Pack your portfolios with agricultural plays like Mosaic (MOS) if Dr. Paul Ehrlich is just partially right about the impending collapse of the world’s food supply.

You might even throw in long positions in wheat (WEAT), corn (CORN), soybeans (SOYB), and rice.

It says a lot that when I update a sector report like this and half the companies have disappeared from takeovers (Potash and Agrium), you should take notice.

The never dull and often controversial Stanford biology professor told me he expects that global warming is leading to significant changes in world weather patterns that will cause droughts in some of the largest food-producing areas, causing massive famines. Food prices will skyrocket, and billions could die.

At greatest risk are the big rice-producing areas in South Asia which depend on glacial run off from the Himalayas. If the glaciers melt, this crucial supply of fresh water will disappear.

California faces a similar problem if the Sierra snowpack fails to show up in sufficient quantities as it has done in five of the last six years.

Rising sea levels displacing 500 million people in low-lying coastal areas is another big problem.

One of the 83-year-old professor’s early books The Population Bomb was required reading for me in college in the 1960s, and I used to drive up from Los Angeles to Palo Alto just to hear his lectures (followed by the obligatory side trip to the Haight-Ashbury).

Other big risks to the economy are the threat of a third world nuclear war caused by population pressures, and global insect plagues facilitated by a widespread growth of intercontinental transportation and globalization.

And I won’t get into the threat of a giant solar flare frying our electrical grid. That is already well covered on the Internet.

“Super consumption” in the US needs to be reined in where the population is growing the fastest. If the world adopts an American standard of living, we need four more Earths to supply the needed natural resources.

We must raise the price of all forms of carbon, preferably through taxes, but cap and trade will work too. Population control is the answer to all of these problems which is best achieved by giving women educations, jobs, and rights, has already worked well in Europe and Japan, and is now unfolding in Latin America.

All sobering food for thought. I think I’ll skip that Big Mac for lunch.

For many, one of the most surprising impacts of the administration’s tariffs on Chinese imports announced today has been a rocketing bond market.

Since the December $116 low, the iShares 20+ Year Treasury Bond ETF (TLT) has jumped by a staggering $16 points, the largest move up so far in years.

The tariffs are a highly regressive tax that will hit consumers hard in the pocketbook, thus reducing their purchasing power.

It will dramatically slow US economic growth. If the trade war escalates, and it almost certainly will, it could shrink US GDP by as much as 1% a year. A weaker economy means less demand for money, lower interest rates, and higher bond prices.

There is no political view here. This is just basic economics.

And while there has been a lot of hand-wringing over the prospect of China dumping its $1.1 trillion in American bond holdings, it is unlikely to take action here.

The Beijing government isn’t going to do anything to damage the value of its own investments. The only time it actually does sell US bonds is to support its own currency, the renminbi, in the foreign exchange markets.

What it CAN do is to boycott new Treasury bond purchases, which it already has been doing for the past year.

The tariffs also raise a lot of uncertainty about the future of business in the United States. Companies are definitely not going to increase capital spending if they believe a depression is coming, which the last serious trade war during the 1930s greatly exacerbated.

While stocks despise uncertainty, bonds absolutely love it.

Those of you who are short the bond market through the ProShares Ultra Short 20+ Year Treasury ETF (TBT) have a particular problem that is often ignored.

The cost of carry of this fund is now more than 5% (two times the 2.10% coupon plus management fees and expenses). Thus, long-term holders have to see interest rates rise by more than 5% a year just to break even. The (TBT) can be a great trade, but a money-losing investment.

The Chinese, which have been studying the American economic and political systems very carefully for decades, will be particularly clever in its retaliation. And you thought all those Chinese tourists were over here just to buy our Levi’s?

It will target Republican districts with a laser focus, and those in particular who supported Donald Trump. It wants to make its measures especially hurt for those who started this trade war in the first place.

