Global Market Comments

June 23, 2020

Fiat Lux

Featured Trade:

(HERE ARE THE FOUR BEST PANDEMIC-INSPIRED TECHNOLOGY TRENDS),

(AMZN), (CHWY), (EBAY), NFLX), (SPOT), (TMUS), (ATVI), (V), (PYPL), (AAPL), (MA), (TDOC), (ISRG), (TMDI)

Global Market Comments

June 23, 2020

Fiat Lux

Featured Trade:

(HERE ARE THE FOUR BEST PANDEMIC-INSPIRED TECHNOLOGY TRENDS),

(AMZN), (CHWY), (EBAY), NFLX), (SPOT), (TMUS), (ATVI), (V), (PYPL), (AAPL), (MA), (TDOC), (ISRG), (TMDI)

By now, we have all figured out that the pandemic has irrevocably changed the course of technology investment. Some sectors are enjoying incredible windfalls, while others are getting wiped out.

The digitization of the economy has just received a turbocharger. It has become a stock pickers market en extemus.

The good news is that we are still on the ground floor of trends that have a decade to run, like working from home, more online food purchases, and a rise in touchless payments. This means there's a huge upside for investors willing to make big bets on what’s expected to become some of the most important technologies in the years ahead.

Covid-19 is a wake-up call to accelerate trends that have been around for years and are now greatly speeding up. The pandemic seems to have triggered a new survival instinct: innovate fast or die. Let me list some of the frontrunners.

1. E-commerce

E-commerce is the No. 1 shelter-in-place beneficiary by miles, as a combination of stay-at-home orders, reduced spending on dining, and government stimulus have sent Americans in search of other ways to spend their money. Even though Covid-19 restrictions are now being eased, the e-commerce industry should still see about 25% growth across all of 2020.

The estimated $60 billion spent by consumers from their stimulus checks has also been a tailwind. While the world is now re-opening, we expect these buckets of available dollars to remain e-commerce tailwinds for the foreseeable future as we expect adjusted retail and travel spend to decline an aggregate of 18% in and for as much as half of all small retail stores to potentially close this year.

When Amazon shares were at $1,000, I wrote a report calculating that its breakup value was at least $3,000 a share. It looks like Amazon may hit that target before yearend….without the breakup.

Want to know the winners? Try Amazon (AMZN), Chewy (CHWY), and eBay (EBAY).

2. Digital Entertainment

The Covid-19 pandemic has also left more Americans in search of digital, at-home entertainment, a trend that’s delivered a huge push for companies like Activision Blizzard that develop online games. New users, time spend gaming and in-game purchases are only accelerating and spell even more lasting benefit for game developers.

Content names like video streaming site Netflix (NFLX), as well as bandwidth and connectivity companies including Comcast (CMCSA) and T-Mobile (TMUS), are names to focus on.

This increased use of high bandwidth applications is likely to continue post-COVID-19 and has the impact of similarly increasing the demand for bandwidth and connectivity. This increases the value of upstream assets in the infrastructure sectors like fiber-based wireline broadband networks and nascent 5G build-outs.

Names to play the space: Netflix (NFLX), Spotify (SPOT), T-Mobile (TMUS), Activision Blizzard (ATVI).

3. Touchless payments

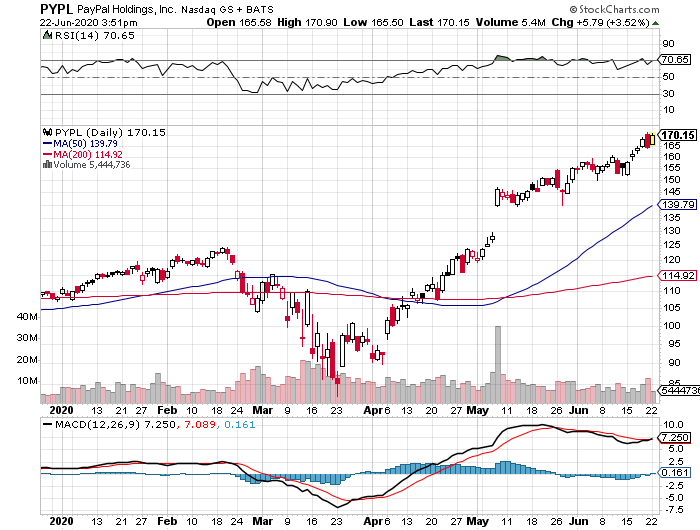

Another trend the stock market still underappreciated is a generational surge in contactless payments, which has recently seen a jump higher amid Covid-19 fears and efforts to minimize physical contact. Companies like Visa (V), Mastercard (MA), and PayPal (PYPL), already integral to the payments world, should be major beneficiaries in the years ahead.

