Mad Hedge Technology Letter

March 19, 2019

Fiat Lux

Featured Trade:

(GOOGLE’S AGGRESSIVE MOVE INTO GAMING),

(GOOGL), (AAPL), (FB), (NFLX), (MSFT) (EA), (TTWO), (ATVI)

Mad Hedge Technology Letter

March 19, 2019

Fiat Lux

Featured Trade:

(GOOGLE’S AGGRESSIVE MOVE INTO GAMING),

(GOOGL), (AAPL), (FB), (NFLX), (MSFT) (EA), (TTWO), (ATVI)

The saturation of tech is upon us.

That is the takeaway from Google’s (GOOGL) hard pivot into gaming.

The goal of their new gaming service is to become the Netflix (NFLX) of gaming allowing gamers to skip purchasing third-party consoles and playing games directly from an Android-based Google device.

Middlemen in the broad economy are getting killed and this is the beginning.

What we are really seeing is a last-ditch effort to protect gaming consoles - these devices will become extinct in less than 20 years boding ill for companies such as Sony and Nintendo

The cloud is still all the rage and companies such as Microsoft (MSFT), Alphabet (GOOGL), and Apple (AAPL) have the natural infrastructure in place to offer cloud-based gaming solutions.

Phenomenon such as internet game Fortnite have shown that consoles are outdated and relying on the cloud as a fulcrum to extract gaming revenue by way of add-ons and in-game enhancements will be the way forward

Another key takeaway from this development is that passive investment is dead, even more so in tech, where these big tech companies are starting to bleed over into each other's territory.

This dispersion will create opportunity and pockets of weakness.

I blame this on a lack of innovation with companies still trying to extract as much as they can from the current smartphone-based status quo which has pretty much run its course.

Technology is itching for something revolutionary and we still have no idea what that new idea or device will be.

The rollout of 5G is promising and companies will need some time to adapt to this super-fast connection speed.

In either case, I can tell you the revolution won’t include foldable smartphones.

In 2018, the gaming industry flourished on accelerating momentum by registering over $136 billion in sales, and the revenue growth rate is already about 15% and increasing.

Naturally, companies such as Amazon and Google want a piece of this action and are hellbent on making inroads in the gaming environment such as Amazon's ownership of Twitch, which is a game streaming service where viewers can watch live tournament-style competitions proving extremely popular with Generation Z.

I applaud this move by Google because they already have proved they can execute on certain mature assets such as YouTube which has become the Netflix replacement of 2019.

Doubling down in the gaming sector would be a bonus as they search a second accelerating revenue driver that will dovetail nicely with the overperformance in YouTube this year.

It’s even possible that YouTube could be modified to support live stream gaming, certainly various synergistic dynamics are at play here.

Even if they fail - it's worth the risk.

Revenue extraction will be painful for certain companies like Facebook (FB) in this new environment, who has seen a horde of top executives abort after the company drastically changed directions, believing the company is on a suicide mission to fines and more regulatory penalties.

I've mentioned in the past that Facebook no longer commands the same type of employee brand recognition they once cultivated.

Facebook will find a tougher time to find the right people they need to execute their private chat plan, by linking the likes of WhatsApp, Instagram, and Facebook Messenger.

This is a high-risk high-reward proposition that could end up with Facebook's co-founder Mark Zuckerberg in tears if regulators give him the cold shoulder, and that is why many executives who are risk-adverse want to cash in now because they sink with the Titanic.

Not only are gaming assets becoming saturated, but the general online streaming environment is attracting a tsunami of supply all at one time.

Online content is already veering into the same type of pricing structures that cable offered traditional customers.

Investors will have to ask themselves, how much will the average consumer spend in content-based entertainment per month?

My guess is not more than $100 per month.

The saturation will cause tech companies to become even more draconian.

Be prepared for some more epic in-fighting until a new gateway of internet monetization opens up.

There has never been a better time to be a tactical and active investor in tech.

The Fang trade has splintered off with each company facing unpredictable futures.