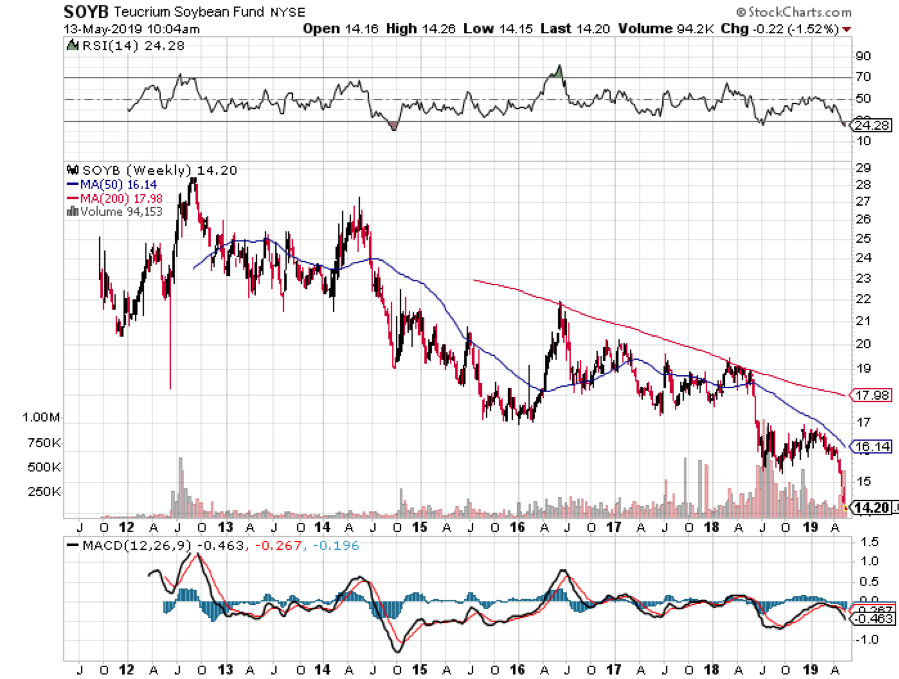

First on the chopping block: soybeans, which are almost entirely produced in red states. In 2016, the last full year for which data is available, the US sold $15 billion worth of soybeans to China. Which are the largest soybean producing states? Iowa followed by Minnesota.

A major American export is aircraft, some $131 billion in 2017, and China is overwhelmingly the largest buyer. The Middle Kingdom needs to purchase 1,000 aircraft over the next 10 years to accommodate its burgeoning middle class. It will be easy to shift some of these orders to Europe’s Airbus Industries.

This is why the shares of Boeing (BA) have been slaughtered recently, down some 13.5% from the top. While Boeing planes are assembled in Washington state, they draw on parts suppliers in all 50 states.

Guess what the biggest selling foreign car in China is? The General Motors (GM) Buick which saw more than 400,000 in sales last year. I have to tell you that it is hilarious to see my mom’s car driven up to the Great Wall of China. Where are these cars assembled? Michigan and China.

The global trading system is an intricate, finally balanced system that has taken hundreds of years to evolve. Take out one small piece, and the entire structure falls down upon your head.

This is something the administration is about to find out.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/03/China-chart-photo-2.jpg282400MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-07-05 02:02:302019-08-05 17:45:34Why US Bonds Love Chinese Tariffs

In summarizing the global financial system today, I recall the classic fifties James Dean movie, Rebel Without a Cause. Two cars are racing towards a cliff and the chicken has to bail out first. But the chicken gets his jacket sleeve stuck on a door knob, and his car dives over the cliff and crashes and burns.

Thus, here we are entranced by the world’s two largest economies in a race towards a cliff, but this time, it’s an economic one. Will rational minds prevail, or will our leaders miscalculate and plunge the world into a Great Depression? In other words, will the crashing car land on us?

That’s what happened during the 1930s when after the 1929 stock market crash lead to tit for tat tariffs that eliminated economic growth for a decade. It was only after the massive defense spending of WWII that the slump ended. This time the script is playing out exactly the same way.