The market assumes that COVID-19 related adoption of digital payments is a near-term benefit for payment service providers, offsetting some of the consumer spending headwinds. However, digitization of payments is part of a multi-year secular growth driver, with COVID-19 as just the latest accelerator.

Names to play the space: Visa (V), PayPal (PYPL), Apple (AAPL), and Mastercard (MA).

4. Telemedicine

Healthcare is one of the most inefficient industries left in the United States. I call it a 19th century industry operating with 21st century technology. While progress has been made, those massive stacks of paper records are finally disappearing, there still is a long way to go.

These days, even doctors don’t want to see patients in person, as they may contract the Coronavirus. Far better to see them online, which could address 90% of most patients. Teledoc (TDOC) does exactly that (click here for my full report).

So does Intuitive Surgical (ISRG), maker of DaVinci Surgical Systems, which enables remote operations for a whole host of maladies. Titan Medical (TMDI) is another name to look at here.

Names to play the space: (TDOC), (ISRG), (TMDI).

Mad Hedge Technology Letter

February 19, 2020

Fiat Lux

Featured Trade:

(BUY THE CORONA DIP),

(VZ), (T), (TMUS), (S), (AAPL), (BABA), (CSCO), (EXPE)

The coronavirus hammer finally came down and hit one of the dominant soldiers of big tech.

Apple (AAPL) led morning headlines nationwide by slashing quarterly revenue guidance stemming from production delays and weak demand in China.

Deleting the China demand for new iPhones is enough for the company to signal a looming revenue miss and rightly so, coronavirus has been 24-hour news for the past 2 months on the Asian continent.

As we speak, the cruise liner named the Diamond Princess is parked outside the port of Yokohama with the victims of infected rising by the day.

The optics are ugly, and China’s cover-up of the spreading went awfully awry and now pandora’s box is open.

Naturally, tech stocks can expect a few percentage points shaved off of this year’s annual growth targets and short-term sluggishness in shares exposed to China revenue.

What are the ramifications?

Telecom companies are in the incubation period of building out 5G wireless networks.

Naturally, tech shares will receive a bounce as network deployment gains traction as management commentary, during company earnings calls, on 5G business heats up.

However, the Mobile World Congress was cancelled by organizers stealing the chance for 5G stocks to hype up their position in 5G.

It is almost guaranteed at this point that China coronavirus will slow down the schedule for 5G wireless network buildouts.

Think about this, SARS lasted roughly half a year during 2002-2003, and the coronavirus appears to be worse than that.

Chinese telcoms will need to delay 5G and related equipment along with business that has around 150 million Chinese ensnared by the domestic quarantine.

Apple’s 5G iPhones in late 2020 could be delayed if there is no meaningful breakthrough in the contagion of the coronavirus and its ill effects on global business.

Apple stock appreciated on the hope that 5G iPhones aim to deliver the first meaningful consumer upgrade cycle in several years with a hefty price tag of $1,250.

This next generation iPhone could get pushed back to 2021 as Apple’s supply chain has been put on ice in mainland China.

If Verizon Communications (VZ), AT&T (T), T-Mobile US (TMUS) and Sprint (S) desire to aggressively expand their 5G networks, they might be in for a rude awakening because semiconductor companies might be stretched to limit and cannot provide the right components with supply chains pressured everywhere.

The truth is that supply chains are impacting diverse and interconnected sectors of the electronics industry.

And the epidemic, arriving at dawn of 5G's mainstream deployment phase, is guaranteed to disrupt the progress of the next-generation wireless standard, as the crisis slows the production of key smartphone components, including displays and semiconductors.

