“I even went to KFC when it came to my city. Twenty-four people went for the job. Twenty-three were accepted.” – Founder and Former CEO of Alibaba Jack Ma when asked about life after university.

“I even went to KFC when it came to my city. Twenty-four people went for the job. Twenty-three were accepted.” – Founder and Former CEO of Alibaba Jack Ma when asked about life after university.

Mad Hedge Technology Letter

June 5, 2019

Fiat Lux

Featured Trade:

(BOX TAKES A HIT)

(BOX), (MSFT), (PYPL)

REVENUE DOWNGRADES – these are meaningful side effects that many public tech companies are grappling with.

To really understand the complete picture of the technology industry, analyzing the fringes goes a long way to telling us the level of health of firms operating in the face of a mammoth trade war.

Before companies start posting decelerating revenue numbers, the warnings and preannouncements come thick and fast.

That is exactly what we have been receiving as of late.

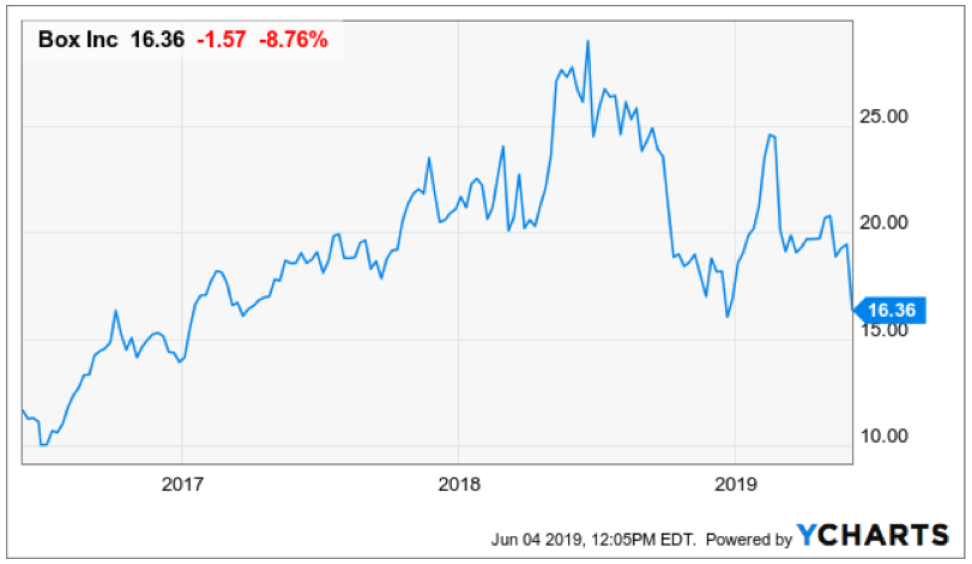

Redwood City-based cloud storage company Box (BOX) nosedived 14 percent at today’s opening after beating financial estimates but offering investors light guidance that fell short of expectations.

In fact, Box had a tidy quarter and its 16% YOY of revenue growth is performance that many industries would give a left arm for.

The $163 million in sales in the first quarter was a beat of about $1.6 million showing that cloud companies are still the kings of the modern economy.

Being that the stock market is forward-looking, mister market didn’t like what Box finished the call with.

Consensus had it that Box would deliver around $700 million of sales in 2019, but the company indicated that the souring climate because of the trade war made this highly unlikely and guided down to between $688 million to $692 million.

This won’t be the last downgrade if there are no resolutions in the next quarter, expect more than a handful to preannounce.

As we speak, both countries are digging their heels in, signaling to each other they are unlikely to budge.

Box is at an inflection point in their history where they are attempting to push their business model into a $1 billion per year operation.

This means chasing after corporate clients who have the scale and volume to satisfy these revenue goals.

Corporate clients usually are prone to having deep overseas supply chains and the diminishing success of these businesses will force them to think twice about partnering with firms like Box.

They might want to now but could put off the decision for a year or two.

The knock-on effect is massive with many areas of the expense puzzle shaved off here and there.

Expect downgrades in the quality of their office coffee beans as well.

Ultimately, many of the second-tier tech companies are at risk of issuing an imminent profit warning or if they don’t make profits, revenue downgrades will happen in the upcoming weeks.

If you thought the dollars are vanishing into thin air, you are wrong.

