Here’s a company for you involved in technology’s tectonic shift towards FinTech in 2019.

They aren’t new, but you’ve probably never heard of them.

It’s Fiserv Inc. (FISV) which sells financial technology and can include customers such as banks, credit unions, securities broker-dealers, leasing, and finance companies.

An inflection point is occurring within the global business and that is financial technology and the rapid integration of it.

Financial institutions are building products around this concept and Fiserv has a head start on the others with more than 30 years of experience in aiding banks, thrifts, and credit unions, managing cash and processing payments, loans, and account services.

The Wisconsin-based company constructed an unstoppable machine leveraging its time-honored relationships and expertise to bring banking to all the screens that pervade daily life.

“Innovation, Integration and Scale” has been the motto that has served this company well for so long.

The company cut its teeth in the trenches helping banks move money long before it became the next big thing.

Five years ago, under the leadership of CEO Jeff Yabuki, there was a corporate flashpoint with upper management realizing they needed to evolve or die.

Yabuki anticipated a near future fueled by mobile wallets and changing consumer expectations - an always-on, never-off connected world.

An environment where consumers want what they want when they want it.

There has been no letup in this trend.

Silicon Valley companies were always the 800-pound gorilla in the room and Fiserv didn’t want to become sideswiped by them.

And in 2014, at the Money 20/20 conference in Las Vegas, Yabuki set out his vision that continues to prevail today.

The financial services industry had become obsessed with point-of-sale transactions.

And at $200 billion in annual domestic sales, it was a business that resonated to all corners of the FinTech world.

It was sensical to persuade consumers to use branded credit or debit cards to pay for stuff in stores and online.

At the time, that was bread-and-butter banking.

To the banks' chagrin, Silicon Valley has gotten in on the act with the likes of Apple (AAPL), Alphabet (GOOGL), PayPal (PYPL), Square (SQ) firing warning shots.

They formulated products of their own, whipped up the necessary scale and maximized the reverberating network effects.

Yabuki urged financiers at the conference to double down on what they did best while looking to grab low-hanging fruits in the short-term.

The business beyond point-of-sale was theirs waiting on a decorative platter – the opportunity was a $55 billion behemoth consisting of consumer-to-consumer, business-to-business and consumer-to-business transactions.

Embracing FinTech translated into massive speed advantages, stauncher security-laced products while offering traditional bank customers higher quality service at their convenience.

Fiserv erected a platform to help financial institutions focus on payments beyond POS called Network for Our World.

The goal of this NOW Network was to help customers' flow of money by paying bills and getting paid.

These entrepreneurs are looking for more efficient ways to collect money owed - they are a lucrative addressable audience for bankers.

The Fiserv sales pitch is working wonders according to the data. The company has 12,000 clients worldwide, with 85 million online banking end-users.

It has rolled out innovative products for payments, processing, risk and compliance, customer service and optimization.

The company has become ever so profitable with a 3-year EPS growth rate of just 15%, but in the last quarter, this metric surged to 23% and projected to rise.

Fiserv also dabbled with some M&A hauling in debit-based assets of Elan Financial Services.

The stellar acquisition, with annual revenue of over $170 million, extends Fiserv’s leadership in payments, broadens client reach and scale, and provides new solutions to enhance the value proposition of the existing 3,000 debit solutions clients.

The deal also gave Fiserv ownership of Money Pass, the second largest surcharge-free ATM network in the U.S., with over 33,000 in-network ATMs.

They also added other major pieces with the purchase of First Data Corp (FDC).

The maneuver is strategically solid, and Fiserv will benefit from a parlay of idiosyncratic opportunities from the combined synergies.

Fiserv will be able to refer First Data's merchant-acquiring services to the banks it currently works with.

I predict cost savings of $1 billion from the deal and potential upside from platform rationalization, which has not yet been included in synergies.

There will be significant upside potential from interest expense savings given refinancing FDC's debt at investment-grade.

Dipping your toe into this name before its multiple inevitable expands is a good long-term strategy.

Profitability is increasing while management has made moves that will fatten its top line business from the 5% internal growth today.

All these growth levers will push up revenues in the upcoming quarters - Fiserv happens to be the right company in the right industry at the perfect time in the technology cycle.

The stock is up over 1,000% in 10 years.

In February 2009, the stock was meddling around $8 and the $83 it trades at today demonstrates the potency of FinTech and the strength in their underlying business model.

I would wait for a sell-off to get into this one, but it’s a keeper.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/02/GOOG-feb5.png566974Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-02-05 01:06:222019-02-05 01:12:18The FinTech Company You've Never Heard of

A highly compelling argument – that was my initial reaction after diving into Elliot Management’s letter to eBay’s (EBAY) shareholders after the ruthless investor activist announced an over 4% stake in one of the original online marketplace giants.

Not only that, hedge fund Starboard Value LP also has gotten in on the act with a position of less than 4%.

Starboard has doubled down agreeing with the general points of Elliot Management’s prognosis on the weakness of eBay’s business model

There are no two ways about it - eBay has been condemned to tech purgatory as of late and is in dire need of a facelift.

If you’re a manager of any sort of magnitude at e-commerce platform eBay, this was the letter of doom and gloom you hoped you would never get.