Unearthing value will become more difficult because these traditional bellwether tech stocks have decoupled and aren't going straight up anymore.

Those zigs and zags will still be buttressed by a secular tailwind of the migration to digital, but there are certain winners and losers that will result of this.

Apple announcing a new streaming product is proof that these Silicon Valley tech firms are desperate for new profit drivers as the woodchips that fuel the fire start to run noticeably short on supply.

At the bare minimum, this looks disastrous for the traditional gaming companies of Electronic Arts (EA), Take-Two Interactive (TTWO), and Activision (ATVI) whose shares have been effectively shelved due to the Fortnite revolution.

EA has fought back with their own Fortnite lookalike called Apex Legends which showed a Fortnite-like trajectory sucking in 10 million players in the first 72 hours.

The stock exploded 16%, signaling this is the new way forward for gaming companies.

As a whole, these traditional gaming studios simply don’t have the firepower to compete with the big boys, let alone possess a strong cloud infrastructure.

“Success is a lousy teacher. It seduces smart people into thinking they can't lose.” – Said Founder and Former CEO of Microsoft Bill Gates

Mad Hedge Technology Letter

March 18, 2019

Fiat Lux

Featured Trade:

(WHY ALPHABET IS THE BEST FANG TO BUY NOW),

(GOOGL), (NFLX), (FB), (TWTR), (DIS)

Why am I bullish on Alphabet (GOOGL) short-term?

Video has muscled its way to the peak of the digital content value chain.

If you don't have video streaming, then you are significantly depriving yourself of the necessary ammunition capable of battling against legitimate content originators.

The optimal type of content is short form yet engaging.

Interesting enough, the format method integrated into systems of Facebook (FB) and Twitter (TWTR) has experienced unrivaled success.

They have been leaning on this model as growth levers that will take them to the next stage of revenue acceleration and rightly so.

This has seen smartphone apps such as Instagram become game-changing revenue machines destroying all types of competition.

The x-factor that stands out in Instagram's, Facebook’s, YouTube’s model is that it's free and they do not absorb heavy expenses from content creation.

It’s certainly cheap when the user is the product.

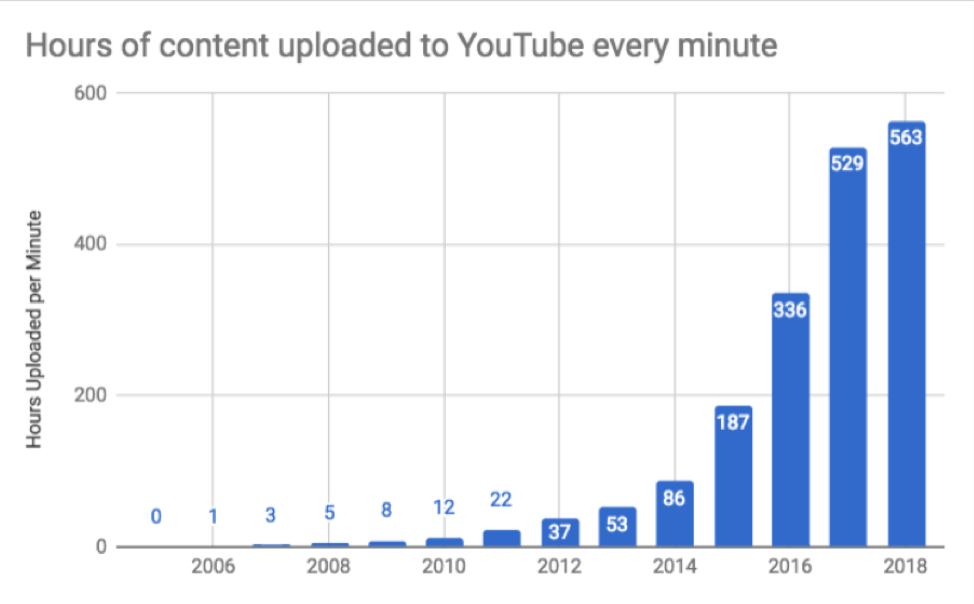

Google’s YouTube service has morphed into something of a phenomenon.

