Global Market Comments

June 11, 2019

Fiat Lux

Featured Trade:

(BEYOND RATIONAL), (BYND)

(PLEASE USE MY FREE DATA BASE SEARCH)

(HOW TO AVOID PONZI SCHEMES)

Global Market Comments

June 11, 2019

Fiat Lux

Featured Trade:

(BEYOND RATIONAL), (BYND)

(PLEASE USE MY FREE DATA BASE SEARCH)

(HOW TO AVOID PONZI SCHEMES)

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Mad Hedge Technology Letter

June 10, 2019

Fiat Lux

Featured Trade:

(WILL REGULATION KILL TECHNOLOGY?)

(FB), (MSFT), (GOOGL)

The Technology Hunger Games of 2019 is best viewed through the lens up top - the 30,000-foot view will offer insight into how the cookie will crumble.

Understanding the mechanisms which will either stop the Silicon Valley tech renaissance in its wake or deliver a supercharged boost to this sector is essential to dissecting the U.S. economy moving forward.

Silicon Valley has experienced a sensational generation by any yardstick and sometimes that is lost in the fog of war with the 24-hour news cycle hellbent on stealing the mojo of the tech industry.

Do or die regulation is shaping up to be the most critical acid test in the tech industry since the creation of the internet.

How will big American tech firms adjust to this new normal of government intervention forcing them to meaningfully alter their DNA?

Is a paradigm shift in store for the relationship that is the consumer and a tech company?

The American economy is probably the closest thing that can be passed off as unfettered capitalism.

This type of capitalism is predicated on scarce regulation which is an important part of the underlying theory.

With thin regulation, “animal spirits” can mushroom industries and its underlying companies to superstardom, we have seen this over and over again with companies like Google and Facebook.

On the flip side, we have austerity and economic vigilance.

Just to take a look around the globe and you will understand what I mean.

Germany is the economic gem of Europe and its namesake union motoring the 28-country block as the mainstay hub of innovation and value creation in the region.

But that does not mean they condone unfettered capitalism.

This is the same government that buttressed the call for austerity for the Greek and Italian government when these two entered uncontrollable debt cycles.

Deutsche Wohnen SE fell 8.7% in Frankfurt, while Vonovia SE dropped 5.5% whom are Germany’s largest residential landlords.

I thought buy to let was a guaranteed cash cow? What happened?

Germany’s largest residential landlords publicly traded shares cratered on the anxiety that Berlin will enact a rent freeze for the next five years in reaction to a surge in rental prices.

Deutsche Wohnen who owns 112,000 units is fighting fiercely to overturn this piece of legislation as they are the main recipient or culprits of the housing renaissance causing residential property opportunities or challenges to explode in the artsy Germany city.

Although residential property income is hardly connected to the fortunes of global technology, the regulation sets the tone for other pieces of the economy as a whole.

Take a quick rundown of other European nation states and the red tape is slapped around in abundance.

The end result is that Europe, even with German ingenuity, has been unable to deliver a tech company that can look the Silicon Valley FANGs in the eye and regulation is a big reason why.

Europe is essentially America with no tech companies because of it.

If you want to shovel through the recycling to pick up a name or two, then Swedish-based Spotify, the music streaming platform, would be apt and on the chips side, ARM Holdings, a British semiconductor company with many of its chips installed inside of Android systems.

These names are few and far between.

ARM Holdings was acquired by Softbank for $23 billion in 2016, a bargain buy at 2019 standards.

While America has privatized away many industries, take a look at other countries like China, who are propping up zombie banks and other state-owned companies accumulating more junk-graded debt.

I would argue that centrally planned economies like China and North Korea possess governments who get in the way of their economy more often than not to maintain strict control over its populace.

This is why private businesses often get the shaft of the top-down way of governing which hurts the free or not so free markets.

The biggest event in tech in the next 2 years will be if the big tech giants break up or not because of anti-trust tinged worries.

Microsoft’s regulatory mess was the last time the American government rolled up their sleeves and intervened this boldly into the tech sector and the functioning of it.

