Mad Hedge Technology Letter

April 16, 2018

Fiat Lux

Featured Trade:

(THE HIGH COST OF DRIVING OUT OUR FOREIGN TECHNOLOGISTS),

(EA), (ADBE), (BABA), (BIDU), (FB), (GOOGL), (TWTR)

Mad Hedge Technology Letter

April 16, 2018

Fiat Lux

Featured Trade:

(THE HIGH COST OF DRIVING OUT OUR FOREIGN TECHNOLOGISTS),

(EA), (ADBE), (BABA), (BIDU), (FB), (GOOGL), (TWTR)

There is only so much juice you can squeeze from a lemon before nothing is left.

Silicon Valley has been focused mainly on squeezing the juice out of the Internet for the past 30 years with intense focus on the American consumer.

In an era of minimal regulation, companies grew at breakneck speeds right into families' living quarters and was a win-win proposition for both the user and the Internet.

The cream of the crop ideas were found briskly, and the low hanging fruit was pocketed by the venture capitalists (VCs).

That was then, and this is now.

No longer will VCs simply invest in various start-ups and 10 years later a Facebook (FB) or Alphabet (GOOGL) appears out of thin air.

That story is over. Facebook was the last one in the door.

VCs will become more selective because brilliant ideas must withstand the passage of time. Companies want to continue to be relevant in 20 or 30 years and not just disintegrate into obsolescence as did the Eastman Kodak Company, the doomed maker of silver-based film.

The San Francisco Bay Area is the mecca of technology, but recent indicators have presaged the upcoming trends that will reshape the industry.

In general, a healthy and booming local real estate sector is a net positive creating paper wealth for its people and attracting money slated for expansion.

However, it's crystal clear the net positive has flipped, and housing is now a buzzword for the maladies young people face to sustain themselves in the ultra-expensive coastal Northern California megacities. The loss of tax deductions in the recent tax bill make conditions even worse.

Monthly rental costs are deterring tech's future minions. Without the droves of talent flooding the area, it becomes harder for the industry to incrementally expand.

It also boosts the salaries of existing development/operations staffers who feed into the local housing market spiking prices because of the fear of missing out (FOMO).

After surveying HR tech heads, it's clear there aren't enough artificial intelligence (AI) programmers and coders to fill internal projects.

Compounding the housing crisis is the change of immigration policy that has frightened off many future Silicon Valley workers.

There is no surprise that millions of aspiring foreign students wish to take advantage of America's treasure of a higher education because there is nothing comparable at home.

The best and brightest foreign minds are trained in America, and a mass exodus would create an even fiercer deficit for global dev-ops talent.

These US-trained foreign tech workers are the main drivers of foreign tech start-ups. Dangling financial incentives for a chance to start an embryonic project at home is hard to pass up.

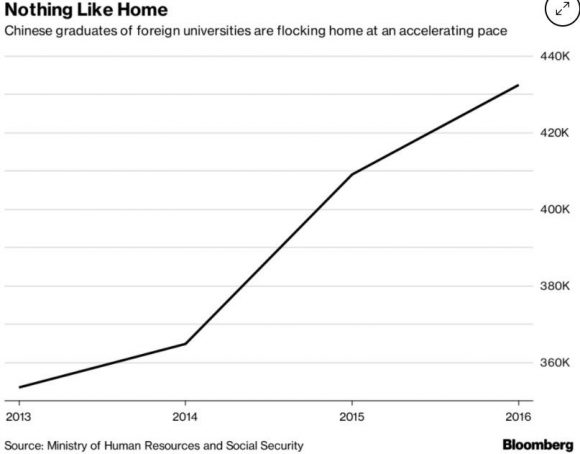

Ironically enough, there are more AI computer scientists of Chinese origin in America than there are in all of China.

There is a huge movement by the Chinese private sector to bring everyone back home as China vies to become the industry leader in AI.

Silicon Valley is on the verge of a brain drain of mythical proportions.

If America allows all these brilliant minds to fly home, not only to China but everywhere else, America is just training these workers to compete against American companies in the future.

