Mad Hedge Technology Letter

May 7, 2019

Fiat Lux

Featured Trade:

(THE LURKING DANGERS BEHIND FACEBOOK)

(FB), (WFC), (NFLX)

Mad Hedge Technology Letter

May 7, 2019

Fiat Lux

Featured Trade:

(THE LURKING DANGERS BEHIND FACEBOOK)

(FB), (WFC), (NFLX)

The current business model of social media is dead, and the future model seems in doubt – that was the take away from world's largest social media platform at F8 that I attended, its annual developer conference.

Co-founder and CEO Facebook (FB) Mark Zuckerberg stated at the event that “in our digital lives, we also need both public and private spaces,” an impromptu call to action to migrate users into a new private digital world with Facebook dictating the terms.

The sushi must really be hitting the fan for Zuckerberg to announce his future vision of social media, and the writing is on the wall for his current social media experiment, that is, if he continues along at the same rate.

The projected $5 billion fine incurred by Facebook from the Federal Trade Commission over its privacy handling of personal data is peanuts for the social media company, but this could be the first of numerous fines doled out by regional and national regulatory bureaus that span from the Bay Area to Vietnam.

Facebook is a company that made over $55 billion in revenue last year and the $5 billion would amount to less than 10% of annual sales.

From that $55 billion, Facebook earned profits of over $22 billion, and this $22 billion is what the regulatory battles are about, along with the co-founder’s tenacious defense of deploying his users as free content.

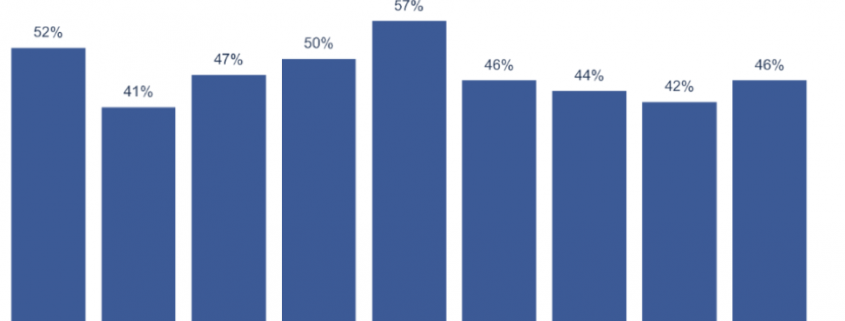

The firm has continued to post operating margins of over 40% and delivered margins of 46% last quarter, a sequential rise of 4% in Q4 2018.

The Oracle of Omaha better known as Warren Buffet cited necessitating accountability for CEOs that drive a company into a government bailout especially banks.

He advocated that these executives and their spouses should be stripped of their net worth if they damage shareholder value.

The comments were directed at the way Wells Fargo’s (WFC) former CEO Tim Sloan crippled Wells Fargo and has since been sidelined during the long bull market in equities.

At some point, Zuckerberg could confront similar ructions because of his efforts at perverting democracy that has caused innumerable damage to American democracy and global society, and I am certain his legion of lawyers are already hatching a plan to tackle this thorny predicament.

If you ponder about his announcement in a zero-sum environment, it makes no sense for Facebook to pivot to “private” messages.

This leads me to believe his words are smoke and mirrors so that Facebook can perpetuate its duopoly and force digital ad players to continue to drink from the same Kool-Aid.

As before, Zuckerberg still believes this game of cat and mouse is a half-baked marketing fix.

This is why many of his trusted disciples such as former executive Chris Cox left under a shroud of mystery citing “artistic differences” in terminating his tenure at Facebook.

It is clear to many that Facebook is barreling straight into an even more frightening future.

What does the announcement mean from a business perspective?

Zuckerberg will continue to purge anyone that disagrees with him, even trusted lieutenants, and continue to integrate the family of apps into one big platform that includes Facebook, Instagram, and WhatsApp messenger.

These three will become one and thus, Zuckerberg’s ad machine rolls on like the dystopian action film Mad Max.

Let me remind you, these drastic measures boil down to Facebook doing everything they can to keep content costs down.

