Global Market Comments

August 22, 2024

Fiat Lux

Featured Trade:

(THE TOP SEVEN CHINESE RETAILIATION TARGETS),

(AAPL), (GM), (WMT), (TGT), (BA), (SBUX), (CAT),

(AND MY PREDICTION IS….)

Global Market Comments

August 22, 2024

Fiat Lux

Featured Trade:

(THE TOP SEVEN CHINESE RETAILIATION TARGETS),

(AAPL), (GM), (WMT), (TGT), (BA), (SBUX), (CAT),

(AND MY PREDICTION IS….)

It’s looking like the trade war between the US and China is going to heat up some more, no matter who wins the presidential election. It is no longer a question of “if”, but “how much” and “when.”

Please forgive me, but I am new at this. I have only been covering China for 50 years now since the Cultural Revolution was sweeping an impoverished, starving third-world communist country.

With a massive US trade deficit with China in 2023, the Middle Kingdom has become a top administration target.

A real trade war would cause thousands of businesses in the US to go bankrupt and leave millions unemployed. Transpacific transportation would ground to a halt, filling up harbors with hundreds of redundant ships.

Trillions of dollars of direct investment in the two countries would be held hostage.

In other words, a trade war would be like cutting off our noses to spite our faces.

Just as America has its Tea Party and right-wing conspiracy theorists, so does China.

Their entire worldview revolves around the merciless exploitation of China by the Western powers that took place during the 19th century.

British trading companies, like Jardine Matheson, imported cheap opium from India and sold it to the Chinese at the point of a gun, triggering three wars. With only primitive weapons at hand, the Chinese were powerless to resist.

By the time of the fall of the Qing Dynasty in 1912, the entire country had been carved up into spheres of influence dominated by the West and Japan.

Then the Japanese invaded in 1937, and 29 million Chinese died. As recently as 1938, my Marine Corps uncle, Colonel Mitchell Paige, was charged with protecting American gunboats cruising the Yangtze River.

To us, this is all ancient history inhabiting dusty textbooks in libraries never visited. Patriotic Chinese feel like this happened yesterday.

You could dismiss all this as academic musings.

But national pride and sovereignty are really big deals in China today.

During China’s last trade war with Japan only five years ago, several Japanese facilities were burned down by angry, uncontrollable mobs, and visiting businessmen were assaulted on the street. Trade ground to a halt.

So it behooves us to analyze which companies will suffer the most from any deterioration in the US-Chinese relationship before markets figure this out. The Chinese are not interested in any “America First” policy in any way, shape, or form.

Here is my hit list:

1) Apple (AAPL) – Yes, Cupertino, CA-based Apple has a big fat bull’s-eye on its back. The company is a vast, finely tuned machine that needs everything to work perfectly to deliver hundreds of millions of iPhones around the world.

The number of things that can go wrong here can’t be counted. What if the one million workers at its Foxconn subcontractor fail to show up for work someday? What if they are not allowed to go to work? What if they burn THAT factory down?

Another problem is that Chinese growth is a key part of Apple’s long-term sales strategy. A Chinese boycott would put a huge dent in those plans.

Remember, Apple is getting it from both sides, with Trump promising a 35% import duty on all Apple products. That would certainly hurt sales.

I’m sure Apple management is on tenterhooks as to how all this will play out in the coming months.

There is no backup plan here. Apple is just too big and too sophisticated to change any part of its incredibly complex supply chain in less than a decade.

2) General Motors (GM) – Is one of the most globalized US companies of all. (GM) can’t build a car in Detroit without 40% of its parts coming from Japan, Mexico, South Korea, or dozens of other countries.

General Motors is also hugely dependent on Chinese sales. It sells more Buicks in China than it does in the US. That is one-third of GM’s total worldwide sales.

Next, the company plans to sell Chinese-made Buicks in America.

While we weren’t looking, General Motors has become a Chinese company, and many others are falling suit.

3) Wal-Mart (WMT) – Imagine walking into your local Walmart one day and finding out that all of the prices have been marked up by 35%.

This is the reason why the company is called the “Chinese Embassy.” I dare you to find anything there that is NOT made in China, except for the food and the flowers (a dozen long stem red roses are only $10!).

Like Apple, the company is so big that any change in its supply chain would take years. You can add Target (TGT) to this hit list for the same reasons.

On top of that, Wal-Mart has 432 stores operating in China. Imagine the effect that a boycott would have there.

4) Boeing (BA) - The local flight school that maintains my plane has been totally taken over by Chinese students. That is because China needs to buy $1 trillion worth of aircraft over the next 20 years, some 6,800 jetliners in all.

Boeing expects to provide the lion’s share of these. The company has already entered the planning phases for the construction of a giant new aircraft assembly plant in China.

