Global Market Comments

May 11, 2022

Fiat Lux

Featured Trade:

(JOIN ME ON CUNARD’S MS QUEEN VICTORIA

FOR MY JULY 9, 2022 SEMINAR AT SEA)

Global Market Comments

May 11, 2022

Fiat Lux

Featured Trade:

(JOIN ME ON CUNARD’S MS QUEEN VICTORIA

FOR MY JULY 9, 2022 SEMINAR AT SEA)

Global Market Comments

May 10, 2022

Fiat Lux

Featured Trade:

(MAY 4 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (ROM), (ARKK), (LMT), (RTN), (USO), (AAPL), (BRKB), (TLT), (TBT), (HYG), (AMZN)

Below please find subscribers’ Q&A for the May 4 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley.

Q: How confident are you to jump into stocks right now?

A: Not confident at all. If you look at all of my positions, they’re very deep in the money and fully hedged—I have longs offsetting my shorts—and everything I own expires in 12 days. So, I’m expecting a little rally still here—maybe 1,000 points after the Fed announcement, and then we could go back to new lows.

Q: Would you scale into ProShares Ultra Technology ETF (ROM) if you’ve been holding it for several years?

A: I would—in the $40s, the (ROM) is very tempting. On like a 5-year view, you could probably go from the $40s to $150 or $200. But don’t expect to sleep very much at night if you take this position, because this is volatile as all get out. It's not exactly clear whether we have bottomed out in tech or not, especially small tech, which the (ROM) owns a lot of.

Q: Is it time to buy the Ark Innovation ETF (ARKK) with the 5-year view?

A: Yes. I mentioned the math on that a couple of days ago in my hot tips. Out of 10 positions, you only need one to go up ten times to make the whole thing worth it, and you can write off everything else. Again, we’re looking at venture capital type math on these leverage tech plays, and that makes them very attractive; however I’m always trying to get the best possible price, so I haven’t done it yet.

Q: We’ve been hit hard with the tech trade alerts since March. Any thoughts?

A: Yes, we’re getting close to a bottom here. The short squeeze on the Chinese tech trade alerts that we had out was a one-day thing. However, when you get these ferocious short covering rallies at the bottom—we certainly got one on Monday in the S&P 500 (SPY) —it means we’re close to a bottom. So, we may go down maybe 4%-6% and test a couple more times and have 500- or 1000-point rallies right after that, which is a sign of a bottom. There’s a 50% chance the bottom was at $407 on Monday, and 50% chance we go down $27 more points to $380.

Q: Is the Roaring 20s hypothesis still on?

A: Yes absolutely; technology is still hyper-accelerating, and that is the driver of all of this. And while tech stocks may get cheap, the actual technology underlying the stocks is still increasing at an unbelievable rate. You just have to be here in Silicon Valley to see it happening.

Q: Do you like defense stocks?

A: Yes, because companies like Lockheed Martin (LMT) and Raytheon (RTN) operate on very long-term contracts that never go away—they basically have guaranteed income from the government—meeting the supply of F35 fighters for example, for 20 years. Certainly, the war in Ukraine has increased defense spending; not just the US but every country in the world that has a military. So all of a sudden, everybody is buying everything—especially the javelin missiles which are made in Florida, Georgia and Arizona. The Peace Dividend is over and all defense companies will benefit from that.

Q: Is Buffet wrong to go into energy right now? How will Berkshire Hathaway Inc. (BRK.B) perform if energy tanks?

A: Well first of all, energy is only a small part of his portfolio. Any losses in energy would be counterbalanced by big gains in his banking holdings, which are among his largest holdings, and in Apple (AAPL). Buffet does what I do, he cross-hedges positions and always has something that’s going up. I think Berkshire is still a buy. And he's not buying oil, per say; he is buying the energy producing companies which right now have record margins. Even if oil goes back down to $50 a barrel, these companies will still keep making money. However, he can wait 5 years for things to work for him and I can’t; I need them to work in 5 minutes.

Q: You must have suffered big oil (USO) losses in the past, right?