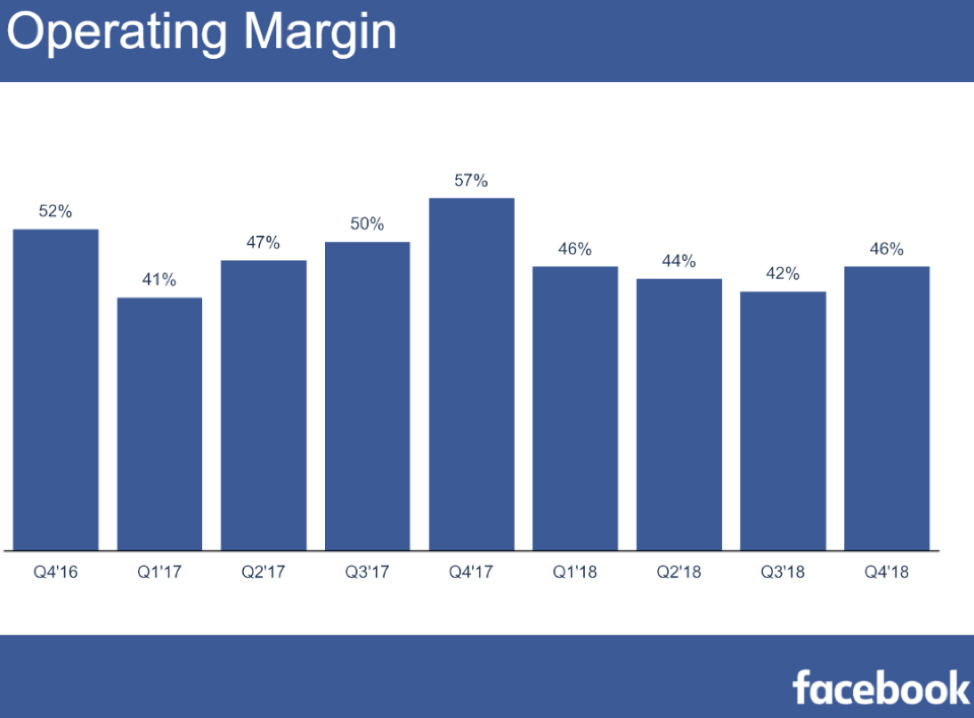

If they, for example, have to go the same route as Netflix (NFLX) - overpaying for the best actors and directors to generate premium content, the stock would halve the next day.

And that is what Zuckerberg is desperately hoping to avoid after the 30% dip in shares in 2018 because of regulatory headwinds.

Combining the three apps would be impossible to regulate at a time that regulation is rearing its ugly head.

Zuckerberg is intentionally upping the ante and accruing more risk in the hope that Facebook can outmuscle its way through in one piece.

The ad industry is crying out for something new, but as long as Zuckerberg’s claws are firmly into the meat of the digital ad budgets for most companies, he gets to decide how the industry develops because he knows the ad dollars will stick.

In the future, your private chats won’t be private because Zuckerberg will be mining the data for ad dollar revenue.

No matter what he says, nothing will change unless Facebook goes in an entirely new direction which would inhibit sales.

Until the fines become material, let’s say 70% of annual revenue or something of that nature, a $5 billion hit to the bottom line will not persuade the management to transform their practices.

Expect less privacy, and WhatsApp and Instagram to be heavily monetized through ad promotion and data mining even though Zuckerberg pledging his company won’t hold user data “longer than necessary.”

As for Facebook itself, Zuckerberg can’t throw his baby out with the bathwater and will hope to minimize its deceleration by bundling it with the growth trajectory of WhatsApp and Instagram.

Instead of major structural changes, Zuckerberg continues to beat around the bush saying, “You should expect that we’re not going to store your data in countries where there's weak data protection.”

This is not the crux of the problem and shows Zuckerberg is still paying lip service and not ponying up to reality.

Attaching Facebook and its dying model is not an attractive strategy leading to a slew of executive resignations.

I believe this could all end in calamity for Zuckerberg as he figures piling on more risk onto the elevated risk levels is the right decision making Warren Buffet’s point for him about CEO’s accountability.

Should Zuckerberg refund shareholders if his flight turns into a suicide mission then claims to be an unwitting victim?

And how does he even refund democracy with his apps causing major unrest to society such as killings that occur because of the distribution of fake news on his platforms?

Making a hot potato hotter might work for the short term and if ad dollars stream into WhatsApp and Instagram, Zuckerberg will claim victory.

But at some point, the potato will scald his hands so bad that it will drop.

Your private chats will be the content at the fulcrum of his data broker empire since his “digital town square” approach isn’t working anymore.

The company is utterly incentivized to figure out how to continue this ad revenue carnival because 93% of total revenue last quarter came from digital ads which is up from the prior year when it constituted 89%.

It all sounds like a big brother apocalyptical novel, which we are in, scarily, in putting out this dialogue before the firestorm starts, Facebook wants to normalize, and front runs the craziness of selling your private chat data before it becomes a national issue.

Will regulators shut this down or will they be naïve and turn a blind eye?

Global Market Comments

April 23, 2019

Fiat Lux

Featured Trade:

(LAS VEGAS MAY 9 GLOBAL STRAGEGY LUNCHEON)

(APRIL 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(FXI), (RWM), (IWM), (VXXB), (VIX), (QCOM), (AAPL), (GM), (TSLA), (FCX), (COPX), (GLD), (NFLX), (AMZN), (DIS)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader April 17 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What will the market do after the Muller report is out?

A: Absolutely nothing—this has been a total nonmarket event from the very beginning. Even if Trump gets impeached, Pence will continue with the same kinds of policies.

Q: If we are so close to the peak, when do we go short?

A: It’s simple: markets can remain irrational longer than you can remain liquid. Those shorts are expensive. As long as global excess liquidity continues pouring into the U.S., you’ll not want to short anything. I think what we’ll see is a market that slowly grinds upward until it’s extremely overbought.

Q: China (FXI) is showing some economic strength. Will this last?

A: Probably, yes. China was first to stimulate their economy and to stimulate it the most. The delayed effect is kicking in now. If we do get a resolution of the trade war, you want to buy China, not the U.S.

Q: Are commodities expected to be strong?

A: Yes, China stimulating their economy and they are the world’s largest consumer commodities.

Q: When is the ProShares Short Russell 2000 ETF (RWM) actionable?

