Global Market Comments

October 17, 2019

Fiat Lux

Featured Trade:

(UPDATING THE MAD HEDGE LONG TERM MODEL PORTFOLIO),

(USO), (XLV), (CI), (CELG), (BIIB), (AMGN), (CRSP), (IBM), (PYPL), (SQ), (JPM), (BAC), (EEM), (DXJ), (FCX), (GLD)

Global Market Comments

October 17, 2019

Fiat Lux

Featured Trade:

(UPDATING THE MAD HEDGE LONG TERM MODEL PORTFOLIO),

(USO), (XLV), (CI), (CELG), (BIIB), (AMGN), (CRSP), (IBM), (PYPL), (SQ), (JPM), (BAC), (EEM), (DXJ), (FCX), (GLD)

Global Market Comments

October 9, 2019

Fiat Lux

Featured Trade:

(HOW FINTECH IS EATING THE BANKS’ LUNCH),

(BAC), (C), (WFC), (SQ), (PYPL),

(WCAGY), (FISV), (INTU), (BABA),

It was another dreadful DAY for the banks. All bank shares are now down in 2019 with the sole exception of JP Morgan, which is up a modest 10% since January 1. Although their core business is good, the share price hasn’t even bothered to mail it in.

So, I thought it would be time to take another look at what is disrupting the 200-year-old business model of this sector. And that would be Fintech, shorthand for Financial Technology.

To say that fintech was gobbling up the financial industry’s lunch would be a vast understatement. But here’s the problem. Fintech is taking over the world one transaction at a time in an industry that sees billions of transactions a year. The change is almost invisible. If someone were blowing up bank branches on a large scale this would be a far easier trend to see, but the net effect is the same.

The potential market is enormous. While the world’s physical money totals $5 trillion, actual assets controlled by banks today total a staggering $90 trillion.

Why this is all happening now is due to a confluence of several independent technologies. The number of people on the Internet has soared from 1.8 billion in 2010 to 4 billion today, to 8 billion by 2024.

Smartphone usage is diffusing at a similar rate. The roll out of 5G wireless assures that all communications will occur seamlessly, quickly, including financial transactions. Blockchain is enabling encryption on an industrial scale.

This has enabled the rise of a number of online firms over just the last few years that are rapidly taking over a number of traditional banking functions.

So far, the greatest impact has been overseas. Many countries that lack banking infrastructure are leapfrogging straight to mobile. It makes a ton of sense. Poor countries lack the capital to build expensive branch networks to raise fund, and the expertise on how to invest the deposits once in hand.

Good Money (https://goodmoney.com ) is an example of the new online banks that have burst onto the scene. The company offers depositors a generous 1.8% interest rate on overnight funds. Legacy banks are still paying close to zero, even though the Fed has raised rates seven times in three years.

US banks charge an average of $400 in fees a year for a full-service account. Good Money charges nothing.

You will never know where the money goes when you place it with Citibank (C), Bank of America (BAC) or Wells Fargo (WFC). At Good Money, you can specify that your funds be lent to a certain industry or even a specific company. While this means nothing to you or me, it is important issue to oriented Millennials.

Such efforts are called Crowdlending. It first took off in the US with startups like Prosper and Lending Club in the mid 2000s. We’re not talking small potatoes here, or a market that might develop someday. In 2018, some 22,000 businesses extended $380 billion in such loans.

There are other big markets ripe for disruption. I had to pay a Filipino developer $500 for some work he did on my website. Wells Fargo wanted to charge me $50 and the wire transfer would have taken a week. An outfit called Payoneer, Israel-based, did it for $5 and it took 5 seconds.

Wire transfer fees are in fact a global industry worth billions of dollars a year that is there for the taking. The SWIFT international transfer network alone processes some 24 million transactions per day.

It may not surprise many of you that China already has a huge lead in this area. It’s logical since their established banking system is primitive at best. China has three times more mobile phones than the US, five times more Internet customers, sees 10 times more eat-out orders, and 50 times more mobile transactions. In a future where data is currency, this is huge.

Ant Financial, an affiliate of Alibaba (BABA), is in the forefront, facilitating an eye-popping $8 trillion worth of transactions in 2017. Using artificial intelligence to scour public records for past borrowing, income, education, web surfing preferences, and even political leanings, smart finance can use artificial intelligence to gin up a quickie FICO score and generate a new $200 micro loan in as little as eight seconds.

Bank of America eat your heart out.

What gives the Chinese such an advantage here is their huge market, with some 800 million online participants. The money Ant Financial makes isn’t important now. It’s the digitized data they’re collecting and the way it can be manipulated with artificial intelligence. That gives them immense market power. Remember, in the new world, data is the new currency and the Chinese are creating more than we ever will.