Its interface is easy to use, and followers have a simple time navigating around its platform.

Familiar news outlets such as Sky News, Bloomberg News, and even CNBC news have recently installed their live feeds on YouTube's main platform scared of losing aggregate eyeballs.

And even more intriguing is that YouTube has become a legitimate competitor to Netflix's (NFLX) online video streaming platform.

YouTube has sensed the outsized pivot to their free platform and has double down hard by installing 5-second ads at the front end and middle of videos.

Of Alphabet’s total $39.3 billion revenue pocketed in Q4 2018, ads constituted 83% or an astounding $32.6 billion.

I feel that Alphabet shares are currently undervalued, and I believe that we will see outperformance from Alphabet shares for the rest of 2019 based on YouTube's performance relative to expectation.

YouTube’s ever-growing presence showing up in the top line will offer the growth investors desire to pile into these shares as the company wrestles with future projects such as Waymo.

That's not to say that their traditional advertisement business of Google Search is failing.

Investors can expect continuous 20% to 25% growth in this cash cow business, but the reason why Alphabet share has not been able to break out is that investors have baked this into the pie.

Therefore, YouTube is really the X Factor and will take them to this new promised land with shares surging past the $1,250 mark and more importantly, staying at that level.

YouTube brought in about $15 billion in 2018 and that consisted of about 10% of Alphabet’s total annual revenue.

However, the company is just scratching its surface of what it can accomplish with this fast-growing revenue driver and I can extrapolate this growth segment turning into 20% or 25% of the company’s annual revenue in the next few years.

Google does not strip out YouTube revenue in its reporting, therefore, it's difficult to put my finger on exactly how much YouTube is carving out in terms of revenue.

I can also assume that if Netflix continues to raise the cost of monthly subscription, this strategy will directly hurt its revenue acceleration ability as it relates to competing with Google's YouTube because YouTube's free service is demonstrably attractive to viewers hoping to discover high-quality content relative to a $20 per month Netflix subscription.

I do agree that Netflix is a great company and a great stock, but as they slowly raise the price of content, this will gift YouTube a huge chunk of Netflix’s marginal audience freeing itself from the shackles of Netflix’s price rises.

At some point, online video streaming will become as expensive as the cable bundles now, and at that point, we know that saturation is imminent boding negative for Netflix.

What I do envision in the short-term future are consumers in America will pay into several unique bundles such as Netflix, maybe Disney (DIS), ESPN and merely stick with these as their base content generators as more consumers cut their cord and hard pivot from traditional cable packages that are becoming less appealing by the day.

And don't forget that at some point, Netflix will have to demonstrate profitability and the huge cash burn that permeates throughout the business will be exposed when subscription growth starts to fade away.

In every possible variant, YouTube will become an outsized winner in the media wars because the quality of the free content keeps improving, the cost for consumers stays at 0, and their best of breed ad tech migrating from their Google search into YouTube just keeps getting more surgical and efficient.

Not only are the positive synergies from the best of breed ad tech aiding YouTube’s model, but just think about YouTube having access to the Google cloud and saving expenses by accessing this function to store data onto the Google Cloud.

If this was a standalone service, they would have to subcontract cloud storage functions to third-party cloud company causing the content service to spend millions and millions of dollars per year in expenses.

This would have the potential of crushing the bottom line.

That is just one example of the synergies that Google can take advantage of with YouTube under its umbrella of assets.

And think about self-driving vehicles, Google could potentially equip YouTube as a pre-programmed application inside of autonomous vehicle platform tech with YouTube popping up on the multiple screens.

I assume that there will be multiple screens inside of cars with self-phone driving technology because of the lack of driving required.

The worst maneuver that Alphabet could do right now is spinoff YouTube into its own company, and if that happens, YouTube won't be able to take advantage of the various synergies and benefits of being an Alphabet asset.