The equity Gods have been harsh to eBay as PayPal (PYPL), one of the Mad Hedge Technology Letter’s favorite picks in 2019, has risen over 130% after spinning off from eBay in 2015.

eBay is down substantially since that point in time reflecting a poorly run business in a secular growth industry that has produced home runs most evident in the performance of Jeff Bezos’ Amazon.com (AMZN).

The gist of Elliot’s diagnosis centered around the terrible operational execution at the Silicon Valley firm.

It essentially repeats this premise over and over throughout the content.

Current management is historically bad that any efficiencies implemented into the platform would boost growth reverting it back to a point closer to a trajectory that echoes closer to a normal high growth e-commerce company.

How did eBay peter out to mediocrity?

Let me explain.

There is a time-established pattern that Elliot Management identified – eBay management increasing spend to stimulate growth, failing to deliver the goods and reverting back to square one.

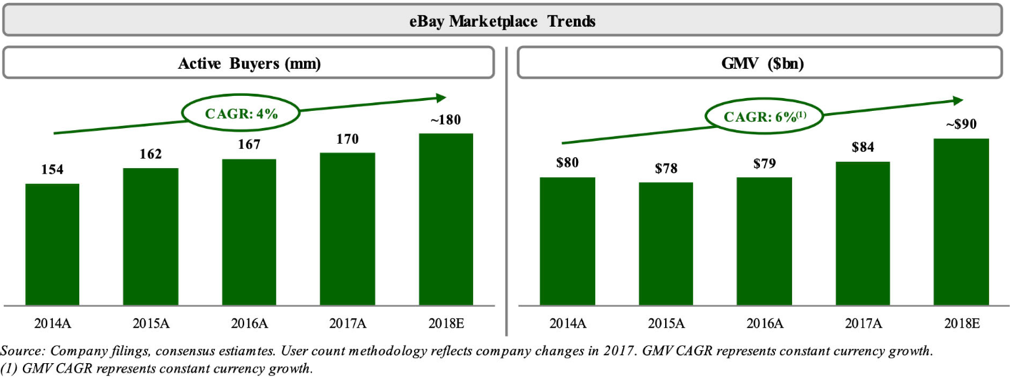

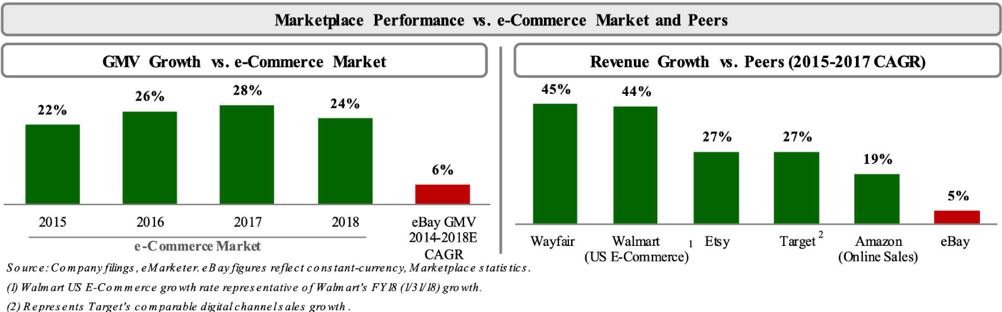

The result is paltry growth in the mid-single digits which can be seen in minimal growth numbers in the gross merchandise volume (GMV), a metric established to gauge the total amount of volume pushed through eBay.

The activist hedge fund claimed that shares could potentially double if their calculated plan could shortly be deployed.

The plan was straight forward and there was no innovative x-factors described or pivot to augmented reality or machine learning that many firms like to hype up.

Elliot’s strategy is purely operational relating to the core business – where is Tim Cook when you need him!

The argument originates from whether eBay management can allocate resources more efficiently, focus on boosting foundational growth in the core marketplace, and develop new verticals that were completely missed in its development, then the stock would react favorably.

I would even double down and say that if they do half of what they promise in the Elliot’s letter, shares should pop at least 30%.

eBay exists under a backdrop of massive secular drivers fueling e-commerce.

The industry is the most robust in the economy and is expanding in the mid-20% even as global sales are about to eclipse the $3 trillion mark.

E-commerce just has a penetration rate of 10% and the runway is long which should enable mainstay companies to grow their top and bottom line if not botched completely.

Average consumer spending is in the throes of major disruption from analog brick and mortar stores to digital e-commerce, and eBay’s strategic position offers an advantageous platform to carve out e-commerce success moving forward.

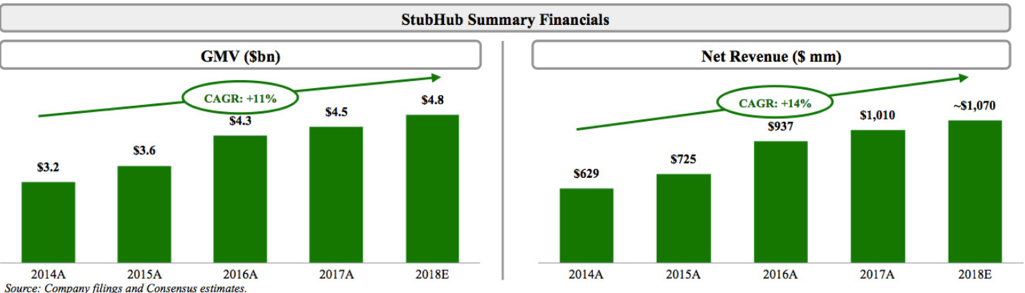

The first thing Elliot wants to do is reach up their sleeve for a little financial engineering magic by spinning out in-house mega-growth assets of StubHub, the e-ticket event vendor, and its portfolio of premium classified properties that possess double-digit sales growth and elevated margins.