A premier example is Baidu co-founder Robin Li who received his master's degree in computer science from the State University of New York at Buffalo in 1994.

After graduation, his first job was at Dow Jones & Company, a subsidiary of News Corps., writing code for the online version of the Wall Street Journal.

During this stint, he developed an algorithm for ranking search results that he patented, flew back to China, created the Google search engine equivalent, and named it Baidu (BIDU).

Robin Li is now one of the richest people in China with a fortune of close to $20 billion.

To show it's not just a one-hit wonder type scenario, three of the top five start-ups are currently headquartered in Beijing and not in California.

The most powerful industry in America's economy is just a transient training hub for foreign nationals before they go home to make the real cash.

More than 70% of tech employees in Silicon Valley, and more than 50% in the San Francisco Bay Area are foreign, according to the 2016 census data.

The point that really hits home is that the insane cost of housing is preventing burgeoning American talent from migrating from rural towns across America and moving to the Bay Area.

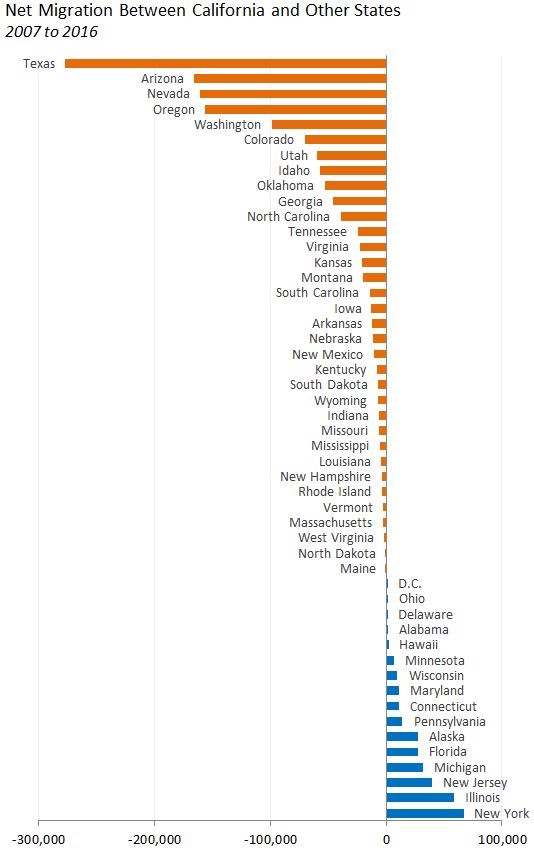

This trend was reinforced by domestic migration statistics.

Between 2007 and 2016, 5 million people moved to California, and 6 million people moved out of the state.

The biggest takeaways are that many of these new California migrants are from New York, possess graduate degrees, and command an annual salary of more than $110,000.

Conversely, Nevada, Arizona, and Texas have major inflows of migrants that mostly earn less than $50,000 per year and are less educated.

That will change in the near future.

Ultimately, if VCs think it is expensive now to operate a start-up in Silicon Valley, it will be costlier in the future.

Pouring gasoline on the flames, Northern Californian schools are starting to close down as there is a lack of students due to minimal household formation.

The biggest complaint is that there is no affordable housing.

