Global Market Comments

June 5, 2020

Fiat Lux

Featured Trade:

(JUNE 3 BIWEEKLY STRATEGY WEBINAR Q&A),

(FB), (M), (UAL), (LVS) , (WYNN), (MS), (SPX), (TBT), (TLT), (AAPL), (FB), (MSFT), (SDS), (SPX), (AMZN) (LEN), (KBI), (PHM), (TSLA)

Global Market Comments

June 5, 2020

Fiat Lux

Featured Trade:

(JUNE 3 BIWEEKLY STRATEGY WEBINAR Q&A),

(FB), (M), (UAL), (LVS) , (WYNN), (MS), (SPX), (TBT), (TLT), (AAPL), (FB), (MSFT), (SDS), (SPX), (AMZN) (LEN), (KBI), (PHM), (TSLA)

Below please find subscribers’ Q&A for the June 3 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Domino's Pizza (DPZ) is at all-time highs? Would you buy this name right here, right now?

A: No, I would not even buy their pizza. You would be crazy to buy them right now up here this high. I prefer Round Table, the pizza not the stock. All of these “reopening” stocks are way overextended.

Q: Will the riots delay the recovery?

A: Yes, they will, it could take as much as another 1% off the current GDP growth rate. It’s hitting the already worst-hit sector—retailers. Many retailers will not come back from these, especially the small ones. These businesses were just returning from being closed for two months when they got burned down. But we won’t see it in the macro data for many months because its happening largely at the micro level. If you didn’t like Macy’s (M) before when it was headed for Chapter 11, you definitely won’t like it now that it is burning down.

Q: If airlines like United Airlines (UAL) can’t use the middle seat, do you see ticket prices going up 10%, 25%, or 50%?

A: Yes. In theory, to just cover the middle seat, they have to increase prices 33%. And there will be a whole lot of new costs that the airlines have to endure as part of this pandemic, such as extra cleaning, disinfecting, and temperature taking. So, they’re really going to need to increase prices by 50% or more just to break even. My guess is that the airline industry will shrink in half in the fall when all the government bailout money runs out. So, I've been telling people to take profits on the airlines, especially if you have a double or triple in them, or if you have the LEAPS.

Q: Is Facebook (FB) immune from any big selloff?

A: No, nobody is immune—look how much Facebook sold off in March, some 35%. Mark Zuckerberg seems to be making a deal with the devil, accommodating the president with unrestricted incendiary Facebook posts. And the consequences of a Democratic win for Facebook could be hugely negative, so I am not participating in that one. Mark doesn’t have a lot of friends in congress right now so regulation looms.

Q: What do you think about buying Las Vegas Sands (LVS) or Wynn Resorts (WYNN) on the expectation of reopening?

A: I’m a Nevada resident and get frequently updated on the casino news. They’re only going to be allowed half of peak casino visitors that they had in January, so they will generate huge losses. Almost all companies are being allowed to reopen back to half the level that guarantees bankruptcy in 3-6 months. But we won’t see that in the numbers for many months either. I’m negative on any industry that depends on packing people in, like airlines, cruise lines, and movie theaters.

Q: What are the chances of a mass student debt cancellation?

A: That is a possibility if the Democrats win in November, and it has already been proposed. It is about a $1.5 trillion ticket. If you’re bailing out large companies, small companies, airlines, and the oil industry, why not students? It would have the benefit of adding 10 million more consumers to the economy, who are not current participants because they have massive student debts that are appreciating at 10% a year and have terrible credit ratings. So that would be another great economic stimulus measure. By the way, I paid off my student loans 40 years ago in a lump sum payment with my first paycheck from Morgan Stanley (MS). How much did four years of college cost during the 1960s? $3,000. Such a deal.