Chip companies and their shares have naturally been rocked by the recent news and they aren’t the only ones.

Expedia (EXPE), the online travel company, revealed it will avoid providing a full-year forecast as the online travel services company reevaluates the impact of the coronavirus outbreak on its operations.

Investors can imagine that on mainland China, the situation is grim exerting a fundamental impact on the country’s consumers and merchants and will slice off revenue growth in the current quarter.

Alibaba (BABA), the Amazon of China, told investors that the virus is undermining production and output in the economy because many workers are stuck at home.

The virus has also changed the commerce patterns of consumers by pulling back on discretionary spending, including travel and restaurants.

The Chinese e-commerce giant’s revenue surged year-over-year by an impressive 38% to 161.5 billion yuan ($23.1 billion), while net income rose 58% to 52.3 billion yuan, but that could symbolize the high-water mark.

Chief Executive Officer Daniel Zhang and Chief Financial Officer Maggie Wu were explicit in mentioning that risks from the pandemic could deaden a piece of revenue moving forward and they weren’t shy about stating this.

Sound bites such as “overall revenue will be negatively impacted,” and expecting growth to be “significantly” negative is quite black and white.

China is almost certain to print weak GDP growth numbers because of cratering imports and a big drop in demand.

Echoing Alibaba’s weakness was network infrastructure company Cisco (CSCO) with a revenue shortfall of 3.5% year-over-year as major product categories like Infrastructure Platforms and Applications were hit.

Cisco must find new cycles in core activities to regain any momentum and chip companies must do the same as the administration turns the screws on Huawei and injects more barriers to U.S. chip companies selling abroad.

This adds to the broader risks of elevated corporate debt and the upcoming U.S. election where tech management is nervous that a new President could throw big tech under the bus.

The coronavirus pours fuel on the flames.

The silver lining is the blows to these companies are softened by the ironic fact that big tech has become the safety trade to the coronavirus and even if 5G is delayed, chip stocks will eventually benefit from a fresh wave of revenue drivers when the 5G network is finally deployed.

However, it is way too early to announce the death of big tech, there are far too many secular tailwinds driving these companies.

The tech bull market is still intact and there will be opportunity to buy.

Global Market Comments

January 9, 2020

Fiat Lux

Featured Trade:

(WEDNESDAY, FEBRUARY 5 MELBOURNE, AUSTRALIA STRATEGY LUNCHEON)

(CAPTURING SOME YIELD WITH CELL PHONE REITS),

(CCI), (AMT), (SBAC),

(JNK), (SPG), (AMLP), (AAPL), (VZ), (T), (TMUS), (S)

I am constantly bombarded with requests for high-yield, low-risk investments in this ultra-low interest rates world.

While high-yield energy Master Limited Partnerships LIKE (AMLP) can offer double-digit returns, they carry immense risks. After all, if the prices of oil drop to $5-$10 a barrel, replaced by alternatives as I eventually expect, all of these instruments will get wiped out.

You can earn 5%-8% from equity-linked junk bonds. However, their fates are tied to the future of the stock market at a 20-year valuation high against flat earnings.

You might then migrate to Real Estate Investment Trusts (REITs) like Simon Property Group (SPG), which acts as a pass-through vehicle for investments in a variety of property investments. However, many of these are tied to shopping malls and the retail industry, the black hole of investment today.

So where is the yield-hungry investor to go?

