Below please find subscribers’ Q&A for the Mad Hedge Fund Trader December 12 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader

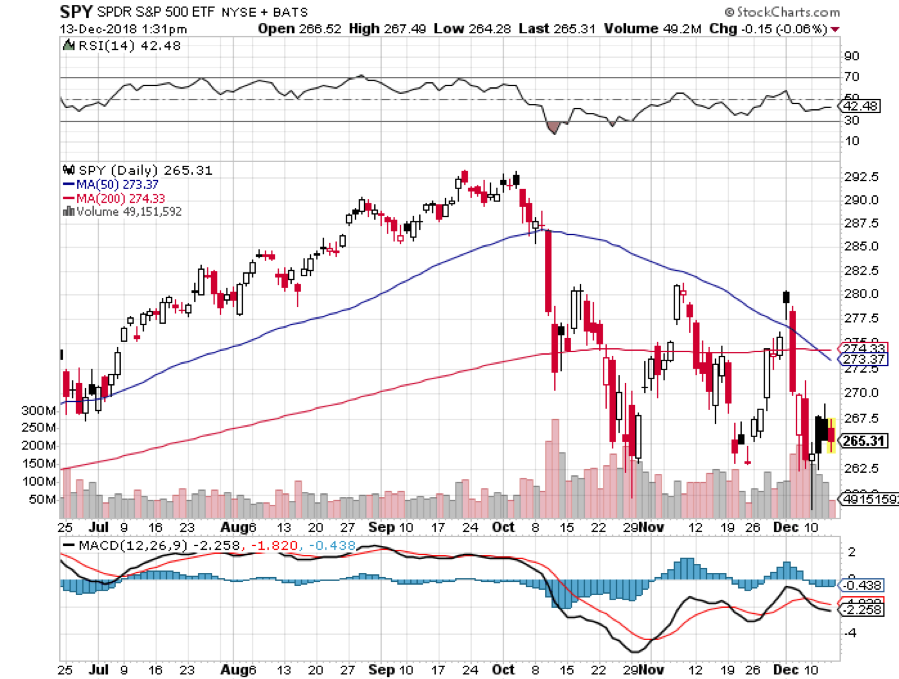

Q: Is the bottom in on the S&P 500 (SPX) or are we going to go on another retest?

A: It’s stuck right in the 2600-2800 range, and I think that’s probably where we bounce off of 2600 again. The question is whether or not we can clear the top of the range at 2800. If we can’t, I would fully expect a retest of this bottom in which case I could see it going down to 2500.

Q: You say you’ll go 100% cash by Dec 21st but also stated that the S&P 500 will go up 5% by the year's end. Should we stay in until we get the up 5% move?

A: Yes, all of our options positions expire by the 21st but if you’re just long in stocks, I would stay long, probably through the end of the year.

Q: Will the Chinese-U.S. dispute ruin the Tech industry?

A: No, I think the Trump Administration will have to do some kind of deal and call it a victory, otherwise the trade war will pull the U.S. into recession. If we go into the next presidential election with another recession—well, no one has ever survived that. Even with the China-U.S. dispute, the U.S. is still dominant in the Tech industry and will continue to do so for decades to come.

Q: China has managed to duplicate Micron Technology’s (MU) biggest selling chip, undercutting prices—thoughts?

A: True, Micron is the lowest value added of the major chip producers, therefore their stock has gotten hit the worst of any of the chip stocks down by about 46%, but I know Micron very well and they have a whole range of chips they’re currently upgrading, moving themselves up the value change to compete with this. So, that makes it a great company to own for the long term.

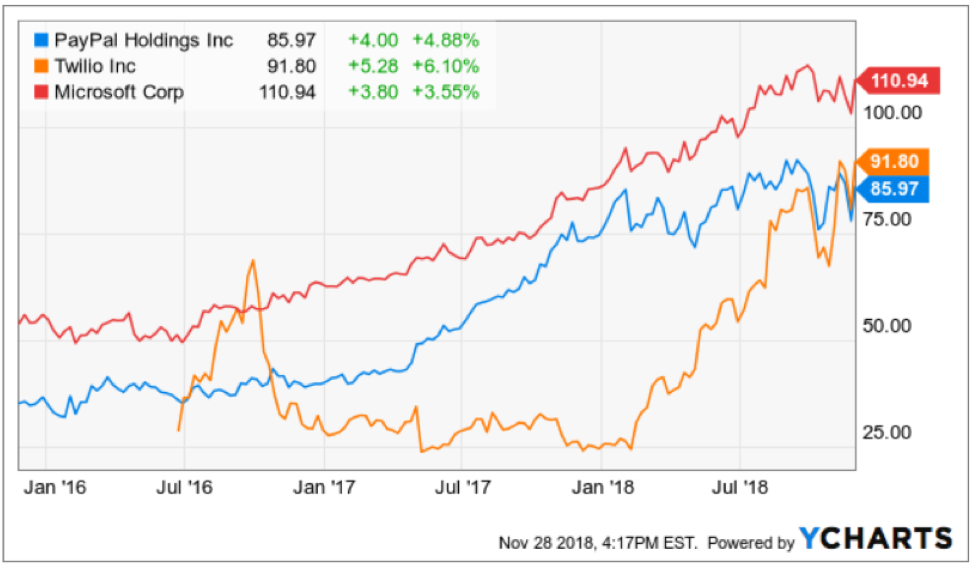

Q: I’m up 90% on my PayPal (PYPL) position—should I take a profit?

A: Yes! Absolutely! How many 90% profits have you had lately? You are hereby excused from this webinar to go execute this trade. And well-done Dr. Denis! And thank you for the offer of a free colonoscopy.

Q: What can you say about Spotify (SPOT)?

A: No, thank you—there’s lots of competition in the music streaming business. We are avoiding the entire space. The added value is not great, and many of these companies will have a short life. And with China’s Tencent growing like crazy, life for Spotify is about to become dull, mean, and brutish.

Q: What’s your view on currencies?

A: So you’re looking to make another fortune? Yes, I think the Euro (FXE) and the Yen (FXY) really are looking hard to rally, and the trigger could be dovish language in the next Fed meeting. Once the Fed slows its rate of interest rates rises, the currencies should take off like a scalded chimp.

