There comes a time in every trader’s life when it’s time to face harsh reality and admit that you’re just dead wrong.

As much as I thought a I had strong case for the best stocks to move sideways before continuing their upward drive, the markets decided otherwise. One thing I have learned over my half-century of trading is that you never argue with Mr. Market. He is always right.

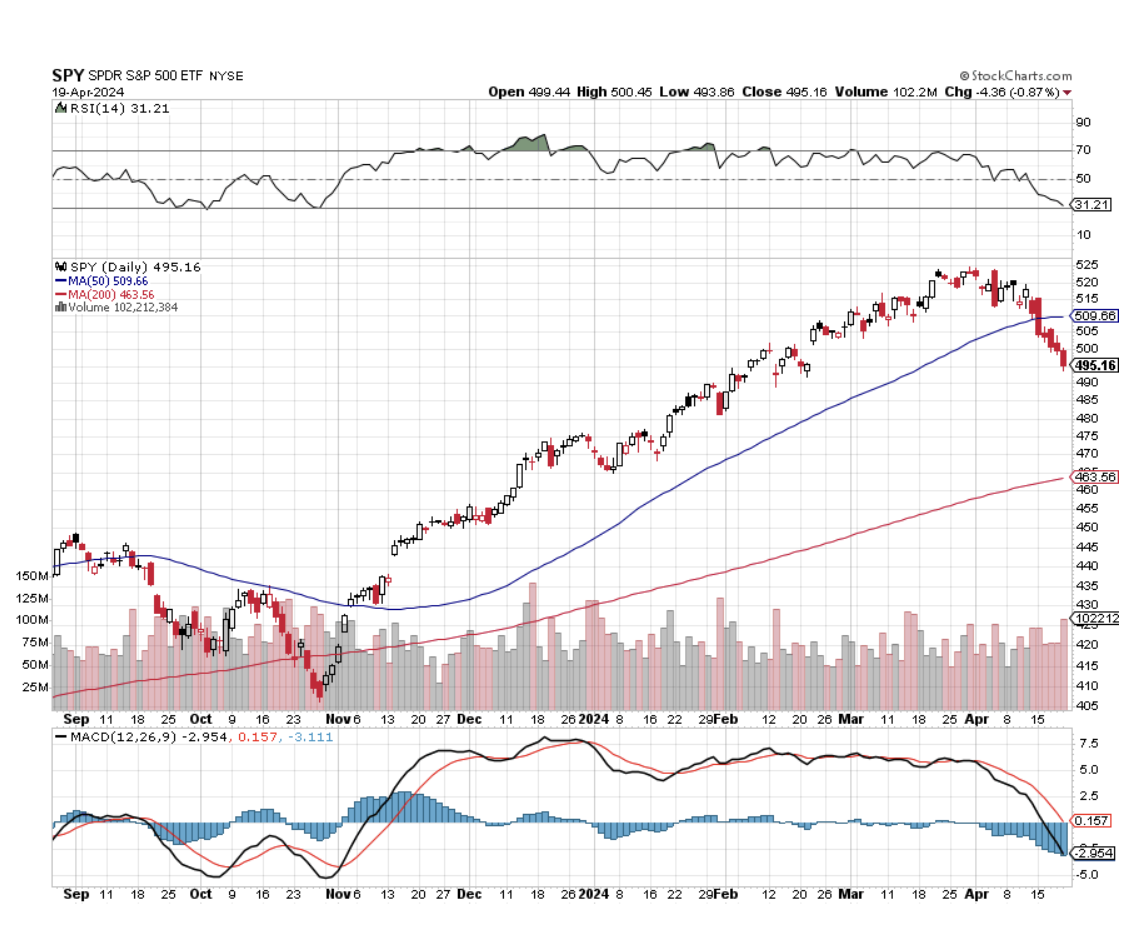

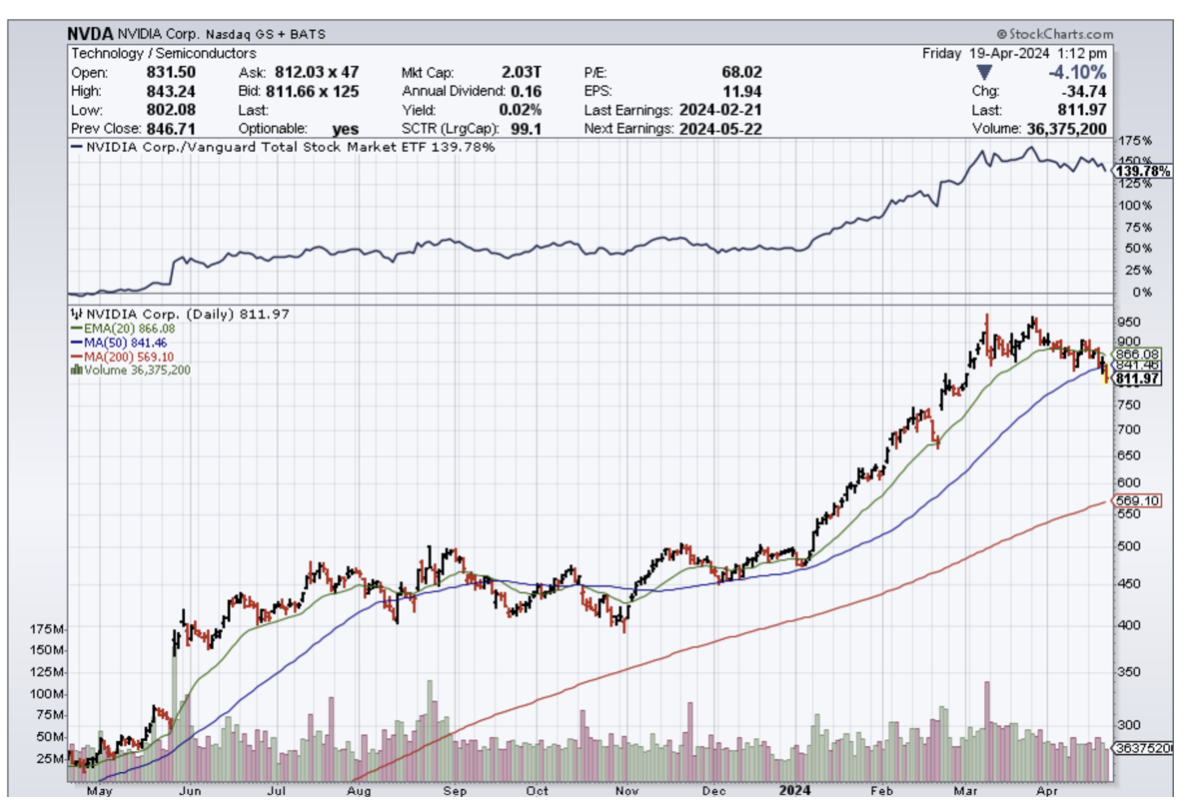

So it was with some dismay that on Friday, I watched NVIDIA (NVDA) shares slice through its 50-day moving average at $840 like a hot knife through butter putting the shares into a free-fall. Virtually the next print was the low of the day at $760, down 10% on the day.

There was no new news about (NVDA). Its prospects look as bright as ever, and there are a series of conferences of earnings reports over the coming month to remind us of that. But sometimes, the market just doesn’t care.

(NVDA) has had a great run, up some 144% since October. During this time, I executed a dozen profitable long-side trades. But when you’re that aggressive you know in advance that the last trade is going to kill you and that is the case today. (NVDA) is falling because of the sheer weight of its price.

New flash: while (NVDA) is still the cheapest big tech stock in the market, cheap stocks can get cheaper as we all know.