The problem with early, under-the-radar but broad-ranging trends, it can be tough to flesh out pure investment plays. Listed liquid tradable stocks are few and far between. You can simply go out and buy Square (SQ) and PayPal (PYPL) and you’d be half the way there in getting some good exposure.

Here’s the problem with that plan. PayPal has tripled in the last two years, while Square has gone ballistic with a 2,000% gain. I expect further appreciation from here, but those ships have already sailed.

A better way to participate might be the Global X Fintech Thematic ETF (FINX), granted you have all the usual problems with specialized ETFs here such as liquidity, high management fees, and tracking error. But you do get exposure to a number of companies that are either domiciled abroad or are not yet publicly listed.

The five largest holdings of (FINX) include Square (SQ), Wirecard AG (WCAGY), Temenos Group AG, Fiserve Inc (FISV), and Intuit (INTU).

You could also simply buy Alibaba. However, as long as America’s trade war with China continues, all Chinese stocks will perform poorly. Given the stubbornness of both sides, the earliest that can happen is January, 2021.

To learn more about (FINX), please go to the manager’s website by clicking here.

Mad Hedge Technology Letter

September 27, 2019

Fiat Lux

Featured Trade:

(THE REBIRTH OF WESTERN UNION)

(WU), (PYPL), (SQ)

This is not your father’s Western Union (WU).

Western Union (WU), the payment remittance service, is a legacy company that is going to harvest the most from a full migration to digital.

That is exactly what is currently happening.

Part of the 25% gain in the stock this year is a nod of approval in the direction the company is heading to.

At its most recent investors’ day presentation, the firm boosted its positive earnings guidance, which was primarily driven by its growth strategy on different verticals.

Western Union’s revamped growth strategy is buttressed by its ability to meet increasing demand from global consumers and businesses for fast and reliable cross-border money transfer and payment solutions.

The company is shying away from the brick-and-mortar operations of yore and choosing a strategy that leverages Western Union’s continued investment in key capabilities such as digital, real-time account payout, compliance, and artificial intelligence.

These nice additions have positioned the company to show strength in one of the most holistic and versatile payment engines in the world.

Western Union has its eyes set on expanding its core consumer-to-consumer business as well as other payment segments where global organizations can utilize its cross-border solutions to expand into fresh markets or better serve existing customers.

Western Union predicts a 23% operating margin by 2022 and a low-double-digit EPS CAGR through 2022.

The operating margin and EPS targets presume a 2020-2022 revenue CAGR of 2% to 3%, compared with the 2019 revenue base excluding divestitures.

The revenue ramp up signals growth in consumer money transfer, driven by its website westernunion.com and other third-party digital services and mid-single-digit growth from Business Solutions.

Operating profit margin and EPS targets also reflect $150 million in total annual savings expected by 2022.

The company expects to succeed in operating efficiencies from initiatives aimed at optimizing commissions and reducing third-party spending.

These initiatives will boost the bottom line an extra $50 million in annual savings to operating profit by 2022.

From 2020 to 2022, Western Union expects to extract more than $3 billion of operating cash flow and return approximately $2.5 billion to $3 billion to shareholders through dividends and share repurchases.

The company is a cash cow and attractive for many traditional investors who value this type of cash flow.

Other pathways to higher revenue include partnerships that provide customized payments solutions to organizations such as e-Commerce businesses expanding into emerging markets, end-to-end cross-border solutions to third-party organizations to solve consumer money transfer needs, and cross-border services, such as foreign exchange and cash management.

Slagging off the brick-and-mortar payments model for the digital platform is the low-lying fruit here and Western Union has a phase of overperformance in them before they will be thwarted with substantial revenue resistance.

Could this one day turn into a legitimate and mature fintech payment platform such as PayPal Holdings (PYPL) and Square (SQ)?

Offering low cost and efficient services is the first step in the right direction and I can say I’ve seen weirder things happen in the world.

Western Union certainly is in a position of strength as it cruises into the first innings of its digital migration and I believe there is more room to run for the stock until $30.

Mad Hedge Technology Letter

August 2, 2019

Fiat Lux

Featured Trade:

(THE GREAT LATIN AMERICAN INTERNET PLAY),

(MELI), (PYPL), (AMZN), (EBAY)

How do you get exposure to the e-commerce story in Latin America?

The best way to do that is to dive into Mercado Libre (MELI), meaning “free market” in Spanish, an Argentine company incorporated in the United States that operates online marketplaces dedicated to e-commerce and online auctions, including mercadolibre.com.

Mercado Libre was established as an Argentine company in 1999 and Founder & CEO Marcos Galperin, while attending Stanford University, acquired funding from HM Capital Partners co-founder John Muse to start his brainchild.