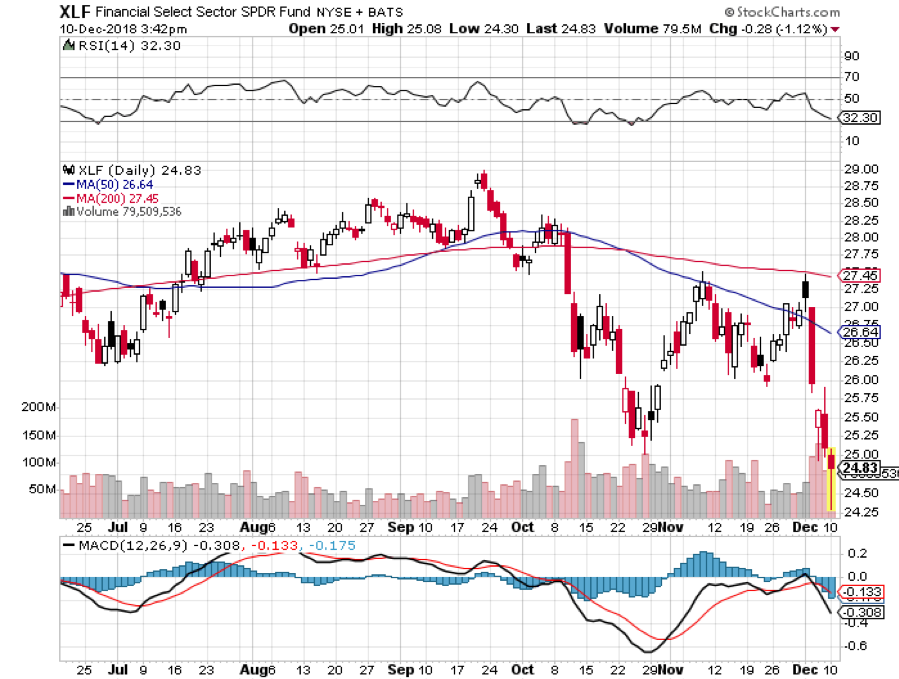

Q: Will the banks (XLF) rally in the next 6 months for a better sell?

A: Many people are waiting for a rally in the banks so they can unload them and haven’t gotten it—they’re back to pre-election price levels. The issue here is structural, and you don’t get recoveries from major structural changes in an industry. It’s significant that this is the first bull market that had no net new employment in the banks whatsoever; the business is fading away. They are the new buggy whip makers. These gigantic national branch networks will all be gone in ten years because the banks can’t afford them.

Q: Would you enter the Microsoft (MSFT) trade today?

A: I actually think I would; Microsoft only pulled back 10% when everything else was dropping 30%, 40%, or 50%. That shows you how many people are trying to get into this name so if you could take a little short-term pain (like 5%), the stock outright is probably a screaming buy here. I think it’ll go to $200 one day, so here at $110-$111 it looks like a pretty good deal. The story here is that Microsoft is rapidly taking market share from Amazon (AMZN) in the cloud business and that’s going to continue.

Q: When will you be updating your long-term model portfolio?

A: I usually do it at the end of the year, and rarely make any big changes. I’ll still be selling short bonds and still like Tesla (TSLA) and Exxon (XOM).

Q: I just joined your service. What is the best way to get started?

A: I’ll give you the same advice that I gave every starting trader at Morgan Stanley (MS). Start trading on paper only. When you are making money reliably on paper, move up to using real money, but only with one contract per position. When that is successful, slowly increase your size to 2, 3, 5, 10, and 20 contracts. Pretty soon, you will be swinging around 1,000 contracts a lot like I do. The further you move down the learning curve the greater you can increase your size and your risk. If you never get past the paper stage at least it’s not costing you any money.

I hope this helps.

Good luck and good trading.

John Thomas

CEO & Publisher The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2018-12-14 01:07:522018-12-13 17:03:09December 12 Biweekly Strategy Webinar Q&A

Gazing into the future, investors know it’s time to deploy strategies to make money in 2019.

This year has been a bizarre one for technology stocks.

The industry was overwhelmed by a relentless geopolitical circus that had more sway on tech stock’s price action than in any year that I can remember.

Technology stocks have never been more intertwined with politics.

The so-called FANGs have really been taken out behind the woodshed and beaten, and their get-out-of-jail card is no longer free to access with politicians eyeing them as take down targets.

They are no longer invincible even if they still earn bucket loads of money.

A good amount of the public animosity towards the big tech companies has been directed to socially awkward CEO of Facebook Mark Zuckerberg and his negligence towards the concept of personal data.

Facebook was once the best company in technology to work, I can tell you now that prospective applicants are scrutinizing Facebook’s actions with a gimlet eye and turning to other opportunities.

Current Facebook employees are putting in feelers out to former colleagues planning optimal exit strategies.

Remember that it’s not my job to always tell you which tech stocks are going up, but also to tell you which tech stocks are going down.

One stock poised to outperform in 2019 is international FinTech company PayPal (PYPL).

The stock has proven to be Teflon-like deflecting the pronounced volatility that has soured the tech sector in the second half of the year.

The pendulum of regulation-flipping will concoct new winners for 2019 and I believe PayPal is one of them.

PayPal is in a dominant market position with a core customer base of 254 million users and growing.

The company is so dominant that it processes almost 30% of all global payments excluding China where foreign companies are barred from operating in the FinTech space.

The quality of the product is demonstrated by a recent note from research firm Nielsen offering data showing that on average, PayPal customers complete transactions 88.7% of the time.

This astoundingly high number for PayPal checkout conversion is about 60% better than “other digital wallets” and 82% better than “all payment types."

PayPal’s home country, United States, is still vastly unmonetized in terms of the breadth of penetration of online and e-commerce payments.

America has failed so far to adopt the amount of FinTech that Chinese consumers have rapidly embraced.

The great news is that late-stage adoption of FinTech services will offer PayPal a path to profits that bodes well for the earnings and its share price in 2019 and beyond.

Investors can expect total payment volumes (TPV) consistently nudging up in the mid-20% range.

The firm helmed by Dan Schulman is just scratching the surface on pricing power.

PayPal has changed its approach of ‘one‐size‐fits‐all’ in merchant contracts to a dynamic pricing model reflecting the value‐add of recently acquired products that are more powerful.

Jetlore, launched in 2014, is a provider of predictive artificial intelligence for retail companies able to comb through the data to help boost sales.

Hyperwallet distributes payments to those that sell online, and its purchase was centered around protecting the company's core business, enabling marketplaces to pay into PayPal accounts.

iZettle, an international mobile point-of-sale (POS) provider, is better known as the Square of Europe and has a large footprint. The relationship in PayPal has sounded alarm bells in Britain for being too dominant.

Simility, an AI-based fraud prevention specialist, round out a comprehensive list of new tools and services to PayPal’s all-star caliber lineup that can offer upgrades to businesses through a hybrid solution.