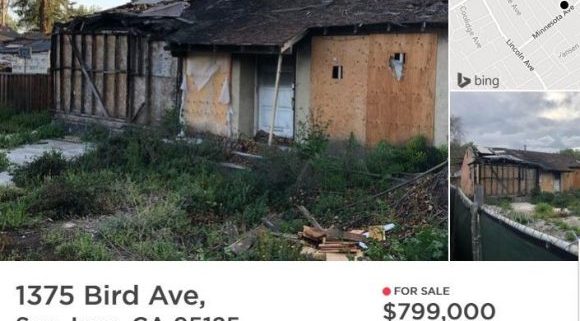

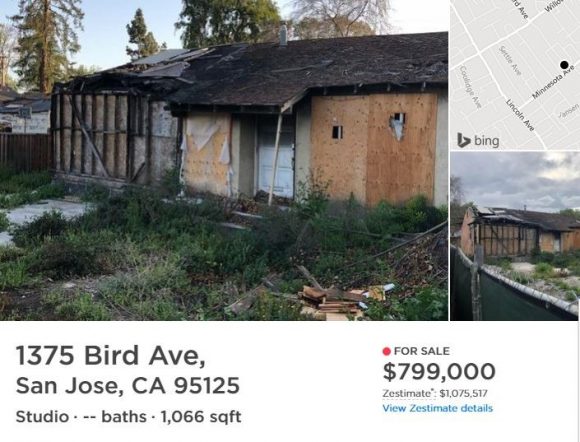

A 1,066-square-foot property in San Jose's Willow Glen neighborhood went on sale for $800,000.

This would be considered an absolute steal at this price, but the catch is the house was badly burned two years ago. This is the price for a teardown.

When you combine the housing crisis with the price readjustment for big data, it looks as if Silicon Valley has peaked.

Yes, the FANGs will continue their gravy train but the next big thing to hit tech will not originate from California.

VCs will overwhelmingly invest in data over rental bills, and the percolation of tech ingenuity will likely pop up in either Nevada, Arizona, Texas, Utah, or yes, even Michigan.

Even though these states attract poorer migrants, the lower cost of housing is beginning to attract tech professionals who can afford more than a burnt down shack.

Washington state has become a hotbed for Bitcoin activity. Small rural counties set in the Columbia Basin such as Chelan, Douglas, and Grant used to be farmland.

The bitcoin industry moved three hours east of Seattle for one reason and one reason only - cost.

Electricity is five times cheaper there because of fluid access to plentiful hydro-electric power.

Many business decisions come down to cost, and a fractional advantage of pennies.

Once millennials desire to form families, the only choices are regions where housing costs are affordable and areas that aren't bereft of tech talent.

Cities such as Las Vegas and Reno in Nevada; Austin, Texas; Phoenix, Arizona; and Salt Lake City, Utah, will turn into hotbeds of West Coast growth engines just as Hangzhou-based Alibaba (BABA) turned that city into more than a sleepy backwater town with a big lake at its center.

The overarching theme of decentralizing is taking the world by storm. The built-up power levers in Northern California are overheated, and the decentralization process will take many years to flow into the direction of these smaller but growing cities.

Salt Lake City, known as Silicon Slopes, has been a tech magnet of late with big players such as Adobe (ADBE), Twitter (TWTR), and EA Sports (EA) opening new branches there while Reno has become a massive hotspot for data server farms. Nearby Sparks hosts Tesla's Gigafactory 1 and most likely its next addition.

The half a billion-dollars required to build a proper tech company will stretch further in Austin or Las Vegas, and most of the funds will be reserved for tech talent - not slum landlords.

The nail in the coffin will be the millions saved in taxes.

The rise of the second-tier cities is the key to staying ahead of the race for tech supremacy.

__________________________________________________________________________________________________

Quote of the Day

"Twitter is about moving words. Square is about moving money." - said CEO of Twitter, Jack Dorsey, to The New Yorker, October 2013

Global Market Comments

April 13, 2018

Fiat Lux

Featured Trade:

(ANNOUNCING THE MAD HEDGE LAKE TAHOE, NEVADA, CONFERENCE, OCTOBER 26-27, 2018),

(APRIL 11 GLOBAL STRATEGY WEBINAR Q&A),

(TLT), (TBT), (GOOGL), (MU), (LRCX), (NVDA) (IBM),

(GLD), (AMZN), (MSFT), (XOM), (SPY), (QQQ)

Below please find subscribers' Q&A for the Mad Hedge Fund Trader April Global Strategy Webinar with my guest co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Many of your April positions are now profitable. Is there any reason to close out before expiration?

A: No one ever got fired for taking a profit. If you feel like you have enough in hand - like 50% of the maximum potential profit in the position, which we do have in more than half of our current positions - go ahead and take it.

