“Spotify has paid more than two billion dollars to labels, publishers and collecting societies for distribution to songwriters and recording artists.” – Said CEO of Spotify Daniel Ek

“Spotify has paid more than two billion dollars to labels, publishers and collecting societies for distribution to songwriters and recording artists.” – Said CEO of Spotify Daniel Ek

Mad Hedge Technology Letter

October 4, 2019

Fiat Lux

Featured Trade:

(WHY YOU ARE ABOUT TO LOSE YOUR JOB)

(SPECIAL AUTOMATION ISSUE)

The hammer has been brought down on the financial industry.

Robots are here and here to stay - automation is taking place at a breakneck speed displacing worker from all industries.

In a recent report by Wells Fargo, the U.S. financial industry will supposedly fire 200,000 workers in the next decade because of the advancements of automating processes.

Yes, humans are going obsolete and banking will effectively become algorithms working for a handful of executives and engineers controlling the algorithms.

The catalyst in this equation is the direct capital of $150 billion annually that banks spend on technological development in-house which is higher than any other industry.

Private businesses aren’t charities and banks are doing this all in the name of lower cost, shedding employee wage packets, and boosting efficiency rates.

We forget to realize that employee compensation absorbs up to 50% of bank’s expenses.

The 200,000 job trimmings would result in 10% of the U.S. bank jobs axed for the hyped-up “golden age of banking” that should deliver extraordinary savings and extra services to the customer.

I would argue that cost savings due to technological enhancements have already had an outsized surge in available services to the client as mobile and online banking has increased functionality allowing U.S. customers to maintain tight internet control over their bank account from anywhere that has an internet connection.

The most gutted part of banking jobs will be in the call centers because they will be substituted by chatbots.

A few years ago, chatbots were awful, even spewing out arbitrary profanity, but they have slowly crawled up in performance metrics to the point where some customers do not even know they are communicating with an artificial engineered algorithm.

The wholesale adoption of automating the back-office staff isn’t the end of it, the front office will experience a 30% drop in numbers sullying the predated ideology that front office staff is irreplaceable heavy hitters.

As it is, front-office staff is in the midst of getting purged with 2018 representing a fifth year of decline.

Front-office traders are being replaced by software engineers as banks follow the wider trend of every company migrating into a tech company.

Efficiencies do not stop there; the adoption of artificial intelligence will lower mortgage processing costs by 20% and the accumulation of hordes of data will advance the marketing effort into a smart, hybrid cloud-based and hyper-targeted strategy.

You would think that less workers mean higher pay for the employees - you thought wrong.