A: Probably very soon. You really do see the double top forming in the Russell 2000 (IWM), and if we don’t get any movement in the next day or two, it will also start to roll over. The Russell 2000 is the canary in the coal mine for the main market. Even if the main market continues to grind up on small volume the (IWM) will go nowhere.

Q: Why do you recommend buying the iPath Series B S&P 500 VIX Short Term Futures ETN (VXXB) instead of the Volatility Index (VIX)?

A: The VIX doesn’t have an actual ETF behind it, so you have to buy either options on the futures or a derivative ETF. The (VXXB), which has recently been renamed, is an actual ETF which does have a huge amount of time decay built into it, so it’s easier for people to trade. You don’t need an option for futures qualification on your brokerage account to buy the (VXXB) which most people don’t have—it’s just a straight ETF.

Q: So much of the market cap is based on revenues outside the U.S., or GDP making things look more expensive than they actually are. What are your thoughts on this?

A: That is true; the U.S. GDP is somewhat out of date and we as stock traders don’t buy the GDP, we buy individual stocks. Mad Hedge Fund Trader in particular only focuses on the 5% or so—stocks that are absolutely leading the market—and the rest of the 95% is absolutely irrelevant. That 95% is what makes up most of the GDP. A lot of people have actually been caught in the GDP trap this year, expecting a terrible GDP number in Q1 and staying out of the market because of that when, in fact, their individual stocks have been going up 50%. So, that’s something to be careful of.

Q: Is it time to jump into Qualcomm (QCOM)?

A: Probably, yes, on the dip. It’s already had a nice 46% pop so it’s a little late now. The battle with Apple (AAPL) was overhanging that stock for years.

Q: Will Trump next slap tariffs on German autos and what will that do to American shares? Should I buy General Motors (GM)?

A: Absolutely not; if we do slap tariffs on German autos, Europe will retaliate against every U.S. carmaker and that would be disastrous for us. We already know that trade wars are bad news for stocks. Industry-specific trade wars are pure poison. So, you don't want to buy the U.S. car industry on a European trade war. In fact, you don’t want to buy anything. The European trade war might be the cause of the summer correction. Destroying the economies of your largest customers is always bad for business.

Q: How much debt can the global economy keep taking on before a crash?

A: Apparently, it’s a lot more with interest rates at these ridiculously low levels. We’re in uncharted territory now. We really don't know how much more it can take, but we know it’s more because interest rates are so low. With every new borrowing, the global economy is making itself increasingly sensitive to any interest rate increases. This is a policy you should enact only at bear market bottoms, not bull market tops. It is borrowing economic growth from futures year which we may not have.

Q: Is the worst over for Tesla (TSLA) or do you think car sales will get worse?

A: I think car sales will get better, but it may take several months to see the actual production numbers. In the meantime, the burden of proof is on Tesla. Any other surprises on that stock could see us break to a new 2 year low—that's why I don’t want to touch it. They’ve lately been adopting policies that one normally associates with imminent recessions, like closing most of their store and getting rid of customer support staff.

Q: Is 2019 a “sell in May and go away” type year?

A: It’s really looking like a great “Sell in May” is setting up. What’s helping is that we’ve gone up in a straight line practically every day this year. Also, in the first 4 months of the year, your allocations for equities are done. We have about 6 months of dead territory to cover from May onward— narrow trading ranges or severe drops. That, by the way, is also the perfect environment for deep-in-the-money put spreads, which we plan to be setting up soon.

Q: Is it time to buy Freeport McMoRan (FCX) in to play both oil and copper?

A: Yes. They’re both being driven by the same thing: China demand. China is the world’s largest new buyer of both of these resources. But you’re late in the cycle, so use dips and choose your entry points cautiously. (FCX) is not an oil play. It is only a copper (COPX) and gold (GLD) play.

Q: Are you still against Bitcoin?

A: There are simply too many better trading and investment options to focus on than Bitcoin. Bitcoin is like buying a lottery ticket—you’re 10 times more likely to get struck by lightning than you are to win.

Q: Are there any LEAPS put to buy right now?

A: You never buy a Long-Term Equity Appreciation Securities (LEAPS) at market tops. You only buy these long-term bull option plays at really severe market selloffs like we had in November/December. Otherwise, you’ll get your head handed to you.

Q: What is your outlook on U.S. dollar and gold?

A: U.S. dollar should be decreasing on its lower interest rates but everyone else is lowering their rates faster than us, so that's why it’s staying high. Eventually, I expect it to go down but not yet. Gold will be weak as long as we’re on a global “RISK ON” environment, which could last another month.

Q: Is Netflix (NFLX) a buy here, after the earnings report?

A: Yes, but don't buy on the pop, buy on the dip. They have a huge head start over rivals Amazon (AMZN) and Walt Disney (DIS) and the overall market is growing fast enough to accommodate everyone.

Q: Will wages keep going up in 2019?

A: Yes, but technology is destroying jobs faster than inflation can raise wages so they won’t increase much—pennies rather than dollars.

Q: How about buying a big pullback?

A: If we get one, it would be in the spring or summer. I would buy a big pullback as long as the U.S. is hyper-stimulating its economy and flooding the world with excess liquidity. You wouldn't want to bet against that. We may not see the beginning of the true bear market for another year. Any pullbacks before that will just be corrections in a broader bull market.

