Global Market Comments

October 22, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or HEADING FOR LAKE TAHOE),

(SPY), (TLT), (VIX), (MSFT), (AMZN), (CRM), (ROKU),

(BRING BACK THE UPTICK RULE!)

Global Market Comments

October 22, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or HEADING FOR LAKE TAHOE),

(SPY), (TLT), (VIX), (MSFT), (AMZN), (CRM), (ROKU),

(BRING BACK THE UPTICK RULE!)

There’s nothing like a quickie five-day tour of the Southeast to give one an instant snapshot of the US economy. The economy is definitely overheating and could blow up sometime in 2019 or 2020.

Traffic everywhere is horrendous as drivers struggle to cope with a road system built to handle half the current US population. Service has gotten terrible as workers vacate the lower paid sectors of the economy. Everyone you talk to tells you business is great, from the CEOs down to the Uber drivers.

I managed to miss Hurricane Michael by two days. Hartsfield Jackson Atlanta International Airport was busy with exhausted transiting Red Cross workers. The Interstate from Savanna to Atlanta, Georgia was lined with thousands of downed trees. In Houston mountains of debris were evident everywhere, the rotting, soggy remnants of last year’s Hurricane Harvey.

I managed to score all day parking in downtown Atlanta for only $8. I kept the receipt to show my disbelieving friends at home.

Bull markets climb a wall of worry and this one has been no exception. However, the higher we get the greater the demands on the faithful.

Last week saw my Mad Hedge Market Timing Index plunge to an all-time low reading of 4. I back-tested the data and was stunned to discover that October saw the steepest selloff since the 1987 crash, which saw the average crater 21% in one day.

And while evidence of a coming bear market is everywhere, the reality is that stocks can keep rising for another year. Market bottoms are easy to quantify based on traditional valuation measure, but tops are notoriously difficult to call. Look for one more high volume melt up like we saw in January and that should be it.

Real interest rates are still zero (3.2% bond yields – 3.2% inflation), so there is no way this is any more than a short-term correction in a bull market.

The world is still awash in liquidity

The Fed says they’re still raising rates four times in a year no matter what the president says. Look for a 3.25% overnight rate in a year, and 4% for three months funds. If inflation rises to 4% at the same time, real rates will still be at zero.

There certainly has not been a shortage of things to worry about on the geopolitical front. After Saudi Arabia was caught red-handed with video and audio proof of torturing and killing a Washington Post reporter, it threatened to cut off our oil supply and dump their substantial holding of technology stocks.

Tesla made another move towards the mass market by accelerating its release of the $35,000 Tesla 3. Production is now well over 6,000 units a month.

If you had any doubts that housing was now in recession, look no further than the September Existing Home Sales which were down a disastrous 3.5%. In the meantime, the auto industry continues to plumb new depths. In some industries, the recession has already started.

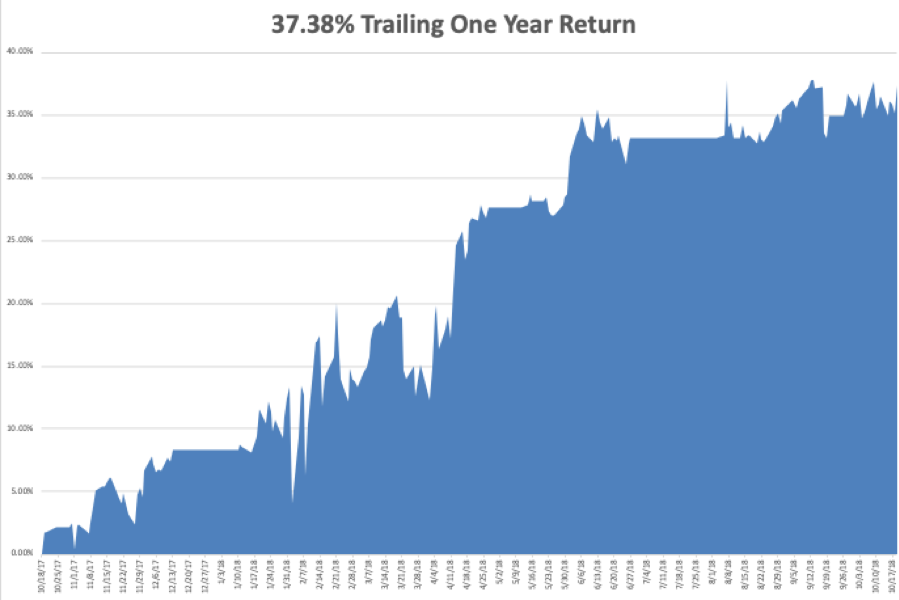

We have been killing it on the trading front. My 2018 year-to-date performance has bounced back to a robust 29.07%, and my trailing one-year return stands at 35.37%. October is up +0.68%, despite a gut-punching, nearly instant NASDAQ swoon of 10.50%. Most people will take that in these horrific conditions.

My single stock positions have been money makers, but my short volatility position (VXX), which I put on early, refuses to go down, eating up much of my profits.