It would be really easy for China to switch a major part of these orders over to Europe’s Airbus Industries, which has been aggressively competing to accomplish exactly that.

Boeing didn’t get the business because of the advanced technology seen in the 787 Dreamliner. Chinese were simply attempting to even out the trade balance.

5) Starbucks (STBX) – Starbucks founder Howard Schultz made no secret of his dislike for Donald Trump before the election. With 2,500 stores in China, and plans to double that figure, he had little other choice.

With relations between the US and China turning colder than the firm’s overpriced ice espresso, sales, growth plans, and share prices could take a big hit. Chinese may have to postpone their caffeine addiction until the next Democratic administration.

6) Caterpillar (CAT) – You can’t have an infrastructure boom anywhere in the world without Caterpillar, whose heavy machinery is the gold standard for large public works projects. I have been covering the company for 40 years.

7) Tesla (TSLA) – Tesla’s factory in China is the company’s biggest seller. If the Chinese expropriate or impede in any way such as through strikes, Tesla’s share price would drop by half instantly. I know the Chinese promised to play nice when Tesla made this groundbreaking, technology-transferring investment. But guess what Elon? The Chinese can change their minds.

As a result of the upcoming US round of massive deficit spending, (CAT)’s share has been one of the best performers since the presidential election.

Unfortunately, this time the company is so heavily invested in China that it has also built a large assembly plant there. China accounts for 20% of the firm’s worldwide sales.

Time for a short?

The net effect on the impairment of business at all of these companies will be lower profits, high volatility of profits, and continued uncertainty. The shares will be forced to trade at a discount.

When you are running a mammoth global business, the last thing in the world you want is unpredictability.

It will also bring a rapid rise in inflation, as prices are raised to offset higher costs and a strong dollar.

Who will be the biggest victims?

Working-class Trump voters in Rust Belt states, least able to afford price hikes, especially those who already have jobs in Midwest manufacturing.

Mad Hedge Technology Letter

June 24, 2024

Fiat Lux

Featured Trade:

(E-COMMERCE PARTNERSHIPS WILL THRIVE)

(TGT), (SHOP), (WMT)

Target (TGT) is partnering with e-commerce specialist Shopify (SHOP) to expand its marketplace for third-party merchants.

This is a big deal so don’t diminish this news.

I honestly applaud this maneuver by Target, because it adds e-commerce footprint without paying a premium for it.

Everyone knows that everything is a total rip-off these days like adding an incremental addressable audience at a tech company.

Target has a lot to do to catch up with Amazon, but that’s the direction they should be headed in.

In the future, there is a highly likelihood that TGTs digital business will determine whether they succeed or fail as a tech company.

Everyone is going digital now. Adapt or die.

Shopify is a powerful back-end ecommerce foundation and integrating that with Target appears as a win-win decision moving forward.

We only need to look at competitor Walmart (WMT) which presides over a booming e-commerce business.

That is by decision as they launched a digital-first strategy and have made serious inroads into picking up e-commerce market share.

This partnership also on boards Target into a whole load of new products that they could only dream of selling and the process was rather painful.

Target Plus operates on an invite-only basis for merchants and currently offers more than 2 million items through more than 1,200 sellers.

Online marketplaces can also be launch pads for profitable advertising businesses, with merchants paying for prominent placement in front of shoppers.

Target more than doubled the number of sellers and products on its marketplace over the past year.

The company plans to maintain its invite-only model and continue vetting sellers on the platform.

Curating the selection — for example, allowing only one vendor to offer any given item — is a strategy that will let Target stand out.

Target’s partner, Shopify, makes software that helps vendors quickly set up online stores and process payments.

The company says it works with millions of merchants in about 175 countries. Globally, shoppers will spend $282 billion this year on stores managed with Shopify software. That’s more than double Target’s projected sales for the year.

We are at the late stage of the tech cycle that has been long in the tooth.

It’s not a shocker at this point for tech models to be petering out and management looking for that extra juice to kick-start revenue growth for however long the rest of the business cycle lasts.

Clearly, debt financing isn’t an option these days and I do believe this is a time when management showed their worth as conditions have been extraordinarily tight for the last 2 years.

There is also no guarantee that business conditions will reverse and go back into that pre-pandemic goldilocks phase.

The jury is still out but higher interest rates could be in the mix for the foreseeable future.

Therefore, it is clever by TGT and SHOP to strike up a partnership in which TGT expands their offerings and SHOP merchants get a crack at a new audience.

These opportunities are limited in fashion, but tech in 2024 isn’t about an unlimited addressable audience.

Tech in 2024 is more about efficiency and staying lean because the past 2 years have really been about cutting the bloat.

