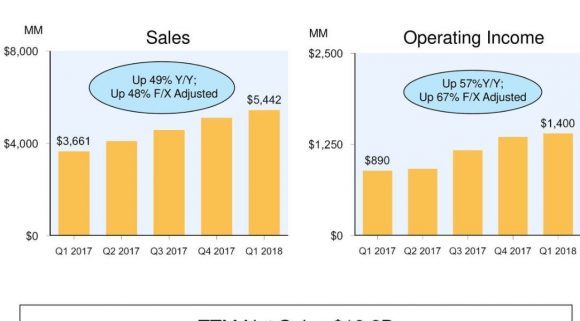

Overall, Facebook grew revenues 49% YOY to $11.97 billion.

There is no getting around that Facebook is a highly profitable business due to the lack of costs. I should be so lucky.

Remember at Facebook, the user is the product.

Instead of paying for rising TAC (Traffic Acquisition Costs) as does Google (GOOGL) or the $8 billion outlay for Netflix's (NFLX) annual content budget, Facebook pours its money into improving its digital platform and advancing its ad tech capabilities.

However, moving forward, Facebook will have to cope with extra regulatory costs.

Facebook recently hired a legion of content supervisors at minimum wage to root out the toxic content roaming around on its platform.

Site operators have doubled to 14,000. This number gives you a taste why the large cap tech names are best positioned to combat the new era of regulation.

Doubling the staff of any business would be a tough cost pill to swallow.

Many companies would go under, but Facebook has the cash to mitigate the additional cost of doing business.

This defensive initiative casts Facebook in a better light than before like a superhero rooting out the evil villain.

Facebook and its co-founder Mark Zuckerberg need to hire a better public relations team to ensure that Mark Zuckerberg isn't pigeonholed in mainstream media as the monster of tech.

The Amazon-effect is infiltrating every possible industry, and even the bigger tech names are coping with the Amazon (AMZN) spillage onto competitors' turf.

A risk down the line is Amazon's booming digital ad business nibbling away at Facebook's own digital ad model.

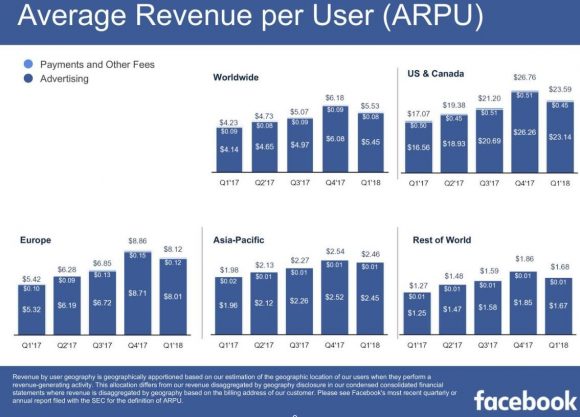

ARPU (Average Revenue Per User) remains robust with Facebook earning $23.59 per North American user, which is the most lucrative geographic location.

Artificial Intelligence (A.I.) is a tool that Facebook has implemented into its platform and monitoring apparatus.

Removing damaging content preemptively is the order of the day instead of being blamed for harboring nefarious content.

One example of this use case has been targeting ISIS- and Al Qaeda-related terror content with 99% of inappropriate content removed before being flagged by a human.

Heavy investments in A.I. will make Facebook a safer place to share content.

Big events exemplify the strength of Facebook.

During the Super Bowl in February, around 95% of national TV advertisers were simultaneously posting ads on Facebook because of the viral effect commercials and posts have during massive events.

Tourism Australia is another firm that bought ads on Instagram and Facebook platforms during the Super Bowl.

The campaign was hugely successful with half the leads for Tourism Australia coming directly from Facebook.

Facebook acts as the go-to provider for quality digital marketing and this will not change for the foreseeable future.

Investors can feel comfortable that there was no advertiser revolt after the big data chaos.

Facebook is improving its ad tech, and new ad products will be introduced to the 2.2 billion MAUs.

For instance, Facebook developed a carousel of rotating ads on Instagram Stories, and advertisers will be able to share up to three video or photos now instead of one. If the user swipes up, the swipe will take them directly to the advertisers' websites.

The shopping experience is more personalized now with an updated news feed that will show a full-screen catalog to help the user find whatever is in their search.

Facebook will only get better at placing suitable ads that mesh with the users' interests or hobbies.

Investors must be cautious to not let macro-headwinds sabotage existing positions.