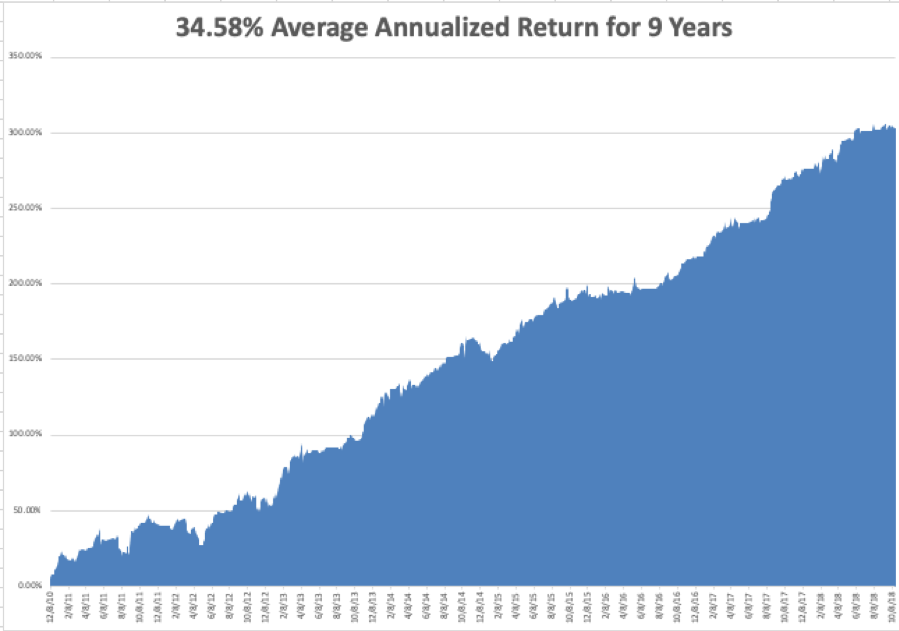

My nine-year return appreciated to 305.54%. The average annualized return stands at 34.58%. Global Trading Dispatch is now only 44 basis points from an all-time high.

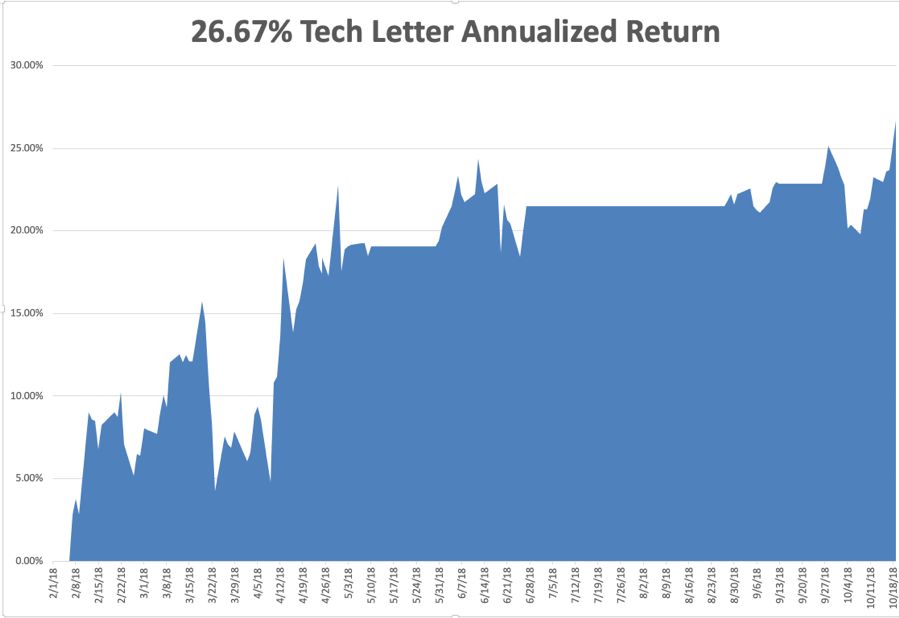

The Mad Hedge Technology Letter has done even better, blasting through to a new all-time high at an annualized 26.67%. It almost completely missed the tech meltdown and then went aggressively long our favorite names right at the market bottom.

I’d like to think my 50 years of trading experience is finally paying off, or maybe I’m just lucky. Who knows?

This coming week will be pretty sedentary on the data front, with the Friday Q3 GDP print the big kahuna. Individual company earnings reports will be the main market driver.

Monday, October 22 at 8:30 AM, the Chicago Fed National Activity Index is out. 3M (MMM), and Logitech (LOGI) report.

On Tuesday, October 23 at 10:00 AM, the Richmond Fed Manufacturing Index is published. Juniper Networks (JNPR), Lockheed Martin (LMT), and United Technologies report.

On Wednesday, October 24 at 10:00 AM, September New Home Sales will give another read on entry-level housing. At 10:30 AM the Energy Information Administration announces oil inventory figures with its Petroleum Status Report. Advanced Micro Devices (AMD), Ford Motor (F), and Microsoft (MSFT) report.