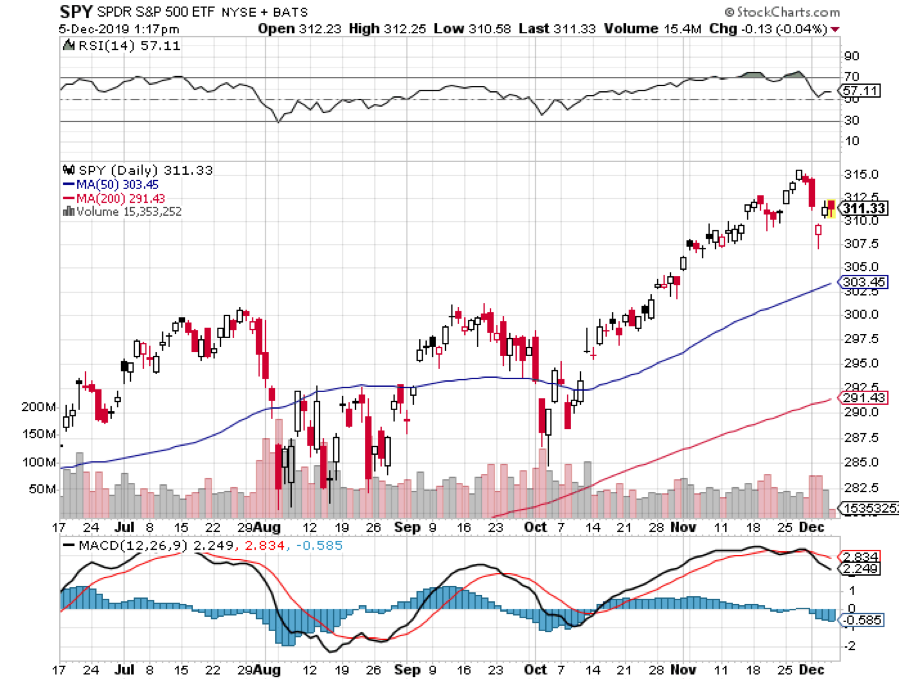

Q: What’s the next resistance level on the S&P 500 (SPX)?

A: The target we’ve been looking for is $3,125. I’m looking for roughly $40 points above that level—it should be about $3,165. We’re in uncharted territory here because nobody’s ever seen a market rise 40% in two months, so any technical recommendation has to be bearish except for a very short term, like intra-day or daily views.

Q: Any correlation between the 1918 epidemic and now?

A: Here is your History of Virology Lesson 101 for today. There is some similarity, but the 1918 flu actually originated on a farm in Kansas, had a 2% death rate, took a trip to Europe, mutated, came back months later, and then had a death rate of 50%. We haven't seen that second wave yet, or major mutations. We have seen a couple of different DNA strands out there though, meaning we would need multiple different vaccines when we get them. By the way, it was called the “Spanish Flu” because during WWI, every country had censorship except Spain because it was not a combatant. So, the pandemic was only reported in the Spanish newspapers.

Q: Would you get out of any of the previously recommended LEAPS?

A: Yes, I would be taking profits on all of your LEAPS—whether tech, domestic, “recovery”, or whatever else—so if we do get a correction over the summer, you can get back in at better prices, with longer expirations. You can go two years out from say August for example. The risk/reward today is terrible.

Q: Would you hold on to the (SDS) right now, or wait for the pullback

A: No, we have offsetting profits on all of our (SDS) positions, until today—if the market keeps accelerating to the upside, SDS losses will start to offset our profits on the positions, so that’s why I would get out.

Q: Should I buy the ProShares Ultra-Short 20 + Year Treasury Bond Fund (TBT)? I don’t do options.

A: You don’t need to do options, (TBT) is an ETF; anybody can buy that, it’s just like buying a stock.

Q: What is happening with the Australian market?

A: It will trade with the US stock market tick for tick, which means they’ve had a fantastic rally, overdue for a selloff. Wait to buy the next dip.

Q: If markets are going to go down soon, why exit the (SDS)

A: It may go up first before it goes down. And in any case, I have a great profit on the combined position of long (SDS) and short bonds. These days, I like taking big profits rather than praying they become bigger. It’s about risk control and knowing what you can get away with in certain market conditions.

Q: Is now the time to sell the highflyers in tech?

A: Yes, I would be selling Apple (AAPL), Facebook (FB), Microsoft (MSFT), and Amazon (AMZN). Get dry powder, which is worth a lot after you’ve seen a move like this; especially if the economy gets worse, which is likely. My late mentor Barton Biggs taught me to always leave the last 10% of a move for the next guy.

Q: At what point do you buy the ProShares Ultra Short S&P 500 ETF (SDS) outright?

A: Only if there is an immediate collapse in the market, which I can’t foresee with any certainty. When you play these bear ETFs, the costs are very high. You are short double the (SPX) dividend, which is about 5% a year, plus hefty management fees. So, you really have to catch a quick, large move to the downside to make any real money.

Q: Real estate seems like the big winner of the pandemic. Will prices be up by the end of the year or is this just a temporary spike?

A: They will be up at the end of the year. I have been telling readers all year that their home will be their best investment in 2020 and that is coming true. Real estate has a massive tailwind behind it which has really been in place for a couple of years now, and that is the millennials upgrading and buying houses. The pandemic has really poured gasoline on the fire and triggered a stampede out of the city and into the suburbs. Having 85 millennials ready to upgrade their homes is a huge positive for the real estate market, and I’d be looking to buy the homebuilders on any dip. That’s probably the best domestic play out there. Buy Lennar Corp. (LEN) and Pulte Homes (PHM) on dips.

Q: Post pandemic, will manufacturing have any way of helping US economic growth, or is bringing back the supply chains fake news?

