Mad Hedge Biotech & Healthcare Letter

October 8, 2019

Fiat Lux

Featured Trade:

(GET ON THE CELGENE BANDWAGON),

(CELG), (BMY), (GSK), (AMGN), (RHHBY), (ROG), (GMAB), (MOR)

Mad Hedge Biotech & Healthcare Letter

October 8, 2019

Fiat Lux

Featured Trade:

(GET ON THE CELGENE BANDWAGON),

(CELG), (BMY), (GSK), (AMGN), (RHHBY), (ROG), (GMAB), (MOR)

If you’re looking for a biotech stock that just relentlessly grinds up every day, Celgene Corporation (CELG) has to be at the top of your list, one of the most dominant players in the industry today.

Thanks to its $74 billion merger with Bristol-Myers Squibb (BMY), the combined companies are expected to push out Amgen in the top spot by 2020. Perhaps a positive indicator that things are looking up is the 50.9% rise in Celgene stock this year.

While the deal with Bristol has been predictably riddled with setbacks and delays, the sale of blockbuster arthritis drug Otezla to Amgen last month over antitrust concerns has finally pushed the merger forward.

While waiting for the merger with (BMY) to be finalized by the end of 2019, Celgene has been busy coming up with ways to attract more investors.

One of the exciting efforts of the biotech giant is its recent collaboration with Immatics Biotechnologies. Celgene joins GlaxoSmithKline (GSK) in the T-cell treatment market. With these two behemoths providing resources for this field, researchers are hopeful that a breakthrough drug will be discovered soon.

This partnership with Immatics saw Celgene shell out $75 million to gain access to three of the smaller firm’s anti-cancer adoptive cell therapies. With Immatics’ focus on T-cell treatments, the collaboration with Immatics will provide Celgene a wider pool of candidates for their solid tumor programs.

Aside from the $75 million upfront payment, Immatics will also receive $505 million in milestone payments for every licensed drug if Celgene decides to exercise the option. That means Celgene will have the opportunity to pay for the full or partial rights on selected assets developed from the T-cell therapies.

Ideally, Immatics would earn over $1.5 billion from the collaboration plus tiered royalties on net profits. As for Celgene, the biotech company will share the rewards with Bristol-Myers.

This collaboration marks the biggest upfront payment received by Immatics since its creation in 2000. The company, which is a spinoff of Germany’s University of Tübingen, adds Celgene to its growing number of partners including Amgen (AMGN), Roche Holding Ltd.(RHHBY), Genussscheine (ROG), Genmab (GMAB), and Morphosys (MOR).

The Munich company’s work on adoptive cell treatments and bispecific antibodies also generated interest from the cancer center of the University of Texas.

Since its creation, Immatics has managed to raise $220 million in venture capital plus roughly $130 million in non-dilutive funding. The Celgene deal puts the company’s total capital at $420 million.

So far, Celgene has reported three quarters of consistently accelerating earnings per share increase and a quarter of notable sales growth. However, the Bristol-Myers deal has yet to be completed. More importantly, some blockbuster products face uncertain futures due to rival copycats.

One major factor contributing to the doubts surrounding the company’s future is the recent sale of Otezla. Since this drug has been Celgene’s major moneymaker for years, it remains to be seen how the company will cope with its loss.

Aside from Otezla, another Celgene blockbuster facing pressure is blood cancer treatment Revlimid. While the multiple myeloma drug reported an 11.4% jump in its second quarter sales this year, the company has yet to fully safeguard it from the patent challenges aiming to end its reign in the market.

While the effects of the Immatics collaboration and the recent developments on the Bristol-Myers merger have yet to concretely manifest themselves, Celgene is expected to display strength when the next earnings release of 2019 draws nearer.

In the third quarter report, the company is projected to post an earnings per share of $2.73. This would indicate a 19.21% year-over-year increase. Meanwhile, its earnings per share for the full year of 2019 is expected to rise by over 23% to reach $10.91. As for its revenue, Celgene is estimated to earn $17.44 billion this year, marking a 14.11% rise from 2018.

