Due to technical problems, I was unable to read your questions. However, I was able to get a print out after the fact.

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader January 9 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

Q: Is the bottom in for stocks?

A: It is for six months to a year. A price earnings multiple at 14X seems to be the line in the sand. The Christmas Eve massacre, which took us down to a (SPY) of $230, was the final capitulation bottom of the entire down move. We may try a few more retests of the lows on bad tweets or data points. But from here on, you’re trying to buy the dip. That’s why I cut my vacation short a week and issued eight emergency trade alerts, five for Global Trading Dispatch and three for the tech letter. By the way, I hope you appreciate those trade alerts because I had to call back staff from vacations in four different countries to get them done. But it was worth it. We’ve had the strongest start to a New Year in a decade, up 5.75%. We made back all our Q4 losses in two days!

Q: Is the strong dollar play (UUP) over? Is it time to start buying Euro (FXE) and Yen (FXE)?

A: Yes, it is. The Fed flipping from hawk to dove sounds the death knell for the dollar. With the expansion of the yield spread between the buck and other currencies stopped dead in its tracks, a massive short covering rally will drive the currencies higher. That’s why I bought the Euro on Monday for the first time in more than a year (FXE). The Japanese yen where the biggest shorts has already moved too far, up 8%. That’s where hedge fund typically finance positions because yen yields have been at zero forever.

Q: How about the Aussie (FXA)? Do we have a shot now?

A: I think so. But the bigger driver with Aussie is the trade war with China. That said, I believe that will get resolved soon too unless Trump wants to run for reelection during a recession. The Aussie also has relatively high-interest rates so it should soar.

Q: Is the government shutdown starting to hurt the economy?

A: Yes, it is. Estimates on the damage the shutdown is doing range from 0.5% to 1% a week. That means at a minimum of 20-week shut down cuts 2019 GDP growth by 1%. If your assumption for growth this year is only 2%, that brings us perilously close to a recession. However, with the big stock market rally of the past week investors clearly believe the shutdown will be over in a week. Buy “Wall” stocks.

Q: What’s the biggest risk to the market now?

A: Companies announced great earnings in October and the stocks promptly collapsed. Q4 earnings start in a few weeks, except this time, the earnings will be smaller. The big one, Apple (AAPL) is reporting on January 29 and will be especially exciting since they already announced a major disappointment. If we get a repeat, you could get another meltdown in February just like we saw last year.

Q: Do you still like gold (GLD)?

A: I did in Q4 as a hedge for a collapsing stock market. Now that stocks are on fire again, I think gold and silver (SLV) will take a rest. You’re not going to get a serious move in gold until we see higher inflation and that is a while off.

Q: Is the bear market in commodities over?

A: I think so, with a flattening interest rate picture and a weakening dollar, the entire commodity complex is looking better. That includes copper (FCX), energy (USO), and the ags (SOYB). What do you buy in an expensive market? Cheap stuff, and all of these are at seven-year lows. I think people are ready to give paper assets a rest. All we need now for these to work is inflation. My cleaning lady just asked for a raise so there’s hope.

Q: The semiconductors have just had a good move. Is it time to get in?

A: You want to buy the semis, like Micron Technology (MU), NVIDIA (NVDA), and Advanced Micro Devices (AMD) when they’ve just had a BAD move. Market conditions have improved, but not to the extent you want to buy the most volatile stocks in the market. That said, if we get another crushing move in February you might dip your toe in with some semis on capitulation day. If you want to buy semis in this environment, you might have a gambling addiction.

Q: If the Fed has stopped raising rates, are you still bearish on the (TLT) and bullish on the (TBT)?

A: I think what governor Jay Powell’s dovish comments will do is put bonds in a six-month range, say 2.45%-3.0% in yield. All of my future bond alerts will trade around those levels. In the option world, we will be setting up a short strangle, betting that interest rates don’t move out of this range for a while. In that case, our two bond positions will be OK, with the nearest money one expiring in only seven trading days.

Q: Is it too late to get into biotech (BIIB)?

A: No, along with technology, biotech will be one of the two leading sectors in the entire market for the next ten years. However, me being an eternal cheapskate, I want to get in again on a decent dip. This is the industry that will cure cancer over the next decade and that will be worth a trillion dollars in profits.

Q: You’ve kept us out of Tesla (TSLA) for a couple of years. Is it time to go back in?