A: It is fake news because if companies bring back production, it will be machines and not people making things. Unless you want to pay $10,000 for an iPhone, or $5,000 for a low-end laptop. Oh yes, and the stocks which made these things would be 90% lower as well. That’s what those products cost in today’s dollars if they were made in the United States. I wouldn't count on any repatriation of US jobs unless people want to work for $3 a day like the Chinese do. Offshoring happened for a reason.

Q: How do I hedge a municipal bond portfolio?

A: You might think about taking profits in muni bonds. They’re yielding around 2% and change. And they could get hit with a nice little 20-point decline if the US Treasury bond market (TLT) falls apart, which it will. Then you can think about buying them back. If you really want to hedge, you sell short the (TLT) against your long muni bond portfolio. But that is an imperfect hedge because the default rate on munis is going to be much higher than it is now than it was in 2008-2009, and much higher than US Treasuries, which never defaults despite what the president has said.

Q: What is dry powder?

A: It means having cash to buy stocks at market bottom. In the 1800s before cartridges were invented, black powder got wet whenever it rained causing guns to fail to shoot. That is the historical analogy.

Q: What do we do now if we’re getting started?

A: It will require a lot of discipline on your part as coming in at market tops is always risky. Wait for the next trade alert. Every one of these is meant to work on a standalone basis. I would do nothing unless you see one of these things happen; any 2 or 3-point rally in bonds (TLT), you want to sell short. We’re just at the beginning of a multiyear trade here so it’s not too late to get back into that. Gold (GLD) is probably safe to buy on the dip here since we are at the very beginning of a historic expansion of the global money supply. I wouldn’t touch any stocks unless we get at least a 10% drop and then I'll start putting out call spread recommendations on single stocks. But right here, on top of the biggest bounceback in stocks in market history, don’t do anything. Just read the research and make lists of things to buy when they do dip—something I do for you anyway.

Q: What about Beyond Meat (BYND)?

A: The burgers are not that bad, but the stock is way overpriced and you don’t want to touch it. It's one of the fad stocks of the day.

Q: Can we access the slides after the webinar?

A: Yes, we post it on the website under your “Account” section about two hours after we’re done.

Q: Are you saying sell everything currently profitable?

A: Yes, I would be selling everything on a short term basis, keep tech and biotech on a long term basis. We are the most overbought in history and you don’t get asked twice to sell tops. But yes, it could go higher before the turn happens. From a risk-reward point of view, it’s terrible to do anything right now.

Q: Could we get a pullback to the $260-$270 area in the S&P 500 (SPY)?

A: Yes, especially if we get a second worse wave of corona and the stimulus takes much longer than we thought to get into the economy, or if the rioting continues.

Q: Should you sell CCI now?

A: Yes, I actually would. You have a 57% gain in the stock in ten weeks, so why not? Long term, it’s a hold.

Q: Are any retail stocks a buy?

A: No, they aren’t because a lot of them are going to go under but you don’t know which ones. After shutting down and losing 60% of their revenues, they’re now being burned down. The pros who do well in the sector are bankruptcy specialists who have massive research teams that analyze every lease in every mall and then cherry-pick. You and I don’t have the ability to do that so stay away.

Q: What is the best way to play real estate?

A: Buy a house. If not, then you buy (LEN), (KBI), and (PHM).

Q: Is it too late to get back in the stock market?

A: Yes, I'm afraid it is. Buying, because it has gone up, is a classic retail investor mistake. After this meltdown, maybe you will learn to buy stocks when everyone else is throwing up on their shoes. That's what I was doing in March and we got returns of 50% to 100% on everything and 500% to 1,000% on the LEAPS (TSLA).

Q: Are you buying puts?

A: No, I am not taking outright short positions any more than I have now because we have a Fed-driven melt-up underway with a stimulus that's 20x larger than that seen during the 2008-2009 Great Recession. When I don’t know what’s going to happen, I get out.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

May 29, 2020

Fiat Lux

Featured Trade:

(JOIN THE JUNE 4 TRADERS & INVESTORS SUMMIT),

(THE CONTINUING DEATH OF RETAIL),

(AMZN), (WMT), (M), (JWN),

(TESTIMONIAL)

If you had to pick the biggest loser of our ongoing pandemic and the trade wars, it would be the retail industry (XRT). Higher costs which can’t be passed on, rising minimum wages, lower selling prices, and a massive inventory glut is not what money-making is all about.

Now, take all of those problems and drop your revenues by half, thanks to the pandemic. A future where touching, feeling, and trying on things before you buy them is about to become an extravagant luxury.

The stocks have delivered as expected, providing one of the worst-performing sectors of the past three years. Half of them probably won’t even make it until Christmas.

In fact, Sears and Macy’s have announced more store closings nationwide. The overhead is killing them in a micro margin world devoid of window shopping customers.

So, I stopped at a Walmart (WMT) the other day on my way to Napa Valley to find out why.