A: Actually I have not, but I have seen other people go bankrupt on faulty assumptions of what energy prices are going to do. In the 1990s Gulf War, someone made an enormous bet that oil would go up when the actual shooting started. But of course, it didn’t, it was a “buy the rumor, sell the news” situation. Energy prices collapsed and this hedge fund had a 100% loss in one day. That is what keeps me from going long energy at the top. And the other evidence that the energy companies themselves believe this is true is that they’re refusing to invest in their own businesses, they won’t expand capacity even though the government is begging them to do so.

Q: Why should we stay short the iShares 20 Plus Year Treasury Bond ETF (TLT) instead of selling out for a profit or holding on due to your statement that the TLT will go down to $105/$110?

A; If you have the December LEAPS, which most of you do, there’s still a 10% profit in that position running it seven more months. In this day and age, 7% is worth going for because there isn’t anything else to buy right now, except very aggressive, very short term, front month options, which I've been doing. So, the only reason to sell the TLT now and take a profit—even though it’s probably the biggest profit of your life—is that you found something better; and I doubt you're finding anything better to do right now than running your short Treasuries.

Q: Are you still short the TLT?

A: Yes, the front months, the Mays, expire in 8 days and I’m running them into expiration.

Q: What will Bitcoin do?

A: It will continue to bounce along a bottom, or maybe go lower as long as liquidity in the financial system is shrinking, which it is now at roughly a $90 billion/month rate. That’s not good for Bitcoin.

Q: Is now the time for Nvidia Corporation (NVDA)?

A: Yes, it’s definitely time to nibble here. It’s one of the best companies in the world that’s dropped more than 50%. I think we’d have a final bottom, and then we’re entering a new long term bull market where we’d go into 1-2 year LEAPS.

Q: What do you think of buying the iShares iBoxx $ High Yield Corporate Bond ETF (HYG) junk bond fund here for 6% dividend?

A: If you’re happy with that, I would go for it. But I think junk is going to have a higher dividend yet still. This thing had a dividend in the teens during the financial crisis; I don’t think we’ll get to the teens this time because we don’t have a financial crisis, but 7% or 8% are definitely doable. And then you want to look at the 2x long junk bond special ETFs, because you’re going to get a 16% return on a very boring junk bond fund to own.

Q: What do you think about Amazon (AMZN) at this level?

A: I think it’s too early and it goes lower. Not a good stock to own during recession worries. At some point it’ll be a good buy, but not yet.

Q: Energy is the best sector this year—how long can it keep going?

A: Until we get a recession. By the way, if you want evidence that we’re not in a recession, look at $100/barrel oil. When you get real recessions, oil goes down to 420 or $30….or negative $37 as it did in 2020. There’s a lot of conflicting data out in the market these days and a lot of conflicting price reactions so you have to learn which ones to ignore.

Q: Should we stay short the (TLT)?

A: Yes, we should. I’m looking for a 3.50% yield this year that should take us down to $105.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

November 4, 2020

Fiat Lux

Featured Trade:

(WHICH JOBS ARE ON THE LINE NEXT?)

(CVX), (CRM), (ALL), (SCHW), (XOM), (RTN)

For every job created by Amazon during the pandemic, there are 10 jobs losses in the brick and mortar retail sector.

That is happening as we speak.

The next phase of job losses will move up the value chain and hit those precious $100,000 per year jobs precisely because the advancement of technology will allow management to seamlessly substitute these highly paid workers with a digital or automated solution.

The evidence is starting to follow through.

In the last few days, ExxonMobil, Chevron (CVX), Charles Schwab, and Raytheon have announced plans to cut thousands of white-collar jobs.

Wells Fargo, Goldman Sachs, Salesforce (CRM), Allstate (ALL) and CNN owner WarnerMedia have already announced a massive wave of firings too.

Corporate America's belt-tightening provides more evidence of the fragile and unforgiving nature of this pandemic.