A: I think I would. If production can ramp up from 7,000 to 10,000 a week, the stock should do the same. The ten-year view for this stock is that it goes from today’s $330 to $2,500. That said, this is a notorious trading stock so it is very important to buy it on a dip. Wait for the next tweet from Elon Musk.

Q: If we enter a bear market in May 2019, what would be the appropriate long-term investments at that time?

A: Nothing beats cash, especially now that you are actually getting paid something decent. You can find cash equivalents now yielding all the way up to 4%. In a bear market, stocks either go down a lot, or a whole lot, so there is nothing worth keeping. The only reason to stay in is to avoid a monster tax bill (my cost on Apple is 25 cents) or you still work for the company.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/John-Thomas-bear.png402291Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-01-10 01:07:202019-07-09 04:42:55January 9 Biweekly Strategy Webinar Q&A

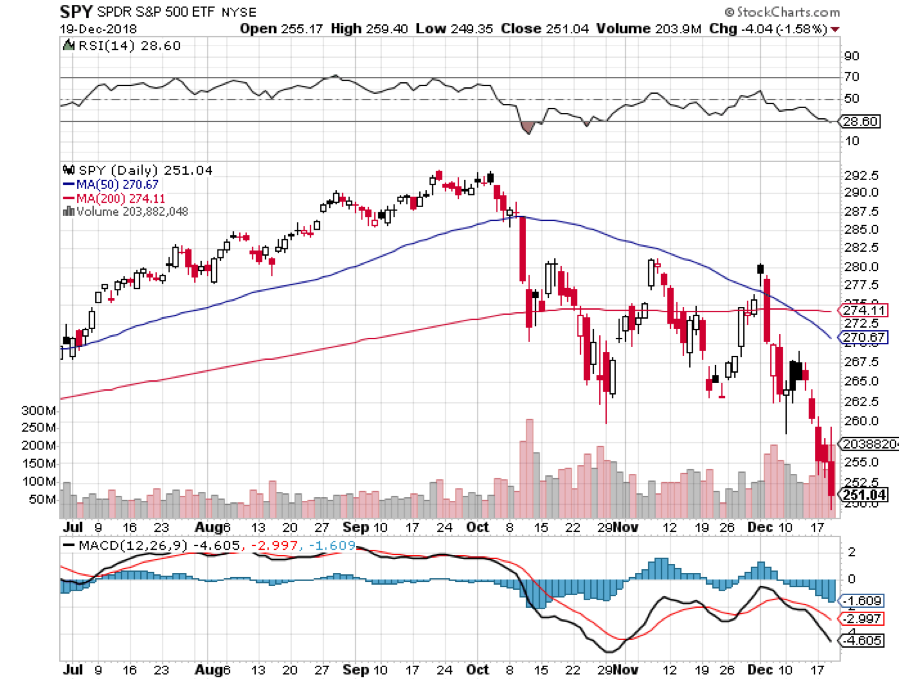

That seems to be the judgment of the markets today in the wake of the Fed’s decision to raise interest rates by 25 basis points. The overnight range for Fed funds is now 2.25%-2.50%.

The Dow Average soared by 350 points going into the decision. Then it plunged by 900 points to 23,200, a new low for 2018. It was one of the largest range days in market history.

Traders chose to focus only on the bad news and completely ignore the good. That makes this a totally “glass half empty” market.

Never mind Chairman Jerome Powell’s statement that the Fed was cutting back its 2019 forecast from three interest rate hikes to only two. Stocks should have rallied 1,000 points on just that! And they still might!

Powell also redefined the meaning of the word “neutral”, taking it down from 3.0% to 2.8%. That means only one more quarter-point hike would take us to the low end of neutral, and that might be it. That should have been worth another 1,000 points, and we still might get that as well.

The Fed affirmed that the economy is still generally strong and that unemployment is at historic lows. Nothing to worry about here.

You can see where I’m going with this.

Down 3,800 points from the October high, stocks are now approaching stupidly cheap prices and valuations. Call it insanely cheap. What we are seeing here is the coiling up of a spring that will lead to an explosive upside move.

That may happen with the quadruple witching options expiration on Friday, the last real trading day of the year. It may wait until January 2, the first trading day of 2019. But coming it is.

And let me throw a theory at you which a hedge fund friend bounced off of me yesterday while I was on one of my legendary night hikes.

What if we really have been in a bear market since January 31 and we are now approaching the end of it? That would give us a typical one-year long bear market from which we are about to blast out to the upside.

When does this new bull market begin? When the last week hands intent on avoiding another 2008 repeat bails on their holdings. In other words, it could happen any day now.

