Mad Hedge Technology Letter

April 30, 2019

Fiat Lux

Featured Trade:

(AMAZON’S NEW GAME CHANGER)

(AMZN), (WMT), (TGT), (UPS), (FDX)

Mad Hedge Technology Letter

April 30, 2019

Fiat Lux

Featured Trade:

(AMAZON’S NEW GAME CHANGER)

(AMZN), (WMT), (TGT), (UPS), (FDX)

Amazon’s free 2-day shipping for Prime Customers is on the verge of becoming free 1-day shipping after the company recently announced this new wrinkle to their business model.

Amazon’s competitors should be shivering in their wake.

But it’s not all doom and gloom for the other e-commerce giants, hardly so, the gap up in the fierce competition will do what General Data Protection Regulation (GDPR) rules in Europe did to competition – enclose the existing players off from the smaller fish.

In examining who will be the last man standing, I have come to the conclusion that it will not just be one or two grinding it out in a vacuum, but more like several winners that will all benefit to certain degrees.

The outsized denominating factor in the e-commerce wars is logistics and who can best put this segment together.

E-commerce companies are being bullied into leaner models because of the premium on heavy scaling that will pile on added costs to make 1-day free shipping a reality.

This isn’t selling lemonade on your driveway, getting 1-day shipping to work will be a tough nut to crack.

The result will be the imminent deterioration of FedEx (FDX) and United Parcel Service (UPS) on the expectation that Amazon will crowd them out.

It could be the case that Amazon improves its logistical capabilities to the point that FedEx and UPS will have to sell itself off or risk death by a thousand cuts.

There looks like no navigational path ahead for these two legacy logistic companies because of the nature of being lower down on the value chain.

The only other choice is if FedEx or UPS is able to jump into the e-commerce business themselves by buying a Kroger to maneuver into the integration process through the other side.

Either way, acquiring a supermarket is no guarantee of future success considering the stakes are about to become higher and higher.

I believe that Walmart will respond to Amazon by rolling out free 1-day shipping with no membership fee, boosting its customer experience while attracting and retaining customers.

Walmart is in this fight until the bitter end and they have invested heavily in improving the technological aspects of the company.

Where does this end?

Logistics will perpetually improve as companies drain more money into logistics, and customers will eventually receive their e-commerce packages in a drone less than 1-hour after payment.

Amazon CFO Brian Olsavsky told investors that Amazon is plunking down $800 million over the quarter in its fulfillment network and that number should rise every year as Amazon has targeted logistics as a huge competitive advantage that they must capitalize on and thrive in.

Amazon already has the option for 1-day free shipping in the European Union and Japan where the delivery distances are truncated.

America poses geographical challenges that will cost more to solve and will rely on the deregulation of future drone flights and cooperation with Amazon sellers to deliver this big step up in customer experience.

The constant iteration upgrades in logistics for the past 20 years have made this possible, and I believe Amazon would be well served to bite the bullet and splurge for UPS or FedEx to make it easier on themselves.

It is not shocking there is a scarcity value of logistic carriers and e-commerce giants will need more logistical capacity to execute free 1-day shipping and eventually free 1-hour shopping.

Amazon hasn’t figured out how to transport physical goods through a computer yet, but I am certain, if there was the technology, they would spend unlimited amounts to get it to that point.

The most ironic aspect of the e-commerce wars is that supermarkets, being a part of e-commerce and the logistics behind it, is the most innovative part of technology at this moment.

Tech companies have identified that customers need to eat three times per day as paramount and are sizzling through cash to build this unfathomable logistics system - effectively working miracles and becoming whirling dervishes to seize this part of the economy.

I would probably label automobiles and the self-driving autonomous technology behind logistics as the second most innovative part of technology at this moment.

As for Amazon’s earnings report, it was a mixed bag, but the good in the bag was astounding.

Profitability boosts through the scaling and efficiency savings inflated the bottom line with EPS in Q1 at $7.09 compared to expectations of $4.72.