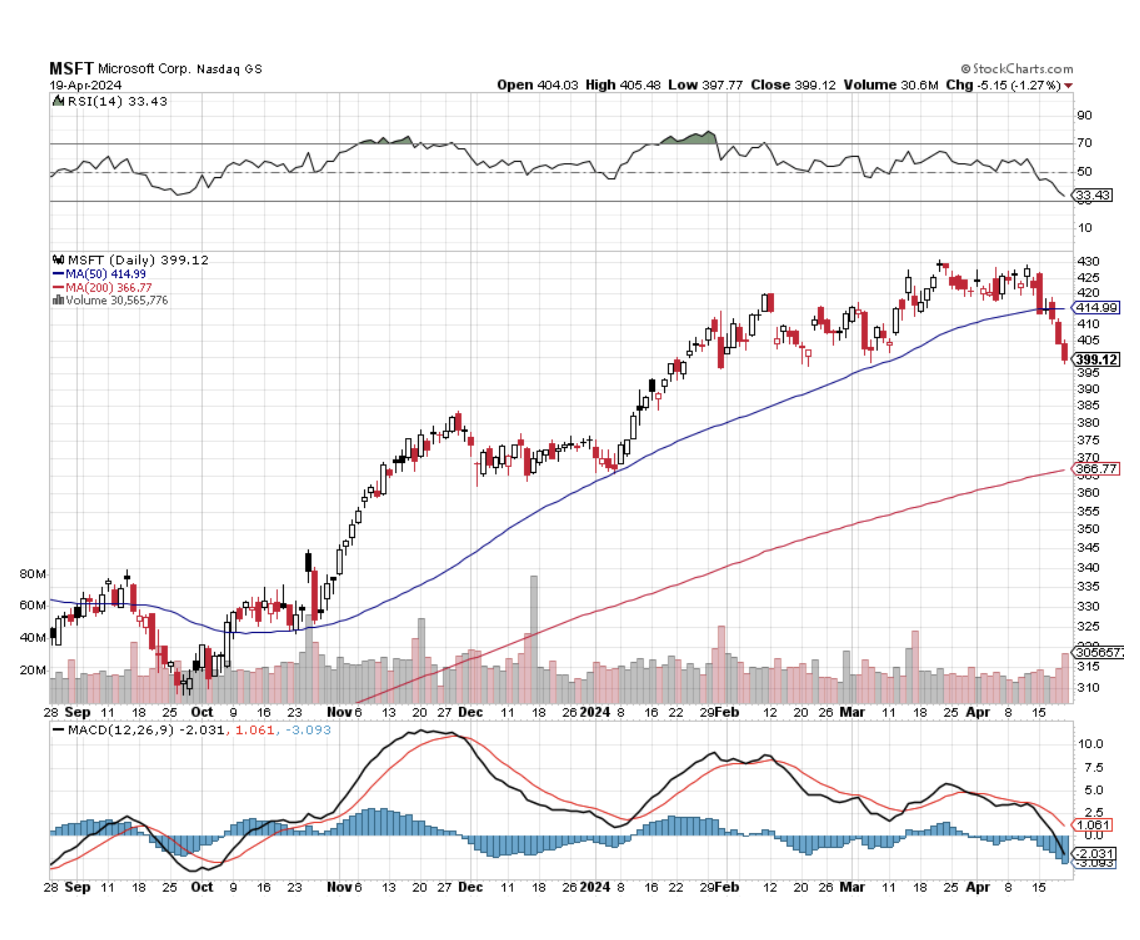

With the advantage of 20/20 hindsight, I should have been paying more attention to the Magnificent Seven 50-day moving averages which have been falling like dominoes. First went Tesla (TSLA) in February and Apple in March. The S&P 500 (SPY) gave it up on Monday and Microsoft (MSFT) on Wednesday. Amazon (AMZN), (META), and (NVDA) were the last to go on Friday.

Sure you can blame the April 19 option expiration when traders were loaded to the hilt with expiring longs with all these stocks they had to dump. The dreaded month of May, when traders go to die, and the summer doldrums are just two weeks away. Algorithms poured gasoline on the fire exaggerating the moves, as they always do. But still, wrong is wrong.

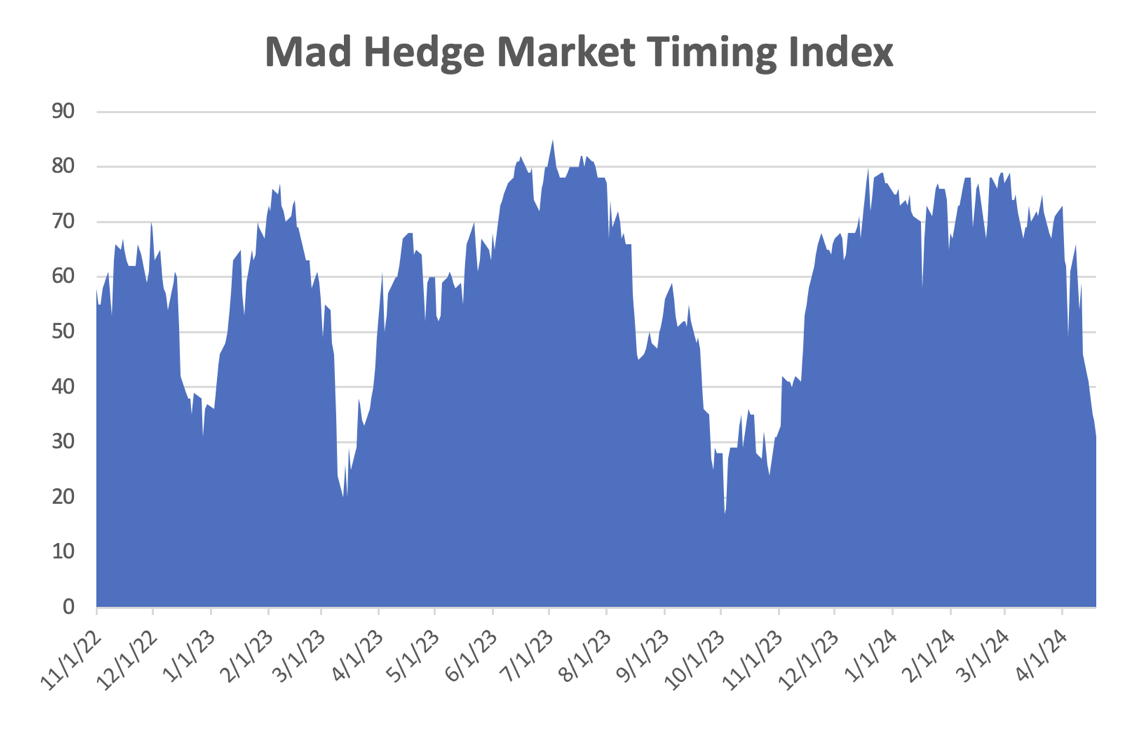

And there’s my mea culpa for 2024. I am human after all. I’m not right all the time, I just act like it. If the horrific market action last week has one silver lining, it’s that it sets up the next great trades, for which there will be many. With my Mad Hedge AI Market Timing Index down to a lowly 31 that may not be far off.

Your next question is “How far down is down?” In the worst-case scenario, the 200-day moving average is in play for all of these. That is pegged at $463 for the S&P 500, $569 for (NVDA), $377 for (MSFT), $150 for (AMZN), and $308 for (META). (AAPL) and (TSLA) already lost their 200-days a long time ago. In other words, the market is in the process of giving up all its 2024 gains and then some.

Sure, the 200 days are all rising sharply so it's unlikely we’ll hit these dire numbers. Still, it's best to prepare your boss for the worst and then let serendipity work its magic.

Remarkably, my commodity and precious metal stocks, where I had eight of ten long positions, stuck to the script and moved sideways instead of down. If you throw bad news on a stock and it refuses to fall, you buy the hell out of it. So that will be my next move in the market, once I clean all the mud off my face and pull the arrows out of my rear.

Those of us who have been trading gold for a long time, I’ve been doing it for 50 years and 60 if you count the Kennedy silver dollars I collected, will tell you that this new bull market in the barbarous relic is a very strange one.

None of the traditional factors that drive gold up are present. Interest rates have lately been rising, not falling. ETF financial demand fell all last year, and much of that money was diverted to Bitcoin. Retail demand, especially from Asia, has also been falling off a cliff. Gold miners have in no way been leading the price of the yellow metal because of their excess leverage as they usually do. But gold has seen a 34% rally off the October low.

Go figure.

It turns out that central bank buying has increased dramatically, especially from China, enough to offset all the other no-shows. The conflict in the Middle East is also drawing in more flight to safety demand. The good news is that the Chinese buying will continue. The bad news is that this might be a precursor to the invasion of Taiwan as it flees the Western financial system.

What does all this mean? When the traditional demand for gold returns, interest rates, ETFs, and retail, the price of gold will move a lot higher. The barbarous relic can easily reach $2,800 this year and possibly $3,000. The miners will play catch up. Buy (GLD) on dips and silver (SLV) as well, which has a lot of catching up to do.

I just thought you’d like to know.