Interesting food for thought.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2018-12-20 01:07:332018-12-19 19:06:46The Glass Half Empty Market

On Friday, five serious hedge fund managers separately called me out of the blue and all had the same thing to say. They had never seen the market so negative before in the wake of the worst quarter in seven years. Therefore, it had to be a “BUY”.

I, on the other hand, am a little more cautious. I have four 10% positions left that expire on Friday, in four trading days, and on that day I am going 100% into cash. At that point, I will be up 3.5% for the month of December, up 31.34% on the year, and will have generated positive return for one of the worst quarters in market history.

I’m therefore going to call it a win and head for the High Sierras for a well-earned Christmas vacation. After that, I am going to wait for the market to tell me what to do. If it collapses, I’ll buy it. If it rockets, I’ll sell short. And I’ll tell you why.

These are not the trading conditions you would expect when the economy is humming along at a 2.8% annual rate, unemployment is running at a half-century low, and earnings are growing a 26% year on year. You can’t find a parking spot in a shopping mall anywhere.

However, the lead stocks like Apple (AAPL), Amazon (AMZN), and Netflix (NFLX) have plunged by 30%-60%. Price earnings multiples dropped by a stunning 27.5% from 20X to 14.5X in a mere ten weeks. Half of the S&P 500 (SPY) is in a bear market, although the index itself isn’t there yet. I would rather be buying markets on their way up than to try and catch a falling knife.

There is only one catalyst for that apparent yawning contradiction: The President of the United States.

Trump has created a global trade war solely on his own authority. Only he can end it. As a result, asset classes of every description are beset with uncertainty, confusion, and doubt about the future. Analysts are shaving 2019 growth forecasts as fast as they can, businesses are postponing capital spending plans, and investors are running for the sidelines in droves. Business confidence is falling like a rock

To paraphrase a saying they used to teach you in Marine Corps flight school, “It’s better to be in cash wishing you were fully invested than to be fully invested wishing you were in cash.”

The Chinese have absolutely no interest in caving into Trump’s wishes. They read the New York Times, see the midterm election result and the opinion polls, and are willing to bet that they can get a much better deal from a future president in two years.

I have been dealing personally with both Trump and the Chinese government for four decades. The Middle Kingdom measures history in Millenia. The president lives from tweet to tweet. The Chinese government can take pain by simply ordering its people to take it. We have elections every two years with immediate consequences.

The best we can hope for is that the president folds, declares victory, and then retreats from his personal war. This can happen at any time, or it may not happen at all. No one has an advantage in predicting what will happen with any certainty. Not even the president knows what he is going to do from minute to minute.

It is the possibility of trade peace at any time that has kept me out of the short side of the stock market in this severe downturn. That robs a real hedge fund manager of half his potential income. Trade peace could be worth an instant rally of 10% in the stock market. Even a lesser move, like the firing of trade advisor Peter Navarro, would accomplish the same.

The market was long overdue for a correction like the one we have just had. Investors were getting overconfident, cocky, and excessively leveraged. In October, we really needed the tide to go out to see who was swimming without a swimsuit. But if the tide goes out too far, we will all appear naked.

Thanks to some very artful trading, my year to date return recovered to +27.54% boosting my trailing one-year return back up to 27.54%. I covered an aggressive short position in the bond market (TLT) for a welcome 14.4% profit. I also took profits with an instant winner in PayPal (PYPL). On the debit side, I stopped out of an Apple call spread for a minimal loss.

December is showing a very modest loss at -0.26%. The market has become virtually untradeable now, with tweets and China rumors roiling markets for 500 points at a pop. And this is against a Dow Average that is down a miserable -2.8% so far in 2018. I should have listened to my mother when she wanted me to become a doctor.