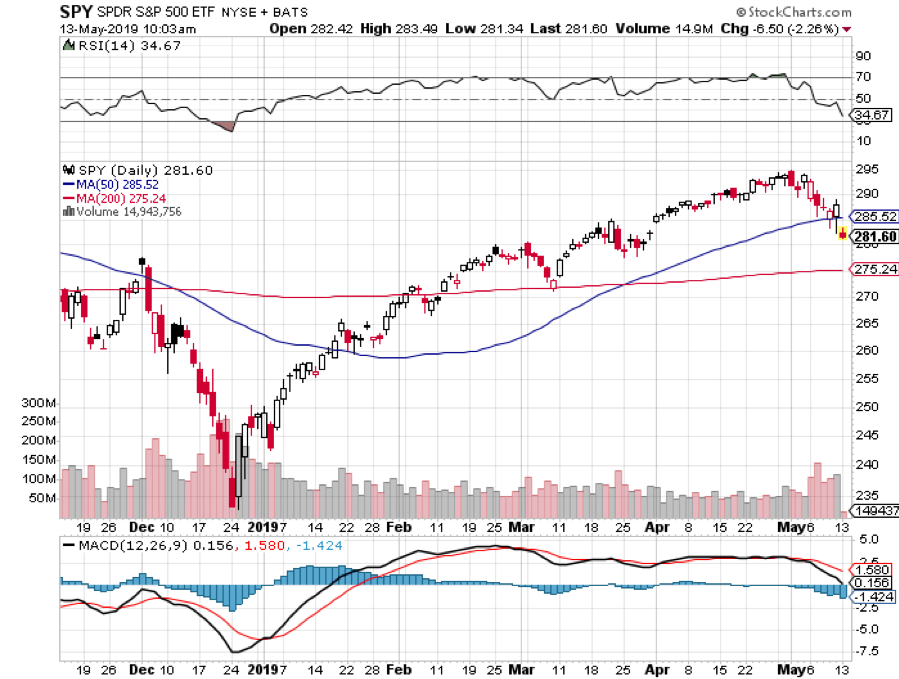

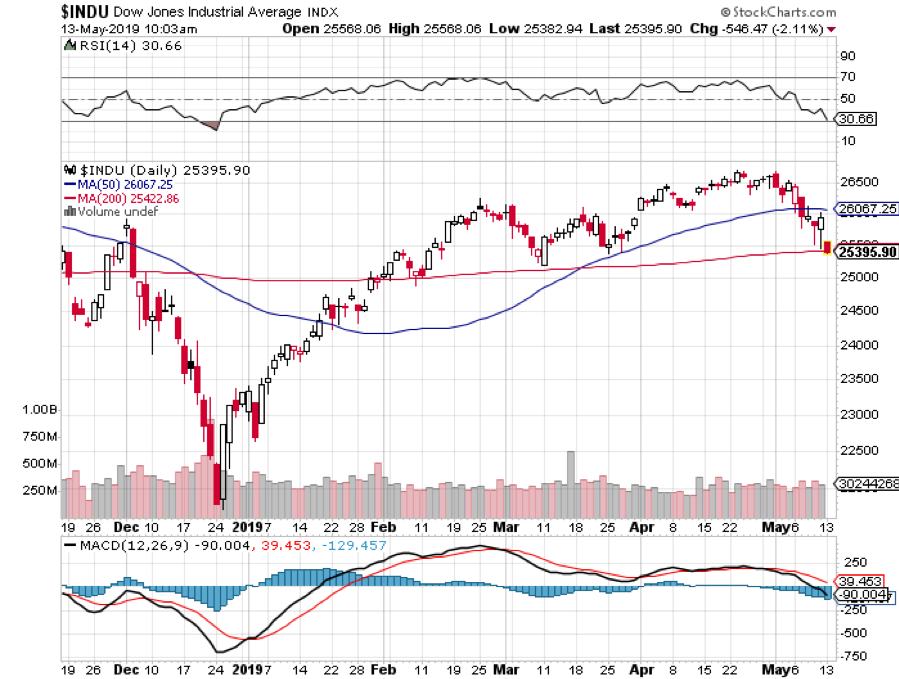

Certainly, the stock market believes in the rosier scenario. The Dow average only fell 1,278 points last week. In a real “NO DEAL” case, it would have given up the full 4,500 points it gained since December.