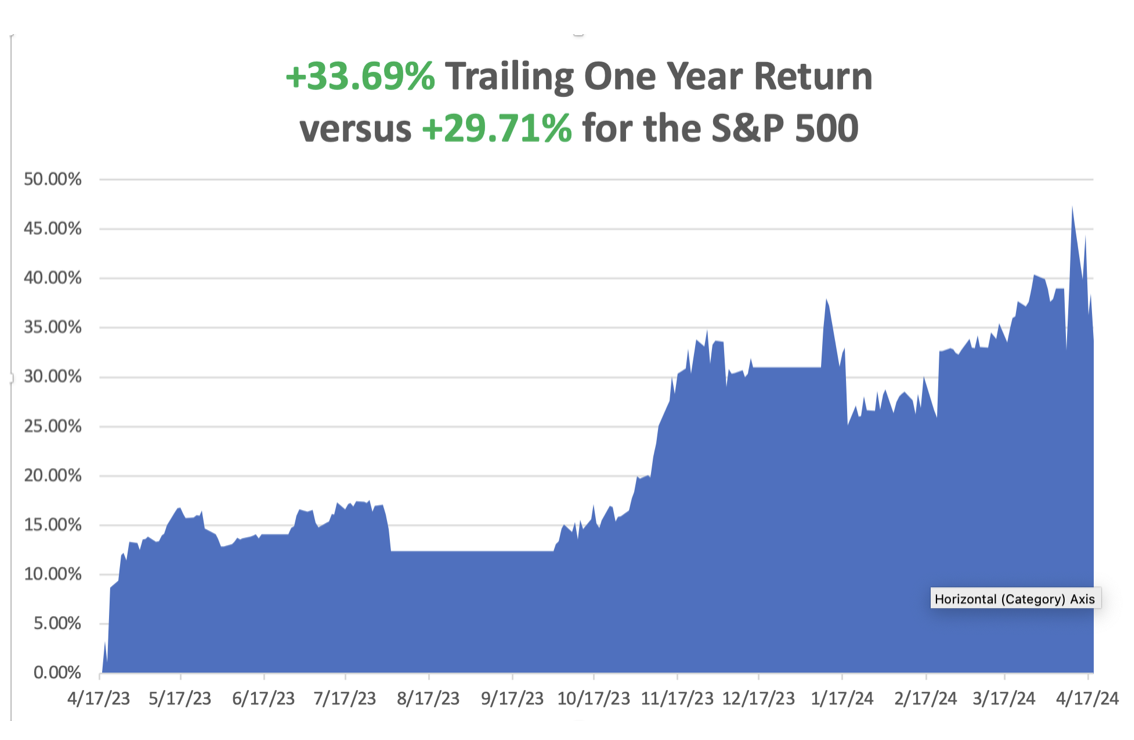

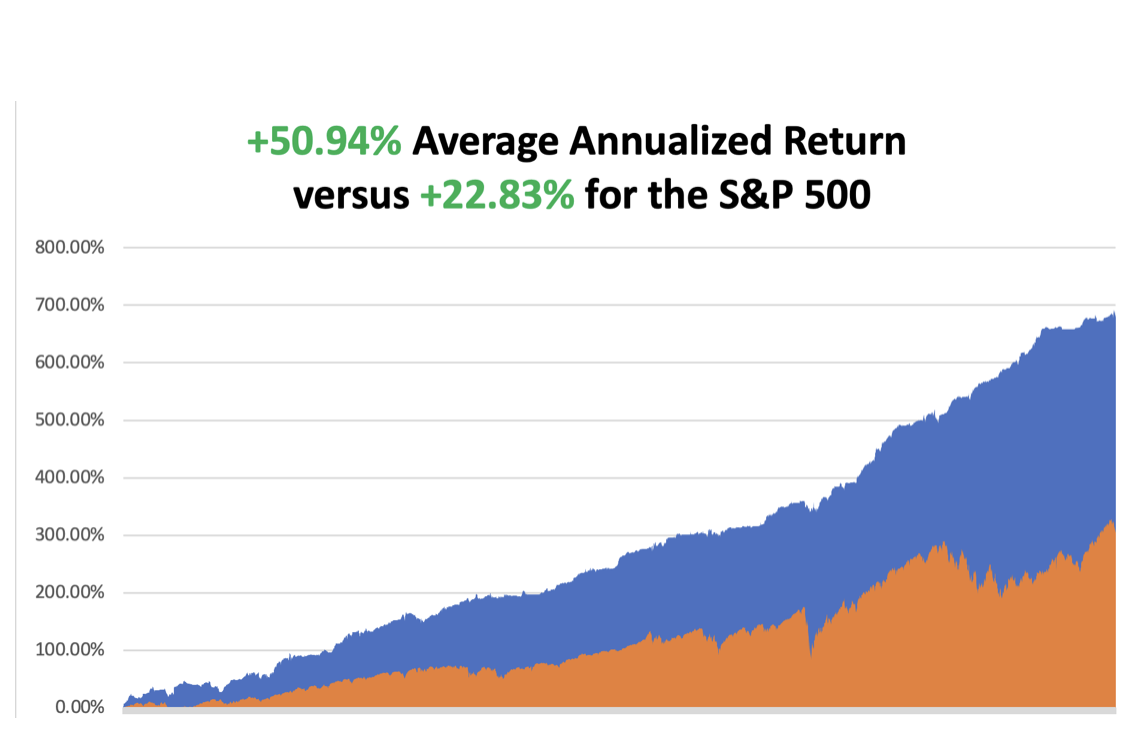

So far in April, we are down a heartbreaking -6.69%. My 2024 year-to-date performance is at +14.47%.The S&P 500 (SPY) is up +2.68%so far in 2024. My trailing one-year return reached +33.69% versus +29.71% for the S&P 500. That brings my 16-year total return to +676.63%.My average annualized return has recovered to +50.94.

Some 63 of my 70 round trips were profitable in 2023. Some 20 of 28 trades have been profitable so far in 2024.

I stopped out of my long in Tesla last week at cost, expecting further downside, which happened. A week early the position had been at max profit. I let my April longs expire at a max profit on April 19 in Freeport McMoRan (FCX), Occidental Petroleum, ExxonMobile (XOM), Wheaton Precious Metals (WPM), and Gold (GLD).

That leaves me with my remaining May longs in (TLT) and (FCX) a double long in (NVDA) and 60% in cash. Volatility Index ($VIX) Hits Six-Month High, on threats of a New Iran War, Oil Supply Cut-offs, and topping stocks. It’s been a long and dry desert crossing, but we are finally back to reach the $20 handle. The volatility trade is back. For a double bonus, the Mad Hedge Market Timing Index also dropped below 50 for the first time since October. Options traders will love it!

Junk Bonds See Biggest Outflows in a Year, as the Federal Reserve’s hawkish approach to inflation makes investors wary, sending yields soaring to 6.33%. Yields won’t peak until the Fed actually cuts rates. Buy (JNK) and (HYG) on dips.

Netflix (NFLX) Adds 9.33 Million New Subscribers, nearly double analyst forecasts, including my five kids who aren’t allowed to share my password anymore. But the shares dropped on weak Q2 guidance. Netflix has rebounded from a slowdown in 2021 and 2022 to grow at its fastest rate since the early days of the coronavirus pandemic. That is due in large part to its crackdown on people who were using someone else’s account. The company estimated more than 100 million people were using an account for which they didn’t pay.

Mortgage Rates Top 7.0% for the first time in 2024, adding dead weight to the housing market. Most borrowers are now taking out adjustable 5/1 ARMS and then praying for a Fed rate cut later this year.

Existing Home Sales Dive by 4.3% in March to 4.19 million units on a sign-contract basis. Inventories rose 4.47% to a 3.2-month supply, up 14% YOY. The median price of an existing home sold in March was $393,500, up 4.8% from the year before. Regionally, sales fell everywhere except in the North, where they rose 4.2% month-to-month. Sales fell hardest in the West, down 8.2%. Prices are highest in the West. Housing Starts Plunge, down 14.5% in March. Permits for future construction of single-family houses fell to a five-month low. Residential investment rebounded in the second half of 2023 after contracting for nine straight quarters, the longest such stretch since the housing market collapse in 2006. But the recovery appears to be losing steam. China Surprises with Q1 GDP Growth at 5.3%, but who knows how real these numbers really are? They don’t line up with individual data like international trade. Peak China is behind us. Avoid (FXI).