We are just scratching the surface of what YouTube can accomplish, and I believe this upcoming overperformance isn’t in the price of the stock yet.

If the Fed continues its “patient” strategy towards interest rates at a macro level, Alphabet will easily soar past $1,250 and it can easily gain another 10% in 2019.

If any “regulation” risk as a result of extremist content rears its ugly head, buy shares on the dips because the algorithms are in place to eradicate this material and any fine will be manageable.

“We need to bring Android and Chrome to every screen that matters for users, which is why we focused on phone, wearables, car, television, laptops, and even your workplace.” – Said CEO of Google Sundar Pichai

Mad Hedge Technology Letter

March 14, 2019

Fiat Lux

Featured Trade:

(AIRBNB’S SECOND THOUGHTS),

(AIRBNB)

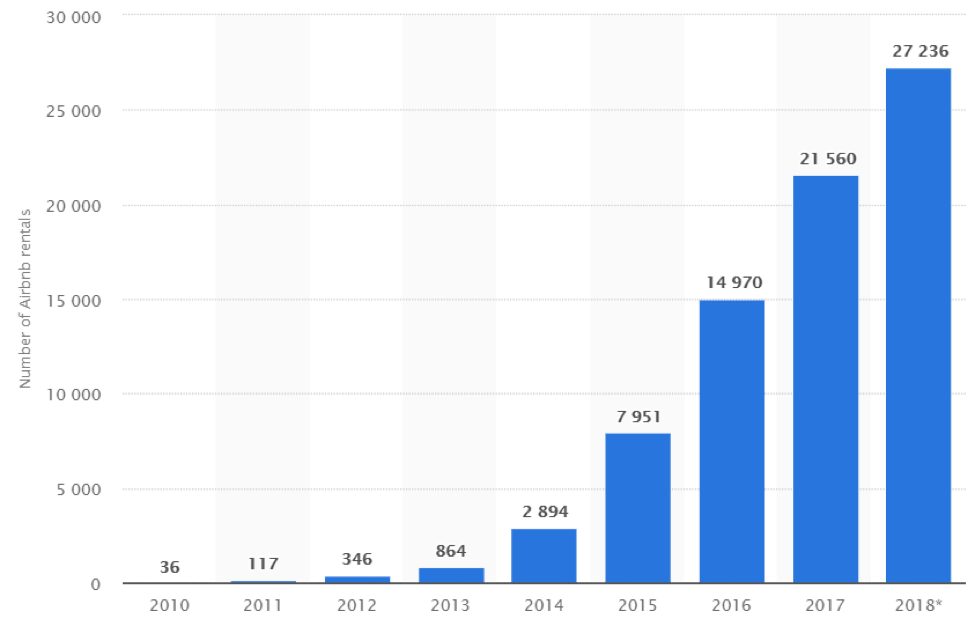

In an unusual U-turn, Airbnb co-founder Nathan Blecharczyk revealed sudden skepticism on his companies’ odds of going public in 2019.

The base case was that Airbnb was on schedule to be listed in mid-2019.

Blecharczyk fueled confusion by going on record saying that Airbnb “are taking the steps to be ready to go public in 2019. That doesn’t mean we will go public in 2019.”

The company is currently valued at $31 billion.

The co-founder resisted in offering a specific explanation in why the company is hesitant in pulling back from the public market, but part of the factors could boil down to the Brexit mess currently ongoing at 10 Downing Street and the trade war between America and China creating uncertainty around crucial Airbnb housing markets.

Executing the IPO is another quandary where the Securities and Exchange Commission (SEC) shuttered its IPO division during the government shutdown and its staff has not regained full capabilities.

The global economic slowdown has made IPO investors nervous and the slew of IPOs planned for 2019 could take rolling rain checks to ensure the stability of newly minted shares.

This is not the only problem roiling Airbnb.

Taxes.

Municipalities are sick of being shafted from the outsized revenues pocketed by Airbnb.

