Mad Hedge Technology Letter

March 31, 2025

Fiat Lux

Featured Trade:

(THE TRUTH ABOUT AUTOMATION AND BANKING)

(SQ), (PYPL), (APPL), (AMZN)

Mad Hedge Technology Letter

March 31, 2025

Fiat Lux

Featured Trade:

(THE TRUTH ABOUT AUTOMATION AND BANKING)

(SQ), (PYPL), (APPL), (AMZN)

Automation is taking place at warp speed displacing employees from all walks of life.

According to a recent report, the U.S. financial industry will depose of 400,000 workers in the next decade because of automating efficiencies.

Yes, humans are going the way of the dodo bird and banking will effectively become algorithms working for a handful of executives and engineers.

The x-factor in this equation is the $150 billion annually that banks spend on technological development in-house which is higher than any other industry.

Welcome to the world of lower costs, shedding wage bills, and boosting performance rates.

We forget to realize that employee compensation eats up 50% of bank expenses.

The 400,000 job trimmings would result in 20% of the U.S. banking sector getting axed.

The hyped-up “golden age of banking” should deliver extraordinary savings and premium services to customers at no extra cost.

This iteration of mobile and online banking has delivered functionality that no generation of customers has ever seen.

The most gutted part of banking jobs will naturally occur in the call centers because they are the low-hanging fruit for the automated chatbots.

A few years ago, chatbots were suboptimal, even spewing out arbitrary profanity, but they have slowly crawled up in performance metrics to the point where some customers are unaware that they are communicating with an artificially engineered algorithm.

The wholesale integration of automating the back-office staff isn’t the end of it, the front office will experience a 30% drop in numbers sullying the predated ideology that front-office staff are irreplaceable heavy hitters.

Front-office staff has already felt the brunt of downsizing with purges carried out in 2022 representing a twelfth year of continuous decline.

Front-office traders and brokers are being replaced by software engineers as banks follow the wider trend of every company transitioning into a tech company.

The infusion of artificial intelligence will lower mortgage processing costs by 30% and the accumulation of hordes of data will advance the marketing effort into a smart, multi-pronged, hybrid cloud-based, and hyper-targeted strategy.

The last two human bank hiring waves are a distant memory.

The most recent spike came in the 7 years after the dot com crash of 2001 until the sub-prime crisis of 2008 adding around half a million jobs on top of the 1.5 million that existed then.

After the subsidies wear off from the pandemic, I do believe that the banking sector will quietly put in the call to trim even more.

The longest and most dramatic rise in human bankers was from 1935 to 1985, a 50-year boom that delivered over 1.2 million bankers to the U.S. workforce.

This type of human hiring will likely never be seen again in the U.S. financial industry.

Recomposing banks through automation is crucial to surviving as fintech companies like PayPal (PYPL) and Square (SQ) are chomping at the bit and even tech companies like Amazon (AMZN) and Apple (AAPL) have started tinkering with new financial products.

And if you thought that this phenomenon was limited to the U.S., think again, Europe is by far the biggest culprit by already laying off 102,000 employees in 2021, more than 10x higher than the number of U.S. financial job losses and that has continued in 2022, 2023 and 2024.

In a sign of the times, the European outlook has turned demonstrably negative with Deutsche Bank announcing layoffs of 40,000 employees as it scales down its investment banking business.

Don’t tell your kid to get into banking, because they will most likely be feeding on scraps at that point.

THE LAST STAGE OF HUMAN-FACING BANK SERVICES IS NOW!

Mad Hedge Technology Letter

December 27, 2024

Fiat Lux

Featured Trade:

(THE TRUTH ABOUT AUTOMATION AND BANKING)

(SQ), (PYPL), (APPL), (AMZN)

Automation is taking place at warp speed, displacing employees from all walks of life.

According to a recent report, the U.S. financial industry will depose of 400,000 workers in the next decade because of automating efficiencies.

Yes, humans are going the way of the dodo bird, and banking will effectively become algorithms working for a handful of executives and engineers.

The x-factor in this equation is the $150 billion annually that banks spend on technological development in-house, which is higher than any other industry.

Welcome to the world of lower costs, shedding wage bills, and boosting performance rates.