I'll probably run all of our April expirations into expiration day because they are very deep in the money. Also, because of the higher volatility and because of higher implied volatility on individual stock options, you're being paid a lot more to run these into expiration than you ever have been before, so that is another benefit.

Of course, one good reason to take profits now is to roll into another position, and when we find them, that may be exactly what we do.

Q: What do you think will be the impact of the US hitting Syria with missiles?

A: Initially, probably a 3-, 4-, or 500-point drop, and then a very rapid recovery. While the Russians have threatened to shoot down our missiles, in actual fact they can't hit the broad side of a barn. When Russians fired their cruise missiles at Syrian targets, half of them landed in Iran.

At the end of the day, it doesn't really impact the US economy, but you will see a big move in gold, which we're already starting to see, and which is why we're long in gold - as a hedge against all our other positions against this kind of geopolitical event.

Q: Will 2018 be a bull market or a bear market?

A: We are still in a bull market, but we may see only half the returns of last year - in other words we'll get a 10% profit in stocks this year instead of a 20% profit, which means it has to rise 12% from here to hit that 10% up by year-end.

Q: What is your take on the ProShares Ultra Short 20+ Year Treasury Bond Fund (TBT)?

A: I am a big buyer here. I think that interest rates (TLT) are going to move down sharply for the rest of the year. The (TBT) here, in the mid $30s, is a great entry point - I would be buying it right now.

Q: How do you expect Google (GOOGL) to trade when the spread is so wide?

A: It will go up. Google is probably the best-quality technology company in the market, after Facebook (FB). We'll get some money moving out of Facebook into Google for exactly that reason; Google is Facebook without the political risk, the regulatory risk, and the security risks.

Q: Are any positions still a buy now?

A: All of them are buys now. But, do not chase the market on any conditions whatsoever. The market has an endless supply of sudden shocks coming out of Washington, which will give you that down-400-points-day. That is the day you jump in and buy. When you're buying on a 400-down-day, the risk reward is much better than buying on a 400-point up day.

Q: What is "sell in May and go away?"

A: It means take profits in all your positions in May when markets start to face historical headwinds for six months and either A) Wait for another major crash in the market (at the very least we'll get another test of the bottom of the recent range), or B) Just stay away completely; go spend all the money you made in the first half of 2018.

Q: Paul Ryan (the Republican Speaker of the House) resigned today; is he setting up for a presidential run against Trump in 2020?

A: I would say yes. Paul Ryan has been on the short list of presidential candidates for a long time. And Ryan may also be looking to leave Washington before the new Robert Mueller situation gets really unpleasant.

Q: What reaction do you expect if Trump resigns or is impeached?

A: I have Watergate to look back to; the stock market sold off 45% going into the Nixon resignation. It's a different world now, and there were a lot more things going wrong with the US economy in 1975 than there are now, like oil shocks, Vietnam, race riots, and recessions.

I would expect to get a decline, much less than that - maybe only a couple 1,000 points (or 10% or so), and then a strong Snapback Rally after that. We, in effect, have been discounting a Trump impeachment ever since he got in office. Thus far, the market has ignored it; now it's ignoring it a lot less.

Q: Thoughts on Micron Technology (MU), Lam Research (LRCX), and Nvidia (NVDA)?

A: It's all the same story: a UBS analyst who had never covered the chip sector before initiated coverage and issued a negative report on Micron Technology, which triggered a 10% sell-off in Micron, and 5% drops in every other chip company.

He took down maybe 20 different stocks based on the argument that the historically volatile chip cycle is ending now, and prices will fall through the end of the year. I think UBS is completely wrong, that the chip cycle has another 6 to 12 months to go before prices weaken.

All the research we've done through the Mad Hedge Technology Letter shows that UBS is entirely off base and that prices still remain quite strong. The chip shortage still lives! That makes the entire chip sector a buy here.

Q: Can Trump bring an antitrust action against Amazon?

A: No, no chance whatsoever. It is all political bluff. If you look at any definition of antitrust, is the consumer being harmed by Amazon (AMZN)?

Absolutely not - if they're getting the lowest prices and they're getting products delivered to their door for free, the consumer is not being harmed by lower prices.

