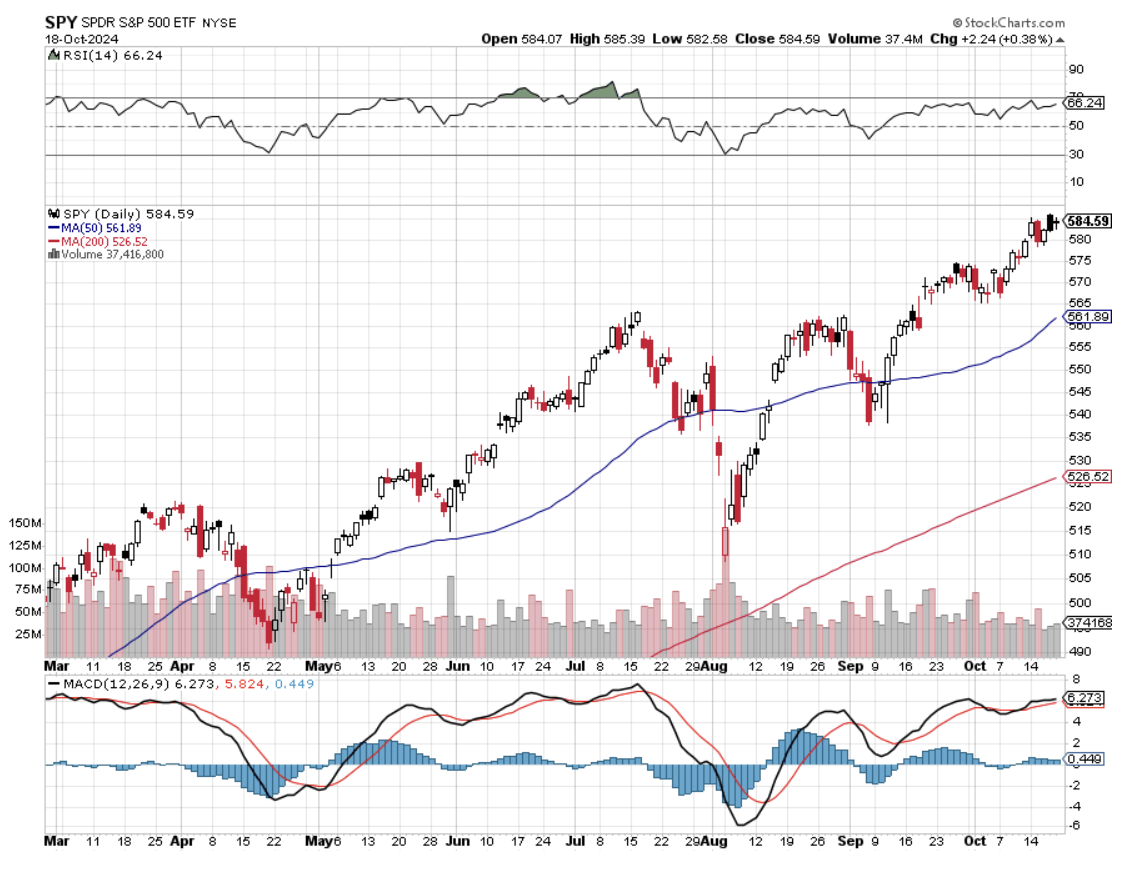

We are now nearly three months into an almost straight-up move in the stock market, and money managers everywhere are scratching their heads. We are now only 136 points or 2.32% from my yearend (SPX) target of 6,000, which is starting to look pretty conservative. The price-earnings multiple for the S&P 500 is now 21X, the Magnificent Seven 28X, and NVIDIA 65X.

I’ve seen all this before.

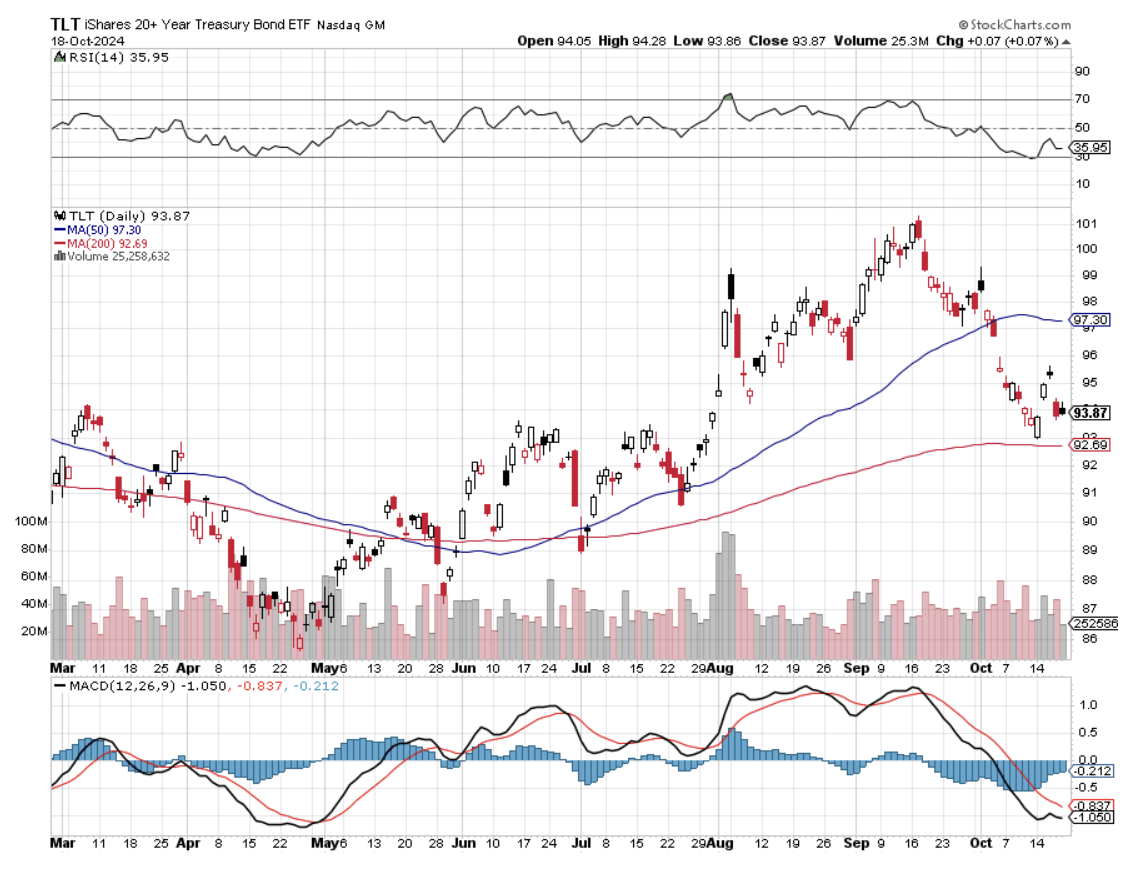

We are about as close to a perfect Goldilocks scenario as we can get. Interest rates and inflation are falling. A 3% GDP growth rate means the US has the strongest major economy and is the envy of the world. We have entered the euphoria stage of the current market move in almost all asset glasses. Gold (GLD) has gone up almost every day. Some big tech remains on fire. Energy prices are in free fall. Even bonds (TLT) are trying to put in a bottom.

Complacence is running rampant.

So, how the heck do we trade a market like this? You play the laggard trade.

The biggest risk to the gold trade is that it has gone up 40% in a year. So, what do you do? The response by traders has been to move into lagging silver (SLV) (AGQ), which has been on a tear since September.

Had enough with the Mag Seven? Then, rotate in the sub $1 trillion part of the market with Broadcom (AVGO), ASML Holdings NV (ASML), Micron Technology (MU), and Lam Research (LRCX).

Tired of watching your DH Horton (DHI) go up every day? Then, flip into smaller homebuilders like Pulte Homes (PHM) and Lennar (LEN).

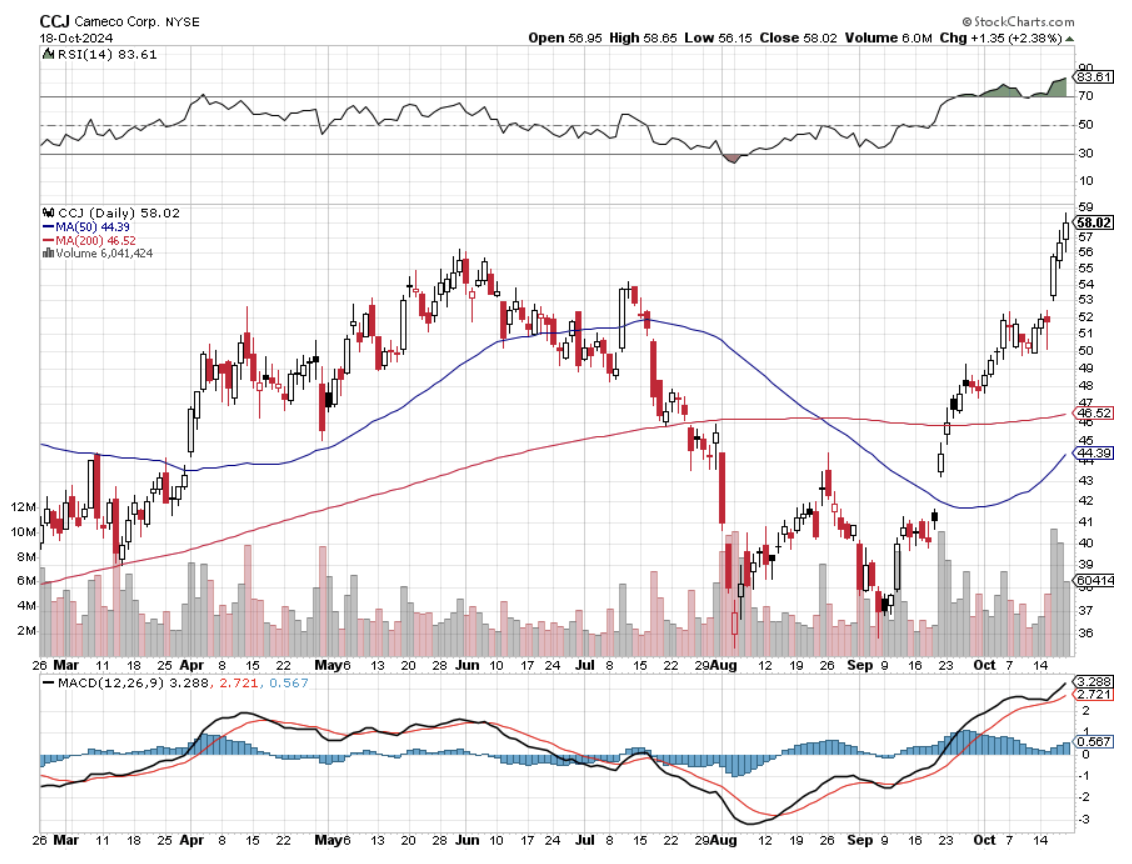

And then there is the biggest laggard of all, the nuclear trade, which is just crawling out of a 40-year penalty box. With news that Amazon (AMZN) was planning to order up to eight Small Modular Reactors to power its AI efforts, all uranium plays continue to go ballistic. The proliferation of power-hungry data centers is driving the greatest growth of power needs since WWII and the Manhattan Project.