Elliot argues that these two assets would perform better on a standalone basis because they wouldn’t be bogged down by eBay turning around the core business which could possibly result in some misallocated capital and delays.

The valuation of eBay’s Classified Groups assets is around $4.5 billion, but segment that out and the value could represent $10 billion.

The same boost in valuation applies to event ticket seller platform StubHub. The company is valued at just $2.2 billion under the umbrella of eBay but tear the baby out of eBay’s uterus and suddenly the valuation balloons to a rosier $4 billion.

Watching from afar, Elliot has pinpointed management’s “self-inflicted mis-execution” and management must summon all their power and resources to direct “singular attention to growing and strengthening marketplace.”

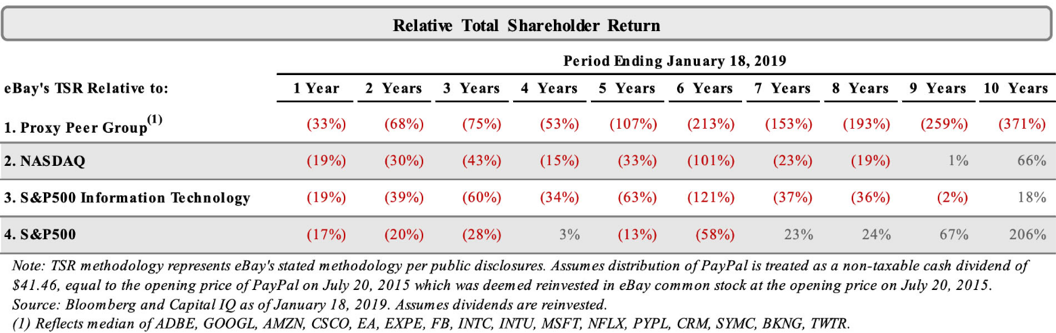

eBay has severely underperformed in share price relative to its peers by 107% in the past 5 years. Extrapolate the time horizon to 10 years and the underperformance shoots up to 371%.

These have been the tech golden years and there is no feasible excuse to why this company hasn’t been able to perform better or equal relative to their peer group.

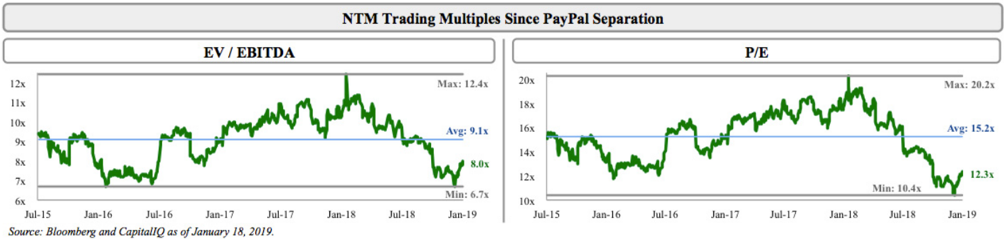

eBay is the second biggest e-commerce platform in the world but only trades at a PE of 12 showing the malaise of investor sentiment surrounding this name.

This is unfortunate because eBay has strong embedded actionable communities in South Korea, Australia, Italy, Germany, U.K., U.S., and Canada.

The tools are there but it is hard to take a stab when the tool is blunted by poor management.

Compare slow growth with the rocket-fueled growth of asset StubHub which has almost doubled revenue in the past 5 years.

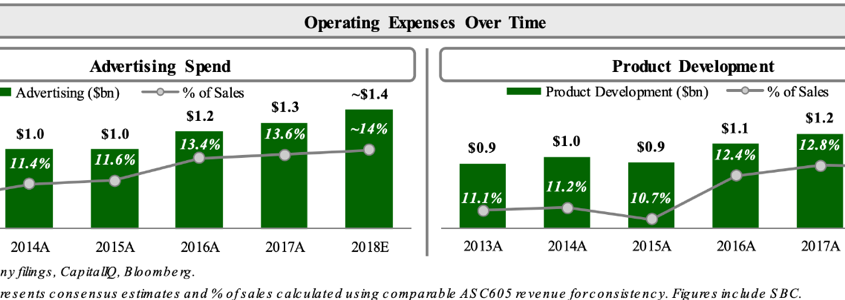

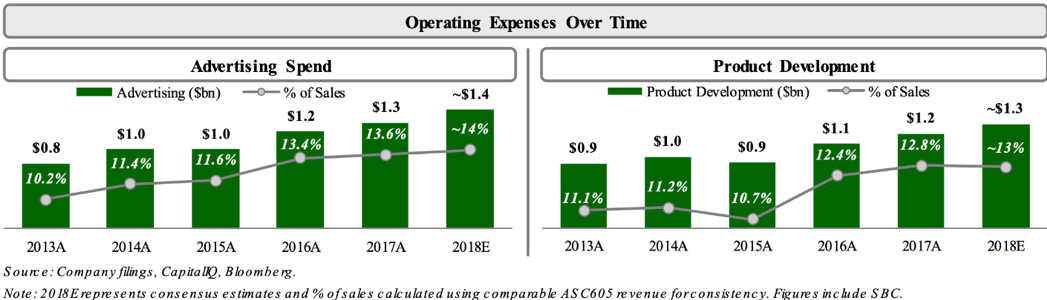

eBay has lifted advertising spend by 70% since 2013 and revved up product development by 45% as well. This has surprisingly led to material margin declines because of the failure of these initiatives to take hold.