A prolonged trade war until the next election would take us well into a recession and back to down the 18,000 that prevailed before the last presidential election.

For the short term, the S&P 500 (SPY) is clearly gunning for the 200-day moving average at $275. That would take us down 6.78% from the recent high. I have been using soybean prices (SOYB) as an indicator of China trade negotiation success. It hit a seven-year low this morning.

It's all about trade talks all the time now and nobody has the slightest idea of what is coming next. So, I’ll sit back and wait until the Volatility Index (VIX) hits $30, or the (SPY) drops to $275 before entertaining another trade alert. Until then, I’ll maintain my 100% cash position.

I reach all these conclusions after two days of solid sleep, recovering from four days of bacchanalia at the SALT conference in Las Vegas. I'll write more about this when the market stops crashing long enough for me to write it up.

Long term followers of this letter are laughing because they recall that two years ago I predicted that the next bear market would start precisely on May 10 at 4:00 PM EST. That estimate was arrived at by an intricate calculation of the timing of a coming yield curve inversion and recession.

The S&P 500 (SPY) hit an all-time high of $295 on May 2 at 4:00 PM EST, seven trading days early. Who knew that it would be a Tweet that did it?

Uber went public last week, likely at an $82 billion valuation which sucked $10 billion out of the market. Not helping was a stock market crash and an Uber driver’s strike that spread from the US to London. After car operating expenses are taken out, drivers only net a paltry $5 an hour.

The Fed warned about high stock prices, and business borrowing is at an all-time high just two days before the market dumped. Maybe we should listen to our central bank?

US Job Openings soared in March, by a stunning 346,000 to 7.5 million. This is what tops look like.

Bonds exploded to the upside on stock market panic, as the world stampedes to “RISK OFF.” There’s a great (TLT) short sale setting up here, but not quite yet.

The US trade deficit hit a five-year low in March, down 16.2% to $20.7 billion. This is due to a big 23.7% jump in US exports to China, thanks to China’s massive economic stimulus program, not ours. But at what cost?

The Mad Hedge Fund Trader dumped its last position Monday morning and, as a result, was completely up 50 basis points on the week. You may have noticed that I have been stopping out of positions must faster than usual recently and now you know the reason why.

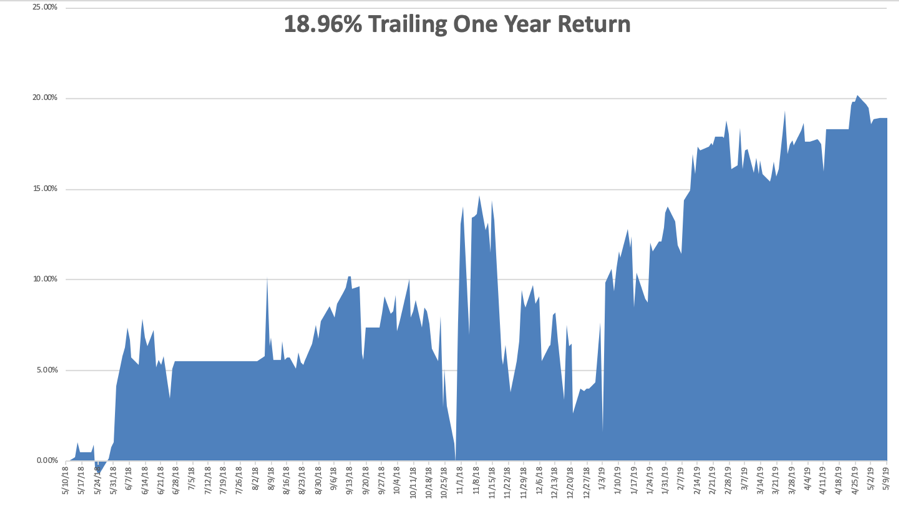

Global Trading Dispatch closed the week up 14.59% year to date and is down -1.13% so far in May. My trailing one-year retreated to +18.96%.

