“When we launch a product, we're already working on the next one. And possibly even the next, next one.” – Said CEO of Apple Tim Cook

“When we launch a product, we're already working on the next one. And possibly even the next, next one.” – Said CEO of Apple Tim Cook

Mad Hedge Technology Letter

December 9, 2019

Fiat Lux

Featured Trade:

(THE BEYOND MEAT BOMB),

(BYND), (TSN), (KRL), (K), (CAG)

Food tech stock Beyond Meat, Inc. (BYND) went from euphoric to absolute dud when shares surged above $240 at the end of July only to crash.

In general, tech stocks have had a successful year, but the second half of the year has been inordinately unkind to growth stocks and Beyond Meat bore the full brunt of the change in market sentiment.

Let me remind you that I am not saying this is a bad company or a bad stock like Uber (UBER) or Lyft (LYFT).

Hardly so.

Investors can take away many positives from their overarching story and even more so as the stock has come down from the heavens settling in the mid-70’s range.

First, plant-based food is not going away anytime soon and is intertwined with the Millennial ethos of living healthier and protecting the planet.

Nonprofit organization The Good Foods Institute has forecasted that the plant-based food market is valued at more than $4.5 billion in the U.S. and grew 11% year over year.

Plant-based meat rose 10% last year, a substantial decrease of 25% year over year, but industry experts believe there is a significant pipeline of international revenue just waiting there for the taking.

More than one-third have tried at least one plant-based meat product, a low figure, but of those that have tasted, 57% make a repeat purchase.

Internationally, sales are expected to go from a $12.1 billion market in 2019 to a $27.9 billion market by 2025. In 2018, plant-based meat sales comprised 1% of all dollar sales in total retail meat in the U.S. and that number is only going to rise.

Let’s compare it with another successful plant-based product that has matured into a winner – milk.

This market has developed into a $1.86 billion market and plant-based milk is further ahead than the plant-based dairy and meat market.

Fortunately, these juxtaposed markets represent substantially overlap and positive demographic correlation of plant-based milk and meat consumers could mean that plant-based meat companies could achieve a similar rise like the plant-based milk companies experienced.

Domestically, plant-based milk now has a 13% share of the overall retail milk market, exploding by 61% from the years 2012 to 2017 and a further 6% rise in 2018.

If plant-based meat enters into the same trajectory as their cousins’ plant-based milk, grabbing 10% of market share from the overall retail meat market is feasible.

The special sauce that initially propelled the share price to the Himalayan highs of July was the insane growth rate which last quarter came in at 211.5% year-over-year.

The company is also surprisingly profitable eking out a $4.10 million performance last quarter on almost $92 million of quarterly revenue.

But I would like to bring investors back to reality and remind them that the company only does $92 million of revenue per quarter and the one before that a touch above $67 million.

This company is still in its infancy and just because it bursts with life in its formative stages does not mean investors can extrapolate that for years ahead.

What are the headwinds and how far off are they?

The most unstable variable rearing its ugly head is intense competition imminently barreling towards Beyond Meat.

An outsized dosage of competition would take an axe to profit margins with minimal chance of a quick reversal even if Beyond Meat manages to offer an outperforming product.

Beyond Meat is the disruptor and reaped a dividend from the first-mover advantage and the subsequent network effects.

But that doesn’t mean larger companies can’t copy them and that is exactly what is happening as we speak.

The competition is rapidly intensifying, specifically from big box protein processors and packaged food players who plan to undercut Beyond Meat price points using excess capacity and a lower gross margin rate profile.

The companies coming for Beyond’s bacon are Tyson Foods Inc. (TSN), Kellogg Co. (K), Hormel Foods Corp. (HRL), and Conagra Brands Inc. (CAG).

These big players will dump volume onto the plant-based food market and Kroger Co. just announced it would introduce 58 plant-based items under its private label Simple Truth in 2020.

Beyond Meat’s strategic position could suffer if consumers prove less brand loyalty and more price-conscious, then Beyond Meat’s first-mover advantage could dissipate and dynamics could revert closer to commodity industry profit margins.

Investors are laser-like focused if Beyond Meat can maintain gross margins over 35% by layering strategic partnerships with businesses that have a widespread addressable audience base.

If Beyond Meat fails in this respect, the competition will gradually destroy its competitive advantage and tank its share price.

The quality of the product has a large role to play in this too.

Another possible headwind is that Impossible Foods’ Impossible Burger is favored by many taste experts in taste tests diminishing Beyond’s product to the second tier.

But If the company can mimic the taste of a high-quality burger and replicate at least 80% of that experience, the products are likely to stick leading to more investment to capture that last 20% of the taste experience.

It is yet to be determined if Beyond Meat can muscle itself through the gauntlet of rigmaroles, and technically, its overhyped beginnings have given way to a more modest share price as of late.