Fortunately, I got in early. This is a trend that could become the next NVIDIA, as the public stocks involved are coming off such a low base. I have personally interviewed the founders and examined Nuscale’s plans with a fine tooth come and consider them genius. The company is, far and away, the overwhelming leader in the sector. The puzzle for the pros who understand the technology is why it took so long. Buy (CCJ), (VST), (CEG), (BWXT), and (OKLO) on dips.

It's like everything is racing towards a key, even with an unknown outcome. There happens to be a big one coming up: the US presidential elections on November 6.

Speaking of elections, I took the time to participate in the first day of voting in Nevada on Saturday, October 19, at the Incline Village Public Library. I waited in line for two hours in a brisk and breezy 40 degrees. I wore my Marine Corps cap and Ukraine Army ID just to confuse people. Some got so tired of waiting in the cold that they went home, retrieved their mail-in ballots, and returned to the polls to drop them off.

I looked back on the line, and women outnumbered the men by three to one. Where did all these women come from? There used to be such a shortage of women at Lake Tahoe that it was impossible to get a date. Hunting, fishing, long-distance backpacking, and skiing weren’t used to attract such large numbers of the female gender. Maybe now they do? But now they’re driving up in Mercedes AMG’s and Range Rovers.

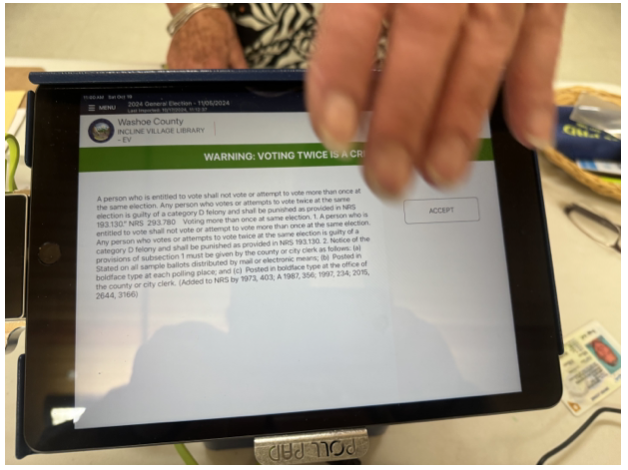

When I finally arrived at the front of the line, I was asked to sign an agreement with my finger, acknowledging that I knew it was illegal to vote twice. The poll worker noticed my ID. When I explained what it was in the Cyrillic alphabet, she burst into tears, apologized, and said she had goosebumps all over.

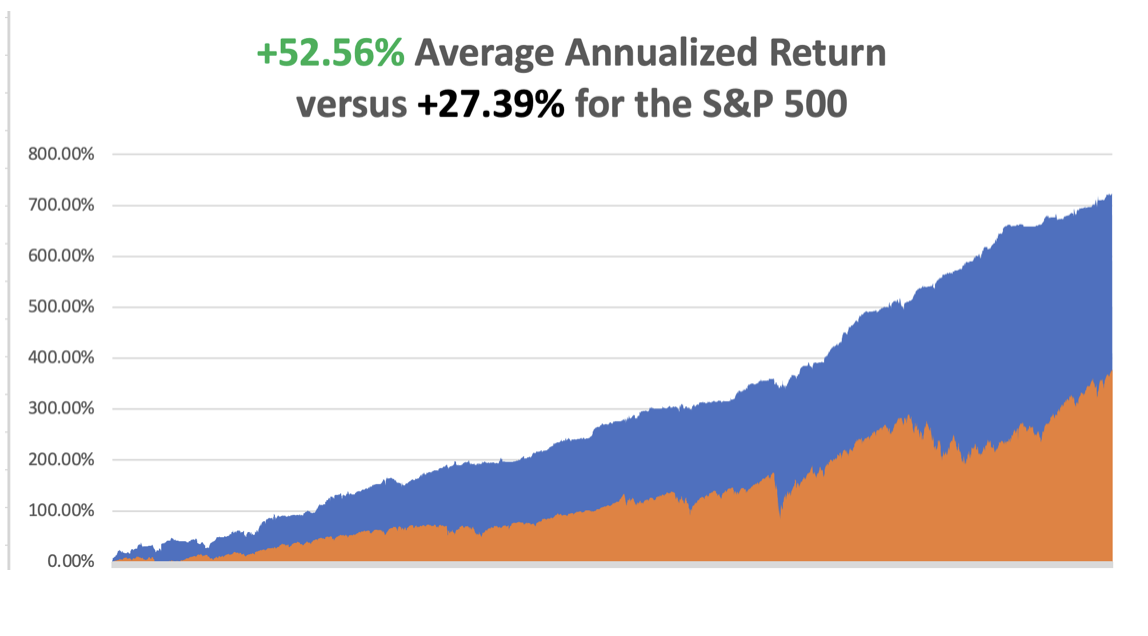

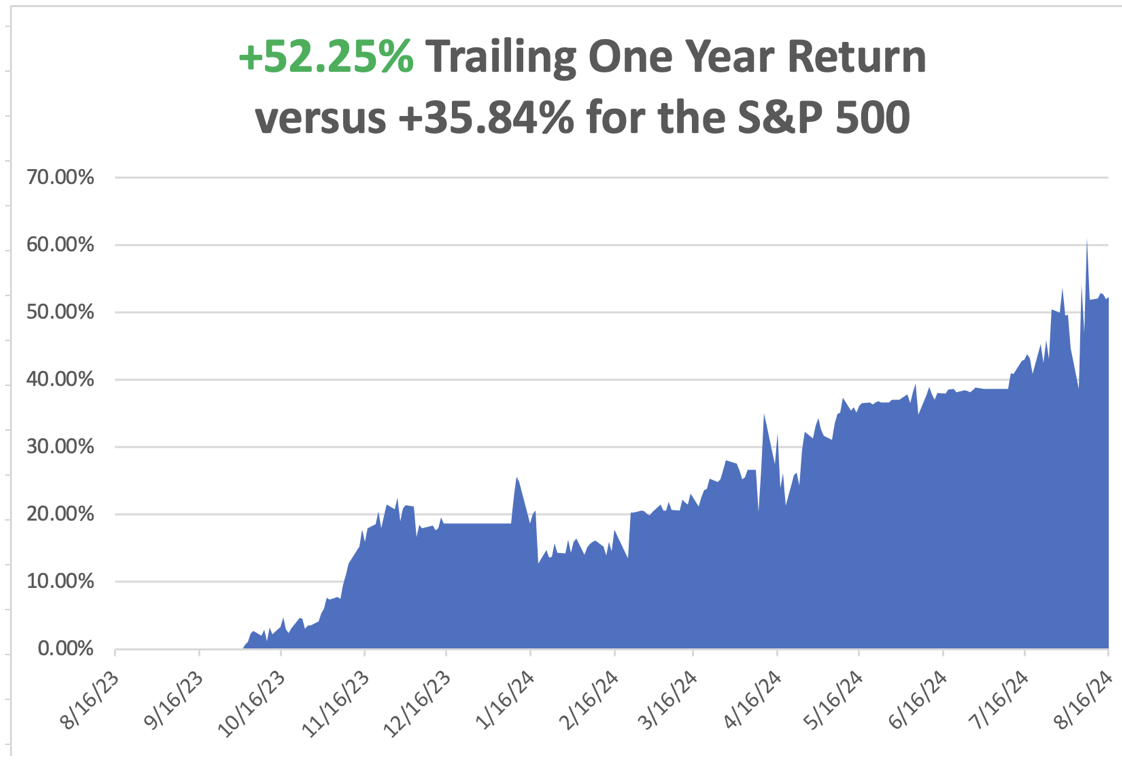

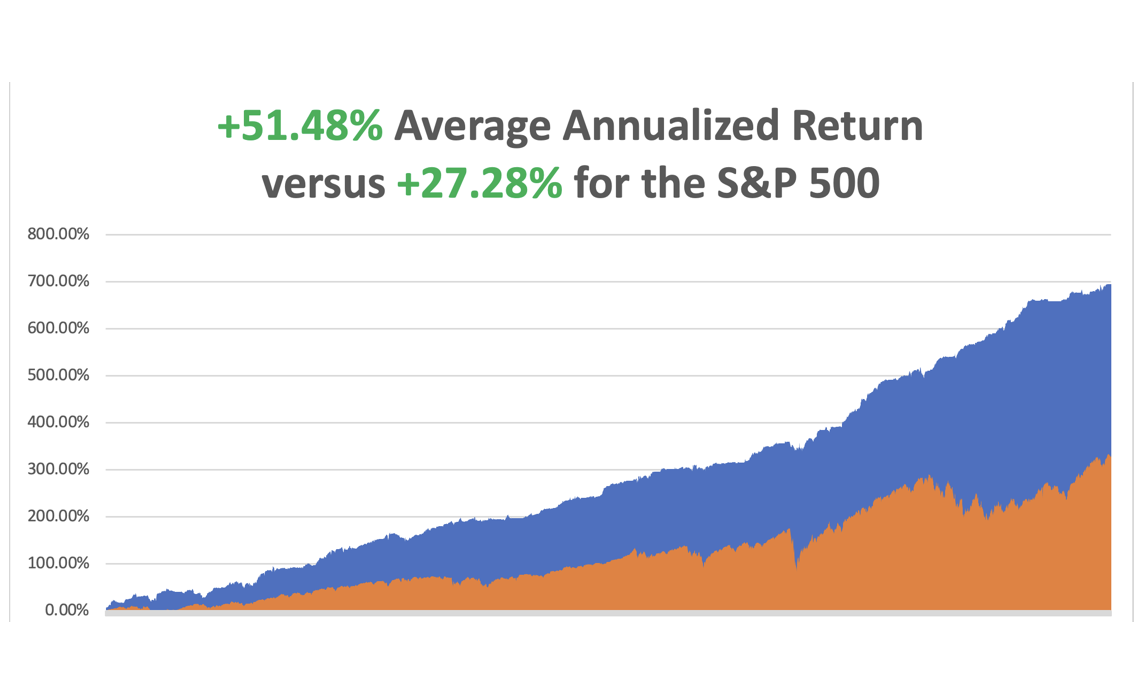

It was another blockbuster week, up over 6%. So far in October, we have gained +4.89%.My 2024 year-to-date performance is at +50.13%.The S&P 500 (SPY) is up +22.43%so far in 2024. My trailing one-year return reached a nosebleed +65.90. That brings my 16-year total return to +726.76%.My average annualized return has recovered to +52.56%.

