Global Market Comments

December 5, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOOD MARKET AND THE BAD MARKET)

(TLT), (XOM), (OXY), (TSLA), (SPY), (BABA), (BIDU), (KBH), (PHM), (LEN), (AAPL)

Global Market Comments

December 5, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOOD MARKET AND THE BAD MARKET)

(TLT), (XOM), (OXY), (TSLA), (SPY), (BABA), (BIDU), (KBH), (PHM), (LEN), (AAPL)

I usually write my Monday strategy letters in the middle of the night in my mind, from 2:00 AM to 3:00 AM, because my feet are too hot, too cold, or because my hip hurts. Then I go back to sleep. If I remember half of it the next morning, then I get a great letter.

I often like to refer to old proven market nostrums and show how true they really are. One of my favorites is the concept of the “good” market and the “bad” market.

The good market is the one for bonds. Vastly more research goes into bonds than stocks because that’s where the respectable, safe, widows and orphan money goes. Global bond markets are also far bigger, worth about $120 trillion. Bond traders usually began their journey at Harvard or Wharton, speak with clipped upper-class accents, and belong to exclusive private clubs that would never let you in for lunch, even with an invitation from a member.

Suffice it to say that the bond market is always right. Their relaxed lifestyle can be explained by the fact that they really only have two variables to look at, Fed policy and the actual supply and demand for money. Working in the bond market is almost like a sinecure, sending you a paycheck every month because you are entitled to it.

The stock market is the complete opposite.

While the bond market was polishing the teacher’s apple at the head of the class, the stock market was smoking cigarettes in the bathroom, endlessly catching detention. The stock market is also smaller, worth about $50 trillion. While bond traders are attending their Rotary meetings, stock traders binge drink and tear up the roads with their new Porsches and Ferraris.

Needless to say, stock traders are always wrong.

That’s because they face a hopeless dilemma. While bond traders have to contemplate only two variables, stock traders have to deal with millions. They have to cope with the hundreds of input variables per company that affect their earnings, and there are over 3,000 companies that trade in the US alone.

To illustrate the point, look at the recent market action.

Both markets have been driven by the same massive liquidity created by the government since 2009. The bond market peaked in August 2020 when it saw the free lunch of ultra-low interest rates soon ending. Stocks didn’t peak until January 2021, some 17 months later. It’s clear that stock traders suffer from a severe learning disorder.

And they’re doing it again.

After a 49% swan dive over two years plus, bonds bottomed on October 14. Stocks may not finally bottom until the spring, six months after bonds. Bonds are now betting that the recession has already begun, we just haven’t seen it in the data yet. Stocks are betting that the recession doesn’t start until 2023, if at all. That’s why it’s been going up.

As for me, I have traded both stocks AND bonds. That’s because before there were stocks, there were bonds as the only thing to trade. As you may recall, stocks were moribund in the 1970s. On top of that, you can add foreign exchange, precious metals, commodities, and volatility. There essentially isn’t anything I haven’t traded.

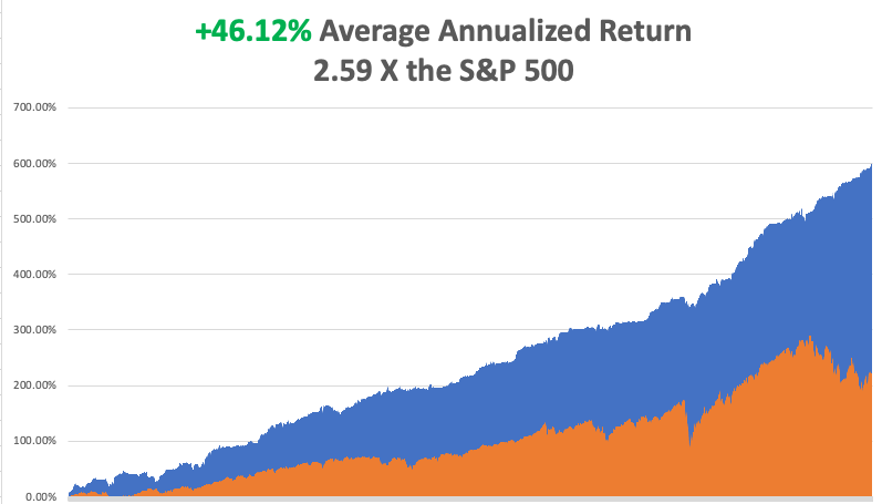

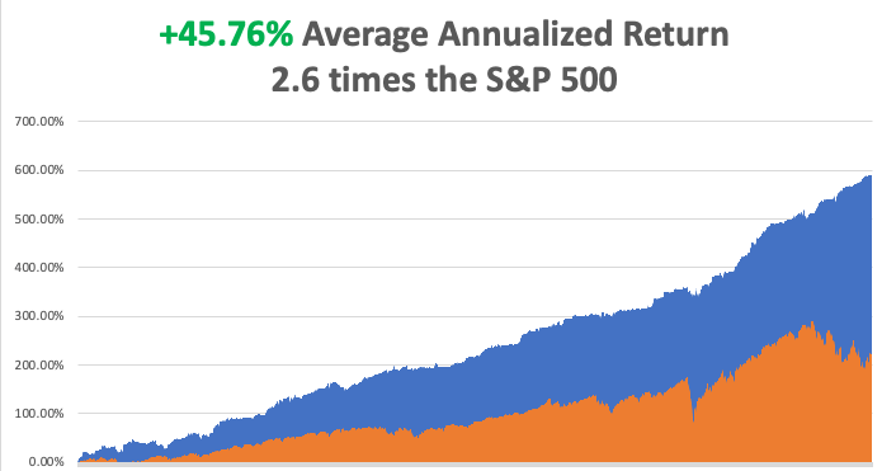

My performance in December has so far tacked on another robust +3.37%. My 2022 year-to-date performance ballooned to +87.05%, a spectacular new high. The S&P 500 (SPY) is down -13.61% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +104.88%.

That brings my 14-year total return to +599.61%, some 2.60 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +46.12%, easily the highest in the industry.

I took profits in my triple weighting in bonds last week (TLT), booking some serious profits. All my remaining positions are profitable, shorts in (XOM), (OXY), (TSLA), (SPY), and one long in (TSLA), with 50% cash for a 30% net short position. We’ve just had a great run and the time to pay the piper is fast approaching.

With an +87.05% profit in hand this year, I don’t get a lot of complaints. However, I have been getting some lately because my trade alerts can be hard to get into.

Of course, it can be challenging to execute when 6,000 subscribers are trying to get into the same position at the same time. But when the entire world joins in, that raises the difficulty to a whole new level.

That is what happened with my trade alert to BUY the (TLT) on November 18. It was the trade alert around the world and the next day, bonds rocketed by $3.50. I laddered in with more positions with higher strike prices getting to a triple long in the bond market. When your trade alerts have a 95% success rate, that is what happens. It is the price of being right, which is better than the alternative.

When I first entered this trade, I thought the ten-year US Treasury yield would plunge from 4.46% to 2.50% by June 2023, taking the (TLT) from $91 to $120.

With the (TLT) at $108 on Friday and the ten-year yield at 3.50%, we are already halfway there. If I AM right and bond yields drop to 2.50%, the 30-year fixed mortgage rate will also drop below 4.00% and you can forget about any real estate crash. That's why the homebuilders (LEN), (KBH), and (PHM) are up 30%-40% since October.

With the ballistic moves in some Chinese stocks over the last two weeks (Alibaba (BABA) up 58%, Baidu ((BIDU) adding 47%, I have received a surge in inquiries about the prospects of the US going to war with the Middle Kingdom.

I have been asked this question continuously for the last 50 years, by several Presidents of the United States on down, and my answer is always the same.

There is not a chance.

The reason is very simple. The Chinese can’t feed themselves. They have not been able to do so for 100 years. With a population of 1.2 billion, the Chinese will never be able to feed themselves.

That means the Chinese are highly dependent on international trade to finance their food imports. When trade is vibrant, China prospers.

When it doesn’t, they start stacking up the bodies like cordwood for mass cremation, as happened when China suffered its last major famine. I know because I was there in the 1970s, and I’ll never forget that smell. As you quickly learn during a famine, there is no substitute for food.

So, what are the chances of China bombing their food supply? I’d say zero. A disruption of even a few months and people start to go hungry. Will they bluff, bluster, and obfuscate for domestic consumption? Every day of the year and that is what they are doing now.

As for buying Chinese stocks, I think I’ll pass for now. There are just too many great American ones on sale. The Chinese moves above are only taking place after horrific declines, 78% for (BABA), and 81% for (BIDU).

And before I go on to the data points, I want to recall a funny story.

One day in London 40 years ago, one of my junior traders at Morgan Stanley walked in with a big smile on his face. He had just gotten a great deal on a Ferrari Testarossa, which then retailed at $360,000, a lot of money for a 25-year-old East Ender in those days.

I thought to myself, “There are no great deals on Ferraris.”

A few months later, he totaled the Ferrari after a late night of binge drinking and racing on London’s damp streets, breaking the vehicle cleanly in half. The insurance company determined that his car was in fact two different Ferraris with two different VIN numbers that had been welded together. The car had split apart at the welds.

Some clever entrepreneur took the intact front end of a rear-ended car and the pristine back half of a car with destroyed hood and made one whole good Ferrari. Since my trader had only insured one car and not two, the insurance company refused to honor the claim.

All I can say is “Beware of friends bearing false Ferraris.”

Nonfarm Payroll Report Comes in Hot in November at 263,000, socking markets for 500 points. A December rate hike of 75 basis points has been firmly put back on the table. The Headline Unemployment Rate stays at a near-record high 3.7%. Average Hourly Earnings were up an inflationary 0.6%. Wages are up 5.1% YOY. The dollar soared on the prospect of higher rates for longer.

JOLTS Job Openings Report Comes in Weaker at 10.33 million in October, down 353,000 from September. High interest rates are finally taking their toll. There are still 1.7 job openings per applicant.

Key Inflation Read Drops, the Personal Consumption Expenditures Price Index falling 0.2% in October, excluding food and energy. It sets up a weak CPI on December 13, which would be very stock market positive.

Powell Turns Dovish, well, sort of, indicating that smaller interest rate hikes could start in December. The comments were made at a Brookings Institution meeting on Wednesday. Stocks rallied big on the news.

US to Ease Venezuela Sanctions, allowing Chevron to resume pumping there for six months after a three-year hiatus. It’s an out-of-the-blue big negative for oil prices. Venezuelan oil production has plunged from 2.1 million barrels a day to only 679, 000 thanks to gross mismanagement of the economy. But beggars can’t be choosers on the energy front. Good thing I’m running a double short in the sector. It’s the last think OPEC plus wanted to hear.

Don’t Expect a Housing Crash, as the financial system was vastly stronger than it was in 2008. A mild recession is already priced in, and bank balance sheets are rock solid. Buy the homebuilders on the next dips now coming off from horrific earnings, (KBH), (PHM), and (LEN).

Don’t Expect an iPhone 14 for Christmas, as pandemic-driven production shutdowns and Foxconn riots in China crimp supplies. It could be a longer wait if you want the new deep purple color. Avoid (AAPL) for now. I expect another big tech dive in 2023.

China Riots Tank Market, raising the specter of extended supply chain problems, especially for Apple (AAPL). Oil was especially hard hit as China is its largest buyer, hitting a two-year low and giving up all 2022 gains. China seems to be sacrificing its older generation, not giving them priority for vaccinations which don’t work anyway. This isn’t going away in a day. Transition to India will take a decade.

Case Shiller Plunges, the National Home Price Index Taking a 1.2% hit in September to 10.6%. Miami, Tampa, and Charlotte, NC showed the biggest YOY increases. You know the reasons why.

Home Rentals to Stay Sticky at Record Levels, with gains at 25-35% over the past 24 months. Homebuyers frozen out of the market by record-high interest rates are forced to rent at any price.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, December 5 at 8:00 AM EST, the ISM Nonmanufacturing PMI for November is out.

On Tuesday, December 6 at 8:30 AM, the Mad Hedge Traders & Investors Summit begins. Click here to register.

On Wednesday, December 7 at 7:30 AM, the Crude Oil Stocks are announced. It’s pearly Harbor Day.

On Thursday, December 8 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Producer Price Index for November.

On Friday, December 9 at 8:30 AM, the Producer Price Index for November. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, I am sitting here in front of the fire at my place in the Berkeley Hills and it is freezing cold and pouring rain outside. Heaven knows we need it.