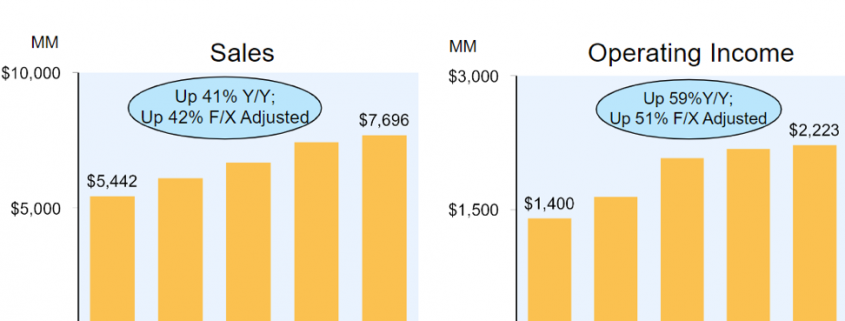

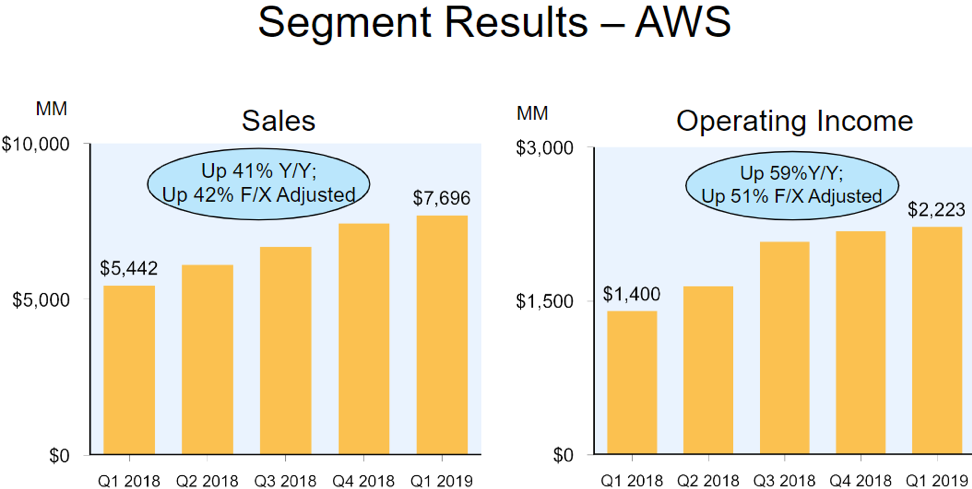

Amazon Web Services (AWS) is still commanding enormous growth rates which is miraculous for a division its size, the cloud unit grew 41% YOY which is down from 49% last year.

On the negative side, the advertising business experienced a sharp slow down growing only 34% YOY to $2.7 billion.

Remember that ad sales were expanding over 100% YOY in prior quarters.

Total Revenue only grew 16.9% which shows how difficult it is to grow at Amazon’s size and brings down the digital ad growth rate almost on par with Facebook.

Walmart and Target will be forced to compete with free 1-day shipping, and this will make their services better as well.

The question is how much pain can investors handle in terms of capital investments?

I believe substantially more.

Walmart and Target shares are poised to move higher on the news because the improvements in their logistical services will widen the gap between the haves and have nots.

These companies are in the midst of persuading investors they should be revalued as tech companies and duly receive growth multiples.

They are doing a great job and imagine how badly this news feels for medium-tier grocers with a minimal digital footprint.

Investors will come to grips that Amazon, Walmart, and Target will pull away from the pack and trade blows with each other.

This time it's Amazon, but it's not the last laugh.

Where does this all lead?

The end game is voice-triggering smart speakers where Amazon and its Echo speaker have a distinctive lead and a market share of around 70%.

Graphic interfaces will exist in only voice-activated form and content will be bundled into voice technology where even managing a Walmart order will require Amazon Echo to register sales.

That type of future is still a way off, but these are the next baby steps in that direction.

In short, revelations of free 1-day shipping to Amazon prime customers is convincingly bullish for Amazon, quite bullish for Walmart, Target, and a death knell for smaller e-commerce platforms and logistic dinosaurs.

“The best customer service is if the customer doesn't need to call you, doesn't need to talk to you. It just works.” – Said CEO of Amazon Jeff Bezos

Mad Hedge Technology Letter

April 29, 2019

Fiat Lux

Featured Trade:

(A TESLA ENTRY POINT IS FINALLY OPENING UP)

(TSLA), (LYFT), (UBER)

CEO of Tesla Elon Musk touting his company’s ability to deploy robo-taxis in the next 12 months miffed many industry analysts.

Few tech CEOs would have the balls to get on stage and put themselves out there in that type of manner.

