"My experience in business helps me as an investor, and my investment experience makes me a better businessman," said Oracle of Omaha, Warren Buffett.

"My experience in business helps me as an investor, and my investment experience makes me a better businessman," said Oracle of Omaha, Warren Buffett.

The conventional wisdom on Electric Vehicles (EVs) is that they are here to stay.

The secular trends of harsher government environmental policy, a healthy global economic backdrop, rapid-fire technological development, and broad-based mainstream acceptance are the catalysts that will place EVs at the apex of the digital transportation movement for the rest of this century.

EVs are set to eventually capture more than 60% of market share, forcing legacy automotive and niche start-ups to reinvest into their operations in a fiercely competitive industry.

The EV industry still has a mountain to climb as it only represented less than 1% of total global auto unit sales in 2016. That percentage has gradually risen to 1.25% at the end of 2017.

The transition to 60% EV share of total units will organically occur in a slow and steady manner giving automakers ample time to shed legacy technology.

Cost is a major obstacle for widespread EV adoption. Many consumers cannot afford one, but price efficiencies are slowly dropping the cost of owning an EV, appealing to the masses with sleeker models possessing price tags similar to normal cookie-cutter sedans such as the Tesla Model 3.

EV makers have coped with the arduous task of constructing a car within truncated cost limitations. They make up the difference by offering a proliferation of premium add-ons such as souped-up engines and glitzy interiors that extract additional marginal revenue from well-off individuals.

EV technology advancement paired together with higher emission standards will narrow the gap between electric vehicles and the legacy internal combustion engine within the next decade.

Modern EVs new to market such as the Tesla Model 3 could serve as a springboard for able consumers to dive head in to EV revolution.

The disruption time horizon will take around 15 years and affect 80% of the market.

EV mania is destined to integrate with the traditional concept of a car to give transportation breakthrough A.I. functionality, user-friendly connectivity, and self-driving capabilities.

Let's face it, it's easier to install computer systems and software in an electrified platform, and the technologies complement each other.

About 60% of autonomous, light vehicle retrofits are constructed over an electric powertrain, and an additional 21% go with a hybrid powertrain.

Thus, owning the best autonomous vehicle (AV) technology stocks positions investors for the next leg of hyper-accelerating tech.

Waymo's leadership in the AV space is frightening for Tesla, which trails the Alphabet subsidiary that smoothly rolled out its for-profit service in Arizona in early 2018.

Aptiv PLC made a massive splash in the deep-end by acquiring the second best AV technology company NuTonomy. The Cambridge, MA-based tech firm spun off from MIT in 2013, for $450 million late last year and was spun out again in 2017.

Delphi Technologies spun out its legacy and tech business into two separate companies. The legacy part of the company is now the ticker symbol (DLPH), and the AV company became Aptiv PLC (APTV).

Spin-offs give organizations the opportunity to streamline operations and allow the market to value the company on an independent basis instead of the sum of the parts. This can lead to uncorking additional shareholder value.

Aptiv is the closest thing on the market you will find for an unfettered play on self-driving technology.

Management declined against merging its legacy and AV technology, which is a smart move considering legacy technology gets the wrong rub of the green by investors.

NuTonomy lags Alphabet's Waymo but has been operating robo-taxis in Singapore since 2016. Delphi has gifted additional engineers, reinforcing its fantastic technical talent.

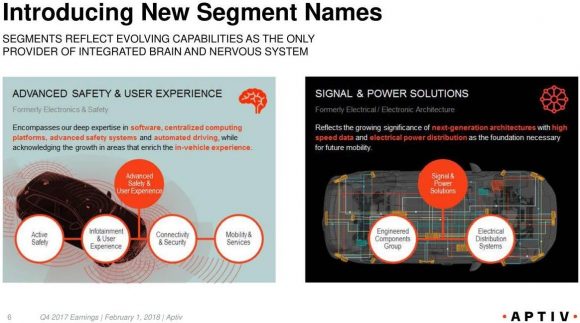

Aptiv has split its business into two new different segments in the new company.

The Advanced Safety and User experience segment will act as the brain in the vehicle, emphasizing software know-how to guarantee user security while a centralized system maintains connectivity.