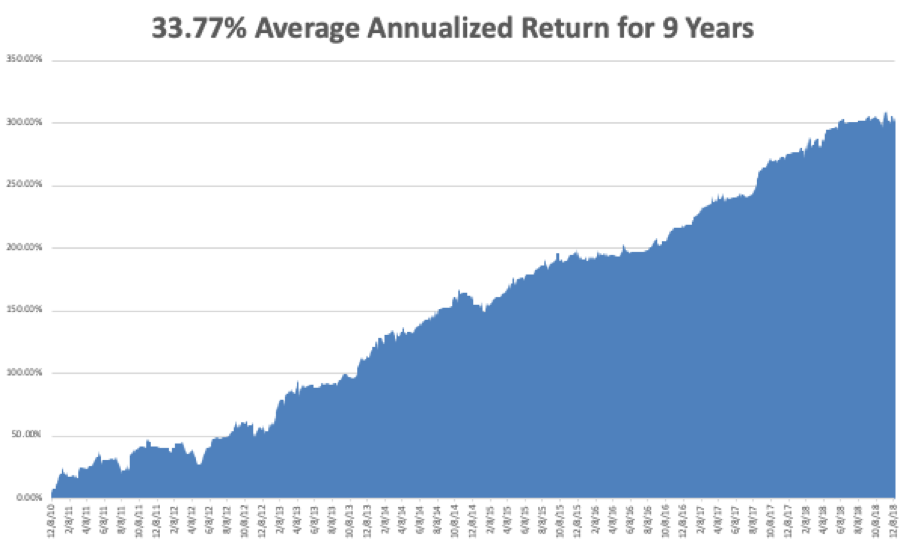

My nine-year return nudged up to +304.01. The average annualized return revived to +33.77.

The upcoming week is all about housing data, with the big focus on the Fed’s interest rate hike on Wednesday.

Monday, December 17 at 10:00 AM EST, the November Homebuilders Index is out.

On Tuesday, December 18 at 8:30 AM, November Housing Starts are published.

On Wednesday, December 19 at 10:00 AM EST, November Existing Home Sales are released.

At 10:30 AM EST the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

At 2:00 PM the Federal Reserve Open Market Committee announces a 25 basis point rise in interest rates, taking the overnight rate to 2.25% to 2.50%. An important press conference with governor Jay Powell follows.

Thursday, December 20 at 8:30 AM EST, we get Weekly Jobless Claims.

On Friday, December 21, at 8:30 AM EST, we learn the latest revision to Q3 GDP which now stands at 2.8%.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’ll be battling snow storms driving up to Lake Tahoe where I’ll be camping out for the next two weeks. Mistletoe, eggnog, and endless games of Monopoly and Scrabble await me.

Good luck and good trading!

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2018/12/Skii-Resort.png354474MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-12-17 01:06:132018-12-16 21:17:04The Market Outlook for the Week Ahead, or There’s No Santa Claus in China

The only good thing to be said about last week is that it only lasted four days. If it had been open a fifth, the Dow Average (INDU) might have fallen another 800 points.

This is the first time since 1972 that every single asset class lost money for the year, and we were in the heat of an oil shock back then.

To earn money to pay for college, I was running a handy little business buying junk heap Volkswagen Beetles in California, getting them repainted in Mexico, and then selling them for huge profits in Los Angeles. That’s me, ever the entrepreneur.

As it was, three consecutive 800-point drops are the sharpest selloff we have seen since the 1987 crash. But despite all the violence and handwringing, the market is exactly where it was nearly two months, six months, ten months, and one year ago.

Talk on the street is rife of hedge funds blowing up, fat finger trades, and algorithms run wild. This could be the first stock market correction untouched by human hands.

What we have seen is some of the most extreme volatility in history with no net movement. And you wonder why institutions are so relaxed.

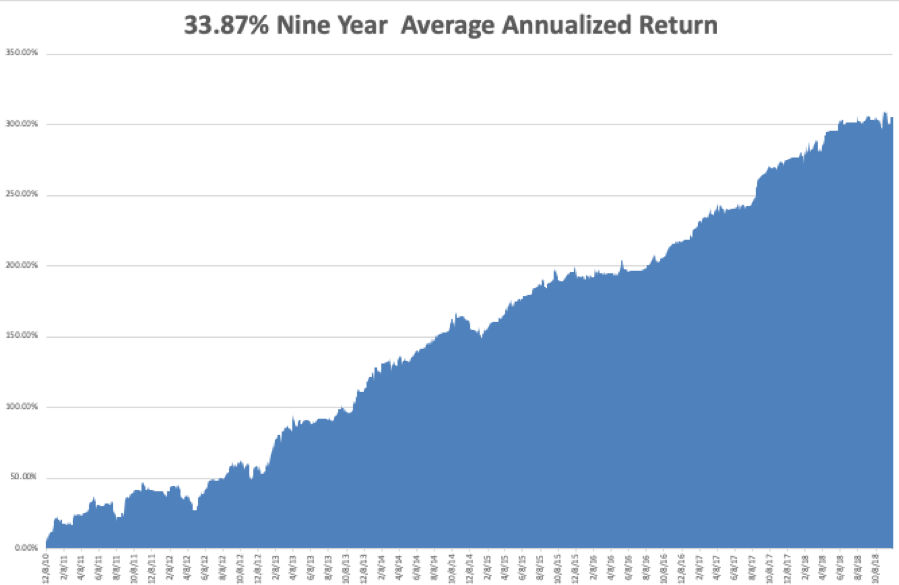

Let’s face it, we have all had it way too easy way too long. Who makes an average annualized return of 33.87% for 10 years? Oops, that’s me.

What happens next? One more dive to truly flush out the last of the nervous leveraged longs and then the long-promised Christmas rally.

Remember, markets will always do what they have to do to screw the most people, and that would be stopping traders out of their positions and then closing the year at multi-month highs.

Apple (AAPL) in particular was pummeled mercilessly, besieged by analyst downgrades almost every day. Steve Jobs’ creation is now down a stunning $65, or $27.9%. It dropped 40% when Steve died. I’m sure both Apple and Warren Buffet are in there soaking up stock every day with the shares at a half-decade earnings multiple low and laughing all the way to the bank.

But here’s the problem with that logic. Fundamentals can be very dangerous in an out-and-out panic. As my friend John Maynard Keynes used to say, “Markets can remain irrational longer than you can remain liquid.” Apple and Warren Buffet can wait out this correction, but can you, especially if you are a trader? If the stock falls further, they’ll just buy more.

The week started with such promise in the euphoria and afterglow of the G-20 Summit in Buenos Aires. It only lasted 24 hours when we discovered that nothing the administration said was true, all refuted by the Chinese when they got home to Beijing.

On Thursday, we learned that while the president’s team was negotiating, they arrested of the scion of one of China’s top tech companies while changing planes in Canada for a vacation in Mexico. It was equal to arresting the number two at Apple.

That little tidbit alone was worth a drop of 1,600 Dow points. As a result, half of all senior executive visit to the Middle Kingdom were instantly cancelled. Who wants to have “Hostage” listed on their resume?

If that were the only thing to worry about, the market would have bounced back sharply the next day and we would all be back in the Christmas mood.

But it’s not. Recession forecasts are starting to multiply like rabbits.

The Fed is growing cautious with 4 of 12 districts reporting slowing growth, said the Wednesday Beige Book report. The word “tariffs” is mentioned 39 times and is cited as a major reason for the lack of business clarity, and therefore capital investment for 2019.

The bond market is calling for a recession as “inversion” become the word of the year. The 2 year-10 years spread has shrunk to 12 basis points, an 11-year low, while the 3 year-5 year is already inverted. Massive short covering of bonds by hedge fund has ensued.

The ensuing bond melt-up was the most extreme in years as heavily short hedge funds ran for the sidelines. Now that they’re out, it’s safe to sell short again.

The November Nonfarm Payroll came in at a weak 155,000, but headline unemployment still hugs a half-century low. I saw the first really solid evidence of a recession when I drove by a high-end housing project in an upscale neighborhood and saw that it was abandoned with all equipment and tools removed. The developer obviously froze construction to get out of the way of a rapidly slowing economy.

In fact, things have gotten so bad that they may start getting good again. Instead of raising rate three times like clockwork in 2019, the Fed may adopt a “one and done” policy in December. That is where the bond market received its recent shot of adrenaline.

I doubt it as our nation’s central bank is a profoundly backward-looking organization. If the economy was hot a year ago, that means interest rates have to be raised today.

When will someone start spiking the eggnog? An awful lot of people are starting to discount a 2019 recession no matter what the administration says. If the Santa Claus rally doesn’t start this week, it will be too short to notice.