I am not normally a customer of this establishment. But I was on my way to a meeting where a dozen red long stem roses would prove useful. I happened to know you could get these for $10 a dozen at Walmart, 60% cheaper than anywhere else.

After I found my flowers, I browsed around the store to see what else they had for sale. The first thing I noticed was that half the employees were missing their front teeth.

The clothing offered was out of style and made of cheap material. It might as well have been the Chinese embassy. Most concerning, there was almost no one there, customers OR employees.

The Macy’s downsizing is only the latest evidence of a major change in the global economy that has been evolving over the last two decades.

However, it now appears we have reached both a tipping point and a point of no return. The future is happening faster than anyone thought possible. The pandemic has forced business evolution to move at hyper fast forward and the Death of Retail is no exception.

I remember the first purchases I made at Amazon 20 years ago. I personally knew the founder, Jeff Bezos, from my Morgan Stanley days. The idea sounded so dubious that I made my initial purchases with a credit card with only a low $1,000 limit. That way, if the wheels fell off, my losses would be limited.

And how stupid was that name, Amazon, anyway? At least he didn’t call it “Yahoo” because it was already taken.

Today, I do almost all of my shopping at Amazon (AMZN). It saves me immense amounts of time while expanding my choices exponentially. And I don’t have to fight traffic, engage in the parking space wars, or wait in line to pay.

It can accommodate all of my requests, no matter how bizarre or esoteric. A WWII reproduction Army Air Corps canvas flight jacket in size XXL? No problem!

A used 42-inch Sub Zero refrigerator with a front door ice maker and water dispenser? Have it there in two days, with free shipping at one fifth the $17,000 full retail price.

So I was not surprised when I learned that Amazon accounted for 25% of all new online sales in 2019 in a market that is already growing at a breathtaking 20% YOY.

In 2000, after the great “Y2K” disaster that failed to show, I met with Bill Gates Sr. to discuss his foundation’s investments.

It turned out that they had liquidated their entire equity portfolio and placed all their money into bonds. It turned out to be a brilliant move, coming mere months before the Dotcom bust and a 20-year bull market in fixed income which only peaked two months ago.

Mr. Gates (another Eagle Scout) mentioned something fascinating to me. He said that unlike most other foundations their size, they hadn’t invested a dollar in commercial real estate. Today, that looks like a prescient move in the extreme with 60% of mall tenants skipping their rent.

It was his view that the US economy would move entirely online, everyone would work from home, emptying out city centers, and rendering commuting unnecessary. Shopping malls would become low rent climbing walls and paintball game centers.

Mr. Gates’ prediction may finally be occurring. In the San Francisco Bay area, the only employed people are those who are telecommuting.

Even before the pandemic, it was common for staff to work Tuesday-Thursday at the office, and from home on Monday and Friday. Productivity increases. People are bending their jobs to fit their lifestyles. And oh yes, happy people work for less money in exchange for personal freedom, boosting profits.

The Mad Hedge Fund Trader itself may be a model for the future. We are entirely a virtual company, with no office. Everyone works at home in four countries around the world. Oh, and we all use Amazon to do our shopping.

The downside to this is that whenever there is a snowstorm anywhere in the country, it affects our output. Two storms are a disaster, and at three, such as last winter, we grind to a virtual halt.

The main thing I am worried about is the Internet in the Philippines which is unable to handle the tenfold increase in demand since the start of the pandemic. They don’t have our infrastructure. If you wonder why your customer support at any company has suddenly gotten poor, that is the reason.

You may have noticed that I can work from anywhere and anytime (although sending a Trade Alert from the back of a camel in the Sahara Desert was a stretch), so was sending out an Alert while hanging on the cliff face of a Swiss Alp. But they both made money.

Moroccan cell coverage is better than ours, but the dromedary’s swaying movement made it hard to hit the right keys.

The cost of global distribution is essentially zero. Profits go into a bonus pool shared by all. Oh, and we’re hiring, especially in marketing.

It is happening because the entire “bricks and mortar” industry is getting left behind by the march of history.

Sure, they have been pouring millions into online commerce and jazzed up websites. But they all seem to be poor imitations of Amazon, with higher prices and worse service. It is all “hour late and dollar short” stuff.

In the meantime, Amazon has soared by an eye-popping 56% since the March 23 low and is one of the top-performing big-cap stocks of 2020. There is now a cluster of Amazon analyst forecasts targeting the $3,000 mark, including me.

And here is the bad news. Bricks and Mortar retailers are about to lose more of their lunch to Chinese Internet giant Alibaba (BABA), which is ramping up its US operations and is FOUR TIMES THE SIZE OF AMAZON!

There’s a good reason why you haven’t heard much from me about retailers. I made the decision 30 years ago never to touch the troubled sector.