They still exist but are actively being pushed around to different parts of the global economy and there is one main recipient of the flow of funds.

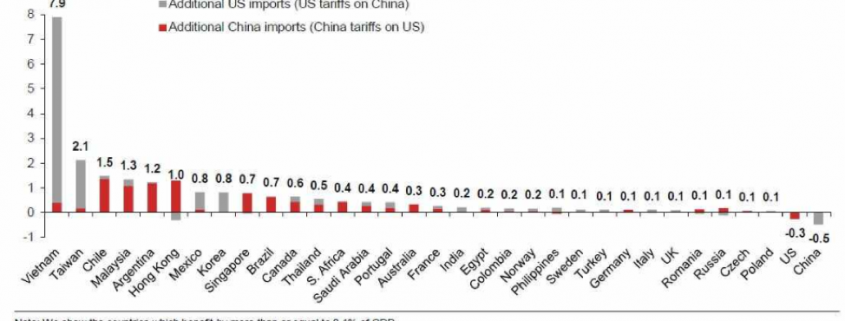

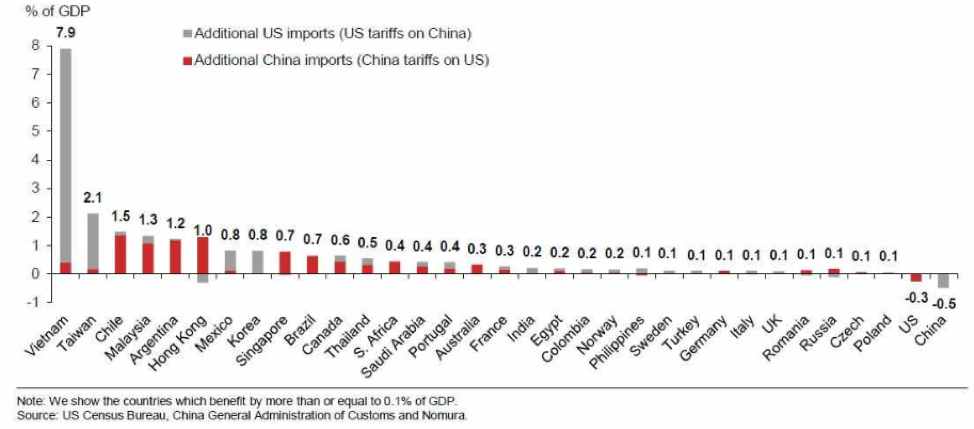

Since tariffs have created a situation where it is too expensive to export or import from America and China, one country, in particular, has welcomed an avalanche of new money.

Many supply chains are moving over to Vietnam as we speak.

Malaysia, Chile, and Argentina have also seen an uptick in trade flows.

And you can bet that every drop of manufacturing foreign capital right now is avoiding China like the plague until they get more clarity on trade policy or weighing up moving operations to America, so they aren’t charged a tariff for selling to Americans.

Many Chinese manufacturers are using a workaround - offshoring their business taking a cue from America in the 1990s.

Vietnam has already gained 7.9% of GDP in new businesses from Chinese and American corporations.

America is past the point of no return as many executives believe this could be a dog fight in the trenches until 2035.

Better to move now and salvage what they can.

Many experts have chimed in admitting that Vietnam is what China was 20 years ago, offering manufacturers cheap labor and growing know-how in high precision industries.

Throw into the mix that Vietnam has a huge Chinese minority population which many not only speak the local language but also can communicate in Chinese, then it seems like a natural fit to source goods from there.

It could play out quite ironically with American tech companies deploying this exact carbon copy of a strategy, and we might see Chinese and American factories and research centers standing shoulder to shoulder with one another dotted around Ho Chi Minh City and Hanoi.

Expect Vietnam to be the next to ride the economic rollercoaster that China enjoyed for 30 years.

Effectively, tech profits and other American industries have seen their margins and revenue repackaged and delivered to the Vietnamese economy.

The Chinese and American economies are in for some short-term grinding and if they can’t get along at some point, Vietnam and others will be handsomely rewarded.

Investors need to keep a watch out for the next batch of data from second tier tech companies that will offer a glimpse into the future and how this trade war is playing out.

I believe the cleanup hitters like Microsoft and PayPal still swing a heavy bat and that won’t go away for the rest of 2019, but the little guys could get bullied with some revenue resets.

“My favorite things in life don't cost any money. It's really clear that the most precious resource we all have is time.” – Said Co-Founder and Former CEO of Apple Steve Jobs

Mad Hedge Technology Letter

June 4, 2019

Fiat Lux

Featured Trade:

(THE GOVERNMENT’S WAR ON GOOGLE)

(GOOGL), (FB), (AMZN)

I told you so.

It’s finally happening.

The Department of Justice (DOJ) preparing an antitrust probe on Google (GOOGL) was never about if but when.

The Federal Trade Commission is in the fold as well, as they have secured the authority to investigate Facebook (FB).

The probe will peel back the corrosive layers of Facebook and Google’s businesses such as search, ad marketplace and its other assets in order to excavate the truth.

Investors will get color on whether these businesses are gaining an unfair advantage and perverting the premise of fair competition that every tech company should abide by.

Tech companies skirting the law and living on the margins are in for a stifling reckoning if these probes pick up steam.

Facebook is about to get dragged through the mud kicking and screaming facing an unprecedented existential crisis that have repercussions to not only the broad economy for the next 50 years, but far beyond American shores with America mired in a trade war pitted against the upstart Chinese most powerful tech companies.

Even though I have consistently propped up Alphabet on a pedestal as possessing a few of the most robust assets in tech, I have numerous times flogged their dirty laundry in public view, referencing the regulatory risks that could rear its ugly head at any time.

These companies have been playing with fire and everyone knows it, but in the world of short-term results via stock market earnings report, this trade kept working until governments decided to get their act together because of the accelerating erosion of government trust partly facilitated by technology apps.

As much as a handful of Americans have monetized Silicon Valley to great effect, I can tell you that I spend a great deal of my time abroad, and American soft power is at a generational low ebb.

Blame technology - our dirty secrets are not only exposed in frontal view but it’s pretty much a 3D view of the good, bad, and the ugly and there is a lot of ugly.

I am not saying that punishment is a given for these ultra-rich firms swimming in money.

Historically, Alphabet has stymied regulators before beating out an antitrust investigation in 2013 after a two-year inquiry ended with the FTC unanimously voting to halt the investigation.

Remember that this time around, the probe follows the fine in Europe when The European Union slapped Google with a $1.69 billion for actively disrupting competition in the online advertisement sector.

The European Commission claimed that Google installed exclusivity contracts on website owners, preventing them from populating on non-Google search engines.

It was quite a dirty trick, but do you expect much of anything else from one of the most crooked industries in the economy?

And this wasn’t the first time that Google has run amok.

EU regulators levied a $5 billion penalty on Google for egregious violations regarding its dominance of its Android mobile operating system.

Google was accused by the EU of favoring its in-house apps and services on Android-based smartphones giving manufacturers no alternative but to bundle Google products like Search, Maps and Chrome with its app store Play ensuring that Alphabet would benefit from a lopsided arrangement.

Anti-trust legislation has a myriad of supporters including the current administration who have stepped up its onslaught on Silicon Valley.

President of the United States Donald Trump has even hurled insults at Amazon (AMZN) creator Jeff Bezos and even claimed that Alphabet’s artificial intelligence has aided China’s technological rise.

To say FANG companies are in the good graces of Washington would be laughable.

I would point to Facebook to accelerating the regulatory headwinds as investors have seen Co-Founder and CEO Mark Zuckerberg fire every major executive that has opposed his vision of merging Facebook, Instagram, and WhatsApp into a cesspool of apps that pump out precious big data.

The tone-deaf boss has doubled down to reinvigorate the growth after Facebook sold off from $210.

Board members want Zuckerberg out and he is defiant against any attack on his leadership spinning it around as a vendetta on his reign.

Facebook is walking straight into a minefield and the rest of Silicon Valley is guilty by association, the contagion is that bad.

Facebook is the one to blame because of the daily nature of social interaction on its platform and the pursuance of revenue through hyper-targeting data that 3rd party companies pay access for.

They have no product.

Amazon sells consumer goods which is not as bad.

Facebook facilitates the social dialogue that has unwittingly boosted extremism of almost every type of form possible.

It has given the marginal and nefarious characters in society a platform in which to engineer devastating results and Facebook have an incentive to turn a blind eye to this because of the lust for user engagement.

This has resulted in heinous activities such as terror attacks being broadcasted live on Facebook like the 2019 New Zealand massacre at a mosque.

The former security chief at Facebook Alex Stamos hinted that Mark Zuckerberg’s tenure should wind down and the company needs to shape up and hire a replacement.

The security implications are grave, and many Americans have uploaded all their private information onto the platform.

What is the end game?

Facebook is in hotter water than Google, not by much, but their business model engineers more mayhem than Google currently.

Facebook could get neutered to the point that their ad model is dead and buried.

If Facebook goes down, this would unlock a treasure chest full of ad dollars looking for new avenues.

Facebook’s most precious asset is their data which might be blocked from being monetized moving forward.

Without data, they are worth zero.

The existential risk is far higher for Facebook than Alphabet.

No matter what, Alphabet will still be around, but in what form?

Assets such as YouTube, Google Search, and Waymo, which are all legitimate services, could get spun out to fend for themselves creating many offspring left to sink or swim.

In this case, YouTube, Google Maps, Chrome, Google Play, and Google Search would still possess potent value and offer shareholders future value creation.

Waymo would become a speculative investment based on the future and would be hard to predict the valuation.

Then there is the issue of whether Chinese companies would dominate the collection of FANGs after the split or not.

As I see it, Chinese tech companies will not be allowed to operate in the U.S. at all, and anti-trust repercussions will have many of these homegrown tech companies carved out of their parents to reset a level playing field in a way to re-democratize the tech economy.

This would spur domestic innovation allowing smaller companies to finally compete on a national stage.

The government finally clamping down epitomizes the current volatile tech climate and how Alphabet who has some of the best assets in the industry can go from barnstormer to pariah in a matter of seconds.

As for Facebook, they have always had a bad stench.

The cookie could still crumble in many ways, each case looks high risk for Facebook and Google for the next 365 days.

Stay away from these shares until we get any meaningful indication of how things will play out, but I have a feeling this is just the beginning of a tortuous process.

“Facebook was not originally created to be a company. It was built to accomplish a social mission - to make the world more open and connected.” – Said Co-Founder and CEO of Facebook Mark Zuckerberg

Mad Hedge Technology Letter

June 3, 2019

Fiat Lux

Featured Trade:

(WHY THE UBER IPO FAILED)

(UBER), (LYFT)

Do you want to invest in a company that loses $1 billion per quarter?

If you do, then Uber, the digital ride-sharing company, is the perfect match for you.

Uber couldn’t have chosen a worse time to go public, smack dab in the middle of a trade war almost as if an algorithm squeezed them into tariff headlines that are currently rocking the equity markets.

The tepid price action to Uber’s first period of being a public company has been nothing short of disastrous with the company tripping right out of the gate at $42.

The company that Travis Kalanick built would have been better served if they decided to go public in the middle of their growth sweet spot a few years ago.

Hindsight is 20/20.

Uber took in $2.58B last year during the same quarter and they followed that up with 20% growth to $3.1B, hardly suggesting they are delivering on hyper-growth an investor desire.

It will probably become the case of Uber hoping to manage growth deceleration as best as it can.

Infamously, the company has been busy putting out fires because of past poor leadership that threatened to blow up their business model.

The fall out was broad-based and current CEO of Uber Dara Khosrowshahi was brought in to subdue the chaos.

That worked out great in 2017 and damage control nullified further erosion in the company, but since then, management has not carved out an attractive narrative.

Just as bad, investors have no hope on the horizon that Uber can mutate into a profitable company.

It seems that costs could spiral out of control and even though the company is growing, the company is not a growth company anymore.

Investors must look themselves in the mirror and really question why they should invest in this company now.

In the short-term, positive catalysts are scarce.

The reaction to their first earnings report was slightly positive as management indicated that competition is easing up, spinning a negative issue into a positive light.

Remember that Uber bled market share after their management issues that I mentioned and Lyft (LYFT) has caught up significantly.

Lyft has also grappled with poor price action to their stock after they went public.

The result from both companies going private to public around the same time means that they will not be able to undercut each other on price because public investors will not give the same type of leash that private investors did.

This will cause losses to cauterize because subsidizing drivers will decelerate, and the pool of drivers will shrink.

In addition, passenger fares could rise because Uber will have no choice but to consider profitability when pricing rides meaning higher costs to the user.

What I am saying rings true for many tech companies and raising prices to satisfy shareholders is not a groundbreaking phenomenon.

As I see it, offering rides on the cheap could be coming to a screeching halt and nurturing margins could be the new order of the day.

The subsidizing effect can be found in the higher than normal gross bookings for the quarter of $14.65 billion, up 34% from the same period in 2018.

Cheaper fares will drive demand, and if Uber stopped helping out with the cost of rides, the 34% would fall to single digits in a heartbeat.

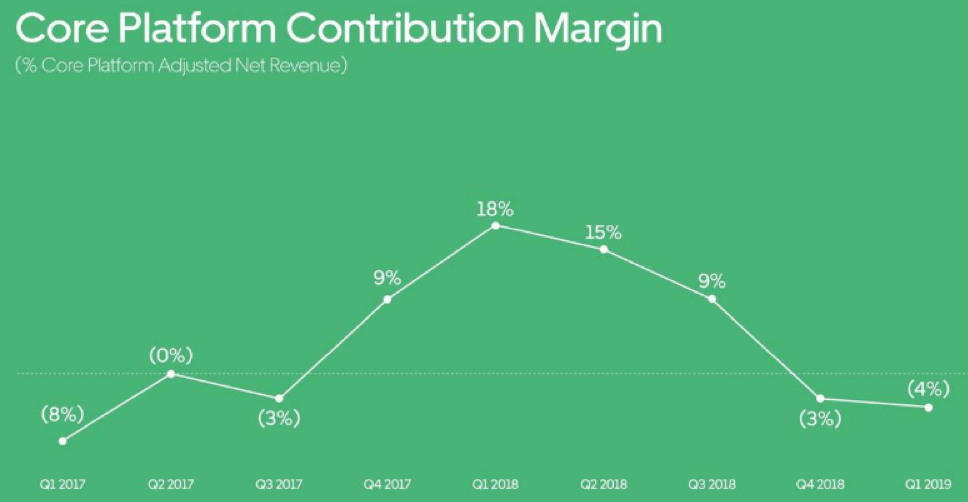

Even more worrying is the negative core platform contribution margin falling 4.5%, meaning the amount of profit it makes from its core platform business divided by adjusted net revenue is on the down.

Uber was able to post a positive 17.9% growth rate during the same period last year.

When the core business is reacting negatively, it’s time to go back to the drawing board.

I believe that the underlying problem with Uber is that they aren’t making any big moves to their business model that would put them in the position to foster hyper-growth.

Incremental changes like removing drivers who fail to collect a 4.6 or above rating and creating a subscription model for its higher growth Uber Eats division are just a drop in the bucket of what they could be doing with its brand and clout.

If investors were waiting for a big step forward with shiny announcements during the first earnings call as a public company, then they were left thirsting for more.

Uber gave us a mini baby step when they need leaps in 2019.

The bigger success might be that Uber had no monumental blow ups which is a telling sign that Uber has at least stabilized operations.

The downside with its food delivery business is that private businesses such as Postmates and DoorDash are private and can still tolerate even bigger losses which will put pressure on Uber Eats to endure the same type of losses.

As it stands, net revenue for its Uber Eats segment rose 31% to $239 million, but then investors must understand this business is scarily exposed and could be attacked by the venture capitalists boding ill for the stock.

Then considering that Uber’s fastest growing geographical segment is Latin America, last quarter was nothing short of abysmal with revenue cratering by 13% to $450 million.

Regulatory risks will cause American companies to take big write-downs the further away they operate from America, and Indian regulation is rearing its ugly head with e-commerce companies bearing the brunt of it.

Looking down the road, Uber has a faulty business model because of a lack of autonomous driving technology, and they will need to partner with a Waymo or Tesla which will destroy margins even more.

Uber has no chance of profitability in the near term, and the data suggests they have lost their growth charm.

Do not buy Uber here, it will become cheaper, and at some point, around $30, this name will be a good trade.

Management needs to up the ante in order to show investors why they are better than Lyft.

![]()

“Based on my experience, I would say that rather than taking lessons in how to become an entrepreneur, you should jump into the pool and start swimming.” – Said Co-Founder and Former CEO of Uber Travis Kalanick