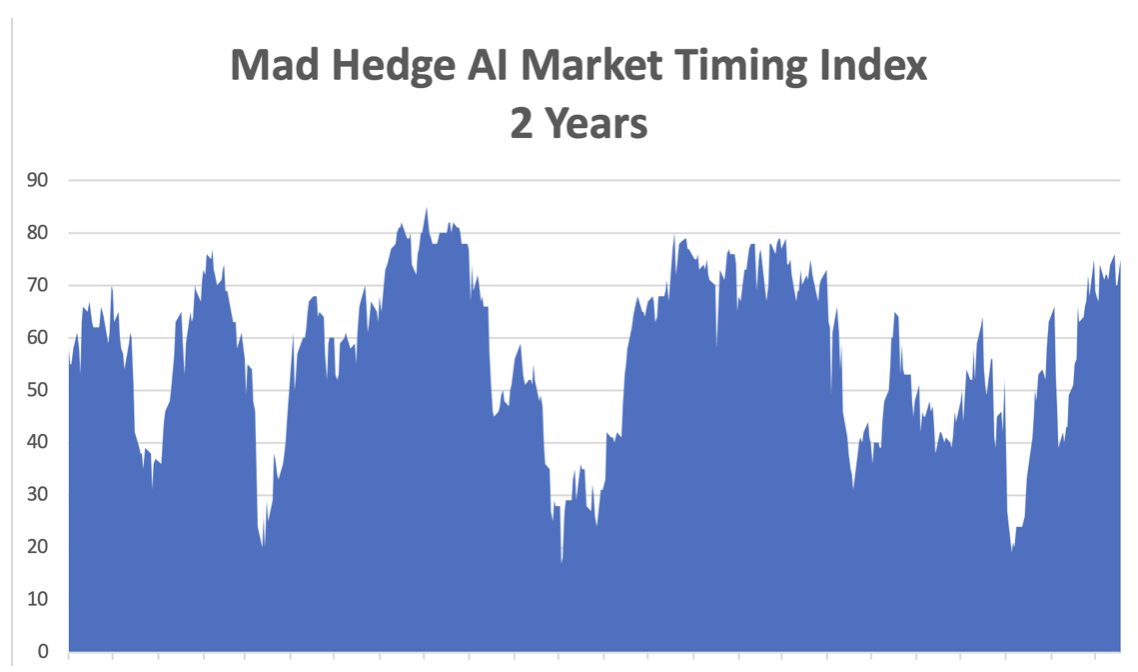

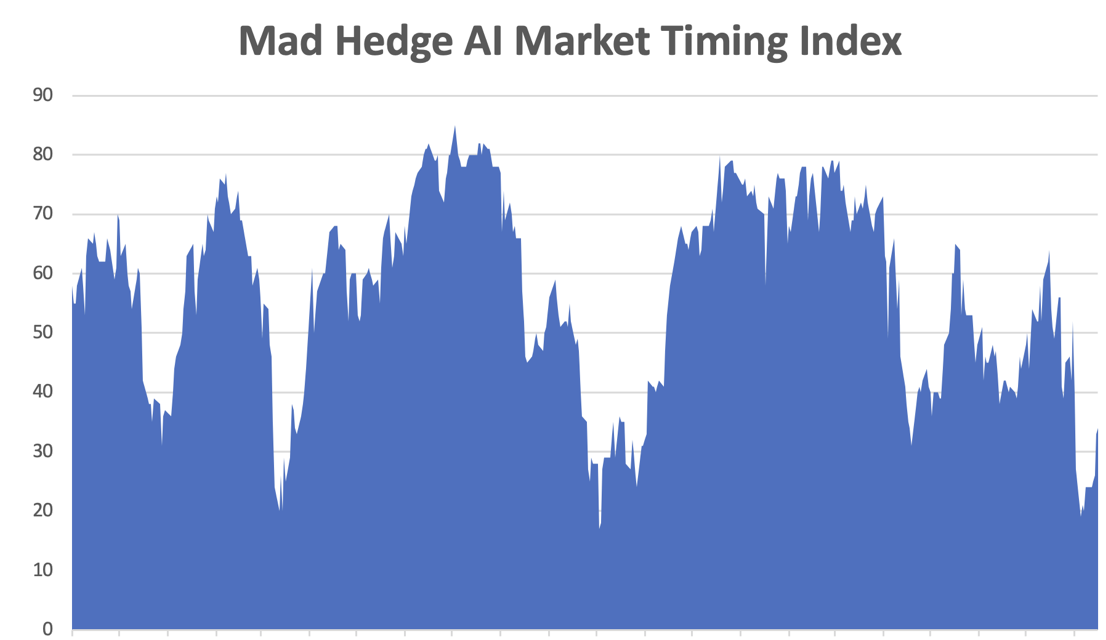

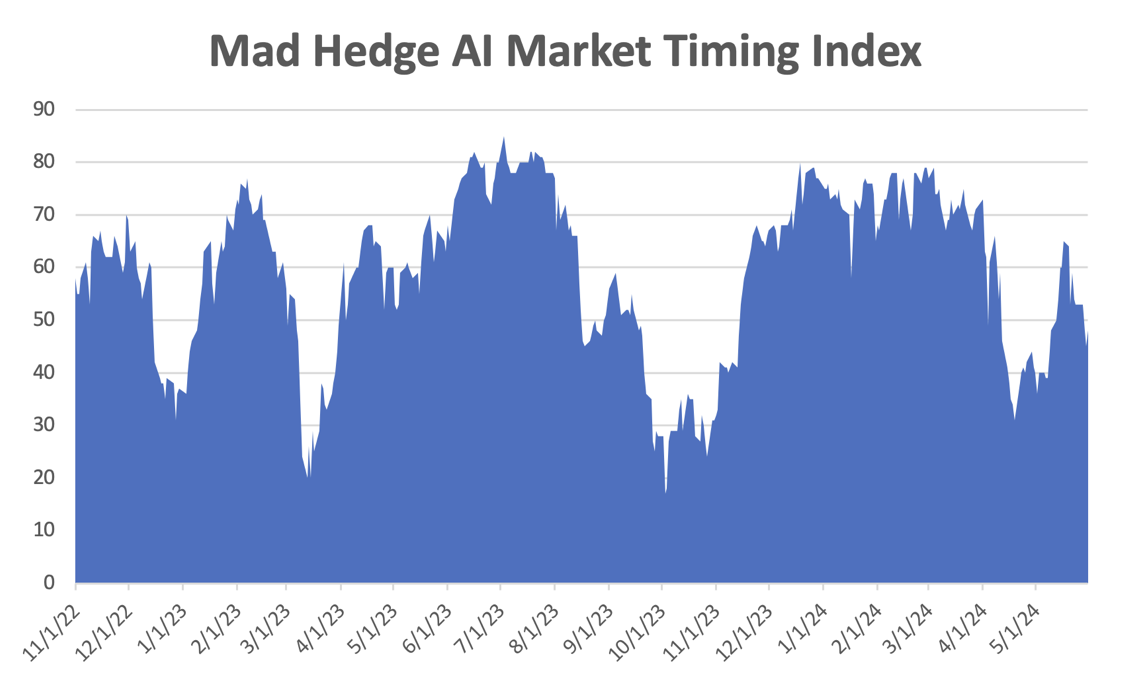

With my Mad Hedge Market Timing Index at the 70 handles for the first time in five months, I am remaining cautious with a 70% cash and 30% long. I look for a small profit in (TSLA) to reduce risk. Two of my positions expired at their maximum profit point for (NEM) and (DHI) on Friday, October 18 options expiration.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 60 of 80 trades have been profitable so far in 2024, and several of those losses were really break-even. Some 16 out of the last 19 trade alerts were profitable. That is a success rate of +75.00%.

Try beating that anywhere.

Risk Adjusted Basis

Current Capital at Risk

Risk On

(TSLA) 11/$165-$175 call spread 10.00%

(JPM) 11/$195-$205 call spread10.00%

(GLD) 11/230-$235 call spread 10.00%

Risk Off

NO POSITIONS 0.00%

Total Net Position 30.00%

Total Aggregate Position 30.00%

Netflix Soars on Blockbuster Earnings, up 11% at the opening on a 5 million gain in subscribers. The company posted earnings per share of $5.40 for the period ended Sept. 30, higher than the $5.12 LSEG consensus estimate.

Crucially, Netflix saw momentum in its ad-supported membership tier, which surged 35% quarter over quarter. The streaming wars are over, and (NFLX) won. Buy (NFLX) on dips.

Silver is Ready to Break Out to the Upside after a year-long-range trade. The white metal is a predictor of a healthy recovery and a solar rebound. It’s a long overdue catch-up with (GLD). Buy (AGQ) on dips.

Apple China Sales Jump 20% on the new iPhone 16 launch. Both Apple and Huawei's (HWT.UL) latest smartphones went on sale in China on Sept. 20, underscoring intensifying competition in the world's biggest smartphone market, where the U.S. firm has been losing market share in recent quarters to domestic rivals. Buy (AAPL) on dips.

Taiwan Semiconductor Soars on Spectacular Earnings, dragging up the rest of the chip sector with it. The world's largest contract chipmaker raised its expectation for annual revenue growth and said sales from AI chips would account for mid-teen percentage of its full-year revenue. U.S.-listed TSMC shares rose nearly 9%, and if gains hold, the company's market capitalization would cross $1 trillion. Buy (NVDA) on dips.

Weekly Jobless Claims Fall. Initial claims for state unemployment benefits dropped 19,000 last week to a seasonally adjusted 241,000 for the week ended Oct. 12, the Labor Department said on Thursday. Economists polled by Reuters had forecast 260,000 claims for the latest week. Claims jumped to more than a one-year high in the prior week, attributed to Helene, which devastated Florida and large swathes of the U.S. Southeast in late September.

Morgan Stanley Announces Blowout Earnings, fueling a 32% profit jump for the third quarter. Revenue from the trading business rose 13%. That followed gains recorded by its biggest rivals as the market business lifted fortunes across the industry, and a steady rebound in investment banking fees increased dealmaking. The wealth unit generated revenue of $7.27 billion, higher than analysts’ expectations, with $64 billion in net new assets. The unit boosted its pretax margin to 28%, driven by growth in fee-based assets. Buy (MS) on dips.

Global EV Sales Up 30% in September, with the largest gains in China. Gains in the U.S. market have been lagging in anticipation of the Nov. 5 election. Chinese carmakers are seeking to grow their sales in the EU despite import duties of up to 45% and amid cooling global demand for electric cars. Chinese and European automakers were going head-to-head at the Paris Car Show on Monday. Buy (TSLA) on dips.

Dollar Hits Two Month High on rising US interest rates. Ten-year US Treasuries have risen from 3.55% to 4.12% since the September Nonfarm Payroll Report. A string of U.S. data has shown the economy to be resilient and slowing only modestly, while inflation in September rose slightly more than expected, leading traders to trim bets on large rate cuts from the Fed. Buy all foreign currencies on dips (FXA), (FXE), (FXB), (FXY).

S&P 500 Value Gain Hits $50 Trillion, since the 1982 bottom, which I remember well and is up 50X. The index hit a record high Wednesday and is trading Thursday at around 5770, up 21% so far in 2024. The index’s value is up sixfold since it stood at $8 trillion at year-end 2008, near the depth of the bear market during the financial crisis.

JP Morgan Delivers Blowout Earnings. Its stock, trading around $223, was on course for its biggest daily percentage gain in 1-1/2 years.

