Mad Hedge Biotech & Healthcare Letter

March 31, 2020

Fiat Lux

Featured Trade:

(MORE PLAYERS ENTER THE RACE FOR A CORONA CURE)

(MRNA), (ARCT), (JNJ), (SNY), (GOVX), (ALT), (NVAX), (GSK), (GNBT), (VXL.V), (INO), (APDN), (CADILAHC)

Mad Hedge Biotech & Healthcare Letter

March 31, 2020

Fiat Lux

Featured Trade:

(MORE PLAYERS ENTER THE RACE FOR A CORONA CURE)

(MRNA), (ARCT), (JNJ), (SNY), (GOVX), (ALT), (NVAX), (GSK), (GNBT), (VXL.V), (INO), (APDN), (CADILAHC)

Special issue on COVID-19 vaccines: Moderna Inc (MRNA), Arcturus (ARCT), Johnson & Johnson (JNJ), Sanofi (SNY), GeoVax (GOVX), Altimmune (ALT), Novavax (NVAX), GlaxoSmithKline (GSK), Generex (GNBT), Vaxil Bio (VXL.V), Inovio Pharmaceuticals (INO), Applied DNA Sciences (APDN), Zydus Cadila (CADILAHC)

The hunt is definitely underway for potential treatments to fight COVID-19 but coming up with vaccines will take a much longer time.

Since we already have the genetic code of the novel coronavirus (click here for the link), researchers can now use the complete blueprint to come up with ways to defeat this disease.

With code in hand, it takes a supercomputer just three hours to create model vaccines. Then it is just a question of how fast you can make them, if at all. Many proposed models are far beyond our existing technology.

To date, there are roughly 35 companies and academic organizations actively seeking ways to come up with a COVID-19 vaccine. While the process will still take time, there are several promising prospects.

Among the companies working on this, Moderna Inc (MRNA) has been recognized as the first biotechnology company to conduct human trials to test its COVID-19 vaccine in March. The trial includes 45 males and non-pregnant females aged 18 to 55.

Moderna’s vaccine utilizes the genetic sequence of the novel coronavirus. Basically, the goal is to build a vaccine out of messenger RNA.

Aside from Moderna, another biotech company called Curevac has been at the forefront of this cutting-edge technology.

In China, RNACure Biopharma has been working with Fudan University and Shanghai JiaoTong University on using the same technique to come up with a vaccine as well.

China’s CDC along with Tongji University and Stermina as well as Duke-NUS in partnership with Arcturus (ARCT) are also using a similar approach.

Although Moderna’s vaccine reached Phase 1 in record time, authorities cautioned that the development time frame is somewhere between 12 and 18 months — and this is even dubbed as an “overly optimistic” timeline.

Meanwhile, there are companies like Sanofi Pasteur (SNY) elected to use previously deployed vaccine platforms in earlier epidemics like SARS.

Johnson & Johnson (JNJ) also decided to employ the same strategy using its Ebola vaccine platform. In fact, JNJ shared that it’ll be ready to conduct human testing of its non-replicating viral vector by November.

Aside from JNJ, another biotechnology company in China called CanSino Biologics (HKG: 6185) in collaboration with the Academy of Military Medical Sciences is utilizing the same technology.

Just last week, Chinese authorities approved CanSino’s Phase 1 clinical trials.

Apart from JNJ and CanSino, other biotechnology companies are also working on a vaccine using the same non-replicating viral vector technology.

The list includes Wuhan’s BravoVax along with GeoVax (GOVX), Altimmune (ALT), Vaxart (VXRT), Greffex, and the University of Oxford.

Another strategy is employed by Novavax (NVAX), which is to construct a “recombinant” vaccine.

In a nutshell, this strategy entails extraction of the genetic code for the protein found on the Sars-CoV-2. This is a part of the virus that can trigger the immune system. This will then be pasted into the genome of a bacterium or yeast.

In effect, this vaccine will force the microorganisms to produce huge quantities of the protein to be able to fight off the virus.

Big biotechnology companies like Sanofi and GlaxoSmithKline (GSK) are following the same technique.

Smaller firms are also in on the action including Generex Biotechnology Corporation (GNBT), Vaxil Bio (VXL.V), EpiVax, and Clover Biopharmaceuticals.