Remember that Microsoft missed search.

They allowed Google and then Facebook to launch and now we are back at the anti-trust table figuring out again if a reset is necessary or not.

This happened to Microsoft because they were scared to go into that part of tech for fear of more anti-trust scrutiny.

If the government does pound Silicon Valley with harsh anti-trust rulings, these big platforms won’t be able to lean on its richer parent companies to bail them out since they will be separate.

I believe that if Google, Apple, and Amazon are cut apart and set free into the world, it will incite another technological renaissance for another thirty years.

Competition mixed with free markets has a funny way of working itself out.

As I see it, these monstrous platforms are stifling innovation now and choking off smaller companies in the incubation stage that could become the next Google.

Releveling the playing field will spur economic innovation, improve technological techniques, boost job creation, and deliver even better customer experience and prices to the consumer.

Another development which is just as interesting is the market for big data.

Data could be rerouted from the proprietary black boxes of Google and Facebook and into a public market that puts a price on data.

If big data ever became a commodity sold from a market, it would mean that the accuracy of data would improve, and companies would be able to produce better products.

As it stands, big companies receive free data by the gimmick of giving away free services, these companies, in turn, manipulate and slice up the data any way they see fit to monetize.

I believe that the ad marketplace for Facebook and Google is somewhat of a broken and disconnected experience with many third-party companies questioning if it is a black hole that ad budgets are disappearing into.

The digital ad industry will undergo a serious facelift because of government regulation.

If big tech is divvied up, there will be winner and losers.

Not every tech company will survive the breakup because not every tech company is created equal.

A new type of digital marketplace will be formed once again allowing small business to bypass Facebook creating another tsunami of wealth creation.

If the FANGs aren’t broken up, then expect unfettered capitalism to go unperturbed, albeit with slow to moderate growth, instead of the renaissance I mentioned above.

Incremental gains cannot supplant wholesale enhancements.

This all means that your only choice is to own technology stocks in both scenarios – particularly the best of breed with the most cutting-edge technology.

The only way to suppress tech shares in the long run is if the American economy decides to socialize or nationalize big swaths of the private economy.

Let’s hope Washington doesn’t kill the goose that lays the golden eggs.

“I want to put a ding in the universe.” – Said Co-Founder and Former CEO of Apple Steve Jobs

Global Market Comments

June 10, 2019

Fiat Lux

Featured Trade:

(JUNE 21 AUCKLAND NEW ZEALAND STRATEGY LUNCH)

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR THE GRAND PLAN)

(MSFT), (GOOGL), (AMZN), (TESLA), (TLT), ($TNX)

Come join me for lunch at the Mad Hedge Fund Trader’s Global Strategy Luncheon, which I will be conducting in Auckland, New Zealand on Friday, June 21, 2019.

An excellent meal will be followed by a wide-ranging discussion and question-and-answer period.

I’ll be giving you my up-to-date view on stocks, bonds, currencies, commodities, precious metals, and real estate.

I also hope to provide some insight into America’s opaque and confusing political system. And to keep you in suspense, I’ll be throwing a few surprises out there too. Tickets are available for $231.

I’ll be arriving early and leaving late in case anyone wants to have a one-on-one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at a downtown boutique hotel the location of which that will be emailed with your purchase confirmation.

I look forward to meeting you and thank you for supporting my research. To purchase tickets for the luncheon, please click here.

You knew when the price of margaritas was going up that the new Mexican tariff dispute was not going to last very long, especially going into the summer. No wonder the Texas senators were so upset.

As of this writing, the tariffs have been called off two days before they were going to be implemented and a week after they were threatened. But who knows? They could be back on again at any time once the Mexicans fail to deliver on their undoubtedly impossible promises.

The Mexican standoff does, however, provide valuable lessons on how markets may perform going into the 2020 presidential election; arbitrarily create an unnecessary crisis, just as arbitrarily end it, and then collect more votes from your base.