Tariff Wars Heat Up, US President Joe Biden is threatening China again, and this time he wants to triple the China tariff rate on steel and aluminum imports. On Wednesday, the president will visit the United Steelworkers headquarters in Pittsburgh and has vowed his saber-rattling is not just empty threats. His rhetoric on China could make relations between the US and the Middle Kingdom that much frostier as we enter into the heart of the US election race.

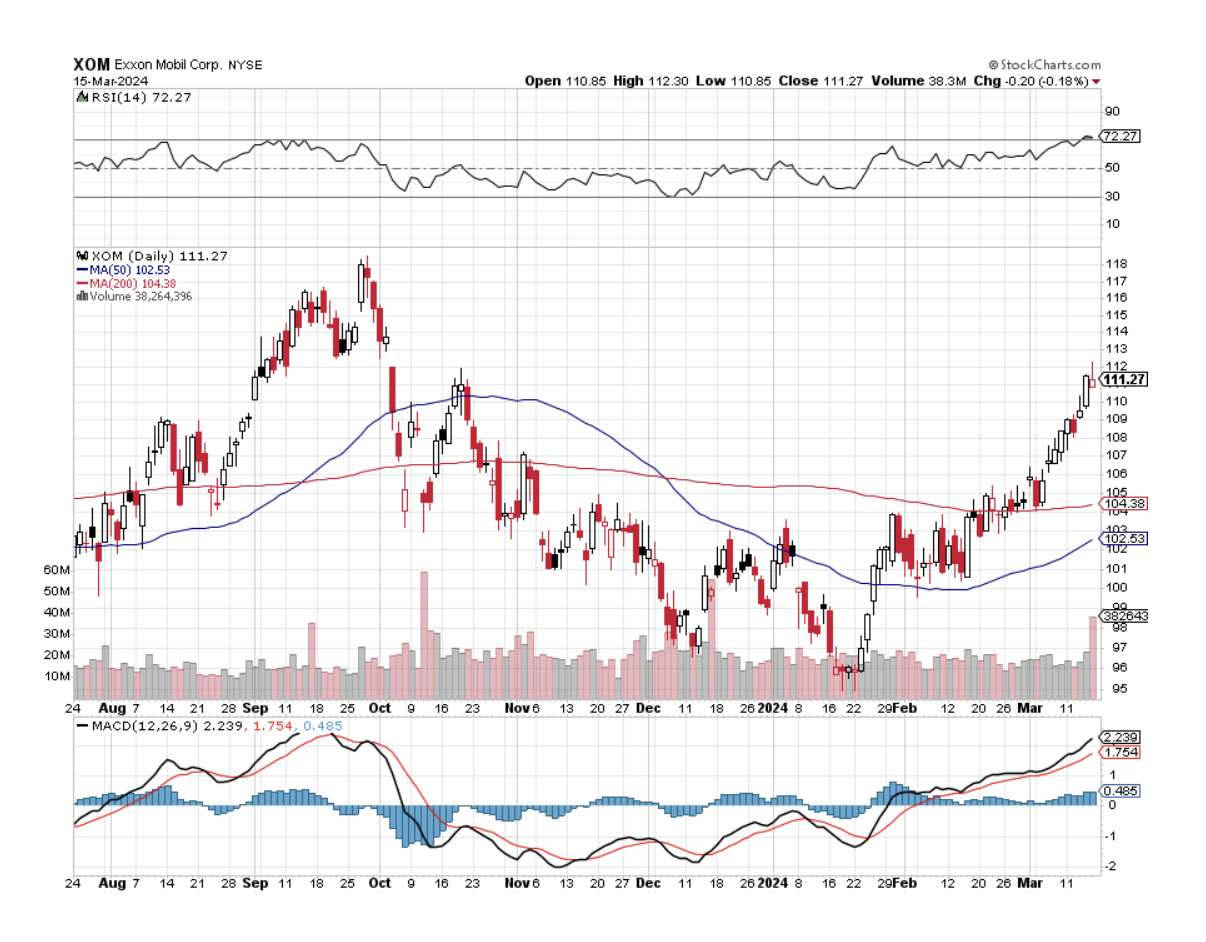

Biden Boosts the Cost of Alaska Oil Drilling Leases, from $10,000 to $160,000, the first increase since 1920. There is also a bump in the royalty on extracted oil, from 12.25% to 16.27%. The government is no longer giving away oil found on its land for free. Coddling of the oil companies is over. Oil companies will no longer bid for cheap oil leases with the intention of sitting on them for decades. The US is currently the largest oil (USO) producing country in history at 13 million barrels/day and hardly needs any subsidies, which date back to the Great Depression. Buy energy stocks on dips, like (XOM) and (OXY), which are posting record profits.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, April 22, at 7:00 AM EST, the Chicago Fed National Activity Index is announced.

On Tuesday, April 23 at 8:30 AM, New Home Sales are released.

On Wednesday, April 24 at 2:00 PM, Mortgage applications come out.

On Thursday, April 25 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, April 26 at 8:30 AM, Consumer Expectations. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I spent a decade flying planes without a license in various remote war zones because nobody cared.

So, when I finally obtained my British Private Pilot’s License at the Elstree Aerodrome, home of the WWII Mosquito twin-engine bomber, in 1987, it was cause for celebration.

I decided to take on a great challenge to test my newly acquired skills. So, I looked at an aviation chart of Europe, researched the availability of 100LL aviation gasoline in Southern Europe, and concluded that the farthest I could go was the island nation of Malta.

Caution: new pilots with only 50 hours of flying time are the most dangerous people in the world!

Malta looms large in the history of aviation. At the onset of the Second World War, Malta was the only place that could interfere with the resupply of Rommel’s Africa Corps, situated halfway between Sicily and Tunisia. It was also crucial for the British defense of the Suez Canal.

So, Malta was mercilessly bombed, at first by Mussolini’s Regia Aeronautica, and later by the Luftwaffe. By April 1942, the port at Valletta became the single most bombed place on earth.

Initially, Malta had only three obsolete 1934 Gloster Gladiator biplanes to mount a defense, still in their original packing crates. Flown by volunteer pilots, they came to be known as “Faith, Hope, and Charity.”

The three planes held the Italians at bay, shooting down the slower bombers in droves. As my Italian grandmother constantly reminded me, “Italians are better lovers than fighters.” By the time the Germans showed up, the RAF had been able to resupply Malta with as many as 50 infinitely more powerful Spitfires a month, and the battle was won.

So Malta it was.

The flight school only had one plane they could lend me for ten days, a clapped-out, underpowered single-engine Grumman Tiger, which offered a cruising speed of only 160 miles per hour. I paid extra for an inflatable life raft.

Flying over the length of France in good weather at 500 feet was a piece of cake, taking in endless views of castles, vineyards, and bright yellow rapeseed fields. Italy was a little trickier because only four airports offered avgas, Milan, Rome, Naples, and Palermo. Since Italy had lost the war, they never experienced a postwar aviation boom as we did.

I figured that if I filled up in Naples, I could make it all the way to Malta nonstop, a distance of 450 miles, and still have a modest reserve.

Flying the entire length of Italy at 500 feet along the east coast was grand. Genoa, Cinque Terra, the Vatican, and Mount Vesuvius gently passed by. There was a 1,000-foot-high cable connecting Sicily with the mainland that could have been a problem, as it wasn’t marked on the charts. But my US Air Force charts were pretty old, printed just after WWII. But I spotted them in time and flew over.

When I passed Cape Passero, the southeast corner of Sicily, I should have been able to see Malta, but I didn’t. I flew on, figuring a heading of 190 degrees would eventually get me there.

It didn’t.

My fuel was showing only a quarter tank left and my concern was rising. There was now no avgas anywhere within range. I tried triangulating VORs (very high-frequency omnidirectional radar ranging).

No luck.

I tried dead reckoning. No luck there either.

Then I remembered my WWII history. I recalled that returning American bombers with their instruments shot out used to tune in to the BBC AM frequency to find their way back to London. Picking up the Andrews Sisters was confirmation they had the right frequency.

It just so happened that buried in my pilot’s case was a handbook of all European broadcast frequencies. I looked up Malta, and sure enough, there was a high-powered BBC repeater station broadcasting on AM.

I excitedly tuned in to my Automatic Direction Finder.

