Global Market Comments

March 29, 2019

Fiat Lux

SPECIAL FANG ISSUE

Featured Trade:

(FINDING A NEW FANG),

(FB), (AAPL), (NFLX), (GOOGL),

(TSLA), (BABA)

Global Market Comments

March 29, 2019

Fiat Lux

SPECIAL FANG ISSUE

Featured Trade:

(FINDING A NEW FANG),

(FB), (AAPL), (NFLX), (GOOGL),

(TSLA), (BABA)

Mad Hedge Technology Letter

March 25, 2019

Fiat Lux

Featured Trade:

(APPLE’S BIG PUSH INTO SERVICES)

(AAPL), (GS), (NFLX), (GOOGL), (ROKU)

The future of Apple (AAPL) has arrived.

Apple has endured a tumultuous last six months, but the company and the stock have turned the page on the back of the anticipation of the new Apple streaming service that Apple plans to introduce next week at an Apple event.

The company also recently announced a partnership with Goldman Sachs (GS) to launch an Apple-branded credit card.

In the deal, Goldman Sachs will pay Apple for each consumer credit card that is issued.

These new initiatives indicate that Apple is doing its utmost to wean itself from hardware sales.

Effectively, Apple's over-reliance on hardware sales was the reason for its catastrophic winter of 2018 when Apple shares fell off a cliff trending lower by almost 35%.

This new Apple is finally here to save the day and will demonstrate the high-quality of engineering the company possesses to roll out such a momentous service.

Frankly speaking, Apple needs this badly.

They were awkwardly wrong-footed when Chinese consumers in unison stopped buying iPhones destroying sales targets that heaped bad news onto a bad situation.

I never thought that Apple could pivot this quickly.

Apple's move into online streaming has huge ramifications to competing companies such as Roku (ROKU).

In 2018, I was an unmitigated bull on this streaming platform that aggregates online streaming channels such a Sling TV, Hulu, Netflix and charges digital advertisers to promote their products on the platform through digital ads.

I believe this trade is no more and Roku will be negatively impacted by Apple’s ambitious move into online streaming.

What we do know about the service is that channels such as Starz and HBO will be subscription-based channels that device owners will need to pay a monthly fee and Apple will collect an affiliate commission on these sales.

Apple needs to supplement its original content strategy with periphery deals because Apple just doesn’t have the volume to offer consumers a comprehensive streaming product like Netflix.

Only $1 billion on original content has been spent, and this content will be free for device owners who have Apple IDs.

Apple's original content budget is 1/9 of Netflix annual original content budget.

My guess is that Apple wants to take stock of the streaming product on a smaller scale, run the data analytics and make some tough strategic decisions before launching this service in a full-blown way.

It's easier to clean up a $1 billion mess than a $9 billion mess, but knowing Apple and its hallmarks of precise execution, I'd be shocked if they make a boondoggle out of this.

Transforming the company from a hardware to a software company will be the long-lasting legacy of Tim Cook.

The first stage of implementation will see Apple seeking for a mainstay show that can ingrain the service into the public's consciousness.

Netflix was a great example, showing that hit shows such as House of Cards can make or break an ecosystem and keep it extremely sticky ensuring viewers will stay inside a walled pay garden.

Apple hopes to convince traditional media giants such as the Wall Street Journal to place content on Apple's platform, but there has already been blowback from companies like the New York Times who referenced Netflix’s demolition of traditional video content as a crucial reason to avoid placing original content on big tech platforms.

Netflix understands how they blew up other media companies and don’t expect them to be on Apple’s streaming service.

They wouldn’t be caught dead on it.

Tim Cook will have to run this race without the wind of Netflix’s sails at their back.

Netflix has great content, and that content will never leave the Netflix platform come hell or high water.

Apple is just starting with a $1 billion content budget, but I believe that will mushroom between $4 to $5 billion next year, and double again in 2021 to take advantage of the positive network effect.

Apple has every incentive to manufacture original content if third-party original content is not willing to place content on Apple's platform due to fear of cannibalization or loss of control.

Ultimately, Apple is up against Netflix in the long run and Apple has a serious shot at competing because of the embedment of 1 billion users already inside of Apple's iOS ecosystem that can easily be converted into Apple streaming service customers.

If you haven't noticed lately, Silicon Valley's big tech companies are all migrating into service-related SaaS products with Alphabet (GOOGL) announcing a new gaming product that will bypass traditional consoles and operate through the Google Chrome browser.