In terms of its merger with Bristol-Myers, the two pharmaceutical giants are anticipated to have a combined total of 10 drugs already in the late-stage testing phase and six drugs ready to be released soon.

Additionally, the companies disclosed that they have roughly 50 drugs slated for early and mid-stage testing. Among those, 21 are reported to be focused on oncology treatments.

Buy Celgene on the next 5% dip in the shares. It seems to be on a tear.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Mad Hedge Technology Letter

October 7, 2019

Fiat Lux

Featured Trade:

(NEVER CONFUSE A GREAT SERVICE WITH A GREAT STOCK)

(SPOT), (APPLE), (GOOG), (NFLX)

Global Market Comments

October 7, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WILL HE OR WON’T HE?)

(INDU), (USO), (TM), (SCHW), (AMTD), (ETFC), (SPY), (IWM), (USO), (WMT), (AAPL), (GOOGL), (SPY), (C)

Customers like to call me and tell me how cheap Spotify is.

Well, it’s cheap for more than one reason.

Even though Spotify (SPOT) dominates the music streaming space just like Netflix (NFLX) dominates the video streaming space, that does not mean investors should go out and buy the stock by the handful.

The numbers are quite impressive when you consider that Spotify boasts 100 million paying music subscribers.

In the iOS world, Apple (APPL) has 60 million music subscribers while Google (GOOGL) has only 15 million music subscribers.

Why do I mention Google?

They aren’t in the online streaming business, or are they?

Google has signaled its intent that they won’t just allow Spotify and Apple to turn the online streaming industry into a duopoly.

They are the third horse in the race.

Recently, Google announced that its YouTube Music app would now come preinstalled on all new Android devices.

Naturally, absorption rates will increase dramatically, and this app could become quite sticky.

Apple has a moat around its castle because of the iOS system but Spotify has no defenses against such attack.

Spotify is a slave to the Android platform to reach customers which is dominated by Google by not only their software but also their hardware now.

Spotify won a recent deal to preinstall its music app on Samsung (SSNLF) devices, but this won’t be the case for most devices.

Google has a two-way money-making strategy for YouTube Music service through both advertising and subscription sales.

Accessibility comes with ads and to remove ads, YouTube Music charges $9.99 per month.

Consumers spent $7.0 billion on music streaming subscriptions in 2018 and diversifying away from Google Search is something that CEO Sundar Pichai is hellbent on.

Google has lept into selling cloud computing services and hardware products, including speakers, in search of non-advertising revenue.

In reaction, Spotify cannot just lay vulnerable like a sitting duck, and have announced tests for a price increase for family plan subscribers in Scandinavia.

The family plan in Sweden currently costs about 149 Swedish krona ($15.45) per month, similar to the pricing in the United States and the rest of Europe and it will be interesting to see if they can stomach a 13% increase.

I bet there will be a revolt as Scandinavians know they can just hook up to YouTube with an ad-less browser to listen to whatever they want for free.

Looking to lucrative markets to squeeze more juice out of a lemon would have a higher chance of succeeding if a level up in service is also offered.