Second is market share; normally, antitrust cases are brought when market shares get up to 70 or 80%. That's what we had with Microsoft (MSFT) in the 1990s and IBM (IBM) in the 1980s. The largest share Amazon has in any single market is 4%, so no there is basis whatsoever.

By the way, no president has ever attacked a private company on a daily basis for personal reasons like this one. Thank the president for giving us a great entry point for a stock that has basically gone up every day for two years. It's a rare opportunity.

Q: How will the trade war end?

A: I think the model for the China trade war is the US steel tariffs, where we announced tariffs against the entire world, and then exempted 75% of the world, declaring victory. That's exactly what's going to happen with China: We'll announce massive tariffs, do nothing for a while, and then negotiate modest token tariffs within a few areas. The US will declare victory, and the stock market rallies 2,000 points. That's why I have been adding risk almost every day for the last two weeks.

Q: Would you be buying ExonMobil (XOM) here, hoping for an oil breakout?

A: No, I think it's much more likely that oil is peaking out here, especially given the slowing economic data and a huge onslaught in supply from US fracking. We're getting big increases now in fracking numbers - that is very bad for prices a couple of months out. The only reason oil is this high is because Iran-sponsored Houthi rebels have been firing missiles at Saudi Arabia, which are completely harmless. In the old days, this would have caused oil to spike $50.

Q: Would you be selling stock into the rally (SPY), (QQQ)?

A: Not yet. I think the market has more to go on the upside, but you can still expect a lot of inter-day volatility depending on what comes out of Washington.

Q: Do you ever use stops on your option spreads?

A: I use mental stops. They don't take stop losses on call spreads and put spreads, and if they did they would absolutely take you to the cleaners. These are positions you never want to execute on market orders, which is what stop losses do. You always want to be working the middle of the spread. So, I use my mental stop. And when we do send out stop loss trade alerts, that's exactly where they're coming from.

Q: Will the Middle East uncertainty raise the price of oil?

A: Yes, if the Cold War with Iran turns hot, you could expect oil to go up $10 or $20 dollars higher, fairly quickly, regardless of what the fundamentals are. It's tough to be blowing up oil supplies as a great push on oil prices. But that's a big "if."

Hello from the Italian Riviera!

Global Market Comments

April 10, 2018

Fiat Lux

Featured Trade:

(DON'T MISS THE APRIL 11 GLOBAL STRATEGY WEBINAR),

(IT'S ALL ABOUT WHAT HAPPENS NEXT),

($INDU), (GOOGL),

(HOW AMERICA'S PLUNGING EDUCATION SURPLUS WILL DAMAGE YOUR PORTFOLIO), (UUP)

Stock markets are only in the business of discounting what happens next. I spend so much time anticipating the coming moves in shares that I can't even remember what I had for breakfast.

This is why technical analysis is such a bust as an investment strategy, except on an intraday basis only, as it is entirely founded on historical data. It is 100% backward looking.

So, I'll take you through the same thought experiments that convinced me to adopt a much more aggressive stance toward the markets after spending two months hiding in the weeds.

What happens after stocks hit new highs? They hit new lows, as they did on April 1, when the Dow Average plunged to 23,600.

What happens after markets hit new lows? They hit new highs again, supported by the strongest earning reports in history, which begin on Friday, April 13.

What happens after the inflation scare we received in the January Nonfarm Payroll Report with the surprise pop in average hourly earnings?

Inflation non-events, which unfolded with average hourly wages that came in subdued with the February and March Nonfarm Payroll Reports.

What follows a trade war? Trade peace, which is yet to come, but will arrive eventually nevertheless.

All of this points to stock markets that are in the process of putting in the lows for 2018. That means it is time to start ramping up your risk, as I did with three rapid Trade Alerts yesterday.

What does this look like on the charts? Alphabet (GOOGL) is a perfect example, which is in the process of putting in a very convincing triple bottom around the $1,000 level, right around the 200-day moving average.

What if I'm wrong?

