Mad Hedge Technology Letter

May 3, 2018

Fiat Lux

Featured Trade:

(THE INCREDIBLE SHRINKING TELEPHONE INDUSTRY)

(TMUS), (S), (NFLX), (T), (VZ), (CHTR), (CMCSA)

Mad Hedge Technology Letter

May 3, 2018

Fiat Lux

Featured Trade:

(THE INCREDIBLE SHRINKING TELEPHONE INDUSTRY)

(TMUS), (S), (NFLX), (T), (VZ), (CHTR), (CMCSA)

Talk is cheap.

Do not believe half-truths that go against economic convention.

This was the case when T-Mobile (TMUS) CEO John Legere and Sprint (S) CEO Marcelo Claure popped up on live TV promoting affordability, elevated competition, and massive 5G infrastructure investments if the two companies joined forces in a $26.5 billion deal.

This was a case of smoke and mirrors. The speculative claim of adding 3 million workers and investing $40 billion into 5G development is just a line pandering toward President Trump's nationalistic tendencies.

They want the deal to move forward any way possible.

Jack Ma, founder and executive chairman of Alibaba (BABA), met President Trump at Trump Towers before his term commenced and promised to add 1 million jobs in order to curry favor with the new order.

Where are those jobs?

If this merger came to fruition, market players would shrink from 4 to 3 - a newly reformulated T-Mobile plus Verizon (VZ) and AT&T (T).

Pure economics dictate that shrinking competition by 25% would create pricing leverage for the leftover trio.

Industry consolidation is usually met with accelerated profit drivers because companies can get away with reckless price increases without offering more goods and services.

Being at the vanguard of the 4G movement, America overwhelmingly benefited from lucid synergistic applications that fueled domestic job growth and economic gains.

Japanese and German players were hit hard from missing out in leading the new wave of wireless technology.

T-Mobile and Sprint wish to be insiders of this revolutionary technology and this is their way in.

In the past, T-Mobile jumped onto the scene with aggressively twisting its business model to fight tooth and nail with Verizon and AT&T.

It was moderately successful.

T-Mobile even offered affordable plans without contracts offering customers optionality and advantageous pricing.

It was able to take market share from Sprint, which is the monumental laggard in this group and the butt of jokes in this foursome.

The average cost of wireless has slid 19% in the past five years, and traditional wireless Internet companies are sweating bullets as the future is murky at best.

The bold strategy to merge these two wireless firms derives from an urgent need to combat harsh competition from the two titans Verizon and AT&T.

The merger is in serious threat of being shot down by the Department of Justice (DOJ) on antitrust grounds.

History is littered with companies that became complacent and toppled because of monopolistic positions.

Case in point, the predominant force in the American and global economy was the American automotive industry and Detroit in the 1950s.

Detroit had the highest income and highest rate of home ownership out of any major American city at that time.

Flint, Michigan, oozed prosperity, and the top three car manufacturers boasted magnanimous employee benefits and a tight knit union.

During this era of success, 50% of American cars were made by GM and 80% of cars were American made.

The car industry could do no wrong.

This would mark the peak of American automotive dominance, as local companies failed to innovate, preferring stop-gap measures such as installing add-ons such as power steering, sound systems, and air conditioning instead of properly developing the next generation of models.

American companies declined to revolutionize the expensive system put in place that could produce new models because of the absence of competition and were making too much money to justify alterations.

It's expensive to make cars but neglecting reinvestment yielded future mediocrity to the detriment of the whole city of Detroit.

The tech mentality is the polar opposite with most tech firms reinvesting the lion's share of operational profit, if any, back into product improvement.

Sprint got burned because it skimped on investment. It is in a difficult predicament dependent on T-Mobile to haul it out of a precarious position.

GM, Ford, and Chrysler met their match when Toyota imported a vastly more efficient way of production and the rest is history.

Detroit is a ghastly remnant of what it used to be with half the population escaping to greener pastures.

A carbon copy scenario is playing out in the mobile wireless space and allowing a merger would suppress any real competition.

To add confusion to the mix, fresh competition is growing on the fringes desiring to disrupt this industry sooner than later by cable providers such as Charter (CHTR) and Comcast (CMCSA) entering the fray offering mobile phone plans.