If the stock enters into the $50 price range, it would be an advantageous price point to scale into this leader of food tech, but I would monitor it closely because the narrative could change on a dime and the story could sour if their strategy begins to fail.

“You may think using Google's great, but I still think it's terrible.” – Said Co-Founder of Google Larry Page

Mad Hedge Technology Letter

December 6, 2019

Fiat Lux

Featured Trade:

(AUGMENTED REALITY IS HEATING UP),

(AAPL), (LITE), (QCOM), (NVDA), (ADSK), (FB), (MSFT), (SNAP)

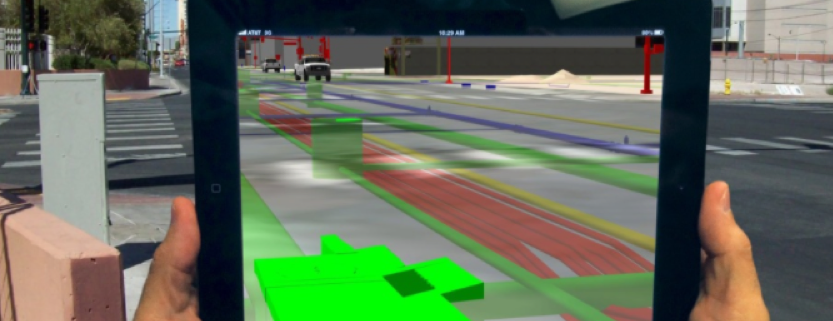

First, what is augmented reality for all the newbies?

Augmented reality is an interactive experience of a real-world environment where the objects that reside in the real world are enhanced by computer-generated perceptual information, sometimes across multiple sensory modalities.

Augmented reality (AR) went rival in 2016 when the Pokemon Go mania captivated everyone from children to adults.

No sooner than 2021, the AR addressable market is poised to mushroom to $83 billion - a sizeable increase from the $350 million in 2018.

Much like machine learning, corporations are learning to marry up this technology with their existing products supercharging the performance.

Ulta Beauty, for example, has acquired AR and artificial intelligence start-ups to help customers digitally test the final appearance of makeup before users purchase the product.

That is just one micro example of what can and will be achieved.

Looking deeper into the guts, Qualcomm (QCOM) is hellbent on making their chips a critical part of the puzzle.

The company is better known for a telecom and a semiconductor play, not often lumped in with a list of AR stocks.

Qualcomm is strategically positioned to capitalize on the integration of augmented reality in mainstream corporate business embedding their chips into the devices.

Maximizing Qualcomm’s future role in the industry, the company announced in 2018 that it would be developing a chipset specifically for AR and VR applications.

This broad-based solution will make it easier for other developers to bring new glasses to the marketplace.

Autodesk (ADSK) is one of my favorite software stocks and a best of breed of industry design.

They sell 3D rendering software to designers and creators by offering a platform in which they can transform 2D designs into digital models that are both interactive and immersive, creating compelling experiences for end-users.

Autodesk has an array of powerful software suites to augment virtually any application, such as 3ds Max, a 3D modeling program; Maya LT game development software; its automotive modeling program VRED; and Forge, a development platform for cloud-based design.

Facebook (FB) has been piling capital into AR for years.

CEO Mark Zuckerberg wants to create an alternative profit-driver and is desperate to wean his brainchild from the digital ad circus.

One example is Facebook’s Portal TV and its Spark AR which is the platform responsible for mobile augmented reality experiences on Facebook, Messenger, and Instagram.

It supplies the virtual effects for consumers to play around with, but it is yet to be seen if consumers gravitate towards this product.

Lumentum (LITE) is the leader in 3D-sensing markets developing cloud and 5G wireless network deployments.

They manufacture 3D sensor lasers that can be used with smartphones to turn handsets into a sort of radar. Sensors are clearly a huge input in how AR functions along with the chips.

CEO of Apple (AAPL) Tim Cook put it best when he earlier said, “I do think that a significant portion of the population of developed countries, and eventually all countries, will have AR experiences every day, almost like eating three meals a day, it will become that much a part of you.”

He said that in 2016 and AR has yet to mushroom into the game-changing sector initially thought partly because the roll-out of 5G is taking longer than first expected.

Apple consumers will need to then adopt a 5G device or phone to really get the AR party started and that won’t happen until the backend of next year.

My initial channel checks hint that the Cupertino firm is planning a 5.4-inch model, two 6.1-inch devices, and one 6.7-inch phone, all of which will support 5G connectivity.

I surmise that Apple’s two premium devices will feature “world-facing” 3D sensing, a technology that could help Apple boost its augmented-reality capabilities and support other feature improvements on its priciest devices.

Apple has had a big hand in Lumentum's growth and will continue to buy their sensors, but other key component suppliers will get contracts such as Finisar, a manufacturer of optical communication components and subsystems.

Apple planned to debut AR glasses by 2020, but the rollout is now delayed until 2022.