Facebook's underlying growth drivers remain intact, but the stock is vulnerable to regulation headline risk that caps its short-term upside.

There is also the possibility that another Cambridge Analytica is just around the corner, which would result in a swift 10% correction.

Next earnings report should be interesting because it will reflect the first quarter that Facebook has operated with higher security expenses and will go a long way to validating its business model in a new era of rigid regulation.

If Facebook does not fill in the moat around the business, then Facebook is braced to grow top and bottom line with minimal resistance.

The cherry on top was the additional $9 billion of buybacks giving the stock price further support.

Facebook is a long-term hold but a risky short-term trade.

_________________________________________________________________________________________________

Quote of the Day

"Never trust a computer you can't throw out a window." - said Apple cofounder Steve Wozniak.

Mad Hedge Technology Letter

May 1, 2018

Fiat Lux

Featured Trade:

(AMAZON KILLS IT AGAIN),

(AMZN), (WMT), (FB), (TGT), (GOOGL)

Jeff Bezos is a god.

Well, not quite but he is turning into one after Amazon delivered a mythical earnings report that left Amazon haters in awe.

The Amazon bears patiently waiting for the day of reckoning will have to wait longer as Amazon smashed earnings expectations by a magnitude of two or three.

Amazon had a lot riding on the most recent earnings report after racing to new highs in mid-March.

The brief macro-correction then gave investors yet another entry point into one of the best companies of our generation that is still up more than 30% this year.

Amazon Web Services (AWS) revenue reaccelerated from its 42% growth last year to a high octane 49% YOY and made up a disproportionate 73% of Amazon's operating income.

Amazon is heavily reliant on the AWS segment to carry it through feast or famine.

According to Jeff Bezos, its critically acclaimed cloud segments' outstanding results originate from the "seven-year head start before like-minded competition."

This reaffirms the benefit of first-mover advantage with which large cap tech is obsessed.

There is room for other companies in the cloud space, with the cloud industry expanding 20% in 2018 to $186 billion.

Therefore, expanding by 20% is the bare bones minimum to be considered relevant.

Amazon has positioned itself to funnel in the most dollars that migrate toward the cloud as the industries pioneer and best of breed.

After the latest earnings report, Amazon is in pole position to become the first publicly traded $1 trillion company.

This latest quarter wrapped up its 62nd consecutive quarter of 20% plus growth.

And the commentary coming out of the earnings reports makes it almost certain that Amazon will capture more market share.

There were a few bombshells dropped that were unequivocal positives for investors.

First, Amazon has become the third player in digital ad industry with the duopoly of Google search and Facebook.

Amazon revved up its digital ad revenue by 139% QOQ to a substantial $2.03 billion per quarter business.

This business is particularly appetizing because of its high margins and will help alleviate tight margins on the e-commerce side.

Amazon's digital ad business is by far the fastest growth lever in its portfolio. It will ramp up this side of the business whose main function is to match consumers with suitable products that consumers otherwise would miss out on in a standard Amazon search.

The extraordinary numbers support the notion that the hoopla of Washington regulation is all bark and no bite.

Facebook also delivered a prodigious quarter for the ages amid testimony and public backlash that resulted in immaterial damage to top- and bottom-line numbers.

The second bombshell announced was the change in pricing to prime members. Amazon upped its annual prime membership to $119 from $99.

This additional $20 price hike, or 20% on 100 million prime members, will swell revenue by an extra $2 billion of incremental revenue.

In total, Amazon will accrue a bonus of 4% of revenue by this price change.

Amazon has a high fixed-cost business, and slightly tweaking prices will create a huge windfall with the revenue almost entirely flowing down to the bottom line in the form of pure profit.

Many industry analysts claim that Amazon has the best management team in the industry and explicate this company as an "Internet staple."

More than 100 million products are delivered with free shipping for Amazon prime customers. This is starkly higher than the 20 million products shipped for free in 2014.

Amazon does everything in its power to offer a unique and efficient experience for customers.

The customer satisfaction reveals itself by the rock-bottom churn rate.

Amazon prime at an annual cost of $119 is such a value that no analysts even dared to ask Amazon CFO Brian Olsavsky if consumers would take issue with the rise in price.

Investors and strangers alike assume that broad-based reoccurring revenue from annual prime membership is a given.

In an era of mass-scrutinization, Amazon's earnings call seemed like a celebration of the mythical achievements that are changing consumer behavior by the day.