Good Luck and Good Trading

John Thomas

CEO & Publisher

Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

April 18, 2019

Fiat Lux

Featured Trade:

(NETFLIX’S WORST NIGHTMARE)

(NFLX), (DIS), (FB), (AAPL)

Netflix came out with earnings yesterday and revealed guidance that many industry analysts were dreading.

It appears that Netflix’s relative subscriber growth rate has reached the high-water mark for now.

Competition is rapidly encroaching Netflix’s moat.

In a letter to shareholders, management opined revealing that they do not “anticipate these new entrants will materially affect our growth.”

I am quite bothered by this statement because one would have to be blind, deaf, and dumb to believe that Disney (DIS) or Apple’s (AAPL) new products will not take away meaningful eyeballs from Netflix.

These companies are all competing in the same sphere – digital entertainment.

Papering over the cracks with wishy washy rhetoric was not something I was doing backflips over.

Netflix’s management knew this earnings report had nothing to do with results because everyone wanted to reassess how bad the new entrants would make life for Netflix.

Disney has the content to inflict major damage to Netflix’s business model.

The mere existence of Disney as a rival weakens Netflix’s narrative substantially in two ways.

First, Disney’s entrance into the online streaming game means Netflix will not have a chance to raise subscription prices for the short to medium term.

The last price hike was done in the nick of time and even though management mentioned it followed through “as expected,” losing this financial lever gives Netflix less ammunition going forward and caps EPS growth potential.

Second, another dispiriting factor is the premium for retaining and acquiring original content will skyrocket with more firms jockeying for the same finite amount of actors, producers, directors, and writers.

This particular premium cannot be quantified but firms might try to bid up the cost of certain talent just so the other guy has to foot a bigger bill, this is done in professional sports all the time.

Firms might even take actors off the table with exclusive contracts just to frustrate the supply of content generators.

Uncertainty perpetuates with the future cost of content unable to be baked into the casserole yet, and represents severe downside risk to a stock which trots out an expensive PE ratio of 133.

Growth, growth, and more growth – that is what Netflix has groomed investors to obsess on with the caveat of major strings attached.

This model is highly effective in a vacuum when there are no other players that can erode market share.

Delivering on growth justifies heavy cash burn, and to Netflix’s credit, they have fully delivered in spades.

The strings attached come in the form of steep losses in order to create top of the line content.

Planning to revise down annual cash flow from $3 billion to $3.5 billion in 2019 will serve as a litmus test to whether investors are ready to shoulder the extra losses in the near term.

I found it compelling that Disney Plus will debut at $6.99 per month – add that to the price of Netflix’s standard package of $12.99 and you get a shade under $20.

Disney hopes to dictate spending habits by psychologically grouping Disney and Netflix for both at under $20.

The result of breaching the $20 threshold might push customers into ditching Netflix and sticking with the $6.99 Disney subscription.

Then there is the thorny issue of Netflix’s growth – the quality and trajectory of it.

The firm issued poor guidance for next quarter projecting total paid net adds of 5.0m, representing -8% YOY with only 300,000 adds in the US and 4.7m for the international segment.

Alarm bells should be sounding in the halls when the most lucrative segment is estimated to decelerate by 8% YOY.

Domestic subscriptions deliver higher margins bumping up the average revenue per user (ARPU).

Contrast this with Netflix’s basic Indian package costing $7.27 or 500 rupees and a mobile package of $3.63 or 250 rupees.

In my opinion, domestically decelerating in the high single digits does not justify the additional annual cash burn of half a billion dollars even if you accumulate millions of more Indian adds at lower price points.

This leads me to surmise that the quality of growth is beginning to slip, and Netflix appears to be running into the same type of quagmire Facebook (FB) is facing.

These models are grappling with stagnating or slowing North American growth and an emerging market solution isn’t the panacea.

The Netflix Indian packages are actually considered expensive by local standards meaning that Netflix’s won’t be able to crowbar in price hikes like they did in America.

On the positive side, Netflix did beat Q1 estimates with paid net adds up 9.6 million with 1.74m in the US and 7.86m internationally, up 16% YOY.

Netflix was able to reach revenue of $4.5B, a company record mostly due to the $2 price hike during the quarter in America.

The letter to shareholders simplifies Netflix’s tactics to investors explaining, “For 20 years, we’ve had the same strategy: when we please our members, they watch more and we grow more.”

What this letter doesn’t tell you is that Disney and the looming battle with Netflix will reshape the online streaming landscape.

In simple economics, an increase of supply caps demand, and don’t get sidetracked by the smoke and mirrors, Disney and Netflix are absolutely fighting for the same eyeballs no matter how much Netflix plays this down.

To highlight an example of how these two are directly competing against each other – let’s take the cast of Monica, Chandler, Rachel, Ross, Joey, and Phoebe – in the hit series Friends.

Netflix acquired the broadcasting rights from Warner Bros, who owns Disney, and it was the most popular show on Netflix.

Warner Bros, knowing that Disney were on the verge of rolling out an online streaming product, renewed Netflix for 2019 at $80 million.

Not only were they hand feeding the enemy in broad daylight, but they handicapped their new products as it is about to debut.

Whoever made that decision must go into the hall of shame of boneheaded online content decisions.

Once 2020 rolls around, Disney will finally be able to slap Friends on Disney Plus where it belongs, and the streaming wars will heat up to a fever pitch.