One of the missteps resulting in this margin softness is the dysfunctional execution of its online platform infected by technical problems and operational headwinds.

A few notable events were a 2014 broad-based password hack and the botched fix to that problem exacerbated by a muddied communication strategy.

During this time, eBay was outmaneuvered by Google’s (GOOGL) search algorithm resulting in a massive decline in traffic as a result of this painful change.

The next year was similarly awful with a shoddy mobile application that did not resonate with customers and was put out to pasture shortly after rolling it out.

An online marketplace offering a platform for over four million buyers and sellers to carry out business requires high-level functioning. A failure to deliver this experience has caused long-time users to jump ship to other niche vertical platforms.

Innovative endeavors aren’t part of this new strategy to remake the company.

The underlying strategy effectively spells out that eBay needs to become more like Amazon and any sort of moderate success in doing that will positively boost the stock price – let’s call it what it is – an operational overhaul and nothing more than that.

The complaints don’t stop there and last year eBay was inundated with technical issues that included incorrect billing, deleted photos, warped title presentation, and senior management took the blame in a podcast confessing that management needs to pull things together and they “don’t want to repeat (the same mistakes) on a number of levels. And the technology issues that we have had with the platform are on top of the list.”

eBay is not a startup and presides over a profitable business.

Returning capital to shareholders was part of the plan as well.

This entails repurchasing shares of up to $5 billion which was $1 billion more than the original guidance – Elliot Management is an activist investor after all hoping to super-charge shareholder income streams.

Elliot wants to implement a 1.5% dividend yield due to eBay’s high free cash flow model.

After 2020, Elliot wants to allocate 80% of free cash flow for share repurchases and earmark the other 20% for M&A activity.

It is difficult to surmise if this plan will work smoothly or not, but if Elliot can bring in the correct team to execute this plan, I would give them the benefit of the doubt as making this plan into a viable success seems realistic.

But it is yet to be seen how laborious it will be to get the people they want through the door.

eBay is truly a unique asset and the chopped-down nature of its shares would stage a remarkable turnaround if some proven management from Amazon’s executive team could be captured and convinced that eBay is a legitimate option.

Easier said than done, but this is a step in the right direction.

My Luger is firmly in my holster and waiting for some action - if there are any whiffs of a real turnaround then I’ll shoot out some eBay trade alerts.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/01/operating-expense.png3001047Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-24 01:06:222019-07-09 04:55:37Activists Lay In on eBay

Going into January 2018, the big banks were highlighted as the pocket of the equity market that would most likely benefit from a rising rate environment which in turn boosts net interest margins (NIM).

Fast forward a year and take a look at the charts of Bank of America (BAC), Citibank (C), JP Morgan (JPM), Goldman Sachs (GS), and Morgan Stanley (GS), and each one of these mainstay banking institutions are down between 10%-20% from January 2018.

Take a look at the Financial Select Sector SPDR ETF (XLF) that backs up my point.

And that was after a recent 10% move up at the turn of the calendar year.

As much as it pains me to say it, bloated American banks have been completely caught off-guard by the mesmerizing phenomenon that is FinTech.

Banking is the latest cohort of analog business to get torpedoes by the brash tech start-up culture.

This is another fitting example of what will happen when you fail to evolve and overstep your business capabilities allowing technology to move into the gaps of weakness.

Let me give you one example.

I was most recently in Tokyo, Japan and was out of cash in a country that cash is king.

Japan has gone a long way to promoting a cashless society, but some things like a classic sushi dinner outside the old Tsukiji Fish Market can’t always be paid by credit card.

I found an ATM to pull out a few hundred dollars’ worth of Japanese yen.

It was already bad enough that the December 2018 sell-off meant a huge rush into the safe haven currency of the Japanese Yen.

The Yen moved from 114 per $1 down to 107 in one month.

That was the beginning of the bad news.

I whipped out my Wells Fargo debit card to withdraw enough cash and the fees accrued were nonsensical.

Not only was I charged a $5 fixed fee for using a non-Wells Fargo ATM, but Wells Fargo also charged me 3% of the total amount of the transaction amount.

Then I was hit on the other side with the Japanese ATM slamming another $5 fixed fee on top of that for a non-Japanese ATM withdrawal.

For just a small withdrawal of a few hundred dollars, I was hit with a $20 fee just to receive my money in paper form.

Paper money is on their way to being artifacts.

This type of price gouging of banking fees is the next bastion of tech disruption and that is what the market is telling us with traditional banks getting hammered while a strong economy and record profits can’t entice investors to pour money into these stocks.

FinTech will do what most revolutionary technology does, create an enhanced user experience for cheaper prices to the consumers and wipe the greedy traditional competition that was laughing all the way to the bank.

The best example that most people can relate to on a daily basis is the transportation industry that was turned on its head by ride-sharing mavericks Uber and Lyft.