Nothing. And now my fuel was down to one-eighth tanks and it was getting dark!

In an act of desperation, I kept playing with the ADF dial and eventually picked up a faint signal.

As I got closer, the signal got louder, and I recognized that old familiar clipped English accent. It was the BBC (I did work there for ten years as their Tokyo correspondent).

But the only thing I could see were the shadows of clouds on the Mediterranean below. Eventually, I noticed that one of the shadows wasn’t moving.

It was Malta.

As I was flying at 10,000 feet to extend my range, I cut my engines to conserve fuel and coasted the rest of the way. I landed right as the sun set over Africa.

While on the island, I set myself up in the historic Excelsior Grand Hotel. Malta is bone dry and has almost no beaches. It is surrounded by 100-foot cliffs. I paid homage to Faith, the last of the three historic biplanes, in the National War Museum in Valetta.

The other thing I remember about Malta is that CIA agents were everywhere. Muammar Khadafy’s Libya was a major investor in Malta, recycling their oil riches, and by the late 1980s owned practically everything. How do you spot a CIA agent? Crewcut and pressed, creased blue jeans. It’s like a uniform. What they were doing in Malta I can only imagine.

Before heading back to London, I had to refuel the plane. A truck from air services drove up and dropped a 50-gallon drum of avgas on the tarmac along with a pump. Then they drove off. It took me an hour to hand pump the plane full.

My route home took me directly to Palermo, Sicily to visit my ancestral origins. On takeoff to Sardinia, wind shear flipped my plane over, caused me to crash, and I lost a disk in my back.

But that is a story for another day.

Who says history doesn’t pay!

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

“Faith”

The Andrews Sisters

Spitfire

Grumman Tiger

https://www.madhedgefundtrader.com/wp-content/uploads/2024/04/andrews-sisters.png582506april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-04-22 09:02:302024-04-22 12:00:50The Market Outlook for the Week Ahead, or Facing Harsh Reality

It’s been a slap in the face lately in the tech market as the market has realized that rate cuts are not imminent.

The party is over in the short term until a catalyst re-ignites the bull market rally.

The softness has put a real dent into the momentum and trajectory of tech stocks.

Now we are confronted with the sad reality that inflation is here to stay because hot report after hot report is confirming tech investors' greatest fear, that inflation is not transitory like the Fed once said.

In fact, inflation has been a serious problem now for over 4 years and the same Fed that botched the transitory inflation issue is still in charge.

My bet is that they won’t ease prematurely with all the heat they received from the failed transitory inflation call.

Yet here we are with the tech market selling off in the short-term and healthily pulling back.

Even AI chip stock Super Micro Computer (SMCI) is back around $750 per share after skyrocketing past $1,200 per share.

The froth for now is ebbing.

Readers had to expect that a consolidation of some kind was in the cards and that is what we are going through right now.

In the near term, earnings are our best hope for a positive catalyst to offset all the negativity about inflation and interest rates.

There is a good chance we don’t even get one rate cut this year with all the hot job numbers, because the data is just too good to ignore.

In the recent stretch of the bull run, investors looked past higher rates, based in part on their belief that policy cuts were around the corner.

With wage growth starting to cool and excess savings draining, asset markets have seemingly stepped in to help sustain US consumption, adding more than $10 trillion to household net worth in the past year.

Companies need to show that they’re capitalizing on economic strength to expand earnings.

The tech market needs to show in the upcoming earnings season that the artificial intelligence optimism that started with the launch of ChaptGPT is more than hype.

Not all earnings outlooks are created equal, of course, and one can imagine a scenario in which AI darlings Nvidia and Microsoft fan optimism.

Consensus is that we will experience about 5% earnings growth for the S&P 500 from the same period last year excluding the volatile energy sector.

Meanwhile, the economy probably grew about 2.9% in the first quarter, according to the Atlanta Fed’s GDP Now tracker, and that should translate into encouraging earnings and outlooks.

I am of the opinion that all the heavy lifting will be done by several tech behemoths that also double-dip in the AI narrative.

This has also created a massive vacuum of weakness after the likes of MSFT and NVDA.

The narrowness of leadership is a result of a winner takes all of the economy and just several corporations consolidating at the top.

Competition is so fierce that it has left Apple and Tesla by the wayside.

We will reach that 5% earnings growth, but strip out a few tech stocks, and that number is likely to be flat or minus.

I believe the narrowness of leadership will be a hallmark of the future bull market and not just some one-off exception.

Some readers have no idea how ultra-competitive it is at the top of the stock market pyramid with companies fighting for the incremental investment dollar.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-04-19 14:02:362024-04-19 15:29:42Tech Earnings Is The Next Catalyst

Intel (INTC) is an intriguing chip company that has been around for a long time but has seldom been at the vanguard of the tech movement.

Until now…

Remember the US government is pouring dollars at the tune of billions upon billions into the domestic semiconductor industry to maintain a competitive advantage that is quickly being challenged by China.

Intel could solidify itself as a real tech player if it can figure out the foundry business which has been largely ineffective as of late.

Even if the foundry business is a big-time loss maker right now, Intel is laying the groundwork to become a strategically important company to the US government and US tech industry in 5 years.

Government dollars are usually viewed as a more stable stream of revenue.

It’s true that Intel is better known for designing its own chips, but that type of barrier to entry isn’t as high as foundry production.

Many chip companies aren’t interested in the production of what they design, because of the capital-intensive nature of the process.

It’s easier to outsource designs and just collect the product after.

Intel shares fell 4% last Tuesday after the company revealed long-awaited financials for its semiconductor manufacturing business or foundry business.

Intel said its foundry business recorded an operating loss of $7 billion in 2023 on sales of $18.9 billion. That’s a wider loss than the $5.2 billion Intel reported in its foundry business in 2022 on $27.5 billion in sales.

It has been pitching investors to double down on an external foundry business to make chips for other companies.

In theory, it sounds promising.

Intel’s role as one of the only U.S. companies doing cutting-edge semiconductor manufacturing on American soil was a big reason it secured nearly $20 billion in CHIPS and Science Act funding last month.

Its management said that it expected its foundry’s losses to peak in 2024 and eventually break even “midway” between this quarter and the end of 2030.

The company previously said that Microsoft (MSFT) would use its foundry services and that it has $15 billion of revenue for the foundry already booked.

The foundry business at Intel will ostensibly drive larger revenue momentum each approaching year to 2030.

Granted, it doesn’t take one day for chip production to come online, but the contract signed with Microsoft is a positive signal that will likely lead to other behemoths inking deals.

Intel even admitted that the lack of profitability in the foundry business from the past was correctable through better focus and execution.

I do believe Intel morphing into a multi-dimensional chip company is highly supportive of a higher share price only if they can get a handle on expense control.

Many times companies go too big with the government subsidies and need even more subsidies to dig themselves out of a hole.

I don’t believe that will be the case with Intel’s foundry business and installing a concrete plan has gone a long way to soothe investor fear.

The stock was crushed in 2020 and hit a nadir of $25 per share in 2023.

Intel shares then reversed and doubled to around $50 per share.

They have now settled in the high $30 range and I do believe any dips should be bought and held long-term.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-04-08 14:02:142024-04-08 16:22:09Branching Out

Ignore the lessons of history, and the cost to your portfolio will be great. Especially if you are a bond trader!

Meet deflation, upfront and ugly.

If you look at a chart for data from the United States consumer prices are rising at an annual 3.2% rate. The long-term average is 3.0%.

This is above the Federal Reserve’s own 2.0% annual inflation target, with most of the recent gains coming from housing costs.

We are not just having a deflationary year or decade. We may be having a deflationary century.

If so, it will not be the first one.

The 19th century saw continuously falling prices as well. Read the financial history of the United States, and it is beset with continuous stock market crashes, economic crises, and liquidity shortages.

The union movement sprung largely from the need to put a break on falling wages created by perennial labor oversupply and sub-living wages.

Enjoy riding the New York subway? Workers paid 10 cents an hour built it 125 years ago. It couldn’t be constructed today, as other more modern cities have discovered. The cost would be wildly prohibitive. Look no further than the California Bullet Train, now expected to cost $100 billion. A second transbay tube in San Francisco will cost $29 billion.

The causes of the 19th-century price collapse were easy to discern. A technology boom sparked an industrial revolution that reduced the labor content of end products by ten to a hundredfold.