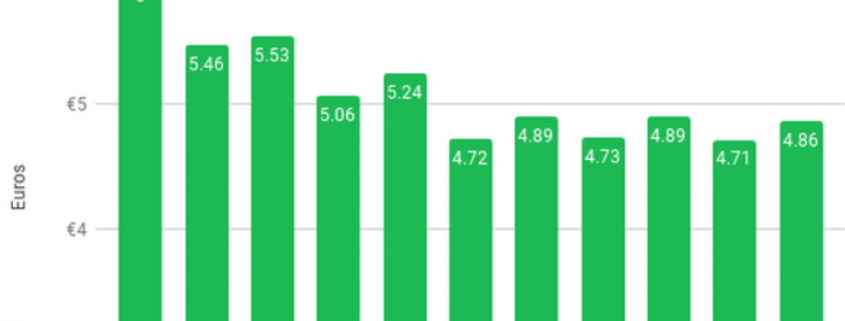

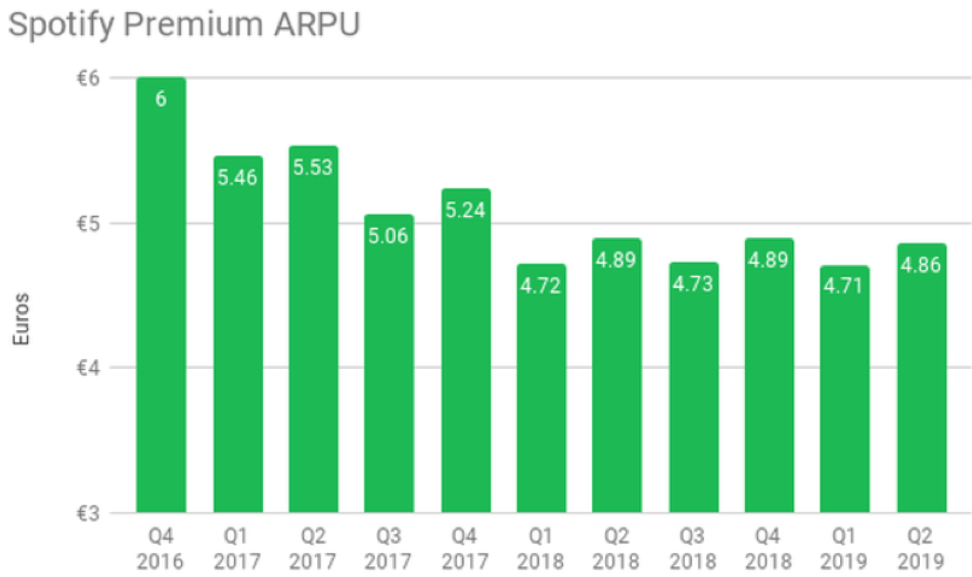

The desperation is palpable as Spotify’s Average Revenue Per User (ARPU) falls off a cliff and is the reinforcement I need to feel that this business is impossible to make money in.

Just the unforgivable headwind that licensing music eats up is enough pain with allocating 75 cents on every $1 of revenue.

The company has been in a precarious position right out of the gates.

Even publishers have gripes against Spotify's declining ARPU, since a large part of their contracts include revenue-sharing agreements with the music streamer.

Ultimately, Spotify is a service that cannot differentiate itself through exclusive original series and films which is inherent to survival.

Their attempts to allow individual singers to upload backfired because only their users are interested in hearing the 0.1% of popular music deemed popular from mainstream culture.

Spotify, Apple Music, and Google will possess more or less the same library of music that most people want to listen to.

Then it comes down to what platform is more convenient than the other.

Apple and Google have strong financial backing giving them higher pain thresholds if they lose money.

Until Spotify can find a magical way to make their product unique, they are on the path to a death by thousand cuts even if they do have a great product.

Once again, the markets are playing out like a cheap Saturday afternoon matinee. We are sitting on the edge of our seats wondering if our hero will triumph or perish.

The same can be said about financial markets this week. Will a trade deal finally get inked and prompt the Dow Average to soar 2,000 points? Or will they fail once again, delivering a 2,000-point swan dive?

I vote for the latter, then the former.

Still, I saw this rally coming a mile off as the Trump put option kicked in big time. That's why I piled on an aggressive 60% long position right at last week’s low. Carpe Diem. Seize the Day. Only the bold are rewarded.

Or as Britain’s SAS would say, “Who dares, wins.”

It takes a lot of cajones to trade a market that hasn’t moved in two years, let alone take in a 55% profit during that time. But you didn’t hire me to sit on my hands, play scared, and catch up on my Shakespeare.