The new Signal and Power Solutions segment will act as the nervous system in the vehicle by enabling high-speed data fluidity within the next-gen architecture. This segment includes the cable management and connector products that contribute a further $1 billion of revenue to the top line.

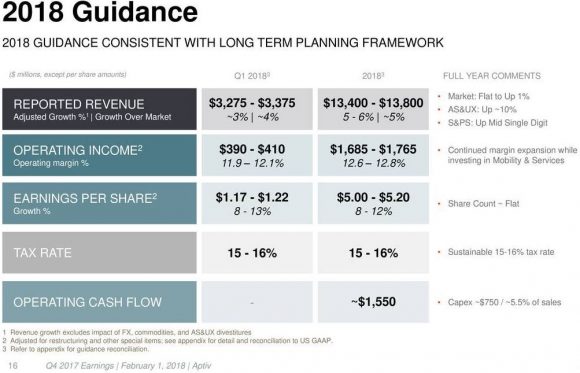

In total, Aptiv procured $12.9 billion in annual revenue in 2017, which was a boost of 4.9% from 2016. Earnings per share growth was up 10.5% YOY.

Investors cannot reasonably expect AV companies to annually grow top line by 20% to 30% as cloud companies, and the margins are unfortunately less savory. The dynamics of the business are different, and the revenue guidance of $13.4 to $13.8 billion should keep investors happy.

The pipeline is in fine fettle with $19.3 billion in bookings, which represent the lifetime gross revenue for consummated contracts.

Some of the outsized awards came in the form of an active safety contract with an OEM alliance, a high-voltage mobile charger contract from a leading North American EV producer, and an architectural contract for BYD's SUV platform in China.

It's no wonder both of the newly crafted segments expect a 10% boost in revenue for 2018.

NuTonomy is such a gem of a company that it is shocking that a large-cap tech firm declined to swoop in.

Half a billion is peanuts for such valuable and innovative technology.

Level 4 and Level 5 grade technologies are already starting to mature.

Other minor acquisitions of analytics firms Control-Tec and Movimento will initiate data monetization opportunities that effectively analyze their aggregated data then translate data into actionable profit-making opportunities.

Big data analytics are needed to decipher the path forward after compiling millions of miles of auto-robo data. And algorithms needing refinement are starving for the data, too.

A fully connected user experience will become standard in these robo-cars, and an integrated, optimized architecture is the secret sauce to commercialization of Level 4 and Level 5 automated vehicles.

Aptiv and Waymo are the only end-to-end system providers of the integrated brain and nervous system in a vehicle.

By late 2018, NuTonomy will have more than 150 Level 4 vehicles in live action.

Aptiv forecasts about $300 million in revenue from Level 4 or Level 5 AV systems by 2025.

Level 4 is practically autonomous - ready with a driver waiting to take control if need be.

Level 1, 2 and 3 revenues will mushroom to $1.8 billion per year, more than tripling from $500 million today.

Ottomatika, a Carnegie Mellon University spin-off founded in 2013, which provides software for self-driving cars, and NuTonomy are the in-house duo entirely focused on complex Level 4 and Level 5 solutions.

The shared access to the system has been set up to allow multiple teams access to the algorithms and technology that feeds through to other parts of the business.

Aptiv PLC is the perfect company to place in a buy and forget portfolio because AV monetization is still in its incubation phase.

Just as investors of pure cloud plays recently have been rewarded in spades, pure AV technology companies will be rewarded as mass rollouts of for-profit services become commonplace.

__________________________________________________________________________________________________

Quote of the Day

"The only constant in the technology industry is change." - said CEO of Salesforce Marc Benioff

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

April 11, 2018

Fiat Lux

Featured Trade:

(TRADING THE NEW VOLATILITY),

(VIX), (VXX),

(THE TWO CENTURY DOLLAR SHORT), (UUP)

I have been trading the Volatility Index (VIX) since it was first created in 1993.

Let me tell you, the Volatility Index we have today is not your father's Volatility Index.

The (VIX) was originally a weighted measure of the implied volatility of just eight S&P 100 at-the-money put and call options.

Ten years later, in 2004, it expanded to use options based on a broader index, the S&P 500, which allows for a more accurate view of investors' expectations on future market volatility. That formula continues until today.

There were two generational lows in the (VIX) that have taken place since inception.