Instead of employing 100 women for a day to make 100 spools of thread, a single man operating a machine could do the job in an hour.

The dramatic productivity gains swept through the developing economies like a hurricane. The jump from steam to electric power during the last quarter of the century took manufacturing gains a quantum leap forward.

If any of this sounds familiar, it is because we are now seeing a repeat of the exact same impact of accelerating technology. Machines and software are replacing human workers faster than their ability to retrain for new professions. If you want to order a Big Mac at McDonald’s these days, you need a PhD in Computer Science from MIT. The new stores have no humans to take orders.

This is why there has been no net gain in middle-class wages for the past 40 years. That is until the pandemic hit which created labor shortages that are still working their way out. It is the cause of the structurally high U-6 “discouraged workers” employment rate, as well as the millions of millennials still living in their parent’s basements.

To the above add the huge advances now being made in healthcare, biotechnology, genetic engineering, DNA-based computing, and big data solutions to problems. Did anyone say “AI”?

If all the major diseases in the world were wiped out, a probability within 10 years, how many healthcare jobs would that destroy?

Probably tens of millions.

So the deflation that we have been suffering in recent years isn’t likely to end any time soon. In fact, it is just getting started.

Why am I interested in this issue? Of course, I always enjoy analyzing and predicting the far future, using the unfolding of the last half-century as my guide. Then I have to live long enough to see if I’m right.

I did nail the rise of eight-track tapes over six-track ones, the victory of VHS over Betamax, the ascendance of Microsoft (MSFT) operating systems over OS2, and then the conquest of Apple (AAPL) over Motorola. So, I have a pretty good track record on this front.

For bond traders especially, there are far-reaching consequences of a deflationary century. It means that there will be no bond market crash, as many are predicting, just a slow grind up in long-term bond prices instead.

Amazingly, the top in rates in this cycle only reaches the bottom of past cycles at 5.49% for ten-year Treasury bonds (TLT), (TBT).

The soonest that we could possibly see real wage rises will be when a generational demographic labor shortage kicks in during the late2020s.

I say this not as a casual observer, but as a trader who is constantly active in an entire range of debt instruments.

I just thought you’d like to know.

Hey, Have You Heard About John Deere?

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/john-thomas-08.jpg400400MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2024-03-20 09:02:142024-03-20 09:57:37Welcome to the Deflationary Century

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE BIG ROTATION IS ON),

(SNOW), (FCX), (XOM), (TLT), (ALB), (NVDA), (MSFT), (AAPL), (META), (GOOGL), (GOLD), (WPM), (UNP) (FDX), (UNG)

Here is the only statistic you need to know right now.

If NVIDIA (NVDA) continues growing at the same rate it has for the last year it will be larger than the entire global economy by 2030, about $100 trillion, up from the current $2 trillion.

Which suggests that it might not actually achieve that lofty goal. Others have reached the same conclusion as I and the stock held up remarkably well in the face of absolutely massive profit-taking last week.

I have been through past market cycles when other stocks seemed to want to go to infinity. There was Apple (AAPL) in the 1980s which went ballistic, then died, was reborn, and then went ballistic again. It is now capped out at a $2.7 trillion market valuation.

Then we all had a great time trading Tesla, which exploded from a split-adjusted $2.35 to $424 and now seems mired in one of its periodic 80% corrections. But mark my word, it is headed to $1,000 someday, taking it up to a $3.2 trillion valuation.

So if NVIDIA isn’t going to $100 trillion what else should be buying right now?

The answer has been apparent in the market for the past two weeks. Interest rate-sensitive commodities have been on a tear, rising 15%-20% across the board. Investors have been using expensive stocks like (NVDA), (MSFT), (AAPL), (META), and (GOOGL) as ATMs to fund purchases of cheap stocks which in some cases have not moved for years.

It really has been an across-the-board move with money pouring into the entire interest rate-sensitive sectors, including copper (FCX), gold (GOLD), silver (WPM), lithium (ALB), Aluminum (AA), and energy (XOM).

It has spread to other economically sensitive stocks like Union Pacific (UNP) and FedEx (FDX). There seems to be an Americaneconomic recovery underway, and the bull market is broadening out. The good news is that it’s not too late to get involved.

A lot of it is investor psychology. Investors fear looking stupid more than they fear losing money. If you buy NVIDIA here on top of a one-year tripling and it tanks you will look like an idiot. If you buy commodities here and they grind up for the rest of 2024 you will look like a genius.

While many of you got slaughtered by the collapse of natural gas this winter, with (UNG) cratering from $32 down to a lowly $15, there is in fact a silver lining to this cloud. Cheap energy costs are now permeating throughout the entire global economy and are filtering down to the bottom lines of companies, municipalities, and even governments.

This has been made possible by the growth of US natural gas production from 1 trillion MM BTUs to 7.5 trillion in just the past ten years. The US is now the largest gas and oil producer in the world by a large margin. Replacing Russia as Europe’s largest energy source in just a year was thought impossible and is now a fact and is also enabling the Continent to stand up to Russian Aggression.

There is hope after all.

One question I constantly received during last week’s Mad Hedge Traders & Investors Summit was “When will Tesla (TSLA) shares bottom? The answer is a very firm “Not yet!”

I have been trading the shares of Elon Musk’s creation for 15 years and can tell you that big surges in the stock always precede major generational changes at the company.

We had a nice run from my $2.35 split-adjusted cost when the first Model S came out (I got chassis number 125 off the assembly line), replacing the toy-like two-seat Tesla Roadster, which was built on a cute little Lotus Elise body from England.

The next big run came with the advent of the much cheaper Model 3 in 2017. The ballistic melt up to $424 began with the launch of the small SUV Model Y in 2020, now the biggest-selling car in the world. All we needed was for Elon Musk to sell $10 billion worth of his own stock by early 2022 to put the final top in.

Which raises the question of when the next major generational change at Tesla. That would be the introduction of the $25,000 Model 2 in 2025. Since everything at Tesla happens late (Elon uses deadlines to flog his staff), it better count on late 2025. That means you should start scaling in around the summer. I am already running the numbers on call spreads and LEAPS now.

Can it fall more in the meantime? Absolutely. $150 a share looks like a chip shot. But to only focus on the EV business, which will account for a mere 10% of Tesla’s final total profits, is to miss Elon’s long-term grand vision of a carbon-free world.

Tesla is in the process of becoming the largest electric power utility in the US, eventually providing charging for 150 million cars. It is taking over the car insurance business. My own premiums on my Model X have plunged by 90%.

It's on the way to becoming the world’s largest processor and recycler of lithium. Tesla has a massive large-scale power storage business that no one knows about.

I fully expect Tesla to become the world’s largest company in a decade. Tesla at $1,000 a share here we come. And while the car business may be slow to turn around, the ingredients that go into the cars, like copper (FCX), Aluminum (AA), and lithium (ALB) are starting to move now.