After all the trade war continues to inflame by the day, the algorithms are still running amok, and the president still has a Twitter account.

What did it today? The Congressional Budget Office forecast of $1 trillion deficits running indefinitely? Or the FBI raids on the offices of the president's personal lawyer?

Then markets will edge down to the next support levels, about 4% lower than the most recently visited bottom, or about 22,600 in the Dow Average.

So, it would seem that the really smart thing to do here is to build options positions that can take that 4% hit, and STILL expire at their maximum profit points.

And this is exactly what I have been doing for the past two weeks: piling on long positions in the best technology stocks, and adding to short positions in bonds.

For fans of LEAPS, long dated out-of-the-money option call spreads one year or more out, this is the best time this year to get involved.

I'll give you an example.

BUY one June 21, 2019 $1,000 call at $145.00

SELL one June 21, 2019 $1,050 call at $120.00

NET COST = $25.00

In the event that (GOOGL) closes over $1,050 on June 21, 2019, or up 3% from today's closing level, the profit on this position would amount to $25.00 from an initial cost of $25.00, or a 100% gain in 14 months.

The only catch is that if the recession comes sooner than expected, the value of this position falls to zero in 14 months.

If you go deeper out-of-the-money with your strike prices, the potential profit rises by a multiple.

You can generate this kind of astronomical return with any of the FANGs assuming no real movement of the stock in a year.

It looks pretty good to me.

You heard it here first.

Winter Is Ending

Global Market Comments

April 9, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE'S THE BIG CALL),

(JPM), (GOOGL), (GLD), (TLT), (VXX),

(HOW TO "SNOWBALL" YOUR FORTUNE WITH BENJAMIN FRANKLIN)

Well that tears it!

Flamethrowers! Yes, on the list of 125 products that China is imposing new 25% import duties are flamethrowers.

And I was so looking forward to getting a flamethrower of my own with which to singe lazy and errant stock analysts from whom we all are afflicted.

I guess I'll just have to buy American, which I already do with my cars (Teslas).

The real call here is that the NASDAQ has entered a well-defined trading range, from 6,600 to 7,600, where it will remain trapped for six months until the November midterm congressional elections. After that, we will rally 10% in year-end rally.

The deep in-the-money call spread strategy I employ is ideally suited to this kind of go-nowhere market. While other traders are tearing their hair out, you'll be raking in the money every month as if you've just been adopted by a new rich uncle.

The president, absolutely cacophonous about the riches created by a rising stock market, has developed lockjaw in a falling one.

The reason was provided by trade advisor Peter Navarro, who said quite simply that the markets were wrong in their belief that trade wars decimate share prices.

My half century of trading tells that markets are never wrong, only people are.

And while the chief architect of our China trade policy has never been there, I managed to find it in 1974. It's easy. You just head east.

Here are some harsh numbers to show you how quixotic the administration policies are. By imposing $25 billion in import duties to protect dying American industries, investors cut $3 trillion off of US stock market capitalization.

That is a 120:1 risk reward AGAINST us. That's NOT the kind of trade I'm used to strapping on.

I'm sure the Chinese are thinking, "How would you like to lose another $3 trillion?" "How about a recession and bear market?" and "See you $25 billion and raise you $50 billion!"

Here is a number that gets lost in translation of the $1 trillion in two-way trade between the US and China. Some 90% of the profits accrue to the US. It is an issue that officials in Beijing have been complaining to me about for decades, which essentially makes them the low-waged manufacturing colony.

That iPhone X that Foxconn makes for $100 Apple (AAPL) sells for $1,000 in the US.

One then has to ask the cogent question, "If you're winning the game, why change the rules?"

The Chinese are not a nation you want to antagonize. They endured 2 million casualties in Korea just to inflict 50,000 on us. Chosin Reservoir looms large in my family - the best fighting retreat in history carried out by the Marine Corp.

The Chinese can also suffer more pain than Americans, with most only one or two generations out of a $300 annual per capita income.

Will the US November congressional election affect economic fundamentals" I doubt it. The mere fact that the election is out of the way is worth a 10% stock market rally into year-end.