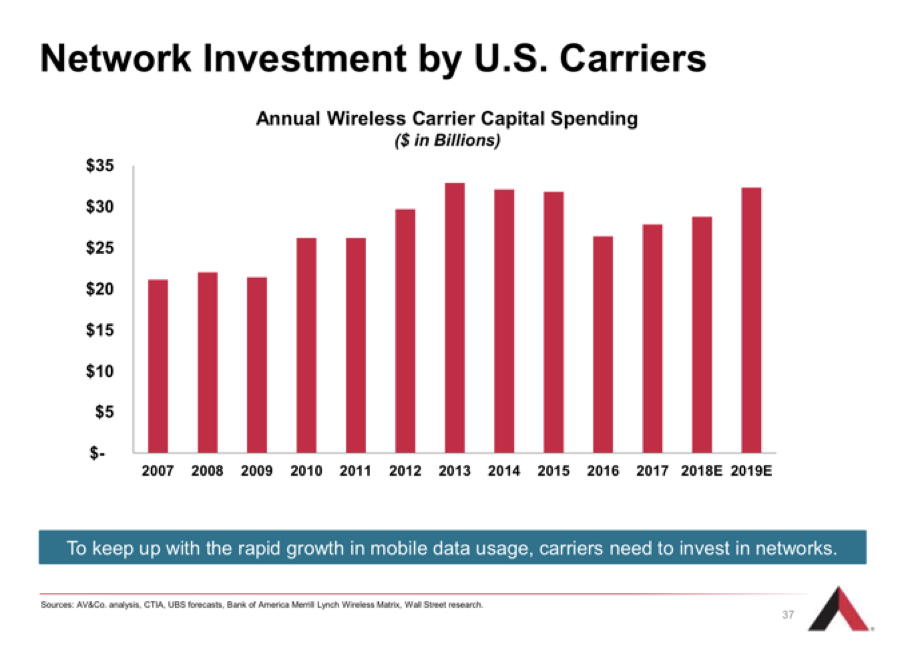

You may have heard about something called 5G. This refers to the rollout of fifth-generation wireless technology that will increase smartphone capabilities tenfold. Whole new technologies, like autonomous driving and artificial intelligence, will get a huge boost from the advent of 5G. Apple (AAPL) will launch its own 5G phone in September.

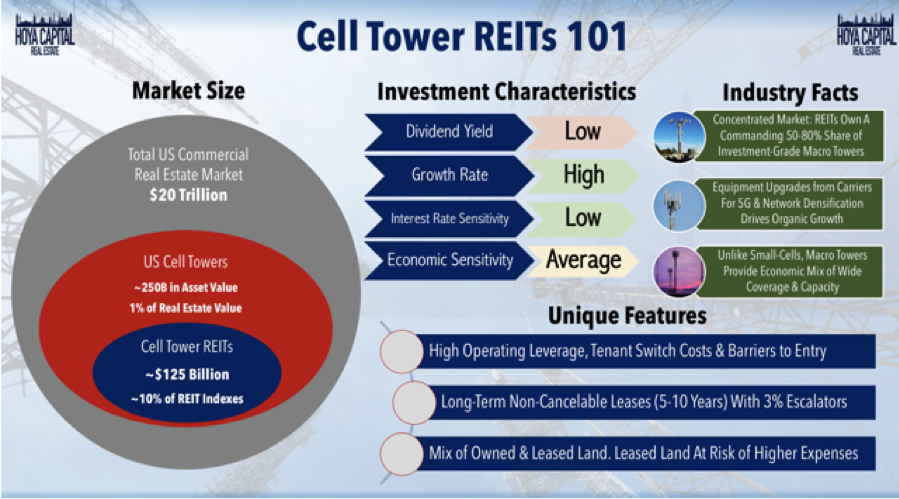

5G, like all cell phone transmissions, rely on 50-200-foot steel towers strategically placed throughout the country, frequently on mountain peaks or the tops of buildings. With demand from the big phone carriers soaring, there is a construction boom underway in cell phone towers. There just so happens to be a class of REITs that specializes in investment in this sector.