The University of Georgia, Baylor College of Medicine, and the University of Miami are pursuing the same lead as well.

On top of these, several biotechnology companies use a DNA-based approach to come up with a vaccine.

Last March 12, the Bill & Melinda Gates Foundation provided a $5 million grant to Pennsylvania-based biotech firm Inovio Pharmaceuticals (INO) to help the company speed up the tests needed for its DNA vaccine called INO-4800.

This is on top of the roughly $9 million in funding it received from the Coalition for Epidemic Preparedness Innovations earlier.

At the moment, INO-4800 is in preclinical studies with plans to push it to Phase 1 clinical trials by April.

Aside from Inovio, Applied DNA Sciences (APDN), Zydus Cadila (CADILAHC), Takis, and Evivax are also pursuing the same strategy.

Despite implementing the most effective and even draconian measures to contain COVID-19, these tactics only managed to slow down the spread of the virus.

With the World Health Organization tagging this situation as a pandemic, everyone has become more desperate in the search for a vaccine because only a vaccine can stop people from getting sick.

However, even the unprecedented speeds afforded, the biotechnology companies couldn’t change the fact that developing a vaccine requires at least a year. It’s crucial to not make mistakes along the way especially since the product could potentially be injected into most of the world’s population.

After all, there’s only a single thing that can be considered worse than a bad virus — and that is a bad vaccine.

Mad Hedge Biotech & Healthcare Letter

December 17, 2019

Fiat Lux

Featured Trade:

(WHY THE M&A BOOM WILL SPILL INTO 2020),

(BMY), (CELG), (NOVN), (LOXO), (ROG), (ONCE), (MRK), (SAN), (ARQL), (THOR), (AMRN), (GSK), (AMGN), (GILD)

The biotech industry is breaking out, with the sector witnessing tremendous growth in the later part of 2019. With the stocks surging, it looks like the new year is setting up to a strong start that could continue well up into 2020.

Despite the anxiety over the feared government price controls in the drug sector, the early thinking in the biotech world remains optimistic. In fact, the stage seems to be set for even bigger news come 2020. This prediction comes on the heels of the over $7 billion deals closed just this summer alone.

To date, approximately $100 billion total potential value of research and development have been spent by biotech companies since June 2019, with $11 billion paid upfront in cash.

Among those deals, the biggest so far is Bristol-Myers Squibb’s (BMY) $74 billion acquisition of Celgene (CELG). Another massive agreement is Novartis AG’s (NOVN) $9.7 billion acquisition of The Medicines Company (MDCO).

Eli Lilly and Co’s (LLY) $8 billion takeover of rare genetic mutation drug Vitakvi creator, Loxo Oncology (LOXO), also signified notable movements in the industry along with Johnson and Johnson’s (JNJ) $5.8 billion buyout of robotic surgery company Auris Health. Even Roche Holding AG (ROG) is expected to complete its $4.3 billion merger with gene therapy company Spark Therapeutics (ONCE) before the year ends.

Not far behind are Merck and Co’s (MRK) $2.7 billion acquisition of ArQule (ARQL) as well as Sanofi SA’s (SAN) $2.5 billion buyout of clinical-stage DNA base pair treatment company Synthorx Inc (THOR).

The majority of the deals were in the oncology space, with three times as many oncology deals made compared to the number two sector, the neurology sector. To put things in perspective, seven of the top 10 deals made in 2019 involved oncology treatments.

What can we expect in 2020?

A number of drug candidates remain in the pipeline, but one mid-cap biotech company is anticipated to make big bucks next year. The catch? It’ll need the help of a bigger and more established company to make it happen. That is, this promising company has become the most eligible buyout candidate for 2020.

Amarin Corporation (AMRN) has taken center stage when it became the first-ever company to hit positive results for its prescription omega-3 treatment, Vascepa -- a feat that none of the other biotech giants managed to accomplish. Actually, competitor GlaxoSmithKline (GSK) created its own omega-3 treatment, Lovaza, only to have it fail to reach its goal.

Barring any major setback, Vascepa is slated as the next blockbuster treatment in the cardiovascular disease space -- possibly even displacing Pfizer’s (PFE) Lipitor as the king of this segment. In fact, several major healthcare groups like the American Heart Association, American Diabetes Association, the European Society of Cardiology have already endorsed Vascepa as an effective treatment for LDL cholesterol.