Hotels have been incessantly complaining that they are on the leash for taxes that Airbnb does not have to face even though they are directly competing.

Things are about to change.

Let’s take the state of Maryland as an example.

Hosts are now pre-warning potential guests that they are on the hook for 15.5% in taxes upon arrival.

The sticker shock could have the effect of killing demand or reducing it severely.

Another bill before the Senate Budget and Taxation Committee would force short-term rental brokers to collect the 6% Maryland sales and use tax at the time of booking and pass on the fees to the state.

And this is just the beginning when you consider the onslaught of regulation other states are grappling with.

Take for instance, Maryland’s neighbor Washington D.C.

The capital has come down heavy-handed on the short-term rental platform forbidding property owners renting out 2nd homes.

They have also limited the days owners can rent out their house if they are not currently present in the city forcing owners to stick around to maximize revenue.

As of now, D.C. taxes Airbnb and other short-term rental companies 14.5% and the company has aired its grievances claiming favoritism towards the local hotel industry.

City councilors have cited figures as much as $96 million over four years of potential lost taxes.

Airbnb has been painted as the scapegoat by many jurisdictions around America when you consider that traditional hotels are taxed at 13% if averaged out in the largest 150 cities.

In many cases, Airbnb is treated not as a hotel and is responsible to self-report its occupancy and revenue data giving them a chance to find loopholes to push large amounts of revenue streams through unscathed.

Governments are also dealing with additional headaches of a wave of displacement for regular payroll jobs because of the domination of Airbnb units.

This whole situation will go from bad to worse because local government is frothing at the mouth when they understand the potential tax windfall they could seize from these online platforms.

Whether legitimate or not, states could cite taxes on hotels as a starting point and start purging Airbnb of revenue through cumbersome charges, fees, licenses, penalties, and regulation.

Airbnb could end up with a bunch of Miami Beach markets on their books with the situation on the ground turning into a slugfest.

The state is at war with property owners who rent out their unit short-term with owners trying to skirt the law.

Any rentals of less than 6 months have been illegal in Miami for years.

Fines were small amounts just three years ago but the tsunami of demand to rent units at tourist hot-spots has ignited the debate of short-term rentals and the pros and cons to business and the community.

The fines have exploded to $20,000 for each citation and the local government has bombarded owners with over $8 million in fines since 2016.

Complicating the matter, owners are often not even the culprits renting out the units.

Tenants who sign up for legitimate leases are running the show themselves muddying the situation in who is liable for the fine – the owner or the tenant?

Short-term rentals have generated over $10 million in taxes to Miami-Dade County in 2018, but the state is continuing to take the stance that this tax would have flooded their coffers plus more from hotels.

This sets up a dire situation in which Airbnb will need to report quarterly earnings 4 times per year and explain to analysts and investors alike the state of regulations and engagement with authorities.

I believe the situation will deteriorate with both sides entrenching more looking to get what they want potentially turning into a legal circus.

Tech firms are known to play hardball and brinkmanship encourages rapid growth, however, this will be harder as a public company.

Airbnb is on the way to ex-growth as mounting financial and regulatory burdens are engulfing the firm.

Better to get their ducks all in a row and supercharge growth one last time before the founders finally get their big payday.

Delaying the IPO is a risky move, but if they can squeeze out a few local victories from a New York, London, or another high market revenue driver and the fact they have been cash flow positive for the last few years, look for them to rush into the IPO and cash out.

And when that time comes, Airbnb’s ultimate competitive advantage of paying minimal taxes in many locales could be dead and buried and the company might become a shell of its former self.

I’ve seen crazier things happen.

“When you offer consumers choice, let them vote with their wallets.” - Said Co-Founder of Airbnb Nathan Blecharczyk

Mad Hedge Technology Letter

March 13, 2019

Fiat Lux

Featured Trade:

(NVIDIA STEPS UP ITS GAME),

(NVDA), (INTC), (MSFT), (ANET), (CSCO), (MCHP), (XLNX)