This positivity surrounding the sum of the parts will allow the company to build custom solutions for merchants of all sizes.

Augmenting a solid, stable business is a start-up inside of PayPal’s umbrella of assets with enormous growth potential called Venmo making up one of PayPal’s large future bets.

Venmo is a peer-to-peer payment app acquired by PayPal in 2013.

It is a favorite and mainstay of Millennial users who have gravitated towards this FinTech platform.

PayPal is intently focused on monetizing Venmo and the strategy is paying dividends with last quarter seeing 24% of Venmo traffic monetized which is up sequentially from 17% the quarter before.

Part of the increase in profits can be attributed to integrating Uber Eats into the platform, tacking on a charge for instant money transfers linked to bank accounts, and a Venmo debit card rolled out to the masses.

This innovation was not organic and in fact borrowed from FinTech Square, a great company led by Jack Dorsey, but the stock is incredibly volatile scaring off a certain class of investors.

Former CFO of Square Sarah Friar left her post at Square to boldly take on a CEO job at Nextdoor, a social network app, illustrating that an executive management job at Square is a golden credential able to springboard workers to a CEO job in Silicon Valley.

Shares of Square have doubled in 2018 and 2017, and the recent weakness in shares is more of a case that Square went too far over its skis than anything materially wrong with the company as well as a harsh macro climate that stung most of tech.

The price action can sometimes be breathtaking with 7% moves up and down all in a few days.

If you are searching for a slow grinder on the way up, then Microsoft (MSFT) would be a better tech play to plop your money into.

In my eyes, Microsoft is the most durable, all-terrain tech stock that will weather any type of gale-force squall in 2019.

For me, CEO of Microsoft Satya Nadella is the best CEO out there in the tech industry minus Jeff Bezos at Amazon (AMZN).

The Azure Cloud business is ferociously nipping at Amazon’s heels and Nadella has created a subscription-based monster out of legacy components left behind by failure Steve Ballmer who almost sunk Microsoft.

The stock has risen three-fold since Nadella took the reins, and I believe that Microsoft will soon surpass the trillion-dollar market capitalization level and end 2019 as the most valuable tech company.

Microsoft is indestructible because it’s a hybrid mashup of a growth company whose legacy products are also still delivering fused with a top-notch gaming division and a chance at catching the Amazon cloud.

The only company that can compare in terms of potency is Amazon.

Microsoft is not a one-trick pony like Apple, Facebook, Netflix and the way I see it, there are only two top companies in the tech landscape that will leave the last three companies I mentioned in the rear-view mirror.

Echoing Microsoft, PayPal has adopted a similar magical formula with its legacy core growing at 20% yet has growth levers with Venmo layered with targeted add-on companies that will enhance the firm’s offerings.

Moving forward, tech companies that have one or more growth drivers funded by a successful legacy base will become the ultimate tech stocks.

Playing on the same trope, Adobe (ADBE) is another company that has a software-based iron-clad legacy twinge to it and has the potential to spread its wings in 2019.

PayPal, Microsoft, and Adobe do not have the potential to double like Square or Roku next year, but they have minimal China trade war risk if things turn ugly, highly profitable with growing EPS, and are pure software companies whose CEOs put a massive emphasis on software development.

Expect this trio to melt up in 2019, and be prepared to strap on call spreads at advantageous entry points.

Another pure software service stock I love for 2019 is Twilio (TWLO) who I chronically use when I call an Uber to shuttle me around and take weekend getaways on Airbnb.

I would also lump Salesforce (CRM) into the discussion for stocks to buy in 2019 too.

Notice that all the stocks I favor next year are heavily weighted towards software and not hardware.

Hardware is going out of fashion at warp speed, the China tariffs just exacerbated this trend since most of the hardware supply chains are based in China.

Currently, the Mad Technology Letter has open positions in Microsoft and PayPal and if you are like most people online, you will probably use their service next year and more than a few times.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2018-12-13 05:16:372018-12-13 05:18:14How PayPal is Destroying Legacy Banking

Mad Hedge Fund Trader John Thomas was interviewed on a major news network a few days ago talking out the state of the global financial markets. I thought you would be interested in the Q&A that followed.

Q: Bonds (TLT) have come down a lot on sudden flight to safety bid, with the 30-year yield under 2.9%. Do you see yields going back up in the short term?

A: Absolutely, yes. This is a one-time only panic triggered by the failure of the G-20 Summit in Buenos Aires. And we got the second leg down from the arrest of the CFO of Huawei, one of China's biggest companies, so that has triggered a short-term panic. It's temporary and we're going to bounce back strong. In fact, we already have. Now is a great time to be shorting bonds and buying stocks.

Q: How bad are things at Facebook (FB)? Is the bad news priced into the stock?

A: No, all the bad things are not priced into the stock. That’s why we are telling people that Facebook is a “No touch.” Bad news seems to come out every day, it’s a black swan a day stock, you don’t want to be anywhere near it. They will get some regulation, but nobody knows what it is, or how much it will affect profitability. But when a big company has to change their business model in a hurry, you don’t want to be anywhere near it. Far easier to buy it on the way up than on the way down.

Q: Will a cut in the oil supply by OPEC stem the spiraling down price of Oil (USO)? Is there a trade here?

A: “Yes” to both questions. OPEC will probably announce some sort of price cut/production cut in the next meeting which will get prices off the floor. Everyone ramped up their production to try to beat price falls which then makes the price fall worse, which is always what happens. So, yes, I would be buying oil here. I'd be buying oil stocks here too. There is your trade.

Q: Will the markets hold the February Lows?

A: Yes.

Q: If it does not hold, how far can it fall?

A: Worst case, you may get a fall straight down sucking all the sellers. But if you flip the algorithms to the buy side then it’s off the races. Markets have a habit of doing that quite a lot this year, so I think the lows have been made and you want to be buying stocks here. The fundamentals behind the market are just too strong to get beyond what algorithms are doing, what damage algorithms can do on a day trading basis. So yeah, I don't think that we're going to new lows, these are the new lows right here.

Q: Do you see an American Recession by the end of 2019?

A: Yes, I see the bull market ending in the next 3 to 6 months and recessions starting after that. That said, there is plenty to be made on the upside in coming months and then there's a ton of money to be made on the downside after that. That’s when you want to be attending my short selling school which you also get with a subscription to my service.

Q: Will the Chinese (FXI) allow the Yuan to collapse to fuel imports AND stimulate their GDP growth rate?

A: Yes. They have largely offset all of the import duties imposed by the US by depreciating their currency by 10%. If we raise duties more, they'll just cut their currency value by the same amount, so the actual dollar landed price is unchanged. There's nothing the US can do about that. We're already playing our best cards so it’s not like we can do to retaliate if they devalue their currency more. That’s the problem you have shooting all of your arrows on the first attack.