We forget to realize that employee compensation eats up 50% of bank expenses.

The 400,000 job trimmings would result in 20% of the U.S. banking sector getting axed.

The hyped-up “golden age of banking” should deliver extraordinary savings and premium services to the customer at no extra cost.

This iteration of mobile and online banking has delivered functionality that no generation of customers has ever seen.

The most gutted part of banking jobs will naturally occur in the call centers because they are the low-hanging fruit for automated chatbots.

A few years ago, chatbots were suboptimal, even spewing out arbitrary profanity, but they have slowly crawled up in performance metrics to the point where some customers are unaware that they are communicating with an artificial engineered algorithm.

The wholesale integration of automating the back-office staff isn’t the end of it, the front office will experience a 30% drop in numbers, sullying the predated ideology that front-office staff are irreplaceable heavy hitters.

Front-office staff has already felt the brunt of downsizing, with purges carried out from 2022 representing a twelfth year of continuous decline.

Front-office traders and brokers are being replaced by software engineers as banks follow the wider trend of every company transitioning into a tech company.

The infusion of artificial intelligence will lower mortgage processing costs by 30%, and the accumulation of hordes of data will advance the marketing effort into a smart, multi-pronged, hybrid cloud-based, and hyper-targeted strategy.

The last two human bank hiring waves are a distant memory.

The most recent spike came in the 7 years after the dot com crash of 2001 until the sub-prime crisis of 2008, adding around half a million jobs on top of the 1.5 million that existed then.

After the subsidies wear off from the pandemic, I do believe that the banking sector will quietly put in the call to trim even more.

The longest and most dramatic rise in human bankers was from 1935 to 1985, a 50-year boom that delivered over 1.2 million bankers to the U.S. workforce.

This type of human hiring will likely never be seen again in the U.S. financial industry.

Recomposing banks through automation is crucial to surviving as fintech companies like PayPal (PYPL) and Square (SQ) are chomping at the bit, and even tech companies like Amazon (AMZN) and Apple (AAPL) have started tinkering with new financial products.

And if you thought that this phenomenon was limited to the U.S., think again, Europe is by far the biggest culprit by already laying off 102,000 employees in 2021, more than 10x higher the number of U.S. financial job losses, and that has continued in 2022, 2023 and 2024.

In a sign of the times, the European outlook has turned demonstrably negative, with Deutsche Bank announcing layoffs of 40,000 employees as it scales down its investment banking business.

Don’t tell your kid to get into banking because they will most likely be feeding on scraps at that point.

THE LAST STAGE OF HUMAN-FACING BANK SERVICES IS NOW!

Mad Hedge Technology Letter

June 21, 2024

Fiat Lux

Featured Trade:

(CUPERTINO NEEDS A REBOOT)

(AAPL), (PYPL), (SQ)