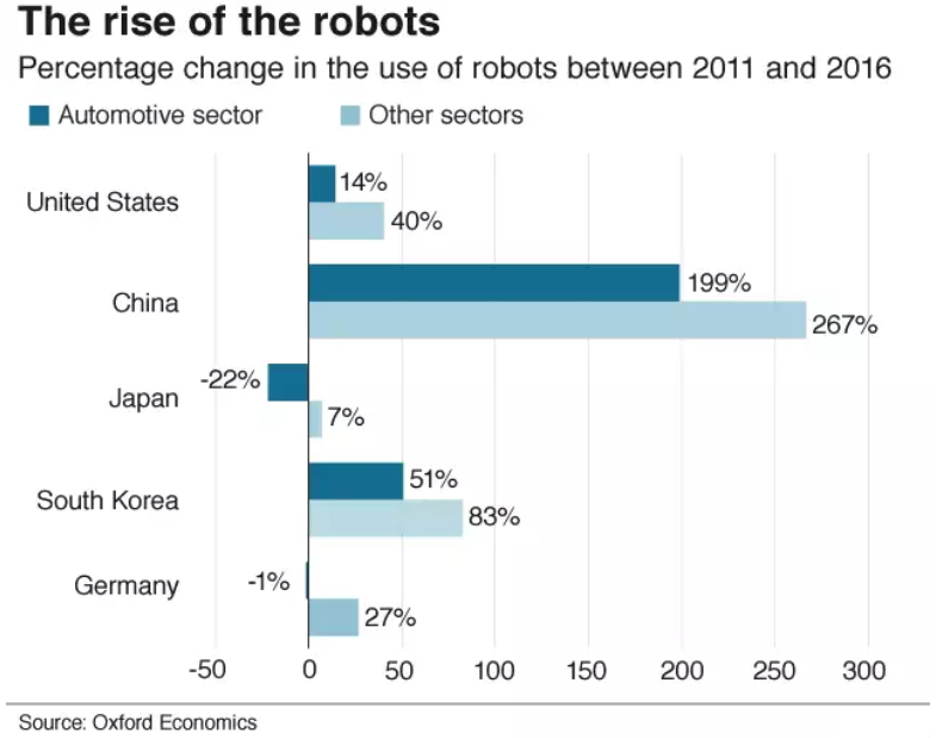

Global consultant McKinsey & Company forecasts over 800 million global workers could be replaced by robots by 2030.

The most exposed jobs on the cutting block consist of artificial intelligence (AI), a subset of automation where machines learn to use judgment and logic to complete tasks.

Stanford University doctoral candidate Michael Webb analyzed the data for 16,000 AI-related patents and more than 800 job descriptions and found that highly educated, well-paid workers will become more impacted by the spread of AI.

Bachelor’s degree holders would be exposed to AI over five times more than those with only a high school degree.

That’s because AI is especially superior at completing tasks that require planning, learning, reasoning, problem-solving, and predicting — most of which are skills required for white-collar jobs.

Other closely related jobs are in robotics and software and are likely to impact the physical and routine work of traditional blue-collar jobs.

This will sap the demand from everything from home buying and shopping to credit card defaults if a large swath of the U.S. population earns no income.

The rolling wave of white-collar layoffs is very impactful because this is the group that possesses the most purchasing power in the U.S. economy which is a consumption-driven economy.

Evidence is starting to pop up all over the board.

For instance, Charles Schwab (SCHW) said it would cut about 1,000 jobs following its takeover of TD Ameritrade.

Efficiencies, or the lack of it, have never been more magnified where companies are slashing redundant jobs upon mergers.

In the short term, white-collar workers have fared far better during the pandemic than blue-collar workers, who tend to be younger and have less education.

This is because white-collar workers have been able to operate from a home office where the bulk of blue-collar workers do not have that option.

But in the long term, technology through automation is also going to swallow up these higher-paid workers.

That is not to play down the trend of mass furloughs and layoffs in various industries, but technology and artificial intelligence will be deployed to cut high-paying jobs when it improves.

I believe that in 10 years or less, the technology will improve by leaps and bounds to the point where companies are able to install and scale it globally in an instant.

Those jobs will then go poof!

Nearly 40% of low-income workers lost their jobs in March and it is likely that the U.S. economy will never see that level of peak employment again.

Many people were rehired or found jobs elsewhere as the US economy reopened. After peaking at nearly 15% this spring, the unemployment rate has descended steadily, falling to 7.9% in September.

The mounting signs of white-collar job cuts cannot be ignored.

In another example, Allstate announced in late September that it would lay off 3,800 employees.

The insurance giant blamed the job cuts on the lack of driving during the pandemic and the refunds given to customers.

The pandemic resulted in fewer accidents, thus needing fewer claims people.