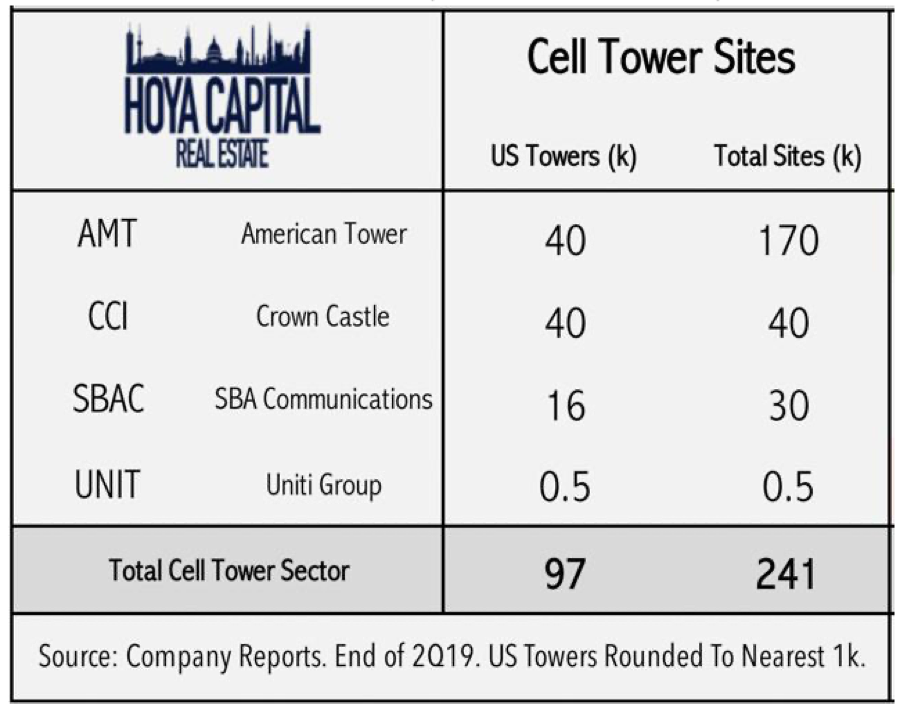

Cells Phone REITs constitute a $125 billion market and make up 10% of the REIT indexes. They own 50%-80% of all investment-grade towers. They are all benefiting from a massive upgrade cycle to accommodate the 5G rollout. These REITs own or lease the land under the cell towers and then lease them to the phone companies, like Verizon (VZ), AT&T (T), T-Mobile (TMUS), and Sprint (S) for ten years with 3% annual escalation contracts.

American Tower (AMT) is far and away the largest such REIT, with 170,000 towers, has provided an average annual return over the past ten years, and offers a fairly safe 1.65% yield. They are currently expanding in Africa. Even during the 2008 crash, (AMT) still delivered an 8% earnings growth.

SBA Communications (SBAC) is the runt of the sector with only 30,000 towers. However, it has a big presence in Central and South America and is seeing earnings grow at a prolific 80% annual rate. (SBAC) is offering a 1.48% yield at today’s prices.

Crown Castle International (CCI) is in the middle with 40,000 large towers and 65,000 small ones. 5G signals travel only a 1,000 meters, compared to several miles for 4G, requiring the construction of tens of thousands of small towers where (CCI) is best positioned. (CCI) offers a hefty 3.39% yield.

Small cell towers are roughly the size of an extra-large pizza box and will soon be found on every urban street corner in the US. AT&T (T) has estimated that there is a need for over 300,000 small cell phone towers in the US alone.

So, if you’re looking for a sea anchor for your portfolio, a low-risk, high-return investment that won’t see a lot of volatility, Cell phone REITs may be your thing. Buy (CCI) on dips.

Can you hear me now?

Mad Hedge Technology Letter

May 4, 2018

Fiat Lux

SPECIAL SPACE X ISSUE

Featured Trade:

(WILL SPACE X BE YOUR NEXT TEN-BAGGER?)

(EBAY), (TSLA), (SCTY), (BA), (LMT)

Mad Hedge Technology Letter

May 3, 2018

Fiat Lux

Featured Trade:

(THE INCREDIBLE SHRINKING TELEPHONE INDUSTRY)

(TMUS), (S), (NFLX), (T), (VZ), (CHTR), (CMCSA)

Talk is cheap.

Do not believe half-truths that go against economic convention.

This was the case when T-Mobile (TMUS) CEO John Legere and Sprint (S) CEO Marcelo Claure popped up on live TV promoting affordability, elevated competition, and massive 5G infrastructure investments if the two companies joined forces in a $26.5 billion deal.

This was a case of smoke and mirrors. The speculative claim of adding 3 million workers and investing $40 billion into 5G development is just a line pandering toward President Trump's nationalistic tendencies.

They want the deal to move forward any way possible.