Now let's scale this up to the trade war with China. Use fears of an impending recession to get the Fed to lower interest rates in a major way. With the economic data now falling to pieces, futures markets are currently discounting three 25 basis point rate cuts by yearend and two more in 2020. That gets the Fed funds rate down from the current 2.50% to 1.25% in a hurry.

Then what happens? A “beautiful” trade deal is signed with China, hyper-stimulating the economy in the middle of the election. What are stocks worth with a 1.25% fed funds rate? A whole lot more than they are now.

So, here is the setup for the stock market. A treacherous trading range over the next three to six months leading to lower highs and then lower lows. After that, they go ballistic next year.

I have never been a fan of conspiracy theories, and the strategy above depends on a lot of external things going incredibly right. For a start, the Chinese likely do not want to provide any assistance to the president whatsoever in getting reelected.

Still, we all need a model of how the companies, industries, the economy, and world events will transpire before we enter a single trade, and this is the best one I can come up with….today.

It’s not that interest rates are so important anymore. The biggest chunk of the stock market, large-cap tech stocks, are hugely cash flow positive, have no net debt, and actually lose money when rates fall. And rates have been so low for so long that we have all become used to free money.

The biggest impact is on the consumer who accounts for 70% of GDP. Lower credit card rates and home mortgages have an immediate and positive effect on the economy.

The May Nonfarm Payroll Report definitely cast a long shadow over the economy, coming in at only 75,000, less than half of what was expected. March and April were also revised down by an additional 75,000. The headline Unemployment Rate held steady at 3.6%.

Professional Services gained by 33,000, Construction by 4,000, and Health Care by 16,000. Retail was the biggest loser at 7,000.

If it was just one data point that was so horrible, I wouldn’t be so worried. In fact, Private jobs growth hit a nine-year low on Wednesday, with the May ADP in at only 27,000. Is this the canary in the coal mine?

The takeaway here is that the trade war is finally starting to exact its pound of flesh (I’m going to Venice after all), and that the next report could be worse. The Mexican tariffs and the antitrust assault on big tech are too recent to be reflected in the data. It makes a July Fed rate cut a slam dunk (after all, I live in Oakland).

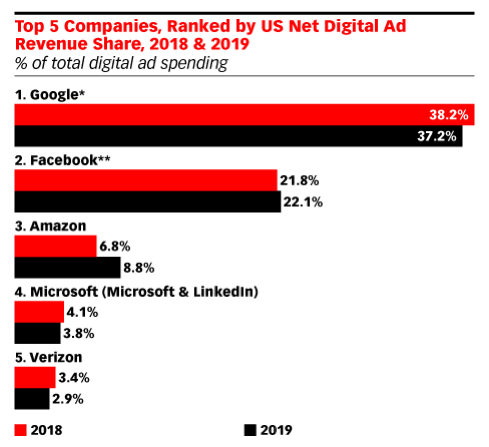

The Justice Department has started an antitrust investigation against Google, claiming that search results favor Google-owned companies. The problem is that Google invented modern online search, with a 92.81% market share. Bing has a 2.38% market share and Yahoo has 1.89%. And while they own search, they contain only 38.2% of the online advertising market.

Microsoft (MSFT) had the same problem during the 1990s, with an antitrust suit brought by the government that lasted a decade. Before that, there was the interminable IBM antitrust suit. I thought Amazon’s (AMZN) head was supposed to be on a plate? Note: I had to Google (GOOGL) the information for this article.

The Fed Beige Book says the economy is slowing, and that is pre-Mexican tariff data. The summer slowdown is here, and GDP growth may fall under 1%. Bond, commodity, and energy markets say the recession is already here, but what do they know?

International trade is in free fall. Expect stocks to hit new 2019 lows while you’re basking on the beach. Your next GM model upgrade is trapped at the border. Sounds like a good time for me to take a trip around the world. Those camels in Egypt are looking better by the minute.

The trade war will cut global airline profits by 21%, from $35.5 billion to $28 billion, says industry trade association IATA in a forecast. More war means less first-class travel. And you wonder why airline share prices have been getting creamed (DAL), (LUV).