But many tech CEOs aren’t Elon Musk.

I believe Musk calling for these bold predictions will help bend the world in his favor, maybe not right away, but before Tesla burns through their horde of cash.

Of course, there is no way in hell he could pull this off today, regulatory hurdles and in-house capability are two severe constraints.

But confidently proclaiming audacious initiatives that become self-fulfilling prophecies is a smart way to align the stars in the way you want.

Musk certainly believes the scent is in the air for the wolves to go in for the killer blow, he just needs a few miracles and a tad bit of luck on his side.

Tesla is now on record hyping up a custom-made robo-taxi capable of running about a million miles using a single battery pack, with all the sensors and computing power for full autonomy, costing less than $38,000 to produce.

They believe this will come out in 2020.

The combination of low vehicle cost, low maintenance cost and an expected powertrain efficiency of 4.5 miles per kWh should make this the lowest cost of ownership and will be the most profitable autonomous taxi on the market.

Using this state of the art robo-taxi to build a ride-sharing service business would effectively mean an Uber or Lyft without drivers.

Tesla would receive 30% of each fare, with the other 70% sent to Tesla owners that would deploy their own cars into the ride-sharing network.

I respect that Musk can feel sentiment behind Tesla's brand slipping away after heavy criticism, personal backlash from a spat with the SEC, and a boatload of competition hoping to smash him in the mouth.

Musk needed to shift the narrative into Tesla’s brand being the most innovative and publicly letting investors know there are more irons in the fire that will entrench Tesla supporters further while giving the Tesla haters more fodder to terrorize Musk.

Tesla is a luxury brand and constructed in the image of Elon Musk - making the impossible possible ethos needed a facelift and Musk gave what his supporters wanted in spades.

His showmanship is not misplaced and is part of who he is. But more importantly, if Tesla makes serious headway in the robo-taxi business in the next 12 months, Musk will be able to stand on the podium to whip up enough support needed to nudge this over the line.

Musk is very much from the mold of build it and they will come, and he has what few other CEOs have – vision.

The vision comes with a pricey premium.

And Musk must nurture this vision and urge believers to keep believing to carry on this act.

I was surprised that one of the most applicable pieces of news in the shareholder letter was something that nobody excavated.

Tesla will build a second-generation Model 3 line in China that projects to be at least 50% cheaper per unit of capacity than the Model 3-related lines in Fremont and at Gigafactory 1.

The cost to produce Model 3's is about to crash all while Tesla is still considered a premium, luxury vehicle.

This will free up space at the Reno Gigafactory and Fremont to focus on the robo-taxi challenge.

The latest news in Shanghai was an explosion at the half-built Gigafactory parking lot, but not much will come of that.

For investors on the sideline, the nadir of Tesla stock is approaching, another more shakeout might give investors the green light for a trade, that is if they aren’t already long-time holders.

Tesla mentioned they had trouble delivering new Teslas to foreign countries because of headwinds putting the logistics in place for the first time.

This one-off write-down will come off the balance sheet in next quarter’s earnings report and more information on the Shanghai Gigafactory will start to filter in aside from its boost to Tesla being able to produce 500,000 cars in 2019 once it comes online.

The Shanghai Gigafactory will unlock substantial value for shareholders once it's fully operational and finishing the construction ahead of time would be a boon.

Part of the plan to go into China results from snapping up more of a battery supply which Musk feels is the Achilles heel right now in Reno.

He continues to fault Panasonic for not delivering enough cells which, in turn, is holding back the power wall business creating a backlog in orders.

Many of the talking heads appearing on major networks were too trigger-happy in tearing Musk to shreds because of the way he speaks in hyperbole.

Musk even came out with another zinger that could pick up traction - an insurance product to marry up with Tesla vehicle purchases because Tesla believed Tesla owners are being price gouged by insurance companies.

As the impact of higher deliveries and cost reduction take full effect, Tesla expects to return to profitability in Q3 and significantly reduce losses in Q2.

Most of the bad news is baked into the stock and there could be another leg-down before this stock starts to look compelling.

Whether you love them or hate them, visionary tech CEOs get a lot of slack because the upside is so lucrative for shareholders.

That is part of why it is excruciating trading the stock led by a moody visionary with a larger-than-life persona, better to buy and hold if you are a Tesla believer.