They are clearly on the back foot with Microsoft (MSFT) further along in the process.

Microsoft already has a second iteration of its AR headset, HoloLens, and is compatible with several apps and has integration with Azure as well.

The head start of 2 years could really make a meaningful impact and might be hard for Apple to recover.

Facebook isn’t the only social media company going full steam into AR, Snap (SNAP) recently unveiled its newest spectacles, which feature AR elements.

Another application of AR is autonomous driving with Nvidia working on improving the driving experience by fusing AR with artificial intelligence.

Nvidia (NVDA) is already thinking about the next generation of AR technologies with varifocal displays, which improve the clarity of an object for a user.

It will take time to transform our relationship with AR, the infrastructure is still getting built out and many people just don’t have a device that will allow us to tap into the technology.

Investors must know that AR-related stocks will start to appreciate from the anticipation of full sale adoption and there could be a killer app that forces the mainstream user to take notice.

Until then, companies jockey for position and hope to be the ones that take the lion’s share of the revenue once the technology goes into overdrive.

“If you think you deserve a raise, you should just ask.” – Said CEO of Microsoft Satya Nadella

Mad Hedge Technology Letter

December 4, 2019

Fiat Lux

Featured Trade:

(THE RUSH TO BUY ONLINE),

(AMZN), (WMT), (TGT), (W), (ETSY), (SHOP), (ADOBE)

There are several overarching seminal tech trends that I swear by.

The generational broad-based migration from analog to digital is a critical foundation that underpins the success of not only tech stocks as a unified sector, but the outperformance of the Mad Hedge Technology Letter.

You’ll be pleased to discover that 2019 is right on queue with digital sales exploding by the American consumer over the holiday shopping period and Americans ditching brick and mortar stores in droves.

Amazon (AMZN) broke records on Cyber Monday bragging that in terms of the number of items sold, it had its "single biggest shopping day."

Black Friday was a big success too selling “hundreds of millions" of products between Thanksgiving and Cyber Monday.

Consumers scooped up the toys, home, fashion and health, and personal care products on Amazon’s e-commerce platform.

Hot ticket items on Black Friday included Amazon's own Echo Dot and Fire TV Stick with Alexa Voice Remote, Play-Doh Sweet Shoppe Cookie Creations, Keurig K-Cafe Coffee Maker and LEGO City Ambulance Helicopter Kit.

Adobe (ADBE) Analytics estimates that the sales for the shopping bonanza easily eclipsed $29 billion, or 20% of total revenue for the full holiday season.

This is the aha moment when digital integration into shopping forced a paradigm shift to the business environment by capturing the focal point of American wallets.

Digital used to be the minority, but going forward, it will dictate the terms of engagement.

What does this mean in the bigger scope of things?

Mobile is the biggest winner of this brave new world.

Shopping apps gave consumers the platform to use their phones as a digital wallet.

Salesforce data discovered that Thanksgiving sales as a proportion of U.S. digital sales grew 17% and mobile sales rose 35% on Black Friday with 65% of total e-commerce executed through a mobile device.

“Black Friday broke mobile shopping records and even when shoppers went to stores, they were now buying nearly 41% more online before going to the store to pick up,” said Taylor Schreiner, principal analyst and head of Adobe Digital Insights.

Shopify (SHOP) did over $900 million in sales this year and 69% were from phones and only 31% from desktop computers.

Black Friday was "the biggest day ever for mobile," tracking $2.9 billion in sales from smartphones alone, or 39% of all e-commerce sales, a 21% increase year over year.

The data also showed that smaller e-commerce outfits had a harder time driving sales than large e-commerce platforms.

The network effect truly works both ways and the success of the biggest and best also correlated to a meaningful decline of physical shopping visit to stores of 6% on Black Friday.

According to The NPD Group's Holiday Purchase Intentions Survey, 20% of sales were picked up in the store. This click-and-collect business has been a huge winner for the likes of Walmart (WMT).

E-commerce leaders are having enormous success introducing omnichannel approaches to the selling channels.

The average order value on Black Friday rose 5.9% year over year to $168, a new record, in part because shoppers have become more comfortable buying expensive items online because the sales are even juicier.

Unfortunately, the rise in volume has meant lower margins.

Discounts averaged between 37% to 47% and home and consumer electronics products were popular.

With all the rumblings of tariff trauma and an approaching recession, the American consumer displayed robustness that largely met the consensus of analysts.

The takeaway is that e-commerce is as healthy as ever and should prolong not only the strength in e-commerce companies but the overall American economy.

The winners are the behemoths of Amazon, Target (TGT), Shopify, and Walmart. Shares should receive a moderate tailwind through the New Year.

Avoid smaller niche players like Etsy (ETSY) and Wayfair (W).

“We want Google to be the third half of your brain.” – Said Co-Founder of Google Sergey Brin