The Amarin medication is projected to peak at $4 billion in annual revenues by 2028. Considering that its manufacturer’s reported third-quarter earnings this 2019 is only at $112.4 million, the approval of Vascepa will undoubtedly be a game-changer for its investors.

However, Vascepa’s incredible potential along with the fact that Amarin has no other drug candidate in its pipeline makes the company ripe for a takeover. For one, it’s not financially capable of juggling both the marketing of Vascepa and developing or building a solid pipeline to support its growth. With the omega-3 treatment’s projected blockbuster status, a bigger and more established company could undoubtedly be more fit to help it reach its potential.

Who are the potential suitors?

Three heavyweights have been repeatedly linked to Amarin: Pfizer, Novartis, and Amgen (AMGN). Since all three have a budding cardiovascular unit, it could be anyone’s game.

However, Novartis’ recent acquisition of The Medicines Company makes it the least likely candidate in the list right now. After all, the latter already has a potential blockbuster cholesterol-lowering drug in Inclisiran.

That paves the way for a new suitor in the form of Gilead Sciences (GILD). Just a few weeks ago, Gilead added Vascepa to one of its ongoing trials involving nonalcoholic steatohepatitis. Whether or not this signifies interest in buying out Amarin is anybody’s guess.

Heading into the next year, the biotech sector is expected to welcome the new year with strong fundamentals and great opportunities for outperformance. While the election may bring changes to policies, the ongoing growth and innovation in this industry make it impossible to be excited for what’s in store for the future.

After all, more and more life-extending and even life-saving treatments are getting discovered by the day. Aside from following the developments in the industry, why not use your knowledge to fatten your pocketbook along the way?

Mad Hedge Biotech & Healthcare Letter

October 8, 2019

Fiat Lux

Featured Trade:

(GET ON THE CELGENE BANDWAGON),

(CELG), (BMY), (GSK), (AMGN), (RHHBY), (ROG), (GMAB), (MOR)

If you’re looking for a biotech stock that just relentlessly grinds up every day, Celgene Corporation (CELG) has to be at the top of your list, one of the most dominant players in the industry today.

Thanks to its $74 billion merger with Bristol-Myers Squibb (BMY), the combined companies are expected to push out Amgen in the top spot by 2020. Perhaps a positive indicator that things are looking up is the 50.9% rise in Celgene stock this year.

While the deal with Bristol has been predictably riddled with setbacks and delays, the sale of blockbuster arthritis drug Otezla to Amgen last month over antitrust concerns has finally pushed the merger forward.

While waiting for the merger with (BMY) to be finalized by the end of 2019, Celgene has been busy coming up with ways to attract more investors.

One of the exciting efforts of the biotech giant is its recent collaboration with Immatics Biotechnologies. Celgene joins GlaxoSmithKline (GSK) in the T-cell treatment market. With these two behemoths providing resources for this field, researchers are hopeful that a breakthrough drug will be discovered soon.

This partnership with Immatics saw Celgene shell out $75 million to gain access to three of the smaller firm’s anti-cancer adoptive cell therapies. With Immatics’ focus on T-cell treatments, the collaboration with Immatics will provide Celgene a wider pool of candidates for their solid tumor programs.

Aside from the $75 million upfront payment, Immatics will also receive $505 million in milestone payments for every licensed drug if Celgene decides to exercise the option. That means Celgene will have the opportunity to pay for the full or partial rights on selected assets developed from the T-cell therapies.

Ideally, Immatics would earn over $1.5 billion from the collaboration plus tiered royalties on net profits. As for Celgene, the biotech company will share the rewards with Bristol-Myers.

This collaboration marks the biggest upfront payment received by Immatics since its creation in 2000. The company, which is a spinoff of Germany’s University of Tübingen, adds Celgene to its growing number of partners including Amgen (AMGN), Roche Holding Ltd.(RHHBY), Genussscheine (ROG), Genmab (GMAB), and Morphosys (MOR).

The Munich company’s work on adoptive cell treatments and bispecific antibodies also generated interest from the cancer center of the University of Texas.

Since its creation, Immatics has managed to raise $220 million in venture capital plus roughly $130 million in non-dilutive funding. The Celgene deal puts the company’s total capital at $420 million.