Mad Hedge Technology Letter gave back some ground with two new very short-term positions in Intuit (INTU) and Google (GOOG) which expire on Friday

Some 11 out of 13 Mad Hedge Technology Letter round trips have been profitable this year.

My nine and a half year profit rose slightly to +314.73%. With the markets in free fall, I am now 100% in cash with Global Trading Dispatch and 80% cash in the Mad Hedge Tech Letter. I’ll wait until the markets find their new range and then jump in on the long side.

The coming week will be pretty boring on the data front.

On Monday, May 13 at 11:00 AM, the April Survey of Consumer Sentiment is announced.

On Tuesday, May 14, 6:00 AM EST, the NFIB Small Business Index is out.

On Wednesday, May 15 at 8:30 AM, March Retail Sales are released

On Thursday, May 16 at 8:30 AM, Weekly Jobless Claims are published. March Housing Starts to come out at the same time.

On Friday, May 17 at 10:00 AM, March Consumer Sentiment is printed.

As for me, I will be flying back from Las Vegas over the weekend having attended the SALT conference and my own Mad Hedge Fund Trader strategy luncheon. The highlight of the week was listening to Woodstock veterans Credence Clearwater Revival. I’ll write more about it next week.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

You Can’t Do Enough Research

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-05-13 11:03:222019-07-09 03:44:07The Market Outlook for the Week Ahead, or a Game of Chicken

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader February 6 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Why are you so convinced bonds (TLT) are going to drop in 2019?

A: I think the Fed will regain the confidence to start raising rates again in the second half. Wage inflation is starting to appear, especially at the minimum wage level in several states. That will crater the bond market as well as the stock market, just as we saw in the second half of 2018. We’re in unknown territory in the bond market; we’re issuing astronomical WWII levels of debt and it’s only a matter of time before the Federal government crowds out private sector borrowers. Even if the bond market sidelines during this time, we will still make the maximum profit in the kind of option bear put spreads I have been putting on.

Q: Why did the Aussie (FXA) go down when they suddenly flipped from rising to cutting interest rates?

A: Interest rate differentials are the principal driver of all foreign exchange rates. They always have been and always will be. Rising rates almost always lead to a stronger currency. And with the US Fed on pause for the foreseeable future, we think the Aussie will be stronger going into 2019.

Q: Do you see the 10-year US Treasury yield going back up to 3.25% this year?

A: Yes, it’ll probably happen in the second half of the year—once the Fed gets its mojo back and decides that high employment and inflation are the bigger threats to the economy.

Q: Has NVIDIA (NVDA) bottomed here?

A: Probably, but you don’t want to touch the semiconductor chip companies until the summer. That’s when all the industry insiders expect the industry to turn and start discounting rocketing earnings after the next recession.

Q: Are stocks expensive here (SPY)?

A: On a trailing basis no, on a forward basis definitely yes. The current price/earnings multiple for the market is 17 now against a 14-20 range in 2018. So, we are dead in the middle of that range now. That’s OK when earnings are rapidly rising as they did last year. But they are falling now and at an increasingly increasing pace.

Q: Do you think the administration used the shutdown to bring forth a recession? To kickstart the pro-economic platform for reelection in 2020?

A: The administration’s view is that the economy is the strongest it’s ever been with no chance of future recession and that they will win the election as a slam dunk. If you believe that, buy stocks; if you don’t, sell them.

Q: How bad do you think Europe (IEUR) will get and does that mean the dollar (UUP) could see parity with the Euro (FXE) soon?