Thursday, October 25 at 8:30, we get Weekly Jobless Claims. Alphabet (GOOGL) and Intel (INTC) report.

On Friday, October 26, at 8:30 AM, a new read on Q3 GDP is announced.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I am headed up to Lake Tahoe this week to host the Mad Hedge Lake Tahoe Conference. The weather will be perfect, the evening temperatures in the mid-twenties, and there is already a dusting of snow on the high peaks. The Mount Rose Ski Resort is honoring the event by opening this weekend.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

October 15, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or OUR HARD LANDING BACK ON EARTH),

(SPY), (QQQ), (TLT), (VIX), (VXX), (MSFT), (JPM), (AAPL),

(DECODING THE GREENBACK),

(DUMPING THE OLD ASSET ALLOCATION RULES)

Truth be told, it’s the really boring, sedentary, go-nowhere markets that drive me nuts, cause me to tear my hair out, and urge me on to an early retirement.

The week started with such promise.

Sunday night I witnessed the first Space X landing of a rocket in California which I could clearly see from the top of Berkeley’s Grizzly Peak some 250 miles away. It was fascinating to see four separate jets steer the spacecraft earthward.

Financial markets had a different landing in mind, the hard kind, if not a crash.

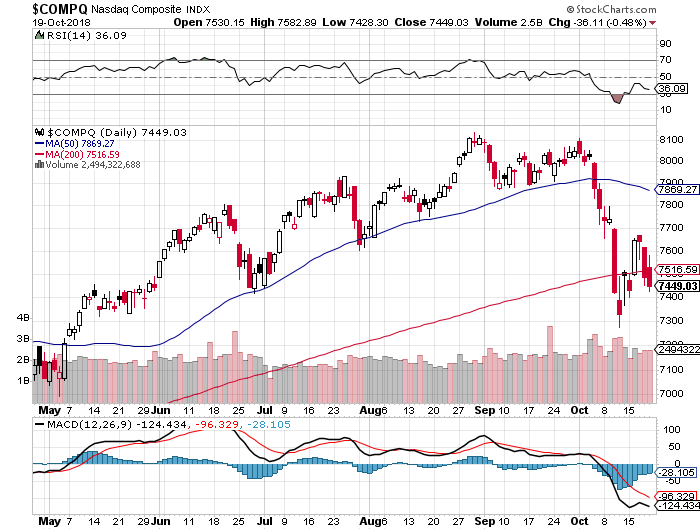

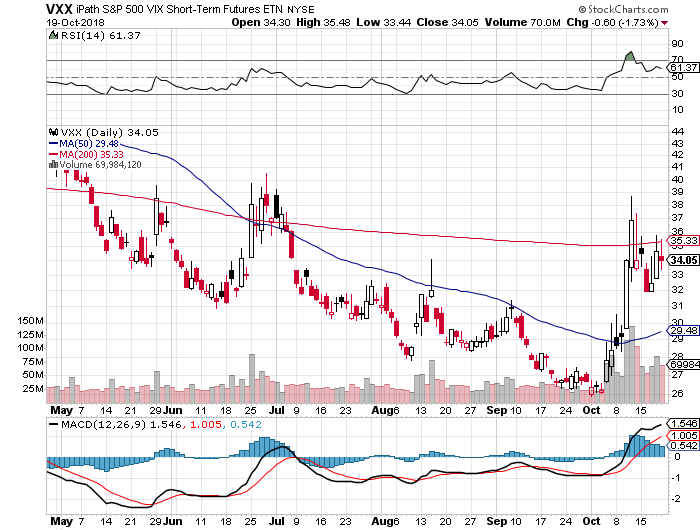

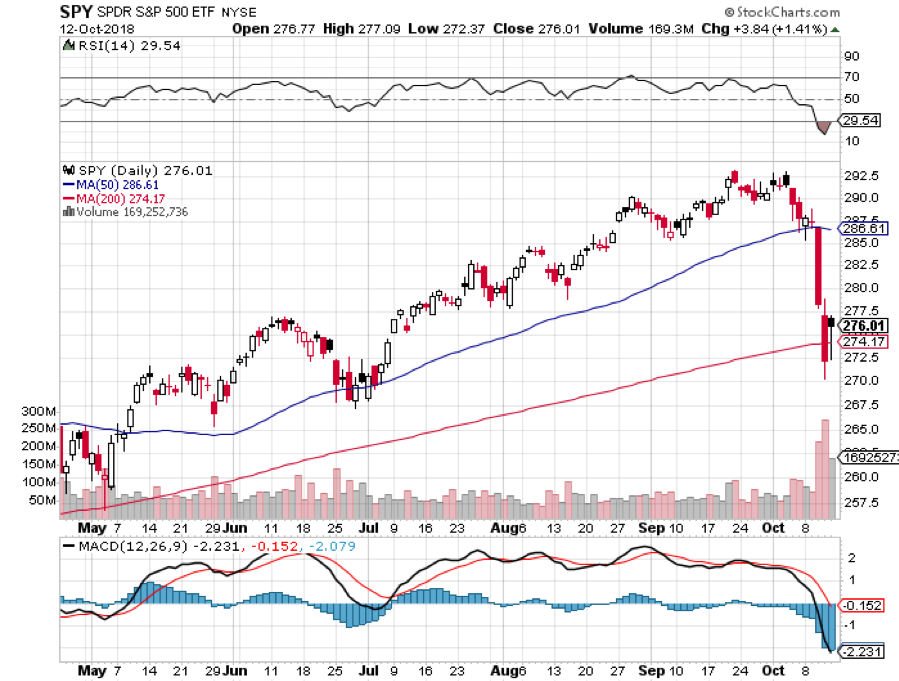

I absolutely love the market we had last week which saw the third biggest down day in history, volatility explode, and $2.6 trillion in stock market capitalization vaporize.

I had to blink when I saw NASDAQ (QQQ) down an incredible 350 points in one day. My Mad Hedge Market Timing Index hit an all-time low at 4.

No wonder insider selling hit $10.3 billion in August, another record. Maybe they know something we don’t.

Chinese Gamer Tencent Postponed their US IPO. It seems they noticed that market conditions had become unfavorable. I know investment bankers hate passing on an opportunity to ring the cash register. I used to be one.

There is no better feeling than being 100% cash going into one of these crashes and then having panicked investors puke their best quality positions to me at a market bottom.