Target obviously has the more upside in this relationship and I expect them to add other partners that can move the needle.

TGTs share price has been flat for the past 6 months and migrating further into a digital strategy could be the formula to nudge that share price back into high gear.

The stock price is now at $150 per share and I do believe TGT has the chance to grind higher closer to $200 per share by year-end.

Global Market Comments

December 15, 2023

Fiat Lux

Featured Trade:

(DECEMBER 13 BIWEEKLY STRATEGY WEBINAR Q&A),

(BYDDF), (TSLA), (NEM), (UNG), (WMT), (TGT), (GOLD), (TLT), (JNK), (HYG)

Below please find subscribers’ Q&A for the December 13 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

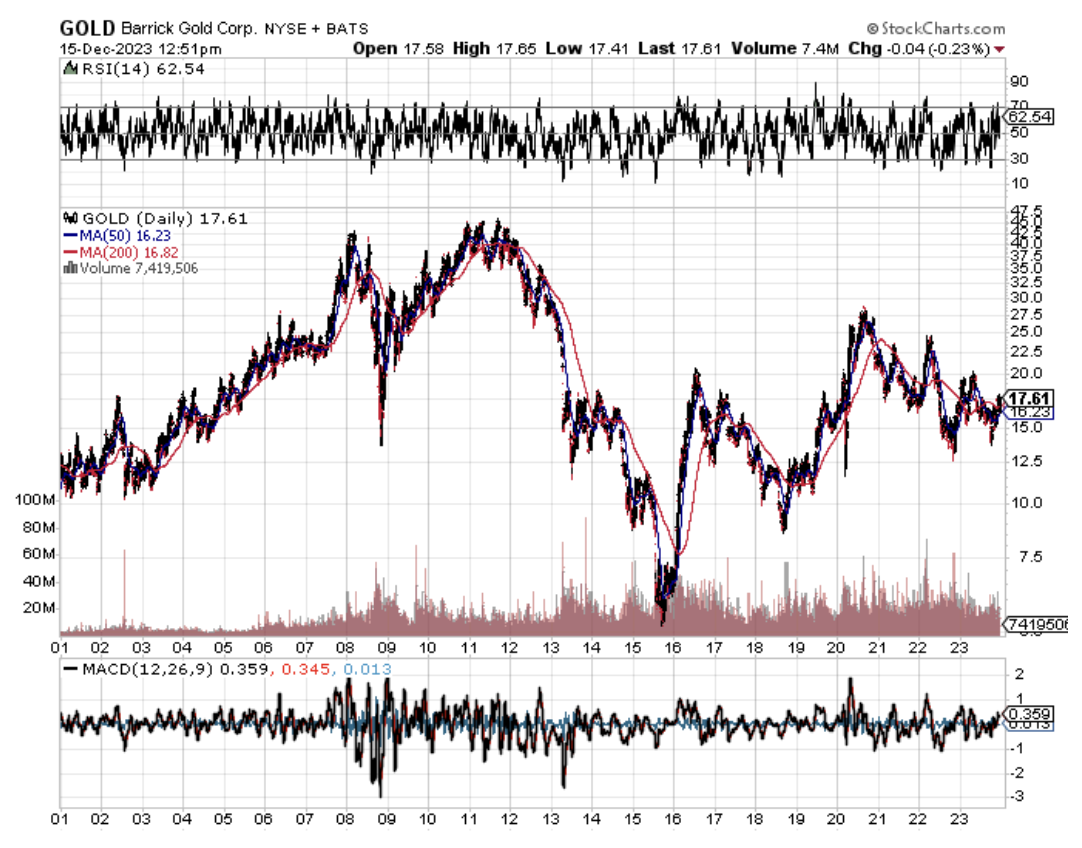

Q: I think it's a good time to buy gold, do you agree? If so, what are your top picks for a long-term hold?

A: I was looking at some very long-term gold charts, and gold tends to have really hot and really cold decades, and we're just finishing a cold decade. In fact, the price of gold today is roughly where it was 12 years ago—it hasn't moved in 12 years. But if you look at the decade before that, it went up ten times from $200 to $2,000, so we're about to enter another hot decade. It may not go up 10X, but 5X is realistic. That would take us up from $2,000 to $10,000, and I think we could see $3,000 as early as 2025.

The best plays are always the gold miners. And my two favorite picks there are Barrick Gold (GOLD) and Newmont Mining (NEM). If you want to be even more aggressive than that, the underlying miners tend to go up at four times the rate of the gold metal. I can also go with junior minors who probably are losing money now, but if gold goes up to $5,000, they'll make money. Those are hugely leveraged, high-risk plays.

Q: Is it time to sell Tesla (TSLA) stock on all long-term accounts?