But don’t ask yellow cab drivers how they think about these tech companies.

Highlighting the strong aversion to traditional banking business is Slack, the workplace chat app, who will follow in the footsteps of online music streaming platform Spotify (SPOT) by going public this year without doing a traditional IPO.

What does this mean for the traditional banks?

Less revenue.

Slack will list directly and will set its own market for the sale of shares instead of leaning on an investment bank to stabilize the share price.

Recent tech IPOs such as Apptio, Nutanix and Twilio all paid 7% of the proceeds of their offering to the underwriting banks resulting in hundreds of millions of dollars in revenue.

Directly listings will cut that fee down to $10-20 million, a far cry from what was once status quo and a historical revenue generation machine for Wall Street.

This also layers nicely with my general theme of brokers of all types whether banking, transportation, or in the real estate market gradually be rooted out by technology.

In the world of pervasive technology and free information thanks to Google search, brokers have never before added less value than they do today.

Slowly but surely, this trend will systematically roam throughout the economic landscape culling new victims.

And then there are the actual FinTech companies who are vying to replace the traditional banks with leaner tech models saving money by avoiding costly brick and mortar branches that dot American suburbs.

PayPal (PYPL) has been around forever, but it is in the early stages of ramping up growth.

That doesn’t mean they have a weak balance sheet and their large embedded customer base approaching 250 million users has the network effect most smaller FinTech players lack.

PayPal is directly absorbing market share from the big banks as they have rolled out debit cards and other products that work well for millennials.

They are the owners of Venmo, the super-charged peer-to-peer payment app wildly popular amongst the youth.

Shares of PayPal’s have risen over 200% in the past 2 years and as you guessed, they don’t charge those ridiculous fees that banks do.

Wells Fargo and Bank of America charge a $12 monthly fee for balances that dip below $1,500 at the end of any business day.

Your account at PayPal can have a balance of 0 and there will never be any charge whatsoever.

Then there is the most innovative FinTech company Square who recently locked in a new lease at the Uptown Station in Downtown Oakland expanding their office space by 365,000 square feet for over 2,000 employees.

Square is led by one of the best tech CEOs in Silicon Valley Jack Dorsey.

Not only is the company madly innovative looking to pounce on any pocket of opportunity they observe, but they are extremely diversified in their offerings by selling point of sale (POS) systems and offering an online catering service called Caviar.

They also offer software for Square register for payroll services, large restaurants, analytics, location management, employee management, invoices, and Square capital that provides small loans to businesses and many more.

On average, each customer pays for 3.4 Square software services that are an incredible boon for their software-as-a-service (SaaS) portfolio.

An accelerating recurring revenue stream is the holy grail of software business models and companies who execute this model like Microsoft (MSFT) and Salesforce (CRM) are at the apex of their industry.

The problem with trading this stock is that it is mind-numbingly volatile. Shares sold off 40% in the December 2018 meltdown, but before that, the shares doubled twice in the past two years.

Therefore, I do not promote trading Square short-term unless you have a highly resistant stomach for elevated volatility.

This is a buy and hold stock for the long-term.

And that was only just two companies that are busy redrawing the demarcation lines.

There are others that are following in the same direction as PayPal and Square based in Europe.

French startup Shine is a company building an alternative to traditional bank accounts for freelancers working in France.

First, download the app.

The company will guide you through the simple process — you need to take a photo of your ID and fill out a form.

It almost feels like signing up to a social network and not an app that will store your money.

You can send and receive money from your Shine account just like in any banking app.

After registering, you receive a debit card.

You can temporarily lock the card or disable some features in the app, such as ATM withdrawals and online payments.

Since all these companies are software thoroughbreds, improvement to the platform is swift making the products more efficient and attractive.

There are other European mobile banks that are at the head of the innovation curve namely Revolut and N26.

Revolut, in just 6 months, raised its valuation from $350 million to $1.7 billion in a dazzling display of growth.

Revolut’s core product is a payment card that celebrates low fees when spending abroad—but even more, the company has swiftly added more and more additional financial services, from insurance to cryptocurrency trading and current accounts.

Remember my little anecdote of being price-gouged in Tokyo by Wells Fargo, here would be the solution.

Order a Revolut debit card, the card will come in the mail for a small fee.

Customers then can link a simple checking account to the Revolut debit card ala PayPal.

Why do this?

Because a customer armed with a Revolut debit card linked to a bank account can use the card globally and not be charged any fees.

It would be the same as going down to your local Albertson’s and buying a six-pack, there are no international or hidden fees.

There are no foreign transaction fees and the exchange rate is always the mid-market rate and not some manipulated rate that rips you off.

Ironically enough, the premise behind founding this online bank was exactly that, the originators were tired of meandering around Europe and getting hammered in every which way by inflexible banks who could care less about the user experience.

Revolut’s founder, Nikolay Storonsky, has doubled down on the firm’s growth prospects by claiming to reach the goal of 100 million customers by 2023 and a succession of new features.

To say this business has been wildly popular in Europe is an understatement and the American version just came out and is ready to go.

Since December 2018, Revolut won a specialized banking license from the European Central Bank, facilitated by the Bank of Lithuania which allows them to accept deposits and offer consumer credit products.

N26, a German like-minded online bank, echo the same principles as Revolut and eclipsed them as the most valuable FinTech startup with a $2.7 Billion Valuation.