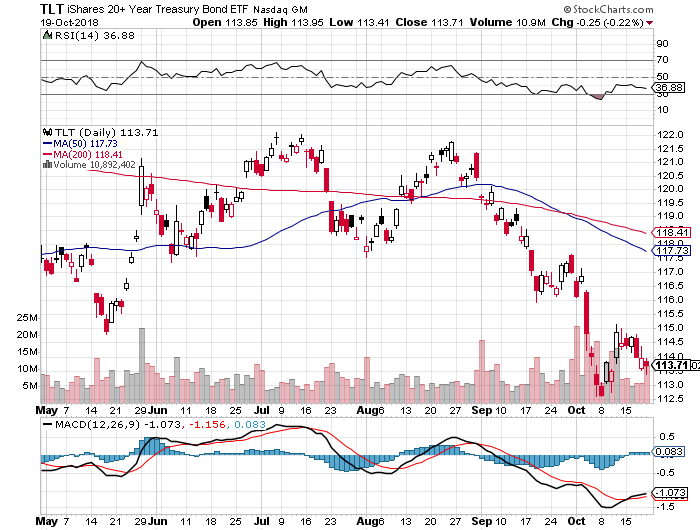

On Thursday, I backed up the truck and issued four perfectly timed Trade Alerts, picking up Microsoft (MSFT), Apple (AAPL), and the S&P 500 (SPY), and covering my short position in the bond market (TLT).

In fact, I believe I had my best week of the year even though I only added modestly to my annual return. Look at the charts below and you’ll see that I suffered a 9% drawdown during the February meltdown. Maybe I’m getting wiser as I get older? One can only hope.

This time, I managed to limit my loss to a modest 2.5% and am nearly unchanged on the month despite the Dow Average at one point nearly giving up all its gains for 2018. This is also against a horrific backdrop of hedge fund performance that is now showing losses for 2018.

The Volatility Index (VIX) made a move for the ages, at one point kissing the $29 handle, up from $11 two weeks ago. During the 600-point swoosh down on Thursday, I couldn’t get any of my staff on the phone. The entire company was logged into their personal trading accounts, buying puts on the iPath S&P 500 VIX Short-Term Futures ETN (VXX) as fast as they could.

Which leads me to believe that the bottom is near. Earnings and valuation support start kicking in big time at these levels, and the blackout period for company share buybacks started ending with the bank earnings last Friday.

When you take a $1 trillion buyer out of the market, it has a huge effect no matter how strong the fundamentals are. Start buying those dips. Their return is similarly eventful. I’ve already started to invest my 95% cash position.

Further eroding confidence was the president’s statement that the Federal Reserve is crazy. So, now we know the president appoints crazy people to the most important financial positions in the country. White House control of interest rates ahead of elections. Why didn’t I think of that?

Sparking the Friday melt-up was a statement by JP Morgan (JPM) CEO Jamie Diamond saying that a 40-basis point rise in rates is no big deal. The bull market is on. His earnings beat all expectations.

My 2018 year-to-date performance has bounced back to 27.56%, and my trailing one-year return stands at 35.87%. October is almost flat at -0.84%. Most people will take that in these horrific conditions.