Q: Would you rotate some growth to value-based stocks on the expectation of interest rising next year in crush and grow stocks.

A: You got it half right. I would sell the high growth stocks into the next big rally, take my profits, and then go into cash! You don't want to own defensive stocks in bear markets, you want to own cash. Defensive stocks go down in a bear market, only at a slower rate, but go down they do nonetheless. Cash is king. You can earn 3 or 4% on your cash these days. That is much better than a stock that is going down.

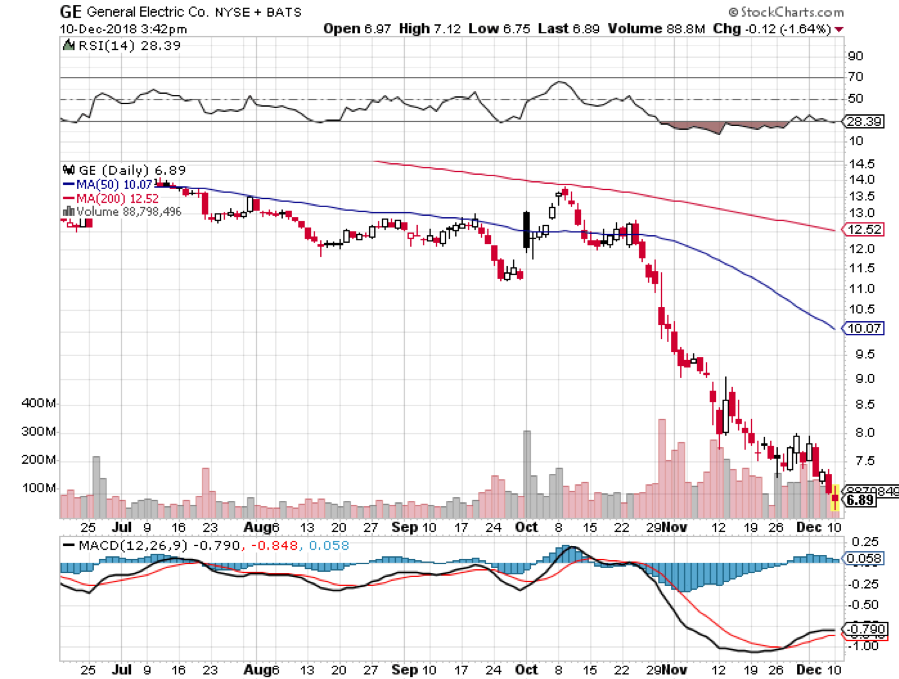

Q: I bought General Electric (GE) about a year ago at $17, and I thought it was a great deal at the time. Unfortunately, it was not, so can (GE) go any lower than it is now? I thought it would hold $10 dollars but then they cut their dividend to one cent and the shares have cratered to seven dollars. What should I do?

A: You're kind of asking me what to do after you close the barn door and the horses have already bolted. If you have (GE), I would keep it at seven dollars. The worst thing, it goes sideways from here. The best case is you get a strong rally and the stock doubles in coming months. This is not a chapter 11 situation as they have too many assets. It’s just a matter of how quickly they can turn around the company. By the way, we told people to stay away from (GE) from $31 all the way down to when it got to single digits. So, we missed that buy every dip mentality in (GE). Thank goodness for that.

Q: Why won’t banks benefit in a rising interest rate environment?

A: The answer is very simple. These are the new buggy whip makers. You don't want to own big banks as they're hobbled by these gigantic branch networks which cost a fortune, and which are all going to disappear in ten years. Fintech companies like Square (SQ) and PayPal (PYPL), these little tiny apps that you've never heard of, they're eating the banks’ businesses one by one. And by the way, even though interest rates are rising, loan volume is falling at a faster rate, so they're making a lot less money than they used to. They're not really allowed to trade markets anymore because the risk is too high. So, even if they knew how to trade markets, they can’t rely on those earnings like they used to. So, avoid the banks like the plague.

Q: Is there any scenario you see stocks rising 10% next year?

A: No. Absolutely not. We're trying to call the top of a 10-year bull market here. The total return on the market in 2019 will probably be negative and could be negative by quite a lot. Maybe by 10%, 15%, or more. So yeah, if you're hanging on for new highs, I would give up that theory and find another one. It could be a very long wait, like a five-year wait before we go back to the old highs we saw in September and before that in January.

Q: Will Geopolitics drive the market more than it did in 2018?

A: Absolutely, it will. In the geopolitics category, you can include the China trade war, the Europe trade war, the possibility that Congress does not approve the new NAFTA. There's a ton of new things that could go wrong next year. And by the way, the burden of proof is now on stocks to prove how good they are. Risk is rising in the market and volatility is rising, but there still is good money to be made for a year-end rally.

Q: Why has gold (GLD) not performed so far?

A: We don't have inflation and gold really needs to get a good ramp up in inflation to get some serious price performance. That said, I expect a return in inflation. The economic data you get lags reality by anywhere from 3 to 6 months, so you will get a rise in inflation well above 3%. That’s when you really start to move on gold, that’s why I'm saying buy the dip.

Q: Would you buy the dollar (UUP)?

A: No, I would not. It’s looking like we have a couple of interest rates rising next year. The dollar will remain strong into that but in some point next year in the whole strong dollar story disappears as the rise in interest rates stops. If the interest rates level, all of the weak dollar plays will take off like a rocket. Those would include the Euro (FXE), Yen (FXY), and emerging markets (EEM). So, watch those spaces very carefully. There are gigantic moves coming in all of those once we stop raising interest rates and once the dollar peaks out.

Q: Will we close at the lows of the year?

A: No, we will not. The lows of the year probably happened right before this interview. I expect a strong rally from here driven by algorithms. Yes, they work on the upside just as well as they do on the downside side. In fact, algorithms really don’t care which way they go just as long as they go.

Q: What securities do you cover?

A: We cover stocks, bonds, commodities, precious metals, real estate, and every trade alert has a recommendation for a stock, an ETF, and an options trade so that way you can tailor the trade alert to meet your own experience level and risk tolerance.

Q: When does the letter come out?

A: It comes out roughly at midnight EST every day before the next trading day. That way early risers can read the letter and then enter their trade alerts at the market opening. It also helps the Europeans read it as their day starts. We have a big following in Europe and an even bigger following in Australia so that is the answer to that question.

Q: Can beginners with no previous experience use your service?