The March Nonfarm Payroll Report was a disappointment for the second month in a row, coming in at a feeble 103,000. The headline unemployment rate remains at a decade low of 4.1%.

The stock market didn't care, with the overwhelming focus now on trade issues.

The really important numbers now, Average Hourly Earnings, were up a slightly inflationary 0.3%, but no one noticed.

The January and February reports we revised downward by a steep 50,000.

Manufacturing gained 22,000 jobs, Health Care was up 22,000, and Professional and Business Services up 33,000. Construction lost 15,000 jobs, thanks to raising interest rates.

The Broader U-6 "Discouraged Worker" unemployment rate dropped 0.2% to 8.0%, a new decade low.

As a stand-alone number, the report is not important. However, look at it in the context of a rising tide of recent, slightly negative economic data reports and one has to start to get concerned. Is it the weather, or the beginning of something larger?

We are only a week off from when the Q1, 2018 earnings season kicks off, which will probably deliver some of the strongest reports in US history.

Until then, the data reports will be relatively benign.

On Monday, April 9, nothing of note is announced.

On Tuesday, April 10, we receive March NFIB Small Business Optimism Index.

On Wednesday, April 11, at 8:30 AM EST, we learn the all-important Consumer Price Index, the most important read on inflation. Bed Bath & Beyond (BBBY) reports.

Thursday, April 12, leads with the Weekly Jobless Claims at 8:30 AM EST, which saw a dramatic rise of 24,000 last week (another bad number). BlackRock (BLK) reports.

On Friday, April 13, at 10:00 AM EST, we get the JOLTS Report on private sector job openings. It is the big day for bank earnings, with Citigroup (C), JP Morgan (JPM), and Wells Fargo (WFC) all reporting.

The week ends as usual with the Baker Hughes Rig Count at 1:00 PM EST. Last week brought a drop of 2.

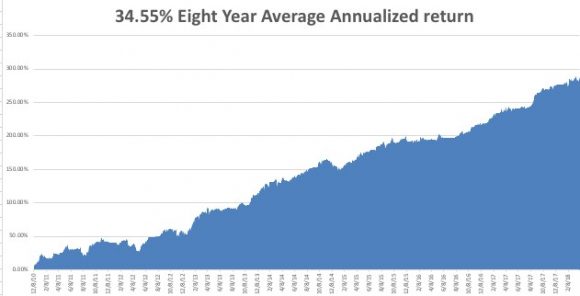

Followers of the Mad Hedge Trade Alert Service enjoyed one of their best weeks in years. Executing on the views above, I nailed the market bottom, hauling in an eye-popping 5.06% in performance in a single day.

I artfully used the huge sell-off days to pile on long positions in Google (GOOGL) and JP Morgan (JPM), and sell short US Treasury bonds and volatility (VXX). On the up days I bought gold (GLD).

It all worked like a charm, and every position is now profitable.

That brings April up to a +4.76% profit, my trailing one-year return to +49.72%, and my eight-year average annualized return up to 34.55%. We are an eyelash short of a new all-time performance high.

As for me, I'll be shutting down my Lake Tahoe estate for a while, not that the snow has turned to rain. The lake level is at a 118-year high, and Reno, NV, is worried about flooding. All the floodgates are open.

What a winter! I barely had time to tear myself away from my screens to visit the slopes.

Good Luck and Good Trading.

Global Market Comments

April 6, 2018

Fiat Lux

Featured Trade:

(FRIDAY, JUNE 15, DENVER, CO, GLOBAL STRATEGY LUNCHEON)

(DON'T MISS THE APRIL 11 GLOBAL STRATEGY WEBINAR),

(A NOTE ON OPTIONS CALLED AWAY),

(TLT), (GOOGL), (JPM), (VXX)

Mad Hedge Technology Letter

April 5, 2018

Fiat Lux

Featured Trade:

(GOOGLE IS FIRING ON ALL CYLINDERS ... BUY THE DIP),

(GOOGL), (FB), (AMZN), (AAPL), (MSFT)