(JPM)'s investment-banking fees surged 31%, doubling guidance of 15% last month. Equities propelled trading revenue up 8%, exceeding an earlier 2% forecast. These earnings are consistent with the soft-landing narrative of modest U.S. economic growth. Buy (JPM) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy is decarbonizing, and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000, here we come!

On Monday, October 21 at 8:30 AM EST, nothing of note takes placeis out. On Tuesday, October 22 at 6:00 AM, the Richmond Fed Manufacturing Index is out.

On Wednesday, October 23 at 11:00 AM, the Existing Home Sales is printed.

On Thursday, October 24 at 8:30 AM, the Weekly Jobless Claims are announced. We also get New Homes Sales.

On Friday, October 25 at 8:30 AM, the US Durable Goods Orders are announced. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I am headed out for early voting in Nevada this morning. It’s been a year since I came back from Ukraine badly wounded, so I thought I would recall my recollections from that time.

You know you’re headed into a war zone the moment you board the train in Krakow, Poland. There are only women and children headed for Kiev, plus a few old men like me. Men of military age have been barred from leaving the country since the Russians Invaded. That leaves about 8 million to travel to Ukraine from Western Europe to visit spouses and loved ones.

After a 15-hour train ride, I arrived at Kiev’s magnificent Art Deco station. I was met by my translator and guide, Alicia, who escorted me to the city’s finest hotel, the Premier Palace on T. Shevchenka Blvd. The hotel, built in 1909, is an important historic site as it was where the Czarist general surrendered Kiev to the Bolsheviks in 1919. No one in the hotel could tell me what happened to the general afterward.

Staying in the best hotel in a city run by Oligarchs does have its distractions. Thanks to the war, occupancy was about 10%. That didn’t keep away four heavily armed bodyguards from the lobby 24/7. Breakfast was well populated by foreign arms merchants. And for some reason, there are always a lot of beautiful women hanging around with nothing to do.

The population is definitely getting war-weary. Nightly air raids across the country and constant bombings take their emotional toll. Kiev’s Metro system is the world’s deepest and, at two cents a ride, the cheapest. It’s where the government hid out during the early days of the war. They perform a dual function as bomb shelters when the missile attacks become particularly heavy.

My Look Out Ukraine has duly announced every incoming Russian missile and its targeted neighborhood. The buzzing app kept me awake at night, so I turned it off. Let the missiles land where they may. For this reason, I reserved a south-facing suite and kept the curtains drawn to protect against flying glass.

The sound of the attacks was unmistakable. The anti-aircraft drones started with a pop, pop, pop until they hit a big 1,000-pound incoming Russian cruise missile, then you heard a big kaboom! Disarmed missiles that were duds are placed all over the city and are amply decorated with colorful comments about Putin.

The extent of the Russian scourge has been breathtaking, with an epic resource grab. The most important resource is people to make up for a Russian population growth that has been plunging for the last century. The Russians depopulated their occupied territory, sending adults to Siberia and children to orphanages to turn them into Russians. If this all sounds medieval, it is. Some 19,000 Ukrainian children have gone missing since the war started.

Everyone has their own atrocity story, almost too gruesome to repeat here. Suffice it to say that every Ukrainian knows these stories and will fight to the death to avoid the unthinkable happening to them. There will be no surrender.

It will be a long war.

Touring the children’s hospital in Kiev is one of the toughest jobs I ever undertook. Kids are there shredded by shrapnel, crushed by falling walls, and newly orphaned. I did what I could to deliver advanced technology and $10,000 in cash, but their medical system is so backward, maybe 30 years behind our own, that it couldn’t be employed. Still, the few smiles I was able to inspire made the trip worth it. This is the children’s hospital that was bombed a few months ago.

The hospital is also taking the overflow of patients from the military hospitals. One foreign volunteer from Sweden was severely banged up, a mortar shell landing yards behind him. He had enough shrapnel in him, some 250 pieces, to light up an ultrasound and had already been undergoing operations for months. It was amazing he was still alive.

To get to the heavy fighting, I had to take another train ride a further 15 hours east. You really get a sense of how far Hitler overreached in Russia in WWII. After traveling by train for 30 hours to get to Kherson, Stalingrad, where the German tide was turned, is another 700 miles east!

I shared a cabin with Oleg, a man of about 50 who ran a car rental business in Kiev with 200 vehicles. When the invasion started, he abandoned the business and fled the country with his family because they had three military-aged sons. He now works at a minimum-wage job in Norway and never expects to do better.

What the West doesn’t understand is that Ukraine is not only fighting the Russians but a Great Depression as well. Some tens of thousands of businesses have gone under because people save during war and also because 20% of their customer base has fled.

I visited several villages where the inhabitants had been completely wiped out. Only their pet dogs remained alive, which roved in feral starving packs. For this reason, my major issued me my own AK47. Seeing me heavily armed also gave the peasants a greater sense of security.

It’s been a long time since I’ve held an AK, which is a marvelous weapon. It’s it’s like riding a bicycle. Once you learned, you never forget.

I’ve covered a lot of wars in my lifetime, but this is the first fought by Millennials. They post their kills on their Facebook pages. Every army unit has a GoFundMe account where doners can buy them drones, mine sweepers, and other equipment.

Everyone is on their smartphones all day long, killing time, and units receive orders this way. But go too close to the front, and the Russians will track your signal and call in an artillery strike. The army had to ban new Facebook postings from the front for exactly this reason.

Ukraine has been rightly criticized for rampant corruption, which dates back to the Soviet era. Several ministers were rightly fired for skimming off government arms contracts to deal with this. When I tried to give $10,000 to the Children’s Hospital, they refused to take it. They insisted I send a wire transfer to a dedicated account to create a paper trail and avoid sticky fingers.

I will recall more memories from my war in Ukraine in future letters, but only if I have the heart to do so. They will also be permanently posted on the home page at www.madhedfefundtrader.com under the tab “War Diary”.

Donating $10,000 to the Children’s Hospital

On the Front at Crimea with a Dud Russian Missile

A Gift or Piroshkis from Local Peasants

One of 2,000 Destroyed Russian Tanks

The Battle of Kherson with my Unit

This Blown Bridge Blocked the Russians from Entering Kiev

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-10-21 09:02:412024-10-21 12:00:25The Market Outlook for the Week Ahead, or Complacence is Running Rampant

After the worst week of the year, we get the best. If you are confused by all of this, so am I.

On the one hand, the downside was firmly rejected by the $8 trillion sitting under the market that has been trying unsuccessfully to get into the market all year. The upside was rejected as well and who knows why? Did it run too far, too fast? Did valuations get overblown? Or was it simply time to take a summer vacation?

Who knows? All three were true.

I don’t really care. I am up 2.67% in August and am 100% in cash. I’m waiting for the market to tell me what to do next. If we get another crash, I’ll buy. I’m selling the next melt-up as well. The only thing I’m really confident in is my 6,000 target for the S&P 500 by year-end which appears right on schedule.

London certainly has become the most internationally diverse city in the world. Last week my tablemates in pubs included two women from Japan who nearly fell out of their chairs when they heard me speak Japanese. A business consultant from Milan was visiting London for the first time. The head of international marketing for Industrial Light & Magic from Mill Valley, CA, filled me in on the latest developments in the digital arts.

Two Arabic-speaking ladies from Oxford University were working for a charity getting food into Gaza. One bartender was headed for Sandhurst, England’s West Point. The other was from China, and I had to explain to him what Bushmills was (it’s an Irish whiskey). Oh, and my barber was from Syria and my cleaning lady was from Barbados.

All seven of my languages were given a thorough workout. There are 56 countries in the British Commonwealth, and it seems like all of them are here at once.

This summer’s crash down, then up offered many lessons and I want to make sure you catch them all. Let every loss be a learning experience, lest you be doomed to repeat it. Of the 20 great single-day losses in the S&P 500 (SPX) since 1923, I have traded through nine. The other 11 took place in the aftermath of the 1929 crash where the market eventually dropped by 90%. But I had many friends who traded all of those. Click here for details.

For a start, it helps a lot if you see a crash coming. This market had been begging for a crash during May and June and I positioned accordingly. I went into the meltdown with nine short positions in July-August, which covered most of my losses. And I only ran positions into very short August 16 option expiration, thus greatly limiting damage incurred by the losers.

I limited losses by stopping out of out-of-the-money losers quickly in (CAT), (BRK/B), and (AMZN), right at the August 5 opening in most cases. I then became super aggressive when the Volatility Index ($VIX) hit $65, a 2-year high. I also went hyper-conservative by adding four technology positions very deep 20% in-the-money in (NVDA), (META), (TSLA), and (MSFT), which instantly became money makers.

I used the first 1,000-point rally to add a short position for a very long, thus neutralizing the portfolio at the middle of the recent range and taking in a lot of extra income.

I did ALL of this while traveling in England, Switzerland, Lithuania, Poland, Austria, and Slovakia, from assorted airport business lounges, hotels, and Airbnb’s. The travel actually helped because the New York market doesn’t open until 3:30 PM each day, giving me plenty of time to plan the day’s strategy.

Now all we have to do is figure out what the Volatility Crash ($VIX) from $65 to $14 in 9 days means, the fastest in history by a huge margin. It usually takes 170 days to make this kind of move. Could it mean that our lives are about to become boring beyond tears once again?

I doubt it.

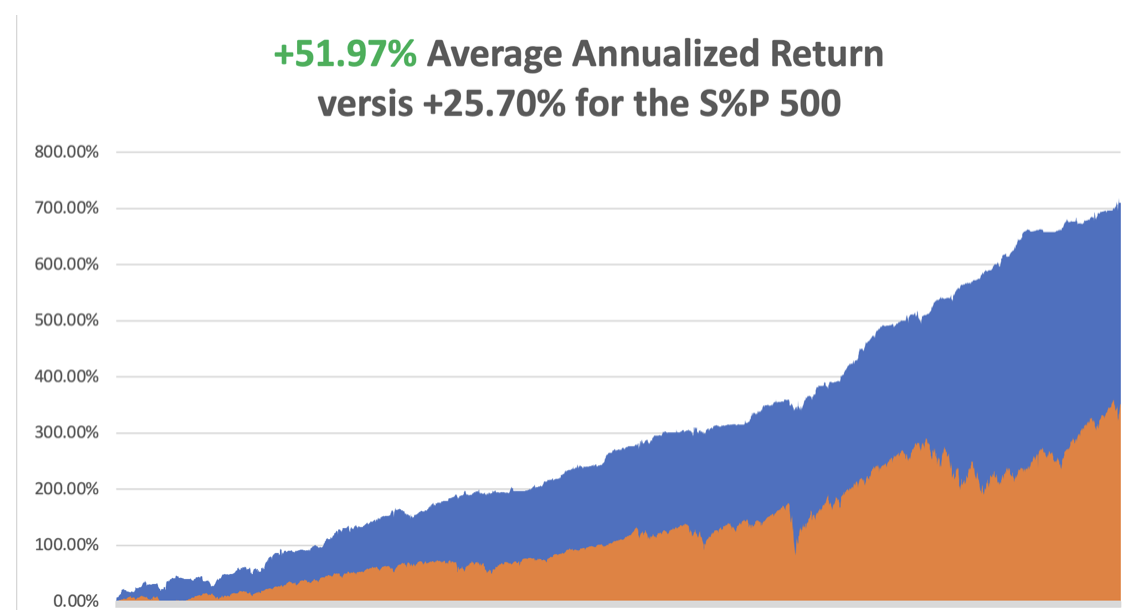

In July we ended up a stratospheric +10.92%. So far in August, we are up by +2.67%. My 2024 year-to-date performance is at +33.61%.The S&P 500 (SPY) is up +16.14%so far in 2024. My trailing one-year return reached +52.25.

