Below please find subscribers’ Q&A for the January 6 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, NV.

Q: Any thoughts on lithium now that Tesla (TSLA) is doing so well?

A: Lithium stocks like Sociedad Qimica Y Minera (SQM) have been hot because of their Tesla connection. The added value in lithium mining is minimal. It basically depends on the amount of toxic waste you’re allowed to dump to maintain profit margins—nowhere close to added value compared to Tesla. However, in a bubble, you can't underestimate the possibility that money will pour into any sector massively at any time, and the entire electric car sector has just exploded. Many of these ETFs or SPACs have gone up 10 times, so who knows how far that will go. Long term I expect Tesla to wildly outperform any lithium play you can find for me. I’m working on a new research piece that raises my long-term target from $2,500 to $10,000, or 12.5X from here, Tesla becomes a Dow stock, and Elon Musk becomes the richest man in the world.

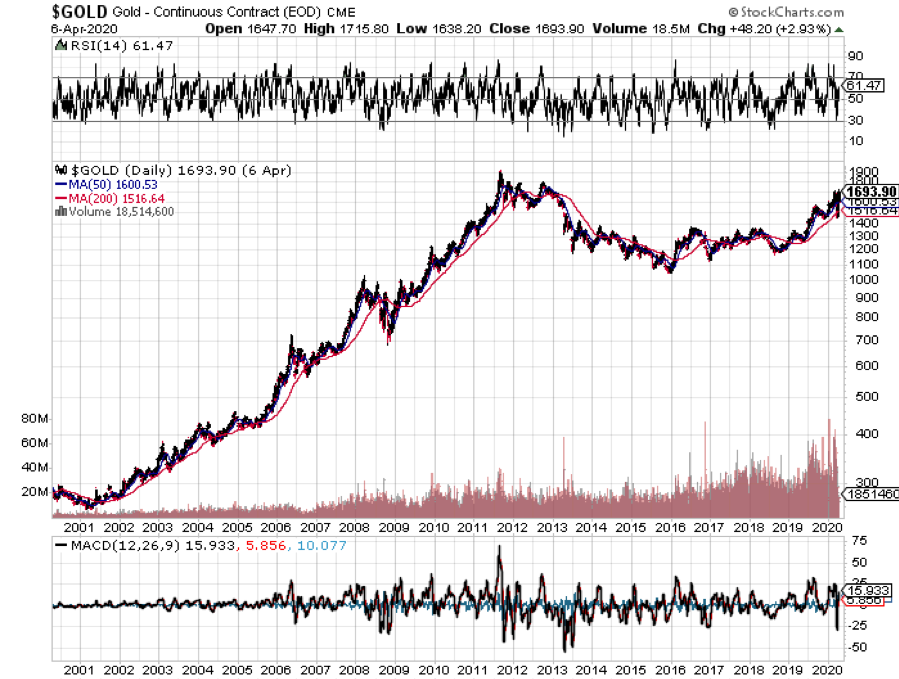

Q: Won’t rising interest rates hurt gold (GLD)? Or are inflation and a weak dollar more important?

A: You nailed it. As long as the rate rise is slow and doesn't get above 1.25% or 1.50% on the ten-year, gold will continue to rally for fears of inflation. Also, if you get Bitcoin topping out at any time, you will have huge amounts of money pour out of Bitcoin into the precious metals. We saw that happen for a day on Monday. So that is your play on precious metals. Silver (SLV) will do even better.

Q: What are your thoughts on TIPS (Treasury Inflation Protected Securities) as a hedge?

A: TIPS has been a huge disappointment over the years because the rate of rise in inflation has been so slow that the TIPS really didn’t give you much of a profit opportunity. The time to own TIPS is when you think that a very large increase in inflation is imminent. That is when TIPS really takes off like a rocket, which is probably a couple of years off.

Q: Will Freeport McMoRan (FCX) continue to do well in this environment?