“If something's important enough, you should try. Even if you - the probable outcome is failure.” – CEO of Tesla Elon Musk

Mad Hedge Technology Letter

April 25, 2019

Fiat Lux

Featured Trade:

(THE RESILIENCE OF TWITTER)

(TWTR), (FB)

Twitter’s (TWTR) earnings offer a rough snapshot into the health of current internet users and Twitter pulling off a strong quarterly performance is a strong indication of how tech earnings as a whole will pan out.

Readers of the Mad Hedge Technology Letter know well that CEO of Twitter Jack Dorsey is one of my favorite tech CEO’s in the valley and I believe he should be leading Apple instead of Twitter and Square.

Twitter had an ideal quarter smashing estimates by surpassing every meaningful metric.

This company has turned the corner and has become the choir boy of social media in relative terms.

Purging the bots in the summer of 2018 was the right move in hindsight, and the performance in the first quarter vindicates Dorsey in making the tough decisions to clean out its system.

As Twitter grows in its Daily Active Usership (DAU), they risk becoming too large to regulate and grabbing back control over their model was the smart thing to do at the time.

Twitter has shifted from emphasizing Monthly Active Users (MAUs) to Daily Active Users (DAUs) in a sign of intent preferring to become integrated with users on a daily basis.

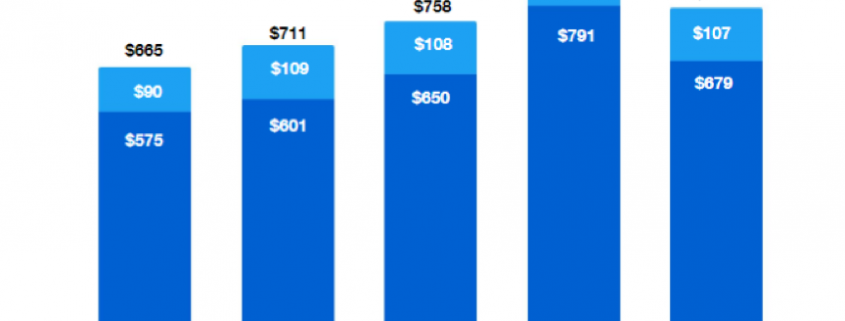

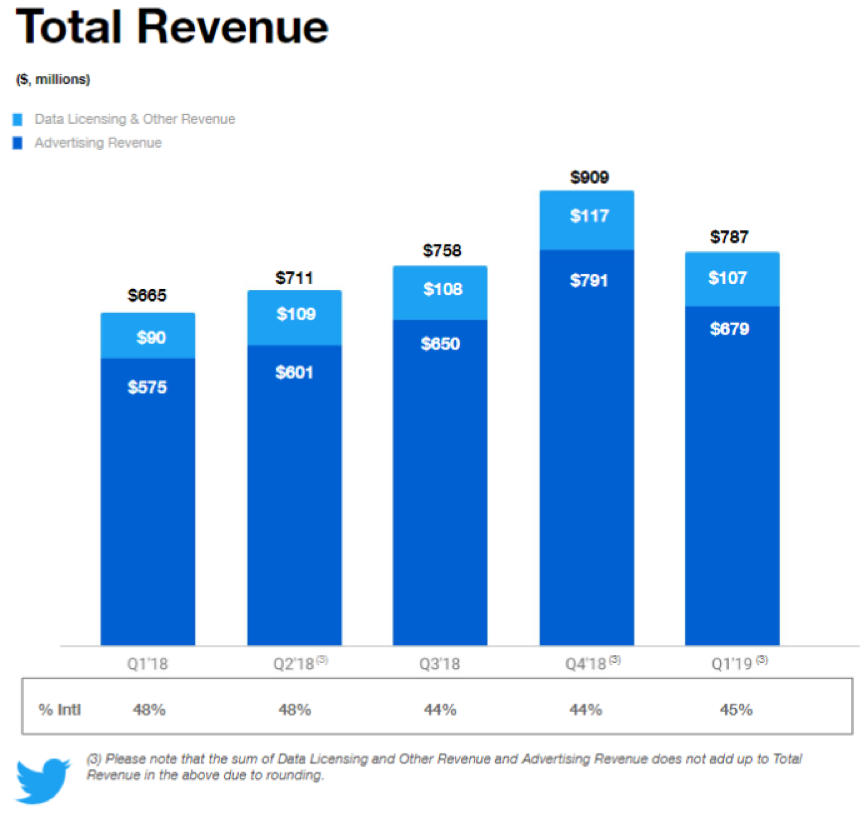

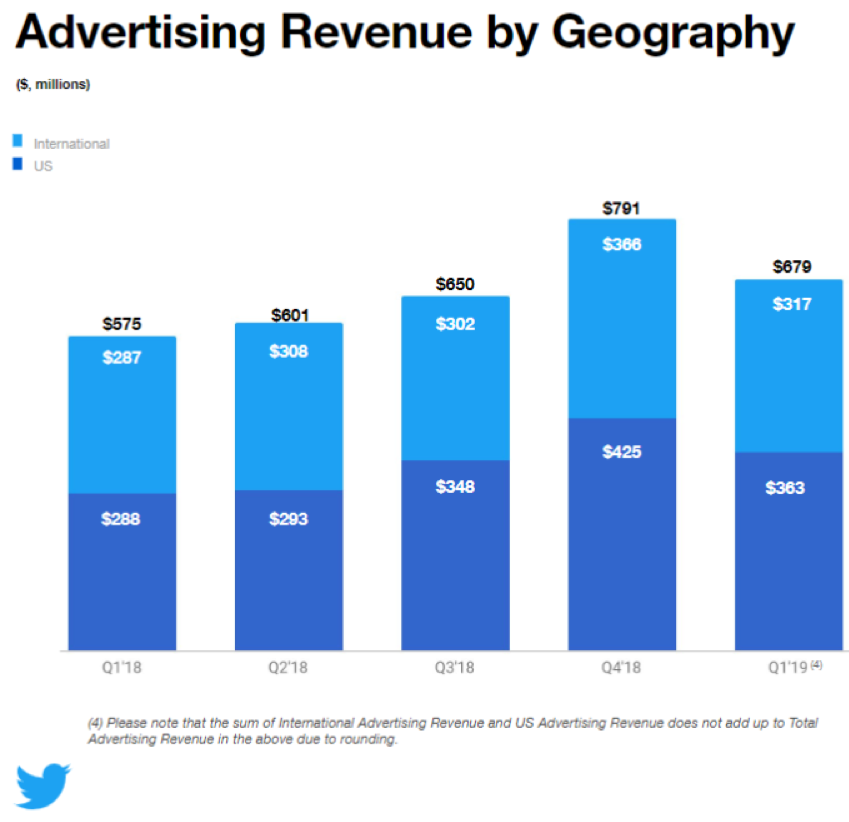

Total revenue of $787 million was up 18% YOY batting away any whispers that the company could be decelerating.

Another bonus was the diversity in ad revenue with 46% coming from the international segment signaling to investors that Twitter is not over-reliant on American Tweets.

American ad revenue rose 26% compared with international ad revenue rising just 10% showing that if you do social media properly instead of hatching cunning plans, it is still a growth business at its core.

The company has started to rev up profitability by reporting first-quarter earnings per share of 37 cents crushing the consensus of 15 cents.