Even Walmart (WMT) announced its own solution to gaming with a new cloud-based gaming service.

I envision Apple traversing into the gaming environment too and using this new streaming service as a fulcrum to launch this gaming product on Apple TV in the future.

The big just keep getting bigger and are nimble enough to go where internet users spend their time and money whether it's sports, gaming, or shopping.

Apple is no longer the iPhone company.

I have said numerous times that Apple's pivot to software was about a year too late.

The announcement next week would have been more conducive to supporting Apple’s stock price if it was announced the same time last year, but better late than never.

Moving forward, Apple shares should be a great buy and hold investment vehicle.

Expect many more cloud-based services under the umbrella of the Apple brand.

This is just the beginning.

Mad Hedge Technology Letter

March 19, 2019

Fiat Lux

Featured Trade:

(GOOGLE’S AGGRESSIVE MOVE INTO GAMING),

(GOOGL), (AAPL), (FB), (NFLX), (MSFT) (EA), (TTWO), (ATVI)

The saturation of tech is upon us.

That is the takeaway from Google’s (GOOGL) hard pivot into gaming.

The goal of their new gaming service is to become the Netflix (NFLX) of gaming allowing gamers to skip purchasing third-party consoles and playing games directly from an Android-based Google device.

Middlemen in the broad economy are getting killed and this is the beginning.

What we are really seeing is a last-ditch effort to protect gaming consoles - these devices will become extinct in less than 20 years boding ill for companies such as Sony and Nintendo

The cloud is still all the rage and companies such as Microsoft (MSFT), Alphabet (GOOGL), and Apple (AAPL) have the natural infrastructure in place to offer cloud-based gaming solutions.

Phenomenon such as internet game Fortnite have shown that consoles are outdated and relying on the cloud as a fulcrum to extract gaming revenue by way of add-ons and in-game enhancements will be the way forward

Another key takeaway from this development is that passive investment is dead, even more so in tech, where these big tech companies are starting to bleed over into each other's territory.

This dispersion will create opportunity and pockets of weakness.

I blame this on a lack of innovation with companies still trying to extract as much as they can from the current smartphone-based status quo which has pretty much run its course.

Technology is itching for something revolutionary and we still have no idea what that new idea or device will be.

The rollout of 5G is promising and companies will need some time to adapt to this super-fast connection speed.

In either case, I can tell you the revolution won’t include foldable smartphones.

In 2018, the gaming industry flourished on accelerating momentum by registering over $136 billion in sales, and the revenue growth rate is already about 15% and increasing.

Naturally, companies such as Amazon and Google want a piece of this action and are hellbent on making inroads in the gaming environment such as Amazon's ownership of Twitch, which is a game streaming service where viewers can watch live tournament-style competitions proving extremely popular with Generation Z.

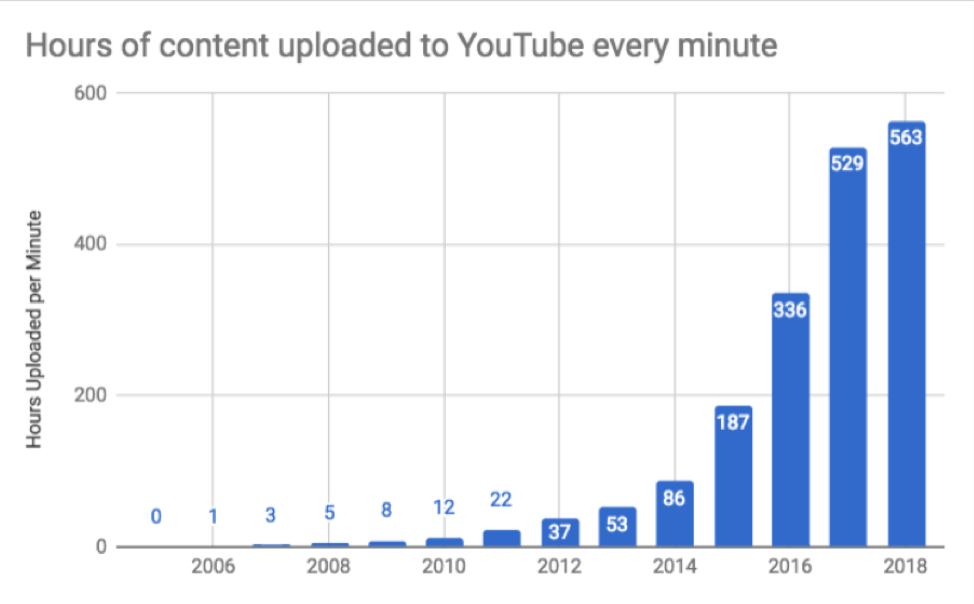

I applaud this move by Google because they already have proved they can execute on certain mature assets such as YouTube which has become the Netflix replacement of 2019.