The lack of inquiry was justifiable this time because the one major shortcoming suddenly remedied itself.

Amazon's doubters frequently attack the lack of margin growth because its business model is first and foremost a land grab for market share ignoring any remnants of margin stability.

Now that Amazon's digital ad business has sprouted up, the margin story, starting from a miniscule base, will go from weakness to an unrelenting success.

Amazon started with its ultra-thin margin e-commerce business that made an operating loss of $160 billion in 2017.

Cranking up a shiny, high margin business will be hard for the other FANGs to compete with as they gyrate toward other businesses that have lower margins than Amazon's digital ad segment.

This is a horrible time to start fighting Amazon in price wars as the paradigm shift to quantitative tightening has made the cost of capital demonstrably pricier.

Operating margins almost doubled from 2% to 3.8% on $51 billion of quarterly sales.

This is a huge deal.

Amazon has been continuously harangued for "not making money." Well, that era is over.

Profits, and not only revenue, will start accelerating and Amazon will become the closest thing to a perfect company.

The years and years of plowing cheap capital back into fulfillment center and e-commerce activity gave Amazon a stained reputation for years.

However, as Amazon turns the screws and uses its foundational leverage to capture additional profits, the other FANGs will be forced down the same path ruining operating margins for the other big players.

Amazon telegraphed its quest for market share strategy to investors years ago, and investors understand they are paying for growth and growth only.

That will change now that profits have become a real part of its arsenal.

There is no doubt that Amazon will deploy its profits back into expanding its company because Jeff Bezos knows that if he can grow Amazon's top-line number, investors will follow suit.

Also, spending means improving the products, and Amazon has never hesitated to spend big.

The move into digital ad growth is a warning shot to Facebook and Google. Amazon will mobilize its workforce to take on other business, and anything that is high margin is fair game.

The future looks bleak for retail competitors Walmart and Target, as the contents of the earnings report reaffirms Amazon's unrelenting assault on the retail sector, which is systematically being dissected by Amazon for fun.

Google search and Facebook are in Amazon's crosshairs. Staving off this monster will be hard to do in the long run.

Amazon has a clear path to further market gains, and operating margins are almost at a tipping point.

Revenue is poised to re-accelerate because of the reignition of AWS to a higher growth trajectory.

Shoring up operating margins through a burgeoning digital ad division will only be a boon to earnings in the future.

Amazon is one of the best companies in the world, and any weakness in the stock should be bought and held forever.

_________________________________________________________________________________________________

Quote of the Day

"I do not fear computers. I fear a lack of them," - said writer Isaac Asimov.

Featured Trade:

Below please find subscribers Q&A for the Mad Hedge Fund Trader April Global Strategy Webinar with my guest co-host Mike Pisani of Smart Option Trading.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Are you out of Alphabet (GOOGL) and Microsoft (MSFT)?

A. I'm out of Alphabet and I'm in Microsoft, but only for the very short term. I'm waiting for another big meltdown day to go back and buy everything back because I think the FANGs and technology in general are still in a secular bull market.

Q. Are Advanced Micro Devices (AMD) and NVIDIA (NVDA) affected by the underperformance of Bitcoin?

A. They are. Bitcoin has been an important part of the chip story for the last two years because mining, or the creation of bitcoins, creates enormous demand for chips to do the processing. I think selling in bitcoin is over for the time being. You had a $25 billion in capital gains taxes that had to be paid by April 15.

People were paying those bills by selling their bitcoins. That's over now, and bitcoin is rallied about 30% since Tax Day because of that. So, yes, bitcoin is getting so big that it is starting to affect the chip sector meaningfully. That is another reason why we see secular long-term growth in the entire chip sector.

Mike Pisani: Interesting take on bitcoin today, and I've been with you on it. I think the worst of it is over; it's going to go. Today is the largest volume day we've seen on it so far. We're up over 15,500 contracts traded.

Q: If you're 100% cash, is now a good time to commit funds to the equity market?

A. Franz, I would say nein. Absolutely not. 2009 was the time to commit funds to the equity market. If you're 100% cash now I would stay out for the next six months. We may get a good entry point over the summer or the fall. I'll let you know when that happens because I will be jumping back in myself.

But right now, a week ahead of the worst six months of equity investment of the year, I would stay away and do research instead. Read your Mad Hedge Fund Trader letters. Build a list of names that you're going to buy on the next meltdown and practice buying meltdowns with your practice account, which doesn't use real money.