N26 will come to America sometime in the spring and already boast 2.3 million users.

They execute in five languages across 24 countries with 700 staff, most recently launching in the U.K. last October with a high-profile marketing blitz across the capital.

Most of their revenue is subscription-based paying homage to the time-tested recurring revenue theme that I have harped on since the inception of the Mad Hedge Technology Letter.

And possibly the best part of their growth is that the average age of their customer is 31 which could be the beginning of a beautiful financial relationship that lasts a lifetime.

N26’s basic current account is free, while “Black” and “Metal” cards include higher ATM withdrawal limits overseas and benefits such as travel insurance and WeWork membership for a monthly fee.

Sad to say but Bank of America, Wells Fargo, and the others just can’t compete with the velocity of the new offerings let alone the software-backed talent.

We are at an inflection point in the banking system and there will be carnage to the hills, may I even say another Lehman moment for one of these stale business models.

Online banking is here to stay, and the momentum is only picking up steam.

If you want to take the easy way out, then buy the Global X FinTech ETF (FINX) with an assortment of companies exposed to FinTech such as PayPal, Square, and Intuit (INTU).

The death of cash is sooner than you think.

This year is the year of FinTech and I’m not afraid to say it.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-17 01:06:502019-07-09 04:56:36Why FinTech is Eating the Banks’ Lunch

As 2019 christens us with new technological trends, building our portfolio and lives around these themes will give us a leg up in battling the algorithms that have upped the ante in our drive to get ahead.

Now it’s time to chronicle some of these trends that will permeate through the tech universe.

Some are obvious, and some might as well be hidden treasures.

Smart Areas Will Conspicuously Advance

American consumers will start to notice that locations they frequent and the proximities around them will integrate more smart-tech.

The hoards of data that big tech possesses and the profiles they subsequently create on the American consumer will advance allowing the possibilities of more precise and useful products.

These products won’t just accumulate in a person’s home but in public areas, and business will jump at the chance to improve services if it means more revenue.

Amazon and Google have piled money into the smart home through the voice assistant initiatives and adoption has been breathtaking.

The next generation will provide even more variety to integrate into daily lives.

Location-based Dispersion Will Ramp Up

The gains in technology have given the consumer broader control over their lives.

The ability to practically manage one’s life from a remote location has remarkably improved leaps and bounds.

The deflation of mobile phone data costs, the advancement of high-speed broadband internet services in developing countries, more cloud-based software accessible from any internet entry point, and the development of affordable professional grade hardware have made life easy for the small business owners.

What a difference a few years make!

This has truly given a headache for traditional companies who have failed to evolve with the times such as television staples who rely on analog advertising revenue.

Millennials are more interested in flicking on their favorite YouTuber channel who broadcast from anywhere and aren’t locally based.

Another example is the quality of cameras and audio equipment that have risen to the point that anybody can become the next Justin Bieber.

Music executives are even using Spotify to target new talent to invest in.

Overhyped Bitcoin Will Finally Take A Siesta From The Mainstream

Blockchain technology has the makings of transforming the world we live in.

And the currency based on the blockchain technology had a field day in the press and backyard summer barbecues all over the country.

Well, 2019 will finally put this topic on the backburner even though Bitcoin won’t disappear into irrelevancy, the pendulum will swing the other direction and this digital currency will become underhyped.

The rise to $20,000 and the catastrophic selloff down to $4,000 was a bubble popping in front of us.

It made a lot of people rich like the Winklevoss brothers Cameron and Tyler who took the $65 million from Facebook CEO Mark Zuckerberg and spun it into bitcoin before the euphoria mesmerized the American public.

On the way down from $20,000, retail investors were tearing their hair out but that is the type of volatility investors must subscribe to with assets that are far out on the risk curve.

The volatility that FinTech leader Square (SQ) and OTT Box streamer Roku (ROKU) have are nothing compared to the extreme volatility that digital currency investors must endure.

E-Sports Will Become Even More Popular

Video games classified as a spectator sport will expand up to 40% in 2019.

This phenomenon has already captivated the Asian continent and is coming stateside.

This is a bit out of my realm as standard spectator sports don’t appeal to me much at all, and watching others play video games for fun is something I am even further removed from.

But that’s what the youth like and how they grew up, and this trend shows no signs of stopping.

Industry experts believe that the U.S. is at an inflection point and adoption will accelerate.

Remember that kids don’t play physical sports anymore because of the risk to head trauma, blown ligaments, and the sheer distances involved traveling to and from venues turn participants away.

Franchise rights, advertising, and streaming contracts will energize revenue as a ballooning audience gravitates towards popular leagues, tapping into the fanbase for successful video game series such as Overwatch.

The rise of eSports can be attributed to not only kids not playing physical sports but also younger people watching less television and spending more time online.

Soon, there will be no difference in terms of pay and stature of pro athletes and video gaming athletes.

The amount of money being thrown at the world’s best gamers makes your spine tingle.

Data Regulation Will Tighten

The era of digital data regulation is upon us and whacked a few companies like Google and Facebook in 2018.

Well, this is just the beginning.

The vacuum that once allowed tech companies to run riot is no more, and the government has big tech in their cross-hairs.

The A word will start to reverberate in social circles around the tech ecosphere – Antitrust.