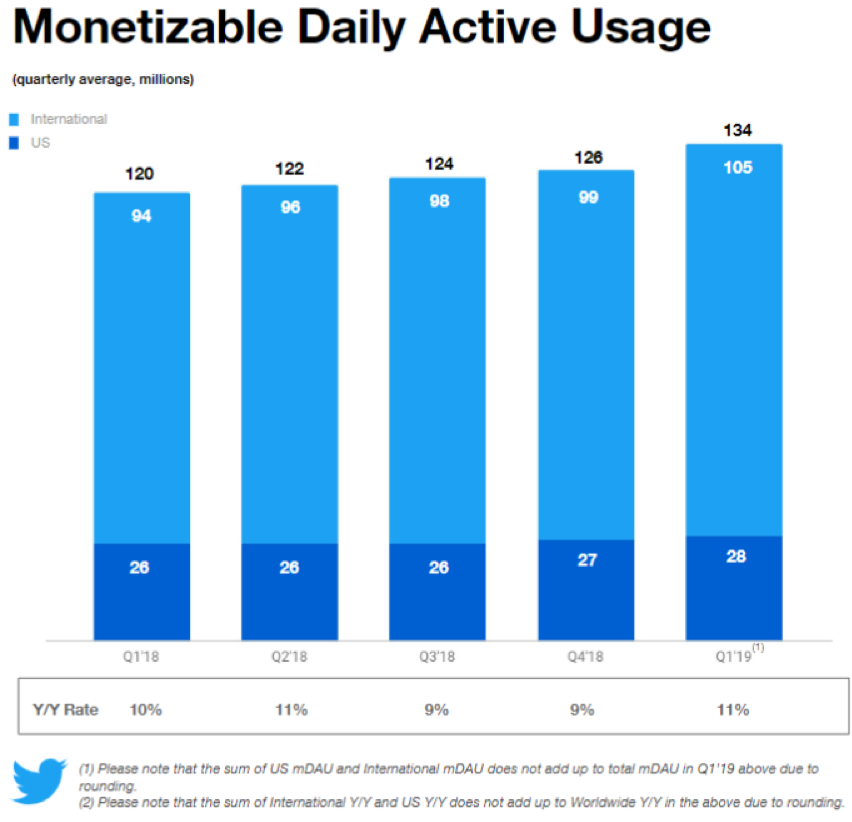

The healthy trajectory of the company is summed up by its rise in Daily Active Users to 134 million, an increase of 11% YOY in an environment where Twitter’s competitors aren’t growing at all.

The concerns that I had about last quarter’s tech earnings report had more to do with forward guidance than the past quarter’s performance because of the supposed deceleration of the global economy.

Twitter passed with flying colors predicting next quarter’s revenue should come in between $770 million to $830 million and operating income between $35 million to $70 million.

Dorsey sees no let down in the coming quarters as the domestic economy will attempt to push its way into its 11th year of expansion.

Headcount is estimated to rise 16% in 2019 after a 2018 where staff grew by 18%.

Total ad engagements increased 23% resulting from higher ad impressions and improved clickthrough rates (CTR) across most ad formats.

Cost per ad engagement (CPE) decreased 4% due to like-for-like price decreases across most ad formats because of an improved CTR which results in advertisers achieving the same number of engagements at a lower price, and a mix shift toward video ad formats that have lower CPEs and higher CTRs.

CPE can differ from one period to another based on geographical performance, ad formats, campaign objectives, and auction dynamics.

Just as important, the customer experience for advertisers is always improving with enhancements to Twitter’s ad platform and ad formats.

Twitter is committed to delivering better relevance making it simpler for advertisers to declare their objective, initiate a campaign, and measure performance.

The possible destructive black swan strongly hovering over social media and its business model is the threat of data privacy and the subsequent regulation to it.

Facebook (FB) and less so Twitter have been dragged into the data privacy debacle, but I believe Twitter has made the moves to get the monkey off their back for at least the next two quarters.

They have also benefitted from being more conservative in how they handle data and from the bulk of tweets being parts of public discourse instead of personalized baby photos.

The structure of Twitter has led to less chaos than Facebook, and Twitter tightening the amount of acceptable mainstream topics even more will close more loopholes into the extreme parts of society that want to disperse content through Twitter.

Twitter is taking a more proactive approach to reducing abuse on the platform and its effects in 2019 with the aim of reducing the burden on victims of abuse and, where possible, taking action before abuse is reported.

As a result, enhancements in Q1 revolved around proactive detection of rule violations and physical, or off-platform, safety — including making it easier to report Tweets that share personal information, helping Twitter remove 2.5 times more of this type of content.

Twitter has also deployed upgraded machine-learning models to detect potential policy violations enabling Twitter to pinpoint Tweets to agents for review, proactively.

The result is Twitter removing more abusive content with better efficiency.

The data backs up Twitter’s abuse prevention initiative with approximately 38% of categorized abuse proactively detected.

Twitter has been profitable for a string of quarters now, responded well to looming regulation fears, and as long as the economy chugs along at its current rate, I believe Twitter will outperform the rest of tech and the domestic economy.

The short-term health of social media also opens the path for Facebook to continue the positive momentum as the summer approaches.

Wait for an entry point on the dip to buy Twitter.

“Twitter has been my life's work in many senses. It started with a fascination with cities and how they work, and what's going on in them right now.” – Said CEO of Twitter Jack Dorsey

Mad Hedge Technology Letter

April 24, 2019

Fiat Lux

Featured Trade:

(WHO BEAT WHOM IN THE APPLE/QUALCOMM BATTLE)

(QCOM), (INTC), (AAPL)