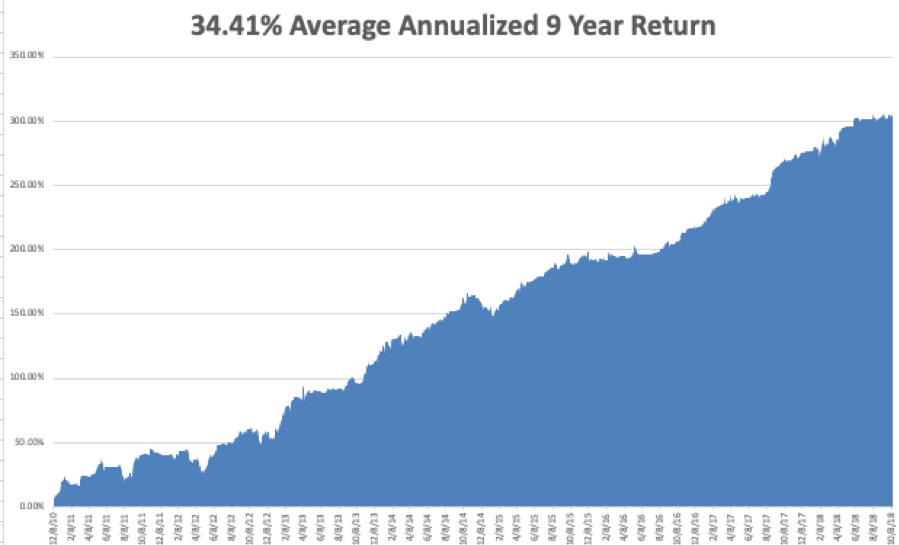

My nine-year return appreciated to 304.03%. The average annualized return stands at 34.41%.

This coming week will be pretty sedentary on the data front.

Monday, October 15 at 8:30 AM brings us September Retail Sales.

On Tuesday, October 16 at 9:15 AM, September Industrial Production is announced.

On Wednesday, October 17 at 8:30 AM, September Housing Starts are published.

Thursday, October 18 at 8:30, we get Weekly Jobless Claims. At 10:00 we learne the September Index of Leading Economic Indicators.

On Friday, October 19, at 10:00 AM, the September Housing Starts are out. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I will spend this week on my Southeastern US roadshow, giving strategy luncheons in Savannah, GA, Atlanta, GA, Miami, FL, and Houston, TX. I love meeting my readers mano a mano who are often a source of my best trading ideas. It looks like I’ll miss Hurricane Michael by three days.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

October 8, 2018

Fiat Lux

Featured Trade:

(A LONG-AWAITED BREATHER IN TECHNOLOGY),

(AMZN), (TGT), (NVDA), (SQ), (AMD), (TLT)

Taking profits - it was finally time.

The Nasdaq has been hit in the mouth the last few days and rightly so.

It was the best quarter in equities for five years, and a quarter that saw tech comprise up to a quarter of the S&P demonstrating searing strength.

It would be an understatement to say that tech did its part to drive stocks higher.

Tech shares have pretty much gone up in a straight line this year aside from the February meltdown.

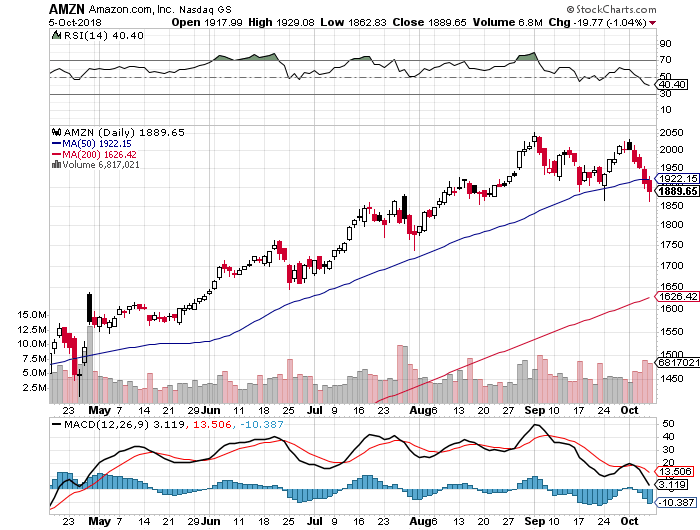

Even that blip only caused Amazon (AMZN) to slide around 10%.

After all the terrible macro news thrown on the market in spades – tech stocks held their own.

Not even a global trade war with the second biggest economy in the world which is critical to exporting products to America was able to knock tech shares off their perch.

At some point, 26% earnings growth cannot sustain itself, and even though the tech narrative is still intact, investors need to breathe.

Let’s get this straight – tech companies are doing great.

They benefit from a secular tailwind with every business pivoting to mobile and software services.

All that new business has infused and invigorated total revenue.

The negative reaction by technology stocks was based on two pieces of news.