I’m going to San Francisco later today to do some Christmas shopping. It’s not the ideal time but in my hopelessly busy schedule, this was the only day this year allocated for this chore.

For some reason, last night I recalled my days as an Ivy League Princeton professor, which I hadn’t thought about for decades.

When Morgan Stanley was a private partnership, before it went public in 1987, the firm represented the cream of the US establishment. There wasn’t anyone in business, industry, or politics you couldn’t reach through one of the company’s endless contacts. We referred to it as the “golden Rolodex.”

One day in the early 1980s, a managing director asked me a favor. Since he had landed me my job there, I couldn’t exactly say no. He had committed to teaching a graduate night class in International Economics at his alma mater, Princeton University, but a scheduling conflict had prevented him from doing so.

Since I was then the only Asian expert in the firm, could I take it over for him? If I had extra time to kill, I could always spend it in the Faculty Club.

I said “sure.”

So, the following Wednesday found me at Penn Station boarding a train for the leafy suburb about an hour away. On the way down, I passed the locations of several Revolutionary War battles. When we pulled into Princeton, I realized why they called these places “piles”. The gray stone ivy-covered structures looked like they had been there a thousand years.

My students were whip-smart, spoke several Asian languages, and asked a ton of questions. Many came from the elite families who owned and ran Asia. I understood why my boss took the gig.

I turned out to be pretty popular at the faculty Club, with several profs angling for jobs at Morgan Stanley. Rumors of the vast fortunes being made there had leaked out.

Princeton was weak in my field, DNA research. But as the last home of Albert Einstein, it was famously strong in math and physics. Many of the older guys had worked with the famed Berkeley professor, Robert Oppenheimer, on the Manhattan Project.

I was still a mathematician of some note those days, so someone asked me if I’d like to meet John Nash, the inventor of Game Theory, which won him a Nobel Prize in Economics in 1994. Nash’s work on partial differential equations became the basis for modern cryptography. I was then working on a model using Game Theory to predict the future of stock markets. It still works today and is the basis the Mad Hedge Market Timing Algorithm.

Weeks later found me driven to a remote converted farmhouse in the New Jersey countryside. On the way, I was warned that Nash was a bit “odd,” occasionally heard voices speaking to him, and rarely came to the university.

I later learned that his work in cryptography had driven him insane, given all the paranoia of the 1950s. Having worked in that area myself, that was easy to understand. His friends hoped that by arguing against his core theories, he would engage.

When I was introduced to him over a cup of tea, he just sat there passively. I realized that I was going to have to take the initiative so as a stock market participant, I immediately started attacking Game Theory. That woke him up and started the wheels spinning. It hadn’t occurred to him that game theory could be used to forecast stock prices.

His friends were thrilled.

I later went on to meet many Nobel Prize winners, as the Nobel Foundation was an early investor in my hedge fund. Whenever a member of the Swedish royal family comes to California, I get an invitation to lunch for the Golden State’s living Nobel laureates. It turns out that 20% of all the Nobel Prizes awarded since its inception live here. Last time, I sat next to Milton Friedman, and I argued against HIS theories.

The other thing I remembered about my Princeton days is my discovery of the “professor's dilemma.” Sometimes a drop-dead gorgeous grad student would offer to go home with me after class. I was happily married in those days with two kids on the way, so I respectfully declined, despite my low sales resistance.

No away games for me.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Nobel Prize

Global Market Comments

November 28, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or LOOKING FOR BIG FOOT),

(NVDA), (VIX), (TLT), (TSLA), (XOM),

(OXY), (TSLA), (SPY), (MA), (V), (AXP)

On October 14, investors finally achieved the portfolios they long desired, not only individuals but institutional ones as well. They got rid of stocks and bonds that had been hobbling them all year and built their cash positions to decade highs.

What happened the next day?

Stocks and bonds went straight up for six weeks. Cash became trash.

For October 14 was the day that the stock market discounted the worst-case economic scenario for 2023, no matter how bad it may get. And it probably won’t get very bad. That’s barring a black swan-type event, like a brand-new global pandemic.

If you think your job can be frustrating, how about mine? If you run with the dumb crowd, the uninformed crowd, the loser crowd, you get your just desserts.

Fortunately, I saw these moves coming a mile off and loaded the boat. I’ve actually made more money on the parabolic move in bonds than some of the enormous moves in stocks. NVIDIA (NVDA) up 50%?

My performance in November has so far tacked on another robust +7.05%. My 2022 year-to-date performance ballooned to +82.42%, a spectacular new high. The S&P 500 (SPY) is down -16.85% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +94.61%.

That brings my 14-year total return to +594.98%, some 2.60 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +45.76%, easily the highest in the industry.

I am going into the month-end surge with a fairly aggressive 40% long, (TLT), (TSLA), 40% short (XOM), (OXY), (TSLA), (SPY), with 20% crash for a totally market-neutral position. We’ve just had a heck of a run, and prices could well stall not far from here for the short term. The post-election rally happened, as predicted in this space.

Like Big Foot, the Yeti, and the Loch Ness Monster, the Fed pivot may soon actually make an appearance. I’m talking months, not years. That’s when our August central bank flips from the most severe tightening of interest rates in history, to a neutral, or one can only pray, an easing stance. This is what the 15% rally in stocks over the last six weeks has been all about.

And here is another old-time worn market nostrum. If investors sense that something is going to happen, they discount it fast, very fast.

Of course, there will be several false starts, denied rumors, and false flags, as there always are. After all, this is my 11th bear market. These will create sudden panic attacks, market selloffs, and Volatility Index (VIX) runs to $30 which are the license to print money for the Mad Hedge Fund Trader. Wait for the market to tell you when to trade. Ignoring it can prove expensive.

As we say here in the west, go off the reservation and you can get a lot of arrows stuck in your back.

How is this even remotely possible with the money supply only at $21.4 trillion, down 2% YOY? That’s a buzz cut from the +30% rate from a year ago.

The answer is that the money is out there, just hiding in different unrecognizable forms. Much of the $4 trillion in pandemic stimulus payments have yet to be spent. Inflation has added $2 trillion in new corporate profits through higher sales prices. Similarly, there is also another $1.5 trillion in pay increases bubbling through the system, also inspired by inflation.

You see this is booming credit card spending, much to the joy of Master Card (MA), Visa (V), and American Express (AXP) and their share price surges we have recently seen.