Ultimately, when Netflix brushes off reality proclaiming that if they please viewers with the same strategy, then everything will be hunky-dory, then I would say they are being disingenuous.

The online streaming industry has started to become more complex by the minute and the “same strategy” that worked wonders in a vacuum before must evolve with the times.

At $360, I would short Netflix in the short to medium term until they prove the headwinds are a blip.

If it goes up to $400, it’s a screaming short because accelerating cash burn, poor guidance, decelerating domestic net adds, and a jolt of new competition aren’t the catalysts that will take shares above the heavenly lands of $400, let alone $450.

Netflix is still a fantastic company though – I’m an avid viewer.

Mad Hedge Technology Letter

April 3, 2019

Fiat Lux

Featured Trade:

()

(GOOGL), (NFLX), (AMZN)

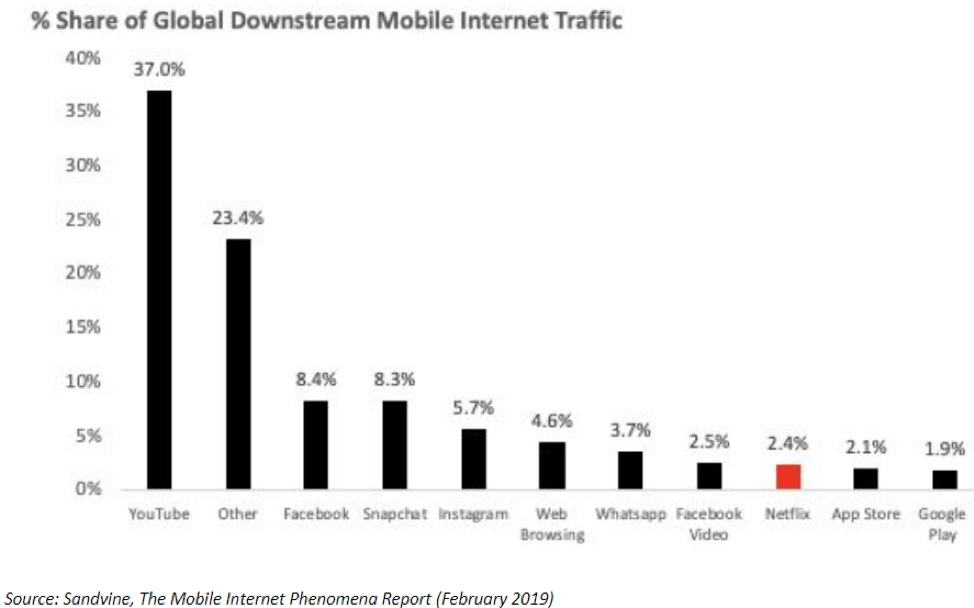

YouTube has to be the online streaming asset of the year even relegating Netflix (NFLX) to the minor leagues – I’ll tell you why.

India is the new China.

Netflix’s growth strategy is intertwined with India and the management has been extraordinarily vocal about their interests there.

The Indian online streaming renaissance isn’t just fueling Netflix’s rise. In fact, YouTube and its free platform are performing miracles along the Ganges River.

How big is YouTube in India?

YouTube already has 245 million monthly active users in India penetrating 85% of the country’s internet population making India one of its best-performing markets.

The company says more than 60% of its streaming hours in India come from outside the six metros, meaning YouTube has captured the hearts and minds of the rural population who cannot afford to pay for online content.

KPMG forecasts India’s online streaming audience to surpass 550 million by 2023 and YouTube will capture 70% of the 550 million audience.

How did YouTube manage to do this?

First, the content is free with ads allowing rural Indians to join in.

Second, local Indians became hooked on Alphabet’s YouTube with Alphabet (GOOGL) taking an already brilliant platform and supercharged it by tailoring it to popular local influencers that are joining in droves inciting a massive network effect.

Effectively, YouTube attracted these influencers with eye-popping audiences to create organic and original content without the $8 billion Netflix planned content budget in 2019.

YouTube was able to do this by borrowing the Instagram format but transferring it to a more effective video platform model.