Mercado Libre received additional funding from JPMorgan Partners, Flatiron Partners, Goldman Sachs, GE Capital, and Banco Santander Central Hispano.

The company has used M&A along with organic growth to drive the company.

Relevant examples are of eBay (EBAY) buying a 19.5% stake in the company and then selling its stake in Mercado Libre in 2016, but the companies continue to expand eBay sellers into Latin America.

The cooperation remains strong with eBay opening its first branded store on the Mercado Libre marketplace from Chile in March 2017.

Mercado Libre has acquired iBazar Como, the Brazilian subsidiary of eBay's earlier acquisition, iBazar S.A.

The success culminated with becoming the first Latin American technology company to be listed on the NASDAQ, under the ticker symbol MELI.

The firm offers investors a way to invest in one of the fastest-growing e-commerce markets in the world.

The company has 280 million registered users out of 644 million people who live in Latin America.

The stock has soared 543% in the last five years making the firm one of the fastest growing e-commerce companies in the world by many metrics.

The main drag is that the valuation looks frothy at these price levels.

Mobile payments have mushroomed naturally because of its title, the "eBay of Latin America."

They can also claim to be the PayPal of the region, thanks to robust growth happening in the MercadoPago digital payments business.

In the first quarter, total payment volume rose 82.5% year-over-year.

Off-marketplace payment volume is up 194% – accelerating each and every quarter.

Off-marketplace payments now comprise 45% of the company's total payment volume, and management sees high penetration trends happening in certain areas.

PayPal (PYPL) have become huge supporters of MercadoLibre with an investment of $750 million into MercadoPago.

The deal will join the firms together to work on the shared vision to digitize the economy, especially for the underbanked, in Latin America.

It's a stamp of approval of Mercado's brand recognition in the region that PayPal chose to invest in the company instead of competing.

How fast is the addressable market growing?

Investors have been seduced by the company's impressive growth in payments, but the core marketplace business is still doing backflips.

Gross merchandise volume (GMV) expanded 27% year-over-year in the first quarter, driven by 70% growth in Mexico.

Brazil is the largest market and expanded GMV by 18% year-over-year in the quarter.

Management referenced supermarket items in Mexico and increasing apparel selection as two areas that are showing strong results.

Apparel is the fastest-growing category, up 79% year-over-year last quarter.

With signs that new development is headed in the right direction, new categories and the company expanding its logistics footprint, the market will definitely expand.

MercadoLibre can grow beyond the marketplace business to become a formidable fintech company.

As it expands into other services, Mercado is fortifying its strong brand across Latin America.

Even as Amazon.com (AMZN) enters the high stakes industry, Mercado's first mover advantage can’t be underestimated.

The stock is pricey so lay off it for the time being but add with any major dips.

Mad Hedge Technology Letter

June 13, 2019

Fiat Lux

Featured Trade:

(THE TRADE WAR MOVES DOWN MARKET)

(DOCU), (PSTG), (ZUO), (MSFT), (PYPL), (ADBE)

To understand the consequences of the global trade war, just take a look at the second-tier software companies.

There has been softness in the latest earnings reports and guidance signaling a lukewarm upcoming summer.

The best-case scenario is the likes of DocuSign (DOCU) and Zuora (ZUO) rallying into the end of the year.

That is hardly a given considering the global turmoil has shifted supply chains in every which way as well as denting overall demand.

Cloud-based companies have seen meaningful weakness this earnings season, even some of them absorbing heavy losses in the wake of their quarterly results, but analysts aren’t ready to write off this industry yet.

Referencing the latest industry survey, 20 software companies reported results in the last month, and of those, only six saw a positive response in their stock prices.

DocuSign and Pure Storage (PSTG) were among names that got clobbered, along with cloud-computing plays like Cloudera Inc., Nutanix Inc., Box Inc., and Pivotal Software Inc.

The current malaise in software is due to higher valuations and macroeconomic issues which subsequently elevates uncertainty.

There is no reason to go hysterical over this, and in no way, shape, or form, does this signal an imminent implosion of cloud companies, any incremental caution may be reversible if macro indicators and sentiment rebound.

And this rebound can be swift once all the stars align together.

Adding to the comfort is that some of the sharp drawdowns were company-specific reasons.

MongoDB Inc. or Zscaler Inc., were coming off strong year-to-date advances in their shares and it was time to take profits before the next upward explosion.

Cybersecurity company Zscaler, is appropriately accounting for outperformance and have already been crushing higher than normal expectations.

DocuSign eclipsed expectations on some metrics but disappointed on others, such as billings growth.

This disappointing miss punished the company with a drop of 15% in the pre-market session, as DocuSign grew sales by 27%, a lower rate than in previous quarters.