As I keep telling my Concierge customers on the phone, there is no playbook anymore. All the old ones have been rendered useless by the pandemic. To succeed and make windfall profits like me, you basically have to make it up as you go along.

The Fed Favors the Slowing of Rate Hikes, making a December increase of only 50 basis points a sure thing, according to minutes released on Wednesday for the prior meeting. Housing especially is taking a big hit. All interest rate plays, like bonds, rallied strongly.

Equities See Monster Inflows, some $23 billion in 35 weeks according to the Bank of America (BAC) flow of funds survey. There have been huge cash flows out of Europe looking for a stronger dollar, fleeing WWIII, and collapsing home currencies. The big chase is on. Time to go short? I am. It could be a big bull trap.

Leading Economic Indicators Dive, off 0.8% in October, double the decline expected and the weakest since the pandemic low in April 2020. There has only been one positive number in this data series in 2022. You have to go back to the financial crisis to find numbers this bad.

S&P Global Manufacturing PMI Takes a Hit in November, down to 47.6 from an estimate of 50. Services fell from 48 to 46.1. It’s another coincident recession indicator.

Existing Home Sales Plunge 5.9% in October to an annualized rate of 4.43 million units. It is the slowest sales pace in 11 years. It's not as bad as expected but is still down a horrific 28.4% YOY. Inventory fell to just 1.22 million units, only a 3.3-month supply, supporting prices in a major way. In fact, prices are still rising, up 6.6% annually to $379,100. Housing accounts for about 20% of the US economy, so here is your recession threat right here.

New Home Sales Come in Hot at 632,000, a real shocker with the 30-year fixed at 7.4%. Low-ball seller financing incentives must be a factor where they buy down rates to lower levels. Free upgrades, like those cherry wood cabinets, bonus rooms, and marble kitchen counters, also help. Prices are still up 15% YOY and inventories rose to a once unbelievable 8.9 months.

OPEC Plus Considering a 500,000 Barrels a Day Increase at their coming December meeting, which Saudi Arabia vehemently denied. The comments came out just as West Texas intermediate was barreling in on a new nine-month low. Saudi Arabia can talk all they want, but it’s tough to beat a coming recession, which every other hard asset class and commodity is now confirming.

Disney Axes Chairman, dumping Bob Chapek and bringing back Bob Iger from retirement. Losing $1.5 billion on the Disney Plus streaming service and losing its special tax status from the State of Florida has its costs. (DIS) is also not a stock to buy if we are going into recession. Avoid (DIS), despite the 10% move today. Let’s first see if Iger can cut costs.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, November 28 at 8:00 AM EST, the Dallas Fed Manufacturing Index for November is out.

On Tuesday, November 29 at 8:30 AM, the S&P Case Shiller National Home Price Index is released.

On Wednesday, November 30 at 8:30 AM, the ADP Private Employment Report for November is published. We also get a number on Q3 US GDP.

On Thursday, December 1 at 8:30 AM, the Weekly Jobless Claims are announced. US Personal Income and Spending for October is also out.

On Friday, December 2 at 8:30 AM, the Nonfarm Payroll Report for November is disclosed. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, by the 1980s, my mother was getting on in years. Fluent in Russian, she managed the CIA’s academic journal library from Silicon Valley, putting everything on microfilm.

That meant managing a team that translated over 1,000 monthly publications on topics as obscure as Artic plankton, deep space phenomenon, and advanced mathematics. She often called me to ascertain the value of some of her findings.

But her arthritis was getting to her, and all those trips to Washington DC were wearing her out. So I offered Mom a job. Write the Thomas family history, no matter how long it took. She worked on it for the rest of her life.

Dad’s side of the family was easy. He was traced to a small village called Monreale above the Sicilian port city of Palermo famed for its Byzantine church. Employing a local priest, she traced birth and death certificates going all the way back to an orphanage in 1820. It is likely he was a direct illegitimate descendant of Lord Nelson of Trafalgar.

Grandpa fled to the United States when his brother joined the Mafia in 1915. The most interesting thing she learned was that his first job in New York was working for Orville Wright at Wright Aero Engines (click here). That explains my family’s century-long fascination with aviation.

Grandpa became a tailer gunner on a biplane in WWI. My dad was a tail gunner on a B-17 flying out of Guadalcanal in WWII. As for me, you’ve all heard of plenty of my own flying stories, and there are many more to come.

My Mom’s side of the family was an entirely different story.

Her ancestors first arrived to found Boston, Massachusetts in 1630 during the second Pilgrim wave on a ship called the Pied Cow, steered by a Captain Ashley (click here).

I am a direct descendant of two of the Pilgrims executed for witchcraft in the Salem Witch Trials of 1692, Sarah Good and Sarah Osborne, where children’s dreams were accepted as evidence (click here). They were later acquitted.

When the Revolutionary War broke out in 1776, the original Captain John Thomas, who I am named after, served as George Washington’s quartermaster at Valley Forge responsible for supplying food to the Continental Army during the winter.

By the time Mom completed her research, she discovered 17 ancestors who fought in the War for Independence and she became the West Coast head of the Daughters of the American Revolution. It seems the government still owes us money from that event.