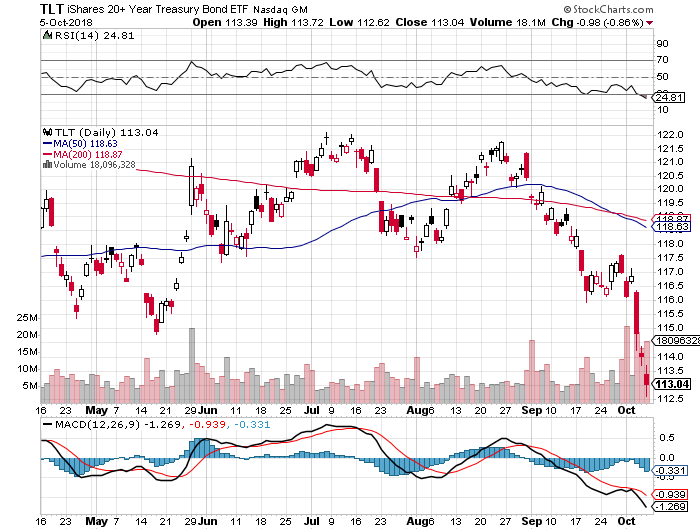

Interest rates (TLT) surging to over 3.2% was the first piece of news.

The increase in rates reinforces that the economy is humming along at a breakneck speed.

Yields are going up for the right reasons and this economy is not a sick one indeed.

As rates rise, other asset classes become more attractive such as CD’s and bonds.

The whole world is looking at the pace of rate rises because this will affect the ability for tech behemoths to borrow money to invest in their expensive well-oiled machines.

Three things are certain - the economy is hot, the smart money is buying on the dip now, and Amazon will still take over your home.

Even in a rising rate environment, Amazon is fully positioned to outperform.

The second catalyst to this correction was Amazon’s decision to hike its minimum wage to $15 per hour.

This could lay the path for workers around the country to demand higher pay.

The move was a misnomer as it will eliminate stock awards and monthly bonuses lessening the burden that Amazon actually has to dole out.

Call this a push – the rise in expenses won’t be material and realistically, Amazon can afford to push the wage bill by another order of magnitude, even though they will not.

This was also a way for Amazon founder Jeff Bezos to keep Washington off his back for a few months, and his generous decision was praised by government officials.

The wage hike underscores the strength of the ebullient American economy, and the consumer will benefit by recycling their wages back into Amazon and the wider economy.

Amazon makes up 50% of American e-commerce sales, and when workers are buying goods online, a good chance its coming from Amazon.

In an environment of full employment, the natural direction of wages is up, and this was due to happen.

You can also look at wage inflation as employees gaining at the expense of the corporation.

However, the massive deflationary trends of technology will also make this wage hike quite irrelevant over time as Amazon will automate more of their supply chain to make up for any wage hike that could damage revenue.

Amazon’s economies of scale give the Seattle-based company enough levers and buttons to push and pull to dilute expenses to make this a non-issue.

Each earnings call usually involves CFO of Amazon Brian Olsavsky explaining the acceleration of efficiencies in fulfilment centers bolstering the bottom line.

The stellar innovation in operational expertise moves up a level each quarter if not two levels.

Ultimately, though expensive on the surface, this won’t affect Amazon’s numbers at all, but more critically please the lower tier of workers who fight and scratch for their daily crust of bread.

This win-win scenario casts a positive image of Bezos in the public eye at a crucial time when he plans to recruit another legion of Amazon workers, as Amazon will shortly announce the location of their second American-based headquarter.

In fact, this turns the screws on the smaller retailers who must match the $15 per hour wage or confront a potential disaster of an entire workforce walking out and joining Amazon.

The mysterious Amazon-effect works in many shapes and sizes.

Big retailers like Target (TGT) have griped that it’s near impossible to find seasonal workers for the upcoming holiday season.

Moreover, if inflation remains moderate but contained – technology will power on.

And it will take more than a few prints of rising inflation to impress the Fed enough to expedite the raising of rates.

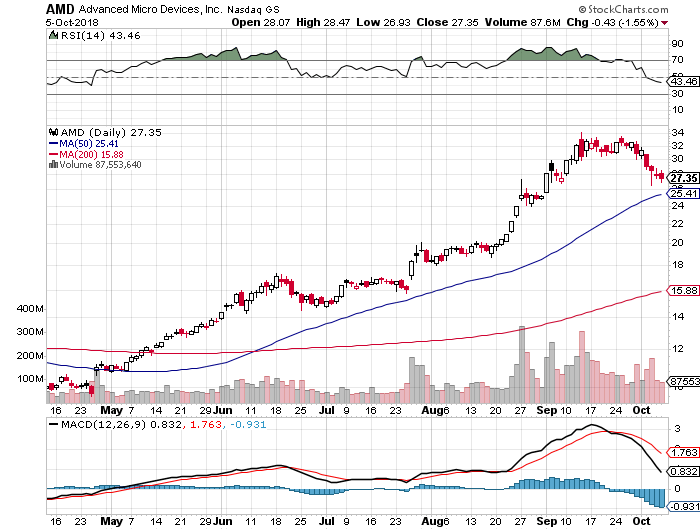

But it is safe to say that investors cannot expect the 100% up moves like in Amazon and Advanced Micro Devices (AMD) in one calendar year moving forward.

Technology has a plate full of challenges facing its share price as we move into the latter part of the fiscal year.

The challenges are two-fold - mid-term elections and navigating a smooth year-end.

Earnings should be good which is already baked into the pie, and the benefits of the tax cut have already worked itself through the system.

The furious pace of share buybacks will eventually subside too.