A: It is not. If you truly are long-term, I think Tesla goes to $10,000 eventually, but we are in the middle of a price war. Price wars are not when you want to be involved in the stock, so I wouldn't be adding to Tesla positions here—I want to see what the final bottom looks like, when the price wars end the prices start to go up, and we'll get that with an economic recovery next year.

Q: Who are Tesla's prime competitors?

A: I would say it's BYD CO., INC. (BYDDF) in China. BYD, which I visited in China 12 years ago, is actually out selling Tesla in China, and they have the ability to produce a super cheap car. They have a $25,000 car in Europe right now, and the fear is that they will make a $15,000 car, and then flood the United States with it. I doubt that will happen; they've never been able to reach American quality and safety standards, and that's why you don't see Chinese cars here. You do see them in other countries like Australia, Hong Kong, and parts of Africa; and they're currently making a big push in Europe, which certainly has all the German car producers worried. Competition is out there and does pose a risk to Tesla, but I think long-term Tesla still wins anyway. By the way, I hasten to mention there are no American competitors to Tesla. Tesla is so far ahead that the big three will never ever catch up and eventually just be reduced to selling Teslas on license.

Q: Where do you think the bottom in oil is?

A: The consensus in the market right now is $62 a barrel. That's about another $6 or $8 lower than here, and then I think we really do bottom out. Then you want to start piling into oil producers like ExxonMobil (XOM), which we had a position in last week, and Occidental Petroleum (OXY), which is the number one pick by Berkshire Hathaway. So those are two good names to go with. What drives these and all other commodities in the future? The answer is a recovering economy. Let's assume we drop from 5.2% last quarter to maybe 2% this quarter—we will accelerate to 5% next quarter, and that's what takes all of your commodity plays upward.

Q: Would you buy retailers here like Walmart (WMT) or Target (TGT)?

A: No. The time to buy retailers is in the run-up to Christmas. I don't know about you, but I'm finished with all my Christmas shopping! You want to buy in the run-up to Christmas shopping, not when it's peaking. Target on the other hand has done really well, and on a massive cost-cutting effort.

Q: When do you think is the first interest rate cut?

A: Since the market has a consensus of May, with some people saying March, I'll go for June. I think this Fed wants to torture us a little bit more and delay any interest rate cuts, but markets will discount that anyway. So it all sets up a great backdrop to buy stocks now, because markets discount things six months in advance, and six months from now is May. That's why we've had the ballistic moves that we've seen in stocks.

Q: Whatever happened to the natural gas trade United States Natural Gas Fund (UNG)?

A: The problem with all these commodity trades is that they are all in one way or another dependent on the weather, and we are having a warm winter, so you can't fool Mother Nature. Not only is it warm here, but it's warm in China, and in Europe. I think they have this thing called…global warming? It makes you ask yourself if you even want to be near an energy trade during a time of global warming, which is accelerating. So anyway, we had a nice profit on this in October—it completely went away. The (UNG) ETF went from $8 all the way down to $4.50, so we'll just have to wait for the cold weather and for (UNG) to ramp up. If it doesn’t happen soon, we may not have a rally this year in natural gas. Pray for snow!

Q: Is junk the best to buy in bonds?

A: It's the best risk-reward ratio; it has a yield roughly 50% higher than TLT with only slightly more risk. The default ratio on junk bonds is actually quite low. And in fact, before you buy (JNK) (SPDR Bloomberg High Yield Bond ETF) or (HYG) (iShares iBoxx $ High Yield Corporate Bond ETF), go to the website and look at their largest holdings and you’ll see what I mean, it's all airlines and cruise lines which had to load up on debt during the pandemic but are doing great right now.

Q: How can the market still rally if it's time to sell and take profit?

A: We get a round of profit-taking at some point, and there's your entry point. Right now, no professional trader is buying anything right now, they're just holding back and seeing when they take profits. And the way traders think is they don't want to trade anymore until they get paid! The year end is ending shortly and the risk-reward favors taking profits and then sitting on the profits. Guess what I'm doing? I'm taking profits and sitting on the profits because traders have bonuses that tend to get paid in January.

Q: On the (TLT) put trade, should one get out once it hits $95?

A: Yes, I always stop out when we hit the nearest strike on a call spread or a put spread. That's a good discipline to have. 90% of the time, if you hold on to expiration, you make the maximum profit in these, but that 10% of the time it's a total write-off, so you get to choose. I try to keep the volatility of the Mad Hedge service low so I always stop out quickly—easier to dig yourself out of a small hole than a big one.

Q: How do you think the next two government shutdowns in January and February will affect the market? Is this a buying opportunity?