There's a lot of things you can get ready to do for the next leg up in the bull market, but buying right now, NO! I would put that in the category of, "Is it time to start shorting bonds question?" that we got a few minutes ago.

Q: Why did tech stocks sell off when they have great earnings results?

A: It's called, "Buy the rumor, sell the news." So many people already own the stocks and were expecting good earnings that there was no surprise when they were announced. These are some of the most over-owned stocks in history.

Everybody in the world owns them. Many people have multiple weightings in them, so when we enter a high-risk macro environment, which we have now, you want to get rid of the most over-owned stocks. That is exactly why all of these stocks that have had great runs are selling off, even though they have great earnings report.

Q: Are financials a good play here with interest rates rising though 3%?

A. Normally I would say yes. However, the macro background for the general market are so negative they are overwhelming any positive fundamentals specific to individual sectors like banks and stocks like Citigroup (C). By the way, financials all reported great results and got killed, so that is why I bailed out of my (C) position this morning at around cost. If you throw the best news in the world on a stock and it won't go up, it's time to get out of there.

Q: Would an unleveraged inverse ETF like the ProShares Short S&P 500 ETF (SH) be good at a spike even now?

A. Yes, but when I say spike up better expect at least 20 (SPY) points or 1,000 Dow points. All these downside ETFs are great but you've got to get in at the right price. You know as they say in trading school, the profit is always made on the "BUY" and not on the "SELL."

So, if you can get on one of these super spikes up on the short side that is a great trade. So is the ProShares Ultra Short ETF (SDS) if you want to do the 2X leverage short fund. We've recently started doing this every month. We've been shorting (SPY)s and buying (VIX) on every one of these spikes up, and it's been working like a charm.

Q: Here's the best question of the day. Your timing has been perfect says Mary in Chicago, Ill.

A: Well, I'll take that kind of question all day long. Thank you very much. You're too nice to do that.

Q: Richard is asking would you buy an NVIDIA (NVDA) LEAP?

A: I would wait for meltdown days. Remember this is a market that gives you lots of meltdown days. Just wait for the next presidential tweet and you might get another 600-700-point dip in the markets. Those are the days you buy LEAPS. You don't have to get buy writing Trade Alerts like I do. You can just enter a limit order in your account. Put it as a stupidly low level to "BUY" and you may get hit. And that's where you really make the big money in this kind of market.

Q: Is there a good one- or two-month trade in Amazon?

A: Yeah, Paul, with this volatility you can pick a big winner like Amazon and you know to buy the 250-point dips and sell the rallies. These ranges are so wide now that even a beginner can make money. So, I would say you have to wait until after tomorrow on Amazon and let them get their earnings out. We know they're going to be great. They're doing home deliveries now to your car.

Q: Can long bond interest rates go up to 4%, and if that happens what would the market do?

A: Yes, they can go up to 4%, and I expect them to probably do that next year. What will it do to the market? Answer: Cause a bear market and a recession. Is that answer clear enough? My bet is that interest rates cap in this cycle much lower than they did in past cycles, maybe 4%-5%. We have been used to zero cost of money for so long that a move to 4% would be like stabbing somebody in the chest. People are much less able to deal with rising rates than they ever have been in the past, so watch this space.

Q: Should I buy the ProShares Ultra Short Treasury ETF (TBT) or the iShares 20+ Year Treasury Bond Fund (TLT)?

A: Brad, it's really is a leverage question for you. The (TLT) is 1X; the TBT is 2X, so I would be taking profits on the (TBT) here and then buying a couple of points lower. Or if you want to keep it for the long term you can but remember the cost of carry on the TBT is around 7% a year.

Q: Yves in Paris, France is asking: What possible scenario will you see material wage growth that could lead to higher inflation?

A: We're starting to see that now with the ultra-low unemployment rates. People are having great difficulty hiring anyone in technology. But at the minimum wage level there seems to be plenty of supply. The other possibility is that the cost of everything else goes up but wages, because technology is replacing jobs so fast there may never be any increase in wages.

So, we will get inflation, but nothing like the inflation we saw in the past driven by rising wages, commodity prices, oil prices, and interest rates. Yes, money is a commodity, which can add quite a lot to the cost of leveraged companies like airlines, REITs, and so on.

Q: Will rising interest rates force the US dollar up?

A. The answer is yes! It has been a long time coming, but if rates continue to rise from here, you can expect that to lead to a continuously rising dollar and falling foreign currencies, and that will become a major drag on the economy and corporate earnings going forward.