Google also offers a mobile phone plan through the Google Fi division.

The fusion of wireless, broadband, and video is attracting competition from other spheres of the business world.

The paranoia served in doses originates from the Netflix (NFLX) threat that vies for the same entertainment dollars and eyeballs.

Remember that AT&T is in the midst of merging with Time Warner Cable, which is the second largest cable company behind Comcast.

The top two in the bunch - AT&T and Verizon - are under attack from online streaming business models, and the Time Warner merger is a direct response to this threat.

There are a lot of moving parts to this situation.

AT&T hopes to leverage new video content to extract digital ad revenue capturing margin gains.

Legere and Claure put on their fearmongering hats as they argued that this deal has national security implications and losing out to Chinese innovation is not an option.

This argument is ironic considering T-Mobile is a German company and Sprint is owned by the Japanese.

Sprint have been burning cash for years and this move would ensure the businesses survives.

Sprint's crippling debt puts it in an unenviable position and this merger is an all or nothing gamble.

Sprint has not invested in its network and is miles behind the other three.

AT&T has outspent Sprint by more than $90 billion in the past 10 years.

This is the last chance saloon for Sprint whose stock price has halved in the past four years.

However, T-Mobile sits on its perch as a healthier rival that would do fine on a stand-alone basis.

Consolidation of this great magnitude never pans out for the consumer as users' interests get moved down the pecking order.

Wireless stocks were taken out and beaten behind the wood shed on the announcement of this news as the lack of clarity moving forward marked a perfect time to sell.

There will be many twists and turns in this saga and any capital put to use now will be dead money while this imbroglio works itself out.

If the deal doesn't die a slow death and finds a way through, the approval process will be drawn out and cumbersome.

The ambitious deadline of early 2019 seems highly unrealistic even with the most optimistic guesses.

The outsized winner from a deal would be AT&T, Verizon, and the newly formed T-Mobile and Sprint operation.

If this new wave of consolidation becomes reality, pricing pressure on the business model would ease for the remaining players, particularly allowing more breathing room for the leaders.

Stay away from this sector until the light can be seen at the end of the tunnel.

_________________________________________________________________________________________________

Quote of the Day

"Everything is designed. Few things are designed well." - said radio producer Brian Reed

Mad Hedge Technology Letter

May 2, 2018

Fiat Lux

Featured Trade:

(FACEBOOK GOES FROM STRENGTH TO STRENGTH),

(FB), (AMZN), (GOOGL), (NFLX)

Everyone and their mother was waiting for Facebook (FB) to fluff their lines, but they defied the odds by posting solid performance.

The data police can go back to eating doughnuts because it is obvious that regulation won't fizzle out the precious growth drivers that Mark Zuckerberg relies on to please investors.

I even begged readers to buy the regulatory dip, and I was proved correct with Facebook shares rebounding from $155 to $173.

The dip buying was proof that investors have faith in Facebook's business model.

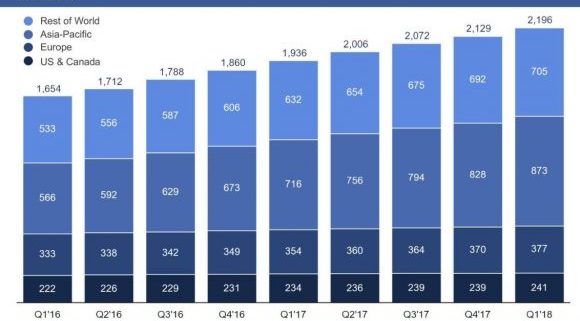

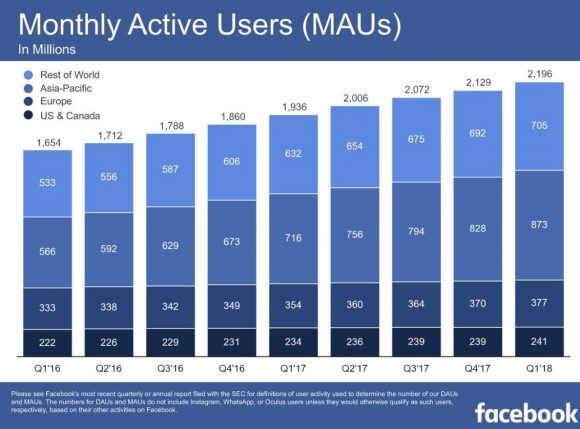

The Cambridge Analytica scandal threatened to tear apart the quarterly numbers and place Facebook in the tech doghouse, but stabilization in Monthly Active Users (MAU) and bumper digital ad revenue growth was the perfect elixir to an eagerly anticipated earnings report.