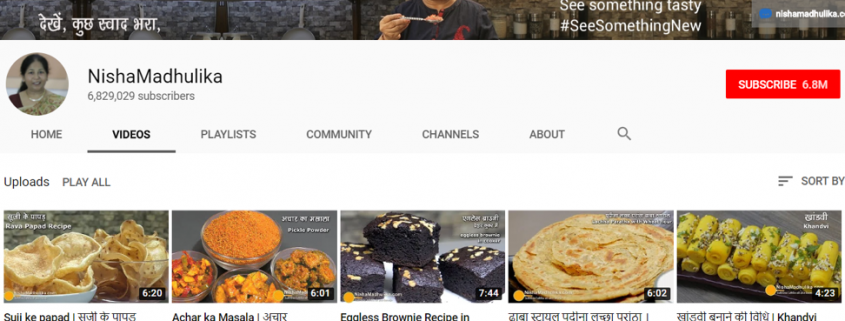

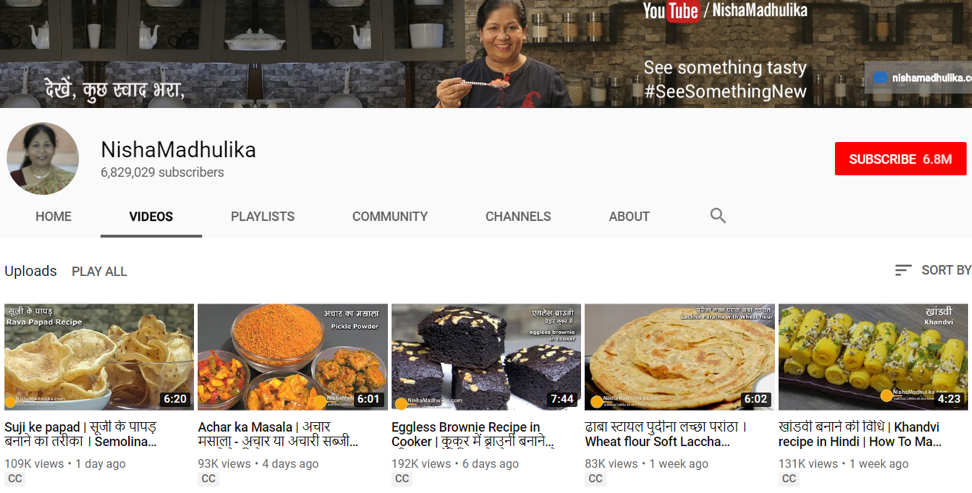

Take for instance Nisha Madhulika whose channel has blossomed into one of the most popular Hindi language-based online cooking channels on the internet.

To see one of her videos, please click here.

Her channel has over 6.8 subscribers, yet, accumulating subscribers is one thing, and making money is another.

Past videos that were posted around 2-3 weeks ago have views between 200,000 to 400,000.

These influencers build up revenue by displaying 3rd party ads generated by Alphabet.

A general rule of thumb is that for every 1 million view, ad revenue collected is around $2,000.

Therefore, Nisha and fellow YouTubers with massive audiences are incentivized to pump out high-quality content in high volume.

Scrolling through her numbers, Nisha appears to average around $700 of revenue per video.

She sprinkles in the occasional viral video that garners 1.5 million views which would earn her a tidy $3,000 for a single video.

Not bad and that is before any of the possible marketing opportunities are quantified.

As long as she focuses on the quality of the videos, she can consistently earn $700 per video, then she can do more by partnering with affiliates to sell 3rd party products and receive a commission that is trackable through the links she leaves at the bottom of her videos.

Nisha’s video business works like this, her channel entails producing 3-5 short videos per week producing around 9-11 million views per month adding up to between $18,000-$22,000 in revenue per month.

Remember that while she is accumulating views for newly posted videos, there are still viewers rummaging through her older content demonstrating the beauty of the network effect.

Older videos in Nisha’s case usually add an extra $3,000-$5,000 per month to the bottom line in pure profit.

Many influencers curate, edit, design, and film the content themselves, or subcontract these jobs for a cheap fee.

An influencer could run their YouTube channel for less than $100 per month minus the fees for the equipment.

YouTube has created a powerful platform for content creators to monetize their original content and give them incentives to stick around and build a business.

Netflix has more of a mercenary model where they contract highly paid actors to contribute a finite amount of content for a fee.

YouTube’s model penetrates to the heart of the average person with regular people instead of propping up overpaid Hollywood actors like Netflix.

In many cases, YouTube’s influencers offer live, raw, and personal access, and the data suggests that live, unscripted content are one of the most monetizable types of content on the market due to its original nature and unpredictability.

That is why live sports like the NFL and NBA are easy to sell, monetize, and in great demand.

I do believe that Netflix has a great product but overpaying for Hollywood’s best talent is not sustainable because the cost-benefit ratio isn’t worth it, which is why Netflix is raising customer prices to monetize the quality of streaming content better.

With other big tech players coming into the market, it will push up the costs for Hollywood talent putting more short-term pressure on their financial model.

Even if Netflix does get the right actors to provide content, they do have their fair share of bad movies.

YouTube’s performance in India will be hard to compete with, even harder when they avoid expensive mistakes, a bad video is simply glossed over and ignored.

Netflix is in the midst of testing a mobile-only Indian subscription package for around $3.64 per month, or 250 Indian rupees, to respond to YouTube’s godlike presence there.

Remember that most rural Indians do not have access to hardware such as computers, laptops, or tablets, and run their lives with cheap Chinese smartphones from Oppo and Vivo.

If you thought $3.64 was a cheap streaming package, then Amazon (AMZN) takes it one step further by offering Amazon prime video for $1.88 per month or 129 Indian rupees.

I like Netflix’s product and the narrative is still intact, but I adore and love YouTube’s transformation that has caught many of us by surprise.

This massive shift wouldn’t be possible without Google’s army of best of breed ad tech.

Even more poignant, YouTube takes direct to consumers to a rawer entry point enhancing the special experience.

The problem with Hollywood talent is that reformulating them onto Netflix’s platform brings them closer to the audience to a certain degree, but not like Nisha’s cooking channel where she can speak directly to the viewer and even interact with her audience in the comment section.

YouTube has mastered this relationship between content creator and audience, and no matter how many times I watch Will Smith’s Bright, I can’t expect him to reply to my comments.

Well, there’s not even a comment section on Netflix’s platform.

In short, Netflix’s Indian strategy is incomplete and I predict that YouTube will extend its lead there because the scalability is well-suited for the Indian rural audience who have little or no discretionary income.