A: Absolutely. Training beginners how to enter the markets for the first time is one of the primary goals of this newsletter. We have customers that range in size from $20 billion dollar hedge funds all the way down to students trading off their dorm room beds with minimal one-contract trades. So yes, it’s for everybody and every trade alert that we send out has a link to a video showing you exactly how to execute this trade on your own trading platform

Q: Are you an algorithm?

A: Well, if I made a machine noise that would help. All I can say is come to one of my global strategy luncheons. You can pinch me and if I bleed, I am real.

Q: You obviously have enough money, why do you do this?

A: Leveling the playing field for the average guy is why I do this. When I worked on Wall Street, I saw so many people get ripped off it used to make me sick. So, this is my chance to get even. Helping you learn how to make money is my way of getting even. That's why I do this.

At the beginning of the interview, I promised you a seasonal trade alert, here is one of the most popular ones, Buy Home Depot (HD) in the Summer before the hurricane season. That’s good every year for a 15% rally and that’s exactly what we got this year. A 15% rally, 2 big hurricanes, big profits, goodbye, and then see you again next year.

Q: Thank you for coming today, John. It was a real pleasure.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2018-12-11 08:02:332018-12-11 07:46:53The John Thomas TV Interview Q&A

It’s been a grueling winter for tech stocks and countless number of positive earnings reports have fell on deaf ears.

Will the bloodletting stop?

Not if Salesforce (CRM) has something to say about it!

And if you thought that tech’s secular tailwinds had vanished, this latest earnings report confirmed that software stocks are alive and are as potent as ever.

That is why I have identified software stocks as the best tech play in the current late-stage economic cycle.

At the Mad Hedge Lake Tahoe Conference, I clearly telegraphed that companies do not pour capital into capex for large and risky projects at this late stage, they search for the additional incremental dollar by arming their staff with optimal and efficient software programs to squeeze more juice out of the lemon.

Salesforce is a great example of this.

Moving forward, Salesforce is on the A-team of the software squad, and ideally positioned to harpoon any whales that come near their boat.

Companies are looking to double down on software initiatives at this point which is another reason why annual IT budgets have shot through the roof.

I have met countless CEOs who guide thousands of staff throughout branches around the world and they told me that one of the big in-house additions has been integrating Salesforce as the main customer relationship management system deleting legacy systems of yore that have pooped out.

The switch bears fruits immediately with operations supercharged like a 5-star high school football prospect on his first month of ‘roids.

Simply put, everything just works a lot better with access to this software.

What CEO wouldn’t want that?

Even more salient is that Salesforce has promoted itself as the emblematic tech growth stock promising to smash $16 billion of annual revenue by next year.

I love that Salesforce commits to ambitious sales targets and always delivers the goods.

A talking head on a prominent financial TV show went on record saying that Apple is the key to the tech narrative perpetuating, I would completely disagree with this statement.

Everyone and his mother have absorbed that Apple iPhones sales have plateaued, I am honestly sick of hearing the same story in the news over and over again.

That is why Apple has been trying to morph into a software and service stock. They are doing a great job at it by the way.

The real conclusive acid test to the tech story are these high growth software stocks because they should be the ones outperforming at this stage in the economic cycle.

If companies tilted towards software like Salesforce, Twilio (TWLO), PayPal (PYPL), Microsoft (MSFT), and Adobe (ADBE), just to name a few of the crown jewels of software stocks, start laying eggs then I would admit the tech story is dead.

But it’s not.

Salesforce is poised to continue its ascent and that basically means quarterly sales growth in the mid-20s for the foreseeable future.

There is an addressable market of $200 billion and the pipeline is rich as ever could be.

Salesforce has really turned the corner with free cash flow and profitability. It was only a few years ago they were turning in heavy losses, but this new Salesforce will be even more profitable as the network effect makes the sum of the parts and each add-on cloud-based software tool even more valuable.

Companies just love the breadth of functionality that Salesforce offers and their pension for product enhancement is really owed to CEO Marc Benioff who never shies away from calling his peers out and never cuts corners.

In fact, Marc Benioff is one of the good guys in an increasingly rotting Silicon Valley, part of this has to do with him growing up as a local lad in Burlingame, just a stone throw from his newly built palatial Salesforce Tower gracing downtown San Francisco’s picturesque skyline.

Benioff has more skin in the game as a local and publicly supported Proposition C, effectively a bill that would charge a homeless tax on big earning corporations in San Francisco.

Benioff has also promised to fund any subsequent legal attack that attempts to unravel this homeless tax putting his money where his mouth is.

Benioff noted that he has seen no softness in the macro spending environment.

And even with all the crazy headlines spinning around in the media, there has been no material impact from any supposed peak or downshift in the business environment.

Not only is Salesforce dredging up SME deals at a fast rate, they are quickly targeting the big kahunas.

The number of deals generating more than $1 million was up 46% YOY in the third quarter.

The volume of $20 million-plus relationships is also growing significantly.

In the past quarter, Salesforce renewed and expanded a 9-figure relationship with one of the largest banks in the world.

Salesforce is able to upsell their cloud tools to customers and these firms eat up the Einstein built-in functionality that uses artificial intelligence to improve the existing software.

North America comprised 71% of total revenue which is why this software company will reap the rewards for any extension of this economic cycle because they are largely domestic and best in show.

Salesforce beat and raised its outlook calming the frayed nerves of investors looking to dump software stocks.

Just look at the billings growth that was anticipated at 19%, Salesforce smashed it by 8% coming in at 27%.

Not only are they scooping up new customers, but renewals have been just as robust.

The truth is that Salesforce can’t roll out enough cloud-based software products to meet the insatiable demand.

All of this backs up my thesis that software stocks will be the outsized winners of 2019.

The FANGs are not dead, I rather hold an Amazon (AMZN) or Apple (AAPL) long term if I had the choice.

But at this stage, investors should be piling into all the crème de la crème software stocks.

Avoid them at your peril.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-29 08:01:202018-11-29 07:39:20Salesforce Knocks It Out of the Park

One of the fastest parts of technology growing at a rapid clip is fintech.

Fintech has taken the world by storm threatening the traditional banks.

Companies such as Square (SQ) and PayPal (PYPL) are great bets to outlast these dinosaurs who have a laser-like focus on technology to move the digital dollars in an efficient and low-cost way.