Management might finally bring out the spin doctors claiming the stronger dollar and worsening trade war is the reason to guide down.

At least tech companies doing business in China might follow this playbook.

Either way, tech shares are demonstrably sensitive right now and while the market needs tech to lead the way, the sector is exhausted from the burden of carrying the bulk of the load.

Freak-outs on rate surges have been a common experience for those old hands presiding over markets for decades.

These are all the staples of a 9th year bull market.

Typical late stage topping action is normal in economic cycles.

After the dust settles, the overreaction will give way to great buying opportunities at great prices, albeit it in the higher quality names.

The chip sector is still one to avoid unless the names are Advanced Micro Devices or Nvidia (NVDA).

Legacy companies have always been a no-go.

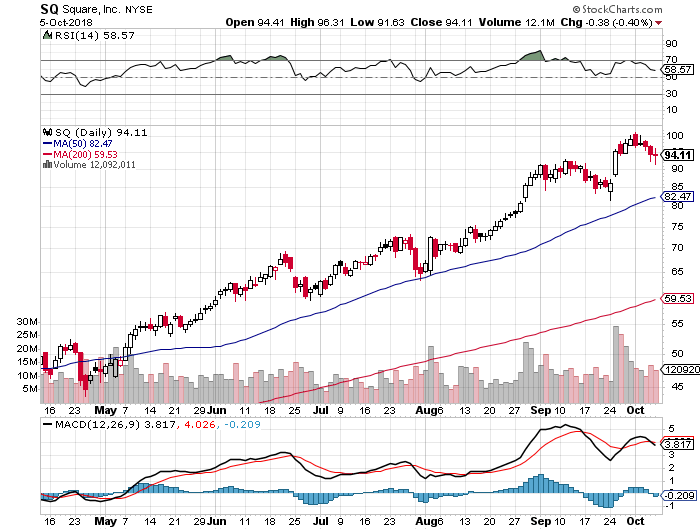

If you want hyper-growth, fin-tech name Square (SQ) would be an ideal candidate.

If buy and hold is your cup of tea, any 10% discount would be a great entry point in any of these quality companies.

Global Market Comments

October 5, 2018

Fiat Lux

Featured Trade:

(WEDNESDAY OCTOBER 17 HOUSTON STRATEGY LUNCHEON INVITATION),

(OCTOBER 3 BIWEEKLY STRATEGY WEBINAR Q&A)

(SPY), (VIX), (VXX), (MU), (LRCX), (NVDA), (AAPL), (GOOG), (XLV), (USO), (TLT), (AMD), (LMT), (ACB), (TLRY), (WEED)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader October 3 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: Will the market keep increasing for the rest of the year?

A: We haven’t had the pullback yet, so the short answer is yes. My yearend target of and S&P 500 (SPY) for the end of 2018 still stands. You can’t argue with the immediate price action. That said, the market is wildly overbought for the medium term and is approaching valuation levels we haven’t seen since the Dotcom peak in 2000. That why I am running a 70% cash trading book now.

Q: Should I be buying the Volatility Index (VIX) here?

A: Look at the bottom where we broke back in August, if we go down there and sit for a couple of days, then go out and buy the March 2019 $40 iPath S&P 500 VIX Short-Term Futures ETN (VXX) calls—way out of the money, way far in the future—and that way if you get any bounce in the (VIX) in the next 6 months, you’ll make a ton of money on that. You can buy them today for 50 cents. Plus, we could get one of these situations where there’s a major selloff once we’re into the new year, so a 6-month (VXX) call option would hedge that.

Q: Given the choice of Apple (AAPL) or Google (GOOG), which would you buy?

A: If you’re a conservative, old lady, widow and orphan type, you’d probably want to buy Apple— it’s almost turned into a utility, it’s so reliably safe, going up and has a nice dividend. If you want to be aggressive, swinging for the fences young stud and are looking for a double, I would go with Google—much higher growth pattern, pays no dividend and has had a 3-month consolidation going sideways. The only thing that could hurt this company would be government regulation, but with the Democrats possibly taking control of Congress in November, the prospect of government regulation of the entire technology sector could rapidly fade away.

Q: When should I get into Health Care (XLV)?

A: I think you have to wait at this point. To me, it’s tremendously overbought at the moment, but is still enjoying a long-term bull move. This is one of my two favorite sectors in the entire market. It has been rising for four months now, even though the Trump threat of price cuts are constantly overhanging the market.

Q: Is oil (USO) going to 100?

A: Because of the disruptions caused by the Iran sanctions and the tearing up of the Iran Nuclear Treaty, Trump has created a short squeeze in oil prices. He is threatening to boycott any country that buys oil from Iran, so Iran is shipping their oil through China, which is already under sanctions itself. However, that is easier said than done. The oil business is much more complicated than people realize. For China to take Iranian oil, they literally have to build new refineries from scratch to process the crude from Iran; no two crudes are alike. When you build a major supply, you have to build refineries to match that, and you have to get it there. This market will eventually stabilize, but in the meantime, there is a big short squeeze going on in Europe.