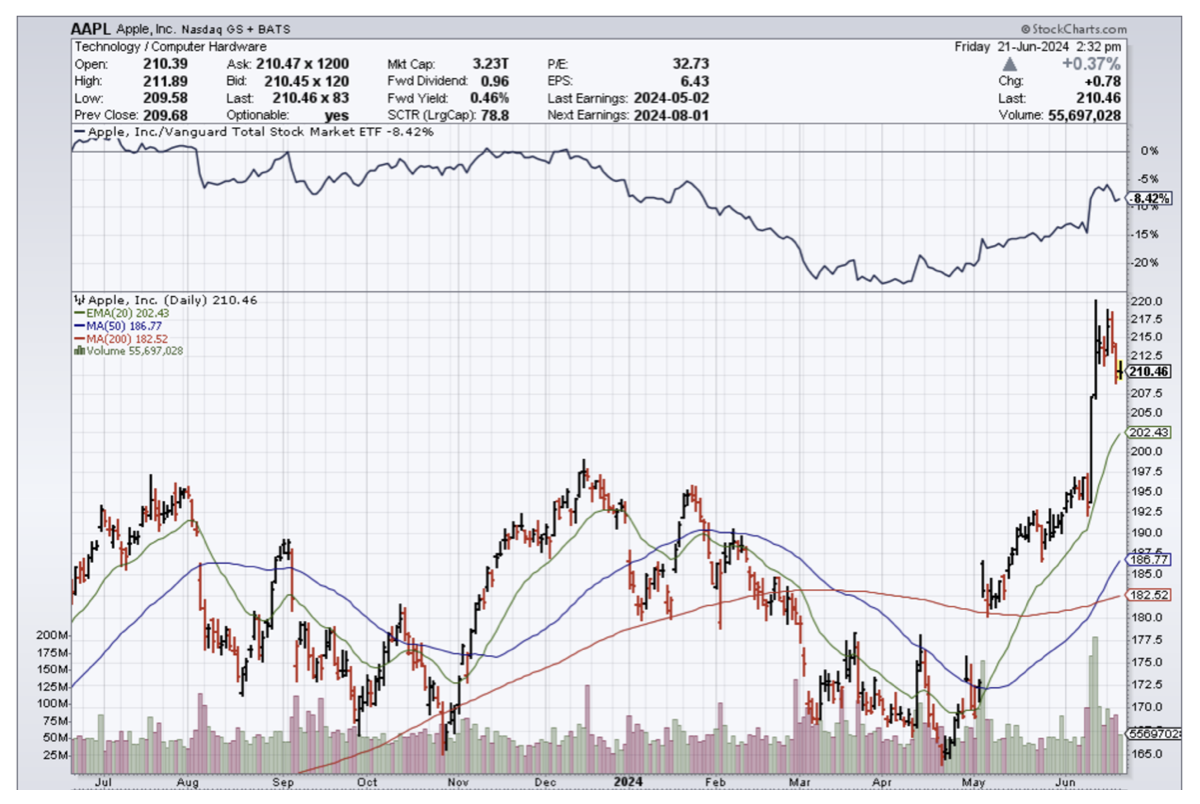

Fintech used to be the shiny new car and in the last year or two, the sub-sector has entirely reversed.

Look at stock like PayPal (PYPL) or Square (SQ), their market cap is only 20% of what it was in 2021.

The fintech hype didn’t match the results and it definitely wouldn’t be something that Steve Jobs would be interested in getting into.

Getting into the weeds a little, the fintech industry has been saturated.

Too many vendors chasing after the same customers with the same homogenous products doesn’t seem like something Apple is usually associated with.

Almost as if the behavior suggests a mea culpa, Apple officially stopped issuing loans through Apple Pay Later, its buy-now-pay-later program that launched last year.

The move comes after Apple said it would start allowing installment loans later this year in its Apple Pay checkout process through third-party companies, such as Affirm, and credit and debit cards from issuers, such as Citigroup.

This Apple product certainly would have turned into a buy now – pay never platform.

I won’t say that Apple should stay in their lane – they certainly shouldn’t.

The reason is that they are a one-trick pony hoping to pivot into another lucrative cash cow business like the iPhone business. They desperately need to become a two-trick pony but they can’t find that special sauce yet.

Apple also recently announced they are putting their Apple Vision VR goggles on the backburner.

It is sad to see Apple go from project to project with such little follow-through.

They are Apple and many still think that brand still carries a lot of weight.

In the short term, they will get a pass for contracting some terrible projects, but only for so long.

One could argue that wearables like the Apple Watch and the iPad have been somewhat successful and I do acknowledge they have had some stickiness in terms of revenue.

However, the already saturated fintech payments business is a head-scratcher.

Sometimes it’s best to let fintech be fintech and allow them to experience the race to zero.

Apple is bigger and better – their customers deserve something that delivers higher value.

Clearly, the management at Apple at the highest levels is lacking the creative juices to push through something trendsetting or cutting edge and now that is starting to become a serious threat to future cash flows.

The OpenAI partnership was a copycat move and I am not sure if they have really planned how they will seemingly integrate this new tool into their products.

Remember, OpenAI could destroy some of Apple’s products because AI is still rife with errors and can even cause major losses to the share price.

What if the CEO of Apple Tim Cook wakes up one day and AI has deleted half of Apple’s internal software or emailed all of Apple’s intellectual property to a fierce rival?

What if AI magically wires $100 billion of Apple’s war chest to a 3rd world bank under the banner of improving world hunger or balancing income inequality?

Remember that AI has no common sense and that could be very dangerous.