A: Absolutely, yes, it is a buying opportunity. Shutdowns tend to be short, but you may get a lot of political turmoil, especially in the House. After the Long Island by-election to replace the disgraced George Santos the Republican majority is likely to shrink to only two seats. The House could fire another speaker, for example. We're kind of in unprecedented territory here in terms of the US government, but at any stock market decline, you would be a big buyer. That's how to play it. If people want to puke out on what's happening in Washington—thank you very much, I'll take your stock.

Q: Are we still bullish on the Barack Gold (GOLD) LEAPS?

A: Absolutely, especially if you have the 2025 expiration. There is an easy double or triple here.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

At BYD in China 2011

Global Market Comments

August 15, 2023

Fiat Lux

Featured Trades:

(THE TOP SIX CHINESE RETALIATION TARGETS),

(AAPL), (GM), (WMT), (TGT), (BA), (SBUX), (CAT),

(AND MY PREDICTION IS….)

CLICK HERE to download today's position sheet.

Global Market Comments

June 14, 2022

Fiat Lux

Featured Trade:

(THE MAD HEDGE TRADERS & INVESTORS SUMMIT IS ON FOR JUNE 14-16)

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or WHAT HAPPENS WHEN YOUR BEST FRIEND BECOMES YOUR WORST ENEMY?)

(SPY), (TLT), (TSLA), (CCJ), (TGT), NVDA), (JPM), (BAC), (C)

Of course, I am talking about the Federal Reserve.

The Fed was the best friend of share owners, pressing interest rates lower from March 2009. That remained the case for 12 years until November 2021 when its notorious pivot took place, flipping overnight from an easing to a tightening posture.

It's actually worst than that. In fact, our nation’s central bank morphed overnight from the easiest monetary policy in history to the most aggressive tightening.

Stock markets have noticed, the Dow average giving up 20% in six months, and the final lows are probably not in yet.

I would bet money that you are expecting the worst-case scenario to happen. After all, the last serious selloff in 2008-2009 took the index down a heart-palpitating 52%.

What’s more, every oil shock of the last 50 years was followed by a recession, and we are clearly in one now. So, you are right to fear for your net worth and retirement security.

However, my work suggests that the best-case scenario will happen. Who is right, you or me?

You already know the answer.

Let me tell you what is already priced in the stock market: a Russian invasion of Ukraine, inflation at a 40-year high and climbing, a doubling of mortgage interest rates in a half year, peaking of the housing bubble, popping of technology and Bitcoin bubbles, and 200 basis points of Fed interest rate hikes.

With all this negativity already in the market, I would say that it is impossible for stocks NOT to go up. All that is left is to suck in one last round of non-believers on the short side before the indexes start a move to new all-time highs. That could take months at the most.

The only question now is whether a further 5% decline to an S&P 500 of 3,600, or a final puke out low of 3,500, down 7.5%. That means you should start scaling into your favorite longs now, the Cadillacs at Volkswagen prices.

So, let’s do some thinking outside the box here.

Tech stocks are cheaper now than after the low point of the Great 2000 Dotcom Bust. But they are still expensive compared to the main market. The S&P without technology stocks is now valued at earnings multiple of 13X versus 17x main market.

That is well into decade-low territory. That’s why I have included financials like (JPM), (BAC), and (C) in my list of “must own sectors'.

It's clear that inflation will bedevil the market for months to come given the dramatic acceleration we saw in May, from 0.3% to 1%. Let me tell you that there are only two ways to end inflation, and they could be done overnight.

*End all US support for Ukraine and throw in with Vladimir Putin. That would shave $50 off the price of oil immediately and get gas prices below $3.00 a gallon. You might have a hard time selling this to the thousands of Americans going over to Ukraine to volunteer.

*Cause a sharp recession immediately. The Fed is already well on their way to doing this with three guaranteed 50 basis point rate hikes by September. The first thing to collapse in a recession is oil demand. In the last recession, it went to negative $37 in the futures market (I got stopped out at -$5). This is why the oil industry isn’t interested in investing a dime at these oil prices. They are responsible to their shareholders, not Biden’s reelection prospects.

If there is a recession, it’s an invisible one. It’s a recession where you can’t hire anyone, can’t buy anything, subcontractors give you a six-month timeline with a straight face, and it takes a year to get delivery of a damn sofa. This recession miserably fails my “look out the window test.”

But at my advanced age, I don’t get surprised anymore.

Boba tea anyone? Who knew?

Consumer Price Index slaughters stocks, taking the Dow Average down 1,600 points, or 5% in two days, the worst move in two years. It’s typical bear market action. May inflation hit 8.6%, a new 40-year high. But you have to more than double to hit the old 1980s peak. New stock lows are in easy reach.

Lumber crashes, down 50% from the highs in months, with the near-complete cessation of new orders from builders. They see a recession just around the corner with higher interest rates and no new home buyers. It’s proof that the current inflation is spiking and setting up for a big fall.