Q: When is a good time to buy TIPS?

A: Just like your Treasury bond short, I would buy Treasury Inflation Protected Securities (TIPS) on the next rally in bond prices (TLT) and dip in yields. That will give you a decent entry point. That said, TIPS have been a horrible performer for the last 10 years because there has just been no inflation. A lot of people just keep TIPS as a hedge in their portfolio and it just costs them money every year.

Q: Which could blow up, Brad wants to know, TBT or TLT?

A: The easy answer there is probably neither. But if I had to pick between the two, the (TBT) would be the one to blow up because it's a 2X and has a lot less liquidity. So, I can't image in what world has (TBT) blowing up, but then I don't watch zombie TV shows either.

Q: I think US equities are expensive. Are emerging markets (EEM) or Europe (HEDJ) a better bet for the rest of the year?

A: I would say yes. Because if interest rates here in the US go higher that means a stronger dollar. That means a weaker US stock market. Because US companies are punished by a rising dollar. And European and Asian companies benefit from a rising dollar and falling home currencies, so that makes Europe the first choice of any of the global markets.

Q: Does oil going to $100 have a chance of bringing down the US economy?

A: Absolutely yes. If oil prices don't start to slow down, they will start having a big impact on the economy because that means rising prices for any energy consumer, which is you and me.

With no ability to offset that by rising prices of your products that would put a squeeze on any oil consuming industry, which is why things like the transports and consumer staples have been performing so poorly. If we get to $100, then you're really looking at a full-on recession and bear market for stocks. By bear market I mean down 25% or more in stocks.

Q: How do you see the India ETF?

A: We like it. India is the No. 1 pick of any hedge fund investor in emerging markets, and the ETF you can buy there is the PowerShares India Portfolio ETF (PIN).

Mad Hedge Technology Letter

April 26, 2018

Fiat Lux

Featured Trade:

(THE SMALL AI PLAY YOU'VE NEVER HEARD OF),

(BOX), (GOOGL), (MSFT), (AMZN), (IBM)

The cloud segment of technology is hotter than hot, and as this sector starts to trade at a big premium, investors will have to look further down the chain of command to find a reasonable deal.

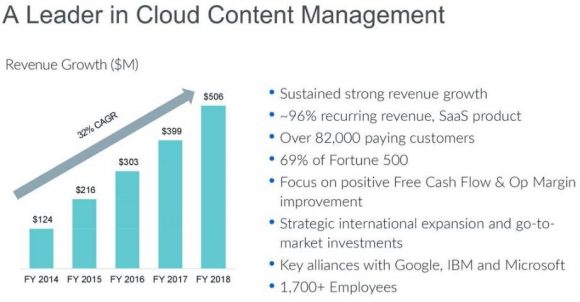

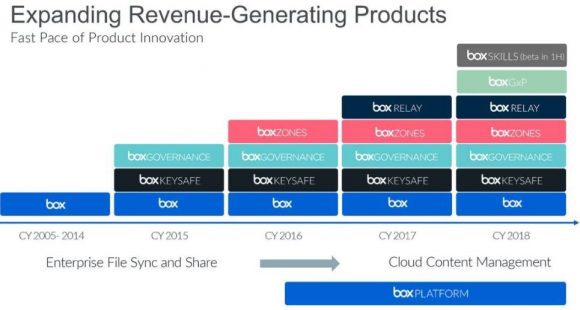

An up-and-coming cloud service Box (BOX) has gone undiscovered and is in position to seize a larger share of the cloud market moving forward.

The firm is led by CEO Aaron Levie who dropped out of my old alma mater USC in 2005 to start a cloud company with acting CFO and childhood friend Dylan Smith.

Last quarter was record-setting for Box, and it had a number of significant six- and seven-digit deals. Keep in mind Box's revenues are paltry compared to the behemoths that run this industry.

The platform has seen gradual success from all corners of the business world with various businesses from insurance claims processors to wealth advisors who use Box as a back-end platform.

Health care is another industry deploying the Box platform to aid and develop cloud services for patients.

In a general sense, the beauty of the cloud is the propensity to adapt to any company that is willing to go digital.

Even though many legacy companies are not natively digital, the cloud can twist and contort to fit the customers' needs.

Levie raised some compelling arguments for the continued tech momentum stating that imminent regulation in Europe through General Data Protection Regulation (GDPR) will act as a "broader tailwind in compliance and security efforts."