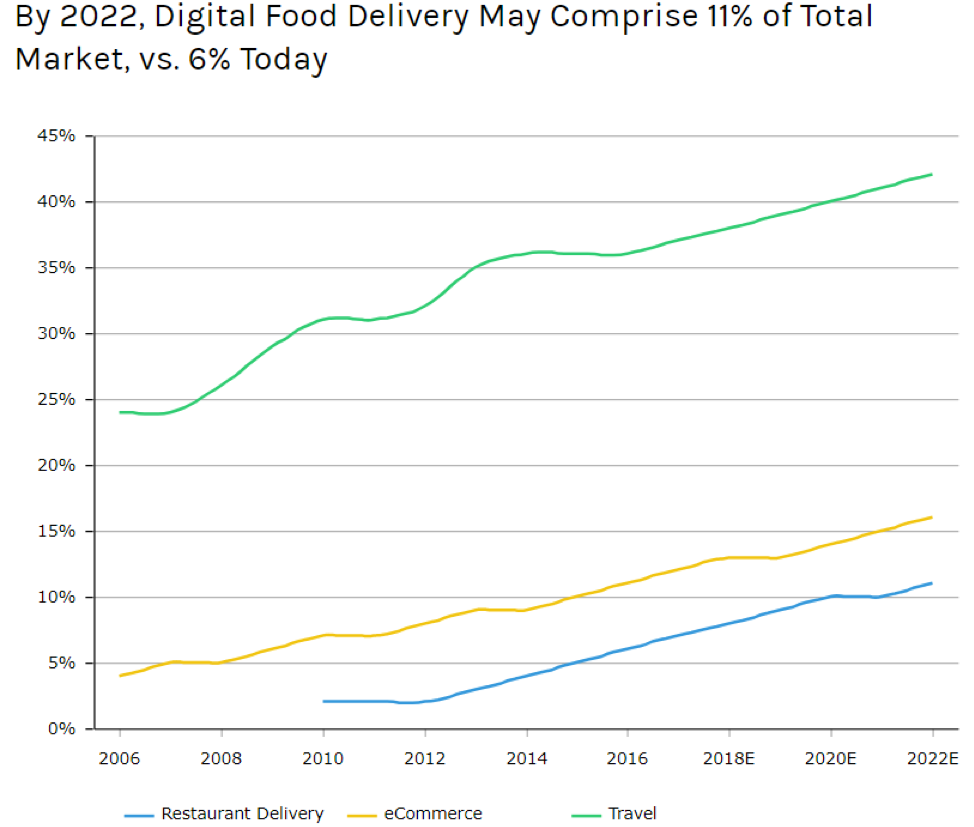

Another section of the technology movement that has caught my eye morphing by the day is the online food delivery segment that has soaring operating margins aiding Uber on their quest to go public next year.

There have been whispers that Uber could garner a $120 billion valuation dwarfing Chinese tech giant Alibaba’s (BABA) IPO which was the biggest IPO to date at $25 billion.

Uber is following in Amazon’s footsteps executing the “blitzscaling” method to suppress competition.

This strategy involves scaling up as quick as possible and seizing market share before anyone can figure out what happened.

The growth explodes at such speed that investors pile in droves throwing inefficient capital at the business leading the company to make bold bets even though profit is nowhere to be seen.

Blitzscaling has fueled American and Chinese tech to the top of the global tech charts and the trade war is mainly about these two titans jousting for first and second place in a real-time blitzscale battle of epic proportion.

The audacious stabs at new businesses usually end up fizzling out, but the ones that do have the potential to blaze a trail to profitability.

One business that has Uber giving hope of one day returning capital to shareholders is Uber Eats – the online food delivery service.

Total sales of restaurant deliveries will hit 11% of revenue if the current trend continues in 2022 marking a giant shift in consumer attitudes.

No longer are people eating out at restaurants, according to data, younger generations view ordering from an online food delivery platform as a direct substitute.

This mindset is eerily similar to Millennials attitude towards entertainment.

For many, Netflix (NFLX) is considered a better option than attending a movie theatre, and all forms of outdoor entertainment are under direct attack from these online substitutes.

One firm on the forefront of this movement has been Domino’s Pizza (DPZ).

You’d be surprised to find out that over half of the Domino’s Pizza staff are software developers.

They have focused on the customer experience doubling down on their online platform to offer the easiest way to order a pizza.

In 2012, the company was frightened to death that it still took a 25-step process to order a pizza.

By 2016, Domino’s rolled out “zero-click ordering” offering 15 different ways to order their product across many major platforms including Amazon’s Alexa.

This has all led to 60% of sales coming from online and rising.

The consistency, efficiency, and seamless online payment process has all helped Dominoes stock rise over 800% since May 2012 and that is even with this recent brutal sell-off.

Uber is perfectly positioned to take advantage of this new generation of dining in.

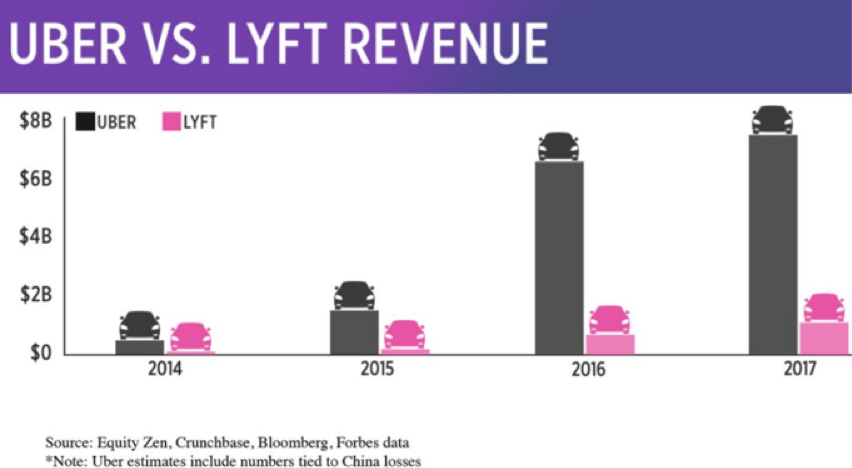

In the third quarter, Uber booked $2.1 billion of gross booking volume in their powerful online food delivery service.

The 150% YOY rise makes Uber Eats a force to be reckoned with.

Uber’s investment into e-scooters and bike transportation stems from the potential synergies of online food delivery efficiency.

It’s cheaper to deliver pizzas on a bicycle or anything without an internal combustion engine.

If you ever go to China, the electric powered three-wheel modified tuk-tuk with a storage compartment in the back instead of passenger seating is pervasive.

Often navigating around narrow alleyways is inefficient for a four-wheel automobile, and as Uber sets its sights on being the go-to last mile deliverer of food and whatnot, building out this vibrant transport network is vital to its long-term vision.

In fact, Uber is not an online ride-sharing platform, it will be something grander and its Uber elevate division could showcase Uber’s adaptability by making air transport cheap for the masses.