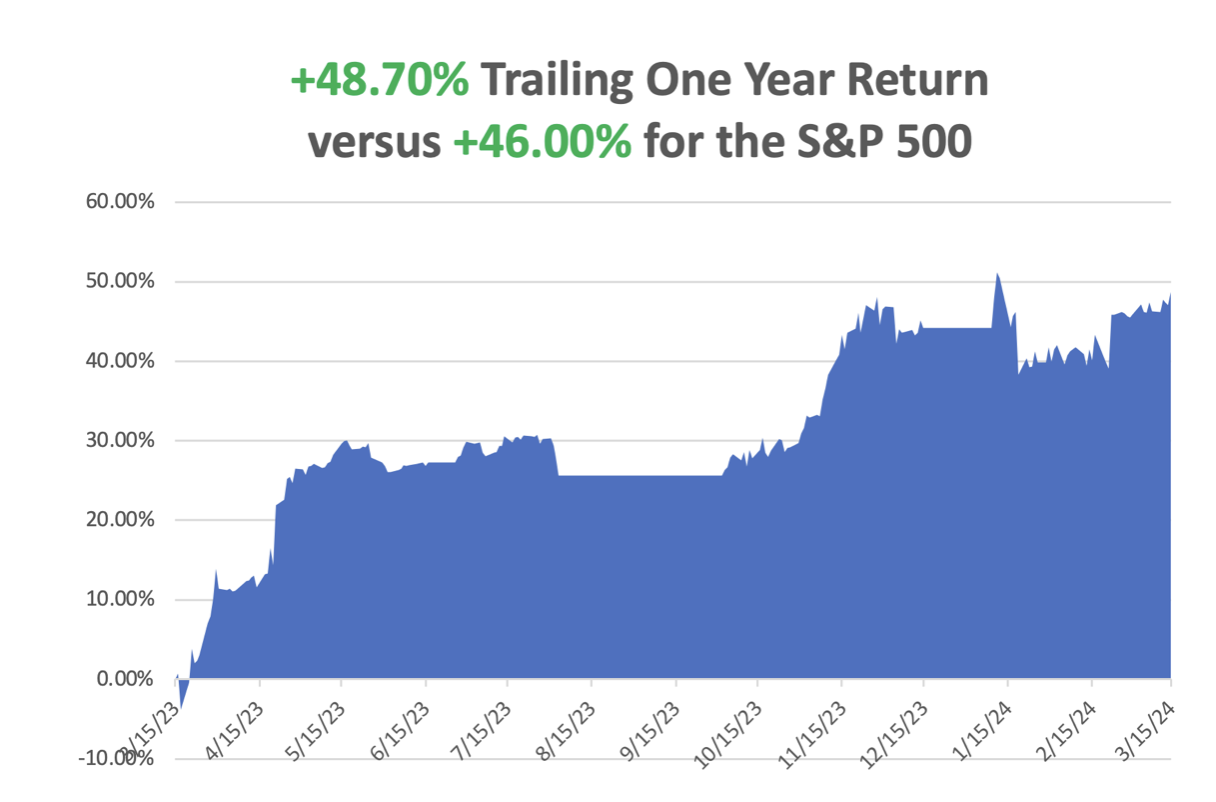

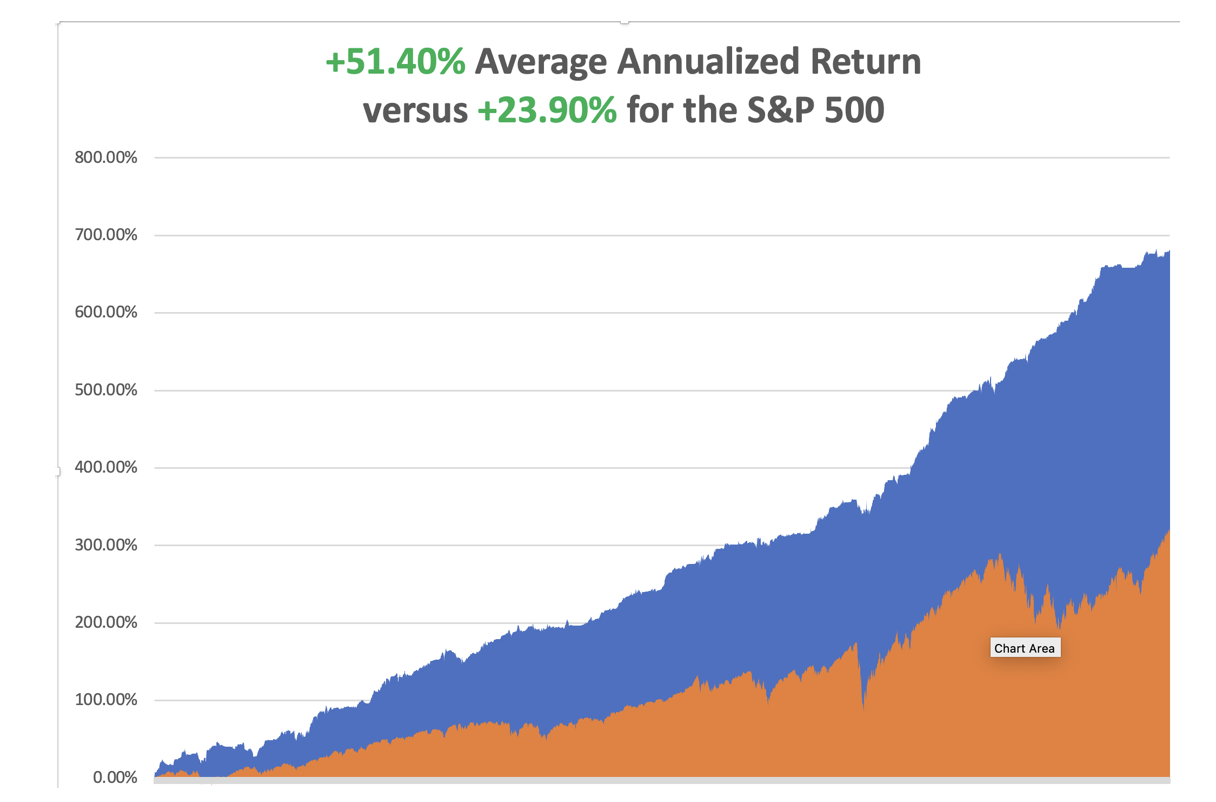

In February we closed up +7.42%. So far in March, we are up +1.34%. My 2024 year-to-date performance is at +4.48%.The S&P 500 (SPY) is up +6.92% so far in 2024. My trailing one-year return reached +48.70% versus +27.25% for the S&P 500. That brings my 16-year total return to +681.11%.My average annualized return has recovered to +51.40%.

Some 63 of my 70 round trips were profitable in 2023. Some 11 of 19 trades have been profitable so far in 2024.

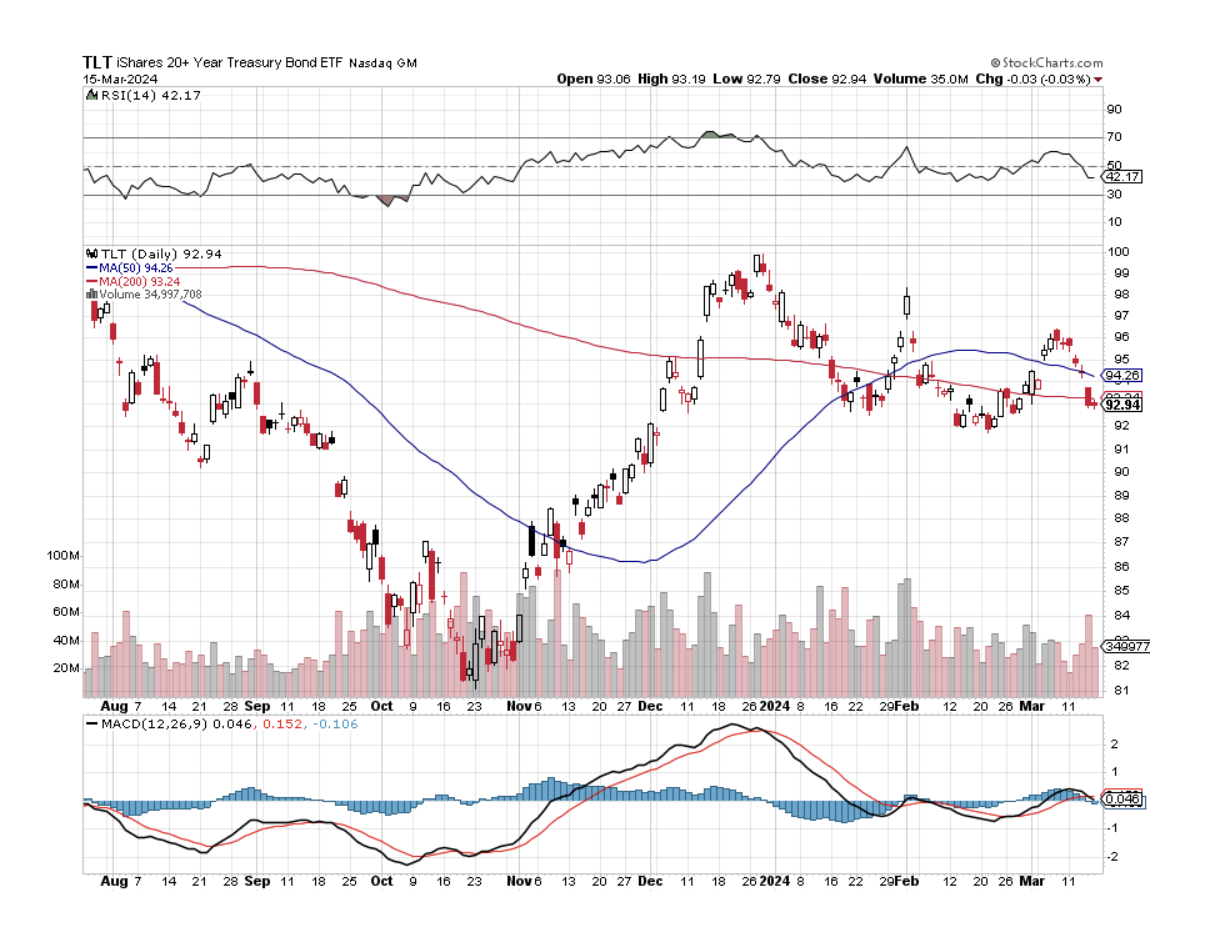

I stopped out of my position in Snowflake (SNOW) for a small loss figuring that the tech rally’s days may be number after the most heroic move in history. I then rotated the money into new longs in Freeport McMoRan (FCX) and ExxonMobile (XOM). I also took profits on my short in bonds (TLT) after a $3.50 point dive there. I am maintaining a long in (TLT). I am 70% in cash and am looking for new commodity plays to pile into.