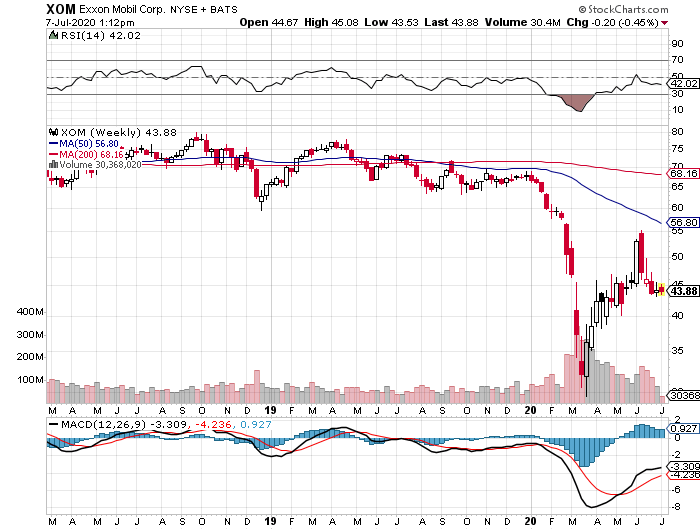

ExxonMobil (XOM) announced it will cut 1,900 jobs in the United States, mostly at its headquarters in Houston.

A broader reorganization by Exxon will slash 14,000 jobs by the end of 2022.

Energy companies have been disproportionately impacted because the demand shock has halved oil revenues.

This list goes on and on as Raytheon (RTN) disclosed it will lay off 4,000 contractors, mostly engineers, as well as 1,000 corporate employees.

And that's on top of Raytheon previously announcing plans to lay off 15,000 employees because of the downturn in the aviation industry.

Government, local and federal, has to confront a massive loss of revenues which will affect its ability to hire and maintain government workers.

Layoffs could rise among government workers because the pandemic has set off an epic budget crunch at states and local municipalities.

Eventually, whether it's 5 or 10 years down the line, the next set of solutions will inherently lead to the A word which every employee dreads – Automation.

Going 100% remote means face to face communication has slowed down to a crawl and management is less inclined to reward employees who “put on a good face” and for the sake of their own survival have turned to employees that perform well.

There will be an ultimate race to the bottom with spiraling wages and human workers unable to justify their place when competing with machines.

This inevitably leads into the world of analytics to management part of the staff for better or worse and many companies have gone from all to nothing in an instant.

I know this is a lot of information to process, but the ones getting on board with the new normal will thrive and the ones late to implement the necessary measures will flounder.

2020 has been a strange year, and get ready for new twists and turns in the last two months.

Each ensuing year will most likely get weirder because of the heavy introduction of automation into human lives.

Global Market Comments

July 8, 2020

Fiat Lux

Featured Trade:

(TRADING THE BLUE WAVE STOCK MARKET),

(FB), (AAPL), (MSFT), (AMZN), (ADBE), (SQ), (PYPL), (CRM), (SGEN), (REGN), (ILMN) (FEYE), (PANW), (AMD), (MU), (NVDA), (TSLA), (LEN), (PHM), (KBH), (XOM), (CVX), (XOM), (RTN), (NOC), (LMT), (KOL), (X), (GE)

At this point, it is possible that the president may lose the November election.

He is 14 points behind Democratic candidate Joe Biden in the polls. The odds at the London betting polls have him losing by a similar amount. My old employer The Economist magazine in London gives him a 10% chance of winning using a mix of economic and polling data.

And this assumes the election is held today. The fact is that the president is digging himself into a deeper hole every day, taking the wrong side of every issue confronting the country today. He seems to be refighting the Civil War….and taking the Confederate side when even the State of Mississippi is taking its symbol off its flag.

So, what will the post-Trump world look like? Will taxes go through the roof? Will the market crash? Is it time to go 100% cash, change our names, and move to a country with no US extradition treaty?

I don’t think so. In fact, with stocks soaring to meteoric new highs every day, the market expects that a Biden administration will be great news for stocks, perhaps the best ever.

Taxes will certainly go up. Favorable tax treatment of the energy, real estate, and private equity funds will get axed. Carried interest will finally become history. Marginal tax rate on net income over $1 billion could get hiked to the Roosevelt levels of 80-90%.