The first was in 1998 during the heyday of the mammoth hedge fund Long-Term Capital Management. The firm sold short volatility down to the $8 level and used the proceeds to buy every bullish instrument in the universe, from Japanese equities to Danish mortgage bonds and Russian government debt.

Then the Russian debt default took place and the (VIX) rocketed to $40. LTCM suffered losses in excess of 125% of its capital, and went under in two weeks. It took two years to unwind all the positions, while the (VIX) remained $40 for a year.

To learn more detail about this unfortunate chapter in history, please read When Genius Failed by Roger Lowenstein. The instigator of this whole strategy, John Meriwether, once tried to hire me and is now safely ensconced in a massive estate at Pebble Beach, CA.

The second low came in January of 2018, when the (VIX) traded down to the $9 handle. This time around, short exposure was industrywide. By the time the (VIX) peaked on the morning of February 6, some $8 billion in capital was wiped out.

So here we are back with a (VIX) of $20.48. But I can tell you that there is no way we have a (VIX) $20.48 market.

This is because (VIX) is calculated based on a daily closing basis. It in no way measures intraday volatility, which lately has become extreme.

During 11 out of the last 12 trading days, the S&P 500 intraday range exceeded 2%. This is unprecedented in stock markets anywhere any time.

It has driven traders to despair, driven them to tear their hair out, and prompted consideration of early retirements. The price movements imply we are REALLY trading at a (VIX) of $50 minimum, and possibly as high as $100.

Of course, everyone blames high frequency traders, which go home flat every night, and algorithms. But there is a lot more to it than that.

Heightened volatility is normal in the ninth year of a bear market. Natural buyers diminish, and volume shrinks.

At this point the only new money coming into equities is through corporate share buybacks. That makes us hostage to a new cycle, that of company earnings reports.

Firms are now allowed to buy their own stock in the run up to quarterly earnings reports to avoid becoming afoul of insider trading laws. So, the buyers evaporate a few weeks before each report until a few weeks after.

So far in 2018 this has created a cycle of stock market corrections that exactly correlate with quiet periods. This is when the Volatility Index spikes.

And because the entire short volatility industry no longer exists, the (VIX) soars higher than it would otherwise because there are suddenly no sellers.

So, what happens next when companies start reporting Q1, 2018 earnings? They announce large increases in share buybacks, thanks to last year's tax bill. And a few weeks later stocks take off like a scalded chimp, and the (VIX) collapses once again.

That's why the Mad Hedge Fund Trader Alert Service is short the (VIX) through the IPath S&P 500 VIX Short Term Futures ETN (VXX) April, 2018 $60-$65 in-the-money vertical bear put spread.

Just thought you'd like to know.

Mad Hedge Technology Letter

April 11, 2018

Fiat Lux

Featured Trade:

(WHY YOU SHOULD BE BETTING THE RANCH ON TECHNOLOGY),

(AMZN), (NFLX), (FB), (Samsung), (Tencent)

Global IT spending is forecasted to surpass $3.7 trillion in 2018, a boost of 6.2% YOY, according to a report released by leading technology research firm Gartner, Inc. (IT).

This year is the best growth rate forecasted since 2007, and is a precursor to a period of flourishing IT growth.

IT budgetary resilience is oddly occurring in the face of a tech backlash engulfing Mark Zuckerberg as collateral damage during higher than normal volatility due to an unstable geo-political environment and nonstop chaos in the White House.

Zuckerberg's reputation has been torn to shreds by the media and politicians alike.

Tech has had better weeks and months, for instance as this past January when tech stocks went up every day. Facebook (FB) still had a great business model in January as well.

The biggest takeaway from the report was the outsized capital investments going into enterprise software, which spurs on exponential business formation.

Enterprise software will successfully record its highest spend rate increasing by 11.1% YOY to $391 billion. This is far and away an abnormally fast pace of increase, but is completely justified based on every brick and mortar migrating toward data harnessing.

The software industry will benefit immensely by the universal digitization of all facets of life as software acts as the tool that businessmen use to propel companies to stardom.

Application software spending will healthily rise into 2019, and infrastructure software also will continue to grow, boosted by the revamping of laggard architecture.

Data center systems are predicted to grow 3.7% in 2018, down from 6.3 percent growth in 2017. The longer-term outlook continues to have challenges, particularly for the storage segment.