Facebook showed resilience by growing (MAU) to 2.2 billion, up 13% at a time when attrition could have reared its ugly head.

The market breathed a huge sigh of relief as the Facebook beat came to light.

The battering that Facebook received in the press effectively lowered the bar and Facebook delivered in spades.

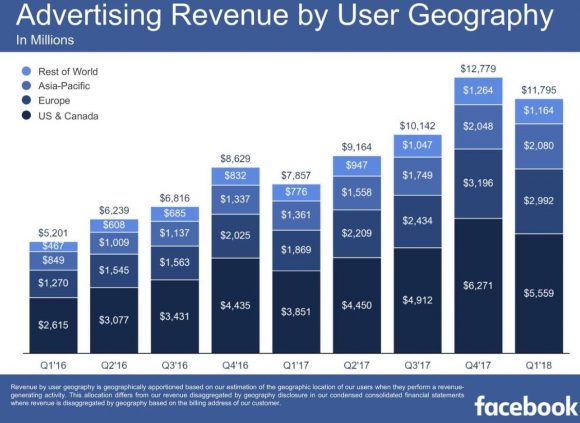

The unfaltering migration to mobile continues throughout the industry with mobile digital ad revenue making up 91% of ad revenue, which is a nice bump from the 85% last quarter.

Overall, Facebook grew revenues 49% YOY to $11.97 billion.

There is no getting around that Facebook is a highly profitable business due to the lack of costs. I should be so lucky.

Remember at Facebook, the user is the product.

Instead of paying for rising TAC (Traffic Acquisition Costs) as does Google (GOOGL) or the $8 billion outlay for Netflix's (NFLX) annual content budget, Facebook pours its money into improving its digital platform and advancing its ad tech capabilities.

However, moving forward, Facebook will have to cope with extra regulatory costs.

Facebook recently hired a legion of content supervisors at minimum wage to root out the toxic content roaming around on its platform.

Site operators have doubled to 14,000. This number gives you a taste why the large cap tech names are best positioned to combat the new era of regulation.

Doubling the staff of any business would be a tough cost pill to swallow.

Many companies would go under, but Facebook has the cash to mitigate the additional cost of doing business.

This defensive initiative casts Facebook in a better light than before like a superhero rooting out the evil villain.

Facebook and its co-founder Mark Zuckerberg need to hire a better public relations team to ensure that Mark Zuckerberg isn't pigeonholed in mainstream media as the monster of tech.

The Amazon-effect is infiltrating every possible industry, and even the bigger tech names are coping with the Amazon (AMZN) spillage onto competitors' turf.

A risk down the line is Amazon's booming digital ad business nibbling away at Facebook's own digital ad model.

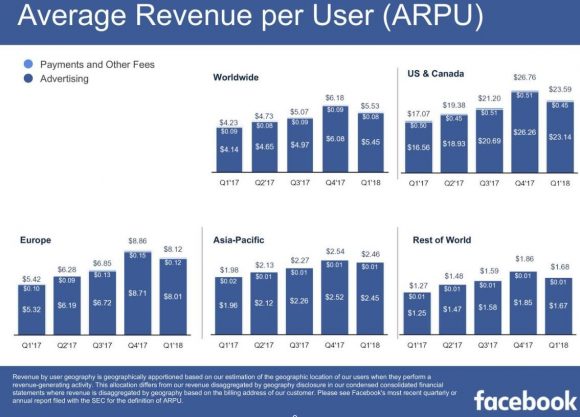

ARPU (Average Revenue Per User) remains robust with Facebook earning $23.59 per North American user, which is the most lucrative geographic location.

Artificial Intelligence (A.I.) is a tool that Facebook has implemented into its platform and monitoring apparatus.