Biden has already announced an increase in the corporate tax rate from 21% to 28%. That will cut earnings for the S&P 500 by $9 a share. But the stock market is not the economy, with S&P earnings only accounting for 10% of US GDP.

And the $9 companies lose in taxes they will make back and more from new government spending, which isn’t slowing down any time soon. Some 14,000 American bridges need to be rebuilt. The Interstate Highway System is a shambles. High-speed broadband needs to go rural. The electrification of the US needs to accelerate to accommodate the millions of electric cars headed our way.

I believe that eventually, 51 million Americans will lose their jobs as a result of the pandemic. Perhaps a third of those are never coming back because the future has been so accelerated. That will leave the broader U-6 Unemployment rate stuck in double digits for years, maybe for decades.

So, we’re going to need some kind of Roosevelt style programs like the Works Progress Administration (WPA) and the Civilian Conservation Corps (CCC) who built much of the monolithic infrastructure that we all enjoy today.

At least 300,000 educated workers could immediately be put to work in contact tracing. Millions more could be employed in national infrastructure programs. One thing is certain. A new administration won’t stop massive government spending, it will simply redirect it.

And let's face it. A Biden win would bring a big expansion of Obamacare. With the best healthcare technology in the world, private industry has done the world’s worst job controlling the pandemic.

Countries with well-run national healthcare systems like Australia, New Zealand, Japan, and Singapore have almost wiped out the disease. This is why I am avoiding the healthcare sector for the foreseeable future.

Who are the big winners of all this? Big tech (FB), (AAPL), (MSFT), (AMZN), medium tech (ADBE), fintech (SQ), (PYPL), the cloud (CRM), and biotech (SGEN), (REGN), and (ILMN).

Cybersecurity will always be in demand (FEYE), (PANW). The global chip shortage will continue to worsen (AMD), (MU), (NVDA).

And Tesla (TSLA)? What can I say? It is already up nearly 100-fold from my initial $16.50 recommendation in 2010, and I’ve bought three Tesla’s (two S’s and an X).

Followers of the Mad Hedge Trade Alert service know that I am already long these names up the wazoo, and is why I am up 26% in 2020. It’s simply a matter of all pre-pandemic trends hyper-accelerating, which we were already tapped into.

If you have to add a purely domestic sector, a gigantic Millennial tailwind will keep homebuilders bubbling for years like (LEN), (PHM), and (KBH).

And while you won’t find me as a player here, retail will recover. The sector has not prospered during the current administration, thanks to a trade war with China and the pandemic.

And the losers? There is a classification of “Trump” stocks you don’t want to be anywhere near. Energy will do terribly (XOM), (CVX), (XOM), with Texas tea possibly revisiting negative numbers. If you take away the tax breaks, energy hasn’t really made money in decades.

Defense stocks (RTN), (NOC), (LMT) will take a big hit from budget cutbacks and fewer wars. Coal (KOL) will finally get shut down for good, probably sold to China in bankruptcy proceedings. Industrials will continue to lag (X), (GE), with no more free handouts from the government and no technology advantage.

So if Biden wins, you don’t need to slit your wrists, hang yourself from the showerhead, or cease investing completely. Just take your stock market winnings and go out and get drunk instead.

Global Market Comments

January 10, 2020

Fiat Lux

Featured Trade:

(FRIDAY, FEBRUARY 7 PERTH, AUSTRALIA STRATEGY LUNCHEON)

(JANUARY 8 BIWEEKLY STRATEGY WEBINAR Q&A),

(VIX), (VXX), (TSLA), (SIL), (SLV),

(WPM), (RTN), (NOC), (LMT), (BA), (EEM)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader January 8 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: If the market is doing so well, why is the Fed flooding the market with liquidity?

A: It’s election year, so their primary focus is to get the president reelected and do everything they can to make sure that happens. If we continue at the current rate, the Fed will have zero ability to get us out of the next recession which will make it much deeper than it would be otherwise. Doing this level of borrowing and keeping interest rates near zero with the stock market going up 30% a year is insane, and we will be severely punished for it in the future.

Q: With the Volatility Index (VIX) near a 12-month low and the Mad Hedge Market Timing Index near an all-time high, is this a good time to put on LEAPs for the (VXX)?