Box also announced a "readiness (GDPR) package" revealing that tech companies have been planning for the regulation overhaul up to 18 months in advance.

Even though mass media sensationalism would lead investors to believe the threat of regulation is about to blindside this whole sector, the unrest has been bubbling up for quite some time allowing tech companies ample time to get their houses in order.

Box actually sees the genesis of GDPR as a critical part of the cloud adoption process.

As dinosaur systems become outdated, a sense of safety reinforced by strong cybersecurity protection, strong privacy rules, and content compliance will nudge companies to head for the cloud like a drunk sailor to a pub.

Legacy platforms are the most susceptible to cyber-criminals and rogue hackers.

The analog defense is no match for sophisticated cyber-espionage, and GDPR will be another "driving force" behind the macro-migration shift to the cloud, just based on the security aspect alone.

Another pearl of wisdom offered by Box is that the bulk of clients requiring cloud products are integrating Microsoft Office 365.

This software acts as a lynchpin to any cloud service.

I must confess that I am writing this story on Microsoft Office 365 now, and most businesses cannot function without the dizzying array of Excel, PowerPoint, and Word.

Box has a strong relationship with Microsoft and has incisive insight into the synergies the cloud industry spins off.

The integration of Office 365 has complemented the Azure cloud with tighter cohesiveness.

The school of thought is the collective cloud industry is a $50 billion per year market and growing, offering smaller firms healthy growth levers to advance at the same time that the Microsofts (MSFT) and Amazons (AMZN) overperform.

At the Sohn Investment Conference in New York, Chamath Palihapitiya, a venture capitalist and former Facebook executive, extolled Box as a great way to play Artificial Intelligence (AI).

The shares spiked almost 13% upon his adulation.

A recent completed survey showed 66% of business leaders feel the pace of digitization must pick up in their own offices.

The speed of innovation is something that keeps most CEOs up at night. Wake up tomorrow and it is possible their core products could be outdated or disrupted by a new Amazon threat.

That is the world we live in now.

Only 42% of CIOs admitted they have a digital strategy. And of those digital strategies, they are mostly digital second or third, not digital first, blueprints.

In the same PricewaterhouseCoopers (PwC) survey, companies conceded that only 40% of IT teams are able to pursue the newest innovations with adopting specific operational needs in mind.

The micro-environment harbors the same bullishness as the macro-factors.

Box is hitting all the right notes.

Revenue is advancing at a 24% per year clip, and annual revenue surpassed the half a billion mark.

Box has indicated it expects to cross the $1 billion annual revenue threshold sometime in mid- to late 2021, giving the company more than three years to double revenue.

Recent reports support Box's growth trajectory.

About 60% of revenue derives from firms that employ more than 2,000 workers, highlighting Box's propensity to emphasize enterprise cloud development instead of small individual users.

Working with larger companies gives Box the opportunity to cross-sell more powerful add-ons, delivering a net expansion rate of 14%.

Migrating to a new cloud platform is incredibly sticky boosting retention rates. Box's churn rate is flourishing with a best of breed 4% per year. The key to expediting cloud success is quickening its pace of new product rollout.

Box attempts to give exactly what customers need with a spate of new concoctions.

Box GxP is a new product calibrated around life science companies. The Box GxP compliance is up to date with FDA regulations. And, Box has the ability to retire legacy ECM (Enterprise Content Management) systems.

This new service has experienced solid traction around the world as we head toward a world where legacy software becomes obsolete.

The second new offering is Box Skills, still in beta mode, which is a part of Box's artificial intelligence strategy.

Box is platform neutral allowing in-house architecture to support partnerships with Google, Microsoft, Amazon, and IBM to nail down third-party cloud tools that Box customers need.

Box Skills is a framework that brings the best machine learning innovation to content securely stored in Box.

This is managed through artificial intelligence, which automatically contextualizes images through detection protocols. Text recognition is automated for the benefit of the user, too.

Audio intelligence renders text transcripts and detects topics that can be searched in Box to locate an audio file by words or topic.

Video intelligence offers transcription, topic detection, and facial recognition allowing users to jump around video files in a non-linear fashion.

Palihapitiya effectively gave Box a free commercial to the tech investing world. His bull thesis for Box squarely centers around its AI innovations, specifically Box Skills.

The last new service to market is Box Transform, which is the advanced consulting arm of Box.