That brings my 16-year total return to +710.24.My average annualized return has recovered to +51.97%.

I spent the entire week taking profits. I cashed in on my longs in (GLD) and (DHI) and covered shorts in (TSLA), (JPM), (AAPL), and (DHI). I am now 100% in cash and boy does it feel good.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 49 of 66 trades have been profitable so far in 2024, and several of those losses were really break-even. That is a success rate of 74.24%.

Try beating that anywhere.

The “Soft Landing” is Back, or so says Goldman Sachs after the meteoric rise in share prices of the last ten days. The extreme concerns about the U.S. economy that have re-emerged over the past month appear overblown and investors shouldn’t get too defensive. The recent spike of market volatility had more to do with positioning than a real scare about economic growth and that investors should “keep the faith” that the U.S. avoids a recession, while also avoiding a revival in inflation.

Now it’s Volatility That’s Crashing, down a record 49 points from $65 to $16 in 9 trading days, suggesting that investors may be returning to strategies that bank on low stock volatility despite a near-meltdown in equities early this month. The ($VIX) long-term median level is $17.6. Similar reversions in the so-called fear gauge have, on average, taken 170 sessions to play out.

Consumer Price Index is a Snore, at 0.2% MOM and 2.9% YOY, below the long-term average. Ebbing inflation aligns with anecdotes from businesses that consumers are pushing back against high prices, through bargain hunting, cutting back on purchases, and trading down to lower-priced substitutes. Stock was a snore as well.

Consumer Sentiment Drops, to an eight-month low according to the University of Michigan. It was revised higher to 66.4 in July 2024 from a preliminary reading of 66.

The Yen Carry Trade is Back, with hedge funds piling back into positions they baled on only two weeks ago. It’s just a matter of math, now that the Bank of Japan has given up on raising interest rates anytime soon. What this means is more leverage, risk, and volatility for global financial markets. I love it!

New Home Construction Dives, in July to the lowest level since the aftermath of the pandemic as builders respond to weak demand that’s keeping inventory levels high. Total housing starts decreased 6.8% to a 1.2 million annualized rate last month, dragged down the biggest decline in single-family units since April 2020

Global EV Sales Jump 21% YOY, in July thanks to a large rise in China. In the European Union MG Motor, owned by China's SAIC Motor Corp, expects to be hit hardest by provisional imposed on EVs imported from China. Europe is not going to give away its core industry, especially Germany’s. EVs - whether fully electric (BEV) or plug-in hybrids (PHEV) - sold worldwide were at 1.35 million in July, of which 0.88 million were in China, where they were up 31% year-on-year.

Refi’s Rocket 35% in a Week, the result of falling inflation and a monster rally in the bond market. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) fell slightly to 6.54% from 6.55%. The refinance share of mortgage activity increased to 48.6% of total applications from 41.7% in the previous week

US Producer Price Index Fades, coming in at a weak 0.1%, and giving the interest rate cut crown a high five. Stocks took off like a scalded chimp. Treasury yields fell on Tuesday as wholesale inflation measures came in softer than expected. The yield on the ten-year US Treasury was lower by about 4 basis points at 3.867%.

Foreign Investors Pull Record Amount from China, $15 billion in Q2. Chinese firms invest a record $71 billion overseas at the same time. It’s why the Chinese yuan has been so weak. The glory days are never coming back. Avoid (FXI).

Weekly Jobless Claims totaled 227,000, a decrease of 7,000 from the previous week and lower than the estimate for 235,000.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, August 19 the Meeting of Central Bankers at Jackson Hole begins. Traders will peruse the tea leaves looking for clues about future interest rates policy. All the major countries of the world have already started cutting rates except the US. On Tuesday, August 20 nothing of note is released.

On Wednesday, August 21 at 8:30 PM EST, the Minutes from the last FOMC meeting are released.

On Thursday, August 22 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, August 16 at 8:30 AM,Federal Reserve Chairman Jay Powell speaks. Also, New Home Sales are disclosed. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, when a Concierge member invited me to spend a week in Lithuania, I jumped at the chance. I had never been to this miniscule country of 3 million, formerly a part of the Soviet Union. The last time I spent any appreciable amount of time in Eastern Europe was in 1968, at the height of the Cold War.

My friend grew up in the old USSR. He remembers as a child having to go to school in the snow wearing worn-out shoes repaired with duct tape because there weren’t any in the stores.

I remember the old Soviet Union and it was grim beyond belief. Standards of living were sacrificed for military spending in the extreme. I remember I swapped my Levi’s for a worn-out pair plus $50 because they were unobtainable.

My friend cashed in on the collapse of the Soviet Union and the mass privatizations that followed. As a trader in Gazprom shares, he made millions. Now he lives a life of leisure, taking occasional potshots at the market with my assistance. He has been with me since 2011.

Knowing I was an avid pilot he treated me to a day at the local glider club. Introduced as a Top Gun instructor who had flown everything from RAF Spitfires to F-18s, and whose grandfather had worked for Orville Wright, the club pilots were somewhat in awe. I was asked to sign logbooks, which is a great honor among pilots.

I donned my parachute with ease, and everyone relaxed. A tow plane took us up to 2,500 feet, we pulled the release from the cable and suddenly were floating over the endless green forests of Eastern Europe.

I took the stick and performed some light aerobatics, careful not to scare the daylights out of my co-pilot. The thing that really impresses you about gliders is the complete silence. No earplugs inside your headphones here, just the whooshing of the wind. We headed for the nearest clouds in search of uplifting thermals.

I was informed that birds knew more about thermals than any of us, and sure enough, we found a flock and followed them right in. We immediately picked up a few hundred feet, our electronic altimeter whining all the way.

Flying with the birds on a perfect day, how cool is that?

We could have stayed up for hours but I had a lunch appointment. So we yanked on the speed brakes and plummeted down towards the field. At 50 feet, wind shear hit us from the side and we fell like a ton of bricks, bouncing hard. My left elbow smashed against the side of the cockpit inflicting a big gash.

The glider club rushed the aircraft expecting the worst, but I gave them a thumbs up. Any landing you walk away from is a good landing. I later learned that the previous day another pilot broke both legs executing the same maneuver.

When the Soviet Union broke up in 1991, we thought it would take 100 years to integrate the former republics with the West. Although Lithuania is still one of the cheapest countries in Europe, the improvement in the standard of living has been enormous. Old Towns in Europe are usually prime real estate with the most expensive accommodation. Here it’s so cheap that you see a lot of young families with kids in strollers on the sidewalks and in the parks.

They have adopted our vices too, with elaborate tattoos commonplace and teenagers vaping on every street corner.

In the capital city of Vilnius, I developed a work schedule that was tolerable. I spent my mornings walking the Old Town, visiting palaces, castles, baroque churches, museums, and art galleries. Then when the New York Stock Exchange opened up at 4:30 PM I was at my computer banging out my trade alerts as fast as I could write them. The market closed at 11:00 PM. Thank goodness the bars were still open.

Of course, the language is a challenge. Usually, I can understand half of what is going on in Europe. But Lithuanian is a direct descendant of Sanskrit so I couldn’t understand a single word. Everyone under 40 speaks English so I was thankfully able to do my grocery shopping with some assistance.

Every year, I like to return to all my favorite countries, plus add one or two new ones. Where will next year’s new countries be? I’m already scheduled to visit Nicaragua, Columbia, Panama, Costa Rica, and Curacao before yearend. Estonia, Argentina, Latvia, Brazil, Tahiti, who knows?

Ask me in 2025.

To watch a short video of my Lithuanian glider flight, please click here.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/08/John-Thomas-Lithuania-1.png8541136april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-08-19 09:02:512024-08-19 10:16:56The Market Outlook for the Week Ahead, or Lessons Learned

Below please find subscribers’ Q&A for the August 15 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from London, England

Q: Do you think we’ll still have another significant test of the lows for the year, or was that it last week? Stocks are rebounding huge this week.

A: They never really went down very much. The average drawdown IN THE S&P 500 (SPY) in any given year is 15%. We only got a 10% drawdown this month because there is still $8 trillion dollars in cash sitting under the market, which never got into stocks. All of this year it's been waiting for a pullback, so I was kind of surprised we even got 10%. I was forecasting maybe 6%. So could we get a new low? You never discount the possibility, but we really have to have another shocking data point to get down to a 15% correction. That is exactly what triggered this sell-off with the Nonfarm Payroll we got in early July. So give me another rotten Nonfarm Payroll report, and we could be back at last week's lows. Which is why I'm 100% cash. I want to have tons of dry powder, if and when that happens.

Q: We've seen a big increase in refi’s for homes in the last week. Is this going to be positive for the economy?

A: Absolutely yes, and that's why we're not going to have a recession. You get housing back into the economy which has been dead meat for almost 3 years now, and suddenly one quarter to one-third of the economy recovers. So that's what takes us into probably 3% economic growth for another year in 2025.

Q: What do you think of the Chipotle CEO (CMG) moving to take over Starbucks (SBUX)?

A: I think it's a very positive move. Starbucks was dead in the water. Their stores are old and dirty and products need refreshing. So if anyone needs a fresh view it's Starbucks, and the guy from Chipotle has a spectacular track record. Chipotle is probably one of the more successful fast-food companies out there. I usually don't ever play fast food—the margins are too low, but I certainly like to watch the fireworks when they happen.

Q: Should I be shorting airline stocks here like Delta Airlines (DAL), now that a recession risk is on the table?

A: Absolutely not. If anything, airlines are a buy here. They've had a major sell-off over the last 3 months for many different reasons, not the least of which was the software crash that they had a month ago. This is not shorting territory. That was 3 months ago for the airlines. Just because it's gone down a lot doesn't mean you now sell, it's the opposite. You should be buying airlines. I usually avoid airlines because they never have any idea if they're going to make money or not, so it's a very high-risk industry, and the margins are shrinking. Let me tell you, the airlines in Europe are absolutely packed. The fares are rock bottom and the service is terrible. Anybody who thinks the consolidation of the airline industry brought you great service has got to be out of their mind.

Q: Do you have any rules on when you stop loss?

A: The answer is very simple. If I do call spreads, whenever we break the nearest strike price, I'm out of there. That’s where the leverage works exponentially against you. Usually, you get a 1 or 2% loss when that happens, and you want to roll it into another trade as fast as you can and make the money back. Sometimes you have to do three trades to make up one loss because when you issue stop losses, everybody else is trying to get out of there at the same time. It's not a happy situation to be in, so we try to keep them to a minimum—but that is the rule of thumb. Keep your discipline. Hoping that it can recover your costs is the worst possible investment strategy out there. Hoping is not a winning strategy.

Q: Why don't you wait for the bottom?