A: Europe is bad but they’re not going to raise interest rates anymore. However, they’re not going to cut them either because they’re already at zero. You need rising rates to see a stronger currency and the fact that the U.S. stopped raising rates is an argument for the Euro to go higher.

Q: Are we about to settle into a fading Volatility Index (VIX) environment for the rest of the year?

A: No, we are not; the (VIX) has been fading for 6 weeks. We’re approaching a bottom with the (VIX) here at $15, and the next big move in will probably be to the upside. The market has gotten WAY too complacent.

Q: Which are the most worrisome signals you see in the U.S. economy right now?

A: Weak earnings and sales guidance from all U.S. companies going forward and the immense jump in jobless claims last week as well as the ever-exploding amounts of government debt. Did I mention the trade war with China and the next government shutdown? Traders have a lot on their plate right now.

Q: How far will Lam Research (LRCX) go?

A: We’ve just had a massive 46% move up, so I wouldn’t chase it up here. However, long term there is still an easy double in this stock. They’re tied in with the semiconductor companies; NVIDIA, Advanced Micron Devices (AMD) and Micron Technology (MU) all trade in a group and may take one more run at the lows. Short term it’s overbought, long term it’s a screaming buy.

Q: Will the ag crisis feed into the main economy?

A: It could. All ag storage in the country is full, so farmers are putting the new harvest under tarps where it is rotting away and then claiming on their insurance. If you add another harvest on top of that it will be a disaster of epic proportions. China is America’s largest ag customer. It took decades of investment to develop them a client, and they are never coming back in their previous size. The trust is gone. Bankruptcies are at a ten-year high and that could eventually take down some regional banks which in turn hurt the big banks. However, ag is only 2% of the US economy, so it won’t cause the next recession. It’s really more of a story of local suffering.

Q: If you give out stop and not filled at stop price, when and how do you adjust to exit?

A: I would quickly enter it and if you’re not done quickly move it down five cents. If you don’t get done, do it again. There is no way to know where the real market is in until you put in a real order. There are 11 different option exchanges online and they are changing prices every millisecond. Furthermore, spread trades can get one leg done on one exchange and the second leg done on another, so prices can be all over the place.

Q: What data goes into the Mad Hedge Market Timing Index and how do you use it to time the markets?

A: It uses a basket of 30 different indicators which constantly changes according to what generates the highest return in a 30 year backtest. It includes a lot of conventional data points, like moving averages and RSIs, along with some of our own internal proprietary ones. When we are getting a reading below 20, we are looking to buy. Any reading over 65 and we are looking to sell, and over 80 we will only go short. It works like a charm. It paid for my new Tesla! I hope this helps.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/02/plane.png441829Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-02-08 01:06:592019-07-09 04:08:21February 6 Biweekly Strategy Webinar Q&A

Due to technical problems, I was unable to read your questions. However, I was able to get a print out after the fact.

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader January 9 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

Q: Is the bottom in for stocks?

A: It is for six months to a year. A price earnings multiple at 14X seems to be the line in the sand. The Christmas Eve massacre, which took us down to a (SPY) of $230, was the final capitulation bottom of the entire down move. We may try a few more retests of the lows on bad tweets or data points. But from here on, you’re trying to buy the dip. That’s why I cut my vacation short a week and issued eight emergency trade alerts, five for Global Trading Dispatch and three for the tech letter. By the way, I hope you appreciate those trade alerts because I had to call back staff from vacations in four different countries to get them done. But it was worth it. We’ve had the strongest start to a New Year in a decade, up 5.75%. We made back all our Q4 losses in two days!

Q: Is the strong dollar play (UUP) over? Is it time to start buying Euro (FXE) and Yen (FXE)?

A: Yes, it is. The Fed flipping from hawk to dove sounds the death knell for the dollar. With the expansion of the yield spread between the buck and other currencies stopped dead in its tracks, a massive short covering rally will drive the currencies higher. That’s why I bought the Euro on Monday for the first time in more than a year (FXE). The Japanese yen where the biggest shorts has already moved too far, up 8%. That’s where hedge fund typically finance positions because yen yields have been at zero forever.