The goal of Transform is to arrange a concierge-like Box advisor that can help companies accelerate digital transformation throughout an organization while unlocking efficiencies and productivity for employees.

This service originated from Box's consulting advanced professional services team and will give Box another growth lever. Companies such as Red Hat and Intel have made the consultant- and support-side of the business a robust part of their organizations.

Impeding growth is the cutthroat competition in this space with Amazon, Microsoft, and Google (GOOGL).

However, margins remain strong at 75.5% last quarter, and Box expects margins to slightly dip around 74% this year.

Box has found a warm welcome for its newer products, deriving almost 70% of its new deals from fresh cloud offerings.

Partners are also a big source of new deals comprising more than half the deals over $100,000.

Specifically, IBM (IBM) made up a swath of its larger deals. In a sense, competitors are not really competitors.

They are frenemies. They compete against each other yet innovate and do deals together.

The core growth is supplemented by existing customers that are the best source of extra marginal revenue.

In short, once firms are firmly lodged on a platform, they buy everything on that platform.

Enter a supermarket, and odds are if goods are purchased, the receipt will be from the entered supermarket.

Box is entirely leveraged toward mid-sized and large enterprise business. That is where it makes its money.

The emphasis on large players boosts the ACV (Average Contract Value), which is regarded as a sacrosanct metric for Box.

The amount of data created in 2017 was more data created in the past 5,000 years. In the next five years, data volume with grow by 800%.

Box has continually positioned itself as the firm that can extract a staggering amount of unrealized value locked away in the nooks and crannies of legacy models.

Box is a great long-term hold as these diminutive cloud assets become more valuable by the day.

_________________________________________________________________________________________________

Quote of the Day

"Television won't be able to hold onto any market it captures after the first six months. People will soon get tired of staring at a plywood box every night." - said Darryl F. Zanuck, co-founder of Twentieth Century-Fox Film Corp.

Mad Hedge Technology Letter

April 25, 2018

Fiat Lux

Featured Trade:

(FANGS DELIVER ON EARNINGS, BUT FAIL ON PRICE ACTION),

(GOOGL), (AMZN), (MSFT), (AAPL), (FB),

(DBX), (NFLX), (BOX), (WDC)

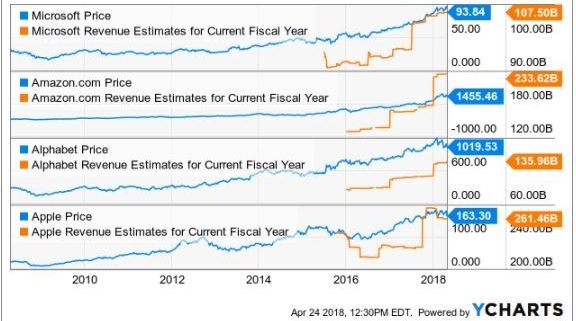

Alphabet (GOOGL) did a great job alleviating fears that large-cap tech would be dragged through the mud and fading earnings would dishearten investors.

The major takeaways from the recent deluge of tech earnings are large-cap tech is getting better at what they do best, and the biggest are getting decisively bigger.

Of the 26% rise to $31.1 billion in Alphabet's quarterly revenue, more than $26 billion was concentrated around its mammoth digital ad revenue business.

Alphabet, even though rebranded to express a diverse portfolio of assets, is still very much reliant on its ad revenue to carry the load made possible by Google search.

Its "other bets" category failed to impact the bottom line with loss-making speculative projects such as Nest Labs in charge of mounting a battle against Amazon's (AMZN) Alexa.

The quandary in this battle is the margins Alphabet will surrender to seize a portion of the future smart home market.

What we are seeing is a case of strength fueling further strength.

Alphabet did a lot to smooth over fears that government regulation would put a dent in its business model, asserting that it has been preparing for the new EU privacy rules for "18 months" and its search ad business will not be materially affected by these new standards.

CFO Ruth Porat emphasized the shift to mobile, as mobile growth is leading the charge due to Internet users' migration to mobile platforms.

Google search remains an unrivaled product that transcends culture, language, and society at optimal levels.

Sure, there are other online search engines out there, but the accuracy of results pale in comparison to the preeminent first-class operation at Google search.

Alphabet does not divulge revenue details about its cloud unit. However, the cloud unit is dropped into the "other revenues" category, which also includes hardware sales and posted close to $4.4 billion, up 36% YOY.