Jack Ma, founder and executive chairman of Alibaba (BABA), met President Trump at Trump Towers before his term commenced and promised to add 1 million jobs in order to curry favor with the new order.

Where are those jobs?

If this merger came to fruition, market players would shrink from 4 to 3 - a newly reformulated T-Mobile plus Verizon (VZ) and AT&T (T).

Pure economics dictate that shrinking competition by 25% would create pricing leverage for the leftover trio.

Industry consolidation is usually met with accelerated profit drivers because companies can get away with reckless price increases without offering more goods and services.

Being at the vanguard of the 4G movement, America overwhelmingly benefited from lucid synergistic applications that fueled domestic job growth and economic gains.

Japanese and German players were hit hard from missing out in leading the new wave of wireless technology.

T-Mobile and Sprint wish to be insiders of this revolutionary technology and this is their way in.

In the past, T-Mobile jumped onto the scene with aggressively twisting its business model to fight tooth and nail with Verizon and AT&T.

It was moderately successful.

T-Mobile even offered affordable plans without contracts offering customers optionality and advantageous pricing.

It was able to take market share from Sprint, which is the monumental laggard in this group and the butt of jokes in this foursome.

The average cost of wireless has slid 19% in the past five years, and traditional wireless Internet companies are sweating bullets as the future is murky at best.

The bold strategy to merge these two wireless firms derives from an urgent need to combat harsh competition from the two titans Verizon and AT&T.

The merger is in serious threat of being shot down by the Department of Justice (DOJ) on antitrust grounds.

History is littered with companies that became complacent and toppled because of monopolistic positions.

Case in point, the predominant force in the American and global economy was the American automotive industry and Detroit in the 1950s.

Detroit had the highest income and highest rate of home ownership out of any major American city at that time.

Flint, Michigan, oozed prosperity, and the top three car manufacturers boasted magnanimous employee benefits and a tight knit union.

During this era of success, 50% of American cars were made by GM and 80% of cars were American made.

The car industry could do no wrong.

This would mark the peak of American automotive dominance, as local companies failed to innovate, preferring stop-gap measures such as installing add-ons such as power steering, sound systems, and air conditioning instead of properly developing the next generation of models.

American companies declined to revolutionize the expensive system put in place that could produce new models because of the absence of competition and were making too much money to justify alterations.

It's expensive to make cars but neglecting reinvestment yielded future mediocrity to the detriment of the whole city of Detroit.

The tech mentality is the polar opposite with most tech firms reinvesting the lion's share of operational profit, if any, back into product improvement.

Sprint got burned because it skimped on investment. It is in a difficult predicament dependent on T-Mobile to haul it out of a precarious position.

GM, Ford, and Chrysler met their match when Toyota imported a vastly more efficient way of production and the rest is history.

Detroit is a ghastly remnant of what it used to be with half the population escaping to greener pastures.

A carbon copy scenario is playing out in the mobile wireless space and allowing a merger would suppress any real competition.

To add confusion to the mix, fresh competition is growing on the fringes desiring to disrupt this industry sooner than later by cable providers such as Charter (CHTR) and Comcast (CMCSA) entering the fray offering mobile phone plans.

Google also offers a mobile phone plan through the Google Fi division.

The fusion of wireless, broadband, and video is attracting competition from other spheres of the business world.

The paranoia served in doses originates from the Netflix (NFLX) threat that vies for the same entertainment dollars and eyeballs.

Remember that AT&T is in the midst of merging with Time Warner Cable, which is the second largest cable company behind Comcast.

The top two in the bunch - AT&T and Verizon - are under attack from online streaming business models, and the Time Warner merger is a direct response to this threat.

There are a lot of moving parts to this situation.

AT&T hopes to leverage new video content to extract digital ad revenue capturing margin gains.

Legere and Claure put on their fearmongering hats as they argued that this deal has national security implications and losing out to Chinese innovation is not an option.

This argument is ironic considering T-Mobile is a German company and Sprint is owned by the Japanese.

Sprint have been burning cash for years and this move would ensure the businesses survives.

Sprint's crippling debt puts it in an unenviable position and this merger is an all or nothing gamble.

Sprint has not invested in its network and is miles behind the other three.