Management blamed the poor performance to an elongated sales cycle.

Bulls were hoping for a beat-and-raise quarter and instead got in-line numbers with some soft spots around the periphery.

Investors aren’t in a charitable mood and the sensitive mood around geopolitics has made investors more agitated with a shorter leash.

There was a tone of a broader deceleration in software demand prompting stronger names to get comingled together, but the bulk of this negative price action has been overdone.

Even further down the pecking order, results from smaller cloud firms have pointed to more fundamental issues, and these stocks have emerged as a particularly weak sub-sector.

A number of these companies reigned in their forecasts, a trend that has buttressed analyst caution over the group.

Considering that many companies have labored and there exist clear narrative similarities, it’s hard not to surmise that some real systemic pains in infrastructure exist.

Many in the industry are acutely aware of the growing chorus of companies blaming competition or poor sales execution.

Lower growth rates are effectively the predominant reason for lower stock prices in this group of cloud companies.

On the flipside of this weaker cloud growth are the heavy hitters who are throwing around their weight getting through largely unscathed.

If any of these bigger cloud companies can fuse together a business model with no China exposure, then shares are likely stable to upward trending.

A company like Adobe (ADBE) is a perfect company to look at with an unpretentious yet steady growth rate and wildly successful products.

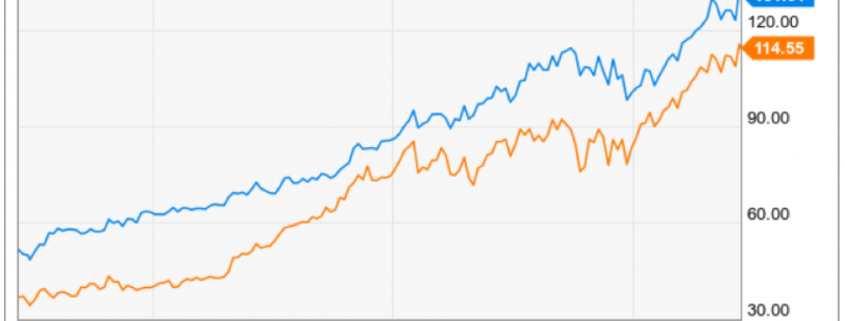

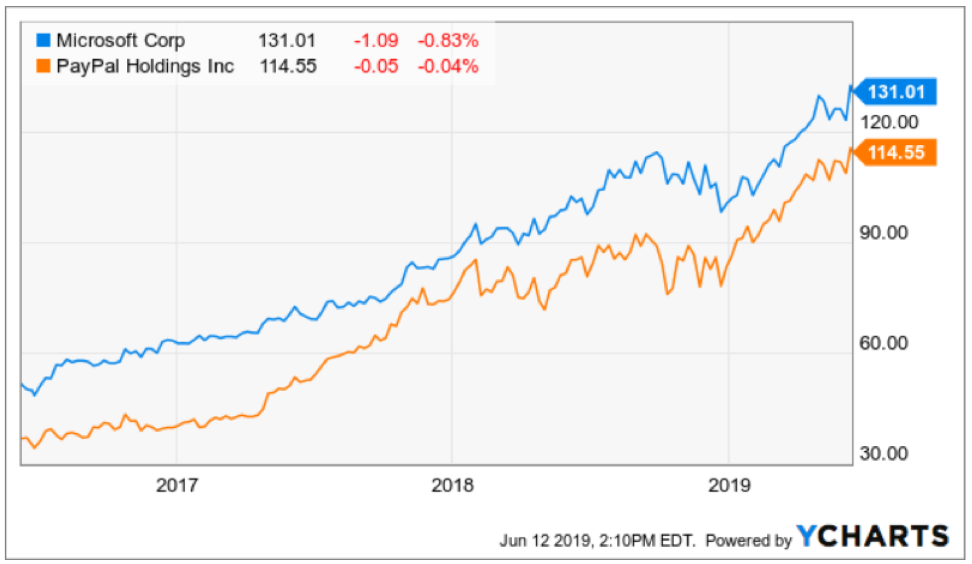

If we were to look at more growth-based companies with larger scale, then PayPal (PYPL) and Microsoft (MSFT) epitomize the type of cloud companies that are thriving in this environment and if geopolitics subsides, take on another 10% in sales.

Not only is the weather hot in the summer, but the anti-trust regulators are turning up the heat on certain tech companies on anti-trust concerns.

This could be a time to wait out those stocks and there could be another move to the upside if regulation is weaker than expected.

Mad Hedge Technology Letter

June 5, 2019

Fiat Lux

Featured Trade:

(BOX TAKES A HIT)

(BOX), (MSFT), (PYPL)