I did this when I realized that management never knew beforehand which of their products would succeed and which would bomb, and therefore, were constantly clueless about future earnings.

The business for them was an endless roll of the dice. That is a proposition in which I was unwilling to invest. There were always better trades.

I confess that I had to look up the ticker symbols for this story, as I never use them.

You will no doubt be enticed to buy retail stocks as the deal of the century by the talking heads on TV, Internet research, and maybe even your own brokers, citing how “cheap” they are because the prices are so low.

Never confuse a low stock price with “cheap.”

It will be much like buying the coal industry (KOL) a few years ago, another industry headed for the dustbin of history. That was when “cheap” was on its way to zero for almost every company. Don’t buy the next coal company.

So the next time someone recommends that you buy retail stocks, you should probably lie down and take a long nap first. When you awaken, hopefully the temptation will be gone.

Or better yet, go shopping at Amazon. The deals are to die for.

To read “An Evening with Bill Gates Sr.,” please click here.

Global Market Comments

May 4, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE NEXT BOTTOM IS THE ONE YOU BUY),

(SPY), (SDS), (TLT), (TBT), (F), (GM), (TSLA), (S), (JCP), (M)

It was only a year ago that I was driving around New Zealand with my kids, admiring the bucolic mountainous scenery, with Herb Albert and the Tijuana brass blasting out over the radio. Believe me, the tunes are not the first choice of a 15-year-old.

Today, it is all a distant memory, with any kind of international travel now unthinkable. For me, that is like a jail sentence. It is all a reminder of how well we had it before and how bleak is the immediate future.

Stock traders have certainly been put through a meat grinder. The best and worst months in market history were packed back to back, down 39% and then up 37%. At the March 23 low, the Dow average had fallen by 11,400 in a mere six weeks. Those who lived through the 1929 crash have lost their bragging rights, if there are any left.

However, like my college professor used to say, “Statistics are like a bikini bathing suit. What they reveal is fascinating, but what they conceal is essential.”

Most of the index gains were achieved by just five FANG stocks. Virtually all of the gains were from “stay at home” companies taking in windfalls from cutting-edge online business models. The “recovery” had a good week, and that was about it.

The other obvious development is that if any business was in trouble before the health crisis, you can safely write them off now. That includes retailers like Sears (S), JC Penny’s (JCP), Macy’s (M), almost all brick-and-mortar clothing sellers, and the small and medium-sized energy industry.

The worst economic data points since the black plague are about to hit the tape. Some 30 million in newly unemployed is nothing to dismiss, and that number grows to 40 million if you include discouraged workers.

That is 25% of the workforce, the same as peak joblessness during the great depression. But $14 trillion in QE and fiscal stimulus is about to hit the market too.

Which brings us to the urgent question of the day: What to do now?

It’s a vexing issue because this is not your father’s stock market. This is not even the market we’d grown used to only six months ago. All I can say is that the virology course I took 50 years ago today is worth its weight in gold.

I think you would be mad not to count a second Covid-19 wave into your calculations. This could occur in weeks, or in months, after the summer respite. This makes a second run at the lows a sure thing. I don’t think we’ll make it, but a loss of half the recent gains is entirely possible.

That takes us back down to a Dow Average of 21,000, or an S&P 500 (SPX) of 2,400.

If you are a long term investor looking to rebuild your retirement nest egg, there are only two sectors left in the market, Tech and Biotech & Healthcare. Looking at anything else is both risky and speculative. So, if we do get another meltdown, these are the only areas you should target.

If I am wrong, the market will probably bounce along sideways in a narrow range for months. That is a dream scenario if you pursue a vertical bull and bear call and put option spread strategy that I have been offering up to followers for the past decade.

Pending Home Sales Were Down a Staggering 20.8% in March and off 16.3% YOY. The worst is yet to come. The West, the first into shelter-in-place, was down a monster 26.8%. Prices still aren’t moving because nobody can buy or sell. The way homebuilder stocks like (LEN) and (KBH) are trading, I’d say your home will be worth a lot more in a year when the huge demographic push resumes. I’m not selling.

The 60,000 peak in deaths proposed by the administration only weeks ago is now looking wildly optimistic. Their worst-case scenario of 200,000 deaths, the announcement of which set the March 23 bottom of the Dow Average at 18,200, is now likely.

It will take place when the epidemic peaks in the southern and midwestern states that never sheltered in place or went in late and are coming out early. That second wave may well create a second bottom in stock prices, and that is the one you jump into and buy with both hands.

US Corona Deaths topped 66,000 last week, more than we lost after a decade of the Vietnam War. Total cases exceed one million.

Bank of America sees negative 30% GDP this quarter annualized, so says CEO Brian Moynihan. His economists expect negative 9% in Q3 and plus 30% in Q4. Suffice it to say, this is the ultra-optimistic case. Q4 doesn’t include the millions of businesses that will disappear because the Paycheck Protection Plan is failing so badly. Most government aid will take three to six months to hit the economy.