I think markets will eventually hit new all-time highs sometime this year. The game is to see how low you can get in before that happens without getting your head handed to you first.

Last week saw seriously dueling narratives. The economic data couldn’t be worse, pointing firmly towards a recession. But the administration went into full blown “jawbone” mode, talking up the rosy prospects of an imminent China trade deal at every turn.

This was all against a Ukraine scandal that reeled wildly out of control by the day. Is there a country that Trump DIDN’T ask for assistance in his reelection campaign? Now we know why the president was at the United Nations last week.

The September Nonfarm Payroll Report came in at a weakish 136,000, with the Headline Unemployment rate at 3.5%, a new 50-year low.

Average hourly earnings fell. Apparently, it is easy to get a job but impossible to get a pay raise. July and August were revised up by 45,000 jobs.

Healthcare was up by 39,000 and Professional and Business Services 34,000. Manufacturing fell by 2,000 and retail by 11,0000. The U-6 “discouraged worker” long term unemployment rate is at 6.9%.

The US Manufacturing Purchasing Managers Index collapsed in August from 49.7 to 47.9, triggering a 400-point dive in the Dow average. This is the worst report since 2009. Manufacturing, some 11% of the US economy, is clearly in recession, thanks to the trade war-induced loss of foreign markets. A strong dollar that overprices our goods doesn’t help either.

The Services PMI Hit a three-year low, from 53.1 to 50.4, with almost all economic data points now shouting “recession.” The only question is whether it will be shallow or deep. I vote for the former.

Consumer Spending was flat in August. That’s a big problem since the average Joe is now the sole factor driving the economy. Everything else is pulling back. Consumer spending, which accounts for more than two-thirds of U.S. economic activity, edged up 0.1% last month as an increase in outlays on recreational goods and motor vehicles was offset by a decrease in spending at restaurants and hotels.

The Transports, a classic leading sector for the market, have been delivering horrific price action this year giving up all of its gains relative to the S&P 500 since the 2009 crash.

Oil (USO) got crushed on recession fears, down a stunning 19.68% in three weeks. The global supply glut continues. Over production and fading demand is not a great formula for prices.

Toyota Auto Sales (TM) cratered by 16.5% in September, to 169,356 vehicles in another pre-recession indicator. It’s the worst month since January during a normally strong time of the year. The deals out there now are incredible.

Online Brokerage stocks were demolished on the Charles Schwab (SCHW) move to cut brokerage fees to zero. TD Ameritrade (AMTD) followed the next day and was spanked for 23%, and E*TRADE (ETFC) punched for 17. These are cataclysmic one0-day stock moves and signal the end of traditional stock brokerage.