Kids who grew up in front of computers all day are also notorious for having little common sense and the end of the day results show.

Nobody knows what will happen, but Apple sure appears defensive and that is always big trouble in Silicon Valley in an industry where you need to know what will happen in the future.

Global Market Comments

May 31, 2024

Fiat Lux

Featured Trade:

(The Mad June traders & Investors Summit is ON!)

(MAY 29 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (AMZN), (META), (NFLX), (GLD), (SLV), (NVDA), (MSFT), (GOOG), (DELL), (MSFT), (TLT), (BRK/B), (PYPL), (BABA), (DD), (XOM), (OXY)

Below please find subscribers’ Q&A for the May 29 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

Q: Since Elon Musk is raising tons of money for his AI startup called xAI, will this impact Tesla’s (TSLA) stock price?

A: Yes, it's a very positive move for Tesla because anytime Elon Musk raises money anywhere in his network, it takes the need off of him to sell Tesla shares for cash. And I think his xAI will be the next trillion-dollar company, and SpaceX is in front of it as another trillion-dollar company. Those stocks, he can sell any time and raise a lot of money, but the other two are still private companies. We can't buy them yet unless we buy some of the public vehicles offered by venture capitalists like Ron Baron who has heavy positions in both Tesla and SpaceX. So, no direct plays yet on these companies, but no doubt when they become incredibly valuable, he'll take them all public and become the richest man in the world two or three times over. So yes, that is a positive.

Q: Where do you think (TLT) will be in the next few months?

A: In a narrow trading range. I think we're basically in a $86 to $91 trading range, and we'll go nowhere until we get clarification on Fed interest rate cuts. At the rate the economy is slowing, we may get one in September, and even if the Fed doesn't cut, the rest of the world will, including Japan, Europe, Great Britain, and so on. So we may get our interest rates dragged down here by foreign countries that all have much weaker economies than the US.

Q: Should I keep buying big tech stocks after Nvidia's (NVDA) blowout earnings?

A: Well, if you recall back in the ancient times of April, Nvidia had a 20% sell-off, and most of the tech stocks were down at least 10%. So, I would wait for the next 20% sell-off of Nvidia not only to buy Nvidia but all other big tech stocks as well, because it basically is a big tech story and will continue for the rest of the year like that. So we're really looking to buy dips among the big tech winners, and those would include Amazon (AMZN), Meta (META), Microsoft (MSFT), and so on.

Q: How long can the US economy go without a recession?

A: Five years. The way our economic cycle works is after a long period of growth, companies get overconfident, over-invest, create excessive capacity in the markets for everything, and that leads to a crash and a recession, deflation, and lower interest rates. So even if we don't get major moves in the (TLT) upside now, you always will over the long term get interest rates going back to 2 or 3% for the 10-year so it’s a great long-term hold. That is the economic cycle—that's what creates bear markets and it’s known as “Boom and Bust”. Long may it live because that’s where we traders earn our crust of bread. But this time may be different. We may go longer than 5 years because AI is still in its infancy, still rolling out, and the number of companies making actual profits in AI will go from 3 to 300 over the next five years.

Q: I'm looking to buy gold in an investment account (GLD). Would you do that now, if so, what would you recommend?

A: I would recommend GLD (SPDR Gold Trust) because the metals are still outperforming the miners, miners being held back by the inflation rates unique to the mining industry, which are much higher than the 3.3% for the general economy. And if you want to add a little more spice to your portfolio, buy some silver (SLV) because it is rising at three times the rate of gold thanks to Chinese speculation. You might buy some copper while you're at it too—it's moving almost as fast as gold is.

Q: Which big tech firm is next to issue a dividend?

A: That's an easy answer, it's Netflix (NFLX). But there's a more important question out here— Which is the next tech stock to issue a stock split? And guess what the answer is? Netflix again, which needs to declare both a dividend and a stock split. It's at an all-time high, has a very high share price, and over time, stocks that split deliver double the performance of the S&P 500. So, the mere announcement will suck in a lot of new retail investors as we just saw with Nvidia (NVDA), where we got a $250 move on the split announcement. So, watch your splits, and in fact, I'm going to be devoting a major piece of next Monday's newsletter to splits and how to play them.

Q: Why has the stock market been so strong this year when interest rates are high?

A: The answer to that is AI. We are still in the very early days of AI, and as I mentioned earlier, only three companies are making money from AI right now. That's Nvidia (NVDA), Microsoft (MSFT), and Google (GOOG). That number will increase as AI moves down the food chain and everybody starts using it, including you and me. I view the AI development as similar to 1995 when all of a sudden we got Netscape, a navigator that made the Internet available to the public, Dell Computers (DELL), and Microsoft (MSFT) software all at once hitting the market and creating the online economy essentially from scratch. Something of that magnitude is what the stock market is discounting now. Think of it in terms of the revolutionary new technologies of 1995, which means we have another 5 or 6 years to go, and that's why the stock market is so strong.

Q: Should I invest in Berkshire Hathaway (BRK/B), or do you think their magic will run out soon?

A: I don't think their magic will ever run out. Of course, the day that Warren Buffett dies it'll be down 10%, but then you'll want to buy it with both hands because Warren has already replaced himself with a first-class management team who is carrying on his strategy. Any selloffs in Berkshire you get this summer, go in there and buy the calls, the call spreads, the stock, the LEAPS, and the kitchen sink. Still a great long-term BUY, and I see $500 either late this year or next year in (BRK/B).

Q: I'm a member of IM Academy.

A: Oh my gosh. I would let your membership expire, except you're probably on auto-renewal, and the only way to stop your subscription is to call your credit card company and ask them to block the billings. That is the problem with these predatory financial newsletters, they're impossible to get out of, even when they promise refunds anytime.

Q: Are there any Chinese stocks you like now?

A: No, but the highest quality stock in China is Alibaba (BABA). It's basically a combination of Amazon and PayPal in China, but you still have a very high political risk investing in anything in China. The currency is very weak, so better fish to fry is my opinion. And I tend to avoid countries suffering from demographic implosions.

Q: Should we buy (TLT) now or wait?

A: I would wait until we get some upside momentum going and we complete a few more downside tests.

Q: What's the best place to put cash in the summer?

A: The answer is always good old 90-day US Treasury bills. They are still paying 5.25%.

Q: What are your thoughts on PayPal (PYPL)?

A: I'm avoiding that sector because of over-competition crushing profit margins; that has been a problem for a couple of years now. Don't confuse “gone down a lot” with cheap.

Q: Which oil companies are the best to invest in right now?

A: You can buy Exxon Mobil (XOM) for the high dividend and the sheer size of the company. My second is Occidental Petroleum (OXY), because Warren Buffett owns 25% of the company, has shrunk the float, and that has a result in magnifying any moves up in the stock. Also, I somewhat admire Warren Buffett's stock-picking ability. And of course, I’ve been following the California company OXY since 1970, back when it was run by Armand Hammer, a friend of Vladimir Lenin, so my connections with the company go back a very long time.

Q: Do you like DuPont (DD) for the three-way split?

A: I do, but DuPont has a major problem looming with lawsuits over the PFAS chemicals—those are the forever chemicals which are all over the country, all over the food supply, and cause cancer. So that could be sort of like a Johnson & Johnson-type liability problem with the talcum powder. So again…why look for trouble? Buying a stock facing that kind of liability could be another tobacco situation.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

June 23, 2023

Fiat Lux

Featured Trades:

(JUNE 21 BIWEEKLY STRATEGY WEBINAR Q&A),

(AAPL), (ABNB), (GLD), (BA), (CAT), (DE), (X), (PYPL), (SQ), (MSFT), (GD), (GE), (INDA), (META) (GOOGL), (CCI), (NVDA), (ABNB), (SNOW), (PLTR), (TSLA)

CLICK HERE to download today's position sheet.

Below please find subscribers’ Q&A for the June 21 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe, NV.

Q: When do we buy Nvidia (NVDA) and Tesla (TSLA)?

A: On at least a 20% dip. We have had ballistic moves—some of the sharpest up moves in the history of the stock market for large stocks—and certainly the greatest creation of market caps since the market was invented under the Buttonwood Tree in 1792 at 68 Wall Street. Tesla’s almost at a triple now. Tripling one of the world's largest companies in 6 months? You have to live as long as me to see that.