Removing damaging content preemptively is the order of the day instead of being blamed for harboring nefarious content.

One example of this use case has been targeting ISIS- and Al Qaeda-related terror content with 99% of inappropriate content removed before being flagged by a human.

Heavy investments in A.I. will make Facebook a safer place to share content.

Big events exemplify the strength of Facebook.

During the Super Bowl in February, around 95% of national TV advertisers were simultaneously posting ads on Facebook because of the viral effect commercials and posts have during massive events.

Tourism Australia is another firm that bought ads on Instagram and Facebook platforms during the Super Bowl.

The campaign was hugely successful with half the leads for Tourism Australia coming directly from Facebook.

Facebook acts as the go-to provider for quality digital marketing and this will not change for the foreseeable future.

Investors can feel comfortable that there was no advertiser revolt after the big data chaos.

Facebook is improving its ad tech, and new ad products will be introduced to the 2.2 billion MAUs.

For instance, Facebook developed a carousel of rotating ads on Instagram Stories, and advertisers will be able to share up to three video or photos now instead of one. If the user swipes up, the swipe will take them directly to the advertisers' websites.

The shopping experience is more personalized now with an updated news feed that will show a full-screen catalog to help the user find whatever is in their search.

Facebook will only get better at placing suitable ads that mesh with the users' interests or hobbies.

Investors must be cautious to not let macro-headwinds sabotage existing positions.

Facebook's underlying growth drivers remain intact, but the stock is vulnerable to regulation headline risk that caps its short-term upside.

There is also the possibility that another Cambridge Analytica is just around the corner, which would result in a swift 10% correction.

Next earnings report should be interesting because it will reflect the first quarter that Facebook has operated with higher security expenses and will go a long way to validating its business model in a new era of rigid regulation.

If Facebook does not fill in the moat around the business, then Facebook is braced to grow top and bottom line with minimal resistance.

The cherry on top was the additional $9 billion of buybacks giving the stock price further support.

Facebook is a long-term hold but a risky short-term trade.

_________________________________________________________________________________________________

Quote of the Day

"Never trust a computer you can't throw out a window." - said Apple cofounder Steve Wozniak.

Mad Hedge Technology Letter

May 1, 2018

Fiat Lux

Featured Trade:

(AMAZON KILLS IT AGAIN),

(AMZN), (WMT), (FB), (TGT), (GOOGL)

Jeff Bezos is a god.

Well, not quite but he is turning into one after Amazon delivered a mythical earnings report that left Amazon haters in awe.

The Amazon bears patiently waiting for the day of reckoning will have to wait longer as Amazon smashed earnings expectations by a magnitude of two or three.

Amazon had a lot riding on the most recent earnings report after racing to new highs in mid-March.

The brief macro-correction then gave investors yet another entry point into one of the best companies of our generation that is still up more than 30% this year.

Amazon Web Services (AWS) revenue reaccelerated from its 42% growth last year to a high octane 49% YOY and made up a disproportionate 73% of Amazon's operating income.

Amazon is heavily reliant on the AWS segment to carry it through feast or famine.

According to Jeff Bezos, its critically acclaimed cloud segments' outstanding results originate from the "seven-year head start before like-minded competition."

This reaffirms the benefit of first-mover advantage with which large cap tech is obsessed.

There is room for other companies in the cloud space, with the cloud industry expanding 20% in 2018 to $186 billion.

Therefore, expanding by 20% is the bare bones minimum to be considered relevant.

Amazon has positioned itself to funnel in the most dollars that migrate toward the cloud as the industries pioneer and best of breed.

After the latest earnings report, Amazon is in pole position to become the first publicly traded $1 trillion company.

This latest quarter wrapped up its 62nd consecutive quarter of 20% plus growth.

And the commentary coming out of the earnings reports makes it almost certain that Amazon will capture more market share.

There were a few bombshells dropped that were unequivocal positives for investors.

First, Amazon has become the third player in digital ad industry with the duopoly of Google search and Facebook.

Amazon revved up its digital ad revenue by 139% QOQ to a substantial $2.03 billion per quarter business.

This business is particularly appetizing because of its high margins and will help alleviate tight margins on the e-commerce side.