CPI Comes in Hot at 0.4% in February. YOY inflation crawled up to 3.2% to 3.1% expected. Higher shelter and gasoline prices are to blame. Bonds tank as interest rate cuts get pushed back. So do stocks. The market was ripe for a correction anyway.

PPI Comes in Hotter than Hot, at 0.6%. That was higher than the 0.3% forecast from Dow Jones and comes after a 0.3% increase in January. Stocks dipped for two minutes and then rocketed back up. Bad news is good news. Go figure.

Weekly Jobless Claims Dip, to 209,000 to an expected 218,000, and down 1,000 from the previous week.It’s a go-nowhere number.

Next-Generation Boeing Delayed Until 2027, says Delta Airlines, a major customer. The 737-10, Boeing's biggest Max plane with a maximum seating capacity of 230 passengers, is pending certification by the U.S. Federal Aviation Administration (FAA). Expect a hard look. Buy (BA) on the next meltdown.

BYD Launches its $12,500 Car, the Model e2 Hatchback, firing another shot across Tesla’s Bow. The EV will initially be available only in China, Tesla’s biggest market, and then in emerging countries without vehicle standards. Don’t expect to see them in the US.

Toyota Agrees to Biggest Wage Hike in 25 Years. Toyota, the world's biggest carmaker and traditionally a bellwether of the annual talks, said it agreed to the demands of monthly pay increases of as much as 28,440 yen ($193) and record bonus payments. Is the Bank of Japan about to raise interest rates? Is the Japanese yen about to rocket?

Inverted What? Economists are going up on the Inverted Yield Curve as a recession indicator. Short-term interest rates have been higher than long-term ones for two years now, but the recession never showed. Relying on obsolete data analysis can be fatal to your wealth.

My Ten -Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, March 18, at 7:00 AM EST, the NAHB Housing Index is announced.

On Tuesday, March 19 at 8:30 AM, Housing Starts for Februaryare released.

On Wednesday, March 20 at 11:00 AM, the Federal Reserve Interest rate decision is published

On Thursday, March 21 at 8:30 AM, the Weekly Jobless Claims are announced.

On Friday, March 15 At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, with all of the hoopla over the Oppenheimer movie winning six Academy Awards, including one for best picture, I thought I’d recall my own experience with the nuclear establishment buried in my long and distant past.

If you were good at math there were only two career choices during the early 1970s: teaching math or working for the Dept of Defense. Since I was sick of university after six years, I chose the latter.

That decision sent me down a long bumpy, dusty road in Mercury Nevada headed for the Nuclear Test Site. There was no sign. You could only find the turnoff from US Highway 95 marked by four trailers owned by the nearest hookers to the top-secret base.

Oppenheimer himself had died three years earlier, a victim of throat cancer induced by the chain-smoking of Luck Strikes that was common in those days. But everyone on the base knew him as they had all worked on the Manhattan Project when they were young men. They worshiped him like a god.

I did meet Edward Teller, who argued in the movie that the atomic bomb was a waste of time because his design of a hydrogen bomb was 100 times more powerful. The problem was that there was no target big enough to justify a bomb of that size (there still isn’t).

As I watched the film with my kids, now junior scientists in their own right, I kept pointing out “I knew him,” except they were gnarly old and white-haired by the time I met them. Of course, they are all gone now.

My memories of the Nuclear Test Site were never to ask questions, my visit to the Glass Desert where the sand had been turned into glass by above-ground tests in the fifties, and skinny dipping with the female staff in the small swimming pool at midnight.

The MPs were pissed.

With the signing of the SALT I Treaty in 1972, underground testing moved to computer models and I lost my job. So I was sent to Hiroshima to interview survivors and write a 30-year after-action report. These were some of the most cheerful people I ever met. If an atomic bomb can’t kill you, then nothing can.

When the Cold War ended in 1992, the United States judiciously stepped in and bought the collapsing Soviet Union’s entire uranium and plutonium supply.

For good measure, my hedge fund client George Soros provided a $50 million grant to hire every unemployed Soviet nuclear engineer. The fear then was that starving scientists would go to work for Libya, Iraq, North Korea, or Pakistan, which all had active nuclear programs. They ended up in the US instead.

That provided the fuel to run all US nuclear power plants and warships for 20 years. That fuel has now run out and chances of a resupply from Russia are zero. The Department of Defense attempted to reopen our last plutonium factory in Amarillo, Texas, a legacy of the Johnson administration.

But the facilities were deemed too old and out of date, and it is cheaper to build a new factory from scratch anyway. What better place to do so than Los Alamos, which has the greatest concentration of nuclear expertise in the world.

Los Alamos is a funny sort of place. It sits at 7,320 feet on a mesa on the edge of an ancient volcano so if things go wrong, they won’t blow up the rest of the state. The homes are mid-century modern built when defense budgets were essentially unlimited. As a prime target in a nuclear war, there are said to be miles of secret underground tunnels hacked out of solid rock.

You need to bring a Geiger counter to garage sales because sometimes interesting items are work castaways. A friend almost bought a cool coffee table which turned out to be part of an old cyclotron. And for a town designing the instruments to bring on the possible end of the world, it seems to have an abnormal number of churches. They’re everywhere.

I have hundreds of stories from the old nuclear days passed down from those who worked for J. Robert Oppenheimer and General Leslie Groves, who ran the Manhattan Project in the early 1940s. They were young mathematicians, physicists, and engineers at the time, in their 20’s and 30’s, who later became my university professors. The A-bomb was the most important event of their lives.

Unfortunately, I couldn’t relay this precious unwritten history to anyone without a security clearance. So, it stayed buried with me for a half century, until now.

Some 1,200 engineers will be hired for the first phase of the new plutonium plant, which I got a chance to see. That will create challenges for a town of 13,000 where existing housing shortages already force interns and graduate students to live in tents. It gets cold at night and dropped to 13 degrees F when I was there.

I was allowed to visit the Trinity site at the White Sands Missile Test Range, the first visitor to do so in many years. This is where the first atomic bomb was exploded on July 16, 1945. The 20-kiloton explosion set off burglar alarms for 200 miles and was double to ten times the expected yield.

Enormous targets hundreds of yards away were thrown about like toys (they are still there). Some scientists thought the bomb might ignite the atmosphere and destroy the world but they went ahead anyway because so much money had been spent, 3% of US GDP for four years. Of the original 100-foot tower, only a tiny stump of concrete is left (picture below).

With the other visitors, there was a carnival atmosphere as people worked so hard to get there. My Army escort never left me out of their sight. Some 79 years after the explosion, the background radiation was ten times normal, so I couldn’t stay more than an hour.

Needless to say, that makes uranium plays like Cameco (CCJ), NextGen Energy (NXE), Uranium Energy (UEC), and Energy Fuels (UUUU) great long-term plays, as prices will almost certainly rise all of which look cheap. US government demand for uranium and yellow cake, its commercial byproduct, is going to be huge. Uranium is also being touted as a carbon-free energy source needed to replace oil.

At Ground Zero in 1945

What’s Left of a Trinity Target 200 Yards Out

Playing With My Geiger Counter

Atomic Bomb No.3 Which was Never Used in Tokyo

What’s Left from the Original Test

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/03/geiger-counter.png438582april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-03-18 09:02:382024-03-18 11:32:08The Market Outlook for the Week Ahead, or The Big Rotation is on

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.