A: Absolutely, yes. We are in a secular decade-long commodity bull market. Any dip you get in Freeport you should buy. The last peak in the previous cycle ten years ago was $50, so there's another potential double in (FCX). I know people have been playing the LEAPS in the calendars since it was $4 a share in March and they have made absolute fortunes in the last 9 months.

Q: Is it a good time to take out a bear put debit spread in Tesla?

A: Actually, if you go way out of the money, something like a $1,000-$900 vertical bear put spread, with the 76% implied volatility in the options market one week out, you probably will make some pretty decent money. I bet you could get $1,500 from that. However, everyone who has gone to short Tesla has had their head handed to them. So, it's a high risk, high return trade. Good thought, and I will actually run the numbers on that. However, the last time I went short on Tesla, I got slaughtered.

Q: Any thoughts on why biotech (IBB) has been so volatile lately?

A: Fears about what the Biden government will do to regulate the healthcare and biotech industry is a negative; however, we’re entering a golden age for biotech invention and innovation which is extremely positive. I bet the positives outweigh the negatives in the long term.

Q: Oil is now over $50; is it a good time to buy Exxon Mobil (XOM)?

A: Absolutely not. It was a good time to buy when it was at $30 dollars and oil was at negative $37 in the futures market. Now is when you want to start thinking about shorting (XOM) because I think any rally in energy is short term in nature. If you’re a fast trader then you probably can make money going long and then short. But most of you aren't fast traders, you’re long-term investors, and I would avoid it. By the way, it’s actually now illegal for a large part of institutional America to touch energy stocks because of the ESG investing trend, and also because it’s the next American leather. It’s the next former Dow stock that’s about to completely disappear. I believe in the all-electric grid by 2030 and oil doesn't fit anywhere in that, unless they get into the windmill business or something.

Q: With Amazon buying 11 planes, should we be going short United Parcel Service (UPS) and FedEx (FDX)?

A: Absolutely not. The market is growing so fast as a result of an unprecedented economic recovery, it will grow enough to accommodate everyone. And we have already had huge performance in (UPS); we actually caught some of this in one of our trade alerts. So again, this is also a stay-at-home stock. These stocks benefited hugely when the entire US economy essentially went home to go to work.

Q: Should we keep our stay-at-home stocks like DocuSign (DOCU), Zoom (ZM), and UPS (UPS)?

A: They are way overdue for profit-taking and we will probably see some of that; but long term, staying at home is a permanent fixture of the US economy now. Up to 30% of the people who were sent to work at home are never coming back. They like it, and companies are cutting their salaries and increasing their profits. So, stay at home is overdone for the short term, but I think they’ll keep going long term. You do have Zoom up 10 times in a year from when we recommended it, it’s up 20 times from its bottom, DocuSign is up like 600%. So way overdone, in bubble-type territory for all of these things.

Q: Are telecom stocks like Verizon (VZ) and AT&T (T) safe here?

A: Actually they are; they will benefit from any increase in infrastructure spending. They do have the 5G trend as a massive tailwind, increasing the demand for their services. They’re moving into streaming, among other things, and they had very high dividends. AT&T has a monster 7% dividend, so if that's what you’re looking for, we’re kind of at the bottom of the range on (T), so I would get involved there.

Q: Should we sell all our defense stocks with the Biden administration capping the defense budget?

A: I probably would hold them for the long term—Biden won’t be president forever—but short term the action is just going to be elsewhere, and the stocks are already reflecting that. So, Raytheon (RTX), United Technologies (UT), and Northrop Grumman (NOC), all of those, you don’t really want to play here. Yes, they do have long term government contracts providing a guaranteed income stream, but the market is looking for more immediate profits, or profit growth like you have been getting in a lot of the domestic stocks. So, I expect a long sideways move in the defense sector for years. Time to become a pacifist.

Q: Is it safe to buy hotels like Marriott (MAR), Hyatt (H), and Hilton (HLT)?

A: Yes, unlike the airlines and cruise lines, which have massive amounts of debt, the hotels from a balance sheet point of view actually have come through this pretty well. I expect a decent recovery in the shares, probably a double. Remember you’re not going to see any return of business travel until at least 2022 or 2023, and that was the bread and butter for these big premium hotel chains. They will recover, but that will take a bit longer.