A: Because nobody knows where the bottoms are. All you can do is scale. When you think things are oversold, when you think things are cheap, then you start buying things one at a time unless you get these giant meltdown days like we got on August 5th. So that's what I probably will be doing, is scaling in on the weak days on stocks that have the best fundamentals. That’s the only way to manage a portfolio.

Q: Is it a good time to buy REITs for income?

A: Absolutely. REITs are looking at major drops in interest rates coming. That will greatly reduce their overheads as they refi, and of course, the recovering economy is good for filling buildings. So I've been a very strong advocate of REITs the entire year, and they really have only started to pay off big time in the last month, and Crown Castle Inc (CCI) is my favorite REIT out there.

Q: I own Freeport McMoRan (FCX). Do you think China’s problems will make FCX a sell?

A: Not a sell, but a wait. China (FXI) is delaying any recovery in a bull market. If we get another move in (FCX) down to the thirties I would double up, because eventually American demand offsets Chinese weakness, and we’ll be back in a bull market on the metals. It's American demand that is delivering the long-term bull case for copper, not the return of Chinese construction demand, which led to the last bull market. So we really are changing horses as the main driver of the demand for copper. It still takes 200 pounds of copper to make an EV whose sales are growing globally.

Q: Is it time to buy (TLT) now?

A: No, the time to buy (TLT) was at the beginning of the year, seven months ago, three months ago, a month ago. Now we've just had a really big $12 point rally, and really almost $18 points off the bottom. I would wait for at least a 5-point drop-in (TLT) before we dive back into that. If you noticed, I haven't been doing any (TLT) trades lately because the move has been so extended. And in fact, if they only cut a quarter of a point in September, then you could get a selloff in (TLT), and that'll be your entry point there. You have to ditch your buy high, sell low mentality, which most people have.

Q: What bond should I buy for a 6 to 10-year investment?

A: I’d buy junk bonds. Junk bonds have always been misnamed, or I would buy some of the high-yield plays like the BB loans (SLRN). With junk bonds, the actual default rate even in a recession, only gets to about 2%. So it certainly is worth having. I still think they're yielding 6 or 7% now, so that's where I would put my money. Or you can buy REITs which also have similarly high yields, like the (CCI), which is around 5% now. Risks in both these sectors are about to decline dramatically.

Q: Will there be an inflation spike next year?

A: No. Technology is accelerating so fast it's wiping out the prices of everything that's highly deflationary, and that pretty much has been the trend over the last 40 years. So don't expect that to change. The post-COVID inflationary spike was a one-time-only event, which then ended two years ago. We've gone from a 9% down to a 2.8% inflation rate; unless we get another COVID-induced inflation spike, there's no reason for inflation to return. Deflation is going to be the next game.

Q: What do you think of the UK economy now that you're in London?

A: Awful! Brexit was the worst thing that happened to England—that's why it was financed by the Russians. Brexit will have the effect of dropping both the economic growth rate and standards of living by half over the next 20 years. Expect England to beg their way back into Europe sometime in the future, although I may not live long enough to see it. There are no English people in London anymore. It's all foreigners. No one can afford it.

Q: Should I leap on Tesla (TSLA) where the current price is?

A: No. We’re waiting for the nuclear winter in EVs to end—no sign of it yet. And unfortunately, Elon Musk is scaring away buyers, especially in blue states, by palling around with Donald Trump, a well-known climate change denier. What's in that relationship? I have no idea. One of the first things Trump did was to dump subsidies for electric cars last time he was president. It's hard to tell who’s gone crazier, Trump or Musk.

Q: I have an empty portfolio, when should we expect your options trade to start coming in again?

A: As soon as I see a great sell-off or a great individual situation like we got a couple days ago with the Mad Hedge Technology Letter in Lam Research (LRCX). That's what we look for all day, every day of the year. There's no point in trading for the sake of trading, that only makes your broker rich, not you. There's no law that says you have to have a trade every day, and actually having cash isn't so bad these days. They're still paying 5% for 90-day T Bills. If you don’t know what T Bills are, look up 90-day T bills on my website.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

(The Mad June traders & Investors Summit is ON!)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WELCOME TO THE MALLARD MARKET and ME AND 23 AND ME),

(AAPL), (GOOGL), (AMZN), (TSLA), (MSFT), (META), (AVGO), (LRCX), (SMCI), (NVR), (BKNG), (LLY), (NFLX), (VIX), (COPX), (T), (NVDA), (LEN), (KBH)

There’s nothing like the comfort and self-satisfaction of having a 100% cash position in a falling market. While everyone else is bleeding red ink, I am happily plotting my next trades.

Of course, the rest of the market isn’t really bleeding red ink, just giving up windfall profits. Still, it’s better to trade from a position of strength than weakness. It makes identifying the next winners easier.

Think of this as the “Mallard Market”. On the surface, it seems calm and peaceful, while underwater, it is paddling along like crazy. The damage has been unmistakable. Dell, the faux AI stock (DELL) crashed by 28%, Salesforce (CRM) got creamed for 34%, and ServiceNow (NOW) got taken to the woodshed for 22%.

It all belies a market that is incredibly nervous and fast on the trigger. The tolerance for any bad news is zero. Yet there has been no market crash as I expected. The 5,300 level for the (SPX) seems to possess a gravitational field, powered by $250 earnings per share and a multiple of 51X.

It was NVIDIA that put the writing on the wall by announcing a 10:1 split that has opened the floodgates for similar prosperous and high-priced companies.

There are now 36 stocks with share prices of $500 or more ripe for splits with $7 trillion in market cap, or 16% of the total market. While splits don’t change the value of a company, perceptions are everything, as they prove shareholder-friendly policies. While individual investors are confused by an onslaught of contradictory research recommendations, splits are a great “tell” on what to buy next.

Apple (AAPL), Alphabet (GOOGL), Amazon (AMZN), and Tesla (TSLA) have already carried out splits, some multiple times, to great success. Of the Magnificent Seven, only Microsoft (MSFT) and Meta (META) have yet to split.

In the tech area Broadcom (AVGO), Lam Research (LRCX), Super Micro Computer (SMCI), and Service Now (NOW) have yet to split. In the non-tech area, there are NVR Inc. (NVR), Booking Holdings (BKNG), Eli Lilly (LLY), and Netflix (NFLX). Many of these are well-known Mad Hedge recommended stocks.

History has shown that stocks rise 25% one year after a split compared to 12% for the market as a whole. A stock’s addition to the Dow Average or the S&P 500 (SPY) provides a boost. If both occur, stocks will absolutely explode. Stock splits are also much more attractive than buybacks at these high prices.

So, I’ll be trolling the market for split-happy candidates.

You should too.

Since it may be some time before we capitulate and take a worthwhile run at new highs, I thought I’d update you on the global demographic outlook, which is always a long-term driver of economies and markets.

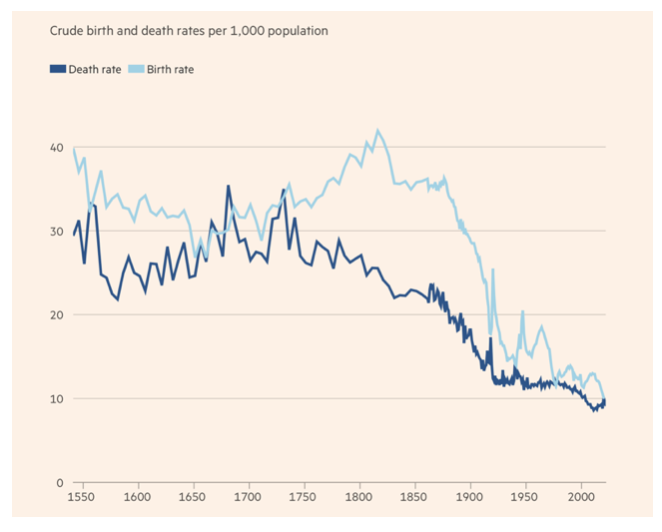

People are now living longer than ever before. But postponing death is only a part of the demographic story. The other is the decline in births. The combination of the two is creating huge changes in the global economy.

The notion of a “demographic transition” is almost a century old. Human societies used to have roughly stable populations, with high mortality matched by high fertility. Families had eight kids and 3-5 usually died in childhood, barely maintaining population growth.

In England and Wales in the 18th and 19th centuries, death rates suddenly plummeted. But fertility did not. The result was a population explosion. As the benefits of economic growth and advances in medicine and public health spread, most of the world has followed a similar transition, but far faster. As a result, human numbers rose fourfold over the last hundred years, from 2 billion to 8 billion.

In time, fertility followed mortality on a downward path across most of the world. As a result, fertility rates in more than half of all countries and territories in 2021 fell below the replacement level. For the world as a whole, the fertility rate was 2.3 in 2021, barely above the replacement of 2.1, down from 4.7 in 1960.

For high-income countries, the fertility rate was a mere 1.6, down from 3.0 in 1960. In general, poor countries still have higher fertility rates than richer ones, but they have been falling there, too.

What explains this collapse in fertility rates? An important part of the answer is the wonderful surprise that more children survived than expected. So, people started to practice various forms of birth control.

But the desire to have many children also shrank sharply. When husbands realized that smaller families meant high standards of living for themselves, family sizes dropped sharply. Even in ultra-conservative Iran, the fertility rate has collapsed from 6.6 in 1980 to only 1.7 in 2021.

A big reason for this shift was that, for their parents, children have moved from being a valuable productive asset in the 19th century to an expensive luxury today. That was back when 50% of our population worked on farms. Today it’s only 2%.

In the meantime, female participation in the economy rose dramatically in the 20th century, including in highly skilled careers. That raised the “opportunity cost” of producing children, especially for mothers. So, they have children later, or even not at all.

Where public childcare is more generous women are encouraged to combine careers with having children. The absence of such help helps explain the exceptionally low fertility rates in much of East Asia and Southern Europe, where parental support is limited.

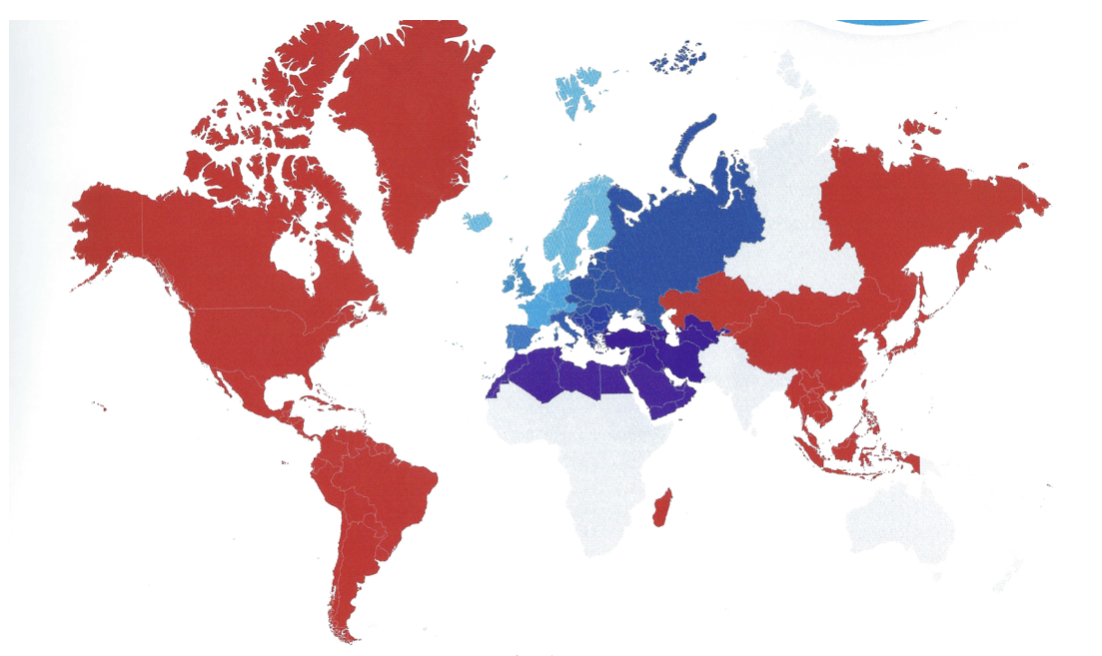

This global shift towards very low fertility, with the exception (so far) of sub-Saharan Africa, is among the most important events driving the global economy. One implication is that the population of Africa is forecast to be larger than that of all today’s high-income countries, plus China by 2060, thanks to the elimination of many diseases there.

Why is all this important?

Because rising populations create larger markets, more profits for corporations, and rising share prices. Shrinking populations have the opposite effect, as China is learning about its distress now. One reason the US is growing faster than the rest of the world is that a continuous stream of new immigrants since its foundation has created endless numbers of new workers and customers. Dow 240,000 here we come!

Just thought you’d like to know.

So far in May, we are up +3.74%. My 2024 year-to-date performance is at +18.35%.The S&P 500 (SPY) is up +10.48%so far in 2024. My trailing one-year return reached +35.74%. That brings my 16-year total return to +694.78%.My average annualized return has recovered to +51.48%.

As the market reaches higher and higher, I continue to pare back risk in my portfolio. I bailed on my last position early in the week, covering a short in Apple for a profit.

Some 63 of my 70 round trips were profitable in 2023. Some 27 of 37 trades have been profitable so far in 2024.

The Fed’s Favorite Inflation Gauge Cools by 0.2% in April, with the PCE, or the Personal Consumer Inflation Expectations Price Index. This one strips out the volatile food and energy components. It gives more credibility to a September rate cut and gave bonds a good day. NVIDIA Shares Continues to Go Ballistic, creating another $800 billion in market capitalization in three trading days. That is the most in history. That took NASDAQ to a new all-time high at 17,000. At $2.8 trillion (NVDA) could become the largest publicly traded company in the world in another day. Today’s tailwind came from an Elon Musk comment that his new xAI start-up would buy the company's high-end H100 graphics cards. Buy (NVDA) on the next 20% dip.

Pending Home Sales Dive, down 7.7% in April, the worst since the Covid market three years ago. The impact of escalating interest rates throughout April dampened home buying, even with more inventory in the market. But the anticipated rate cuts later this year should lead to better conditions, with improved affordability and more supply. Buy (LEN) and (KBH) on dips.

Money Supply Rises for the First Time in More than a Year. Remember money supply? As measured by M2, it sums up the currency, coins, and savings deposits held by banks, balances in retail money-market funds, and more. Data for April released on Tuesday afternoon showed an increase of 0.6% from a year ago. The Fed balance sheet has shrunk by $1.5 trillion in two years, the fastest decline in history, slowing the economy.

AT&T’s (T) Copper is Worth More Than the Company, and with plans to convert half its copper network to fiber by 2025 could free up billions of tons of the red metal to sell on the market. Copper prices have doubled over the past two years, and they could double again by next year. Worldwide there are 7 trillion tons of copper wire in place. Fiber is cheaper and exponentially more efficient than copper, which is facing huge demands from AI, EVs, and the electrification of the grid. Buy copper (COPX) on dips.

Markets are Underpricing Low Volatility (VIX), not a good thing at all-time highs. Volatility across equity and currency markets is low. The Volatility Index (VIX) at $12.46 compares with an average over five years of $21.5 and over the longer term of $19.9. Markets are heavily discounting good news and a disinflationary environment. It is not only stocks. There is also low volatility across currency markets. The DB index of foreign exchange volatility is at $6.3 versus an average of $7.6 over five years and $9.3 over the longer term. This will end in tears.

S&P Case Shiller Jumps to New All-Time High, with its National Home Price Index. The index rose by 1.29%, the fastest growth since April 2023. All 20 major metro cities were up last month and gained 6.5% YOY. Four cities are currently at all-time highs: San Diego, Los Angeles, Washington, D.C., and New York. Prices in San Diego saw the biggest gain, up 11.4% from February of 2023. Both Chicago and Detroit reported 8.9% annual increases. Portland, Oregon, saw the smallest gain in the index of just 2.2%. Unaffordability is the big story in the market right now. The sunbelt is seeing the most weakness, thanks to a post-pandemic construction boom.

Space X’s Starlink Tops 3 million Subscribers, and is rapidly moving towards a global WiFi network. I set up a dozen of these in Ukraine last October and even the Russians couldn’t hack them. It sets a global 200 Mb standard usable in most countries, even the remote Galapagos Islands in the Pacific. It’s only a VC investment now but could become Elon Musk’s next trillion-dollar company.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, June 3, the ISM Manufacturing PMI is released.

On Tuesday, June 4 at 7:00 AM, the JOLTS Job Openings Report will be published.

On Wednesday, June 5 at 7:00 AM, the ISM Services PMI is published.

On Thursday, June 6 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Challenger Job Cuts Report.

On Friday, June 7 at 8:30 AM, the Nonfarm Payroll and headline Unemployment Rate are announced. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, when Anne Wojcicki founded 23andMe in 2007, I was not surprised. As a DNA sequencing pioneer at UCLA, I had been expecting it for 35 years. It just came 70 years sooner than I expected.

For a mere $99 back then they could analyze your DNA, learn your family history, and be apprised of your genetic medical risks. But there were also risks. Some early customers learned that their father wasn’t their real father, learned of unknown brothers and sisters, that they had over 100 brothers and sisters (gotta love that Berkeley water polo team!), and other dark family secrets.

So, when someone finally gave me a kit as a birthday present, I proceeded with some foreboding. My mother spent 40 years tracing our family back 1,000 years all the way back to the 1086 English Domesday Book (click here)

I thought it would be interesting to learn how much was actually fact and how much fiction. Suffice it to say that while many questions were answered, alarming new ones were raised.

It turns out that I am descended from a man who lived in Africa 275,000 years ago. I have 311 genes that came from a Neanderthal. I am descended from a woman who lived in the Caucuses 30,000 years ago, which became the foundation of the European race.

I am 13.7% French and German, 13.4% British and Irish, and 1.4% North African (the Moors occupied Sicily for 200 years). Oh, and I am 50% less likely to be a vegetarian (I grew up on a cattle ranch).

I am related to King Louis XVI of France, who was beheaded during the French Revolution, thus explaining my love of Bordeaux wines, women wearing vintage Channel dresses, and pate foie gras.

Although both my grandparents were Italian, making me 50% Italian, I learned there is no such thing as pure Italian. I come out only 40.7% Italian. That’s because a DNA test captures not only my Italian roots, plus everyone who has invaded Italy over the past 250,000 years, which is pretty much everyone.

The real question arose over my native American roots. I am one-sixteenth Cherokee Indian according to family lore, so my DNA reading should have come in at 6.25%. Instead, it showed only 3.25% and that launched a prolonged and determined search.

I discovered that my French ancestors in Carondelet, MO, now a suburb of Saint Louis, learned of rich farmland and easy pickings of gold in California and joined a wagon train headed there in 1866. The train was massacred in Kansas. The adults were all killed, and the young children were adopted into the tribe, including my great X 5 Grandfather Alf Carlat and his brother, then aged four and five.

When the Indian Wars ended in the 1880s, all captives were returned. Alf was taken in by a missionary and sent to an eastern seminary to become a minister. He then returned to the Cherokees to convert them to Christianity.By then, Alf was in his late twenties so he married a Cherokee woman, baptized her, and gave her the name of Minto, as was the practice of the day.

After a great effort, my mother found a picture of Alf & Minto Carlat taken shortly after. You can see that Alf is wearing a tie pin with the letter “C” for his last name Carlat. We puzzled over the picture for decades. Was Minto French or Cherokee? You can decide for yourself.

Then 23andMe delivered the answer. Aha! She was both French and Cherokee, descended from a mountain man who roamed the western wilderness in the 1840s. That is what diluted my own Cherokee DNA from 6.50% to 3.25%. And thus, the mystery was solved.