So far, Celgene has reported three quarters of consistently accelerating earnings per share increase and a quarter of notable sales growth. However, the Bristol-Myers deal has yet to be completed. More importantly, some blockbuster products face uncertain futures due to rival copycats.

One major factor contributing to the doubts surrounding the company’s future is the recent sale of Otezla. Since this drug has been Celgene’s major moneymaker for years, it remains to be seen how the company will cope with its loss.

Aside from Otezla, another Celgene blockbuster facing pressure is blood cancer treatment Revlimid. While the multiple myeloma drug reported an 11.4% jump in its second quarter sales this year, the company has yet to fully safeguard it from the patent challenges aiming to end its reign in the market.

While the effects of the Immatics collaboration and the recent developments on the Bristol-Myers merger have yet to concretely manifest themselves, Celgene is expected to display strength when the next earnings release of 2019 draws nearer.

In the third quarter report, the company is projected to post an earnings per share of $2.73. This would indicate a 19.21% year-over-year increase. Meanwhile, its earnings per share for the full year of 2019 is expected to rise by over 23% to reach $10.91. As for its revenue, Celgene is estimated to earn $17.44 billion this year, marking a 14.11% rise from 2018.

In terms of its merger with Bristol-Myers, the two pharmaceutical giants are anticipated to have a combined total of 10 drugs already in the late-stage testing phase and six drugs ready to be released soon.

Additionally, the companies disclosed that they have roughly 50 drugs slated for early and mid-stage testing. Among those, 21 are reported to be focused on oncology treatments.

Buy Celgene on the next 5% dip in the shares. It seems to be on a tear.

Mad Hedge Biotech & Healthcare Letter

October 1, 2019

Fiat Lux

Featured Trade:

(THE PLAYERS GUIDE TO BIOTECH INVESTING)

(AMGN), (PFE), (NOVN), (ABBV), (ABT),

(AGN), (ROG), (GSK), (CELG), (JNJ), (BMY)

You can’t watch a game without a program, and the lineup for biotech and healthcare is truly astonishing. No surprise then that the fields account for more or less than 17% of US GPD.

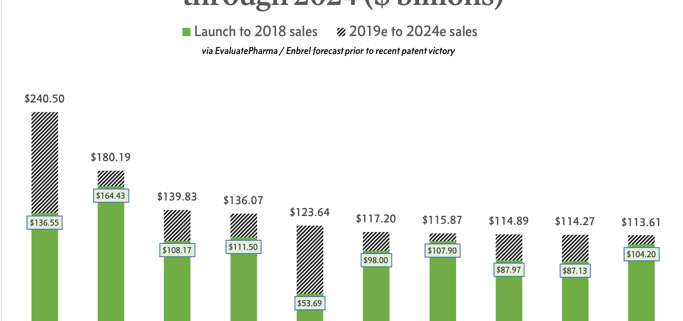

Here is a listing of the biggest $100 billion plus products you have never heard of. The good news is that you have just stumbled across a sector that will generate no less than a staggering $1.4 trillion in sales over the next five years.

That means it’s certainly worth your time getting to know this field. With this amount at stake, it’s no wonder companies manufacturing these blockbuster drugs are sparing no expense to fight off patent vultures.

A good example is Amgen (AMGN), which recently won its case to extend the patent life of rheumatoid arthritis biological Enbrel against Novartis AG’s (NOVN) biosimilar arm Sandoz. Since each extra hour added to patent life means millions of dollars (and sometimes billions) in sales, the additional 10 years of exclusivity for Enbrel is a massive victory for Amgen.

In a recent study released by Evaluate Pharma, Enbrel was ranked third in the top 10 biggest sellers up to 2024. The forward-looking consensus projection anticipates Amgen’s golden goose to hit roughly $140 billion in total revenues in five years – a truly impressive performance particularly for a drug that has been around for more than 20 years. However, Enbrel’s longevity pales in comparison to the other behemoths in the biopharma realm.

Up until 2018, Pfizer’s (PFE) Lipitor held the title of earning the highest lifetime sales in the industry. Since its launch in 1997, the cholesterol drug has raked in $164.4 billion in revenues so far with the number estimated to reach $180 billion by 2024. Lipitor’s success is highlighted more by the fact that it's under a small molecule status and holds approval for a very narrow indication.