Q: How about online booking companies like Expedia (EXPE) and Booking Holdings Inc, owner of booking.com, Open Table, and Priceline (BKNG)?

A: Absolutely; these are all recovery stocks and being online companies, their overhead is minimal and easily adjustable. They essentially had to shut down when global travel stopped, but they don’t have massive debts like airlines and cruise lines. I actually have a research piece in the works telling you to buy the peripheral travel stocks like Expedia (EXPE), Booking Holdings (BKNG), Live Nation (LYV), Madison Square Garden (MSGE) and, indirectly, casinos (WYNN), (MGM) and Uber (UBER).

Q: What about Regeneron (REGN) long term?

A: They really need to invent a new drug to cure a new disease, or we have to cure COVID so all the non-COVID biotech stocks can get some attention. The problem for Regeneron is that when you cure a disease, you wipe out the market for that drug. That happened to Gilead Sciences (GILD) with hepatitis and it’s happening with Regeneron now with Remdesivir as the pandemic peaks out and goes away.

Q: What about Chinese stocks (FXI)?

A: Absolutely yes; I think China will outperform the US this year, especially now that the new Biden administration will no longer incite trade wars with China. And that is of course the biggest element of the emerging markets ETF (EEM).

Q: Will manufacturing jobs ever come back to the US?

A: Yes, when American workers are happy to work for $3/hour and dump unions, which is what they’re working for in China today. Better that America focuses on high added value creation like designing operating systems—new iPhones, computers, electric cars, and services like DocuSign, Zoom—new everything, and leave all the $3/hour work to the Chinese.

Q: What about long-term LEAPS?

A: The only thing I would do long term LEAPS in today would be gold (GOLD) and silver miners (WPM). They are just coming out of a 5-month correction and are looking to go to all-time highs.

Q: What about your long-term portfolio?

A: I should be doing my long-term portfolio update in 2 weeks, which is much deserved since we have had massive changes in the US economy and market since the last one 6 months ago.

Q: Do you have any suggestions for futures?

A: I suggest you go to your online broker and they will happily tell you how to do futures for free. We don’t do futures recommendations because only about 25% of our followers are in the futures market. What they do is take my trade alerts and use them for market timing in the futures market and these are the people who get 1,000% a year returns. Every year, we get several people who deliver those types of results.

Q: Will people go back to work in the office?

A: People mostly won’t go back to the office. The ones who do go back probably won't until the end of the summer, like August/September, when more than half the US population has the Covid-19 vaccination. By the way, getting a vaccine shot will become mandatory for working in an office, as it will in order to do anything going forward, including getting on any international flights.

Q: What is the best way to short the US dollar?

A: Buy the (FXE), the (FXY), the (FXA), or the (UUP) basket.

Q: Silver LEAP set up?

A: I would do something like a $32-$35 vertical bull call spread on options expiring in 2023, or as long as possible, and that increases the chance you’ll get a profit. You should be able to get a 500% profit on that LEAP if silver keeps going up.

Q: What about agricultural commodities?

A: Ah yes, I remember orange juice futures well, from Trading Places, where I also once made a killing myself. Something about frozen iguanas falling out of trees was the tip-off. We don’t cover the ags anymore, which I did for many years. They are basically going down 90% of the time because of the increasing profitability and efficiency of US farmers. Except for the rare weather disaster or an out of the blue crop disease, the ags are a loser’s game.

Q: Can we view these slides?

A: Yes, we load these up on the website within two hours. If you need help finding it just send an email or text to our ever loyal and faithful Filomena at support@madhedgefundtrader.com and she will direct you.

Q: Do you have concerns about Democrats regulating bitcoin?

A: Yes, I would say that is definitely a risk for Bitcoin. It is still a wild west right now and there are massive amounts of theft going on. It is a controlled market, with bitcoin miners able to increase the total number of points at any time on a whim.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader