Global Market Comments

April 15, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or VOLATILITY IS BACK!)

(REMEMBERING TRINITY)

(TLT), (TSLA), (NVDA), (FCX),

(XOM), (WPM), (GLD), (FXI), (FXY), (USO), (GOOGL)

Global Market Comments

April 15, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or VOLATILITY IS BACK!)

(REMEMBERING TRINITY)

(TLT), (TSLA), (NVDA), (FCX),

(XOM), (WPM), (GLD), (FXI), (FXY), (USO), (GOOGL)

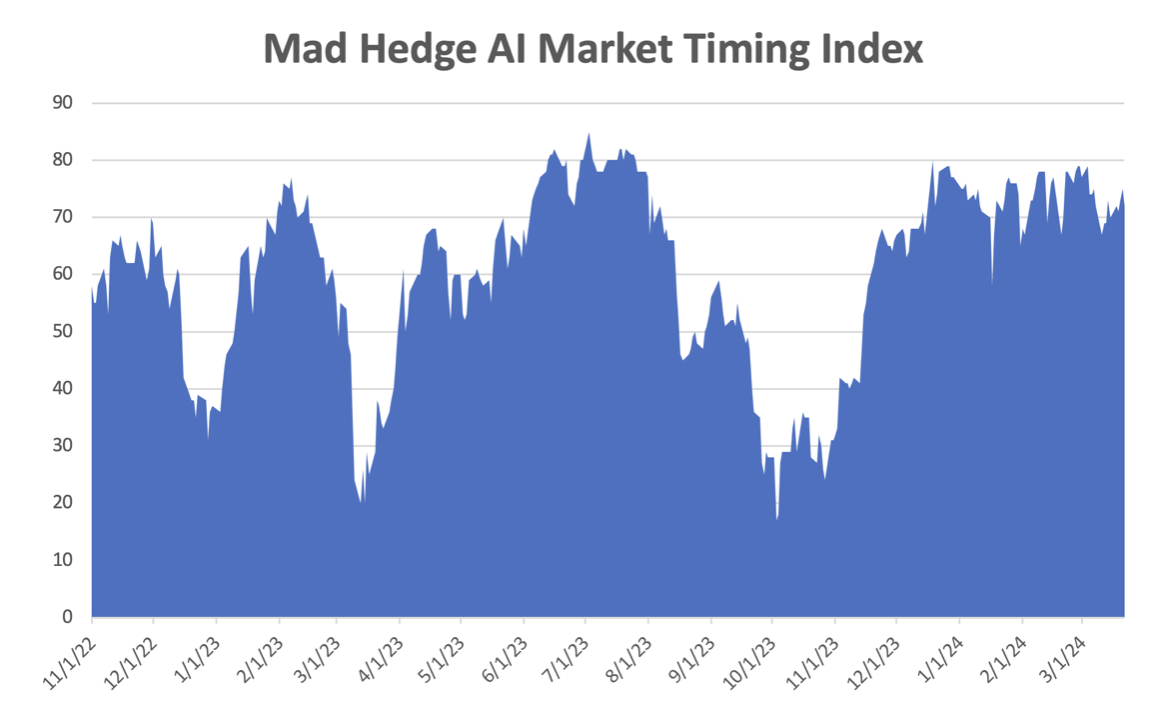

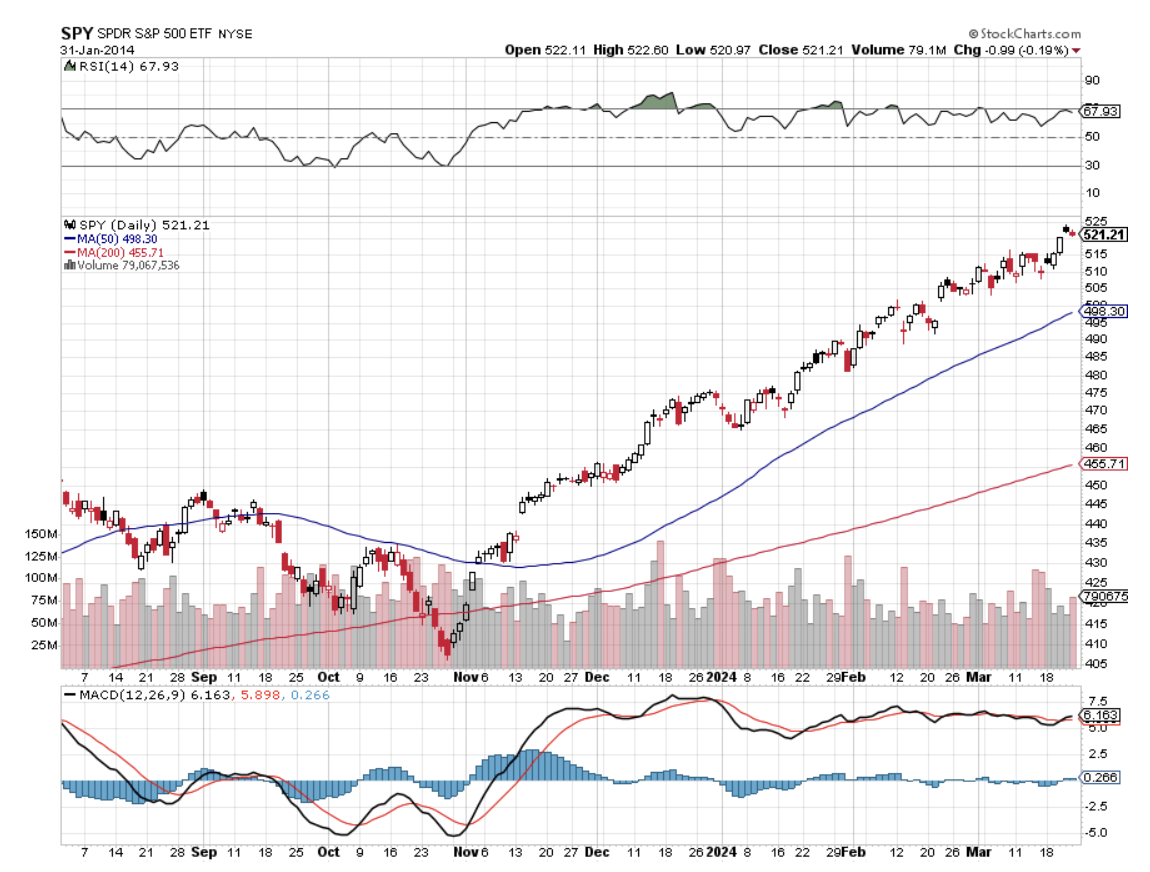

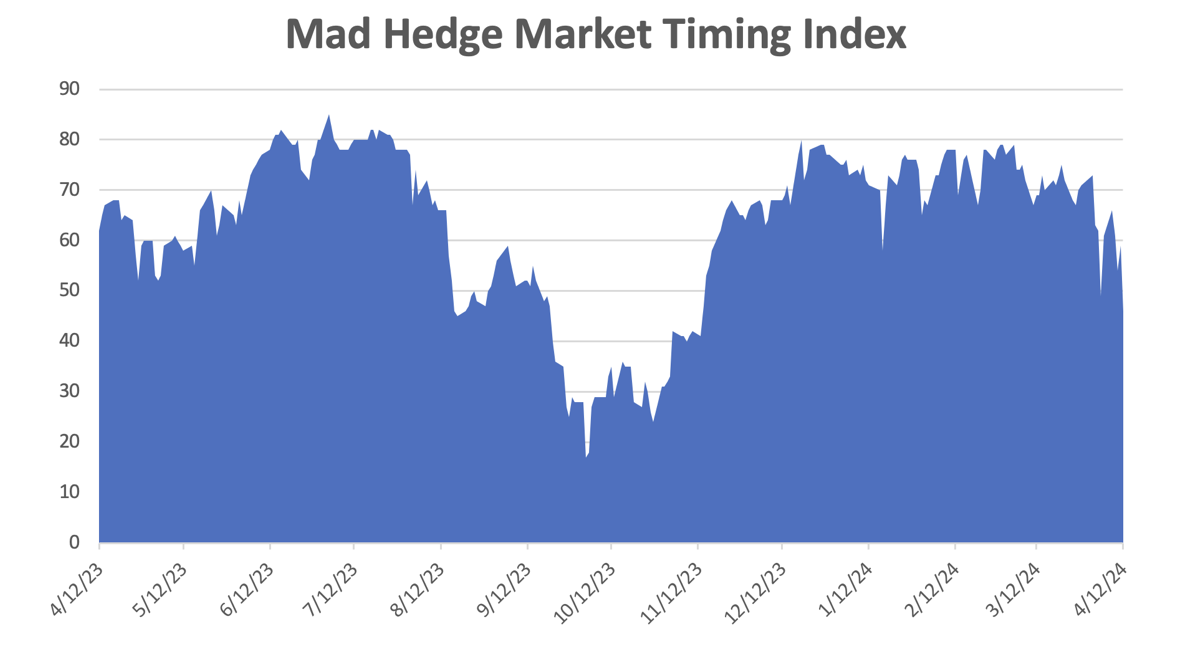

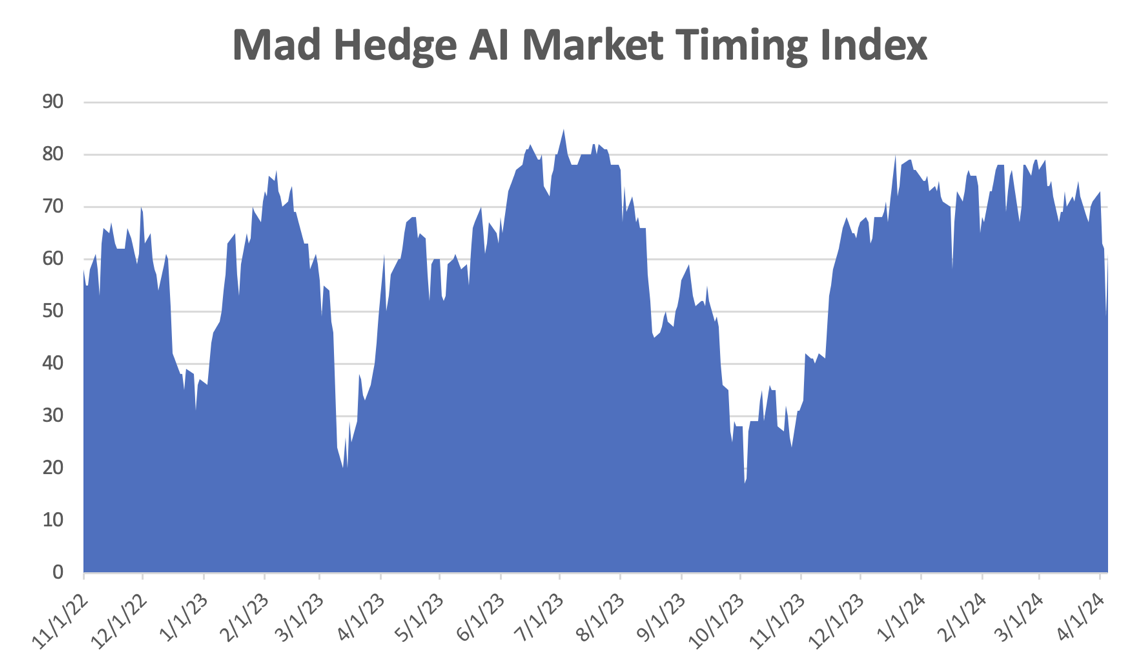

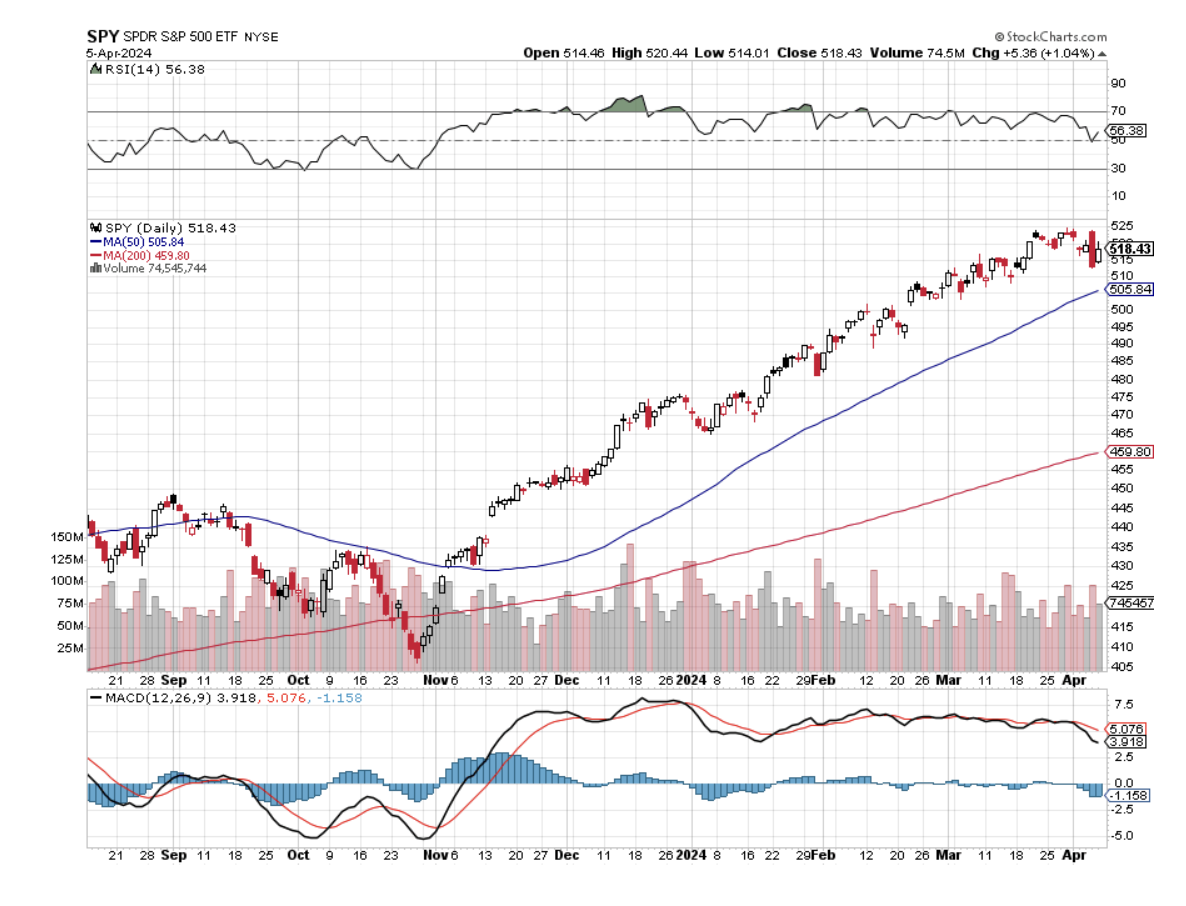

Those who expected markets to go up forever were given a rude awakening last week with a swift slap across the face with a wet kipper. The Volatility Index ($VIX) soared from $12 to $19 and higher highs will unfold this week. The Mad Hedge Market Timing Index dropped below 50 for the first time since October and lower lows beckon.

For those of us who earn our crust of bread off of volatility, its return is like a gift from the gods. The long desert has been crossed and the fresh mountain springs beckon just ahead.

What prompted this ($VIX) melt-up is that many traders and investors are finally throwing in the towel on ANY interest rate cuts in 2024. In a mere four months, we have gone from an expectation of six rate cuts to zero. Not helping matters is that the “May” thing, as in “Sell and Go away” is only two weeks away. After an overcooked Q1, we may be headed into a summer that is the next great Ice Age.

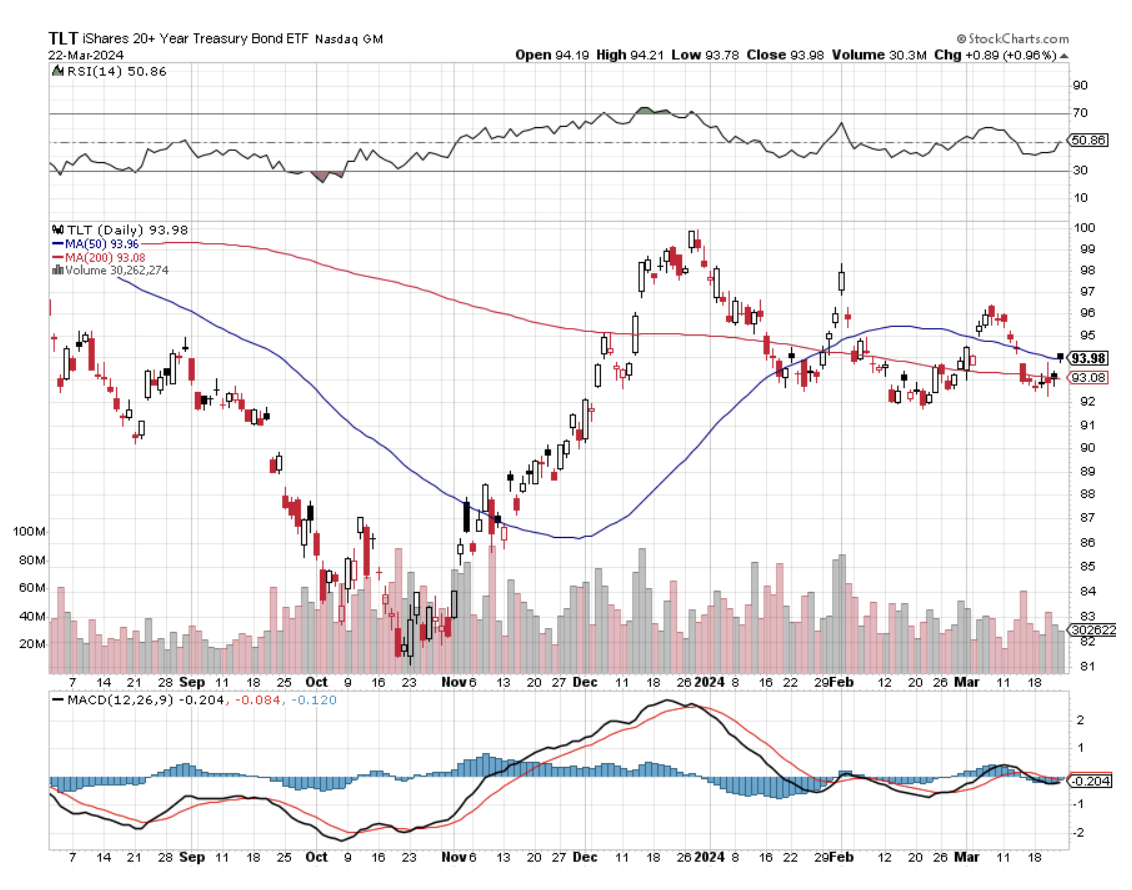

At least that is the assumption we have to make from a trading point of view for the short-term. While this represents a worst-case scenario, I don’t expect bonds to drop much from here, maybe a couple of points, as future interest rate cuts are a certainty. All that has happened is that our rate cuts have been moved out from two months to five months. The next move in interest rates is still down.

At some point, there will be a great bond trade out there, but definitely, not yet!

Watching the market action last week, it was especially impressive how well NVIDIA (NVDA) held up.

NVIDIA is so far ahead of the competition that no one will catch up for years. What the (NVDA) bears don’t get is that the company has a moat so wide it is impossible to cross. Their enormous lead in software is the result of crucial platform decisions made 20 years ago. The key staff are all locked up with ultra-cheap equity options with strike prices around $1-$2.

Virtually everyone has now raised their upside targets for the stock over $1,000/share and there are $1,400 figures out there. That’s because, with a price-earnings multiple of only 30X, it is still the cheapest Big Tech stock in the market. By comparison, its biggest customer, (META) is at 34X, AI Leader (MSFT) is at 38X, and (AMZN) is at a stratospheric 63X.

Efforts by Alphabet (GOOGL) to break into the AI chip business are feeble at best. This is a business that has a very long learning curve with very high capital costs.

Every 15% correction in (NVDA) over the last two years has been a strong “BUY”. It really owns the AI design business. It’s looking at $250-$500 BILLION in sales growth over the next several years.

Santa Clara-based NVIDIA designs and manufactures high-end, top-performing graphics cards or GPUs. There is probably one in your PC. They are essential in the artificial intelligence, automobile, PC, supercomputing, cybersecurity, and gaming industries. As a design company only company NVIDIA represents pure intellectual added value. Its chips are manufactured in Taiwan.

They are also crucial for national defense. The Biden administration recently banned NVIDIA from exporting high-end chips and their manufacturing equipment to China, which they were using to build sophisticated weapons to use against us. Last week China banned NVIDIA chips in a typical tit-for-tat gesture.

We have had a spectacular week here at Mad Hedge Fund Trader.

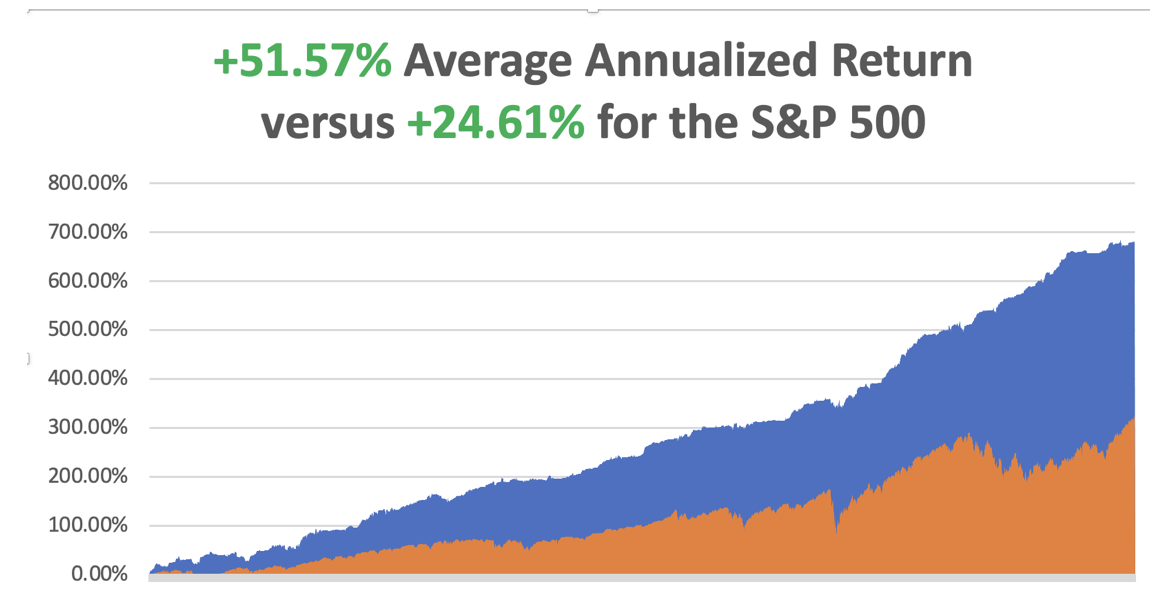

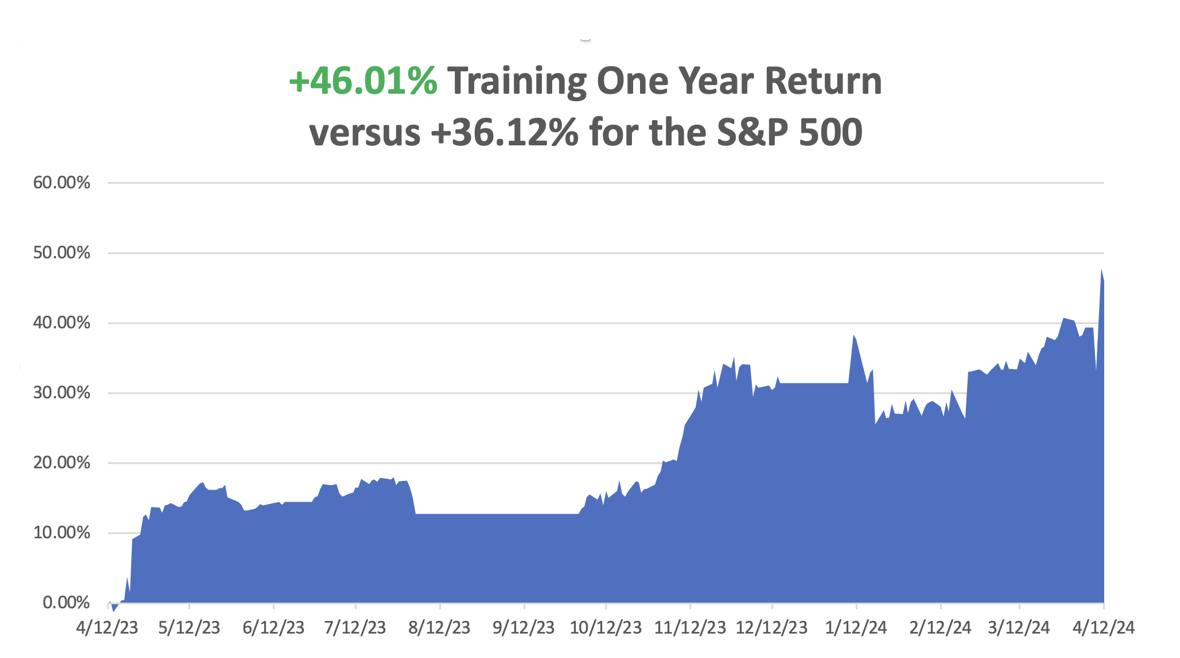

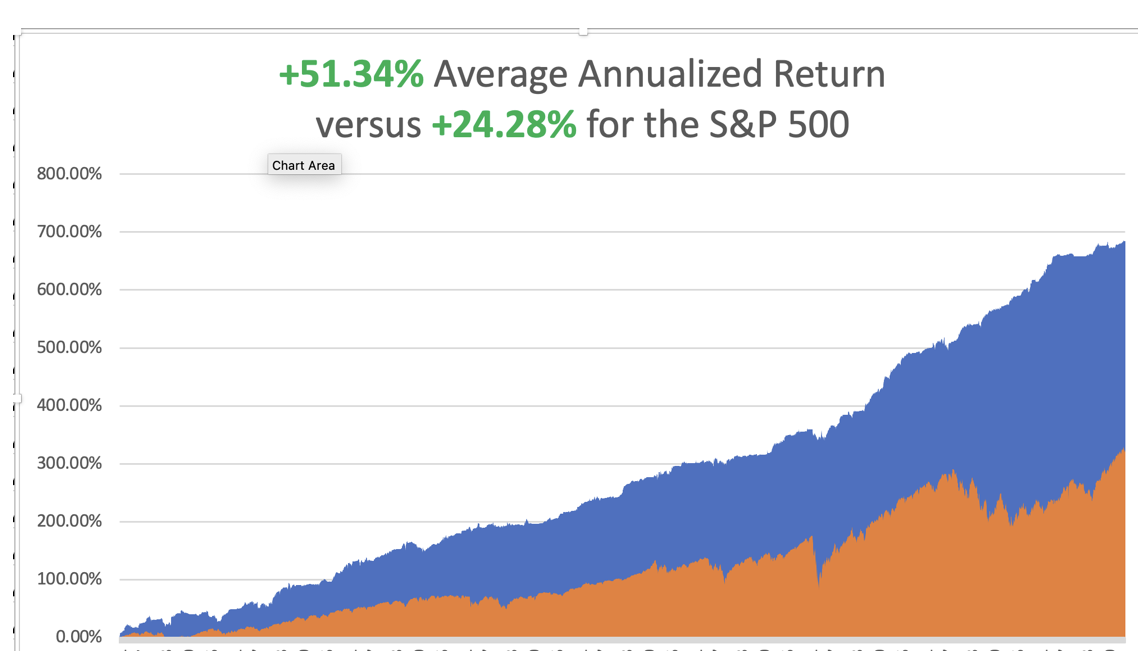

So far in April, we are up +5.20%. My 2024 year-to-date performance is at +14.47%. The S&P 500 (SPY) is up +7.22% so far in 2024. My trailing one-year return reached +46.01% versus +36.12% for the S&P 500.

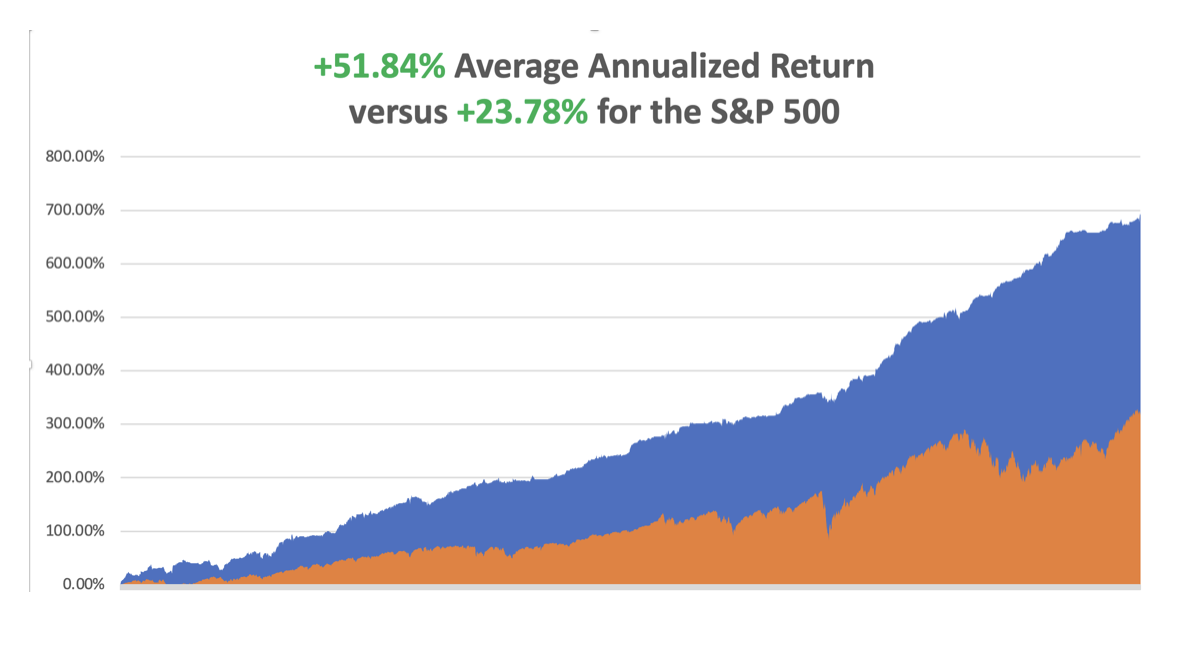

That brings my 16-year total return to +691.20%. My average annualized return has recovered to +51.84%.

Some 63 of my 70 round trips were profitable in 2023. Some 20 of 26 trades have been profitable so far in 2024.

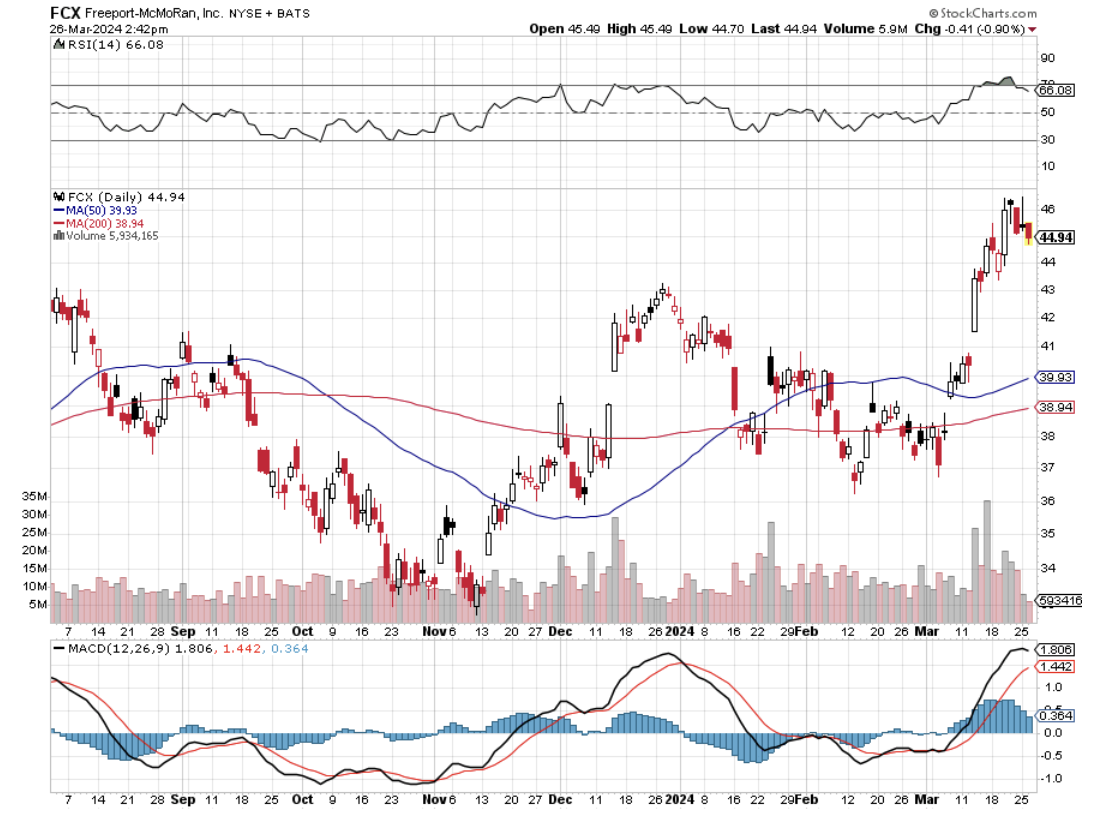

We got a rare dip last week, which I used to rush into four new May positions, double positions in (NVDA) and additional ones in (FCX) and (TLT). I will let my existing April longs expire at a max profit in four days on April 19 in Freeport McMoRan (FCX), Occidental Petroleum (OXY), ExxonMobile (XOM), Wheaton Precious Metals (WPM), Tesla (TSLA), and Gold (GLD).

I am in a rare 100% invested position with no cash given the massive upside breakout in commodity, precious metals, and energy we have witnessed. This is going to be a great month.

Consumer Price Index Comes in Hot at 0.4% for March, the same rate as in February according to the Bureau of Labor Statistics, knocking stocks down 500 points. Housing and transportation were the big badges. Hopes of a June interest rate cut have been dashed. September is now the earliest. Avoid (TLT).

Producer Price Index Comes in Cold at 0.2% for March. On a 12-month basis, the PPI rose 2.1%, the biggest gain since April 2023, indicating pipeline pressures that could keep inflation elevated. Stocks rallied 200 points.

US Dollar Rockets on Hot CPI, hitting a new 34-year high against the Japanese yen at ¥151.55. Bank of Japan's intervention to support the yen is expected. Yen shorts in the futures market hit a five-month high. Avoid (FXY).

China Continues Record Gold Buying, soaking up record amounts. Central banks bought a record 1,082 metric tonnes of gold in 2023. The Bank of China bought a record 735 tonnes of gold in 2023, two-thirds of which were purchased through covert third-party middlemen. An additional 1,411 tonnes, likely to bypass a collapsing Yuan, and a whopping 228 tonnes in January 2024 alone. This is what delivered the barbarous relic’s decisive upside breakout from a three-year trading range. This dwarf’s the record 1,082 metric tonnes of gold global central banks bought in 2023. The world gold market has been taken short and prices will continue to rise.

Gold Derivatives are Now Wagging the Dog. There are 187,000 metric tonnes of gold above ground worth a mere $14.4 billion which price is 50 times that figure in paper derivatives, like ETFs, futures contracts, and options. A metric tonne of gold today is worth $77 million. That increases the barbarous relic’s volatility once it breaks out of long-term trading ranges, which it has just done. With new volatility eventually, some bodies have to float to the surface. The bad news is that this may also be a signal that China will invade Taiwan. Buy (GLD) on dips.

Oil (USO) Spikes on New Iran War Threats, sending Brent to $92, a new 2024 high. Gold (GOLD) and silver (WPM) have gone ballistic as well. Hang on for higher highs.

JP Morgan Misses on Earnings, tanking the shares by $10. The firm earned $23.1 billion in net interest income in the first three months of 2024, up 11% from a year earlier. The bank’s NII haul ended a streak of seven quarters where it posted record levels of the metric. The bank cited deposit margin compression — tightening of profits between what the bank earns on loans and pays out on deposits — and lower deposit balances in the consumer business for the sequential decline. Buy (JPM) on dips.

China’s International Trade Collapses. Exports from China slumped 7.5% year-on-year last month by value, the biggest fall since August last year. They had risen 7.1% in the January-February period.

Hong Kong's major indexes extended losses to more than 2%.

Chinese exporters are continuing to slash prices to maintain sales amid stubbornly weak domestic demand. Avoid (FXI).

Tesla Cancels Model 2, a key part of the bull story for (TSLA). Elon Musk says “Not so fast” and instead highlights the company’s move into robotic self-driving cars. Don’t be so dismissive, as Waymo completed an eye-popping 100,000 robotic taxi rides in San Francisco in December, many with thrilled first-time users. The stock held up incredibly well on awful news indicating that it believes Elon and not the media. Buy (TSLA) on dips.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, April 15, at 7:00 AM EST, the US Retail Sales are announced.

On Tuesday, April 16 at 8:30 AM, US Housing Starts are released.

On Wednesday, April 17 at 2:00 PM, the Beige Book notes from the previous Fed meeting are published

On Thursday, April 18 at 8:30 AM, the Weekly Jobless Claims are announced. At 10:00 AM, Existing Home Sales are out.

On Friday, April 19 at 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, with the spectacular popularity of the Oppenheimer movie, I thought I’d review my own nuclear past. When the Cold War ended in 1992, the United States judiciously stepped in and bought the collapsing Soviet Union’s entire uranium and plutonium supply.

For good measure, my client George Soros provided a $50 million grant to hire every Soviet nuclear engineer. The fear then was that starving homeless scientists would go to work for Libya, North Korea, or Pakistan, which all had active nuclear programs at the time.

They ended up here instead. I just might be that the guy standing next to you in line at Safeway with a foreign accent who knows how to design a state-of-the-art nuclear bomb.

That provided the fuel to run all US nuclear power plants and warships for 20 years. That fuel has now run out and chances of a resupply from Russia are zero. The Department of Defense attempted to reopen our last plutonium factory in Amarillo, Texas, a legacy of the Johnson administration.

But the facilities were deemed too old and out of date, and it is cheaper to build a new factory from scratch anyway. What better place to do so than Los Alamos, which has the greatest concentration of nuclear expertise in the world?

Los Alamos is a funny sort of place. It sits at 7,320 feet on a mesa on the edge of an ancient volcano so if things go wrong, they won’t blow up the rest of the state. The homes are mid-century modern built when defense budgets were essentially unlimited. As a prime target in a nuclear war, there are said to be miles of secret underground tunnels hacked out of solid rock.

You need to bring a Geiger counter to garage sales because sometimes interesting items are work castaways. A friend almost bought a cool coffee table which turned out to be a radioactive part of an old cyclotron. And for a town designing the instruments to bring on the possible end of the world, it seems to have an abnormal number of churches. They’re everywhere.

I have hundreds of stories from the old nuclear days passed down from those who worked for J. Robert Oppenheimer and General Leslie Groves, who ran the Manhattan Project in the early 1940s. They were young mathematicians, physicists, and engineers at the time, in their 20s and 30s, who later became my university professors. The A-bomb was the most important event of their lives.

Unfortunately, I couldn’t relay this precious unwritten history to anyone without a security clearance. So, it stayed buried with me for a half century, until now.

Some 1,200 engineers will be hired for the first phase of the new plutonium plant, which I got a chance to see. That will create challenges for a town of 13,000 where existing housing shortages already force interns and graduate students to live in tents. It gets cold at night and dropped to 13 degrees F when I was there.

I actually started in the nuclear biz during the early 1970s when my math professor recommended me for a job there. In those days, mathematicians had only two choices. Teach or work for the Defense Department. As I was sick of school, I chose the latter.

That led me to drive down a bumpy dirt road in Mercury, Nevada to the Nuclear Test Site where underground testing was still underway. There were no signs. You could only find the road marked by four trailers occupied by hookers who did a brisk business with the nearly all-male staff. My fondest memory was the skinny dipping that took place after midnight in a small pool when the MPs were on break.

I was recently allowed to visit the Trinity site at the White Sands Missile Test Range, the first outsider to do so in many years. This is where the first atomic bomb was exploded on July 16, 1945. The 20-kiloton explosion set off burglar alarms for 200 miles and was double to ten times the expected yield.

Enormous steel targets hundreds of yards away were thrown about like toys (they are still there). Half the scientists thought the bomb might ignite the atmosphere and destroy the world but they went ahead anyway because so much money had been spent, 3% of US GDP for four years. Of the original 100-foot tower, only a tiny stump of concrete is left (picture below).

With the other visitors, there was a carnival atmosphere as people worked so hard to get there. My Army escort never left me out of their sight. Some 79 years after the explosion, the background radiation was ten times normal, so I couldn’t stay more than an hour.

Needless to say, that makes uranium plays like Cameco (CCJ), NextGen Energy (NXE), Uranium Energy (UEC), and Energy Fuels (UUUU) great long-term plays, as prices will almost certainly rise and all of which look cheap. US government demand for uranium and yellow cake, its commercial byproduct, is going to be huge. Uranium is also being touted as a carbon-free energy source needed to replace oil.

At Ground Zero in 1945

What’s Left of a Trinity Target 200 Yards Out

Playing With My Geiger Counter

Atomic Bomb No.3 Which was Never Used

What’s Left from the Original Test

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 8, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE WINDFALL YEAR),

(FCX), (TLT), (TSLA), (NVDA), (FCX),

(XOM), (WPM), (GLD), (CCJ), (META), (AMZN),

(AN EVENING WITH TRAVEL GURU ARTHUR FROMMER)

This year seems to be the year of the windfall.

In January, we loaded up on Big Tech (AMZN), (MSFT), which then went ballistic.

In February, we doubled up on NVIDIA (NVDA), which then nearly doubled.

In March, spotting the shift into commodities, energy, and precious metals we loaded the boat with gold Freeport McMoRan (FCX), gold (GLD), silver (WPH), and oil (XOM), (OXY), which launched into torrid two-week straight up moves which continue. And for good measure, we dove into NVIDIA one more time.

Even the trades I thought about and talked about but never executed took off like a scalded chimp, such as uranium producer Cameco (CCJ), up 30% in weeks.

And while you’d think that trades like this would generate the performance of a lifetime, in fact, I begrudgingly admit I'm lagging behind the index this year. It’s incredibly annoying when after working 12 hours a day seven days a week, the indexers, the investors who sit on their hands all day and do nothing, are making more money than I am.

That’s because I put out a handful of ill-timed short positions in the S&P 500 (SPY) and Freeport McMoRan (FCX) which cut my numbers by half.

You may ask why I suffered the madness of putting out shorts when we are in a bull market and that everything is going straight up every day! That’s because I am the Mad Hedge Fund Trader, not the Mad Long-Term Investor. And hedge funds are always supposed to have balanced longs and shorts. I can tilt this by keeping only one short position against a basket of longs. But even those single longs have proved painfully expensive.

The issue here is that the market is not breathing as it normally does. There is no ebb and flow to let you in and out of positions. Sectors flatline, then launch into bull moves that take them up almost every day for months. That is an impossible market to trade.

I have only seen this twice during my lifetime: during the Great Japanese Stock Bubble of the 1980s and the Dotcom Bubble of the 1990s, which means we are in another one of these great bubbles, which will probably be the last of my lifetime.

The previous two great bubbles went on for five years. Greed can last a long time. If you count the October 26, 2023 low as the start of the new bull market, we have 4 ½ years to run in this one. What is more likely is that the pandemic low in April of 2020 was the start of this new bull market and we have averaged a 25% a year return in stocks since then. That means we have at least another year to run…. or more.

Valuations are at the high end of their recent range at 21 times S&P 500 earnings. But during the 1990’s bubble, the market average reached an earnings multiple in the 30s, and technology stocks reached a stratospheric 100 times earnings.

And today, earnings are still rising, sometimes quite sharply, such as the case with (NVDA) and (META). It’s when earnings are falling but stocks are still rising that you have to worry, as happened in 1999 and the first four months of 2000. In the 1980s in Tokyo, nobody ever looked at earnings.

Another frustration with trading today is the collapse of market volatility from $22 to $12 over the past year. That means we are getting paid half of what we were a year ago for the same options trade. You can make up for this loss of volatility by getting more aggressive with strike prices or maturities, but then that increases the number of stop losses.

And that’s the way it is.

You trade the market you have, not the one you want. But what do I know? I’ve only been doing this for 55 years.

I just thought you’d like to know.

NVIDIA Quarterly Earnings

So far in March, we are down -1.44%. My 2024 year-to-date performance is at +6.67%. The S&P 500 (SPY) is up +7.93% so far in 2024. My trailing one-year return reached +41.09% versus +38.92% for the S&P 500.

That brings my 16-year total return to +684.56%. My average annualized return has recovered to +51.57%.

Some 63 of my 70 round trips were profitable in 2023. Some 13 of 19 trades have been profitable so far in 2024.

I stopped out of my short position in Freeport McMoRan (FCX) last week. Markets that go straight up are hard to trade. I also came off my long in (TLT) close to cost. I initiated new longs in Tesla (TSLA) and NVIDIA (NVDA). I let my existing longs run in Freeport McMoRan (FCX), Occidental Petroleum, ExxonMobile (XOM), Wheaton Precious Metals (WPM), and Gold (GLD).

I am 70% invested and 30% in cash given the massive upside breakout in commodity, precious metals, and energy we have witnessed.

Nonfarm Payroll Jumps by 303,000 in March, almost double what was expected. The headline unemployment rate drops 0.1% to 3.8%. Wages rose 0.3% for the month and 4.1% from a year ago, both in line with Wall Street estimates. Health care led with 72,000 new jobs, followed by government (71,000), leisure and hospitality (49,000), and construction (39,000). Interest rate cuts fade into the future.

Weekly Jobless Claims Jump to 221,000, up 9,000, a two-month high. The weekly claims report from the Labor Department on Thursday also showed fewer people remaining on jobless rolls towards the end of March, suggesting that laid-off workers continued to find work, though not as easily as two years ago. There were 1.36 job openings for every unemployed person in February compared to 1.43 in January. Worker shortages persist in industries like construction.

Investors are Piling into Cash, with Money-Market funds getting $82 billion in the week through Wednesday. Investors are still flocking to cash funds, and history suggests redemptions won’t begin until a year after the Federal Reserve starts cutting interest. 5.35% for 90-day US Treasury Bond yields are still a huge draw for the cautious.

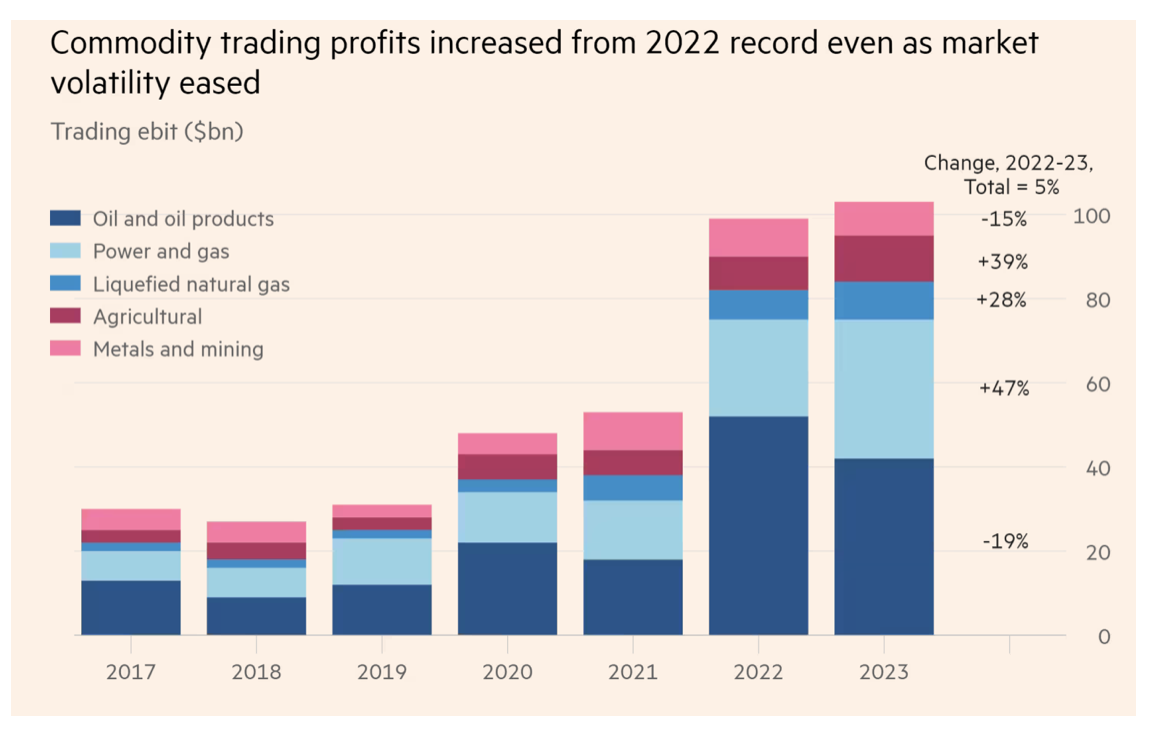

Commodities Trading Firms Harvest Record Profits, some $104 billion in 2023. The surprise increase from 2022, when the fallout from the war in Ukraine pushed up prices and supercharged profits, was driven by a wave of new entrants into the sector — including tech-focused traders and hedge funds — and rising returns from power trading activities. The figures reflect profits from the entire sector, including independent traders, banks, hedge funds, and national oil companies. This year will be even better.

Oil Continues to Bubble of Tight Supplies, supported by geopolitical tensions in the Middle East, concerns over tightening supply, and expectations about demand growth as economies improve. I’m keeping my longs in (XOM) and (OXY) and looking to pick up (COP) and (FANG).

US Dollar to Stay Higher for Longer, as a result of the higher for longer Fed tilt on interest rates. High-yielding currencies are always the strongest. The buck is up 3.3% this year against a currency basket.

Toyota Sales Soar by 20% in Q1, closely followed by Honda at 17.3%. General Motors delivered a pitiful 1.5% decline. Hybrids are the name of the day, outselling EVs and ICE cars. Toyota played it safe and won, at least for now.

Disney Wins Proxy Fight with Nelson Peltz, retaining complete control of the board. It’s a defeat for Peltz and a stamp of approval for the company’s board and CEO Bob Iger’s efforts to turn around the company. Nelson can now sell his shares for a big profit, up 30%.

PCE Comes in Hot at 0.3% for February, and 2.8% YOY, taking bonds. Personal Consumption Expenditures give an early read on inflation trends that the Fed loves. The economy is clearly much hotter than traders understand. Consumer spending shot up 0.8% on the month, well ahead of the 0.5% estimate. Personal income increased 0.3%, slightly softer than the 0.4% estimate.

Tesla Sales are Disastrous as expected, coming in at only 386,810, down 8.5% YOY. Shares drop as much as 6.7%, extending the biggest rout in the S&P 500. Analysts slashed projections in recent days, but not by enough. The Berlin factory was shut down and competition in China is ramping up. Still, Tesla produced 46,561 more cars than it sold in the quarter. For what it’s worth, BYD sales in China were even worse. The bottom for (TSLA) is fast approaching.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, April 8, at 7:00 AM EST, the US Consumer Inflations Expectations are announced.

On Tuesday, April 9 at 8:30 AM, the NFIB Business Optimism Index will be released.

On Wednesday, April 10 at 11:00 AM, the Core Inflation Rate for March is published

On Thursday, April 11 at 8:30 AM, the Weekly Jobless Claims are announced. The final read of the Q2 US GDP is also out.

On Friday, April 12 at 8:30 AM, the Producer Price Index is out. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, since many of you are now planning long overdue summer vacations, I thought I would pass on what I learned from the ultimate travel guru of all time.

After all, who knows how long it will be until the next pandemic? The next decade, next year, or next week?

When I backpacked around Europe in 1968, I relied heavily on Arthur Frommer’s legendary paperback guide, Europe on $5 a Day, which then boasted a cult-like following among impoverished, but adventurous Americans. The charter airline business was then booming, plunging airfares, and suddenly Europe came within reach of ordinary Americans like me.

Over the following years, he directed me down cobblestoned alleyways, dubious foreign neighborhoods, and sometimes converted WWII air raid shelters, to find those incredible travel deals. When he passed through town some 50 years later, I jumped at the chance to chat with the ever-cheerful worshipped travel guru.

Frommer believes there are three sea change trends going on in the travel industry today. Business is moving away from the big three travel websites, Travelocity, Orbitz, and Priceline, who have more preferential lucrative but self-enriching side deals with airlines than can be counted, towards pure aggregator sites that almost always offer cheaper fares, like Kayak.com, Sidestep.com, and Fairchase.com.

There is a move away from traditional 48-person escorted bus tours towards small group adventures, like those offered by Gap Adventures, Intrepid Tours, and Adventure Center, that take parties of 12 or less on culturally eye-opening public transportation.

There has also been a huge surge in programs offered by universities that turn travelers into students for a week to study the liberal arts at Oxford, Cambridge, and UC Berkeley. His favorite was the Great Books program offered by St. John’s University in Santa Fe, New Mexico.

Frommer says that the Internet has given a huge boost to international travel, but warns against user-generated content, 70% of which is bogus, posted by the hotels and restaurants touting themselves.

The 94-year-old Frommer turned an army posting in Berlin in 1952 into a travel empire that publishes 340 books a year, or one out of every four travel books on the market. I met him on a swing through the San Francisco Bay Area (his ticket from New York was only $150), and he graciously signed my tattered, dog-eared original 1968 copy of his opus, which I still have.

Which country has changed the most in his 60 years of travel writing? France, where the citizenry has become noticeably more civil since losing WWII. Bali is the only place where you can still actually travel for $5/day, although you can see Honduras for $10/day. Always looking for a deal, Arthur’s next trip is to Chile, the only country in the world he has never visited.

With the advent of AI, Arthur has been met with an onslaught of new competition. Recently, Amazon (AMZN) has been flooded with hundreds of new travel books written entirely by algorithms. They have no human author who’s ever visited the country in question and are written entirely from existing information found on the Internet. But they’re cheap.

You can easily spot them from their wishy-washy non-committal language and factual errors and omissions. For example, I recently found a travel book about Ukraine that neglected to mention that there was a war going on there and that its cities were being bombed by Russians daily.

Not for me.

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Arthur’s Next Big Play is Bali

1968 on the French Riviera

Global Market Comments

April 5, 2024

Fiat Lux

Featured Trade:

(APRIL 3 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (TLT), (GOLD), (GLD), (WPM), (NVDA), (OXY), (XOM)

Below please find subscribers’ Q&A for the April 3 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Key West, Florida.

Q: What’s going on with gold (GLD)?

A: Well it’s simple; gold hasn’t moved in a year and people want to rotate out of big tech into something that hasn’t moved. Gold has a great long-term story if interest rates fall and if central banks continue to accumulate gold. We could go up quite a lot from here; my goal right now is 3,000/oz by the end of next year.

Q: Are ETFs or single stocks a better buy right now?

A: ETFs are baskets, tend to have high fees, and tend to move at half the rate of single stocks. Single stocks can go up a lot faster and have a lot more risk. So if I have a strong feeling about a particular asset class like gold or silver, I'll go ahead and buy single stock names directly like Barrick Gold (GOLD) and Wheaton Precious Metals (WPM) because I know I’ll get a multiple of the performance of a basket of gold companies.

Q: Ford Motor Co. (F) seems like a better play than Tesla (TSLA) this year. What is your opinion?

A: You’re absolutely wrong, Tesla is a fantastic buy down here, once the EV nuclear winter ends. Tesla could rise a multiple from here—Ford probably not so much. Notice also that GM saw sales fall by 1.5% in the first quarter of this year. Tesla just has the technology; Ford and GM don’t. The long-term outlook for the ICE companies is grim. They have millions invested in internal combustion engine factories, which very soon will be worth nothing more than scrap metal.

Q: Do you have a long-term target on the downside for Tesla (TSLA)?

A: Well I’m currently long the April $140-$150 vertical bull call debit spread that expires in 10 days. To get a price lower than $140, you need to get drastically worse news, which I don't think we’ll get. I think we’re bottoming out right around here; Tesla’s already down 62% from an all-time high. During the pandemic, it dropped 80%.

Q: What is the chance that inflation returns, and what happens if it does?

A: Interest rates rise, and the Fed postpones interest rate cuts even further. However, I don’t think that’s going to happen, because technology and artificial intelligence are having such a huge deflationary impact on the economy that any bad news about inflation will be short-term, and we are in a long-term trend going down.

Q: How does falling Fed QT affect interest rates?

A: It causes them to go down because it means the Fed is selling less of its bond holdings into the market. This means they’re taking less money out of the financial system, meaning liquidity is increasing, which is good for all risk assets. I think the stock market has noticed this by going up almost every day so far this year. So, just as quantitative easing was great for the economy and the stock market, the quantitative tightening was terrible, and the fact that they’re ending it is good for all risk assets.

Q: Where do you see the price rising for iShares 20+ Year Treasury Bond ETF (TLT)?

A: 110 by the end of the year, but we might have another $1.00 or $2.00 of downside first. If you get down to $90 or so, I’ll be knocking out the trade alerts to buy call spreads as fast as I can write them. But first let’s let (TLT) find its new level, and interest rates find their new high.

Q: What is a barbell?

A: A barbell is where we have overweight sections in two parts of the market; one is technology and one is domestic recovery plays. We have nothing in most sectors in between. That’s what we’ve been doing for years, and it works pretty well because you always have something that’s going up. That’s why it’s called a barbell.

Q: If you were doing a new LEAP on Wheaton Precious Metals (WPM), what would you do?

A: I would do an at-the-money, which at this point would be June 2025 $50-$53 verticals bull call spread LEAPS, and I would go out at least a year, probably a year and a half because we’ve just had a very big run in Wheaton Precious Metals—about 25%. LEAPS are things you do at market bottoms, not at market tops. A reversal can be very expensive—they can literally go to zero on you.

Q: What do you think will be the next asset class investors will rotate into after commodities?

A: Big technology. We’re going to be going back and forth between the two sectors probably for years. So, I think tech needs a time correction of several months, where commodities and precious metals and energy will run free, and eventually, they’ll get overbought and want to take a rest, and then everyone rotates back into big tech. In the meantime, big tech and AI are moving forward with their technology.

Q: Why has Carnival Corp (CCL) had such a terrible stock performance, even though they’re having record sales and full ships?

A: They have huge amounts of debt leftover from the pandemic, which they got both from the government and the private sector. If they hadn’t done that, they’d have gone bankrupt, and it’s going to take a long time to pay off all that debt, even though it was at interest rates that were quite low. Plus, if they have to refinance any of that, that can get expensive too because the old loans are at zero or 1%, and the new loans are going to be like 6%, 7%, or 8%. So that has been a drag on Carnival Cruise Lines.

Q: What is a time correction?

A: A time correction is when the stock goes sideways for a period of time without going anywhere because nobody wants to sell it, everyone is bullish, and they’re willing to wait for the next leg up in the bull market. In the meantime, money rotates into other stocks that are moving, like commodities, precious metals, and energy.

Q: Should we take profits off of Barrick Gold (GOLD) after the recent runup, or does it have some more room to go into the upside?