Amazon's digital ad business is by far the fastest growth lever in its portfolio. It will ramp up this side of the business whose main function is to match consumers with suitable products that consumers otherwise would miss out on in a standard Amazon search.

The extraordinary numbers support the notion that the hoopla of Washington regulation is all bark and no bite.

Facebook also delivered a prodigious quarter for the ages amid testimony and public backlash that resulted in immaterial damage to top- and bottom-line numbers.

The second bombshell announced was the change in pricing to prime members. Amazon upped its annual prime membership to $119 from $99.

This additional $20 price hike, or 20% on 100 million prime members, will swell revenue by an extra $2 billion of incremental revenue.

In total, Amazon will accrue a bonus of 4% of revenue by this price change.

Amazon has a high fixed-cost business, and slightly tweaking prices will create a huge windfall with the revenue almost entirely flowing down to the bottom line in the form of pure profit.

Many industry analysts claim that Amazon has the best management team in the industry and explicate this company as an "Internet staple."

More than 100 million products are delivered with free shipping for Amazon prime customers. This is starkly higher than the 20 million products shipped for free in 2014.

Amazon does everything in its power to offer a unique and efficient experience for customers.

The customer satisfaction reveals itself by the rock-bottom churn rate.

Amazon prime at an annual cost of $119 is such a value that no analysts even dared to ask Amazon CFO Brian Olsavsky if consumers would take issue with the rise in price.

Investors and strangers alike assume that broad-based reoccurring revenue from annual prime membership is a given.

In an era of mass-scrutinization, Amazon's earnings call seemed like a celebration of the mythical achievements that are changing consumer behavior by the day.

The lack of inquiry was justifiable this time because the one major shortcoming suddenly remedied itself.

Amazon's doubters frequently attack the lack of margin growth because its business model is first and foremost a land grab for market share ignoring any remnants of margin stability.

Now that Amazon's digital ad business has sprouted up, the margin story, starting from a miniscule base, will go from weakness to an unrelenting success.

Amazon started with its ultra-thin margin e-commerce business that made an operating loss of $160 billion in 2017.

Cranking up a shiny, high margin business will be hard for the other FANGs to compete with as they gyrate toward other businesses that have lower margins than Amazon's digital ad segment.

This is a horrible time to start fighting Amazon in price wars as the paradigm shift to quantitative tightening has made the cost of capital demonstrably pricier.

Operating margins almost doubled from 2% to 3.8% on $51 billion of quarterly sales.

This is a huge deal.

Amazon has been continuously harangued for "not making money." Well, that era is over.

Profits, and not only revenue, will start accelerating and Amazon will become the closest thing to a perfect company.

The years and years of plowing cheap capital back into fulfillment center and e-commerce activity gave Amazon a stained reputation for years.

However, as Amazon turns the screws and uses its foundational leverage to capture additional profits, the other FANGs will be forced down the same path ruining operating margins for the other big players.

Amazon telegraphed its quest for market share strategy to investors years ago, and investors understand they are paying for growth and growth only.

That will change now that profits have become a real part of its arsenal.

There is no doubt that Amazon will deploy its profits back into expanding its company because Jeff Bezos knows that if he can grow Amazon's top-line number, investors will follow suit.

Also, spending means improving the products, and Amazon has never hesitated to spend big.

The move into digital ad growth is a warning shot to Facebook and Google. Amazon will mobilize its workforce to take on other business, and anything that is high margin is fair game.

The future looks bleak for retail competitors Walmart and Target, as the contents of the earnings report reaffirms Amazon's unrelenting assault on the retail sector, which is systematically being dissected by Amazon for fun.

Google search and Facebook are in Amazon's crosshairs. Staving off this monster will be hard to do in the long run.

Amazon has a clear path to further market gains, and operating margins are almost at a tipping point.

Revenue is poised to re-accelerate because of the reignition of AWS to a higher growth trajectory.

Shoring up operating margins through a burgeoning digital ad division will only be a boon to earnings in the future.

Amazon is one of the best companies in the world, and any weakness in the stock should be bought and held forever.

_________________________________________________________________________________________________

Quote of the Day

"I do not fear computers. I fear a lack of them," - said writer Isaac Asimov.