Luxury Home Sales are plunging in New York, in numbers, but not in prices. Anyone who needed debt to trade up is out of the picture.

US drop Covid Testing Requirement for international travelers. Too many Americans trying to get home were getting stranded overseas for weeks because they failed a Covid test. Wheww!! That was a close call!

Americans will spend an extra $730 Billion on energy this year. That’s a heck of a lot to take out of consumer spending. So far, there has been no decline in demand. Much of this money ended up in Russian coffers.

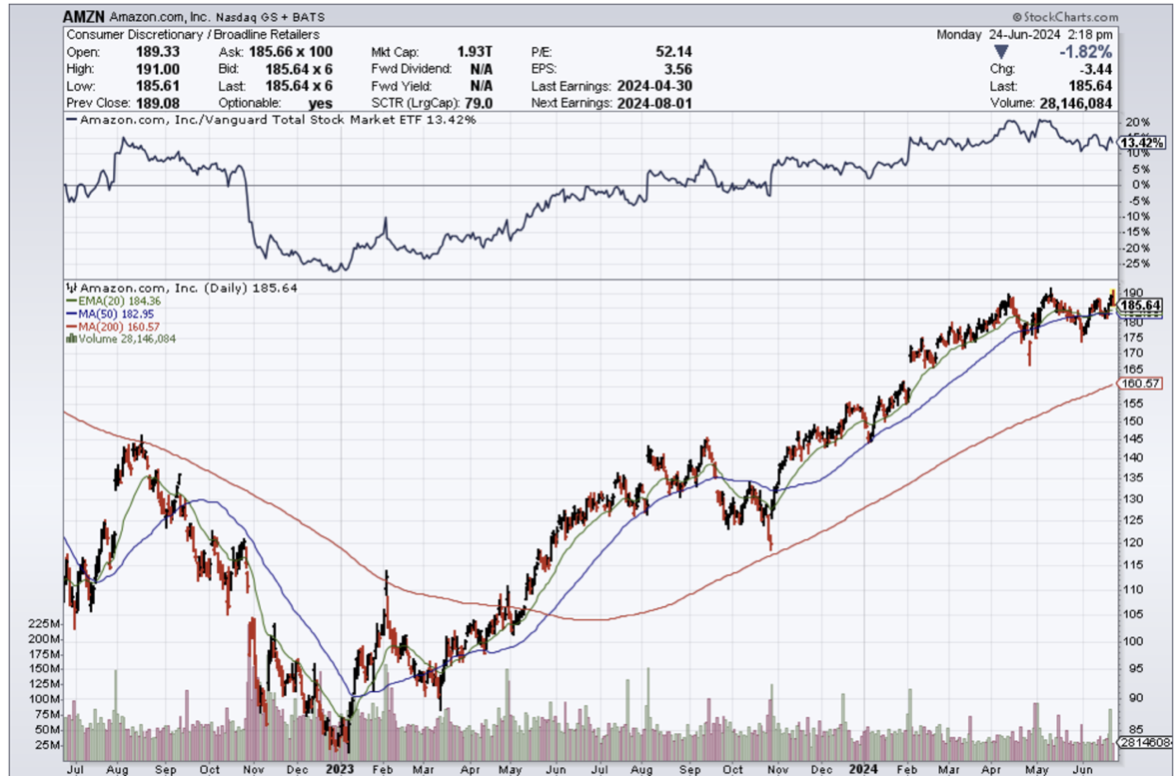

Amazon (AMZN) splits 20:1, triggering an avalanche of new retail buyers. The company is also at the low end of its valuation range anger a gut-punching 41% decline in the share price this year. It may be early, but (AMZN) is definitely a BUY.

Target (TGT) warns of more margin squeeze, with too much inventory and flagging demand. (TGT) has become a bellwether for all of retail, which points to inflation, labor, and supply chain problems.

Uranium Stocks soar on Biden’s plan to buy $4.3 billion worth of enriched uranium, or yellow cake. The move is aimed to replace Russian imports where Russia is one of the world’s largest suppliers. It is the most unexploited form of non-carbon energy out there. Mad Hedge recommended Cameco (CCJ), the world’s second-largest supplier, a month ago. It was up 15% yesterday at the high.

New Home Mortgages hit a 22-year low. With 30-year fixed-rate loans soaring from 2.8% to 5.58% in six months, how can they not? Refis have crashed 75% YOY. Now that the Fed has quit buying, investors won’t touch mortgage-backed securities with a ten-foot pole.

Weekly Jobless Claims pop 29,000 to a five-month high in another hint toward a recession. Continuing Claims are at 1.306 million. The preemptive layoffs by ultra-cautious companies have begun, especially in technology.