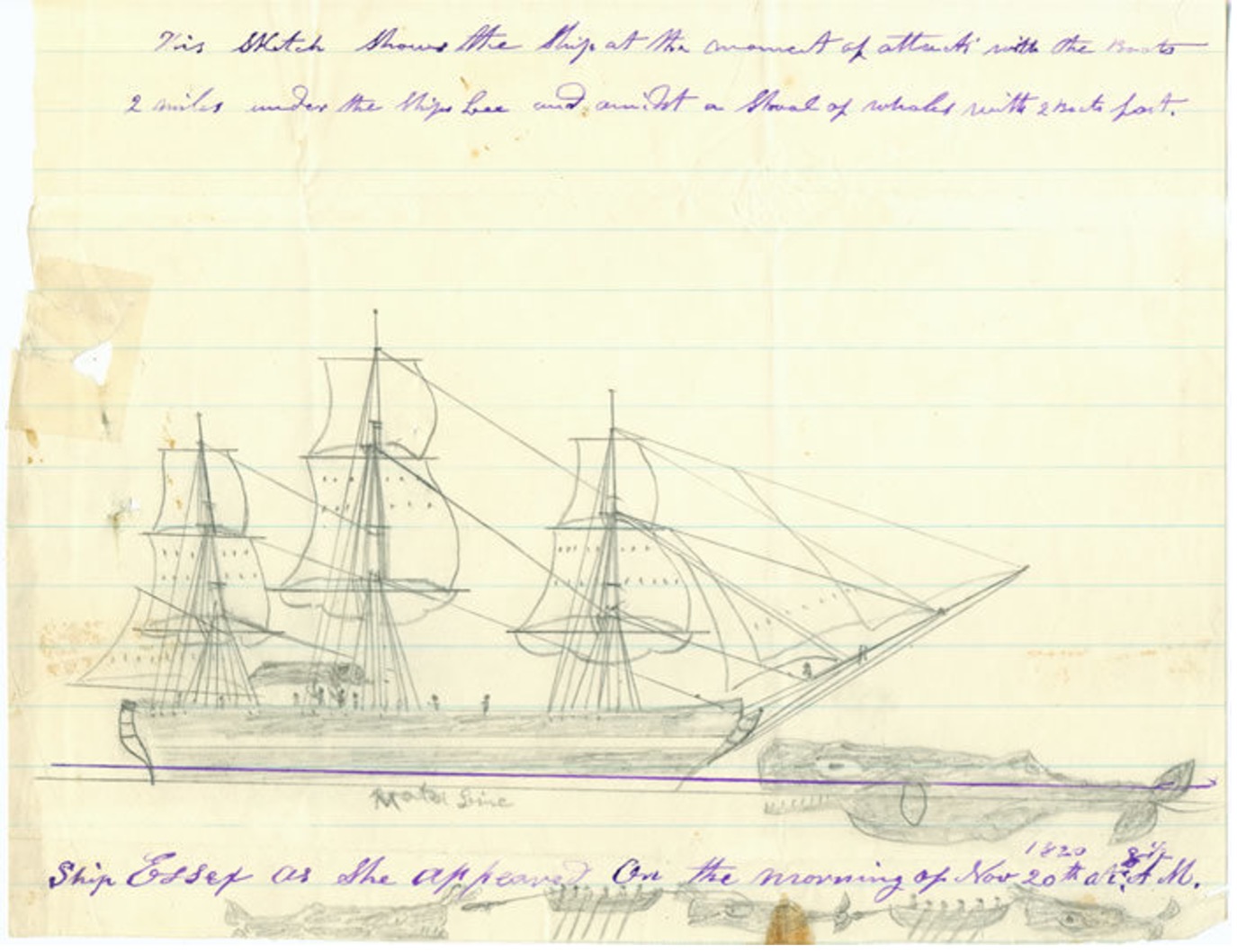

Fast forward to 1820 with the sailing of the whaling ship Essex from Nantucket, Massachusetts, the basis for Herman Melville’s 1851 novel Moby Dick. Our ancestor, a young sailor named Owen Coffin signed on for the two-year voyage, and his name “Coffin” appears in Moby Dick seven times.

In the South Pacific 2,000 miles west of South America, they harpooned a gigantic sperm whale. Enraged, the whale turned around and rammed the ship, sinking it. The men escaped to whaleboats. And here is where they made the fatal navigational errors that are taught in many survival courses today.

Captain Pollard could easily have just ridden the westward currents where they would have ended up in the Marquesas’ Islands in a few weeks. But these islands were known to be inhabited by cannibals, which the crew greatly feared. They also might have landed in the Pitcairn islands, where the mutineers from Captain Bligh’s HMS Bounty still lived. So the boats rowed east, exhausting the men.

At day 88, the men were starving and on the edge of death, so they drew lots to see who should live. Owen Coffin drew the black lot and was immediately shot and devoured. The next day, the men were rescued by the HMS Indian within sight of the coast of Chile, and returned to Nantucket by the USS Constellation.

Another Thomas ancestor, Lawson Thomas, was on the second whaleboat that was never seen again and presumed lost at sea. For more details about this incredible story, please click here.

When Captain Pollard died in 1870, the neighbors discovered a vast cache of stockpiled food in the attic. He had never recovered from his extended starvation.

Mom eventually traced the family to a French weaver 1,000 years ago. Our name is mentioned in England’s Domesday Book, a listing of all the land ownership in the country published in 1086 (click here). Mom died in 2018 at the age of 88, a very well-educated person.

There are many more stories to tell about my family’s storied past, and I will in future chapters. This week, being Thanksgiving, I thought it appropriate to mention our Pilgrim connection.

I have learned over the years that most Americans have history-making swashbuckling ancestors, but few bother to look.

I did.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Happy Thanksgiving from the Thomas Family

USS Essex

Global Market Comments

June 19, 2020

Fiat Lux

Featured Trade:

(JUNE 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (AAPL), (FXE), (FXA), (BA), (UAL), (AAPL), (MSFT), (BIIB), (PFE), (OXY), (SPCE), (WMT), (CSCO), (TGT)

Below please find subscribers’ Q&A for the June 17 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What is the best way to buy long term LEAPS for unlimited profits?

A: There is no such thing as unlimited profits on LEAPS; they are specifically limited to about 500% or 1,000%. Most people will take that. The answer is to wait for crash day. That’s when you dive into LEAPS, or during very prolonged sell-offs like we had in February or March. That’s where you get the bang per buck. On a capitulation day, you can pick up these things for pennies.

Q: How do you explain that all the cities and states that had major COVID-19 outbreaks and deaths are controlled by Democrats?

A: That’s like asking why you don’t get foot and mouth disease in New York City. The majority of US cities are Democratic, while the rural areas tend towards Republicans and the suburbs that flip back and forth. So, you will always get these big hotspots in cities where the population density is highest and there is a lot of crowding because that’s where the people are. Covid-19 is a disease that relies on within six-foot transmission. You are not going to get these big outbreaks in rural places because there are few people. Horse, cow, and pig diseases are another story. That is one reason the disease has become so politicized by the president.

Q: What is the time horizon for your picks?

A: It’s really a price function rather than a time horizon. Sometimes, a trade works in a day, other times it’s a month. I try to send out a large number of trade alerts because we have new subscribers coming in every day and the first thing they want is a trade alert. Occasionally, I’ll make 10% in a day and I take that immediately.

Q: I’m a new investor; trading in a pandemic is one thing, but what about other risks like volcanic eruptions, major solar flares, or global war? How do I prepare for one of three of these things in the next 25 years?