Q: Is it a good time to invest in Bitcoin?

A: No, absolutely not. You only want to invest in Bitcoin when we have an excess of cash and a shortage of assets. Right now, we have the opposite, a shortage of cash and an excess of assets, and that will probably continue for several years.

Q: Should I short Apple (APPL)?

A: Only if you’re a day trader. It’s hugely overbought for the short term, but still in a multiyear long-term uptrend. I think we could see Apple at $300 in the next one or two years.

Q: Is it better to focus on single stocks or ETFs?

A: Single stocks always, because a single stock will outperform a basket that's in an ETF by 2 to 1 or even 3 to 1. That's always the case; whenever you add stocks to a basket, it diversifies risk and dilutes the performance. Better to just own Tesla, and if you want to diversify, diversify to Nvidia, but then I live next door to these two companies. That's what I tell my friends. You only diversify if you don’t know what is going to happen, which is most investors and financial advisors.

Q: Is the bottom of the housing market in, and are we due for a spike in home prices when interest rates can only go lower?

A: Yes, absolutely. In fact, we will enter a new 10-year bull leg for housing because we have a structural shortage of 10 million homes and 82 million millennials desperately trying to buy them at any price. I just got a call from my broker and she is panicking because she is running out of inventory. Even the lemons are starting to move.

Q: When do you think energy will rise?

A: Falling interest rates could be a good key because it sets the whole global economy on fire and increases energy demand.

Q: Outlook for the S&P 500 (SPY) second half of the year?

A: We hit 4,800 at least, maybe even higher. That's about a little more than 10% from here, so it’s not that much of a stretch, not like it was at the beginning of the year when it needed to rise 25% to reach my yearend target.

Q: Best time to invest from here on?

A: Either a 10% pullback in the market, or a sideways move of 3 months—that's called a time correction. It usually counts as a price correction because of course, over 3 months, earnings go up a lot, especially in tech.

Q: I’m seeing grains (WEAT) in rally mode.

A: Yes, that's true. They are commodities, and just like copper’s been rallying, and it’s yet another signal that we may get a much broader global commodity rally in everything: iron ore, coal, energy, gold, silver, you name it.

Q: Will inflation drop to 2%, causing stocks to go on another epic run?

A: The answer is yes, I do see inflation dropping to 2% —maybe not this year, but next year; not because of any action the Fed is doing, but because technology is hyper-accelerating, and technology is highly deflationary. The tech product you bought two years ago is now half the price, and they offer you twice as much functionality with an auto-renew for life. So, that is happening across the entire technology front and feeds into the inflation numbers big time, including labor. There's going to be a lot of labor replacement by machines and AI in the coming years.

Q: Is Airbnb (ABNB) a good stock to buy?

A: Well, if we’re going into the most perfect travel storm of all time, which is this summer, and which is why I’m going to remote places only like Cortina, Italy. Airbnb is the perfect stock to own. It’s a well-run company even in normal times.

Q: Should I buy gold here on the pullback?

A: Yes, you should. Gold is also highly sensitive to any decline in interest rates, and by the way: buy silver, it always moves 2.5x as much as the barbarous relic.

Q: How can inflation not go up if commodities and wage demands are going up due to state and federal unions? What about farm equipment and truck supplies? Costs keep rising, should we buy John Deere (DE)?

A: There are three questions here. Inflation will not go up because, though commodities will rise, they are only 0.6% of the $100 trillion global economy, or $660 billion in 2022. That will be more than offset by technology cutting prices, which is 30% of the stock market. You have to realize how important each individual element is in the global picture. And regarding wage demands going up caused by state and federal unions, less than 11.3% of the workforce is now unionized and that figure has been declining for 40 years. Most growth in the economy has been in non-unionized technology firms which largely depend on temporary workers, by design. What IS unionized is mostly teachers, the lowest paid workers in the economy, so incremental pay rises will be small. Unions were absolutely slaughtered when 25 million jobs were offshored to China during the Bush administration. Buy farm equipment and trucks? Absolutely, buy John Deere (DE) and buy Caterpillar (CAT) on the next dip. I was actually looking at Caterpillar for the next LEAPS the other day, but it’s already had a big run; I'm going to wait for a pullback before I get CAT and John Deere. So, again, people see headlines, see union wage headlines—I say focus on the 89% and not on the 11% if you want to make good decisions.