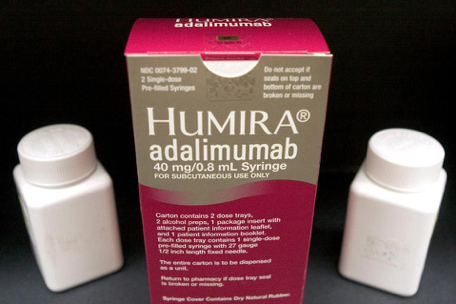

Overtaking Lipitor to take the top spot is AbbVie’s (ABBV) rheumatoid arthritis treatment Humira, which closed with $20 billion in sales in 2018 alone. While some AbbVie investors frown upon the over-reliance of the company on Humira, it appears that the efforts to protect the drug has paid off big time.

With patent protection (132 approved patents!) safeguarding its exclusivity in the market, Humira is projected to reach a total of $240 billion in revenues by 2024. Clearly, the rewards they’ve been reaping show no signs of abating anytime soon.

More importantly, Humira’s robust sales, which makes up almost 70% of the company’s profits, has provided AbbVie with the financial capacity to finally get out of the shadow of parent company Abbott Laboratories (ABT) and come up with its own pipeline. As it happens, AbbVie’s efforts towards this direction have already started with the massive purchase of Allergan (AGN) for $63 billion this year.

Apart from Lipitor, Humira, and Enbrel, there are three more blockbuster products with sales that hit the $100 billion mark as of 2018 -- a figure that would make Ecuador proud to claim as their annual GDP. These are Roche Holding Ltd. Genussscheine’s (ROG) chemotherapy drug Rituxan, Amgen’s anemia treatment Epogen, and GlaxoSmithKline’s (GSK) asthma medication Advair.

One biopharma bestseller that leapfrogged a lot of other drugs in the market is multiple myeloma medication Revlimid -- aka the drug that built Celgene (CELG). With an entry date of 2008, this drug is the newest one on the list. While Revlimid’s sales are impressive, what’s actually quite exciting is the fact that its projected revenues easily outstrip its already notable sales of $53.69 billion.

By 2024, this Celgene blockbuster is estimated to reach $123.64 billion in sales. There’s a caveat to this though as Revlimid’s success in the years to come is dependent on how Celgene plans to deal with generic competition chomping at the bit and ready to attack once the drug reaches its 2022 patent expiration date.

Another big-ticket drug that might see a bit of a decline in sales soon is from Johnson & Johnson (JNJ). While the company has always been aggressive when it comes to dominating the market for its Crohn's Disease drug Remicade, an investigation by the Federal Trade Commission (FTC) might put a damper on things soon. According to recent reports, JNJ has been suspected of contracting payers to ensure market control and stave off competitors.

Meanwhile, the three horsemen of Roche, namely, Rituxan, cancer and eye disease medication Avastin, and breast cancer treatment Herceptin, reached a collective amount of $365 billion in total sales. These three are anticipated to stay put on top of the industry in the next five years as well, thanks to their competitive pricing and aggressive strategies to protect their patents.

Rounding out the list is Amgen’s Epogen, which is expected to add $107.90 billion to the already astounding $115.87 billion it generated for the company. Meanwhile, GSK’s Advair, which brought in $113.61 billion, is expected to pour in an additional $104.20 billion by 2024.

Interestingly, the majority of the top 10 franchise drugs are biologics except for Sanofi’s (SAN) ulcer treatment Zantac, Bristol-Myers Squibb Co’s (BMY) heart medication Plavix, Advair, and of course, Lipitor. In fact, this is considered as the primary reason for their capability to fight off potential copycats for years.

In some cases, their monopoly of the market has allowed them to expand to include various other indications in their coverage. The massive sales of biologics are also rooted in their ability to demand big-ticket reimbursements. Unlike their generic competitors, brand recognition alone makes it more convenient for patients to ask for compensation.

Needless to say, the success stories of these drugs make it quite obvious why these biopharma companies employ a battalion of legal experts to fend off the rise of generics. While the onslaught of biosimilars cannot be helped, these lawyers ensure that patients opting for these versions of the medication would find it incredibly difficult to ask for biosimilar reimbursements.