A: Only if you’re a short-term trader do you want to take advantage of the recent run-up in Barrick Gold. I, however, think the stock could go up another $10 or $20 by the end of the year. I am quite happy to hold on. In fact, on any dips or weak days, I am adding to my position, not looking to run it down.

Q: What do you expect for oil prices?

A: I think we go to the top of the multi-year $62-$95 range and I’m going to run my longs in (XOM) and (OXY) until then.

Q: What do you think of Ken Griffin’s criticism of the US national debt growing at such a fast pace?

A: I’ve been hearing about the national debt for my entire life, since I was 3 years old and my grandfather would lecture me about the national debt, back when it was a pittance compared to what it is now. The fact is, growing national debt seems to have zero impact on any risk asset whatsoever. Stocks are at all-time highs, real estate is at all-time highs and rising, and the dollar is at all-time highs when rising debt was supposed to crush the dollar. The actual fact is that 80% of all the national debt was run up by Republican presidents, so to see Republicans complain about rising debt, especially our most recent president who increased it by $10 trillion is somewhat ironic. The fact s that the national debt is the result of four big tax cuts for billionaires that took place under Kennedy (1960), Reagan (1984), Bush (2002), and Trump (2017), so it’s also ironic that billionaires like Griffin and Paul Tudor Jones are complaining the loudest. They all sound like Cassandras—warning that the sky is falling, but it never seems to happen. In the meantime, I would buy bonds, because they’re not worried about national debt either.

Q: Can Bitcoin go higher after the halving in April?

A: No, the halving is in the price. All of the Bitcoin marketers have been selling you Bitcoin based on that halving for a year now. So the actual halving is going to be a classic “buy the rumor, sell the news” type move.

Q: What do you consider a dip?

A: It’s different for every stock depending on its volatility. It could be 5% for a boring stock, or 20% for something like Nvidia (NVDA).

Q: Does commercial real estate present a systematic risk to the financial markets?

A: No, commercial real estate is only 5% of the loan portfolios of the big banks, and maybe 1% of that will go under. It’s just a normal year of losses for the banks. As for regional banks, they’re the ones that will get hit; they’ll have to do deals to get bought up by the big banks. This is why I think we’re in the process of going from 4,000 banks in the United States to only 6.

Q: Is $100/barrel for oil back in play?

A: No, but $95 is, which is why I went long ExxonMobil (XOM) and Occidental Petroleum (OXY). So, it’s kind of late to get involved here on this trade, but if you are long oil, I would keep it and squeeze the last bit of juice out of those lemons.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 29, 2024

Fiat Lux

Featured Trade:

(A NOTE ON OPTIONS CALLED AWAY),

(TLT), (FCX), (XOM), (OXY), (WPM), (TSLA) (FCX)

Occasionally I get a call from Concierge members asking what to do when their short positions options were assigned or called away. The answer was very simple: fall on your knees and thank your lucky stars. You have just made the maximum possible profit for your position instantly.

We have the good fortune to have SEVEN spreads that are deep in the money going into the APRIL 19 option expiration. They include:

(TLT) 4/$87-$90 call spread

(FCX) 4/$37-$40 call spread

(XOM) 4/$100-$105 call spread

(OXY) 4/$59-$62 call spread

(WPM) 4/$39-$42 call spread

(TSLA) 4/$140-$150 calls spread

(FCX) 4/48-$51 put spread

In the run-up to every options expiration, which is the third Friday of every month, there is a possibility that any short options positions you have may get assigned or called away.

Most of you have short-option positions, although you may not realize it. For when you buy an in-the-money vertical option spread, it contains two elements: a long option and a short option.

The short options can get “assigned,” or “called away” at any time, as it is owned by a third party, the one you initially sold the put option to when you initiated the position.

You have to be careful here because the inexperienced can blow their newfound windfall if they take the wrong action, so here’s how to handle it correctly.

Let’s say you get an email from your broker telling you that your call options have been assigned away. I’ll use the example of the Freeport McMoRan (FCX) April 2024 $37-$40 in-the-money vertical BULL CALL debit spread.

What the broker had done in effect is allow you to get out of your call spread position at the maximum profit point 10 trading days before the April 19 expiration date. In other words, what you bought for $2.60 on March 4 is now $3.00!

All you have to do is call your broker and instruct them to exercise your long position in your (FCX) April 37 calls to close out your short position in the (FCX) April $40 calls.

This is a perfectly hedged position, with both options having the same expiration date, and the same amount of contracts in the same stock, so there is no risk. The name, number of shares, and number of contracts are all identical, so you have no exposure at all.

Calls are a right to buy shares at a fixed price before a fixed date, and one option contract is exercisable into 100 shares.

To say it another way, you bought the (FCX) at $37 and sold it at $40, paid $2.60 for the right to do so, so your profit is $0.40 cents, or ($0.40 X 100 shares X 40 contracts) = $1,600. Not bad for a 30-day defined limited-risk play.

Sounds like a good trade to me.

Weird stuff like this happens in the run-up to options expirations like we have coming.

A call owner may need to buy a long (FCX) position after the close, and exercising his long April $40 call is the only way to execute it.

Adequate shares may not be available in the market, or maybe a limit order didn’t get done by the market close.

There are thousands of algorithms out there that may arrive at some twisted logic that the calls need to be exercised.

Many require a rebalancing of hedges at the close every day which can be achieved through option exercises.

And yes, options even get exercised by accident. There are still a few humans left in this market to make mistakes.

And here’s another possible outcome in this process.

Your broker will call you to notify you of an option called away, and then give you the wrong advice on what to do about it. They’ll tell you to take delivery of your long stock and then most additional margin to cover the risk.

Either that, or you can just sell your shares on the following Monday and take on a ton of risk over the weekend. This generates oodles of commission for the brokers but impoverishes you.

There may not even be an evil motive behind the bad advice. Brokers are not investing a lot in training staff these days. It doesn’t pay. In fact, I think I’m the last one they did train 50 years ago.

Avarice could have been an explanation here but I think stupidity and poor training and low wages are much more likely.

Brokers have so many legal ways to steal money that they don’t need to resort to the illegal kind.

This exercise process is now fully automated at most brokers but it never hurts to follow up with a phone call if you get an exercise notice. Mistakes do happen.

Some may also send you a link to a video of what to do about all this.

If any of you are the slightest bit worried or confused by all of this, come out of your position RIGHT NOW at a small profit! You should never be worried or confused about any position tying up YOUR money.

Professionals do these things all day long and exercises become second nature, just another cost of doing business.

If you do this long enough, eventually you get hit. I bet you don’t.

Calling All Options!

Global Market Comments

March 25, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE BEST WEEK OF THE YEAR),

(PANW), (NVDA), (LNG), (UNG), (FCX), (TLT), (XOM), (AAPL), (GOOG), (MSTR), (BA), (FXY)

You need to have a sense of humor and a strong dose of humility to work in this market. After predicting last week that the market would NOT crash but grind sideways, it then posted the next week of the year. Stocks are actually accelerating their move to the upside.

Of course, we got a big assist from Fed Governor Jay Powell who practically wrote in his own blood a promise that interest rates would be cut at least three times by the end of the year. That is quite a gesture, and all risk assets loved it, even the ones that have been asleep for a year, like gold (GLD) and silver (SLV).

Miraculously, this does happen and there has been a big one over the last two years that nobody knows about.

Cheniere Energy (LNG) shipped 640 tankers full of natural gas (UNG) to Europe last year and 630 in 2022. One tanker provides enough gas to heat one million homes for a month. You can do the math. In total, it has sent out 3,400 tankers since 2016, mostly to China.

When Russia invaded Ukraine in 2022, Europe was totally dependent on Vladimir Putin for gas. Any doubt about the Russian supply was ended when the Nordstream undersea pipeline was mysteriously blown up. A total cut-off would have been an economic disaster and caused the collapse of NATO.

Two years ago, it was believed that even if we could get the gas to Europe, there were no facilities to liquefy natural gas as it is shipped back into natural gas. Then 16 floating de-liquefaction plants showed up out of nowhere.

Natural gas demand has been soaring in the US as well. Over the past 20 years, coal has dropped from generating 50% of the US electric power supply to only 19% (the unused American share of the coal was sold to China). That has eliminated 500 million tons of carbon dioxide from entering the atmosphere.

If you noticed that the skies over American cities are getting clearer, this is the reason.

Much has been made over Biden’s “pause” of permitting for new natural gas facilities. The reality is that it will take four years to build the 16 new gas export facilities that have already been approved. By then, we’ll have a new president. All Biden did was throw a bone at the environmental wing of his party. Such are the ways of Washington.

By the way, the Republican Party now has an environmental wing too. Who knew? It’s all proof that if you live long enough, you see everything.

One of the reasons I have been in love with cybersecurity stocks like Palo Alto Networks (PANW) for the past decade is that hacking is the ultimate growth industry. It never goes out of style, is recession-proof, and is growing at an exponential rate.

It is also getting more sophisticated. The big hackers are franchising their business models, inviting in criminals with minimal computer knowledge, vastly increasing their numbers. They are attacking small vendors to large companies to get access to the big ones. They are also picking targets too poor to afford the big cybersecurity companies. The City of Oakland is a classic example, which was prevented from paying its teachers for six months. And now they have AI.

Spending on cybersecurity is expected to grow from $188 billion in 2023 to $215 billion this year, a gain of 14.36%. The number of data breaches has rocketed by 78% over the past two years. Buy (PANW) on dips, which we are seeing right now.

“We’re going to need a bigger GPU” to borrow a famous line from Stephen Spielberg’s blockbuster Jaws.

If you want a peak at the future, both of our own and NVIDIA stock, check out the company’s latest entry into the chip wars, the $50,000 Blackwell GPU, available in a few months. In layman’s terms, it offers four times the computing ability but requires only one-quarter of the electric power, which is increasingly becoming an AI issue. It also uses deep learning to write its own software.

The chip was introduced by CEO Jensen Huang at the Developers conference in San Jose, which I attended in a venue normally occupied by rock stars. Huang started the conference by warning he was not there to sing. But perform he did, accompanied by a group of dancing robots powered by AI.