US GDP crashed 4.8% in Q1, the worst quarter since the depths of the 2008 Great Recession. Q2 will be far worse. We are now officially in recession, which should last 3-4 quarters. But is it already in the price? Next week’s April Nonfarm Payroll report should be a real humdinger.

Ford (F) lost $5 billion in Q2, and there is no guidance about the future. Avoid (F) on pain of death. Late to electric, they may not make it this time. They’re still in the buggy whip business.

Weekly Jobless Claims topped 3.8 million, bringing the six-week total to a staggering 30 million, more than those lost at the peak of the Great Depression. Florida, California, and Georgia led with applications. This implies a U-6 Unemployment rate of 25% with next week’s April Nonfarm Payroll Report. And the Dow Average is up 37% since March 23?

The Bond Market crashed on a Trump threat to default on US Treasury bonds, of which China owns $900 billion. It’s Trump’s retaliation for the Middle Kingdom spawning the Coronavirus, which he calls the “Chinese virus.” The (TLT) dropped three points on the news. Good thing I am triple short a market that is about to get crushed by massive government borrowing.

A glut of imported autos is parked at sea, steaming in circles, awaiting a recovery in the US economy. They are no doubt finding company with imported oil tankers. So many unwanted cars coming in the land-based storage areas were overflowing. It’s tough to see (F) and (GM) recovering from this. Keep buying made in the USA (TSLA) on dips, which is headed to $2,500 a share.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $0 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch performance had one of the best weeks in years, up a blistering +8.05%. We are now only 6.67% short of a new all-time high. The 100 new subscribers who came in the previous week are sitting pretty and must think I’m some sort of guru.

My aggressive triple weighting in short bond positions came in big time when Trump threatened to default on US debt. My shorts in the S&P 500 (SPY) helped. I took profits on my last long there the previous week. (SDS), another short play, clawed back some losses.

We closed out up a blockbuster +4.55% in April and May is up +2.11%, taking my 2020 YTD return up to only -1.75%. That compares to a loss for the Dow Average of -18.20% from the February top. My trailing one-year return returned to 38.91%. My ten-year average annualized profit returned to +34.00%.

This week, Q1 earnings reports continue and so far, they are coming in much worse than the most dire forecasts. We also get the monthly payroll data, which should be heart-stopping to say the list.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, May 4 at 9:00 AM, the US Factories Orders for March are out and are expected to be disastrous. Berkshire Hathaway (BRK/B) and Eli Lilly (LLY) report.

On Tuesday, May 5 at 11:00 AM, the US Crude Oil Stocks are published and will be another bomb. Netflix (NFLX) and Coca-Cola (KO) report.

On Wednesday, May 6, at 7:15 AM, API Private Sector Employment Report is released. Lan Research (LRCX) and Electronic Arts (EA) announce earnings.

On Thursday, May 7 at 8:30 AM, another horrible Weekly Jobless Claims are out. Bristol Myers Squibb (BMY) reports.

On Friday, May 8, the April Nonfarm Payroll Report is printed, the worst unemployment rate since the Great Depression. AbbVie (ABBV) reports.

As for me, to battle cabin fever, I am setting up a tent in my back yard and staying there tonight, just to change the scenery. The girls need one more campout to qualify for camping merit badge, an important Eagle Scout one, and this will qualify.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader December 4 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: How do you see the markets playing out in 2020?

A: Well, I’m looking at small single-digit positive returns with a lot of volatility. Much of this year’s performance—30% in the S&P 500 (SPY), up 56% for the Mad Hedge Fund Trader—has already been pulled forward from 2020, thanks to super low interest rates and massive deficit spending. So, the more money we make now, the less money we make next year.

Q: How deep will the next recession be?

A: I’m looking for two quarters of small negative numbers like -0.1% or -0.2%, and then it’s off to the races again. That’s when the Golden Age of the Next Roaring Twenties starts, which I have already written a book about (click here).

And it’s possible we may not even see any negative numbers on a quarterly basis; we may just get close to zero, threatening it without actually breaking it. Of course, you could still get a 20% correction in the overall stock market if they only THINK we are going into recession, which has happened many times in the last 10 years.

Q: Are you expecting a market crash?

A: No; I do expect a meaningful pullback but frankly, right now, I do not see the conditions in place for that. None of the traditional causes of recessions, high-interest rates or high oil prices, are evident yet. The biggest threat to the market right now is the 2020 presidential election. And we are at a 14-year high in stock valuations.

Q: How bad will it get for car makers, and will the Tesla (TSLA) plant in Germany affect sales for European cars?

