Mad Hedge Technology Letter

July 24, 2019

Fiat Lux

Featured Trade:

(CIAO SILICON VALLEY),

(AAPL), (CRM), (MSFT), (FB), (AMZN), (GOOGL)

Mad Hedge Technology Letter

July 24, 2019

Fiat Lux

Featured Trade:

(CIAO SILICON VALLEY),

(AAPL), (CRM), (MSFT), (FB), (AMZN), (GOOGL)

Bridgewater Associates Founder Ray Dalio carefully articulates an economic landscape in which the unrelenting chase for short-term tech profits finally catches up meaningfully with the gyrations of tech shares.

All of this could come home to roost and the early manifestations can be found in the housing migratory trends.

The robust housing demand, lack of housing supply, mixed with the avalanche of inquisitive tech money will propel these housing markets to new heights and this phenomenon is happening as we speak.

Salesforce Founder and CEO Marc Benioff has lamented that San Francisco, where ironically he is from, is a diabolical “train wreck” and urged fellow tech CEOs to “walk down the street” and see it with their own eyes to observe the numerous homeless encampments dotted around the city limits.

The leader of Salesforce doesn’t mince his words when he talks and beelines to the heart of the issues.

After relinquishing some of his CEO duties to newly anointed Co-CEO Keith Block, Benioff will have the operational time and a wealth of resources to get on top of the pulse of not only tech issues but bigger picture stuff and he now has a mouthpiece for it with Time Magazine which he and his wife recently bought.

In condemning large swaths of the beneficiaries of the Silicon Valley ethos, he has signaled that it won’t be smooth sailing forever.

In tech wonderland, and he urged companies to transform their business model if they are irresponsible with user data.

The tech lash could get messier this year because companies that go rogue with personal data will face a cringeworthy reckoning as the techlash fury seeps into government policy and the social stigma worsens.

I have walked around the streets of San Francisco myself.

Places around Powell Bart station close to the Tenderloin district are eyesores littered with used syringes that lay in the gutter.

South of Market Street isn’t a place I would want to barbecue on a terrace either.

Summing it up, the unlimited tech talent reservoir that Silicon Valley gorged on isn’t flowing anymore because people don’t want to live there now.

This tech talent, equipped with heart-tugging stories from siblings and anecdotes from classmates getting shafted by the San Francisco dream, has recently put the Bay Area in the rear-view mirror for many who would have stayed if it were 20 years ago.

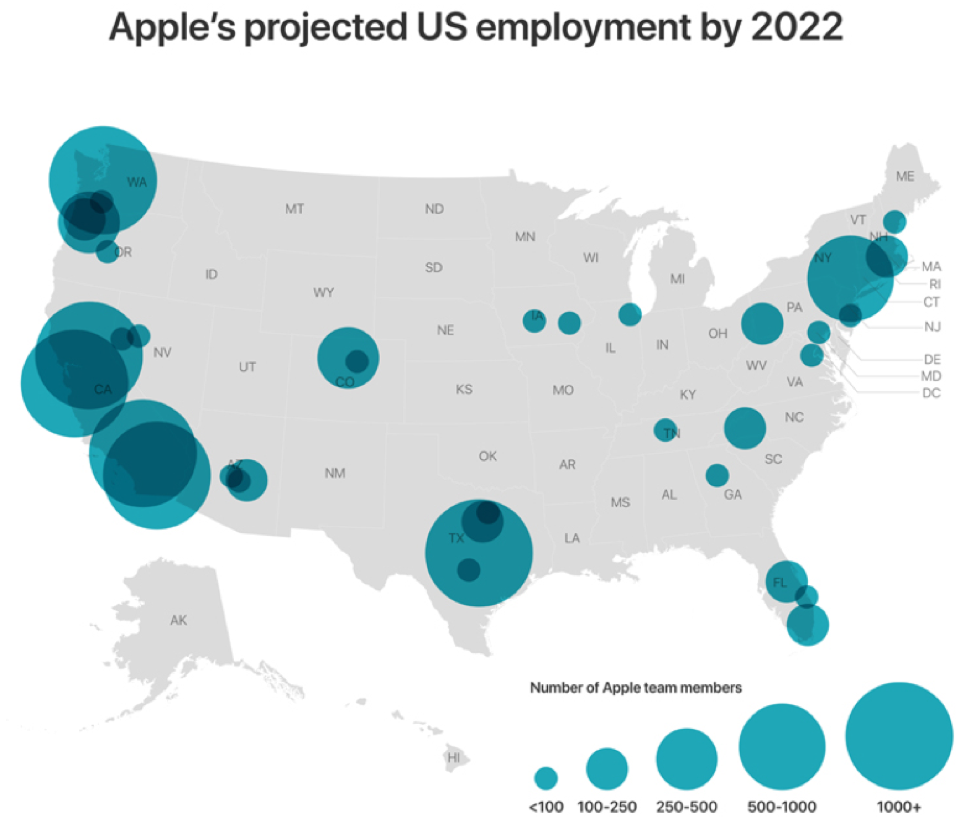

This is exactly what Apple’s $1 billion investment into a new tech campus in Austin, Texas and Amazon adding 500 employees in Nashville, Tennessee are all about.

Apple also added numbers in San Diego, Atlanta, Culver City, and Boulder just to name a few.

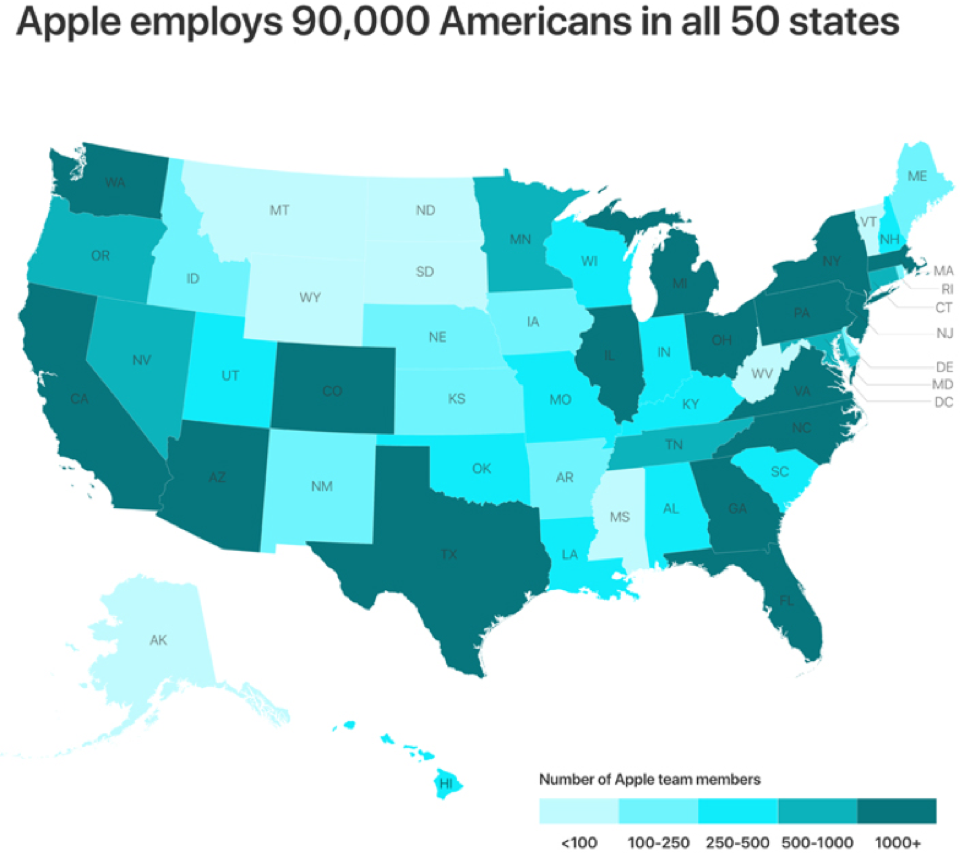

Apple currently employs 90,000 people in 50 states and is in the works to create 20,000 more jobs in the US by 2023.

Most of these new jobs won’t be in Silicon Valley.

Since the tech talent isn’t giddy-upping into Silicon Valley anymore, tech firms must get off their saddle and go find them.

The tables have turned but that is what happens when the heart of western tech becomes unlivable to the average tech worker earning $150,000 per year.

Driving out young people who envision a long-term future elsewhere than the San Francisco Bay Area forces Silicon Valley to adapt to the new patterns revealing themselves.

Sacramento has experienced a dizzying rise of newcomers from the Bay Area itself.

Some are even commuting, making that 60-mile jaunt past Davis, but that will give way to entire tech operations moving to the state capitol.

Millennials are reaching that age of family formation and they are fleeing to places that are affordable and possible to become a new home buyer.

These are some of the practical issues that tech has failed to embrace and to maintain the furious pace of growth that investors' capricious expectations harbor.

Silicon Valley will have to become more practical adding a dash of empathy as well instead of just going by the raw and heartless data.

We aren’t robots yet, and much of the world still augurs to emotional decisions and disregards the empirical data.

But, instead of physical offices being planted in the Bay Area, the tech industry will heed way to the “spirit” of Silicon Valley with offices in far-flung places.

And remember that all of these new tech talent strongholds will need housing, and housing that an IT worker making $150,000 per year desires.

No wonder why San Jose real estate has dropped in the past year, people and their paychecks are on the way out.

Mad Hedge Technology Letter

July 22, 2019

Fiat Lux

Featured Trade:

(DOES ARTIFICIAL INTELLIGENCE WORK FOR YOU?),

(TSLA), (AMZN), (FB)

Anti-A.I. physicist Professor Stephen Hawking was a staunch supporter of preserving human interests against the future existential threat from machines and artificial intelligence (A.I.).

He was diagnosed with motor neuron disease, more commonly known as Lou Gehrig's disease, in 1963 at the age of 21 and sadly passed away March 14, 2018 at the age of 76.

Famed for his work on black holes, Professor Hawking represented the human quest to maintain its superiority against quickly advancing artificial acculturation.

His passing was a huge loss for mankind as his voice was a deterrent to A.I.'s relentless march to supremacy. He was one of the few who had the authority to opine on these issues. Gone is a voice of reason.

Critics have argued that living with A.I. poses a red alert threat to privacy, security, and society as a whole. Unfortunately, those most credible and knowledgeable about A.I. are tech firms. They have shown that policing themselves on this front is remarkably unproductive.

Mark Zuckerberg, CEO of Facebook (FB), has labeled naysayers as "irresponsible" and dismissed the threat. After failing to prevent Russian interference in the last election, he is exhibiting the same defensive posture translating into a de facto admission of guilt. His track record of shirking accountability is becoming a trend.

Share prices will materially nosedive if A.I. is stonewalled and development stunted. Many CEOs who stake careers on doubling or tripling down on A.I. cannot see it die out. There is too much money to lose.

The world will see major improvements in the quality of life in the next 10 years. But there is another side to the coin which Zuckerberg and company refuse to delve into...the dark side of technology.

Defective Amazon (AMZN) Alexa recently produced unexplained laughter because of a mistaken command to start laughing. Despite avoiding calamity, these small events show the magnitude of potential chaos capable of haywire A.I. functions. If one day a user attempts to order a box of tissues and Alexa burns down the house, who is liable?

Tesla's (TSLA) CEO Elon Musk has shared his anxiety about robots flipping the script on humans. Musk acknowledges that A.I. and autonomous vehicles are important factors in the battle for new technology.

The winner is yet to be determined as China has bet the ranch with unlimited resources from Chairman Xi.

The quagmire with China has been squarely centered around the great race for technological supremacy.

A.I. is the ultimate X factor in this race and whoever can harness and develop the fastest will win.

Musk has hinted that robots and humans could merge into one species in the future.

Is this the next point of competition among tech companies? The future is murky at best.

Bill Gates noted that robots should be taxed like humans.

This reflects the bubble in which the ultra-elite reside.

This comment implies that humans and robots are at the same level. It shows a severe lack of empathy for the 40% of working Americans who will be replaced by machines over the next 10 years.

The West is comprised of a deeply hierarchical system of winners and losers. Hawking's premise that evolution has inbuilt greed can be found in the underpinnings of America's economic miracle.

Wall Street has bred a culture that is entirely self-serving regardless of the bigger system in which it finds itself.

Most of us are participating in this perpetual money game chase because our system treats it as a natural part of life.

A.I. will help more people do well in this paper chase to the detriment of the majority.

Quarterly earnings performance is paramount for CEOs.

Return value back to shareholders, or face the sack in the morning.

It's impossible to convince anyone that America's capitalist model is deteriorating in the greatest bull market of all time.

Wall Street has an insatiable hunger for cutting-edge technology from companies that sequentially beat earnings and raise guidance.

Flourishing technology companies enrich the participants creating a Teflon-like resistance to downside market risk.

The issue with Professor Hawking's work is that his timeframe is too far in the future.

Professor Hawking was probably correct, but it will take 25 years to prove it.

The world is quickly changing as science fiction becomes reality.