A: I’m actually worried about all three of those happening this year. If you lived through 1968, everything bad tends to happen in one year, and bad things tend to happen in threes. This is a year where we’re kind of making it up as we go along because there is no precedent. The playbook has been thrown out. Those who always relied on trading stocks and securities predictable ranges got wiped out.

Q: Beijing has quarantined its population again and canceled flights; is this going to cause the Chinese government to ramp up the blame game with the US?

A: Absolutely, the US is the number one Corona incubator in the world by far. We have 120,000 deaths—China had 4,000 deaths with four times the population. Many countries are blaming us for keeping this pandemic alive and spreading it further. But I don’t think foreign relations are a high priority right now with our current government. That said, it is easier for a dictatorship to control an epidemic than a democracy. In China, they were welding people’s doors shut who had the disease.

Q: Do you think taking away the $600 or $1200 stipend for the unemployed is going to crush the chances for many trying to get back to work?

A: It will. A lot of the stimulus measures only delay collapse by a couple of months. The PPP money was only for 2 months; I know a lot of companies are counting on that to stay in business. Some state unemployment benefits run out soon. Either you’re going to have to start forking up $3 trillion every other month, or you’re going to get another sharp downturn in the economy. Cities are bracing themselves for the worst eviction onslaught ever. Mass starvation among the poor is a possibility.

Q: Where do you place stops on vertical spreads?

A: Since vertical spreads don’t lend themselves to technical analysis, you have to draw a line in the sand—for me, it’s 2%. If I lose 2% of my total capital, or 20% on the total position, then I get the heck out of there and go look for another trade. That’s easy for me to do because I know that 90% of the time my next trade is a winner.

Q: Why did you sell your S&P 500 (SPY) July $330/$320 put spread at absolutely the worst moment?

A: The market broke my lower strike price, which is always a benchmark for getting out of a losing trade. When you go out-of-the-money on these spreads, the leverage works against you dramatically. This market isn’t lending itself to any kind of conventional historic analysis. The market went higher than it ever should have based on any kind of indicator you’re using. When the market delivers once in 100 year moves like we had off the March 23 bottom, you are going to be wrong. However, we immediately made the money back by putting on a (SPY) July $335/$340 put spread with a shorter maturity, and a (SPY) July $260-$$270 call spread. If you’re in this business, you’re going to take losses and be made to look like a perfect idiot, like I did twice last week.

Q: Who is getting involved down 10%?

A: I would say you’re getting both institutions and individuals involved down 10%. You keep hearing about $5 trillion in cash on the sidelines, and that’s how it’s coming to work. Plus, we have 13 million new day traders gambling away their stimulus checks.

Q: Why have you not put on a currency trade this year?

A: With the incredible volatility of the stock market, there were always better fish to fry. Currencies haven’t moved that much, and you want stocks that are dropping by 80% in two months and gapping up 200% the next two months. So, in terms of trading opportunities, currencies are number three on that list. Would you rather buy Apple (AAPL) for a 75% move, or the Euro (FXE) for a 6% move? My favorite has been the Aussie (FXA) and it has only gone up 20%.

Q: Do you issue trade alerts on LEAPS?

A: I don’t; most trade alerts are short term trades in the next month or two because we have to generate a large number of them. However, in February, March, and April, we started sending out lists of LEAPS. We sent out about 25 LEAPS recommendations. We did ten for Global Trading Dispatch (BA), (UAL), (DAL), ten for the Mad Hedge Technology Letter (AAPL), (MSFT), and five for the Mad Hedge Biotech & Health Care Letter (BIIB), (PFE). Even if you got just one or two of these, you got a massive impact on your performance because they did go up 500% to 1,000% in 2 months, which is normally the kind of return you see in two years. So, getting people to buy all those LEAPS was probably the greatest call in the 13-year history of this letter. I know subscribers who made many millions of dollars.

Q: I am new to trading; other than placing a trade, what do you recommend I get a handle on in the learning process?

A: We do have two services for sale. We have “Options for the Beginner,” and that I would highly recommend, and I’ll make sure that’s posted in the store. You can’t read or study enough. If you really want to go back to basics, read the 1948 edition of Graham and Dodd, where Warren Buffet got his education actually working for Benjamin Graham in the ’40s.

Q: Will Occidental Petroleum (OXY) go bankrupt?

A: No, they have the strongest balance sheet of any of the oil majors, so I would bet they would hang around for some time. They also have no offshore oil, which is the highest cost source of oil. But it’s going to be a volatile time for a while.

Q: Usually the selling is telling me to go away. With this market, the amount of money on the sidelines, is it going to be a stock picker’s market?

A: Yes, like I said the playbook is out the window. Normally, you get a month’s worth of trading in a month, now you get a month's worth in a day or two. So, we’re on fast forward, Corona is the principal driver of the market and no one knows what it’s going to do. The teens were a great index play. The coming Roaring Twenties will be a stock picker’s market because half of the companies will go out of business, while many will rise tenfold. You want to be in the latter, not the former. And index gets you the wheat AND the chaff.

Q: Will there be another opportunity to buy LEAPS?

A: Yes, especially if we get a second corona wave and it slaps the market down to new lows again. There’s a 50/50 chance of that happening. The rate of Corona cases is now increasing exponentially. We had 4,000 new cases in California yesterday.

Q: How do you see Main Street two years from now? Will the battered middle class ever recover?

They will if they move online. I think main street will be empty in two years. Only the largest companies are surviving because they have the cash reserve to do so. And they seem to be able to get government bailout money far better than the local nail salon or dry cleaner. Again, this was a trend that had been in place for decades but was greatly accelerated by the pandemic. I was in Napa, CA yesterday and half of the storefront shops had gone out of business.

Q: What are your thoughts on the spacecraft company Virgin Galactic (SPCE)?

A: Great for day traders, great for newbies, but not real investment material here. I don’t think the company will ever make money. It was just part of the temporary space had. Better to read about it in the papers and have a laugh than risk your own hard-earned money. Elon Musk’s Space X though is a completely different story.

Q: Which is the better buy now: Walmart (WMT), Costco (CSCO), or Target (TGT)?

A: I’d probably go for Target because they have been the fastest to move to the new online order and curb pickup universe. But Costco is also a great play.

Q: When should I buy Tesla?

A: On the next meltdown or down 30% from here, if and whenever we get that. It’s going to $2,500, then $5,000.