And while NVIDIA’s sales have tripled over the past year, you ain’t seen anything yet. When I recommended (NVDA) for the millionth time at $400 a share last October, my long-term target was $1,000. It recently hit $975, now stands at $943, and shows no sign of abating. NVIDIA could well keep powering on until the actual release of the Blackwell chip.

As in Jaws, I sense a feeding frenzy coming and (NVDA) shorts are the bait.

In February we closed up +7.42%. So far in March, we are up +3.53%. My 2024 year-to-date performance is at +6.67%. The S&P 500 (SPY) is up +9.22% so far in 2024. My trailing one-year return reached +56.98% versus +52% for the S&P 500.

That brings my 16-year total return to +683.30%. My average annualized return has recovered to +51.57%.

Some 63 of my 70 round trips were profitable in 2023. Some 11 of 19 trades have been profitable so far in 2024.

I miniated no new longs last week, content to let my existing longs run in Freeport McMoRan (FCX), bonds (TLT), and ExxonMobile (XOM). I am 70% in cash given the elevated state of the market and am looking for new commodity and energy plays to pile into.

Fed Chair Jay Powell Promises Three Interest Rate Cuts of 25 basis points each, at his press conference on Wednesday. Powell said he did not see "cracks" in the labor market, which he described as "in good shape," noting that "the extreme imbalances that we saw in the early parts of the pandemic recovery have mostly been resolved." These are very pro-risk statements. Buy the dips in everything.

Fed to Dial Back Quantitative Tightening, or QT from the current $120 billion a month. It’s a huge plus for risk assets and explains why the most liquidity-driven ones like gold and silver had such a great day. Buy (GLD) and (SLV) on dips.

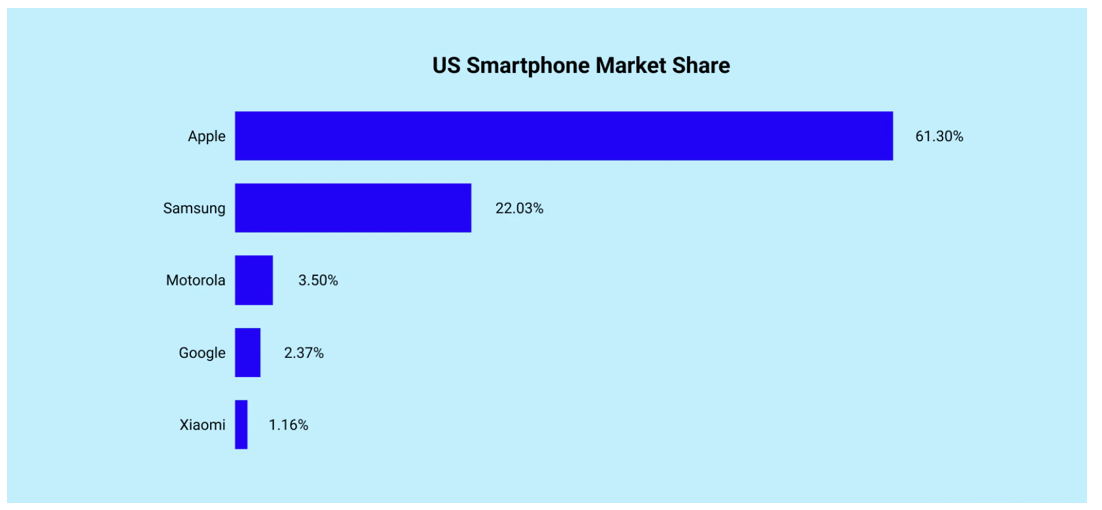

The Dept of Justice Goes After Apple on Antitrust, on its 61.3% share of the US smartphone market. It accused the iPhone maker of blocking rivals from accessing hardware and software features on its popular devices. Google’s (GOOG) Android actually has a bigger global market share at 70.3% with Apple at only 24%. This is another waste of time that will last ten years and go nowhere.

Bank of Japan to Cut Interest Rates as Early as April, bringing to an end a 34-year stimulus program that was a dismal failure. The Japanese yen (FXY) should rocket, but Japanese stocks not so much.

MicroStrategy (MSTR) Dives 18%, the largest owner of Bitcoin, on a crypto correction. MicroStrategy is the largest corporate owner of Bitcoin. (MSTR) just completed a massive borrowing to buy more crypto at the top. After SEC approval of ETFs and the imminent halving, what is left to drive crypto? Avoid (MSTR) which was blindsided by the last 90% crypto correction.

Existing Homes Sales Soar 9.7% in February to 4.38 million units, on a seasonally adjusted annualized basis. Inventory rose 5.9% year over year to 1.07 million homes for sale at the end of February. That represents a still low 2.9-month supply at the current sales pace. Higher demand continued to push the median price higher, up 5.7% from the year before to $384,500.

Home Prices Have Risen by 2.4 Times the Inflation Rate Since 1960. The cost of a typical house in the U.S. is nearly half a million dollars: the median price for a home in the U.S. is $412,778, according to Redfin data. That’s what successful demographic tailwinds leading to a chronic housing shortage get you.

Boeing is Leasing 36 Airbuses, to meet its own unfilled orders caused by production delays. Another panel fell off an airborne plane last week in Medford, OR. Looking for missing parts has become a regular part of every Boeing landing. This is an act of desperation. Avoid (BA)

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, March 25, at 7:00 AM EDT, the US Building Permits are announced.

On Tuesday, March 26 at 8:30 AM, S&P Case Shiller for February is released.

On Wednesday, March 27 at 11:00 AM, the MBA Mortgage Data is published

On Thursday, March 28 at 8:30 AM, the Weekly Jobless Claims are announced. The final read of the Q2 US GDP is also out.

On Friday, March 29 at 2:00 PM, Personal Income and Spending is out. The Baker Hughes Rig Count is printed.

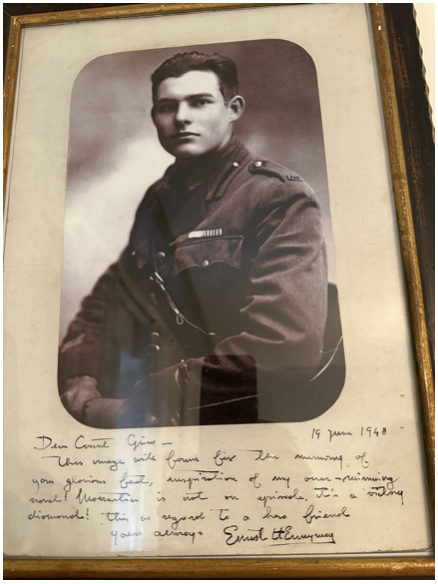

As for me, as I am about to take off for Cuba to visit Finca Vigia (Lookout Farm), the home of Earnest Hemingway and Martha Gellhorn I thought I’d review my long history with this storied family. This is where he finished For Whom the Bells Toll, his epic novel about the Spanish Civil War.

My grandfather drove for the Italian Red Cross on the Alpine front during WWI, where Hemingway got his start, so we had a connection right there going back over 100 years.

Since I read Hemingway’s books in my mid-teens, I decided I wanted to be him and became a war correspondent. In those days, you traveled by ship a lot, leaving ample time to finish off his complete work.

I visited his homes in Key West and Ketchum Idaho. In 2023, he stayed at his Hotel Poste room in Cortina, Italy where he lived for five months during the 1950s. His Cuban residence was high on my list, now that Castro is gone.

I used to stay in the Hemingway Suite at the Ritz Hotel on Place Vendome in Paris where he lived during WWII. I had drinks at the Hemingway Bar downstairs where war correspondent Ernest shot a German colonel in the face at point-blank range. I still have the ashtrays.

Harry’s Bar in Venice, a Hemingway favorite, was a regular stopping-off point for me. I have those ashtrays too.

I even dated his granddaughter from his first wife, Hadley, the movie star Mariel Hemingway, before she got married, and when she was still being pursued by Robert de Niro and Woody Allen. Some genes skip generations and she was a dead ringer for her grandfather. She was the only Playboy centerfold I ever went out with. We still keep in touch.

So, I’ll spend the weekend watching Farewell to Arms….again, after I finish this newsletter.

Oh, and if you visit the Ritz Hotel today, you’ll find the ashtrays are now glued to the tables.

Hemingway in 1917

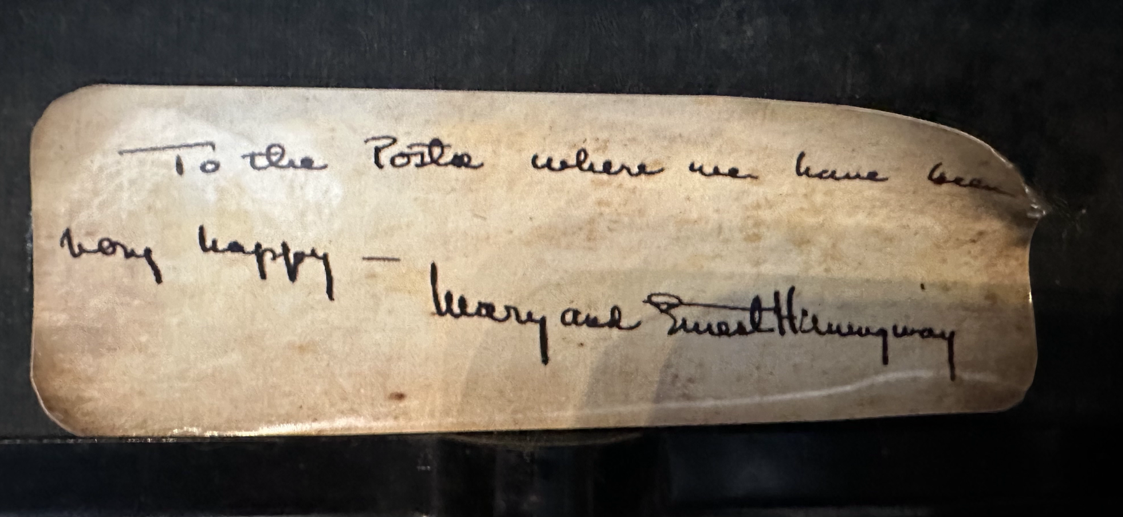

At Work on Hemingway’s Typewriter

Good Luck and Good Trading,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader