"We are unicorn hunters." - Said Founder and CEO of SoftBank Masayoshi Son

"We are unicorn hunters." - Said Founder and CEO of SoftBank Masayoshi Son

Mad Hedge Technology Letter

July 12, 2019

Fiat Lux

Featured Trade:

(CLOUD SECURITY ON THE MARCH)

(OKTA), (ZS), (CRM), (AMZN)

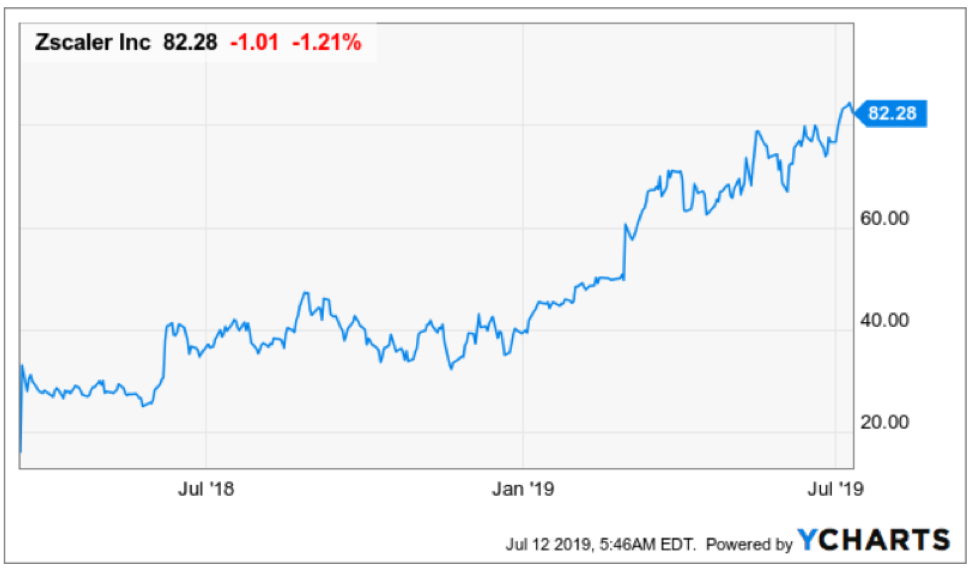

Take a look at these beauties that I recommended at the beginning of December 2018.

At that time, Okta (OKTA) was trading at $62 and Zscaler (ZS) was at $40 on the button – fast forward to today and Okta is now over $136 and Zscaler victoriously sitting at $82.

Oh, how do times change!

That was my reaction watching their performance for the past 7 months giving belief to my assessment that second-tier cloud companies will have a field day this year.

Cloud companies aren’t going away anytime soon, please tattoo that on your forehead.

There isn’t a hotter topic circulating the gossip winds these days than digital security pressured by geopolitics.

Okta is the best in show for identity management – a snazzy term for managing employees’ passwords.

Okta’s products are built on top of the Amazon Web Services cloud.

Coincidentally, Okta was erected in 2009 by a team of former Salesforce (CRM) executives. Salesforce is one of my favorite cloud-based software companies, offering a blueprint for success to other up-and-coming software companies.

Current Okta CEO and founder Todd McKinnon previously served as the Senior Vice President of Engineering at Salesforce.

Other founders include Okta COO Freddy Kerrest who also meandered through the corridors of Salesforce.

I can tell you that you could do much worse than starting a new software company with a collection of Salesforce upper echelon talent.

This all-star team is behind the insatiable growth of Okta whose revenue has grown over 600% since establishing itself.

Okta’s first-quarter results didn’t disappoint with revenues of $125 million—a rise of 50% year-over-year beating the consensus of $117 million.

Subscription revenues comprised 94% of sales and the company expects sales of $130 million amounting to a rise of 37% year-over-year.

Okta’s subscriber base has risen over 500% in the past 5 years and annual contract value of over $100,000 has expanded 60% annually.

The company still loses money but hopes to make some headway on this issue with projected EPS estimated to grow 25% annually in the next five years.

This year spawned a massive divergence between tech who has legs and tech who will be dragged down to the depths of the ocean floor by the heavy weight of regulation, overwhelming competition, or just flat out poor management or inferior product development.

Zscaler echoed similar positive sentiment of Okta by recording a quarter to remember growing revenue by 61% year-over-year while calculated billings grew 55% year-over-year.

In addition to the top line growth, operating margins improved 14% points year-over-year to 8%.

The quarterly results demonstrate the leverage in cloud security business models and the ability to drive growth and profitability.

String together a third consecutive quarter of profitability is just part of the battle, Zscaler will continue to aggressively invest for significant market opportunity that lie ahead.

Cloud security potential means going after a $20.3 billion Total Addressable Market in calendar 2019.

Let me divulge a tad bit about the competitive landscape and why Zscaler is brilliantly positioned for success.

As organizations increasingly make the shift to the cloud, traditional firewall and VPN vendors are finally acknowledging that the legacy security appliances can secure the new digital enterprise and are attempting to build a security cloud using single tenant software designed for on-premise appliances just like you can't create a Netflix service by stacking thousands of DVD players in the cloud.

You can't offer an inline high-performance security cloud by spinning up a bunch of virtual machines in a public cloud. This is a defensive strategy of cloud imitators which, in our view, serves the self-preservation of the vendor, not the needs of the customers.

Zscaler has a significant competitive advantage as a result of the technology, architecture and maturity of cloud security platform including one, Zscaler was born in the cloud, for the cloud just like Salesforce and Workday.

Two, Zscaler has a purpose built globally distributed multi-tenant cloud for fast user experience, unlike imitation cloud, Zscaler requires no back hauling from front doors to a central computing data center of a public cloud.

Three, Zscaler performs SSL inspection at scale as a purpose-built proxy for better security.

Lastly, Zscaler continues to deliver zero trust network access that provides application access without network access reducing business risk unlike firewalls and VPNs.

The duo of Okta and Zscaler are the bright lights of the cloud generation and leading the digital economy in digital security.

"Software is like Lego. You can make anything with it, but it may not be appropriate." - CEO of IMC Worldwide Stuart Sherman

Mad Hedge Technology Letter

July 10, 2019

Fiat Lux

Featured Trade:

(THE LOPSIDED WORLD OF TECH)

(FB), (GOOGL)

Is it unfair?

No, technology is afforded higher multiples than other industries and it’s completely justified.

Don’t allow anyone to convince you that tech companies are expensive because there are plausible reasons why they are expensive and will get even more expensive.

Technology sits on its perch as the single best investment opportunity of not only our lifetime but our children’s lifetime as well.

Huge capital investment is pouring into this glorious opportunity from gleaming offices on Wall Street to Sand Hill Road venture capitalists and even the Saudi Royal Family.

What is money not going into?

If you drive around the urban and suburban roads of America, it’s obvious that not much is going into new infrastructure.

America hasn’t even built a new airport for the past 30 years which CEO of JP Morgan loves to remind his followers of.

The sad truth is that capital is spilling over into the technology sector.

Eclipsing anything that you might believe, technology provides the optimal vehicle to innovate and evolve while offering a platform to incite a surge in performance and profitability.

The agent that is being harnessed to innovate and evolve is the software that is being programmed up to help a slew of other sectors.

Even if a sector hasn’t been touched by the tentacles of software innovation, they rarely stay virgin for long.

Much of the incubator stage capital is funnelled into considerable expenditures on research and development by technology companies, but also the capital is the catalyst to a reactionary tale of steroidal growth fueled by a pipeline of innovative products, services, and unique features.

These products and services are then spread through and delivered to ancillary arteries that serve the subset of the broader economy.

The result is a massive tsunami in incremental productivity when high grade software supercharges every business that implements and integrates the software inside the confines of their business structure.

The supercharge effect of software rapidly forces companies to either evolve fast or go extinct, meaning that whole industries are transformed overnight when they get a whiff of what is happening with their competitor.

Computers and hardware used to take up entire warehouses - they were oversized, bloated, and tended to perform poorly at first.

The evolution of hardware has delivered shiny, modern pocket-sized devices packed with potency.

CEOs are able to manage companies of 10,000 employees just on a screen the size of a wallet all harnessed by, you got it - software.

Even more unbelievable is that the concept of technology must outdo itself, upgrading with every iteration in an increasingly short amount of time, or be cannibalized by a competitor in a blink of an eye.

In the survival of the fittest, the tech industry is the alpha male industry of the American economy.

Nobody understands in what form or shape it will manifest itself in just down the road but it will be the 800-pound gorilla in the room.

Even though software is the fulcrum of the tech industry today, it doesn’t mean it will always be that way.

Trends diverge quickly and you can even ask a semiconductor executive facing a bout of weakness stemming from geopolitical one-upmanship.

Semiconductor companies have been dragged into the middle of a hegemonic battle between the two most dominant economies in the world and revenues will degenerate short term.

Key semi products will not be relinquished because the artificial intelligence that complements these high-grade chips will be the crucial element that determines who runs the world once 5G networks are erected.

Taking away the building blocks that facilitates the artificial intelligence will make it more difficult to produce the finished product.

Handheld devices are another product that has been sidelined for the time being because the global market is currently saturated by smartphones and tablets.

Software has been a key theme for the Mad Hedge Technology Letter and there are no signs of abatement for the foreseeable future.

The truth is that the world will not function without software as we know it and the omnipresence of software stems from the need to automate everything from healthcare devices down to autonomous vehicles.

Even better, software can withhold devastating economic capitulation as many of these companies have bought in to the software miracle and is a fixed part of their model that can’t be replaced.

Just the bare bones type of model badly needs sufficient IT functions to survive.

Then consider that cybersecurity is more and more a part of management’s plan to protect the digital fort from the back to front.

Software requires minimal infrastructure and is difficult to protect via patents or copyright to any effective degree signaling that if software isn’t perpetually improving, they are at risk of being disrupted.

The low barriers of entry consequently mean grassroots start-ups with innovative, game-changing products can appear with a wave of a wand.

After-sales support of the software is becoming a critical part of revenue as software is becoming more complex and requires granular consultation to apply the full range of capabilities demanded of it.

Software as a service (SaaS) is the new payment model that has also poured gas onto the revenue flames.

Software programs used to be purchased once for a fixed price.

The exchange of tender resulted in the consumer obtaining CDs that they inserted into a personal computer hard drive then installed on the desktop.

The technology industry shaped up and realized it could not only extract a one-time fee for software services but accrue an annual fee with the promise of timely and prompt upgrades via the cloud.

A win-win situation unfolded.

In some cases, this has allowed the same companies to make 500% more from the same product and deliver higher performance through enhanced functionality by deploying frequent updates.

And yes, the trade war is stealing some of the tech industries mojo, but software stocks will be most insulated.

The long-term trends are still intact and investors must understand these stocks have had incredible run-ups the past few years, not to mention a great first half of 2019 that saw most software stock rise over 30%.

Investors should be patient and advantageous entry points will be served on a platter but also differentiate between good and bad software stocks.

“Our production system was based on knowledge from former Toyota engineers and we've incorporated a Japanese quality control system too.” – Said CEO of Huawei Ren Zhengfei

Mad Hedge Technology Letter

July 8, 2019

Fiat Lux

Featured Trade:

(YOUR UNCONSCIOUS FUTURE)

(FB), (GOOGL)

This might be one of the most important newsletters you will ever read.

Economies are mainly defined by seismic revolutions, for example, the industrial revolution that cut down simple, archaic jobs to machinery.

As we are on the verge of shuttering the technological revolution that brought us a party bag of treats like the internet, search engines, smartphones and the personal computer, we must brace ourselves for what is next.

Industry 4.0 is the concept of dazzling smart factories augmented by machines connected to a cloud network and software that processes the operations within the system.

The productivity enhancement will boost performance as machines will be able to visualize and surgically solve problems by applying the software that powers it.

Data exchange in manufacturing technologies which include cyber-physical systems (CPS), the Internet of things (IoT), the Industrial Internet of Things (IIOT), and cognitive computing are concepts that will define Industry 4.0.

As income inequality rears its ugly head and becomes center to what politicians run campaigns on, the world must brace for yet another tsunami of unrivaled job loss on levels that we have never seen before.

The social upheaval that economic chaos will create and offer investors monumental investment opportunities.

One of the manifestations of technological evolution is the optimization of business processes through automation, meaning less people are involved in the value creation process.

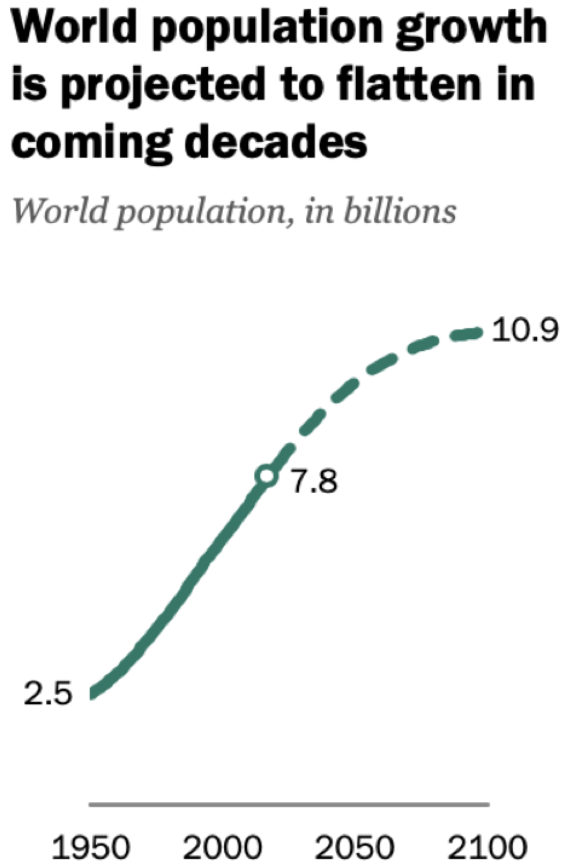

The global population is on the verge of mushrooming from 7.7 billion people in 2019 to 10.9 billion in 2100.

If you think overpopulation and sharing the world’s resources are a problem in 2019, then wait until 2050 when more people are squeezed out of revenue windfalls.

This effectively means the global middle class will accelerate its demise as the job market will bifurcate into a narrow sliver of clear winners and mostly losers and not the muddied version of what we have now.

The first Industrial Revolution also delivered uncertainty that hung over the whole job market, but the world was diverse enough and had ample resources to absorb the negative impact.

The global overpopulation is connected to the economy in the sense that most babies will be born outside of developed industrial economies and the world will see a fiercer rush to gain access to jobs in places such as London, Frankfurt, New York, Tokyo, and Silicon Valley.

The net effect of A.I. could be debated all day, specifically whether the absolute progress made in the development of industry and the products that revolve around it outweigh the torrent of human suffering that it will cause to billions of people who are not employable in that job market.

With exponential computational power to apply A.I., existing behavior will change in society and new cultures will be created because of it.

Economic value will not correlate to the amount of people like it once was, countries like Japan have dived headfirst into automating as much as possible with the best in class technology in robotics.

The world which we know it in 2019 is in the last legs of a nostalgic phase with baby boomers clinging on to what they know growing up in the 1950s.

Soon, that will be eradicated and Millennials will pour what they know and the fallacies they support into the system that is supported by algorithms and machine learning as the first human generation to be technology natives.

We are on the cusp of transformative shifts in the world.

In the next 25 years, technology will start migrating into the chambers of neuroscience.

Technology has discovered that more than 99.99% of human behavior happens at an unconscious level and that the unconscious brain is 10 times faster than the conscious brain.

While at any point of time, the conscious brain can focus only on one task, the unconscious can easily execute infinitely more.

The aspects of human behavior that the rational world has pinpointed is the conscious mind which is an ill-suited representative of human behavior.

The mechanics of the unconscious brain is stuff out of science fiction in 2019 but that will slowly change.

Consciousness has no understanding of what is happening in one’s own unconscious.

Science will be required to squeeze out a mechanism to discern the type of data humans can produce to mold this future subset of technology.

Modern qualitative techniques must be developed to be able to extract data from this important pool of knowledge.

Corporations are at the forefront of this trend and tech power brokers such as Co-Founder and CEO of Facebook Mark Zuckerberg hopes to one day install a chip into consumers' brain so that consumers can access the global network from the brain.

A scary thought but a thought gaining traction, nonetheless.

Ideally, the morally attuned stakeholders carry out the process of benefitting humankind instead of enriching a select few.

That will also be a battle that will define the next generation.

Increased focus on the unconscious processes will cause headaches for companies and there will likely be a numerical cost placed on the data it generates after companies like Facebook (FB) and Google (GOOGL) ran wild with abusing free personal data for decades.

Monitoring and managing the unconscious processes of consumers and employees will be hard at first and then society must assess if this violates privacy or not.

Unconsciousness works best when humans are sleeping or resting.

How can companies capture data on how well someone is using her unconscious brain?

This will befuddle tech companies until there is a solution.

Paradigm shifting scientific discoveries and human innovations have emanated from unconscious processes of the human brain in the past.

We still understand little about how powerful this data could become.

The current emergence of AI will be rooted purely in consciousness and the data that revolves around it, but the problem is that this data isn’t entirely accurate.

In capturing absolutes about complicated topics with current machine learning techniques, it doesn’t synthesize the fact that many areas of the human world deal in many shades of grey.

That is why A.I. is not that good today.

The next big find is if a company doubles down on the unconscious processes and that leads to groundbreaking discoveries in the understanding of accurate human behavior and thought.

“When you give everyone a voice and give people power, the system usually ends up in a really good place. So, what we view our role as, is giving people that power.” – Said Co-Founder and CEO of Facebook Mark Zuckerberg