Although the cloud segment will never dwarf its premier digital ad segment, if Alphabet can ameliorate its cloud engine into a $10 billion per quarter segment, investors would dance in the streets with delight.

Another problem with the FANGs is that they are one-trick ponies. And if those ponies ever got locked up in the barn, it would spell imminent disaster.

Apple (AAPL) is trying its best to diversify away from the iconic product with which consumers identify.

The iPhone company is ramping up its services and subscription business to combat waning iPhone demand.

Alphabet is charging hard into the autonomous ride-sharing business seizing a leadership position.

Netflix (NFLX) is doubling down on what it already does great - create top-level original content.

This was after it shed its DVD business in the early stages after CEO Reed Hastings identified its imminent implosion.

Tech companies habitually display flexibility and nimbleness of which big corporations dream.

One of the few negatives in an otherwise solid earnings report was the TAC (traffic acquisition costs) reported at $6.28 billion, which make up 24% of total revenue.

An escalation of TAC as a percentage of revenue is certainly a risk factor for the digital ad business. But nibbling away at margins is not the end of the world, and the digital ad business will remain highly profitable moving forward.

TAC comprised 22% of revenue in Q1 2017, and the rise in costs reflects that mobile ads are priced at a premium.

Google noted that TAC will experience further pricing pressure because of the great leap toward mobile devices, but the pace of price increases will recede.

The increased cost of luring new eyeballs will not diminish FANGs' earnings report buttressed by secular trends that pervade Silicon Valley's platforms.

The year of the cloud has positive implications for Alphabet. It ranks No. 3 in the cloud industry behind Microsoft (MSFT) and Amazon.

Amazon and Microsoft announce earnings later this week. The robust cloud segments should easily reaffirm the bullish sentiment in tech stocks.

Amazon's earnings call could provide clarity on the bizarre backbiting emanating from the White House, even though Jeff Bezos rarely frequents the earnings call.

A thinly veiled or bold response would comfort investors because rumors of tech peaking would add immediate downside pressure to equities.

The wider-reaching short-term problem is the macro headwinds that could knock over tech's position on top of the equity pedestal and bring it back down to reality in a war of diplomatic rhetoric and international tariffs.

Google, Facebook, and Netflix are the least affected FANGs because they have been locked out of the Chinese market for years.

The Amazon Web Services (AWS) cloud arm of Amazon blew past cloud revenue estimates of 42% last quarter by registering a 45% jump in revenue.

Microsoft reiterated that immense cloud growth permeating through the industry, expanding 99% QOQ.

I expect repeat performances from the best cloud plays in the industry.

Any cloud firm growing under 20% is not even worth a look since the bull case for cloud revenue revolves around a minimum of 20% growth QOQ.

Amazon still boasts around 30% market share in the cloud space with Microsoft staking 15% but gaining each quarter.

AWS growth has been stunted for the past nine quarters as competition and cybersecurity costs related to patches erode margins.

Above all else, the one company that investors can pinpoint with margin problems is Amazon, which abandoned margin strength for market share years ago and that investors approved in droves.

AWS is the key driver of profits that allows Amazon to fund its e-commerce business.

Cloud adoption is still in the early stages.

Microsoft Azure and Google have a chance to catch up to AWS. There will be ample opportunity for these players to leverage existing infrastructure and expertise to rival AWS's strength.

As the recent IPO performance suggests, there is nothing hotter than this narrow sliver of tech, and this is all happening with numerous companies losing vast amounts of money such as Dropbox (DBX) and Box (BOX).

Microsoft has been inching toward gross profits of $8 billion per quarter and has been profitable for years.

And now it has a hyper-expanding cloud division to boot.

Any macro sell-off that pulls down Microsoft to around the $90 level or if Alphabet dips below $1,000, these would be great entry points into the core pillars of the equity market.

If tech goes, so will everything else.

If it plays its cards right, Microsoft Azure has the tools in place to overtake AWS.

Shorting cloud companies is a difficult proposition because the leg ups are legendary.

If traders are looking for any tech shorts to pile into, then focus on the legacy companies that lack a cloud growth driver.

Another cue would be a company that has not completed the resuscitation process yet, such as Western Digital (WDC) whose shares have traded sideways for the past year.

But for now, as the 10-year interest rate shoots past 3%, investors should bide their time as cheaper entry points will shortly appear.

_________________________________________________________________________________________________

Quote of the Day

"Technology is a word that describes something that doesn't work yet." - said British author Douglas Adams.