As soon as the robo-taxi industry gathers steam, Uber will ditch human drivers for self-driving technology saving billions in labor costs.

As it stands, Uber keeps cutting the incentive to drive for them with rates falling to as low as an average of $10 per hour now.

The golden age of being an Uber driver is long gone.

Uber is merely gathering enough data to prepare for the mass roll-out of automated cars that will shuttle passengers from point A to B.

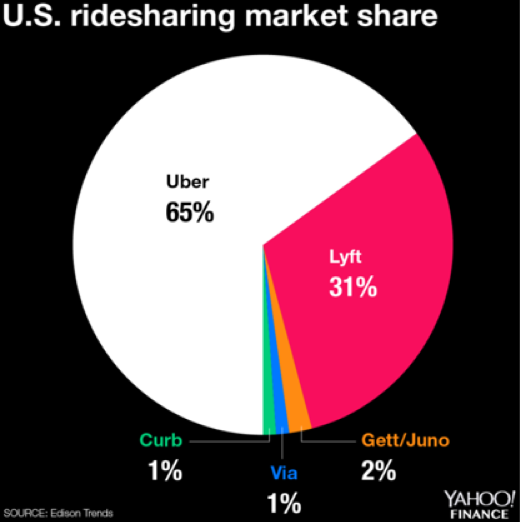

It doesn’t matter that Lyft has gained market share from Uber. Lyft’s market share was in the teens a few years ago and has rocketed to 31% taking advantage of management problems over at Uber to wriggle its way to relevancy.

It does not reveal how poor of a company Uber is, but it demonstrates that Uber’s network is spread over different industries and the sum of the parts is a lot greater than Lyft can fathom.

Lyft is a pure ride-share company and brings in annual revenue that is 4 times less than Uber.

Naturally, Uber loses a lot more money than Lyft because they have so many irons in the fire.

But even a single iron could be a unicorn in its own right.

CEO Dara Khosrowshahi recently talked about its Uber Eats division in glowing terms and emphasized that over 70% of the American population will have access to Uber Eats by the end of next year.

Uber’s position in the American economy as a pure next-generation tech business reverberates with its investors causing Khosrowshahi to brazenly admit that Uber “suffers from having too much opportunity as a company.”

Ultimately, the amped-up growth of the food delivery unit feeds back into its ride-sharing division. These types of synergies from Uber’s massive network effect is what management desires and dovetails nicely together.

In 2018 alone, 40% of Uber Eat’s customers were first-time samplers.

A good portion of these customers have never tried Uber’s ride-sharing service and when they travel for business or leisure, they later adopt the ride-sharing platform leading to more Uber converts.

Uber Freight has enabled truckers to push a button and book a load at an upfront price revolutionizing the process.

The online food delivery service is the place to be right now and it would be worth your while to look at GrubHub (GRUB).

Quarterly sales are growing over 50% and quarterly EPS growth was 61% sequentially for this industry leader.

Profit Margins are in the mid-20% convincingly proving that the food delivery industry will not be relying on razor-thin margins.

Charging diners $5 for delivery and taking a cut from the restaurateurs have been a winning strategy that will resonate further as more diners choose to munch in the cozy confines of their house.

Blitzscaling has led Uber to the online food delivery business and they are pouring resources into it to juice up profits before they go public next year.

The ride-sharing business is a loss-making enterprise as of now, and Uber will need to exhibit additional ingenuity to leverage the existing network to find strong pockets of revenue.

I believe they have the talent on their books to achieve finding these strong pockets making this company an intriguing stock to buy in 2019.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-20 06:06:032018-11-20 05:21:34A Lesson in Blitzscaling

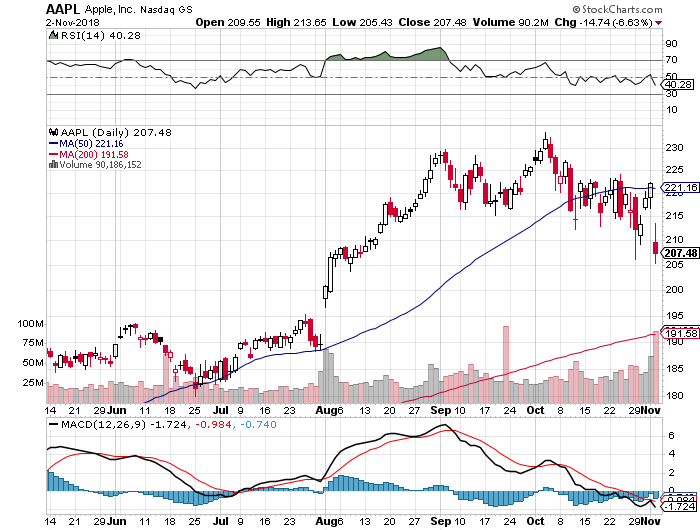

The biggest news of Apple’s earnings results was what Apple decided they will not do in the future – stop publishing iPhone unit sales.

I applaud CEO of Apple Tim Cook for putting this to rest because it is starting to get out of hand. The outbreak of criticism and grief targeted at Cook has to stop because analysts do not understand.

On one hand, it’s important to be aware of the metrics tech companies are judged on, but if analysts aren’t in tune to what these numbers mean in the bigger scheme of things, then it is irrelevant.

Apple is doing everything it can to turn into a software company. They are not interested in battling it out at the low-end of the totem pole because that path is a scrap down to zero margins.

Migrating up the value chain is something that management has identified, and this strategic shift should be met with rapturous celebrations.

Unit sales growth, gross payment value, and monthly views are all metrics that growth companies hold dear to their heart and a way to show to investors they are worth investing in regardless of the cash burn and cringeworthy operating margins.

Apple is way past that point if you haven’t noticed and should be focusing on how to monetize the existing base of customers.

Plain and simple, Apple is not a start-up growth company and taking away this reporting metric will help investors refocus on the real story at hand which is its core of software and services.

With software and services, profitability by way of innovative software offerings will be magnified and highlighted as the roadmap ahead.

As for the last batch ever of iPhone data, Apple has done a brilliant job, to say the least. They exceeded all expectations by smashing the average selling price (ASP) of iPhones at $793.

This is a monumental jump from $618 at the same time last year, a 28% YOY increase.

I did not say that Apple is the world’s best tech company at the Mad Hedge Lake Tahoe Conference, but I did say Apple is by far the highest quality company and this earnings report is a great example of that.

EPS routinely is beat and raised on a sequential basis.

Doubling down on the theme of quality is the revenue numbers from Japan which were up 34% YOY for a group of people who have the harshest view of quality control in the world.