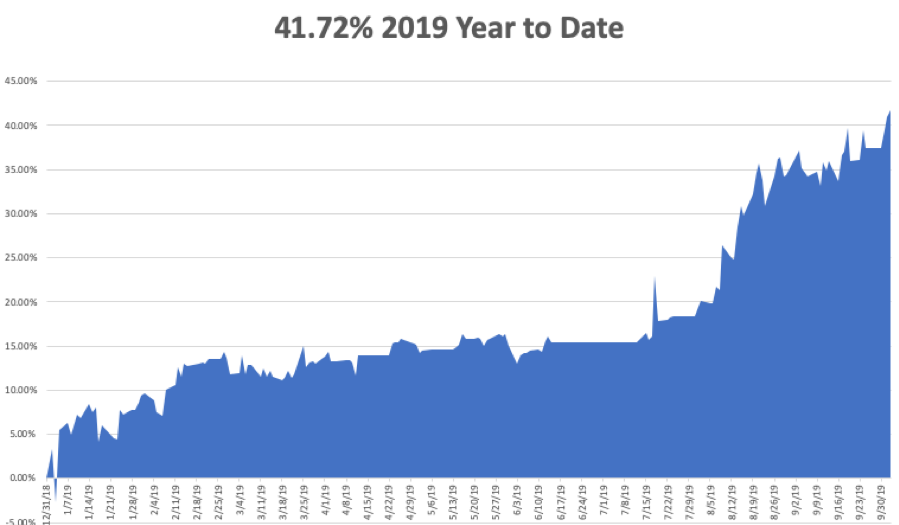

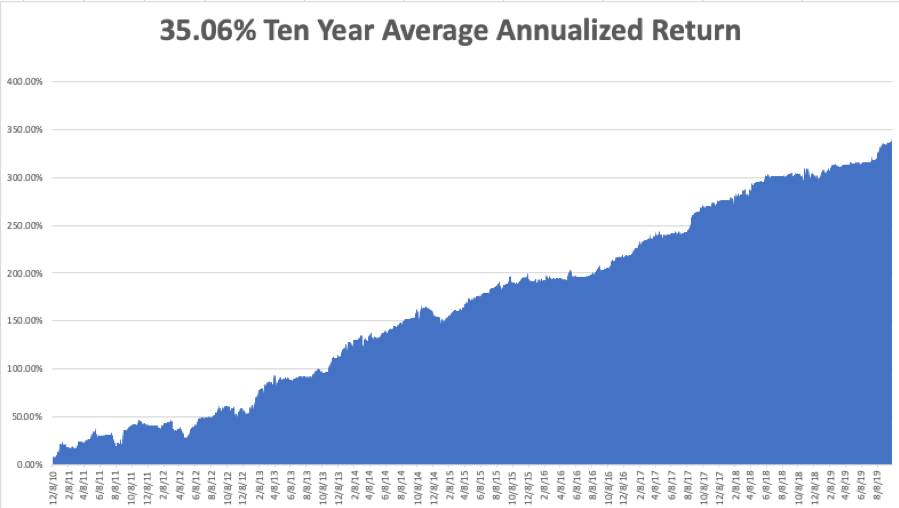

The Mad Hedge Trader Alert Service has blasted through to yet another new all-time high. My Global Trading Dispatch reached new apex of 341.86% and my year-to-date accelerated to +41.72%. The tricky and volatile month of October started out with a roar +5.40%. My ten-year average annualized profit bobbed up to +35.06%.

Some 26 out of the last 27 trade alerts have made money, a success rate of 96.29%! Under promise and over deliver, that's the business I have been in all my life. It works.

I used the recession-induced selloff since October 1 to pile on a large aggressive short dated portfolio. I am 60% long with the (SPY), (IWM), (USO), (WMT), (AAPL), and (GOOGL). I am 20% short with positions in the (SPY) and (C), giving me a net risk position of 40% long.

The coming week is all about the September jobs reports. It seems like we just went through those.

On Monday, October 7 at 9:00 AM, the US Consumer Credit figures for August are out.

On Tuesday, October 8 at 6:00 AM, the NFIB Business Optimism Index is released.

On Wednesday, October 9, at 2:00 PM, we learn the Fed FOMC Minutes from the September meeting.

On Thursday, October 10 at 8:30 AM, the US Inflation Rate is published. US-China trade talks may, or may not resume.

On Friday, October 11 at 8:30 AM, the University of Michigan Consumer Sentiment for October is announced.

The Baker Hughes Rig Count is released at 2:00 PM.

As for me, I’m still recovering from running a swimming merit badge class for 60 kids last weekend. Some who showed up couldn’t swim, while others arrived with no swim suits, prompting a quick foray into the lost and found.

One kid jumped in and went straight to the bottom, prompting an urgent rescue. Another was floundering after 15 yards. When I pulled him out and sent him to the dressing room, he started crying, saying his dad would be mad. I replied, “Your dad will be madder if you drown.”

I never felt so needed in my life.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

“Spotify has paid more than two billion dollars to labels, publishers and collecting societies for distribution to songwriters and recording artists.” – Said CEO of Spotify Daniel Ek

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more