At some point towards the end of 2019, some of these mammoth technology companies could face the mother of all regulation in dismantling their business model through an antitrust suit.

Companies such as Amazon and Facebook are praying to the heavens that this never comes to fruition, but the rhetoric about it will slowly increase in 2019 because of the mischievous ways these tech companies have behaved.

The unintended consequences in 2018 were too widespread and damaging to ignore anymore.

Antitrust lawsuits will creep closer in 2019 and this has spawned an all-out grab for the best lobbyists tech money can buy.

Tech lobbyists now amount to the most in volume historically and they certainly will be wielded in the best interest of Silicon Valley.

Watch this space.

Software Favored To Hardware

The demand for smart consumer devices will fall off a cliff because most of the people who can afford a device already are reading my newsletter from it.

The stunting of smart device innovation has made the upgrade cycle duration longer and consumers feel no need to incrementally upgrade when they aren’t getting more bang for their buck.

The late-cycle nature of the economy that is losing momentum because of a trade war and higher interest rates will see companies look to add to efficiencies by upgrading software systems and processes.

This bodes well for companies such as Microsoft (MSFT), Salesforce (CRM), Twilio (TWLO), PayPal (PYPL), and Adobe (ADBE) in 2019.

Logistics Gets A Boost From Technology

This is where Amazon has gotten so good at efficiently moving goods from point A to point B that it is threatening to blow a hole in the logistic stalwarts of UPS and FedEx.

Robots that help deploy packages in the Amazon warehouses won’t just be an Amazon phenomenon forever.

Smaller businesses will be able to take advantage of more robotics as robotics will benefit from the tailwind of deflation making them affordable to smaller business owners.

Amazon’s ramp-up in logistics was a focal point in their purchase of overpriced grocer Whole Foods.

This was more of a bet on their ability to physically deliver well relative to competition than it was its ability to stock above average quality groceries.

If Whole Foods ever did fail, Amazon would be able to spin the prime real estate into a warehouse located in wealthy areas serving the same wealthy clientele.

Therefore, there is no downside short or long-term by buying Whole Foods. Amazon will be able to fine-tune their logistics strategy which they are piling a ton of innovation into.

Possible new logistical innovations include Amazon attempting to deliver to garages to avoid rampant theft.

This is all happening while Amazon pushes onto FedEx’s (FDX) and UPS’s (UPS) turf by building out their own fleet.

Innovative logistics is forcing other grocers to improve fast giving customers better grocery service and prices.

Kroger (KR) has heavily invested in a new British-based logistics warehouse system and Walmart (WMT) is fast changing into a tech play.

Tech Volatility Won’t Go Away

Current Chair of the Federal Reserve Jerome Powell unleashed a dragon when he boxed himself into a corner last year and had to announce a rate hike to preserve the integrity of the institution.

Markets whipsawed like a bull at a rodeo and investors lost their pants.

Tech companies who have been leading the economy and trot out robust EPS growth out of a whole swath of industries will experience further volatility as geopolitics and interest rate rhetoric grips the world.

Apple’s revenue warning did not help either and just wait until semiconductors start announcing disastrous earnings.

The short volatility industry crashed last February, and the unwinding of the Fed’s balance sheet mixed with the Chinese avoiding treasury purchases due to the trade war will insert even more volatility into the mix.

Powell attempted to readjust his message by claiming that the Fed “will be patient” and tech shares have had a monstrous rally capped off with Roku exploding over 30% after news of positive subscriber numbers and news of streaming content platform Hulu blowing past the 25 million subscriber mark.

Volatility is good for traders as it offers prime entry points and call spreads can be executed deeper in the money because of the heightened implied volatility.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/01/warehouse-robots.png512852Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-09 01:06:182019-07-09 04:58:15Top 8 Tech Trends of 2018

On Friday, five serious hedge fund managers separately called me out of the blue and all had the same thing to say. They had never seen the market so negative before in the wake of the worst quarter in seven years. Therefore, it had to be a “BUY”.

I, on the other hand, am a little more cautious. I have four 10% positions left that expire on Friday, in four trading days, and on that day I am going 100% into cash. At that point, I will be up 3.5% for the month of December, up 31.34% on the year, and will have generated positive return for one of the worst quarters in market history.

I’m therefore going to call it a win and head for the High Sierras for a well-earned Christmas vacation. After that, I am going to wait for the market to tell me what to do. If it collapses, I’ll buy it. If it rockets, I’ll sell short. And I’ll tell you why.

These are not the trading conditions you would expect when the economy is humming along at a 2.8% annual rate, unemployment is running at a half-century low, and earnings are growing a 26% year on year. You can’t find a parking spot in a shopping mall anywhere.

However, the lead stocks like Apple (AAPL), Amazon (AMZN), and Netflix (NFLX) have plunged by 30%-60%. Price earnings multiples dropped by a stunning 27.5% from 20X to 14.5X in a mere ten weeks. Half of the S&P 500 (SPY) is in a bear market, although the index itself isn’t there yet. I would rather be buying markets on their way up than to try and catch a falling knife.

There is only one catalyst for that apparent yawning contradiction: The President of the United States.