AT&T has outspent Sprint by more than $90 billion in the past 10 years.

This is the last chance saloon for Sprint whose stock price has halved in the past four years.

However, T-Mobile sits on its perch as a healthier rival that would do fine on a stand-alone basis.

Consolidation of this great magnitude never pans out for the consumer as users' interests get moved down the pecking order.

Wireless stocks were taken out and beaten behind the wood shed on the announcement of this news as the lack of clarity moving forward marked a perfect time to sell.

There will be many twists and turns in this saga and any capital put to use now will be dead money while this imbroglio works itself out.

If the deal doesn't die a slow death and finds a way through, the approval process will be drawn out and cumbersome.

The ambitious deadline of early 2019 seems highly unrealistic even with the most optimistic guesses.

The outsized winner from a deal would be AT&T, Verizon, and the newly formed T-Mobile and Sprint operation.

If this new wave of consolidation becomes reality, pricing pressure on the business model would ease for the remaining players, particularly allowing more breathing room for the leaders.

Stay away from this sector until the light can be seen at the end of the tunnel.

_________________________________________________________________________________________________

Quote of the Day

"Everything is designed. Few things are designed well." - said radio producer Brian Reed

Rumors hit the market Friday that Sprint (S) will mount a $20 billion takeover bid for T-Mobile (TMUS) in early January. The news caused a late day kerfluffle on what would otherwise have been a slow December pre holiday Friday.

The Shares of both companies immediately jumped 10%, which left many analysts scratching their heads. Normally, the shares of the acquirer falls (they?re spending money), while those of the target rise (they are selling for a premium to the market).

Why do I care about a minor US phone company? Guess who owns Sprint? Softbank, which took over the company for $21.8 billion last July, and carries a hefty 20% weighting in my model-trading portfolio.

The move would make Softbank one of the three largest US carriers. That will automatically trigger an antitrust review by the Justice Department, which blocked a similar takeover attempt for giant AT&T (T) earlier. Look at how Eric Holder stood in the way of the American Airlines-US Air deal, which both firms clearly needed to survive. And this is in a country with 100 airlines. So any decision here could be a long wait.

I think this is just an opening shot in a long campaign that eventually leads up to the Alibaba IPO, expected to be one of the largest in history (the biggest was also from China, the $128 billion deal for the Industrial Bank of China in 2010). Expect to hear a lot about Softbank?s role in all of this in coming months. This should be good for its stock price.

As part of the build up, my old employer, the Financial Times of London, named Alibaba founder and CEO, Jack Ma, as its Person of the Year. The paper chronicles Ma?s rise for abject poverty in Hangzhou, China, where he was the son of impoverished traditional performers, to becoming one of the world?s richest men.

Ma was fascinated by the English language at an early age, and used to listen to my own broadcasts on BBC Radio to learn new words (another one of my former employers). After graduating in 1988, he earned $12 an hour as a teacher in China. While working for the Foreign Trade and International Cooperation, he escorted foreign visitors to the Great Wall. One of them turned out to be Jerry Yang, co founder of Yahoo.

Thus inspired, Ma went on to found Alibaba in 1999. Its initial strategy was to match up Chinese manufacturers with American customers, an approach that proved wildly successful. He then took on Ebay. In the following years the US e-commerce giant saw its Chinese market share plummet from 80% to 8%, most of that going to Alibaba. Today, Alibaba has 600 million registered users, and one day in November it clocked a staggering $6 billion in sales.

The FT estimates its current market value at $100 billion. To read the rest of the FT profile, please click here. Its IPO will be one of the preeminent investment events of 2014. Better to get in early.

Followers of my Trade Alert Service will notice that this is one of the few outright equity trades that I have done this year. This is a way for me to deleverage my exposure after a spectacular stock market run. Equity ownership ducks the time decay that plagues call options, and avoids the leverage inherent in call spreads.

If the stock is unchanged over the holidays, it won?t cost me a dime. One thing is for sure. When the Alibaba IPO is announced, it will be a surprise. The only way to participate is to get in indirectly through a minority owner now.

Don?t expect an allocation from your broker, unless they think it is going o fail.