Q: Is Boeing (BA) a buy on the dip?

A: Yes, they got 1,000 new aircraft orders and the stock hasn't moved. So yes, if you get any kind of selloff down to $200, I'd be hoovering this thing up.

Q: Can you please explain how the profit predictor works?

A: It’s a long story; just go to our website, log in and do a search for “profit predictor,” and you’ll get a full explanation of how it works. It’s actually where Mad Hedge has been using artificial intelligence for 11 years, which is why our performance has doubled. Just for fun, I'll run the piece next week.

Q: Gold (GLD) is having a hard time going up because Russia is being squeezed by other governments. Since they need cash, they may be either selling their gold or stop buying new gold.

A: That is a good point, but at the end of the day, interest rates are the number one driver of all precious metals—period, end of story. We’re long gold too, I’ve got lots of gold coins stashed around the world in various safe deposit boxes, and I'm keeping them. I’ve got even more silver coins, which take up a lot of space.

Q: Do you like India (INDA) long term?

A: Yes, it’s the next China. But as Apple is finding out it is very difficult to get anything done there. A radical reforming Prime Minster Modi may be changing things there with his recent Biden visit and (GE) contract to build jet engines.

Q: What do you think of General Dynamics Corp (GD)?

A: I like General Dynamics because I think defense spending is in a permanent long term upcycle as a result of the Ukraine war. And it won’t end with the Ukraine war—the threat will always be out there, and the buying is done by not only us but all the other countries that think Russia is a threat.

Q: Do you like MP Materials Corp (MP)?

A: Yes, I do. The whole commodities space is ready to take off and go on fire.

Q: What about Square (SQ)?

A: The only reason I’m not recommending Square right now is huge competition in the entire sector, where all the stocks including PayPal (PYPL) are getting crushed. I will pass on Square for now, especially when I can buy US Steel (X) at close to its low for the year.

Q: If you had to pick one: Nvidia (NVDA), Tesla (TSLA), Microsoft (MSFT), Meta (META), and Google (GOOGL), which is the best to buy for next year?

A: All of them. Diversify. If I have to pick the top performer, it’s going to be either Tesla or Nvidia, probably Nvidia. But you need at least a 10% correction before you do anything. Actually, the split-adjusted price for our first (NVDA) recommendation eight years ago was $2 a share.

Q: Do you like Crown Castle International (CCI)?

A: Yes, I like it very much—it has very high dividend yield at 5.5%. The reason it hasn’t moved yet is that as long as interest rates are high, any REIT structure will suffer, and (CCI) has a REIT structure. Sure, it’s in a great sector—5G cell towers—but it is still a REIT nonetheless, and those will start to recover when interest rates go down; that’s why we did a 2.5-year LEAPS on CCI. For sure interest rates are going to go down in the next 2.5 years, and you will double your money on (CCI). That’s why we put it out.

Q: Which mid cap will do best over the long term: Airbnb (ABNB), Snowflake (SNOW), or Palantir (PLTR)?

A: That’s easy: Snowflake. They have such an overwhelming technology on the database and security front; I would be buying Snowflake all day long. Even Warren Buffet owns Snowflake, so that’s good enough for me.

Q: Could you comment on the pace of EV adoption/potential for (TSLA) robot fleet acceleration and implications for oil investments in holding pattern till the eventual collapse to near 0?

A: Yes, oil may collapse to near zero, but it may take twenty years to do it—that’s how long it takes to transition an energy source. That’s how long it took the move from horses and hay to gasoline-powered cars at the beginning of the 20th century. A national robot fleet of taxis with no drivers at all is a couple of years off. There are about 1,000 of them working in San Francisco right now, but they still have more work to do on the software. When it gets foggy, they often congregate at intersections causing traffic jams. Suffice it to say that eventually Tesla shares go to $1,000 and after that, $10,000—that’s my bet. By the way, my Tesla January 2025 $595-$600 LEAPS are starting to look pretty good.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

2018 in Australia