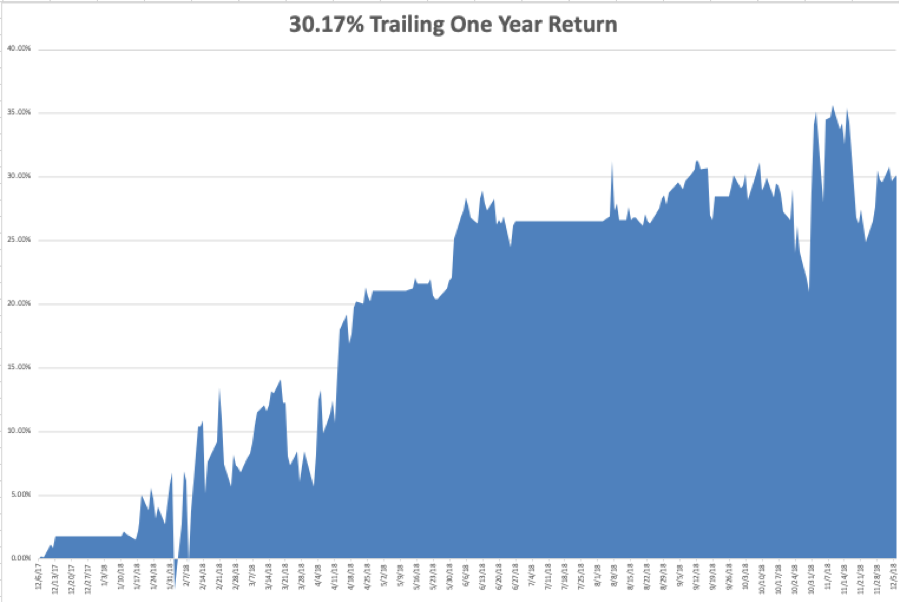

My year-to-date return recovered to +28.42%, boosting my trailing one-year return back up to 30.17%. December is showing a modest gain at +0.62%. That last leg down in the NASDAQ really hurt and was a once-in-18-year event. And this is against a Dow Average that is down a miserable -1.6% so far in 2018.

My nine-year return nudged up to +304.89. The average annualized return revived to +33.87.

The upcoming week is light on data after last week’s fireworks. The CPI is the big one, out Wednesday. Hopefully, that will give us all time to attend our holiday parties.

Monday, December 10 at 8:30 AM EST, the November Producer Price Index is out.

On Tuesday, December 11, November Producer Price Index is out.

On Wednesday, December 12 at 8:30 AM EST, the all-important November Consumer Price Index is released, the most important read we have on inflation.

At 10:30 AM EST, the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

Thursday, December 13 at 8:30 AM EST, we get the usual Weekly Jobless Claims.

On Friday, December 14, at 8:30 AM EST, we learn November Retail Sales.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I will be spending my weekend assembling the ski rack for my new Tesla model X P100D. I’ll be damned if I can get the pieces to fit together, and what is this extra bag of parts for? I hope the car is made better than this!

As for my VW trading business from 46 years ago, repair work done on US registered cars in Mexico was then subject to a 20% import duty. When the customs officer leaned against the car to ask if I had any work done recently, I fibbed. As he walked away I notice to my horror that the front of his pants was entirely covered with fresh green paint.

I never went back. Stocks looked like a better bet.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2018-12-10 03:06:262018-12-10 02:54:47The Market Outlook for the Week Ahead, or Where is Santa Claus?

Last week saw the sharpest move up in stock prices in seven years. Why doesn’t it feel like it? Maybe it’s because we are all recovering losses instead of posting new profits. The mind has a funny way of working like that.

In fact, 2018 may go down as the year that EVERYTHING went down. Stocks (SPY), bonds (TLT), commodities (COPX), precious metals (GLD), foreign currencies (FXE), emerging markets (EEM), oil (USO), real estate (IYR), vintage cars, fine art, and even my neighbor’s beanie baby collection were all posting negative numbers as of a week ago.

In fact, Deutsche Bank tracks 100 global indexes and 88 of them were posting losses on the year. The normal average in any one year is 27. This is why hedge fund are having their worst year in history (except for this one). When your longs AND your shorts plunge in unison, there is nary a dime to be had. Even gold, the ultimate flight to safety asset has failed to perform.

Theoretically, this is supposed to be impossible. When stocks go down, bonds are supposed to go up and visa versa. So are emerging markets and all other hard assets.

This only happens in one set of circumstances and that is when global liquidity is shrinking. There is just not enough free cash around to support everything. So, the price of everything goes down.

The reason most of you don’t recognize this is that last time this happened was in 1980 when most of you were still a gleam in your father’s eye.

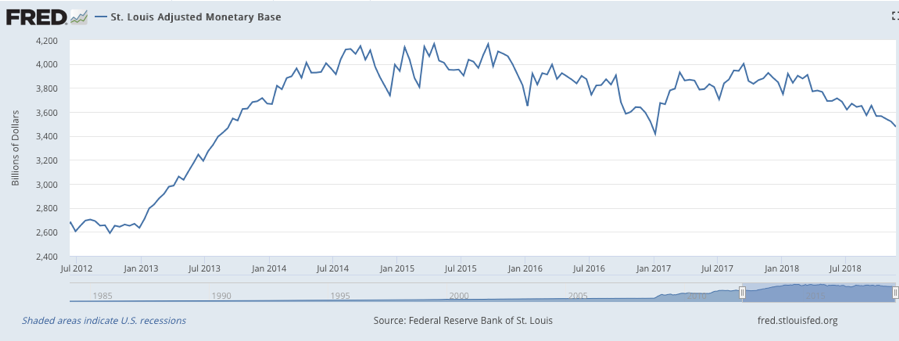

If you don’t believe me check, out the chart below from the Federal Reserve Bank of St. Louis. It shows that after peaking in July 2014, the Adjusted Monetary Base has been going nowhere and recently started to decline precipitously.