The freemium model wins out again.

Affixing a Netflix grade streaming asset to Alphabet’s booming digital ad business is a match made in heaven.

Buy Alphabet on the dip – YouTube’s outperformance in 2019 will surpass expectations and carry Alphabet shares to new all-time highs this calendar year.

Global Market Comments

April 3, 2019

Fiat Lux

Featured Trade:

(WHO WILL BE THE NEXT FANG?)

(FB), (AMZN), (NFLX), (GOOGL), (AAPL),

(BABA), (TSLA), (WMT), (MSFT),

(IBM), (VZ), (T), (CMCSA), (TWX)

FANGS, FANGS, FANGS! Can’t live with them but can’t live without them either.

I know you’re all dying to get into the next FANG on the ground floor, for to do so means capturing a potential 100-fold return, or more.

I know because I’ve done it four times. The split adjusted average cost of my Apple shares is only 25 cents compared to today’s $174, so you can understand my keen interest. My average on Tesla is $16.50.

Uncover a new FANG and the riches will accrue rapidly. Facebook (FB), Amazon AMZN), Netflix (NFLX), and Alphabet (GOOGL) didn’t exist 25 years ago. Apple (AAPL) is relatively long in the tooth at 40 years. And now all four are in a race to become the world’s first trillion-dollar company.

One thing is certain. The path to FANGdom is shortening. It took Apple four decades to get where it is today, Facebook did it in one. As Steve Jobs used to tell me when he was running both Apple and Pixar, “These overnight successes can take a long time.”

There is also no assurance that once a FANG always a FANG. In my lifetime, I have seen far too many Dow Average components once considered unassailable crash and burn, like Eastman Kodak (KODK), General Electric (GE), General Motors (GM), Sears (SHLD), Bethlehem Steel, and IBM (IBM).

I established in an earlier piece that there are eight essential attributes of a FANG, product differentiation, visionary capital, global reach, likeability, vertical integration, artificial intelligence, accelerant, and geography.

We are really in a “What have you done for me lately” world. That goes for me too. All that said, I shall run through a short list for you of the future FANG candidates we know about today.

Alibaba (BABA)

Alibaba is an amalgamation of the Chinese equivalents of Amazon, PayPal, and Google all sewn together. It accounts for a staggering 63% of all Chinese online commerce and is still growing like crazy. Some 54% of all packages shipped in China originate from Alibaba.

The juggernaut has over half billion active users, and another half billion placing orders through mobile phones. It is a master of AI and B2B commerce. There is nothing else like it in the world.

However, it does have some obvious shortcomings. Its brand is almost unknown in the US. It has a huge problem with fakes sold through their sites.

It also has an ownership structure for foreign investors that is byzantine, to say the least. It is a contractual right to a share of profits funneled through a PO box in the Cayman Island. The SEC is interested, to say the least.

We also don’t know to what extent founder Jack Ma has sold his soul to the Beijing government. It’s probably a lot. That could be a problem if souring trade relations between the US and the Middle Kingdom get worse, a certainty with the current administration.

Tesla (TSLA)

Before you bet on a new startup breaking into the Detroit Big Three, go watch the movie “Tucker” first. Spoiler Alert: It ends in tears.

Still, Tesla (TSLA) has just passed the 270,000 mark in the number of cars manufacturered. Tucker only got to 50.

Having led my readers into the stock after the IPO at $16.50, I am already pretty happy with this company. Owning three of their cars helps too (two totaled). But Tesla still has a long way to go.

It all boils down to the success of the $35,000, 200-mile range Tesla 3 for which it already has 500,000 orders. So far so good.

It’s all about scale. If it can produce these cars in sufficient numbers, it will take over the world and easily become the next FANG. If it can’t, it won’t. It’s that simple.

To say that a lot is already built into the share price would be an understatement. Tesla now trades at ten times revenues compared to 0.5 for Ford (F) and (General Motors (GM). That’s a relative overvaluation of 20:1.

Any of a dozen competing electric car models could scale up with a discount model before they do, such as the similarly priced GM Bolt. But with a ten-year lead in the technology, I doubt it.

It isn’t just cars that will anoint Tesla with FANG sainthood. The firm already has a major presence in rooftop solar cell installation through Solar City, utility sized solar plants, industrial scale battery plants, and is just entering commercial trucks. Consider these all seeds for FANGdom.

One thing is certain. Without Tesla, there wouldn’t be s single mass-market electric car on the road today.

For that, we can already say thanks.

Uber

In the blink of an eye, ride sharing service Uber has become essential for globe-trotting travelers such as myself.

Its 2 million drivers completely disrupted the traditional taxi model for local transportation which remains unchanged since the days of horses and buggies.

That has created the first $75 billion of enterprise value. It’s what’s next that could make the company so interesting.

It is taking the lead in autonomous driving. It could also replace FeDex, UPS, DHL, and the US post office by offering same day deliveries at a fraction of the overnight cost.

It is already doing this now with Uber Foods which offers immediate delivery of takeouts (click here if you want lunch by the time you finish reading this piece.)

UberCopters anyone? Yes, it’s already being offered in France and Brazil.

Uber has the potential to be so much more if it can just outlive its initial growing pains.

It is a classic case of the founder being a terrible manager, as Travis Kalanick has lurched from one controversy to the next. The board finally decided he should spend much time on his new custom built 350-foot boat.