The bond market is now gunning for a 1.85% yield, and after that, the 2016 low of 1.33%, as a trade war escalating daily brings forward the next recession. The market has nearly given Trump his 1% cut in interest rates he has been clamoring for. It’s now up to the Fed to follow.

The New York Fed recession indicator is now at 30%, a 12-year high, and with the yield curve now inverted you have to pay attention. This one may be a predicted recession that actually happens. However, recessions usually happen when interest rates spike, not collapse, as they have done.

Thanks to the extreme volatility of the week I gave up my profits for the month of June and have to start all over again. Such is show business. We are now a mere 1.92% below our last all-time high from the previous week. Trading a narrow range with extreme volatility is about the worst kind of market to trade.

It was the antitrust news about the FANGs that really hit me, a core long of mine for the last decade. Thus, I was stopped out of positions in Amazon (AMZN) and Microsoft (MSFT). I was able to hang on to my long in Tesla (TSLA) because the spread was so deep in-the-money.

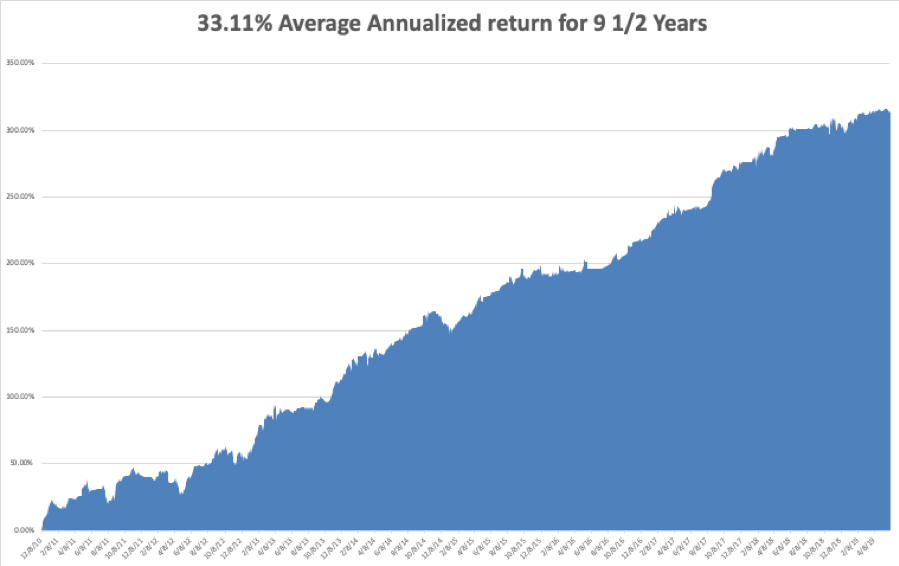

Global Trading Dispatch closed the week up 14.43% year-to-date and is down by -1.29% so far in May. My trailing one-year declined to +13.07%.

My nine and a half year profit fell back to +314.57%. The average annualized return shrank to +33.11%. With the trade war with China raging, I am now 90% in cash with Global Trading Dispatch and 100% cash in the Mad Hedge Tech Letter.

I’ll wait until the markets enjoy a brief short-covering rally before adding any short positions to hedge my longs.

The coming week will be a fairly sedentary one on the data front after last week’s jobs fireworks.

On Monday, June 10 at 12:00 PM, the May Consumer Inflation Expectations report is out.

On Tuesday, June 11, 9:00 AM EST, the May US Producer Price Index is released.

On Wednesday, June 12 at 9:30 AM, the May US Core Inflation is published.

On Thursday, June 13 at 8:30 AM, the Weekly Jobless Claims are printed.

On Friday, June 14 at 9:30 AM, May US Retail Sales are out. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I am spending the weekend packing for my 2019 Mad Hedge World Tour. I’ll be chasing down my mosquito spray for the Philippines, my ice ax and loden hat for Switzerland, my plug adapters and diarrhea treatments for India, and my hangover medicine for Australia. I know I already have all this stuff somewhere, I just have to find it.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

"If a cluttered desk is a sign of a cluttered mind, what is an empty desk a sign of?" asked Albert Einstein.