Doubling down in the gaming sector would be a bonus as they search a second accelerating revenue driver that will dovetail nicely with the overperformance in YouTube this year.

It’s even possible that YouTube could be modified to support live stream gaming, certainly various synergistic dynamics are at play here.

Even if they fail - it's worth the risk.

Revenue extraction will be painful for certain companies like Facebook (FB) in this new environment, who has seen a horde of top executives abort after the company drastically changed directions, believing the company is on a suicide mission to fines and more regulatory penalties.

I've mentioned in the past that Facebook no longer commands the same type of employee brand recognition they once cultivated.

Facebook will find a tougher time to find the right people they need to execute their private chat plan, by linking the likes of WhatsApp, Instagram, and Facebook Messenger.

This is a high-risk high-reward proposition that could end up with Facebook's co-founder Mark Zuckerberg in tears if regulators give him the cold shoulder, and that is why many executives who are risk-adverse want to cash in now because they sink with the Titanic.

Not only are gaming assets becoming saturated, but the general online streaming environment is attracting a tsunami of supply all at one time.

Online content is already veering into the same type of pricing structures that cable offered traditional customers.

Investors will have to ask themselves, how much will the average consumer spend in content-based entertainment per month?

My guess is not more than $100 per month.

The saturation will cause tech companies to become even more draconian.

Be prepared for some more epic in-fighting until a new gateway of internet monetization opens up.

There has never been a better time to be a tactical and active investor in tech.

The Fang trade has splintered off with each company facing unpredictable futures.

Unearthing value will become more difficult because these traditional bellwether tech stocks have decoupled and aren't going straight up anymore.

Those zigs and zags will still be buttressed by a secular tailwind of the migration to digital, but there are certain winners and losers that will result of this.

Apple announcing a new streaming product is proof that these Silicon Valley tech firms are desperate for new profit drivers as the woodchips that fuel the fire start to run noticeably short on supply.

At the bare minimum, this looks disastrous for the traditional gaming companies of Electronic Arts (EA), Take-Two Interactive (TTWO), and Activision (ATVI) whose shares have been effectively shelved due to the Fortnite revolution.

EA has fought back with their own Fortnite lookalike called Apex Legends which showed a Fortnite-like trajectory sucking in 10 million players in the first 72 hours.

The stock exploded 16%, signaling this is the new way forward for gaming companies.

As a whole, these traditional gaming studios simply don’t have the firepower to compete with the big boys, let alone possess a strong cloud infrastructure.

Mad Hedge Technology Letter

March 18, 2019

Fiat Lux

Featured Trade:

(WHY ALPHABET IS THE BEST FANG TO BUY NOW),

(GOOGL), (NFLX), (FB), (TWTR), (DIS)

Why am I bullish on Alphabet (GOOGL) short-term?

Video has muscled its way to the peak of the digital content value chain.

If you don't have video streaming, then you are significantly depriving yourself of the necessary ammunition capable of battling against legitimate content originators.

The optimal type of content is short form yet engaging.

Interesting enough, the format method integrated into systems of Facebook (FB) and Twitter (TWTR) has experienced unrivaled success.

They have been leaning on this model as growth levers that will take them to the next stage of revenue acceleration and rightly so.

This has seen smartphone apps such as Instagram become game-changing revenue machines destroying all types of competition.

The x-factor that stands out in Instagram's, Facebook’s, YouTube’s model is that it's free and they do not absorb heavy expenses from content creation.

It’s certainly cheap when the user is the product.

Google’s YouTube service has morphed into something of a phenomenon.

Its interface is easy to use, and followers have a simple time navigating around its platform.

Familiar news outlets such as Sky News, Bloomberg News, and even CNBC news have recently installed their live feeds on YouTube's main platform scared of losing aggregate eyeballs.

And even more intriguing is that YouTube has become a legitimate competitor to Netflix's (NFLX) online video streaming platform.

YouTube has sensed the outsized pivot to their free platform and has double down hard by installing 5-second ads at the front end and middle of videos.

Of Alphabet’s total $39.3 billion revenue pocketed in Q4 2018, ads constituted 83% or an astounding $32.6 billion.