This was exactly three months before the Federal Reserve ended the aggressive, expansionary monetary policy known as quantitative easing.

The rot started in commodities and spread to precious metals, agricultural prices, bonds, and real estate. In October, it spread to global equities as well. Beanie babies were the last to go.

Want some bad news? Shrinking global liquidity, which is now accelerating, is a major reason why I have been calling for a recession and bear market in 2019 all year.

They say imitation is the sincerest form of flattery. Perhaps that is why 2019 recession calls are lately multiplying like rabbits. Nothing like closing the barn door after the horses have bolted. I wish you told me this in September.

Disturbing economic data is everywhere if only people looked. The S&P Case-Shiller Home Price Index rate of price rise hit an 18-month low at 5.5%. With housing in free fall nationally further serious price declines are to come. With mortgage rates up a full point in a year and affordability at a decade low, who’s surprised?

General Motors (GM) closed 3 plants and laid off 15,000 workers, as trade wars wreak havoc on old-line industries. It looks like Millennials would rather ride their scooters than buy new cars.

Weekly Jobless Claims soared 10,000, to 234,000, a new five-month high. Not what stock owners want to hear. THE JOBS MIRACLE IS FADING!

October New Home Sales were a complete disaster, down a stunning 8.9% and off 12% YOY. These are the worst numbers since the 2009 housing crash. I told you not to buy homebuilders! They can’t give them away now!

Oil plunged again, off 20% in November alone. Is this punishment for Saudi Arabia chopping up a journalist or is the world headed into recession?

It seems we don’t have quiet weeks anymore. Normally, sedentary Jay Powell ripped it up with a few choice words at the New York Economic Club.

By saying that we are close to a neutral rate, the Fed Governor implied that there will be one more rate rise in December and then NO MORE. Happy president. But the historical neutral range is 3.5%-4.5%, meaning there is room for 2-6 X 25 basis point rate hikes to keep the bond vigilantes at pay. Such a card! Thread that needle!

Cyber Monday sales hit a new all-time high, up to $7.3 billion, with Amazon (AMZN) taking far and away the largest share. The stock is now up $300 from its November $1,400 low.

Salesforce, a Mad Hedge favorite, announced blockbuster earnings and was rewarded with a ballistic move upwards in the shorts. Fortunately, the Mad Hedge Technology Letter was long.

The Mad Hedge Alert Service managed to pull victory from the jaws of defeat in November with a last-minute comeback. Add October and November together and we limited out losses to 0.59% for the entire crash.

This was a period when NASDAQ fell a heart-stopping 17% and lead stocks fell as much as 60%. Most investors will take that all day long. I bet you will too. Down markets is when you define the quality of a trader, not up ones, when anyone can make a buck.