A: European carmakers have already been badly affected by Tesla, with Tesla taking over practically the entire luxury end of the market—that’s why companies like Mercedes, Audi and BMW are doing so badly with their shares, and they’re so far behind it’s unlikely they’ll ever catch up. The Berlin factory, I believe, is a battery factory, and after that, there will be a vehicle production factory, probably somewhere in eastern Europe where the cost basis is much lower.

Q: Double Line Capital’s CEO Jeff Gundlach says the US will get crushed in the next recession? Do you agree with him?

A: Well, my first advice to you is never take stock advice from a bond trader. Jeff Gundlach makes these spectacular forecasts, but the timing can be terrible. He can be wrong for 9 months before they finally turn. So, you can go out of business trading off of Jeff Gundlach’s stock advice, though his bond advice is valuable.

Q: Do you have any good recommendations for dividend stocks?

A: Yes, look at the entire cellphone towers REIT sector. That will be a growth sector next year with 5G rolling out and they have very high dividend yields. We’re going to get a significant increase in the number of cell towers thanks to 5G, and there are REITs specifically dedicated to cellphone towers. An example is Crown Castle (CCI), which has a generous 3.45% dividend yield.

Q: Are we in the final stages of a blow-off top for the stock market?

A: Yes, but blow-off tops can continue for many months, so don’t rush to sell short. However, next time the VIX gets down to 11, start buying six-month call options on the Volatility Index (VIX) at the $20 strike price. Go far out in the calendar to minimize time decay and far out of the money on strike prices to maximize your bang per buck.

Q: Gold had a nice day on Monday—is this the start of a reversal from the selling pressure?

A: No, as long as the market is pushing to new highs, which it seems to be doing—you don’t want to be anywhere near gold; wait for a better opening lower down.

Q: Are you sending Trade Alerts out on the Mad Hedge Biotech & Healthcare letter?

A: Not in the form that we see in Global Trading Dispatch or the Mad Hedge Technology Letter. Essentially, everything we’ve put out so far has been a long term buy. Most people know nothing about these sectors and we’re trying to get them into buyable names. So far, we’ve issued “BUYS” for 20 different companies; all of them have gone straight up. So, it’s really more of a long term buy-in hold situation. Since we’re in the very early days of the boom in biotech and healthcare stocks, you don’t want to leave money on the table with short term trade alerts for call spreads when there is a double or triple in the stock at hand. We are doing call spreads in the main market where most stocks are already at all-time highs in order to limit our risk.

Q: Fidelity just said that 50% of baby boomers who manage their own portfolio should rebalance it. What do you think is the best way to optimize my portfolio, as a baby boomer born in 1954?

A: You should always rebalance every year, especially when you get enormous moves in single sectors. The interesting thing this year is that everything went up, so you may not need to rebalance that much. When I say rebalance, I’m referring to rebalancing your weightings of stocks vs bonds. If you’re over 50, you want to have roughly a 50/50 ratio on those. That would suggest pairing back some of your equity weightings, increasing your bond weighting because stocks (SPY) (30% total return) have risen a lot more than bonds (TLT) (19% total return) this year.

Q: Marijuana stock Tilray (TLRY) has just had a pitiful year going from $100 to $20 and missed earnings targets for 4 for straight quarters. Could this go to zero?

A: Yes; after all, how hard is it to grow a weed? I never bought the story on the whole marijuana sector, not only because they are not allowed to participate in the financial sector. It’s an all-cash business; you hear about people moving around suitcases full of $100 bills doing deals in Oakland and Denver. I believe anybody can do this. My real estate agent is quitting his business to go into cannabis farming. Additionally, they’re getting a lot of competition from the black market where everybody used to buy their marijuana because it’s tax-free. There’s about a 40% price difference between the tax-paying legal form of marijuana and the tax-free black market where people used to get their marijuana. There’s no great value added there. It’s not like they’re designing a 96 stack microprocessor.

Q: What do you think about Ali Baba (BABA), the Chinese internet giant?

A: I love it long term. Short term, it will be subject to trade war gyration; so use the big dips to buy into it because long term we come out of this.

Global Market Comments

November 15, 2019

Fiat Lux

Featured Trade:

(NOVEMBER 13 BIWEEKLY STRATEGY WEBINAR Q&A),

(FCX), (TSLA), (FXI), (SPY), (AAPL), (M), (BA), (TLT)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader November 13 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Has the multiyear decline in commodities ended, such as for Freeport McMoRan (FCX)?

A: Yes, for the short term. However, we will almost certainly have another recession scare—or even election scare—sometime next year. That will cause a retest of the recent lows in commodities. The volatility will continue, but the long-term trend is up. The next recession will likely be so short that people will start discounting the recovery now. If you’re only looking for a 2-quarter recession and have a long-term view of your stocks, you probably want to use any kind of dips to buy now. A lot of the recent buying in Tesla (TESLA), by the way, has been of that nature.