Tesla (TSLA) gets an upgrade by UBS, which sees 51% of upside from here to $1,200. Total sales should top 1.4 million vehicles in 2022, up 40% YOY, and that includes lost production of 60,000 in Shanghai. A new Gigafactory in Indonesia is planned with a locked-up supply of Nickel, where the world’s largest supply of the metal resides. Cheap labor helps a lot where 5,000 need to be hired. The company will need six gigafactories to reach 20 million annual production.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With some of the greatest market volatility seen since 1987, my June month-to-date performance recovered to +2.57%.

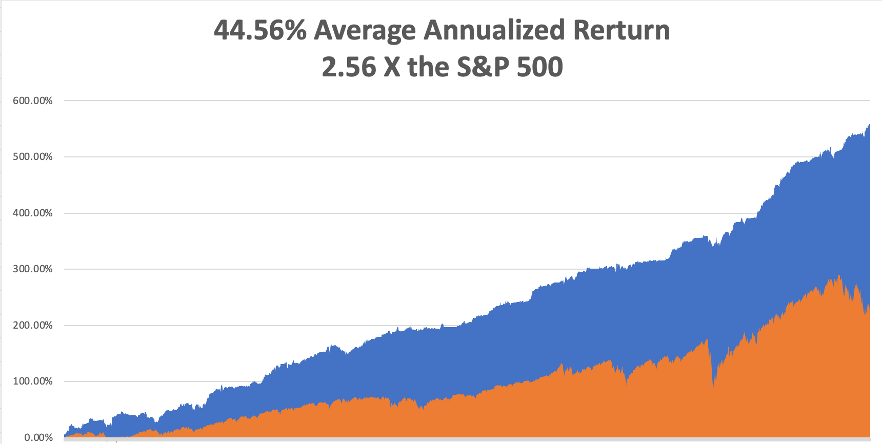

My 2022 year-to-date performance ratcheted up to 44.44%, a new all-time high. The Dow Average is down -13.52% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 66.63%.

That brings my 14-year total return to 557%, some 2.56 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 44.56%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 85.6 million, up 200,000 in a week, and deaths topping 1,011,200 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, June 13 at 8:00 AM EDT, US Consumer Inflation Expectations are out.

On Tuesday, June 14 at 8:30 AM, the Producer Price Index for May is published.

On Wednesday, June 15 at 10:30 AM, Retails Sales for May are announced. The Fed interest rates decision is out at 11:00 AM. The press conference follows at 11:30.

On Thursday, June 16 at 8:30 AM, Weekly Jobless Claims are out. We also get Housing Starts and Building Permits for May.

On Friday, June 10 at 8:15 AM, Industrial Production for May is published. At 2:00, the Baker Hughes Oil Rig Count is out.

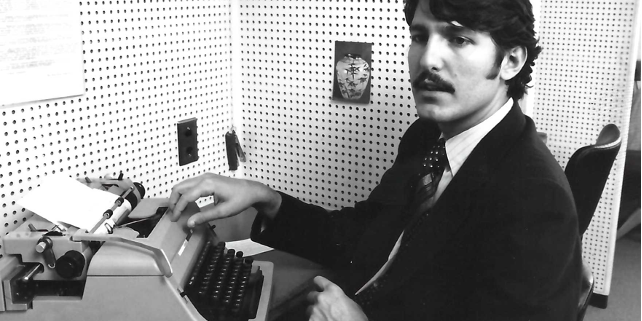

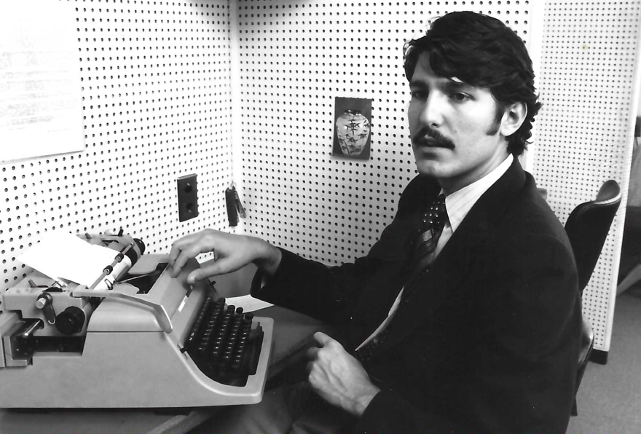

As for me, I have benefited from many mentors and role models over the years, but Al Pinder, last of the New York-based Shipping and Trade News, is one of my favorites. Short with blown hair, glasses, and an always impish smile, he was a regular at lunch where we always played an old dice game called “ballout.”