Trump has created a global trade war solely on his own authority. Only he can end it. As a result, asset classes of every description are beset with uncertainty, confusion, and doubt about the future. Analysts are shaving 2019 growth forecasts as fast as they can, businesses are postponing capital spending plans, and investors are running for the sidelines in droves. Business confidence is falling like a rock

To paraphrase a saying they used to teach you in Marine Corps flight school, “It’s better to be in cash wishing you were fully invested than to be fully invested wishing you were in cash.”

The Chinese have absolutely no interest in caving into Trump’s wishes. They read the New York Times, see the midterm election result and the opinion polls, and are willing to bet that they can get a much better deal from a future president in two years.

I have been dealing personally with both Trump and the Chinese government for four decades. The Middle Kingdom measures history in Millenia. The president lives from tweet to tweet. The Chinese government can take pain by simply ordering its people to take it. We have elections every two years with immediate consequences.

The best we can hope for is that the president folds, declares victory, and then retreats from his personal war. This can happen at any time, or it may not happen at all. No one has an advantage in predicting what will happen with any certainty. Not even the president knows what he is going to do from minute to minute.

It is the possibility of trade peace at any time that has kept me out of the short side of the stock market in this severe downturn. That robs a real hedge fund manager of half his potential income. Trade peace could be worth an instant rally of 10% in the stock market. Even a lesser move, like the firing of trade advisor Peter Navarro, would accomplish the same.

The market was long overdue for a correction like the one we have just had. Investors were getting overconfident, cocky, and excessively leveraged. In October, we really needed the tide to go out to see who was swimming without a swimsuit. But if the tide goes out too far, we will all appear naked.

Thanks to some very artful trading, my year to date return recovered to +27.54% boosting my trailing one-year return back up to 27.54%. I covered an aggressive short position in the bond market (TLT) for a welcome 14.4% profit. I also took profits with an instant winner in PayPal (PYPL). On the debit side, I stopped out of an Apple call spread for a minimal loss.

December is showing a very modest loss at -0.26%. The market has become virtually untradeable now, with tweets and China rumors roiling markets for 500 points at a pop. And this is against a Dow Average that is down a miserable -2.8% so far in 2018. I should have listened to my mother when she wanted me to become a doctor.

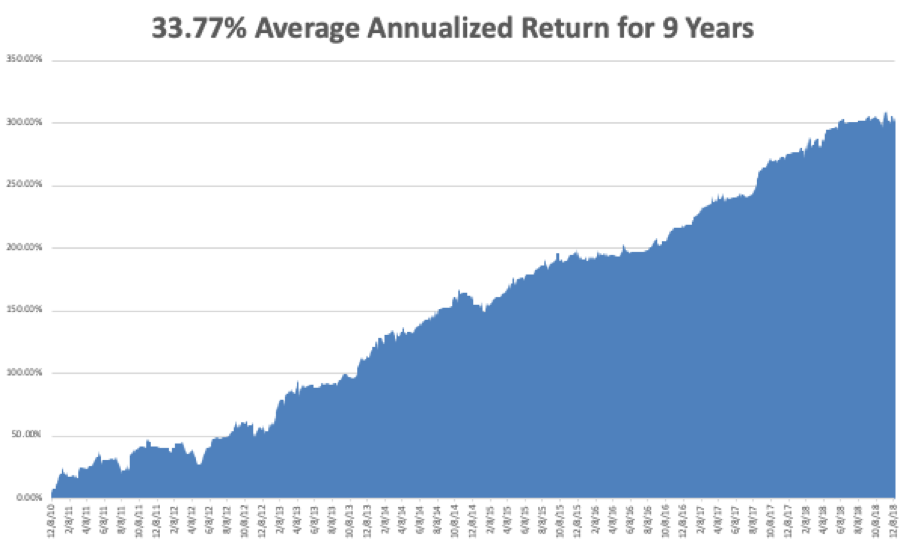

My nine-year return nudged up to +304.01. The average annualized return revived to +33.77.

The upcoming week is all about housing data, with the big focus on the Fed’s interest rate hike on Wednesday.

Monday, December 17 at 10:00 AM EST, the November Homebuilders Index is out.

On Tuesday, December 18 at 8:30 AM, November Housing Starts are published.

On Wednesday, December 19 at 10:00 AM EST, November Existing Home Sales are released.

At 10:30 AM EST the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

At 2:00 PM the Federal Reserve Open Market Committee announces a 25 basis point rise in interest rates, taking the overnight rate to 2.25% to 2.50%. An important press conference with governor Jay Powell follows.

Thursday, December 20 at 8:30 AM EST, we get Weekly Jobless Claims.

On Friday, December 21, at 8:30 AM EST, we learn the latest revision to Q3 GDP which now stands at 2.8%.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’ll be battling snow storms driving up to Lake Tahoe where I’ll be camping out for the next two weeks. Mistletoe, eggnog, and endless games of Monopoly and Scrabble await me.

Good luck and good trading!

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2018/12/Skii-Resort.png354474MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-12-17 01:06:132018-12-16 21:17:04The Market Outlook for the Week Ahead, or There’s No Santa Claus in China

(DECEMBER 12 BIWEEKLY STRATEGY WEBINAR Q&A), (SPX), (MU), (PYPL), (SPOT), (FXE), (FXY), (XLF), (MSFT), (AMZN), (TSLA), (XOM), (SIGN UP NOW FOR TEXT MESSAGING OF TRADE ALERTS)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2018-12-14 01:08:312018-12-13 15:01:56December 14, 2018

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.