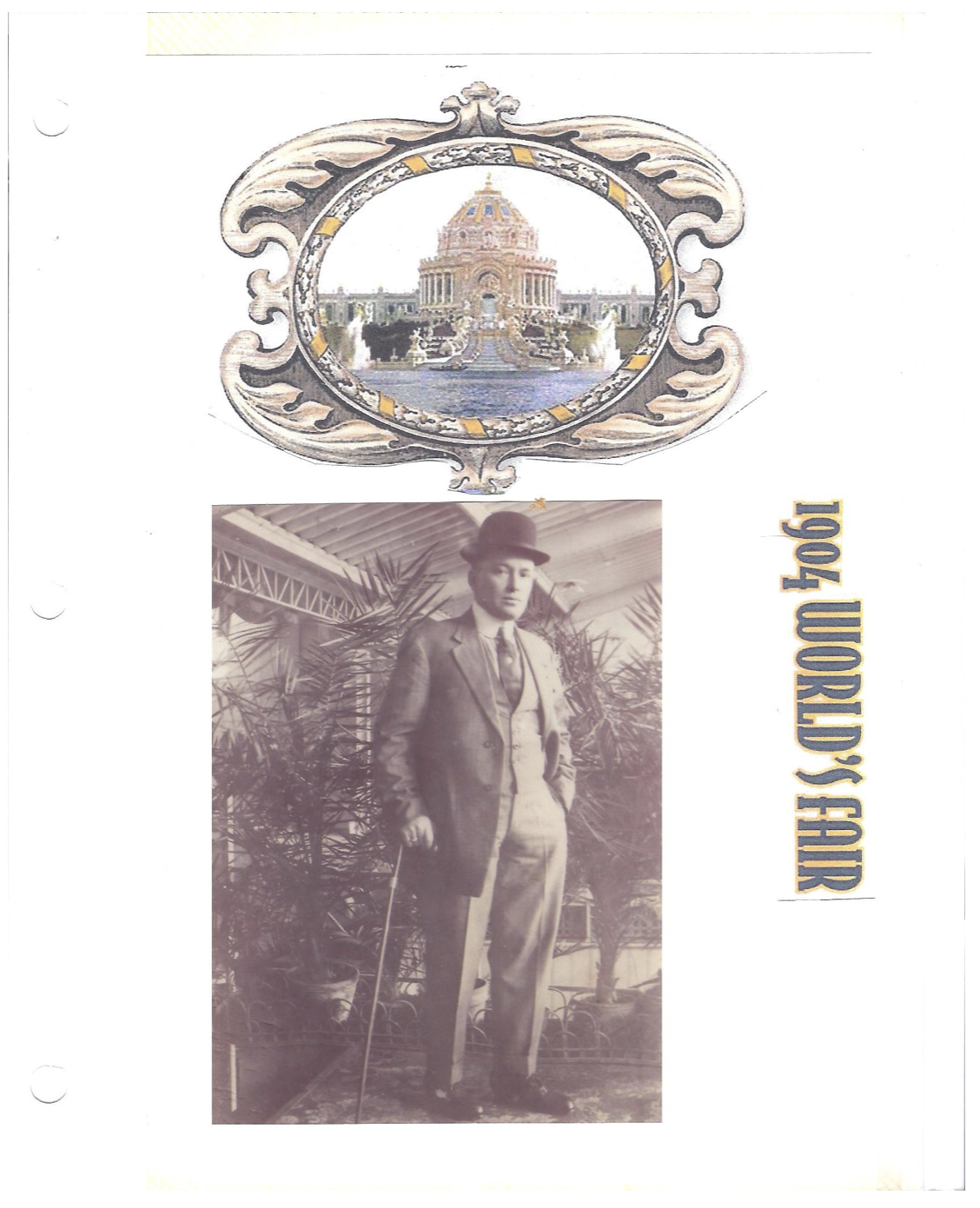

The story has a happy ending. During the 1904 World’s Fair in St. Louis (of Meet Me in St. Louis fame), Alf, then 46, placed an ad in the newspaper looking for anyone missing a brother from the 1866 Kansas massacre. He ran the ad for three months and on the very last day, his brother answered and the two were reunited, both families in tow.

Today, getting your DNA analyzed starts from $119, but with a much larger database, it is far more thorough. To do so, click here.

My DNA Has Gotten Around

It All Started in East Africa

1880 Alf & Minto Carlat, Great X 5 Grandparents

The Long-Lost Brother

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2023/01/alf-minto.jpg252293april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-06-03 09:02:142024-06-03 11:56:52The Market Outlook for the Week Ahead, or Welcome to the Mallard Market

A better headline for this piece would be “The Future of You,” as artificial intelligence is about to become so integral to your work, your investment portfolio, and even your very existence that you won’t be able to live without it, quite literally.

Well, do I have some great news for you. A blockbuster book about the state of play on all things AI will be released on September 25, and I managed to obtain and read an advanced copy. It is entitled: AI Superpowers: China, Silicon Valley, and the New World Order by Dr. Kai-Fu Lee.

The bottom line: The future is even more unbelievable than you remotely imagined. We are at the very early days of this giant megatrend, and the investment opportunities will be nothing less than spectacular.

And here is a barn burner. The price of AI is dropping fast as hundreds of thousands of new programmers pour into the field. Those $10 million signing bonuses are about to become a thing of the past.

Dr. Lee is certainly someone to take seriously. He obtained one of the first Ph.D.’s in AI from Carnegie Mellon University. He was the president of Google (GOOG) China and put in stints at Microsoft (MSFT) and Apple (AAPL). Today, he is the CEO of Sinovation Ventures, the largest AI venture capital firm in China, and is a board director of Alibaba (BABA).

AI is nothing more than deep learning, or super pattern recognition. Dr. Lee dates the onset of artificial intelligence to 1952, when an IBM mainframe computer learned to play checkers and beat human opponents. By 1955, it learned to develop strategies on its own.

Dr. Lee sees the AI field ultimately divided into two spheres of dominance, the U.S. and China. No one else is devoting a fraction of the resources needed to become a serious player. The good news is that Russia and Iran are nowhere in the game.

While the U.S. dominates in the original theory and algorithms that founded AI, China is about to take the lead in applications. It can do this because it has access to mountains of data that dwarf those available in America. China processes three times more mobile phones, five times more Internet customers, 10 times more eat-out orders, and 50 times more mobile transactions. In a future where data is currency, this is huge.

The wake-up call for China in applications took place two years ago when U.S. and Korean AI programs beat grandmasters in the traditional Chinese game of Go. Long a goal of AI programmers, this great leap forward took place 20 years earlier than had been anticipated. This created an AI stampede in the Middle Kingdom that led to the current bubble.

The result has been applications that are still in the realm of science fiction in the U.S. The Chinese equivalent of eBay (EBAY), Taobao, doesn’t charge fees because its customer base is so big it can remain profitable on ad revenues only. Want to be more beautiful in your selfies sent to friends? A Chinese app will do that for you, Beauty Plus.

The Chinese equivalent of Yelp, Dianping, has 600,000 deliverymen on mopeds. The number of takeout meals is so vast that it has been able to drop delivery costs from $6 a meal to 60 cents. As a result, traditional restaurants are dying out in China.

Teachers in Chinese schools no longer take attendance. Students are checked off when they enter the classroom by facial recognition software. And heaven help you if you jaywalk in a Chinese city. Similar software will automatically issue you a citation with a fine and send it to your home.

Credit card fraud is actually on the decline in China as dubious transactions are blocked by facial matching software. The bank simply calls you, asks you to look into your phone, takes your picture, and then matches it with the image they have on file.

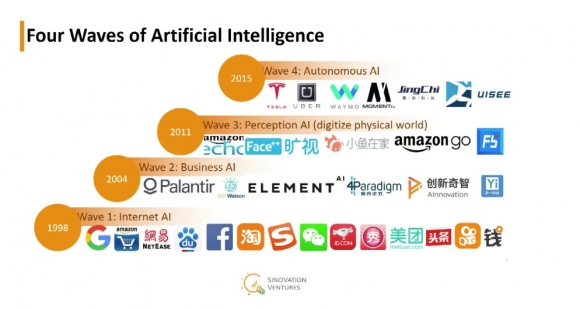

Dr. Lee sees AI unfolding in four waves, and there are currently companies operating in every one of these (see graph below):

1) Internet AI

The creation of black boxes and specialized algorithms opened the door to monetizing code. This was the path for today’s giants that dominate online commerce today, Google (GOOG), Amazon (AMZN), JD.com (JD), and Facebook (FB). Alibaba (BABA), Baidu (BIDU), and Tencent followed.

2) Business AI

Think big data. This is the era we just entered, where massive data from online customers, financial transactions, and health care led to the writing of new algorithms that maximize profitability. Suddenly, companies can turn magic knobs to achieve desired goals, such as stepping up penetration or monetization.

3) Perception AI

Using trillions of sensors worldwide, analog data on any movement, facial expression, sound, and image are converted into digital data, and then mined for conclusions by more advanced algorithms. Cameras are suddenly everywhere. Amazon’s Alexa is the first step in this process, where your conversations are recorded and then mined for keywords about your every want and desire.

Think of autonomous fast food where you walk in your local joint and it immediately recognizes you, offers you your preferred dishes, and then auto bills your online account for your purchase. Amazon has already done this with a Whole Foods store in Seattle.

4) Autonomous AI

Think every kind of motion. AI will get applied to autonomous driving, local shuttles, factory forklifts, assembly lines, and inspections of every kind. Again, data and processing demand take an enormous leap upward. Tesla (TSLA), Waymo (GOOG), and Uber are already very active in this field.

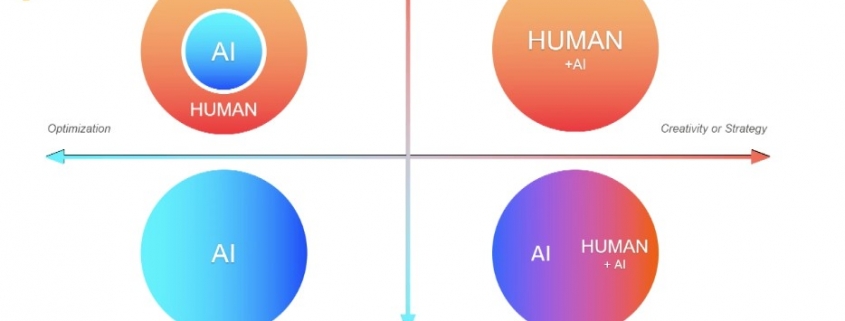

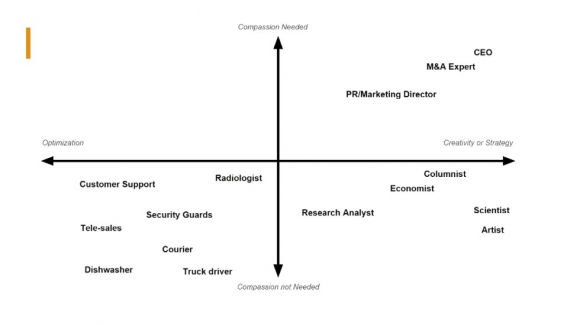

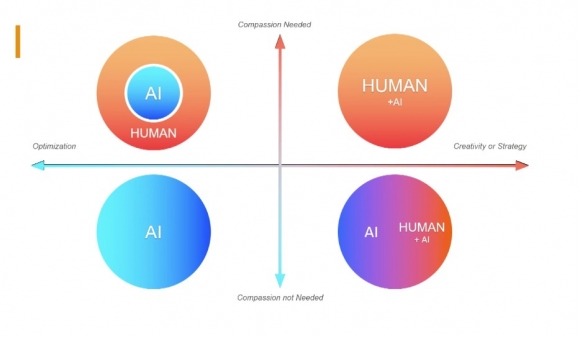

The book focuses a lot on the future of work. Dr. Lee creates a four-part scatter chart predicting the viability of several types of skills based on optimization, compassion, creativity, and strategy (see below).

If you are a truck driver, in customer support, or a dishwasher, or engage in any other repetitive and redundant profession your outlook is grim. If you can supplement AI, such as a CEO, economist, or marketing head you’ll do fine. People who can do what AI can’t, such as teachers and artists, will prosper.

The Investment Angle

There have been only two ways to invest in AI until now. You can buy shares in any of the seven giants above, whose shares have already risen for 100- or 1,000-fold.

You can invest in the nets and bolts parts providers, such as NVIDIA (NVDA), Advanced Micro Devices (AMD), Micron Technology (MU), and Lam Research (LRCX), which provide the basic building blocks for the Internet infrastructure.

Fortunately for our paid subscribers, the Mad Hedge Trade Alert Service caught all of these very early.

What’s missing is the “in-between companies,” which are out of your reach because they are locked up in university labs or venture capital funds. Many of these never see the light of day as public companies because they get taken over by the tech giants above. It’s effectively a closed club that won’t let outsiders in. It’s a dilemma that vexes any serious technology investor.

When quantum computing arrives in a decade, you can take all the functionality above and multiply it by a trillion-fold, while costs drop a similar amount. That’s when things really get interesting. But then, I’ve seen trillion-fold increases in technology before.

I hope I live to see another.

Personally, I Prefer the Original

https://www.madhedgefundtrader.com/wp-content/uploads/2018/09/Human-and-AI-chart-image-3-e1536698568163.jpg337580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2021-08-05 09:02:522021-08-05 15:59:33The New AI Book that Investors are Scrambling For

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.