The year 2020 will signal the real beginning of A.I. in tangible form when autonomous fleets flood main streets and is another step in the direction of human's overreliance on machines.

People on Wall Street are a product of the system in place and earn a tremendous amount of money because they proficiently execute a specialized job.

Traders are busy focusing on how to move ahead of the next guy.

Firms building autonomous cars are free to operate as is.

Hyper-accelerating technology spurs on the development of A.I., machine learning, and enhanced algorithms.

Record profits will topple, and investors will funnel investments back into an even narrower grouping of technology stocks after the weak hands are flushed out.

Professor Hawking said we need to explore our technological capabilities to the fullest in order to avoid extinction.

In 2019, exploring these new capabilities still equals monetizing through the medium of products and services.

This is all bullish for equities as the leading companies associated with A.I. have a red carpet laid out in front of them.

And let me remind you that technology is still the least regulated industry on the planet even if sentiment has pivoted this year.

The only solution is keeping companies accountable by a function of law or creating a third-party task force to regulate A.I.

In 2019, the thought of overseeing robots sounds crazy.

However, by 2020, it might be as normal as uncontrollable laughter from your smart home device.

Mad Hedge Technology Letter

July 19, 2019

Fiat Lux

Featured Trade:

(CLOUD 101)

(AMZN), (MSFT), (GOOGL), (DOCU), (CRM), (ZS)

Global Market Comments

July 17, 2019

Fiat Lux

Featured Trade:

(THE LEADER OF THE PACK),

(GOOGL)

The future is coming a lot faster than anyone expected.

Waymo, once the top-secret Alphabet autonomous driving subsidiary, has beaten all comers to the punch.

The desert state of Arizona granted a permit for it to commence with their autonomous fleet as a commercial entity and the business has rolled out to select riders.

This permit means that Waymo’s futuristic robo-taxi can charge passengers for profit.

The vehicles started testing in 2017 and were monitored with a human safety engineer inside. This is a big deal from a regulatory point of view.

First mover advantage is pivotal in dictating an agenda and setting the rules of the road in the world of innovation.

The desperation of being first to market was epitomized by an email that former top engineer Chris Urmson sent Alphabet founders Larry Page and Sergey Brin, “We have a choice between being the headline or the footnote in history’s book on the next revolution in transportation. Let’s make the right choice.”

Waymo, a subsidiary of Alphabet (GOOG), is the preeminent force in the quest for mass market driver-less vehicles.

Before Waymo was coined, Google's self-driving-car research was an internal program referred to as Project Chauffeur. The project was created in 2009, hidden from the public eye to keep its technology safeguarded from intruders.

Alphabet invested at least $1.1 billion between 2009 and 2015 to grab the undisputed lead position of this newly created industry.

Most industry analysts estimate that commercialization of level 4 self-driving vehicles will occur sometime around 2020.

The time sensitivity is palpable as Waymo has a chance to flood American streets with its technology before GM (GM) or Uber can get off the starting blocks.

Waymo outmuscled its opponents reaching a Level 3 standard in 2012.

Level 4 is the grade that automakers wish to proceed with. Although not fully Level 5 automated, Level 4 technology can operate under controlled factors without a driver.

The Fiat Chrysler minivans tricked out with Waymo technology have been racking up test miles in Phoenix, Arizona to the tune of around 5 million on Level 4 technology.

Arizona has been a fertile breeding ground for driver-less car development since 2015 when Governor Doug Ducey signed an executive order giving authority to state agencies to “undertake any necessary steps to support the testing and operation of self-driving vehicles on public roads within Arizona.”

The success or failure in Arizona will go a long way to test the quality and sustainability of this new phenomenon.

It helps a lot that Phoenix streets are laid out in a simple grid that the current level of artificial intelligence finds easy to recognize and understand.

Waymo is essentially Uber with no driver.

Drivers cost money. Waymo hopes to remove the highest input in ride sharing transport - the driver itself.

Uber routinely shells out driver subsidies equating to around 72% of quarterly gross revenue.

Waymo plans to expand its coverage to other locations.

Google CFO Ruth Porat has gone on record saying “We do continue to explore a range of options beyond the program we’re piloting in Phoenix, including ride sharing and personal use vehicles, logistics, deliveries, and working with cities to help them address public transportation objectives.”

The first commercial operation has been groundbreakingly successful in Arizona and is crucial to enhance consumer sentiment for reliable driver-less vehicles.

The accumulated data will be vital to prove Waymo’s safety record.

If all goes smoothly, Waymo’s autonomous vehicles and technology will spread like wildfire to other locations.

The potential success will fundamentally change the way people live their lives.

Up to 10 million employed drivers are set to be on the chopping block in America.

That includes about 3.5 million professional truck drivers who earn between $30,000-$45,000 per year along with 2 million Uber/Lyft drivers participating in the gig economy at $7.25 an hour.

The mass adoption of autonomous vehicles will eliminate a huge chunk of the American workforce, while redrawing additional income streams to Alphabet (GOOG).

Insurance companies would take a direct hit with the future pipeline of drivers irrevocably thwarted from learning how to drive.

If the preliminary data comes up roses, parents will not allow their 16-year-old kid to learn how to drive and instead throw them into a Waymo to be chauffeured to school.

Also, the tragic 40,000 annual fatalities caused by motor vehicle crashes will drop off a cliff.

The pick up in productivity would be astounding as workers will no longer need to drive themselves anymore, cutting costs and allowing additional time to work while in transit.

The unintended consequences will change the world while making the leaders of the space richer. A deeper underlying effect is that it will strengthen (GOOG)’s credentials going forward to apply A.I. in other spheres.

“If you do build a great experience, customers tell each other about that. Word of mouth is very powerful.” – Said Founder and CEO of Amazon Jeff Bezos

Mad Hedge Technology Letter

July 15, 2019

Fiat Lux

Featured Trade:

(HOW SOFTBANK IS TAKING OVER THE US VENTURE CAPITAL BUSINESS),

(SFTBY), (BABA), (GRUB), (WMT), (GM), (GS)

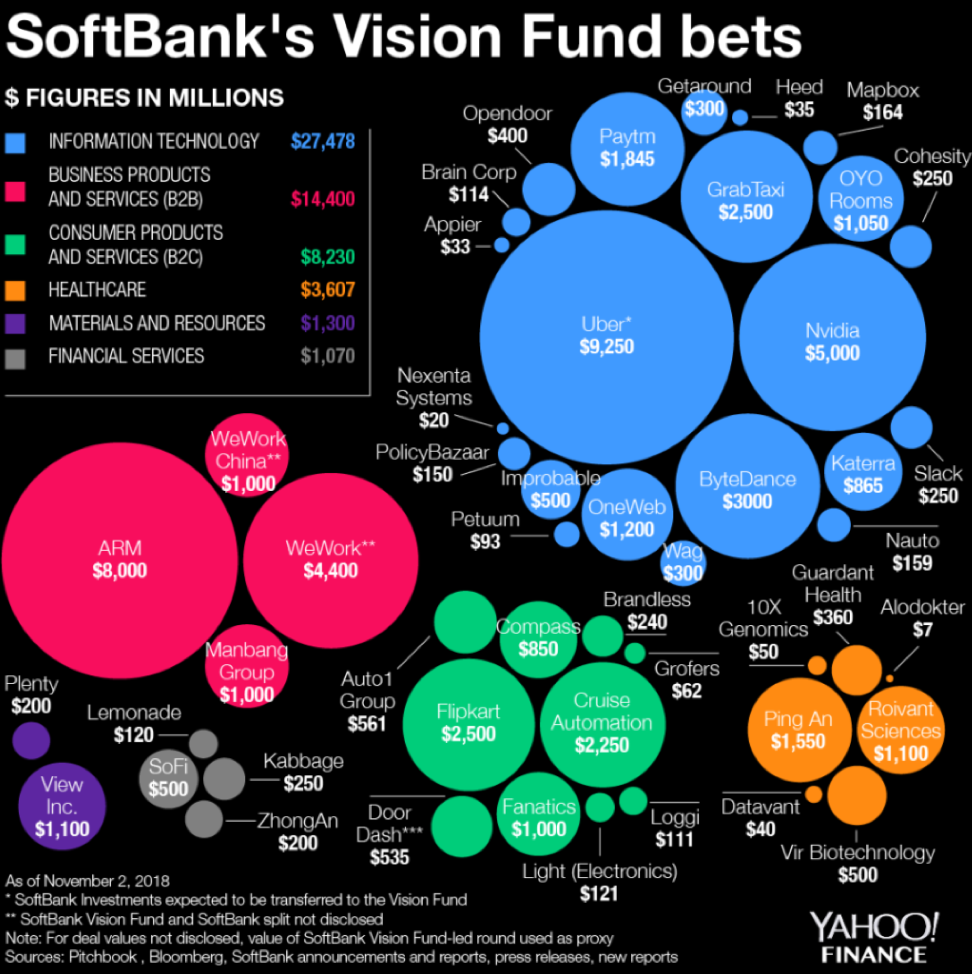

The man with the 300-year vision - Softbank’s Masayoshi Son.

He is the sole force exerting stultifying pressure on the venture capitalists of Silicon Valley.

What a ride it has been so far.

His $100 billion SoftBank Vision Fund has put the Sand Hill Road faithful in a tizzy – utterly revolutionizing an industry and showing who the true power resides with.

He has even gone so far as to double down on his exploits by claiming that he will raise additional $100 billion fund every few years and spend $50 billion per year.

This capital logically would flow into what he knows best – technology and the best technology money can buy.

Lately, Son said it best of the performance of the Vision Fund saying, “Results have actually been too good.”

So good that after this June, Son changed his schedule to spend 3% of his time on his telecom business down from 97% before June.

His telecommunications business in Japan has turned into a footnote.

It was just recently that Son’s tech investments eclipsed his legacy communications company.

Son vies to rinse and repeat this strategy to the horror of other venture capitalists.

The bottomless pit of capital he brings to the table predictably raises the prices for everyone in the tech investment world.

Son’s capital warfare strategy revolves around one main trope – Artificial Intelligence.

He also strictly selects industry leaders which have a high chance of dominating their field of expertise.

Geographically speaking, the fund has pinpointed America and China as the best sources of companies. India takes in the bronze medal.

His eyes have been squarely set on Silicon Valley for quite some time and his record speaks for himself scooping up stakes in power players such as Uber, WeWork, Slack, and GM (GM) Cruise.

Other stakes in Chinese firms he’s picked up are China’s Uber Didi Chuxing, China’s GrubHub (GRUB) Ele.me and the first digital insurer in China named Zhongan International costing him $500 million.

Other notable deals done are its sale of Flipkart to Walmart (WMT) for $4 billion giving SoftBank a $1.5 billion or 60% profit on the $2.5 billion position.

In 2016, the entire venture capitalist industry registered $75.3 billion in capital allocation according to the National Venture Capital Association.

This one company is rivalling that same spending power by itself.

Its smallest deal isn’t even small at $100 million, baffling the local players forcing them to scurry back to the drawing board.

The reverberation has been intense and far-reaching in Silicon Valley with former stalwarts such as Kleiner Perkins Caufield & Byers breaking up, outmaneuvered by this fresh newcomer with unlimited capital.

Let me remind you that it was once considered standard to cautiously wade into investment with several millions.

Venture capitalists would take stock of the progress and reassess if they wanted to delve in some more.

There was no bazooka strategy then.

SoftBank has promised boatloads of capital up front even overpaying in some cases in order to set the new market price.

Conveniently, Son stations himself nearby at a nine-acre estate in Woodside, California complete with an Italianate mansion he bought for $117.5 million in 2012.

It was one of the most expensive properties ever purchased in the state of California, even topping Hostess Brands owner Daren Metropoulos, who bought the Playboy Mansion from Hugh Hefner in 2016 for $100 million.

If you think Son is posh – he is not. He only fits himself out in the Japanese budget clothing brand Uniqlo. He just needed a comfortable place to stay and he hates hotels.

SoftBank hopes to cash in on its $4.4 billion investment in WeWork, an American office space-share company, proclaiming that WeWork would be his “next Alibaba.”

The company plans to shortly go public.

Son continued to say that WeWork is “something completely new that uses technology to build and network communities.”

Other additions to SoftBank’s dazzling array of unicorns is Bytedance, a start-up whose algorithms have fueled shot form video content app TikTok.

The deal values the company at $75 billion.

They have been able to insulate themselves from local industry giants Tencent and Alibaba.

Son has revealed that the Vision Fund’s annual rate of return has been 44%.

Cherry-picking off the top of the heap from the best artificial intelligence companies in the world is the secret recipe to outperforming your competitors.

At the same time, aggressively throwing money at these companies has effectively frozen out any resemblance of competition. Once the competition is frozen out, the value of these investments explodes, swiftly super-charged by rapidly expanding growth drivers.

How can you compete with a man who is willing to pay $300 million for a dog walking app?

This genius strategy has made the founder of SoftBank the most powerful businessman in the world.

Son owns the future and will have the largest say on how the world and economies evolve going forward.