Believe me, Japanese consumers have no desire to ever buy a Chinese smartphone.

The spike in ASPs was triggered by a flight to its collection of ultra-premium smartphones that has enthralled consumers. The ballooning ASP prices led iPhone revenue to spike 29% YOY to over $37 billion crushing the almost $30 million in quarterly revenue the prior year.

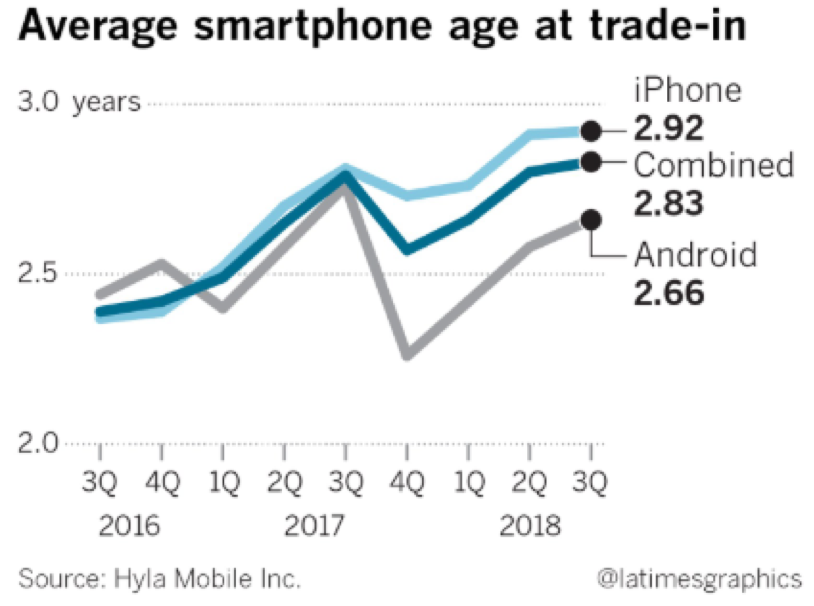

According to data from Hyla Mobile Inc., American iPhones traded in between July 1 and the end of September were 2.92 years old on average, up from 2.37 years old the same period two years earlier.

The reasons are two-fold.

Companies are producing better performing smartphones negating the need to impatiently upgrade right away.

The second reason is that they are just plain out pricey, and not everybody will have the dough to splurge on a new iPhone every year or two.

Thus, Apple has strategically placed itself in the correct manner by producing the best smartphone that customers will eventually adopt but carving out as much revenue while consumers are using their phones longer.

During this time, data usage has exploded as consumers are addicted to their smartphones and relying on a whole host of apps to complete their daily lives.

Apple would be stupid to not position themselves to capture this tectonic shift to more hourly data usage and breaking itself from the reliance of smart device revenue itself.

This is what other tech companies are doing like Roku, albeit at an earlier stage in their growth cycle.

In the future, smartphones will become obsolete replaced by something smaller, nimbler, and perhaps integrated with our brain or body or both.

Apple is also acutely aware that the bombardment of Chinese smartphones and the upward trend in the overall quality of these phones has siphoned off part of the iPhone market in specific segments of the world.

Thus, Apple has barely even touched the emerging markets of India that has been flooded by Chinese mid-tier phones without the branding power of Apple.

Apple doesn’t create these trends, they are merely stitching together smart decisions based upon them.

The next step is also a two-pronged proposition.

Apple needs a full-blown enterprise service based upon the cloud.

They can either buy one and they certainly have the cash to do so. Or they can develop one internally from scratch.

The second issue is that Apple also needs to widen its product service offerings that not only include an enterprise cloud option but also entertainment, news, sports, and everything else that could hook user’s attention and stick them to the iOS operating system until death.

Cementing users to the iOS operating system is the overall goal of all of this software infusion because if users start migrating over to the Android platform, it’s real game, set, and match for Apple as we know it.

Instead of myopic analysts focusing on “unit sales”, smart analysts should be focusing on whether what Apple is doing will tie future users to iOS or not.

I am happy with what I have seen so far but there can be a great deal of improvement going forward.

I think my 2-year-old nephew even knows that iPhone sales are maturing by now. This has not been a new story and I would call it poor reporting from a group of lazy-minded analysts.

It’s true that Apple rode the coattails of its miracle hardware products to a $1 trillion market cap. It was a magnificent achievement. I pat all who were involved on the back.

However, it’s clear as daylight that hardware is not what is going to propel Apple to a $2 trillion market cap.

Lost in all the smoke and mirrors is that revenue was up 20% YOY which is a staggering feat for a $1 trillion company.

Even more muddied in the rhetoric is that there has been minimal slowdown in China even after all the trade war jostling which is a miracle in its own right growing 16% YOY.

Software and services were up 27% YOY pulling in $10 billion and the Apple ecosystem has now reached 330 million paid subscribers, a growth of 50% YOY.

Paid subscribers are the most important metric to Apple now as it shows how many users are percolating inside their eco-system wielding their credit card around for software and services whether its maintenance spend or Apple pay.

Apple pay transaction volume tripled in the past year with four times the growth rate of FinTech player PayPal (PYPL).

Wearables still maintain broad-based growth climbing 50% YOY which is slightly down from the 60% YOY last quarter.

All of the wearables such as the amazing Apple Watch, AirPods, and Beats products have a nice supplemental effect to the Apple eco-system and is an over $10 billion business per year.

I am interested to see if Apple can make the quick pivot to an enterprise software company, and Apple’s announcement of Apple business manager, a method to deploy iOS devices at scale, had an initial sign up of 40,000 companies. Apple needs to bet the ranch on this direction and do it fast.

I would like to see Apple attack the enterprise market with zeal because there is a long runway for them to scale and the bulk of companies would welcome Apple products and services littered around their mobile offices.

The most important soundbite was by CFO of Apple Luca Maestri saying, “Given the increasing importance of our services business and in order to provide additional transparency to our financial results, we will start reporting revenue and total services beginning this December quarter.”

There you go…Apple explicitly saying they are the newest software company on the block that should go alongside the likes of Microsoft (MSFT).

The software theme will continue with the Mad Hedge Tech Letter because there are some real gems out there in the software landscape tied to the cloud.

As for Apple, the earnings report reaffirms my opinion that they just keep getting better and are magicians at adjusting to the current tech climate.

Wait for the stock to find some footing then it’s a definite buy, and for long-term holders, it’s a screaming buy.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/AAPL-chart-nov5.png606814MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-05 01:06:592018-11-02 17:11:08Get Ready for Another Bite of the Apple

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.