Global Market Comments

June 12, 2019

Fiat Lux

Featured Trade:

(MONDAY, JUNE 24 MELBOURNE, AUSTRALIA STRATEGY LUNCHEON)

(AMGEN’S BIG LUNG CANCER BREAKTHROUGH),

(AMGN), (GSK), (MRTX)

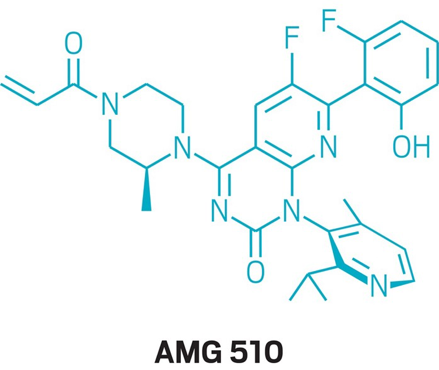

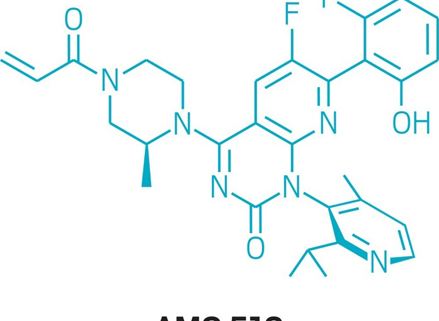

I recently heard that some of my hedge fund friends were loading up on Amgen (AMGN) and now I know why. It’s a company I know well because my UCLA biochemistry professor was its first chairman.

Amgen has accomplished a major medical breakthrough. The company has revealed that its experimental drug, AMG 510, exhibited the ability to significantly shrink the size of tumors by 50%. The results were obtained from early-stage trials performed on advanced lung cancer patients.

In a nutshell, AMG 510 could become the first-ever approved treatment that can target a mutated gene called KRAS which is one of the most common mutations involved in non-small cell lung cancer (NSCLC). The American Cancer Society identified NSCLC as the leading cause of cancer death, accounting for a stunning 85% of lung cancers.

For decades, researchers have been searching for ways to address KRAS mutations, with the sought-after solution dubbed as the "the great white whale of drug discovery." With the first proof-of-concept presented a mere six years ago, the rapid development of Amgen’s new drug has impressed researchers in the field.

Simply put, this drug will be a game changer for particular types of cancer. Subsequently, its success would mean massive profits for Amgen shareholders.

The announcement of AMG 510’s promising results saw a jump in Amgen shares of 6.1% delivering a new two-year high. While this product remains in its initial phase, the fact that this cancer drug addresses a vital unmet need in oncology makes it a prime candidate in becoming the next blockbuster drug for Amgen.

Aside from lung cancer, this drug is also aimed at providing treatment for colorectal cancer and nearly uncurable pancreatic cancer (of which Steve Jobs died). To date, AMG 510 sales are estimated to initially reach more than $1 billion a year and peak at $2 billion.

With the extremely massive market for this particular drug, it comes as no surprise that Amgen is not alone in the race.

So far, two more biopharma companies are looking to develop similar medications: GlaxoSmithKline Plc (GSK) and Mirati Therapeutics (MRTX). While the former has yet to reveal the covalent inhibitor drug it’s currently developing, reports indicate that Mirati’s work involves a drug called MRTX849. Aside from these, no other information has been released by the two companies.

While these are encouraging results vis-à-vis its oncology department, how is Amgen doing so far this year with the rest of its business?

Based on its earnings report in the first quarter of 2019, Amgen recorded $5.6 billion in total revenues. This matches the amount the company reported during the same quarter in 2018. Despite the promising projects in its pipeline, Amgen’s product sales saw a 1% dip globally.

However, its new products showed double-digit increases in the first quarter. Osteoporosis and hypercalcemia drug Prolia reported a 20% increase while cardiovascular medication Repatha also showed a 15% revenue jump during the first quarter. Even the revenues for relapsed multiple myeloma treatment Kyprolis showed a 10% rise in this period.

As for its earnings per share (EPS), Amgen is coming in at $12.53. This indicates an EPS growth of 14.8% this year, which could lead to a projected 5.25% EPS growth for 2020.

Meanwhile, Amgen’s positive outlook particularly with AMG 510 as an additional blockbuster drug in its portfolio prompted the company to adjust its earnings expectations for this year. In terms of its expected revenue, Amgen raised it from $21.8 billion to $22.9 billion range to $22 billion to $22.9 billion.