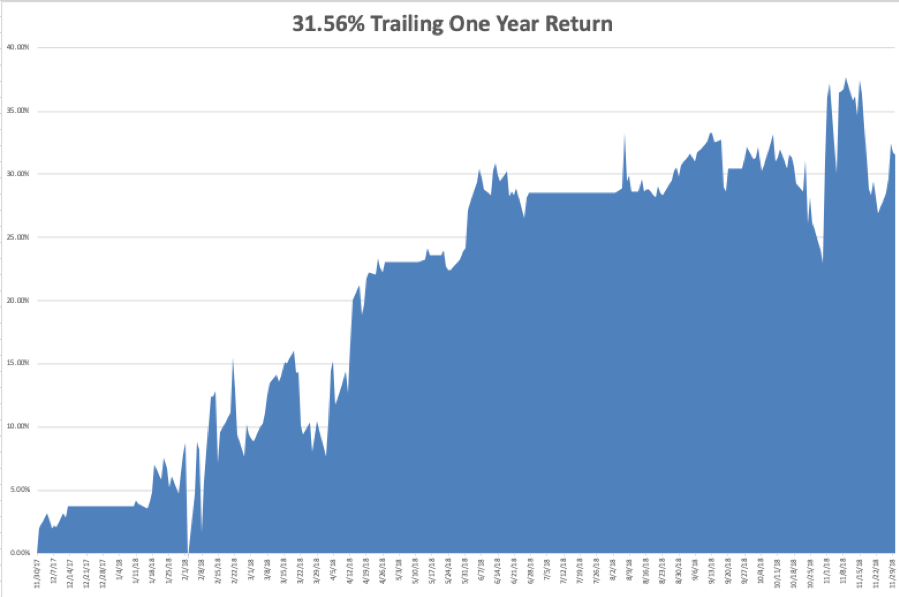

My year to date return recovered to +27.80%, boosting my trailing one-year return back up to 31.56%. November finished at a near-miraculous -1.83%. That second leg down in the NASDAQ really hurt and was a once in 18-year event. And this is against a Dow Average that is up a pitiful +2.9% so far in 2018.

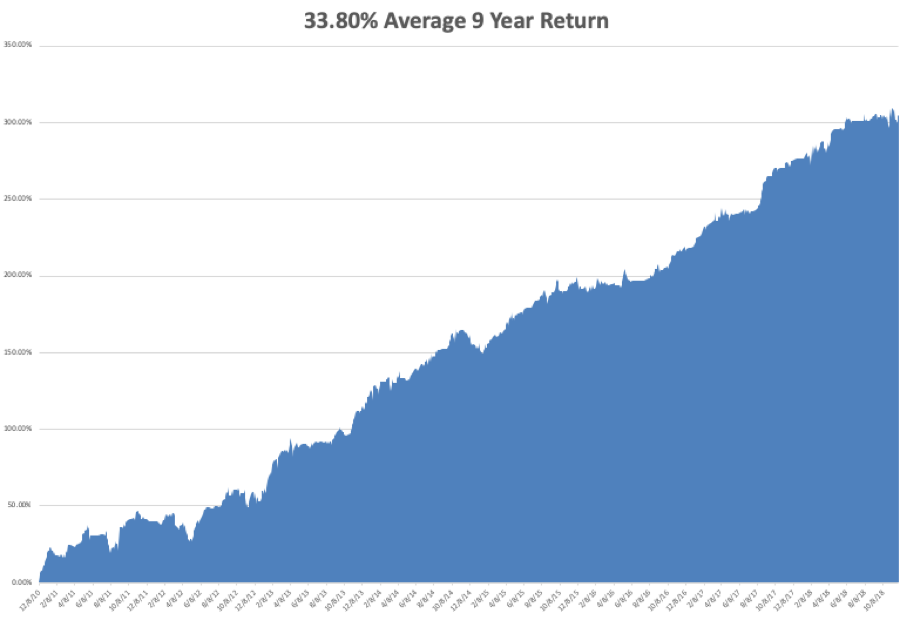

My nine-year return recovered to +304.27. The average annualized return revived to +33.80.

The upcoming week is all about jobs reports, and on Friday with the big one.

Monday, December 3 at 10:00 EST, the November ISM Manufacturing Index is published. All hell will break loose at the opening as the market discounts the outcome of the Buenos Aires G-20 Summit.

On Tuesday, December 4, November Auto Vehicle Sales are released.

On Wednesday, December 5 at 8:15 AM EST, the November ADP Private Employment Report is out.

At 10:30 AM EST the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

Thursday, December 6 at 8:30 AM EST, we get the usual Weekly Jobless Claims. At 10:00 AM we learned the November ISM Nonmanufacturing Index.

On Friday, December 7, at 8:30 AM EST, the November Nonfarm Payroll Report is printed.

The Baker-Hughes Rig Count follows at 1:00 PM. At some point, we will get an announcement from the G-20 Summit of advanced industrial nations.

As for me, I’ll be driving my brand new Tesla Model X P100D which I picked up from the factory yesterday. I’ll be zooming up and down the hills and dales of the mountains around San Francisco this weekend.

I’ll also be putting to test the “ludicrous mode” to see if it really can go from zero to 60 in 2.9 seconds and give passengers motion sickness. I will go well equipped with air sickness bags which I lifted off of my latest Virgin Atlantic flight.

Talley Ho!

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2018/12/John-Thomas-Tesla-3.png368483MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-12-03 01:06:442018-12-02 23:55:13The Market Outlook for the Week Ahead, or The Year EVERYTHING Went Down

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.