The lower relative rate of spend is exacerbated by the chip shortage for memory components, and prices have shot up faster than previously expected.

The new Samsung Galaxy 9 cost an additional $45 in semiconductor chip costs because of the importunate costs that sabotage cost structures.

Exorbitant pricing was set to subside in the early part of 2018, but the dire shortage of chips is here to stay until the end of 2018.

Even though the supply side has ramped up 30%, demand is far outpacing supply, spoiling any chance for tech devices to be made on the cheap.

Global spend for digital devices will grow in 2018, reaching $706 billion, an increase of 6.6 percent from 2017. Not only will we see the standard characters such as phones and tablets, but new creative ways to produce devices in the micro-variety will soon populate our shores.

Amazon Alexa and Apple's HomePod are just the beginning and will spawn micro-devices that would fit nicely into a flashy James Bond film.

The demand for ultra-mobile premium smartphones will slow in 2018 as more consumers delay their upgrade and feel comfortable using older devices -- kind of like a smashed-up Volvo station wagon handed down from sibling to sibling.

In times of uncertainty, corporations hold back spending until the near-term variables can be flushed out, and unforeseen costs causing operational turbulence can be anticipated.

However, the industry has brushed aside the turmoil that has attempted to infiltrate the core growth story.

Investors cannot overlook that total tech spending growth for 2018 is the highest in the past 15 years.

Next quarter's earnings are now on tap, and investors will turn to fundamentals as a cheat sheet for what's in store.

It's undeniable that currently tech stocks aren't cheap anymore. They are also more expensive than they were at the beginning of the year barring Facebook and a few other stragglers.

The momentum has intensified with the five biggest tech firms accounting for more than 14% of the S&P 500 index's weighting.

Tech's relative performance has fended off the bears with PE multiples down a paltry 4.9% this year compared to the cratering of 11.4% in the general market.

And tech is still trading at a tiny fraction of the crisis of the dot-com era.

The outsized reinvestments back into business models don't tell the tale of an industry brought down to its knees begging for salvation.

Look no further than across the Pacific Ocean. Samsung Electronics Co. represents almost 25% in South Korea's Kospi index. At the same time, Asia's most valuable company, Tencent Holdings, makes up almost a 10% weighting in Hong Kong's Hang Seng Index.

Back stateside, about 90% of US tech firms beat revenue estimates in the last quarter of 2017, marking the best success rate for any industry.

The positive sentiment has continued into this year with wildly bullish expectations led by the FANG stocks.

The broader volatility is a gift to investors who hesitated and missed the monster rally that has graced tech the past few years.

Tech is vital to emerging markets. And this is the first year since 2004 that tech constitutes the biggest sector in the MSCI Emerging Markets Index blowing past financials.

Tech had a 28% weighting at the end of 2017, the weighting more than doubling from six years ago.

As it stands today, tech enjoys light regulation and by a long mile. Tech is actually the least regulated industry in America and has used this period of light regulation to stack up profits to the sky.

Banks are nine times more regulated than tech companies, and manufacturing companies are five times more regulated.

Legislation such as Dodd-Frank has done a lot to taper the excesses of the sub-prime frenzy that almost took down Wall Street.

The lean regulation has helped tech companies such as Facebook and Google build a gilt-edged competitive advantage that has been exploited to full effect.

After the Fed closed the curtains on its QE program, tech and its earnings are the sturdiest pillar of the nine-year bull market.

The Street is reliant on the big players to earn its crust of bread and show investors that tech isn't just a flash in the pan.

The two numbers acting as the de-facto indicators of the health of the overall economy are Netflix's subscriber growth numbers and Amazon's AWS Cloud revenue.

These two companies do not focus on profits and are the prototypical tech growth companies.

If they beat on these metrics, the rest of tech should follow suit.

The market is entirely dependent on big tech to drag investors through the time of transition. My bet is that tech will over-deliver booking stellar earnings.

__________________________________________________________________________________________________

Quote of the Day

"By giving the people the power to share, we're making the world more transparent." - said Facebook CEO Mark Zuckerberg

While the Global Trading Dispatch focuses on investment over a one week to six-month time frame, Mad Options Trader, provided by Matt Buckley, will focus primarily on the weekly US equity options expirations, with the goal of making profits at all times. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more