I sat next to Al for ten years at the Foreign Correspondents Club of Japan high up in Tokyo’s Yukakucho Denki Building, we were pounding away on our antiquated Royal typewriters. At the end of the day, our necks would be stiff as boards. Al’s idea of work was to type for five minutes, then tell me stories for ten.

Saying that Al lived a colorful life would be the understatement of the century.

Al covered the Japanese invasion of China during the 1930s, interviewing several key generals like Hideki Tojo and Masaharu Homma, later executed for war crimes. He told me of child laborers in Shanghai silk processors who picked cocoons out of boiling water with their bare hands.

Al could see war with Japan on the horizon, so he took an extended tour of every west-facing beach in Japan during the summer of 1941, taking thousands of black and white pictures. The trick was how to get them out of the country without being arrested as a spy.

So he bought an immense steamer trunk and visited a sex shop in Tokyo’s red-light district where he bought a life-sized, blow-up doll of a Japanese female. His immensely valuable photos were hidden below a false bottom in the trunk and the blow-up doll placed on top.

When he passed through Japanese customs on the ship home from Yokohama, the inspectors opened the trunk, had a good laugh, and then closed it. These photos later became the basis of Operation Coronet, the American invasion of Japan in 1945.

Al was working for the Honolulu Star Bulletin when the Japanese attacked Pearl Harbor on December 7, 1941. Many antiaircraft shells fired at the attacking zeros landed in Honolulu causing dozens of casualties. Al told me every woman on the island wanted to get laid that night because they feared getting raped by the Japanese Army the next day.

Since Al knew China well, he was parachuted into western Yunan province to act as a liaison with Mao Zedong, then fighting a guerrilla war against the Japanese with his Eighth Route Army. Capture by the Japanese then meant certain torture and certain death.

In 1944, Al received a coded message in Morse code to pick up an urgent communication from Washington. So, he hiked a day to the drop zone and when the Army Air Corps DC-3 approached, he lit three signal fires.

A package parachuted to the ground, which he grabbed and then he fled for the mountains. Dodging enemy patrols all the way, he returned to his hideout in a mountain cave and opened the package. It was a letter from the Internal Revenue Service asking why he had not filed a tax return in three years.

When the second atomic bomb fell on Nagasaki, the war ended on August 15. Since Al was the closest man on the spot, he flew to Korea where he accepted the Japanese surrender there.

Al was one of the first to move into the Press Club, which housed war correspondents in one of the only buildings still standing in a city that had been bombed flat.

Al never left Japan because, as with many other war correspondents who arrived with the US military, it was the best thing that ever happened to him. After some initial hesitation, they were treated like conquering heroes, it was incredibly cheap at 800 yen to the dollar, and the women were beautiful.

During the Japanese occupation when the people were starving, Al bought an acre of land in Tokyo’s burned-out prime Akasaka district for a ten-pound can of ham. He spent the rest of his life living off this investment, selling one piece at a time, until it eventually became worth $10 million.

Al went to work for the Shipping and Trade News, an obscure industry trade publication which no one had ever heard of. I sat next to him when he artfully lifted every story out of an ancient book, Ships of the World. But Al always had plenty of money to spend.

When Al passed away in the early 2000s, an official from the American embassy in Tokyo showed up at the Press Club asking if anyone knew all Pinder. We eventually traced a bank branch which held a safe deposit box in his name. In it was proof that the CIA had been bribing every Japanese prime minister of the 1950s. He kept the evidence as an insurance policy against the day when his lucrative deal with the Shipping and Trade News was ever put at risk.

I flew in for Al’s wake and his Japanese wife was there along with most of the foreign press. Everyone was crying until I told the IRS story, then they had a good laugh.

A few years ago, I was invited to give the graduation speech at Defense Language Institute in Monterey, California. The latest bunch of graduates, including my nephew, were freshly versed in Arabic and headed for the Middle East.

The school was founded in 1941 to train Americans in Japanese to gain an intelligence advantage in the Pacific war.

General 'Vinegar Joe' Stillwell said their contribution shortened the war by two years. General Douglas MacArthur believed that an army had never before gone to war with so much advance knowledge about its enemy.

To this day, the school's motto is 'Yankee Samurai'. There on the wall with the school’s first graduates was a very young Al Pinder, still with that impish grin.

Al lived a full life and I still miss him to this day. I hope I can do as well.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Al Pinder

Press Club 1976

Global Market Comments

May 20, 2022

Fiat Lux

Featured Trade:

(MAY 18 BIWEEKLY STRATEGY WEBINAR Q&A),

(C), (FXI), (BABA), (TSLA), (AAPL), (AMZN), (TGT), (FLR), (QQQ),

(FB), (ARKK), (TSLA), (WYNN), (UAL), (ALK), (DAL)