Q: With QE infinity, it doesn’t sound like we’ll get to LEAPS country. Do you agree?

A: No, I wouldn’t agree because at some point, the government might run out of money, the bond market won’t let them borrow anymore, and the money that gets approved doesn’t actually get spent because the works are so gummed up. Plus, Corona is in the driver's seat now. What if we’re wrong and we don’t get 250,000 cases by August, but 500,000 cases? 20 million? There are 100 things that could go wrong and get us back down to lows and only one that can go right and that is a Covid-19 vaccine. We’ve essentially been on nonstop QEs for the last 10 years already and the market has managed many 20% selloffs during that time. If we pursue a Japanese monetary policy, we will get a Japanese result, near-zero growth for 30 years.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 29, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR ANOTHER LEG UP FOR THE MARKET),

(SPY), (TLT), (DIS), (INTU), (FCX), (MSFT),

(QQQ), (CVX), (XOM), (OXY), (TSLA)

This is one of those markets where you should have followed your mother’s advice and become a doctor.

I was shocked, amazed, and gobsmacked when the Q1 GDP came in at a red hot 3.2%. The economy had every reason to slow down during the first three months of 2019 with the government shutdown, trade war, and terrible winter. Many estimates were below 1%.

I took solace in the news by doing what I do best: I shot out four Trade Alerts within the hour.

Of course, the stock market knew this already, rising almost every day this year. Both the S&P 500 and the NASDAQ (QQQ) ground up to new all-time highs last week. The Dow Average will be the last to fall.

Did stock really just get another leg up, or this the greatest “Sell the news” of all time. Nevertheless, we have to trade the market we have, not the one we want or expect, so I quickly dove back in with new positions in both my portfolios.

One has to ask the question of how strong the economy really would have been without the above self-induced drags. 4%, 5%, yikes!

However, digging into the numbers, there is far less than meets the eye with the 3.2% figure. Exports accounted for a full 1% of this. That is unlikely to continue with Europe in free fall. A sharp growth in inventories generated another 0.7%, meaning companies making stuff that no one is buying. This is growth that has been pulled forward from future quarters.

Strip out these one-off anomalies and you get a core GDP that is growing at only 1.5%, lower than the previous quarter.

What is driving the recent rally is that corporate earnings are coming in stronger than expected. Back in December, analysts panicked and excessively cut forecasts.

With half of the companies already reporting, it now looks like the quarter will come in a couple of points higher than lower. That may be worth a rally of a few more percentage points higher for a few more weeks, but not much more than that.

So will the Fed raise rates now? A normal Fed certainly would in the face of such a hot GDP number. But nothing is normal anymore. The Fed canceled all four rate hikes for 2019 because the stock market was crashing. Now it’s booming. Does that put autumn rate hikes back on the table, or sooner?

Microsoft (MSFT) knocked it out of the park with great earnings and a massive 47% increase in cloud growth. The stock looks hell-bent to hit $140, and Mad Hedge followers who bought the stock close to $100 are making a killing. (MSFT) is now the third company to join the $1 trillion club.

And it’s not that the economy is without major weak spots. US Existing Home Sales dove in March by 5.9%, to an annualized 5.41 million units. Where is the falling mortgage rate boost here? Keep avoiding the sick man of the US economy. Car sales are also rolling over like the Bismarck, unless they’re electric.

Trump ended all Iran oil export waivers and the oil industry absolutely loved it with Texas tea soaring to new 2019 highs at $67 a barrel. Previously, the administration had been exempting eight major countries from the Iran sanctions. More disruption all the time. The US absolutely DOES NOT need an oil shock right now, unless you’re Exxon (XOM), Chevron (CVX), or Occidental Petroleum (OXY).

NASDAQ hit a new all-time high. Unfortunately, it’s all short covering and company share buybacks with no new money actually entering the market. How high is high? Tech would have to quadruple from here to hit the 2000 Dotcom Bubble top in valuation terms.

Tesla lost $700 million in Q1, and the stock collapsed to a new two-year low. It’s all because the EV subsidy dropped by half since January. Look for a profit rebound in quarters two and three. Capital raise anyone? Tesla junk bonds now yielding 8.51% if you’re looking for an income play. After a very long wait, a decent entry point is finally opening up on the long side.

The Mad Hedge Fund Trader blasted through to a new all-time high, up 16.02% year to date, as we took profits on the last of our technology long positions. I then added new long positions in (DIS), (FCX), and (INTU) on the hot GDP print, but only on a three-week view.

I had cut both Global Trading Dispatch and the Mad Hedge Technology Letter services down to 100% cash positions and waited for markets to tell us what to do next. And so they did.

I dove in with an extremely rare and opportunistic long in the bond market (TLT) and grabbed a quickie 14.61% profit on only three days.

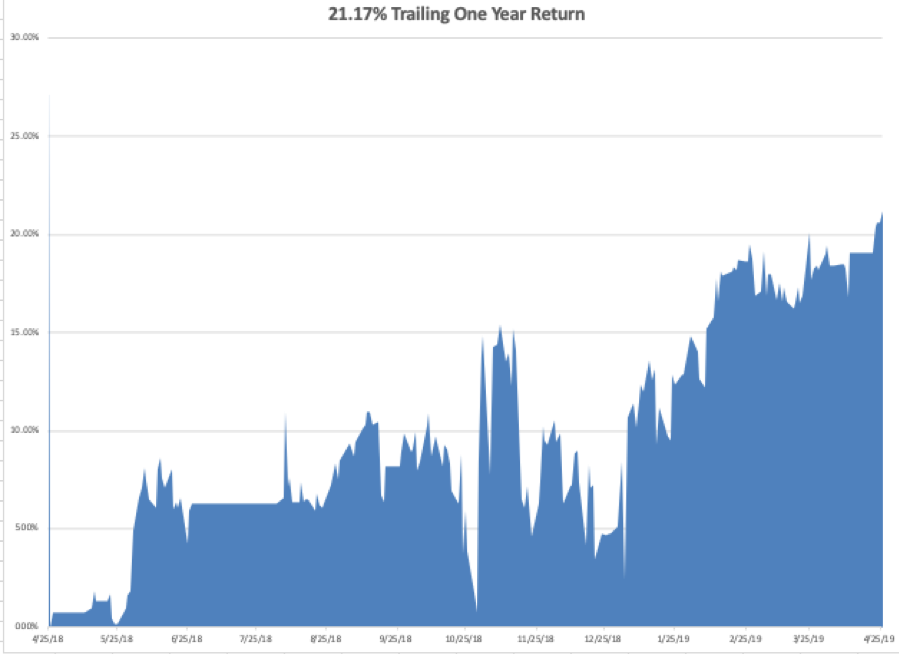

April is now positive +0.60%. My 2019 year to date return gained to +16.02%, boosting my trailing one-year to +21.17%.