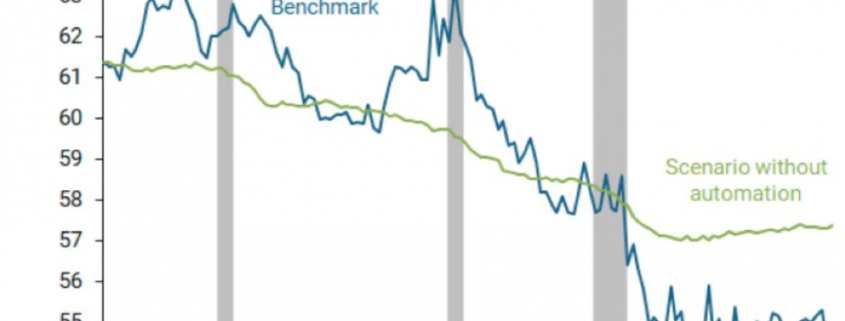

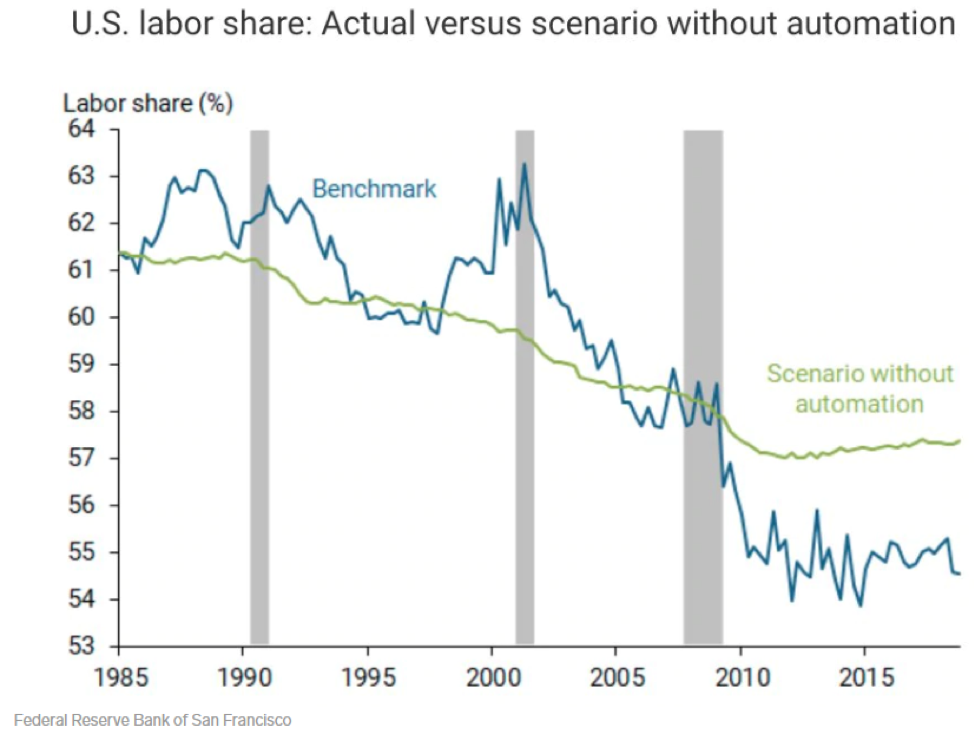

Historically, a strong labor market and low unemployment boosts wage growth, but national income going to workers has dipped from about 63% in 2000 to 56% in 2018.

Causes stem from the deceleration in union membership and outsourcing has snatched away bargaining power amongst workers on top of the mass automation being implemented.

I was recently in Budapest, Hungary and on a main thoroughfare, a J.P. Morgan and Blackrock office stood a stone’s throw away from each other employing an army of local English proficient Hungarians for 30% of the cost of American bankers.

Banks simply possess wider optionality to outsource to an emerging nation or to automate hard-to-fill positions now.

In this game of cat and mouse, companies can easily rebuff workers' attempts to ask for salary raises and if they threaten to walk off the job, a robot can just pick up the slack.

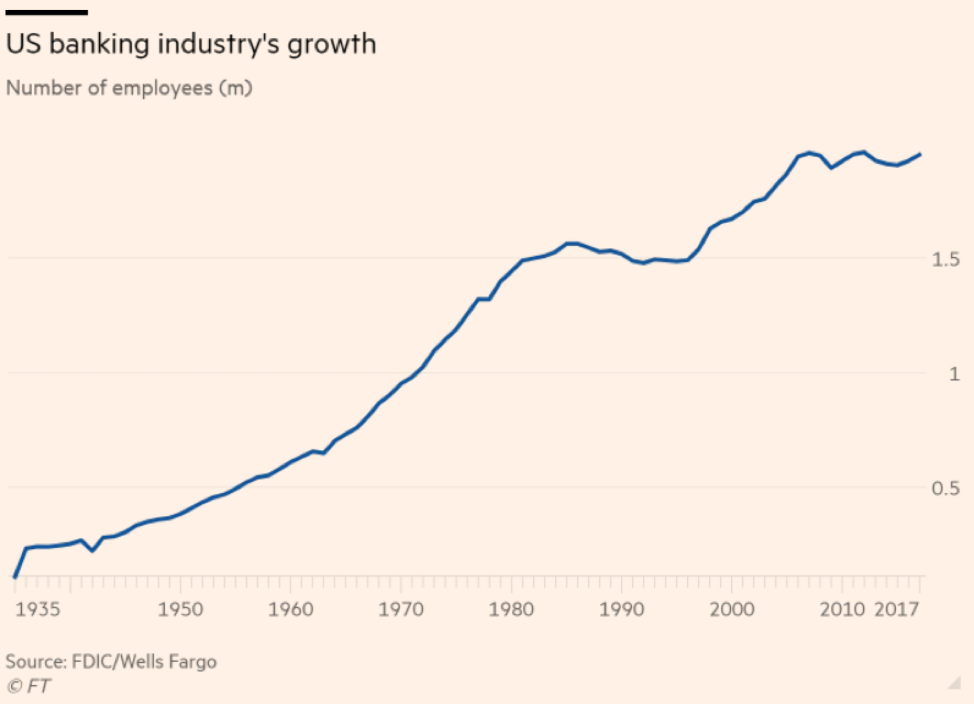

The last two human bank hiring waves are a distant memory.

The most recent spike came in the 7 years after the dot com crash until the sub-prime crisis of 2008 adding around half a million jobs on top of the 1.5 million that existed then.

The longest and most dramatic rise in human bankers was from 1935 to 1985, a 50-year boom that delivered over 1.2 million bankers to the U.S. workforce.

Recomposing banks through automation is crucial to surviving as fintech companies are chomping at the bit and even tech companies like Amazon and Apple have started tinkering with new financial products.

“I don't want to have a major lawsuit against our own government... But look, at the end of the day, if someone's going to try to threaten something that existential, you go to the mat and you fight.” – Said Co-Founder and CEO of Facebook Mark Zuckerberg

Mad Hedge Technology Letter

October 2, 2019

Fiat Lux

Featured Trade:

(IT’S TIMES UP FOR GRUBHUB)

(GRUB), (UBER)

The jury is out, and heads could roll.

That is what the tech market has been telling us and that is why I am slapping a conviction sell rating on the struggling online food delivery company GrubHub (GRUB).

The gig economy has been found out and the industry is about to have their free lunch taken away.

Many tech companies handling cheap labor by employing key workers as independent contractors are about to lose their shirt.

Considering that GrubHub cannot make the unit economics work in their favor when times are good, what do you think will happen if they have to start paying overtime, healthcare, and bonuses to full-time drivers?

Unfortunately for GrubHub, you cannot just strip out the driver in the business model, someone needs to get the hot tacos from point A to point B and back.

Along with higher labor costs, delivery fees are on the verge of cratering because of elevated competition.

GrubHub doesn’t have a monopoly in this industry and restaurants continue to complain that the likes of Postmates, DoorDash, GrubHub and Uber (UBER) Eats rip them off leaving the restaurants with their necks just above water.

GrubHub is so pitiful that they have had to resort to nefarious tactics condemning a failing business model.

Investors should aggressively short the stock or avoid it at all costs.

What type of tricks has GrubHub been up to?

If you hadn’t heard already, Senator Chuck Schumer was in contact with the CEO of GrubHub Matt Maloney over fraudulent fees the food-delivery giant has been charging restaurants nationwide and demands full refunds for cheated customers.

GrubHub was charging restaurants fees for phone calls that didn’t result in food orders and the company admitted wrongdoing.

The company responded by offering only 60 days’ worth of refunds even though this dark practice had taken place for years.

The exploitation took place because of in-house algorithms that calculate fees, which restaurants say can range between $5 and $9 for a single phone call.

GrubHub recently refunded one New York City restaurant vendor over $10,000 for the fraud, covering fees going back to 2014.

GrubHub agreed to extend the refund to 120 days of ill-gotten fees, but many regulators have said this is still not enough.

Then if you didn’t think that was bad, GrubHub had its hand in anti-competitive tactics that sum up the plight of the company.

GrubHub has been creating fake websites, impersonating third party restaurants by undercutting them to take control over their own web sites then taking a larger cut of commissions.

The company says that the fake websites are “a service” for clients, but when the cybersquatting has been to the detriment to the restaurant, using this point of leverage to swindle restaurants out of more fees and sometimes charging them more than 400% of the actual cost.

This insane move has strained relations and murdered trust between GrubHub and outside vendors while making it extraordinarily difficult to take back control over their website.

As you would expect, GrubHub is monetarily incentivized to control the thoroughfare.

A GrubHub spokesman commented saying there would be “no changing of our algorithm” but from how I see it, the writing is on the wall, the equity in the company is in a vicious spiral downward.

It’s hard to make money in restaurants but GrubHub is overreaching big time.

Invest in this company at your peril and avoid all online food delivery platforms, they are simply ghastly investments.

“Computers are useless. They can only give you answers.” – Said Artist Pablo Picasso

Mad Hedge Technology Letter

September 30, 2019

Fiat Lux

Featured Trade:

(COMMISSION-FREE TRADING IS HERE)

(IBKR), (ETFC), (SCHW), (AMTD)

It’s been a long time coming since I first started trading 50 years ago and was charged 25 cents a share to place an order.

The race to zero is over in internet discount brokering world as Interactive Brokers Group, Inc. (IBKR) announced IBKR Lite, a new offering that will provide commission-free, unlimited trades on US exchange-listed stocks and Exchange Traded Funds (ETFs).

It was just a matter of time before one of the big internet brokerages started to offer zero commissions and this move will force the likes of Charles Schwab (SCHW), E-trade (ETFC), TD Ameritrade (AMTD) to follow suit in order to stay competitive.

I’ve written numerous times that this was going to happen and Robinhood, the millennial broker of choice, was the trendsetter coming out the gates with zero commissions and forcing the traditional broker’s hand.

The future is now and welcome to the funeral of trading commissions.

IBKR Lite is for traders seeking a simple, cost-free way to trade US exchange-listed stocks and ETFs and will complement Interactive Brokers’ existing services, which will be rebranded as IBKR Pro. IBKR Lite will be available in October.

I am not surprised that it is Interactive Brokers that is first to roll out a no-commission product.

They are, by far and away, the king of big volume trading and their commissions weren’t that high in the first place.

The customer they deal with is not like the Schwab’s or Fidelity’s who hardly generate large volumes.

Interactive Brokers is able to provide superior pricing because they specialize in data and automating.

This will enable the firms to offer no account minimums and means it will be free to maintain an account for IBKR Lite for professional and retail investors.

What will happen is that Interactive Brokers will sell off your data to analytic companies who know how to scrape the value out of these numbers.

Investors can choose between using IBKR Lite and IBKR Pro and switch between the two levels of service up to three times and then once per quarter.

The broker will re-route the orders of IBKR Lite clients to market makers in exchange for receiving payment for order flow.

Clients that prefer IBKR Pro will continue to receive the best prices generated from a sophisticated algorithm.

So, it becomes a backdoor revenue-generating function like Facebook who resells personal data to third-party analytics companies and in turn allow users to use their platform.

Order flow is inherently valuable for many high-frequency traders (HFT).

But I would say offering trade execution is an actual service where Facebook doesn’t offer anything of note.

A platform to “share” your personal information is not an actual product in my world no matter how you tweak the verbiage.

Either way, the price to the trader is now zero and anyone who trades large volumes is incentivized to go sign up with Interactive Brokers.

This industry has been getting away with highway robbery for years by not only selling order flow but also charging $4.95 or more to trade stocks and ETFs on top of the order flow revenue.

Once the best of the rest see trading volume evaporating as order flow migrates to IBKR, what other options do they have?

I predict that not every broker will be able to execute in this new model and consolidation will be ripe in the future as the weak perish.

As long as these other broker’s stick with the $4.95 per trade of yore, I hate to do it, but slapping on a sell rating is justified.

Welcome to the brave new world of discount stockbroking.

“I am so disturbed by kids who spend all day playing videogames.” – Said Founder of Oracle Larry Ellison