Mad Hedge Technology Letter

April 30, 2018

Fiat Lux

Featured Trade:

(RIDING THE CHIP ROLLER COASTER),

(Samsung), (SK Hynix), (AMD), (NVDA), (INTC), (MU)

The supply side of the chip market is spectacularly volatile, rotating between supply constraints and times of overcapacity.

A good place to analyze the heartbeat of the chip market is across the Pacific on South Korean shores.

South Korea takes pride and joy in having given the world two first-rate semiconductor companies - Samsung and SK Hynix.

Samsung is just behind Intel (INTC) in total annual sales.

American consumers are more familiar with Samsung through its consumer electronics division that constructs Samsung smartphones and tablets.

Samsung's silicon business mirrors the elevated earnings results stateside, as muscular demand derived from global data center expansion devours more chips than Samsung can pump out.

Global data centers in the U.S. and Asia will sustain blistering growth levels into the second quarter.

Samsung has displayed resilience to seasonally shift in the consumer electronics segment by staunchly bolstering its relentless chip business.

Samsung is harvesting the benefits of bountiful investments from over the past decade when this overly cyclical industry was exposed to extreme shifts in worldwide appetite for consumer electronics devices.

More than 70 percent of revenue was generated by the chip division boasting quarterly revenue of $19.25 billion.

In the past, memory chip companies endured a ruthless market environment with a diverse set of players ratcheting up supply on a whim then finding demand crumbling before their eyes.

Restructuring has left the burden of supplying the next generation of technology a backbreaking burden.

Tight chip supply and the general shortage of hardware rears its ugly head in earnings reports with a slew of CEOs complaining about input prices rising worse than global warming sea levels.

In Samsung's earnings call, management groaned that "memory supply and demand fundamentals remain tight."

In SK Hynix's earnings call, it echoed that "demand and supply dynamics in the market will remain favorable."

As large cap tech expands data center initiatives and throws piles of money at autonomous cars, A.I. and cloud computing, Samsung's semiconductor division appears nearly immortal.

Chip prices skyrocketed in this sellers' market and the UBS downgrade of Micron (MU) was a headscratcher.

Analyst Timothy Arcuri turned bearish on Micron citing "cyclical memory concerns" and "big estimate cuts."

Sometimes it feels that analysts don't follow the industry they cover.

It is fair to say chip volume might face marginal cuts closer to 2019, but the pendulum hasn't even started to shift back over to that direction.

Suppliers and buyers both agree that capturing the appropriate volume of chips is the first order of the day.

In response to outsized demand, Samsung will double chip capital spending because of failing to match skyrocketing demand.

Fortifying the bull case, SK Hynix guesstimated DRAM demand for the rest of 2018 to be in the "low-20 percent" and even the injection of new funds for facility expansion is not a proper solution.

Samsung also hammered into investors that it is not in the business to drive the chip prices to zero, and the gross profit metric is more important to them than most people expect.

A goldilocks scenario could ensue with Samsung supplying enough to create price hikes and ploughing its cash back into more silicon expansion.

Korean memory chip producers are expected to enjoy a booming business during the remainder of this year as global DRAM chip demand will surpass supply.

SK Hynix also indicated that server products would supersede mobile products as data center related products are all the rage.

Korea's No. 2 said NAND demand would rise by "mid-40 percent" in 2018, which is double the rise in demand than DRAM products.

Instead of the estimate cuts on which UBS is waiting, the more likely scenario is an easing of chip constraints. The easing will last just long enough before the next massive wave of demand hits with a vengeance.

You read my thoughts - the generational paradigm shift due to hyper-accelerating technology has largely made the boom-bust cycle irrelevant.

Chip demand will go up in a straight line, and this is just the beginning.

Legend has it that demand weakness shows up every 15 years. The last one was the global financial crisis in 2008, and the one before that was the dot-com crash of 2001.

In both instances, the disappearance of demand contributed to massive oversupply. The declining prices set off a price war eradicating margins and revenue.

SK Hynix net profit was $2.89 billion last quarter, an increase of 64.4 percent YOY.

SK Hynix capital allocation layout includes a spanking new factory in Cheongju, a city in South Korea.