I feel that Alphabet shares are currently undervalued, and I believe that we will see outperformance from Alphabet shares for the rest of 2019 based on YouTube's performance relative to expectation.

YouTube’s ever-growing presence showing up in the top line will offer the growth investors desire to pile into these shares as the company wrestles with future projects such as Waymo.

That's not to say that their traditional advertisement business of Google Search is failing.

Investors can expect continuous 20% to 25% growth in this cash cow business, but the reason why Alphabet share has not been able to break out is that investors have baked this into the pie.

Therefore, YouTube is really the X Factor and will take them to this new promised land with shares surging past the $1,250 mark and more importantly, staying at that level.

YouTube brought in about $15 billion in 2018 and that consisted of about 10% of Alphabet’s total annual revenue.

However, the company is just scratching its surface of what it can accomplish with this fast-growing revenue driver and I can extrapolate this growth segment turning into 20% or 25% of the company’s annual revenue in the next few years.

Google does not strip out YouTube revenue in its reporting, therefore, it's difficult to put my finger on exactly how much YouTube is carving out in terms of revenue.

I can also assume that if Netflix continues to raise the cost of monthly subscription, this strategy will directly hurt its revenue acceleration ability as it relates to competing with Google's YouTube because YouTube's free service is demonstrably attractive to viewers hoping to discover high-quality content relative to a $20 per month Netflix subscription.

I do agree that Netflix is a great company and a great stock, but as they slowly raise the price of content, this will gift YouTube a huge chunk of Netflix’s marginal audience freeing itself from the shackles of Netflix’s price rises.

At some point, online video streaming will become as expensive as the cable bundles now, and at that point, we know that saturation is imminent boding negative for Netflix.

What I do envision in the short-term future are consumers in America will pay into several unique bundles such as Netflix, maybe Disney (DIS), ESPN and merely stick with these as their base content generators as more consumers cut their cord and hard pivot from traditional cable packages that are becoming less appealing by the day.

And don't forget that at some point, Netflix will have to demonstrate profitability and the huge cash burn that permeates throughout the business will be exposed when subscription growth starts to fade away.

In every possible variant, YouTube will become an outsized winner in the media wars because the quality of the free content keeps improving, the cost for consumers stays at 0, and their best of breed ad tech migrating from their Google search into YouTube just keeps getting more surgical and efficient.

Not only are the positive synergies from the best of breed ad tech aiding YouTube’s model, but just think about YouTube having access to the Google cloud and saving expenses by accessing this function to store data onto the Google Cloud.

If this was a standalone service, they would have to subcontract cloud storage functions to third-party cloud company causing the content service to spend millions and millions of dollars per year in expenses.

This would have the potential of crushing the bottom line.

That is just one example of the synergies that Google can take advantage of with YouTube under its umbrella of assets.

And think about self-driving vehicles, Google could potentially equip YouTube as a pre-programmed application inside of autonomous vehicle platform tech with YouTube popping up on the multiple screens.

I assume that there will be multiple screens inside of cars with self-phone driving technology because of the lack of driving required.

The worst maneuver that Alphabet could do right now is spinoff YouTube into its own company, and if that happens, YouTube won't be able to take advantage of the various synergies and benefits of being an Alphabet asset.

We are just scratching the surface of what YouTube can accomplish, and I believe this upcoming overperformance isn’t in the price of the stock yet.

If the Fed continues its “patient” strategy towards interest rates at a macro level, Alphabet will easily soar past $1,250 and it can easily gain another 10% in 2019.

If any “regulation” risk as a result of extremist content rears its ugly head, buy shares on the dips because the algorithms are in place to eradicate this material and any fine will be manageable.

Global Market Comments

March 6, 2018

Fiat Lux

Featured Trade:

(WILL UNICORNS KILL THE BULL MARKET?),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

(A NOTE ON OPTIONS CALLED AWAY), (TLT)

Mad Hedge Technology Letter

February 12, 2019

Fiat Lux

Featured Trade:

(MEET YOUR HOME OF THE FUTURE),

(KASITA),

(PLEASE SIGN UP NOW FOR MY FREE TEXT ALERT SERVICE NOW)

Mad Hedge Technology Letter

February 11, 2019

Fiat Lux

Featured Trade:

(HOW FORTNITE IS TAKING OVER THE GAMING WORLD),

(TTWO), (EA), (ATVI), (NFLX), (FORTNITE)