Q: How about the Aussie (FXA)? Do we have a shot now?

A: I think so. But the bigger driver with Aussie is the trade war with China. That said, I believe that will get resolved soon too unless Trump wants to run for reelection during a recession. The Aussie also has relatively high-interest rates so it should soar.

Q: Is the government shutdown starting to hurt the economy?

A: Yes, it is. Estimates on the damage the shutdown is doing range from 0.5% to 1% a week. That means at a minimum of 20-week shut down cuts 2019 GDP growth by 1%. If your assumption for growth this year is only 2%, that brings us perilously close to a recession. However, with the big stock market rally of the past week investors clearly believe the shutdown will be over in a week. Buy “Wall” stocks.

Q: What’s the biggest risk to the market now?

A: Companies announced great earnings in October and the stocks promptly collapsed. Q4 earnings start in a few weeks, except this time, the earnings will be smaller. The big one, Apple (AAPL) is reporting on January 29 and will be especially exciting since they already announced a major disappointment. If we get a repeat, you could get another meltdown in February just like we saw last year.

Q: Do you still like gold (GLD)?

A: I did in Q4 as a hedge for a collapsing stock market. Now that stocks are on fire again, I think gold and silver (SLV) will take a rest. You’re not going to get a serious move in gold until we see higher inflation and that is a while off.

Q: Is the bear market in commodities over?

A: I think so, with a flattening interest rate picture and a weakening dollar, the entire commodity complex is looking better. That includes copper (FCX), energy (USO), and the ags (SOYB). What do you buy in an expensive market? Cheap stuff, and all of these are at seven-year lows. I think people are ready to give paper assets a rest. All we need now for these to work is inflation. My cleaning lady just asked for a raise so there’s hope.

Q: The semiconductors have just had a good move. Is it time to get in?

A: You want to buy the semis, like Micron Technology (MU), NVIDIA (NVDA), and Advanced Micro Devices (AMD) when they’ve just had a BAD move. Market conditions have improved, but not to the extent you want to buy the most volatile stocks in the market. That said, if we get another crushing move in February you might dip your toe in with some semis on capitulation day. If you want to buy semis in this environment, you might have a gambling addiction.

Q: If the Fed has stopped raising rates, are you still bearish on the (TLT) and bullish on the (TBT)?

A: I think what governor Jay Powell’s dovish comments will do is put bonds in a six-month range, say 2.45%-3.0% in yield. All of my future bond alerts will trade around those levels. In the option world, we will be setting up a short strangle, betting that interest rates don’t move out of this range for a while. In that case, our two bond positions will be OK, with the nearest money one expiring in only seven trading days.

Q: Is it too late to get into biotech (BIIB)?

A: No, along with technology, biotech will be one of the two leading sectors in the entire market for the next ten years. However, me being an eternal cheapskate, I want to get in again on a decent dip. This is the industry that will cure cancer over the next decade and that will be worth a trillion dollars in profits.

Q: You’ve kept us out of Tesla (TSLA) for a couple of years. Is it time to go back in?

A: I think I would. If production can ramp up from 7,000 to 10,000 a week, the stock should do the same. The ten-year view for this stock is that it goes from today’s $330 to $2,500. That said, this is a notorious trading stock so it is very important to buy it on a dip. Wait for the next tweet from Elon Musk.

Q: If we enter a bear market in May 2019, what would be the appropriate long-term investments at that time?

A: Nothing beats cash, especially now that you are actually getting paid something decent. You can find cash equivalents now yielding all the way up to 4%. In a bear market, stocks either go down a lot, or a whole lot, so there is nothing worth keeping. The only reason to stay in is to avoid a monster tax bill (my cost on Apple is 25 cents) or you still work for the company.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/John-Thomas-bear.png402291Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-10 01:07:202019-07-09 04:42:55January 9 Biweekly Strategy Webinar Q&A

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.