Its “bro” culture is notorious, even in Silicon Valley.

It is also getting enormous pushback from regulators everywhere protecting entrenched local interests. It has lost its license in London, the only place in the world that offered a decent taxi service pre-Uber. Its drivers are getting beaten up in Paris.

However, if it takes advantage of only a few of the doors open to it, status as a FANG beckons.

Walmart (WMT)

A few years ago, I was heavily criticized for pointing out that half the employees at my local Walmart (WMT) were missing their front teeth. They have since received a $2 an hour's pay raise, but the teeth are still missing. They don’t earn enough money to get them fixed.

The company is the epitome of bricks and mortar in a digital world with 12,000 stores in 28 countries. It is the largest private employer in the US, with 1.4 million workers, mostly earning minimum wage.

The Walmart customer is the very definition of the term “late adopter.” Many are there only because unlike Amazon, Wal-Mart accepts cash and Food Stamps.

Still, if Walmart can, in any way, crack the online nut, it would be a turbocharger for growth. It moved in this direction with the acquisition of Jet.com for $3 billion, a cutting-edge e-commerce firm based in Hoboken, NJ.

However, this remains a work in progress. Online sales account for only 4% of Walmart’s total. But they could only be a few good hires at the top away from success.

Microsoft (MSFT)

Talk about going from being the 800-pound gorilla to an 80 pound one, and then back to 800 pounds.

I don’t know why Microsoft (MSFT) lost its way for 15 years, but it did. Blame Bill Gates’s retirement from active management and his replacement by his co-founder Steve Ballmer.

Since Ballmer’s departure in 2014, the performance of the share price has been meteoric, rising by some 125% over the past two years.

You can thank the new CEO Satya Nadella who brought new vitality to the job and has done a complete 180, taking Microsoft belatedly into the cloud.

Microsoft was never one to take lightly. Windows still powers 90% of the world’s PCs. No company can function without its Office suite of applications (Word, Excel, and PowerPoint). SQL Server and Visual Studio are everywhere.

That’s all great if you want to be a public utility, which Microsoft shareholders don’t.

LinkedIn, the social media platform for professionals, could be monetized to a far greater degree. However, specialization does come at the cost of scalability.

It seems that the future is for Microsoft to go head to head against next door neighbor Amazon (AMZN) for the cloud services market while simultaneously duking it out with Alphabet (GOOGL).

My bet is that all three win.

Airbnb

This is another new app that has immeasurably changed my life for the better. Instead of cramming myself into a hotel suite with a wildly overpriced minibar for $600 a night, I get a whole house for $300 anywhere in the world, with a new local best friend along with it.

Overnight, Airbnb has become the world’s largest hotel chain without actually owning a single hotel. At its latest funding round in 2017, it was valued at $31 billion.

The really tricky part here is for the firm to balance out supply and demand in every city in the world at the same time. It is also not a model that lends itself to vertical integration. But who knows? Maybe priority deals with established hotels are to come.

This is another firm that is battling local regulation, that great barrier to technological innovation. None other than its home town of San Francisco now has strict licensing requirements for renters, a 30 day annual limitation, and a $1,000 a day fine for offenders.

The downtowns of many tourist meccas like Florence, Italy and Paris, France have been completely taken over by Airbnb customers, driving rents up and locals out.

IBM (IBM)

There was a time in my life when IBM was so omnipresent we thought like the Great Pyramids of Egypt it would be there forever. How times change. Even Oracle of Omaha Warren Buffet became so discouraged that he recently dumped the last of his entire five-decade long position.

A recent 20 consecutive quarters of declining profits certainly hasn’t helped Big Blue’s case. It is one of the only big technology companies whose share price has gone virtually nowhere for the past two years.

IBM’s problem is that it stuck with hardware for too long. An entrenched bureaucracy delayed its entry into services and the cloud, the highest growth areas of technology.

Still, with some $80 billion in annual revenues, IBM is not to be dismissed. Its brand value is still immense. It still maintains a market capitalization of $144 billion.

And it has a new toy, Watson, the supercomputer named after the company’s founder, which has great promise, but until now has remained largely an advertising ploy.

If IBM can reinvent itself and get back into the game, it has FANG potential. But for the time being, investors are unimpressed and sitting on their hands.

The Big Telecom Companies

My final entrant in the FANGstakes would be any combination of the four top telecommunication companies, Verizon (VZ), AT&T (T), Comcast (CMCSA), and Time Warner (TWX), which now control a near monopoly in the US.

There is a reason why the administration is blocking the AT&T/Time Warner merger, and it is not because these companies are consistently cited in polls as the most despised in America. They are trying to stop the creation of another hostile FANG.

Still, if any of the big four can somehow get together, the consequences would be enormous. Ownership of the pipes through which the modern economy courses bestows great power on these firms.

And Then….

There is one more FANG possibility that I haven’t mentioned. Somewhere, someplace, there is a pimple-faced kid in a dorm room thinking up a brand-new technology or business model that will take the world by storm and create the next FANG.

Call me crazy, but I have been watching this happen for my entire life.

I want to thank my friend, Scott Galloway, of New York University’s Stern School of Business, for some of the concepts in this piece. His book, “The Four” is a must read for the serious tech investor.

Creating the Next FANG?