A: Yes, in fact, a (VXX) LEAP (Long Term Equity Participation Security, or one-year-plus option spread), is the only LEAP I would put on right now. I get asked about LEAPs every day because returns on them are so huge, but I am holding back on a trade alert on a (VXX) leap because it seems like in January they really want to run this market high and run volatility down low. On the next move to a (VIX) in the $11 handle, you want to put out a one-year LEAP with a $16 strike. And that is essentially a guarantee that you will make money sometime in the coming year on a big down move in the stock market. (VXX) LEAPs are coming, just not yet.

Q: Do you think Iran is done with their attacks against the US or will there be more?

A: The belief there will be no more attacks is to call the end of a 40-year trend. There will be more attacks, and those are going to be your long side entry points. Every geopolitical crisis for the last 10 years has been a great entry point on the long side and the next one will be no different. Just hope you are not one of the victims.

Q: What would a war with Iran mean for the US economy and should I buy defense stocks?

A: You can take the Iraq war, which cost us about $4 trillion, and multiply that by three times to $12 trillion because Iran’s economy is three times the size of Iraq and has a much more sophisticated military. The Iranians are really in a good position because they know the US has no appetite for another Iraq, Afghanistan, or Vietnam. They just want us out of their neighborhood. As far as defense stocks, those really move on very long-term investments and production for government contracts. When you get an attack like this, you get a one-day pop of 5% and then they usually give it all back. So, I wouldn't be chasing defense stocks like Lockheed Martin (LMT), Northrop Grumman (NOC), and Raytheon (RTN) at these high levels—it’s a very high-risk trade.

Q: Will Boeing (BA) take heat from the Ukrainian crash in Tehran?

A: Yes. It’s down about $5, and you might even consider running the numbers on a February call spread. This may be the last chance to get into Boeing at those low levels. The 737 MAX will fly this year, their most important product.

Q: What’s your opinion on Thai Baht?

A: This really is the home here for opinion on all asset classes, large and small. The Thai Baht will rise. It’s a weak dollar play. Money is pouring into all the emerging currencies because of the massive overborrowing that’s going on in the U.S. Countries that overborrow and print money like crazy always debase their currencies over the long term. That makes emerging markets (EEM) a great buy, which are trading at half the valuation levels of US ones.

Q: U.S. hog farmers missed the opportunity of a lifetime last year because of African Swine Flu. Any thoughts on the price of pork and commodities for 2020?

A: They should do better now that we’re at least getting relief from an escalation of the trade war. However, I gave up covering agriculture because the American farmer is just too efficient; every year they just produce more and more crops with fewer and fewer inputs—it’s a loser’s game. They occasionally get bad weather and get a big price spike, but that Is totally unpredictable. I'm staying away from ag stocks. In terms of buying soybeans or Apple, or Google, or Amazon, I’ll take the tech stocks any day over ag’s. Plus, the insiders have a big advantage in ag’s.

Q: What is the ticker symbol for the Silver ETFs?

A: The Silver metal ETF is (SLV), Silver miners is (SIL), and the Silver Royalty Trust, Wheaton Precious Metals, is (WPM).

Q: Why has volatility been so minimal even with massive geopolitical risk going up?

A: Liquidity trumps all. This month, the fed is pumping a record $160 billion into the financial system, and all that money is going into stocks, making them go up and making volatility go down. Until that changes, this trend will continue.

Q: Apple just passed $300, is the next stop $400?

A: Yes, and we could get that this year in the run up to 5G in September. By the way, my average cost on my Apple shares split adjusted is 50 cents. I bought it in the late 1990s when the company was weeks away from bankruptcy.

Q: Any thoughts on Tesla (TSLA)?

A: Yes, go out and buy the car, not the stock. Wait for some kind of pullback. We have just had a fantastic run of good news kicking the stock from $180 up to $490. I think we will make it up to $550 on this run. But you don’t want to get involved unless you’re a day trader because now the risk is very high. The next big move for Tesla is going to be the announcement of a production factory in Berlin, where they will try to take on Mercedes, BMW, VW, and Audi on their home turf. Then, they will own Europe.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 18, 2019

Fiat Lux

Featured Trade:

(OCTOBER 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPX), (C), (GM), (IWM), ($RUT), (FB),

(INTC), (AA), (BBY), (M), (RTN), (FCX), GLD)