Q: Will the US eventually drop all tariffs on Chinese imports (FXI), or do you see the US raising them?

A: I think eventually they will solve the trade war next year, right in front of the election—maybe June/July/August—so that Trump has something to run on. It’s too early to solve it now for political purposes. The whole trade war was essentially designed to depress the economy and then bring in Trump as the savior right before the election, and that has all tariffs disappearing sometime next year. By the way, some of the buying in the market now is discounting the end to the uncertainty of the trade war. So, either that or it ends when Trump leaves office—in either case, that’s 15 months off. Many big institutions think in timeframes much longer than that.

Q: Can the US consumer bring us through the holiday season to have equities (SPY) finish at all-time highs?

A: Yes, they can; I thought we might get a dip to trade off of in Oct/Nov, but we haven't gotten it. It’s looking more and more like a melt-up into year-end, even though it’s a slow-motion melt-up of 50 or 100 points a day.

Q: Will Apple (AAPL) keep going up every day forever?

A: No, don’t forget that Apple can have 40% pullbacks at any time without warning. Usually, they happen with new product launches. I would think we’re getting overextended here. If we somehow get a 10% or 20% pullback in Apple next year, I’d be jumping back into that for the product launch next September when we’ll likely hit $200, which has been my target for Apple for a very long time.

Q: Is it time to make a short term buy of beaten-down retail names like Macy’s (M)?

A: No, I am a person who trades with the long-term trend at all times. Most people are not agile or smart enough to do counter-trend trades and make money, and the risk/reward is also terrible—you make a mistake, you get killed on those. I think this company’s having a going-out-of-business sale, unless we enter a major increase in economic growth in this country, which is nowhere in the cards. If anything, I’m looking for a sharp rally to sell into. Macy’s might want to test that 200-day moving average up there at $20 at some point; that would be a great selling place. But no, we don’t want to touch the retailers right here, and retailers have been very kind to us this year on the short side.

Q: Do you see the United States US Treasury Bond Fund (TLT) as a safe-haven buy at today’s prices, or are bonds overpriced?

A: I think we’re getting the safe-haven bid as a hedge against stocks selling off. Wildly overbought Mad Hedge Market Timing Indexes are also great places to buy bonds because when you finally get the correction in the stock market, money piles into bonds, and you want to be buying the (TLT) before it does that.

Q: Is Boeing (BA) a short for the next 6 months?

A: No, I think the short play on Boeing is over. If we do get another run down to $325, take it as a gift and load the boat. I think the next major move in Boeing is to $400. Buy the dips.

Q: Do you think the Fed will cut one more time before the year is over, or will they hold off?

A: They will hold off—Powell said as much in this morning’s speech. He really said that not only will there be no more cuts this year, but next year as well, because we are essentially eating our seed corn when it comes to the next recession if we do cut rate because that means there will be no tools with which to get out of the recession.

Q: Are you seeing stocks rising to the end of the year, into the first of next year? If so, will there be a pullback during November before a final rise?

A: Yes we are seeing stocks rise to the end of the year; and you would think we will see some kind of pullback, but we have so much liquidity chasing so few stocks now, any pullbacks may be limited.

Q: (TLT) is called the iShares Barclay 20+ year bond fund. In your trade alerts, you talk about 10-year yields. How are the 10-year yields linked to the (TLT)?

A: There isn't a liquid 10-year bond ETF. There are ETFs but they’re fairly illiquid, so I put everyone into the 20-year (TLT) purely for liquidity reasons.

Q: What about going outright long on the (TLT)?

A: That’s not a bad option; the only problem with outright longs is you make no money if we grind sideways for a while, whereas with the options trade, you get in all the time decay. And we only did the December's, which have about 27 days left in them in trading time.

Q: Tesla just announced it will open a Berlin factory—what does this mean for Tesla and the share providers?

A: Well, it creates the means by which Tesla can increase its production from 400,000 cars this year to 5,000,000 cars a year in 10 years. And it’s just one other factory; expect more to come. Interestingly, their first choice was actually Great Britain, but Brexit scared them out of there.

Q: Do you think Silicon Valley should be a judge on political advertising?

A: I think Silicon Valley should not allow publication of obviously false content which they do now. That’s something the mainstream media are not allowed to do or they will get fined by the Federal Communications Commission. That ban does not apply to social media companies like Facebook (FB) and Twitter (TWTR) but should be as they are vastly more powerful than conventional media. Without it, you'll continue to see massive amounts of false information put out on the Internet. I can see the fake info clearly, but most can’t. I saw a statistic yesterday saying that roughly 50% of all information you read on the internet is false.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 18, 2019

Fiat Lux

Featured Trade:

(OCTOBER 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPX), (C), (GM), (IWM), ($RUT), (FB),

(INTC), (AA), (BBY), (M), (RTN), (FCX), GLD)