Q: Do you see the economy going strong into the end of the year?

A: Yes, I do—we still have the tax cuts, global liquidity, and deregulation kicking in, and those things will all work until the end of the year. I think we close at the highs of the year, and after that we’re going to have to start to work hard for our money once again in 2019. The US economy is like a supertanker; it takes a long time to turn it around.

Q: Will the interest rate spike kill the market?

You think? Investors are so used to ultra-low interest rates that a transition to normal rates will be traumatic. Next Friday, we get Core CPI, and if that comes in hot we could see another spike to 3.35% in the ten-year US Treasury bond (TLT). There are now a ton of people desperate to get out of their bond holdings at last week’s prices. This is why I have been selling short the bond market for the past three years and selling as recently as Monday. The next leg down in a 30-year bear market has begun.

Q: Advanced Micro Devices (AMD) has shot over $30—would you sell it?

A: We love the company long term but short term it is just way overdone; take the double and run, and then buy back on the next dip.

Q: Are you still bearish on the chip company?

A: Short term yes, long term no. This sector is now totally driven by the trade war with China. This includes NVIDIA (NVDA), Micron Technology (MU) and LAM Research (LRCX). Lam is particularly exposed because they had ordered to sell ten entire chip factories to China which is now on hold. That said, the day the trade way ends these stocks will all start a 50% run up. If China gets the same free pass and symbolic treaty that Canada did, that could happen sooner than later. If you can’t sleep at night until then, cut your position in half. If you still can’t sleep, cut it again.

Q: Do you think Lockheed Martin (LMT) is a buy Here at $350?

A: No, there is a double top risk for the stock right here. And if the Democrats get control of congress, the whole Trump trade could unwind. That would give the opposition the purse strings and the first thing they’ll do is cut defense spending, which Trump bumped up by $50 billion.

Q: Do you have any views on pot stocks like Aurora Cannabis (ACB), Tilray (TLRY) and (WEED)?

Stay away in droves. They’re this year’s bitcoin stocks. It’s still illegal. That’s why these companies are all based in Canada. And after all it’s a weed. How hard is it to grow? The barriers to entry are zero.

Global Market Comments

October 4, 2018

Fiat Lux

Featured Trade:

(TUESDAY OCTOBER 16 MIAMI GLOBAL STRATEGY LUNCHEON),

(BONDS FINALLY BREAK TWO-YEAR RANGE),

(TLT), (TBT), ($TNX)

I love executing one day wonders.

Since we sold short the US Treasury bond market on Monday, it has plunged a stunning 3 points. Bond yields just performed a rare 10 basis point move up to 3.18%. You usually only see that during a major “RISK OFF” geopolitical event or financial crisis.

You could see all of the key support levels failing like a hot knife for butter. The next support for the United States Treasury Bond Fund (TLT) is now at $111, or some 2.5 points down from here, pointing to a 3.25% yield for the ten-year bond.

My yearend forecast of a ten-year yield of 3.25% and a one-year target of 4.0% is alive and well.

The break marks an important departure from a stubborn two-year trading range….to the downside.

As with major breaks there is not a single a data point that broke the camel’s back. It could have been the agreement to NAFTA 2.0 on Monday or the blistering hot ISM Services print at a 21-year high on Wednesday.

Rather, it has been a steady death by a thousand cuts spread over several points that did it. It was just a matter of time before a 4.2% GDP growth rate crushed the fixed income market.

If I had to point to one single thing that triggered this debacle, it would be Amazon’s (AMZN) decision to give a 25% raise to its 250,000 US employees to $15 an hour.

If Wal-Mart (WMT), McDonald’s (MCD), or Target (TGT) have to resort to the same, you could have a serious outbreak of inflation on 2019. Imagine that, a bidding war for minimum wage workers.

ALL of those costs will be passed on to us, which is highly inflationary, and bonds absolutely HATE inflation.

Other than giving us boasting rights, the bond market move carries several important messages for us.

Money is about to start transferring from borrowers to savers in a major way. You won’t hear about seniors unable to live off of their savings anymore, a common refrain of the past decade.

Cash is now offering a serious competitor to bond and equity investments. And the next recession and bear market have just been moved closer.

The rocketing US budget deficit is starting to bear its bitter fruit as the government is starting to crowd out private sector borrowers. The budget deficit should be running at a $1 trillion annualized rate by the end of this year.

All of you celebrating your windfall tax cuts are getting a sharp reminder that the money has been entirely borrowed, some 40% from foreign bond investors we have been attacking. It will have to be paid back some time.

Of course, we all knew this was coming. It is no accident that the most capital-intensive industries in the country, also the heaviest borrowers, have seen the worst stock performance of 2018 including real estate, REITS, steel, and autos. Their profit margins have all just been seriously chopped.

So, what to do about the bond market now that we have begun the next leg in a 30-year bear market? For a start, don’t sell. Rather, wait for the next rally back up to the old support level at $116. It should revisit the old support level at least once.

When it does, SELL WITH BOTH HANDS.