The insatiable demand brought on by China's quest for technological supremacy is the market the new Cheongju factory will serve.

International chip directors fret that a sudden breakthrough in local Chinese technology could ignite a supply bonanza of cut-rate semiconductors, forcing a recapitulation of the entire industry that encountered egregious oversupply issues about 10 years ago.

But China can't dump low-cost chips into the market due to technological frailties.

Notice that Chinese capital has been flirting with American chip companies for years without success.

The Chinese government even initiated an investigation at the tail end of last year because DRAM price spikes were indigestible for local Chinese companies.

The dearth of supply is not just restricted to one extraneous niche of the hardware industry, as the tightness is broad-based.

Don't look further than AMD (AMD), which specializes in GPU (graphics processing unit) products and has received glowing reviews for its Ryzen and EPYC CPU processors that boast higher-level performance than previous products.

The RX Vega series is the new line of GPUs from AMD that launched last August. Tech-enthusiast website techspot.com described finding these GPUs on sale in stores as "next to impossible."

AMD is well informed of the market outlook and NVIDIA (NVDA) notes that hardware-intensive cryptocurrency mining is stoking excess marginal demand for its products.

AMD is boosting production, but manufacturing is set back by a component shortage in GDDR5 memory, which is needed in the RX 400 card.

The RX 500 card, part of the RX Vega line, is also having delays with a lack of HBM2 memory.

Crypto-fanatics aren't the only consumers clamoring for extra GPUs; gamers require GPUs to perform at top levels.

AMD has even urged retailers to advise gamers of any outlets where they can buy GPUs because of the dearth of supply.

Gamers are being outmaneuvered for GPUs as crypto-miners usually buy up every last unit to transport to mining farms in far-flung places with cheap energy.

Hardware products cannot be produced fast enough to meet demand.

Other industries vying for a portion of chips are military, aerospace, IoT (Internet of Things) products, and autonomous cars.

Incremental supply is accruing but often the supply is added slower than initially thought. Suppliers are hesitant to double down on new factories because of past, bitter experiences at the end of a cycle.

Management monitors inventory channels like a hawk eyeing its prey, and it's clear that organic demand is following through.

After running away with 22.2% growth in 2017, the semiconductor industry is due to take a quick breather expanding in the upper teens in 2018.

A year is an eternity in technology and calling for production "cuts" in a period of massive undersupply is premature.

The claim of "cyclical" headwinds comes at a time of a new-found immunity to cyclical demand and is dubious at best.

This secular story has legs. Don't believe every analyst that pushes out reports. They often have alternative motives.

Nvidia (NVDA) reports earnings on May 10, and CEO Jensen Huang does a great job explaining the development at the front-end of the tech revolution.

Earnings should be extraordinary. Imagine if the price of bitcoin stabilizes, GPU manufacturers will wrestle with continuous quarters of strained supply.

I am bullish on chips.

_________________________________________________________________________________________________

Quote of the Day

"Focus on the 20 percent that makes 80 percent of the difference." - said Salesforce CEO Marc Benioff when asked to explain the story of his cloud business.

Mad Hedge Technology Letter

April 27, 2018

Fiat Lux

Featured Trade:

(WEDNESDAY, JUNE 13, 2018, PHILADELPHIA, PA, GLOBAL STRATEGY LUNCHEON)

(THURSDAY, JUNE 14, 2018, NEW YORK, NY, GLOBAL STRATEGY LUNCHEON)

Come join me for lunch at the Mad Hedge Fund Trader's Global Strategy Update, which I will be conducting in Philadelphia, PA, on Wednesday, June 13, 2018. An excellent meal will be followed by a wide-ranging discussion and an extended question-and-answer period.

I'll be giving you my up-to-date view on stocks, bonds, currencies, commodities, precious metals, and real estate. And to keep you in suspense, I'll be throwing a few surprises out there, too. Tickets are available for $238.

I'll be arriving at 11:45 AM, and leaving late in case anyone wants to have a one-on-one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at an exclusive downtown private club. The precise location will be emailed with your purchase confirmation.

I look forward to meeting you and thank you for supporting my research.

To purchase a ticket, please click here.