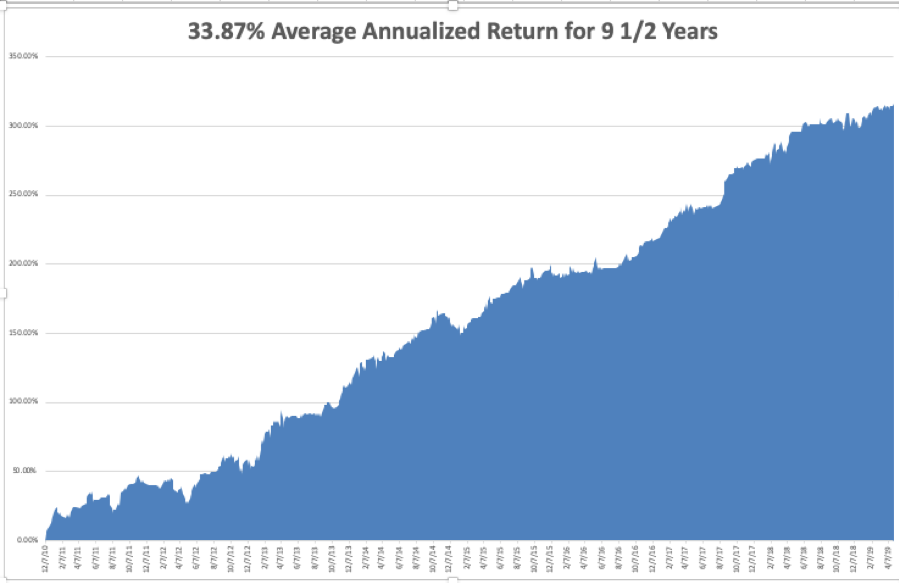

My nine and a half year shot up to +316.16%. The average annualized return appreciated to +33.87%. I am now 80% in cash with Global Trading Dispatch and 90% cash in the Mad Hedge Tech Letter.

The coming week will see another jobs trifecta.

On Monday, April 29 at 10:00 AM, we get March Consumer Spending. Alphabet (GOOGL) and Western Digital (WDC) report.

On Tuesday, April 30, 10:00 AM EST, we obtain a new Case Shiller CoreLogic National Home Price Index. Apple (AAPL), MacDonald’s (MCD), and General Electric (GE) report.

On Wednesday, May 1 at 2:00 PM, we get an FOMC statement.

QUALCOMM (QCOM) and Square (SQ) report. The ADP Private Employment Report is released at 8:15 AM.

On Thursday, May 2 at 8:30 AM, the Weekly Jobless Claims are produced. Gilead Sciences (GILD) and Dow Chemical (DOW) report.

On Friday, May 3 at 8:30 AM, we get the April Nonfarm Payroll Report. Adidas reports, and Berkshire Hathaway (BRK/A) reports on Saturday.

As for me, to show you how low my life has sunk, I spent my only free time this weekend watching Avengers: Endgame. It has already become the top movie opening in history which is why I sent out another Trade Alert last week to buy Walt Disney (DIS).

I supposed that now we have all become the dumb extension to our computers, the only entertainment we should expect is computer-generated graphics with only human voice-overs.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

February 27, 2019

Fiat Lux

Featured Trade:

(WHY CHINA’S US TREASURY DUMP WILL CRUSH THE BOND MARKET),

(TLT), (TBT), ($TNX), (FCX), (FXE), (FXY), (FXA),

(USO), (OXY), (ITB), (LEN), (HD), (GLD), (SLV), (CU),

(THE 13 NEW TRADING RULES FOR 2019)

Years ago, if you asked traders what one event would destroy financial markets, the answer was always the same: China dumping its $1 trillion US treasury bond hoard.

It looks like Armageddon is finally here.

Once again, the Chinese boycotted this week’s US Treasury bond auction.

With a no-show like this, you could be printing a 2.90% yield in a couple of weeks. It also helps a lot that the charts are outing in a major long term double top.

You may read the president’s punitive duties on Chinese solar panels as yet another attempt to crush California’s burgeoning solar installation industry. I took it for what it really was: a signal to double up my short in the US Treasury bond market.

For it looks like the Chinese finally got the memo. Exploding American deficits have become the number one driver of all asset classes, perhaps for the next decade.

Not only are American bonds about to fall dramatically in value, so is the US dollar (UUP) in which they are denominated. This creates a double negative hockey stick effect on their value for any foreign investor.

In fact, you can draw up an all assets class portfolio based on the assumption that the US government is now the new debt hog:

Stocks – buy inflation plays like Freeport McMoRan (FCX) and US Steel (X)

Emerging Markets – Buy asset producers like Chile (ECH)

Bonds – run a double short position in the (TLT)

Foreign Exchange – buy the Euro (FXE), Yen (FXY), and Aussie (FXA)

Commodities – Buy copper (CU) as an inflation hedge

Energy – another inflation beneficiary (USO), (OXY)

Precious Metals – entering a new bull market for gold (GLD) and silver (SLV)

Yes, all of sudden everything has become so simple, as if the fog has suddenly been lifted.

Focus on the US budget deficit which has soared from $450 billion a year ago to over $1 trillion today on its way to $2 trillion later this year, and every investment decision becomes a piece of cake.

This exponential growth of US government borrowing should take the US National Debt from $22 to $30 trillion over the next decade.

I have been dealing with the Chinese government for 45 years and have come to know them well. They never forget anything. They are still trying to get the West to atone for three Opium Wars that started 180 years ago.

Imagine how long it will take them to forget about washing machine duties?

By the way, if I look uncommonly thin in the photo below it’s because there was a famine raging in China during the Cultural Revolution in which 50 million died. You couldn’t find food to buy in the countryside for all the money in the world. This is when you find out that food has no substitutes. The Chinese government never owned up to it.